By Nathan’s Bulletin in Seeking Alpha

Summary

- Petroamerica was a fantastic buying opportunity at C$0.39 in August 2014.

- The stock trades less than 1 times its 2014 EBITDA at the current price of C$0.25.

- An once-in-a-lifetime buying opportunity is an understatement, and I do pound the table on the value this stock currently represents.

Introduction

Petroamerica Oil (OTCPK:PTAXF) was an exploration company a few years ago that managed to become a well-established oil producer in Colombia. Petroamerica is the definition of a cash cow with a rock solid balance sheet and working capital surplus of US$74 million (see Q2 2014 report) that can withstand any short-term and mid-term volatility of the oil price, as mentioned in my “Top Idea” article in late August 2014.

Aside the consistent production growth on a YOY basis, the company also managed to diversify its asset base while increasing significantly its RLI (reserves life index) pro forma the recent transformative acquisition of Suroco Energy. But this deal coincided with the overall correction of the energy sector and the market did not pay attention to it. So Petroamerica remained a grossly undervalued company at C$0.39 per share in late August 2014.

But Albert Einstein has said: “Two things are infinite: the universe and human stupidity. But I’m not sure about the former”. Einstein could not describe better the reason why Petroamerica has dropped over the last weeks, despite the fact it was already a fantastic buying opportunity at C$0.39. The stock was beaten out primarily by the herd mentality, and the fools abandoned the ship, creating an once-in-a-lifetime buying opportunity.

And believe it or not, the phrase “once-in-a-lifetime buying opportunity” is a vast understatement, because Petroamerica trades below 1 times its 2014 EBITDA at the current price of C$0.25 per share.

As such, I decided to pound the table on the value this company currently represents. Given that I compared Petroamerica primarily to its Colombian, Peruvian, Chilean and Brazilian peers in my “Top Idea” article, this time I will compare Petroamerica to other junior oil-weighted competitors (production up to 10,000 boepd) with onshore production and properties in Argentina, Africa and Middle East.

In Part 1, the peers are from Argentina, Nigeria and Kurdistan. In Part 2, the peers will be from other countries which are equally high risk jurisdictions. All these regions carry much higher geopolitical risk than Colombia’s, while the energy companies there receive Brent pricing.

The Irrational Valuation Is Beyond Any Comprehension

As mentioned above, Argentina, Kurdistan and Nigeria carry much higher geopolitical risk than Colombia’s. And there is no question about this, given the continued headwinds all the energy companies have been facing in these three countries on a permanent basis.

The nationalization fears always linger over Argentina during the last years primarily due to YPF’s (NYSE:YPF) nationalization by the Argentinean Government. These fears coupled with a non-business friendly environment have made several big energy companies dump their Argentinean assets to the local producers and exit Argentina. For instance, both Apache (NYSE:APA) and Gran Tierra Energy (NYSEMKT:GTE) sold their Argentinean assets recently and decided to focus their resources to safer areas. The deal will allow Gran Tierra to further focus on Colombia, Peru and Brazil, Gran Tierra’s CEO Dana Coffield said.

Also, Repsol (OTCQX:REPYY) sold its remaining Argentinean assets in May 2014 and exited Argentina too.

Kurdistan has been in the center of violence in the Middle East over the last ten years, let alone now due to the existence of ISIS (Islamic State of Iraq).

Meanwhile, the piracy and the illegal bunkering coupled with the frequent shutdowns, field pipeline and export facility losses have been hampering for years the smooth execution of the business plans of the Nigerian oil producers. This is why, several major players have sold their assets and have left Nigeria during the last years. They went to greener pastures because they were not able to handle all these headwinds anymore.

In contrast, a huge land rush is happening in the energy sector in Colombia, which is undergoing an evolution over the last years. The number of majors coming in Colombia has been increasing, thanks to several reasons that were analyzed in my latest “Top Idea” article (i.e. improved political and security climate with the funding help of the US).

After all, let’s see now Petroamerica’s peers from Argentina, Nigeria and Kurdistan:

1) Mart Resources (OTCPK:MAUXF).

2) Oryx Petroleum (OTC:ORXPF).

3) Eland Oil and Gas (OTC:ELOGF).

4) Apco Oil and Gas (NASDAQ:APAGF).

5) Americas Petrogas (OTCPK:APEOF).

6) Andes Energia (OTCPK:ANEGY).

7) President Energy (OTC:PPCGF).

I am a strong believer that many investors have never heard about most of these companies. And I am also absolutely sure that Petroamerica’s sellers over the last days are definitely among the investors who see most of these companies for the first time in their life.

Well, this does not surprise me and the ignorance has always been one of the primary factors leading to market inefficiency. As such, some more information about Petroamerica’s competitors is more than necessary:

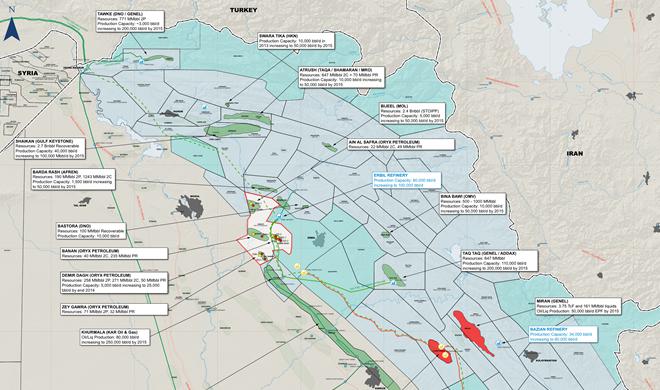

1) Oryx Petroleum’s single producing asset is in Kurdistan, as shown below:

(click to enlarge)

“Source: Oryx website”

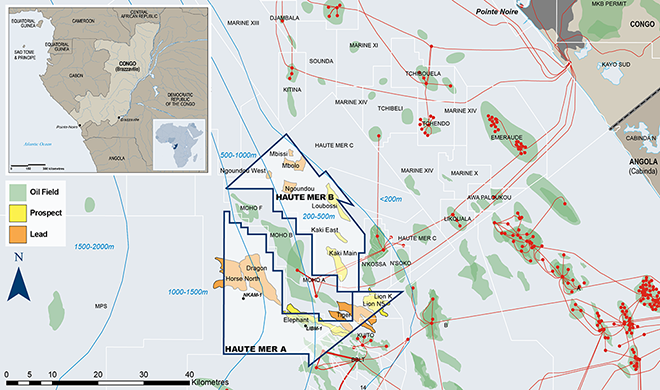

Oryx also has non-producing assets in Nigeria, Senegal and Congo, as shown below:

“Source: Oryx website”

“Source: Oryx website”

“Source: Oryx website”

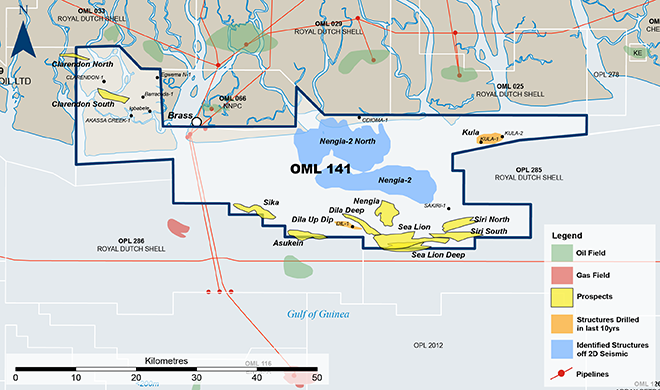

2) Mart’s single-producing asset is the Umusadege field situated in Nigeria, as shown below:

“Source: Mart website”

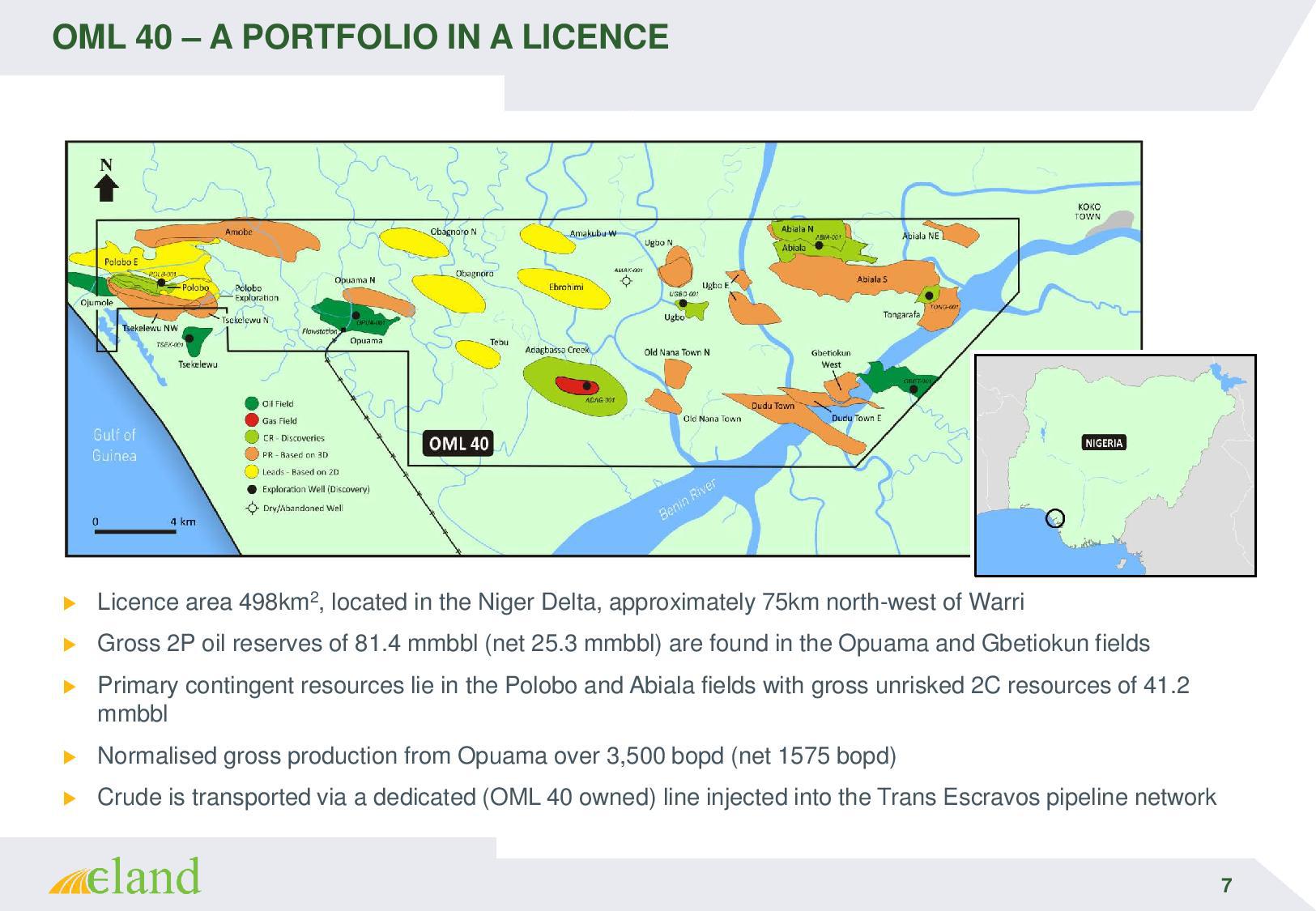

3) Eland’s producing properties are in Nigeria, as illustrated below:

4) Apco’s producing properties are in Argentina (Neuquen Basin, Northwest Basin, San Jorge Basin, Austral Basin) and Colombia, as illustrated below:

(click to enlarge)

“Source: Apco website”

5) Americas Petrogas’ producing properties are in Argentina, as illustrated below:

“Source: Americas Petrogas website”

6) Andes’ producing properties are in Argentina while the company also has non-producing assets in Colombia, Brazil and Paraguay, as illustrated below:

(click to enlarge)

“Source: Andes website:

7) President’s main producing properties are in Argentina, where the company gets most of its production, as illustrated below:

“Source: President website”

President has also a small producing asset in the US and non-producing assets in Paraguay, as illustrated below:

“Source: President website”

and below:

“Source: President website”

I must also point out that:

1) I took into account the working capital surplus or deficiency to calculate the Net Debt and thereby the Enterprise Value accurately ($1 = C$1.11, 1GBP=$1.61).

2) I excluded the EV/2P Reserves key ratio. I did this because this is a backward-looking ratio referring to the companies’ reserves as of December 2013, while we are already in Q4 2014 and the companies have completed a significant part of their drilling programs.

3) The EBITDA estimates are based on a $90/bbl (Brent) scenario by year end.

That being said, I will proceed with the calculations on these two key metrics:

1) Per EV/Production: Here is the table with the first key metric:

| Company | EV($ million) | Q4 2014Production

(boepd) (*) |

EV———

Q4 2014 Production (*) ($/boepd) |

| AndesEnergia | 350 | 1,600(100% light oil) | 218,750 |

| PresidentEnergy | 90 | 600(~80% light oil & NGLs) | 150,000 |

| OryxPetroleum | 880 (**) | 10,000(100% light oil) | 88,000 |

| AmericasPetrogas | 95 | 1,100(100% light oil) | 86,364 |

| MartResources | 460 | 5,500(100% light oil) | 83,636 |

| Eland Oiland Gas | 210 | 3,000(100% light oil) | 70,000 |

| Apco Oiland Gas | 420 | 7,300(56% light oil & NGLs) | 57,534 |

| PetroamericaOil | 125 | 7,400+(97% light/medium oil & NGLs) | 16,892 |

(*): Estimate, based on the latest corporate guidance.

(**): Pro forma the offering of July 2014.

2) Per EV/EBITDA: Let’s check out now the table below with the second key metric:

| Company | EV($ million) | 2014 EBITDA($ million) (*) | EV———

2014 EBITDA |

| AndesEnergia | 350 | 10 | 35 |

| OryxPetroleum | 880 (**) | 35 | 25.14 |

| Eland Oiland Gas | 210 | 10 | 21 |

| PresidentEnergy | 90 | 10 | 9 |

| AmericasPetrogas | 95 | 15 | 6.33 |

| Apco Oiland Gas | 420 | 75 | 5.6 |

| MartResources | 460 | 140 | 3.29 |

| PetroamericaOil | 125 | 130 | 0.96 |

(*): Estimate, based on the latest production guidance.

(**): Pro forma the offering of July 2014.

My Takeaway

Hamsters and gerbills have short-term memories lasting a few hours. I think that the average investor’s memory is better than hamster’s. Reptiles and amphibians have memories lasting few months. And I believe that often the average investor’s memory is hardly better than reptiles’. As such, he forgets quickly without learning from his previous mistakes, and is always ready to throw again and again the baby out with the bath water. This is the case with Petroamerica, since I recommended it at C$0.39 per share in late August 2014.

Since late August 2014, the stock has dropped due to a combination of these reasons:

1) A temporary production disruption in the Putumayo Basin, where Suroco Energy has its producing property (Suroriente Block). As a result of this temporary production restriction, the updated guidance of 7,460 boepd in Q4 2014 was below original 2014 expectations. Nevertheless, it must be pointed out:

a) This temporary disruption did not take place in the Llanos Basin, where Petroamerica has its core producing properties.

b) Suroco’s properties were producing less than 30% of the total Petroamerica’s production.

c) Petroamerica has clearly stated that the production has resumed and normal production operations along with oil evacuation were restored in the Putumayo properties as of October 1, 2014.

d) The YOY production growth is still here, given that Petroamerica was producing 4,390 boepd in Q1 2013 and 6,400 boepd in Q1 2014. Based on the updated guidance of 7,460 boepd, the YOY production growth between Q1 2014 and Q4 2014 is almost 20%.

2) The correction of the oil price and the energy stocks.

3) A dwindling amount of 20 cent warrants holders sold. According to the presentation of September 2013 (slide 29), there were 32.85 million warrants as of August 2013, and according to the latest presentation (slide 23), there were only 9.15 million warrants left as of August 2014.

These warrants were issued as a sweetener for the 2015 note offering, when Petroamerica was a start-up business a few years ago. Those warrant holders have been exercising and cashing out over the last years.

4) The weak hands, the ignorant investors and the short-term traders sold too, running for the hills, so the drop accelerated. Most of them bought on the “Top Idea” article about Petroamerica and were getting shaken out.

The thing is that none of the sellers has realized why he is selling Petroamerica and whether there is a better value out there. None of the sellers has realized the big picture associated with Petroamerica’s peers in Colombia, as described in my “Top Idea” article. None of the sellers has realized the big picture associated with Petroamerica’s peers in Argentina, Africa, and Kurdistan, as described above.

And I am determined to present again the big picture with the help of another article (Part 2) over the next days, because Petroamerica currently is the cheapest oil-weighted producer among all the publicly-traded energy companies in the international markets.

There is not another oil producer that currently trades below 1 times its 2014 EBITDA, while having a pristine balance sheet. And given that my database includes all the publicly-traded energy companies in the US, Canada, Europe, Asia and Australia, I challenge all to write an article about a cheaper energy company with a better balance sheet than Petroamerica’s.

Last but not least:

1) My articles about Petroamerica (Top Idea, Part 1) are based on a relative valuation analysis. In other words, if Brent drops and remains at $90/bbl for many months, it will affect all Petroamerica’s peers that receive Brent pricing. If Brent drops and remains below $90/bbl for many months, it will not affect only Petroamerica’s top and bottom lines.

Based on this easy to understand fact, the current mind-blowing valuation gap between Petroamerica and its peers (Latin American, African, Middle East) is completely unjustifiable, no matter what the Brent pricing is. It does not play one single role whether Brent is at $100/bbl or at $90/bbl.

Petroamerica’s peers currently trade between 4 and 35 times their 2014 EBITDA, while Petroamerica currently trades below 1 times its EBITDA, at the current price of C$0.25 per share. And to be fair, Petroamerica deserves a premium compared to many of its peers, given that many of its peers are leveraged with worse balance sheets and operations in highly risky juridictions, as shown in both my Petroamerica-related articles.

To say it differently, while Petroamerica’s peers have been dropping over the last couple of weeks, Petroamerica should have risen all these days to catch up with its peers’ valuation, closing the tremendous valuation gap.

2) All my previous five energy picks from Colombia (C&C Energia, Petrominerales, Parex, Canacol, Suroco Energy) have risen between 70% and 160% since I recommended them. And Petroamerica Oil at C$0.39 per share was fundamentally better and cheaper than these five companies, let alone now at C$0.25 per share.

3) Three of my previous Colombian picks (C&C Energia, Petrominerales, Suroco Energy) were acquired between 4 and 6 times their EBITDA.

4) Just a few days ago, privately held Pluspetrol Resources agreed to buy Apco Oil and Gas for $427 million, which is 5.6 times its 2014 EBITDA. Apco operates primarily in Argentina and also has some producing Blocks in Colombia, as shown in the previous paragraph.

Apparently, the blindingly obvious is not blindingly obvious for the average investor, and this is why he is always doomed to lose in the stock market. Thanks to the average investor, the smart money makes easy money.

Disclaimer: This article covers a stock trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.