“For a successful technology, reality must take precedence over public relations, for Nature cannot be fooled.” – Richard Feynman – Rogers Commission

“It appears that there are enormous differences of opinion as to the probability of a failure with loss of vehicle and of human life. The estimates range from roughly 1 in 100 to 1 in 100,000. The higher figures come from the working engineers, and the very low figures from management. What are the causes and consequences of this lack of agreement? Since 1 part in 100,000 would imply that one could put a Shuttle up each day for 300 years expecting to lose only one, we could properly ask “What is the cause of management’s fantastic faith in the machinery? … It would appear that, for whatever purpose, be it for internal or external consumption, the management of NASA exaggerates the reliability of its product, to the point of fantasy.” – Richard Feynman – Rogers Commission

(Jim Quinn) The phrase “Throttle Up” jumped into my consciousness in the last week when Trump and his coronavirus task force of government hacks and bureaucrat lackeys announced the guidelines for re-opening America, as if a formerly $22 trillion economy, tied to a $90 trillion global economy, could be turned off and on like a light switch. Clap off, clap on. It just doesn’t work that way. The arrogance and hubris of people who think they can declare a global shut down for a virus and think they can easily deal with the intended and unintended consequences of doing so, is breathtaking in its outrageous recklessness and egotistical belief in their own infallibility.

This contemptible belief in their own superiority has permeated every fiber of those who rule over us, particularly among captured central bankers, corrupt politicians, bought off scientists, and billionaire oligarchs. It is the same groupthink, purposeful failure to address risks, and willfully ignoring those in the trenches that murdered seven astronauts on January 28, 1986 and has created the 2nd Great Depression of today. “Throttle Up” is going to result in the same outcome as it did in 1986.

Thirty-four years ago, on a cold January morning, Space Shuttle Challenger thundered into a crystal-clear blue Florida sky on its 10th voyage into space. The seven astronauts, including civilian Christa McAuliffe, put their trust in the “experts” from NASA, Thiokol, and Rockwell that the shuttle was safe and launching when the temperature was 30 degrees would not pose any added risks. When Richard Covey in Mission Control informed the crew to “go at throttle up”, they expected what their training told them would happen.

Instead, Space Shuttle Challenger exploded in a horrific display witnessed live on TV by 17% of the American population. School children all over the country were watching in their classrooms because McAuliffe was a school teacher chosen from thousands to go into space. It was a tragedy that shook the nation and led to one of Reagan’s better speeches that night, where he addressed the nation’s school children.

“I want to say something to the schoolchildren of America who were watching the live coverage of the shuttle’s takeoff. I know it is hard to understand, but sometimes painful things like this happen. It’s all part of the process of exploration and discovery. It’s all part of taking a chance and expanding man’s horizons. The future doesn’t belong to the fainthearted; it belongs to the brave. The Challenger crew was pulling us into the future, and we’ll continue to follow them.”

And he ended with this line from the poem ‘High Flight’:

“We will never forget them, nor the last time we saw them, this morning, as they prepared for their journey and waved goodbye and ‘slipped the surly bonds of Earth’ to ‘touch the face of God.’”

Thus, began the politician’s use of death to create heroes when human error, hubris, and recklessness is the true cause of avoidable tragedy and despair. Those seven astronauts were not heroes, they were victims. Just as we are all victims of the incompetency, arrogance, corruption and greed of those who lead our government, financial system, and corporate fascist oligarchy passing for capitalism in this globalist-controlled fraud of a former republic.

Using victims to create false heroes has now been elevated to an art form by politicians, the corporate media and mega-corporations to push whatever agenda supports their narrative. The propaganda machine is their most useful tool, as decades of dumbing down the public through government school indoctrination has created millions of pliable useful idiots who will believe anything presented by “experts” on the boob tube. The fear and panic created by politicians and the media about a virus only marginally more dangerous than the common flu is the perfect representation of this power over reality.

The Space Shuttle Challenger disaster is a perfect analogy for the current debacle being perpetrated on the American people by fecklessly corrupt authoritarian politicians, IYI medical “experts”, and fear mongering fake news media pushing the narrative in whatever direction benefits their bottom line. There is the simple technical reason why the Challenger blew up and then there is the real reason – the truthful explanation. What we must understand from history and experience is, if we don’t accept the narratives pushed by “experts” and think critically based upon facts, the truth will eventually be revealed.

The immediate cause of the explosion was a failure in the O-rings sealing the aft field joint on the right solid rocket booster, causing pressurized hot gases and eventually flame to “blow by” the O-ring and contact the adjacent external tank, causing structural failure. The truth is, decisions made and not made over years sealed the fate of those victims, just as we are facing today with this man-made global catastrophe.

After the shuttle disaster, politicians do what they do best, create a commission to cover-up the true cause and protect the establishment from blame. It was led by William Rogers, a government bureaucrat for decades, along with numerous other people with a vested interest in protecting NASA, the massive defense corporations sucking off the government teat, and the crooked politicians supporting NASA.

There were a couple of members from the trenches, like Sally Ride and Chuck Yeager, but the thorn in the side of the establishment was theoretical physicist and Nobel Prize winner Richard Feynman. Despite being racked by cancer, Feynman reluctantly agreed to join the commission, knowing he was going to be out of his element in the swamp of Washington D.C. The nation’s capital, he told his wife, was “a great big world of mystery to me, with tremendous forces.”

Feynman immediately created problems by thinking outside the box and having the gall to ignore the excuses and lies of high-level managers at NASA, Thiokol and Rockwell, while seeking the opinions of the actual engineers who did the real work. His unwillingness to toe the company line irritated the old guard looking to cover up the truth. During a break in one hearing, Rogers told commission member Neil Armstrong, “Feynman is becoming a pain in the ass.”

The establishment always thinks anyone who questions their authority or expertise is a pain in the ass, at best. Often, they treat anyone with an opposing viewpoint as the enemy, and will undertake any means to shut them up and destroy them. Witness how YouTube and Google are currently memory holing anything questioning the establishment narrative about this virus or Joe Biden’s sexual assault on a young woman as a Senator. Feynman embarrassed the “experts” on national TV when he conducted a simple demonstration of why the shuttle blew up.

“I took this stuff I got out of your [O-ring] seal and I put it in ice water, and I discovered that when you put some pressure on it for a while and then undo it, it doesn’t stretch back. It stays the same dimension. In other words, for a few seconds at least, and more seconds than that, there is no resilience in this particular material when it is at a temperature of 32 degrees. I believe that has some significance for our problem.” – Richard Feynman

The truth is top management at NASA knew the O-rings were defective in 1977 and contained a potentially catastrophic flaw. NASA managers also disregarded warnings from engineers about the dangers of launching posed by the low temperatures of that morning, and failed to adequately report these technical concerns to their superiors. Thiokol engineer Bob Ebeling in October 1985 wrote a memo—titled “Help!” so others would read it—of concerns regarding low temperatures and O-rings.

There were numerous teleconferences on the 27th of January where Ebeling and other engineers argued against the launch due to the freezing temperatures. According to Ebeling, a second conference call was scheduled with only NASA and Thiokol management, excluding the engineers. Thiokol management disregarded its own engineers’ warnings and now recommended the launch proceed as scheduled. Ebeling told his wife that night Challenger would blow up. He was right.

The Commission attempted to let NASA’s culture off the hook with no recommended sanctions against the deeply flawed organization. Feynman could not in good conscience recommend NASA should continue without a suspension of operations and a major overhaul. His fellow commission members were alarmed by Feynman’s dissent. Feynman was so critical of flaws in NASA’s “safety culture” that he threatened to remove his name from the report unless it included his personal observations on the reliability of the shuttle, which appeared as Appendix F.

The quote at the beginning of this article about upper management believing there was only a 1 in 100,000 chance of disaster, when the odds were really 1 in 100 or less, came from Feynman’s dissent in Appendix F. The fools at NASA and on the Commission didn’t understand or willfully ignored Feynman’s first principle:

“The first principle is that you must not fool yourself — and you are the easiest person to fool.” – Richard Feynman

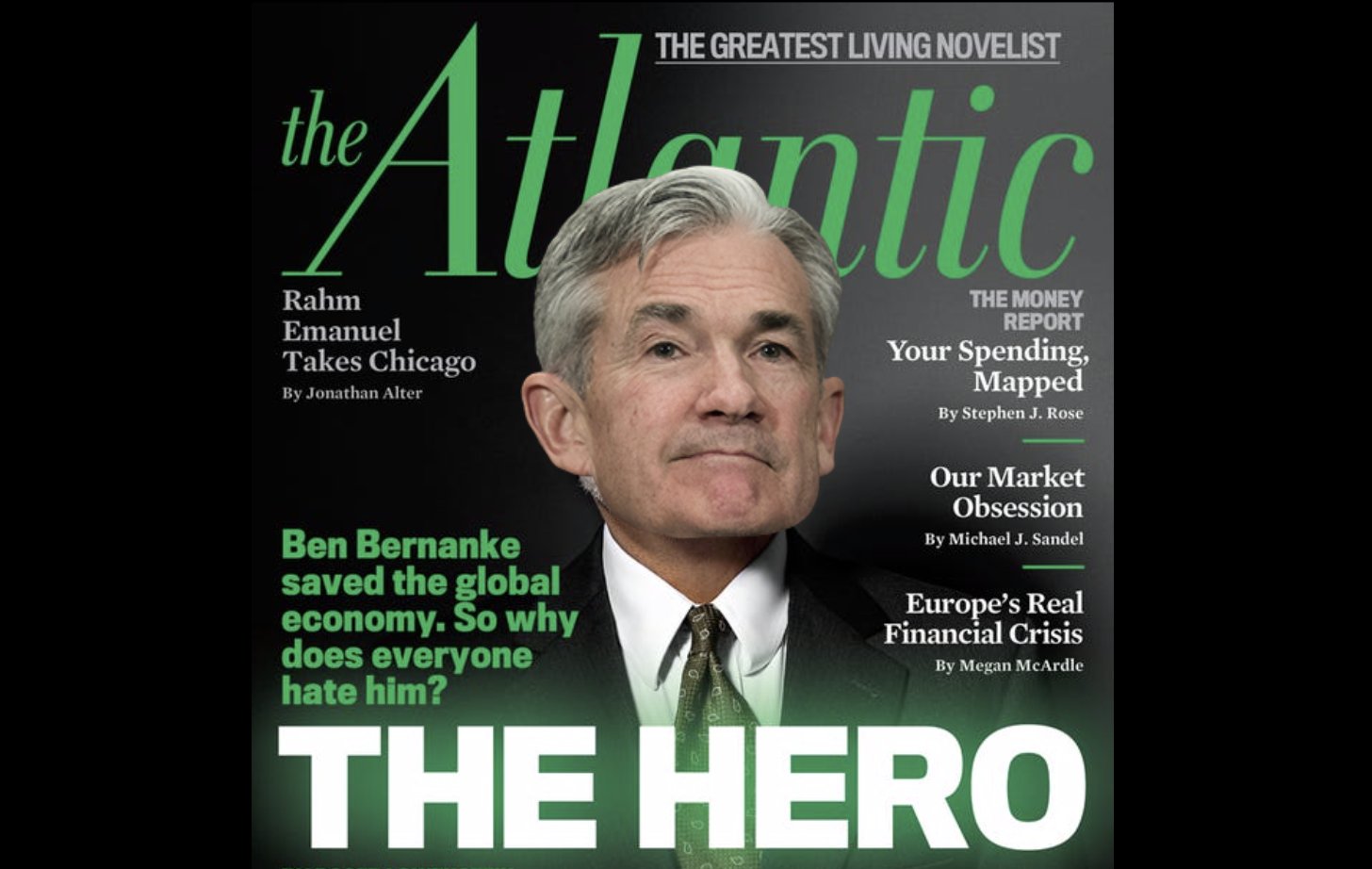

The truth stands on its own and is self-evident. Feynman is an example of an actual hero, not an MSM touted hero like Bernanke, Paulson, Geithner, Powell and the dozens of other psychopaths in suits who have been portrayed in the press as brilliant financial minds that saved the world. Real heroes take a singular stand for the truth, when everyone else goes along with mistruths, half-truths, and false narratives of those with a subversive self-serving agenda. The world is inundated in a blizzard of lies, designed to further the plans of those who control the levers of power and wealth.

Lies, backed by an unceasing stream of propaganda and fear, are being used to panic the masses into willingly abandon their freedoms, liberties and rights for the chains of false safety, security, and state control over every aspect of their lives. It is astonishing to watch in real time as a vast swath of America cowers in their homes, as demanded by their authoritarian elected leaders, while their livelihoods and net worth are purposely destroyed to benefit the .1% ruling class.

I see multiple analogies today with the shuttle disaster and the lessons learned and not learned. The leadership of NASA did not learn, as the same disregard for facts and data led to the Space Shuttle Columbia disaster seventeen years later.

Just as the mid-level engineers at Thiokol warned of imminent disaster for years before the tragedy, there have been voices in the wilderness (scorned and ridiculed as conspiracy theorists) warning about the reckless arrogance of the Federal Reserve and their Wall Street owners, as they pumped up the largest financial bubble in world history as their solution for the catastrophe created by their previous monetary disaster in 2008. Just as the hubristic out of touch leadership of NASA murdered fourteen innocent astronauts, the Fed has now twice destroyed millions of lives in the last twelve years.

These self-proclaimed experts have known the financial system was going to explode since the middle of 2019 when they began a series of desperate ruses, behind the curtain of the debt saturated Ponzi scheme, to keep the Wall Street cabal and hedge fund billionaires from facing the consequences of their fraudulent monetary machinations.

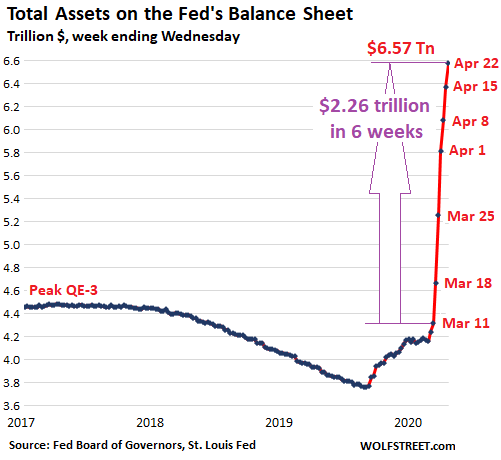

The surprise cutting of interest rates and emergency repo operations every night as we entered 2020 covered up the imminent disaster, as the mindless Harvard and Wharton MBAs programmed their high frequency trading computers to buy, buy, buy. Best economy ever. Greatest in the history of the world. Stock market at all-time highs. Then the China flu arrived, just in time. A quick 30% plunge in the stock market was all the Fed needed to rescue their true constituents – Wall Street and billionaire hedge funds – with $6 trillion, under the guise of saving the financial system for the little people.

If you want to figure out who benefits from a man-made crisis, just follow the money. The Federal government has committed at least $3 trillion of your grandchildren’s money to the crisis thus far, with the Federal Reserve announcing another $6 trillion of monetary support. That’s $9 trillion, or $70,000 per household. The average household size is 2.5. If we assume each household got their $1,200 Covid-19 rebate (actually just giving them back the taxes they already pay), that’s $3,000 per household.

A critical thinking individual might wonder who got the other $67,000 of stimulus, or 95.7% of the money allocated to “save America”. It certainly hasn’t made its way to small business owners who are going out of business faster than burning gas through a defective O-ring. If only $400 billion is making its way into the pockets of formerly working Americans, where did the other $8.6 trillion go?

It went directly into the pockets of Wall Street bankers, hedge fund managers, and the biggest corporations on the planet. The Fed has used this faux crisis to further enrich and bailout the richest men on the planet, while again dropping interest rates to zero and throwing grandma under the bus again. Let her eat cat food, declares Jerome Powell, champion and hero of downtrodden bankers. He’ll be “earning” $25 million a year from Wall Street as his payoff, the minute he saunters out of the Eccles Building in a couple years.

As unemployment approaches 20%, GDP plunges by 30%, food banks are running out of food, citizens remain locked in their homes under threat of arrest, and human misery approaches 1930 Great Depression levels, the Fed has managed to buy enough toxic debt and artificially rig the stock market, to engineer a 27% surge from its March lows. We should all applaud the brilliance of Powell and his fellow sycophants, as they have saved the asses of the .1%, for now.

The fate of this country was sealed well before this overblown hyped coronavirus appeared, to accelerate our demise. The warnings about too much debt, rigged financial markets, unrestrained politicians running trillion dollar deficits, silicon valley giants conspiring with the Deep State to turn the country into a surveillance state, a military industrial complex creating conflict around the globe, and a state media propaganda machine providing false information to the masses, were dismissed by those who could have acted.

The deficit is now expected to hit $3.7 trillion in 2020, pushing the national debt to $27 trillion. This country is 231 years old and 85% of our debt has been taken on in the last 23 years. The Fed’s balance sheet was $800 billion in 2008. It will shortly surpass $10 trillion, just a mere 1,250% increase in 12 years. Do you understand the analogy with the Space Shuttle Challenger yet?

We’ve left the launchpad at the same rate and angle as the Fed balance sheet. Those in charge assure us they have everything under control, but the coronavirus will prove to be our frozen O-ring. It has been decades of mismanagement, corruption, bad decisions, horrible leadership, delusional thinking, herd mentality, and an inability to summon the courage to deal with critical problems before they blew our country into a million smoking pieces of debris.

Average Americans are trapped in the crew cabin relying on Trump, Powell, Mnuchin, and a myriad of other “experts” to safely launch the American economy back into space. Trump has convened a re-opening task force consisting of dozens of CEOs from the biggest mega-corporations on earth. I know because I watched him read their names for fifteen minutes during one of his daily mind-numbing press conferences. If you had any doubt about who your leaders work for, that list tells you all you need to know. No one from your local steak shop, butcher or candlestick maker are represented on this task force. It reminded me of the list of prominent people chosen for the Rogers Commission.

The belief by those in charge that things can just go on as if nothing has happened are as delusional as the NASA administrators who were willfully blind to the truth of an impending disaster. The actions taken by the political and financial arms of the Deep State have guaranteed this malfunction will prove fatal for our country. The only question is how many seconds we have before our throttle up moment. I tend to be a pessimist, so I am leaning towards an explosion before the November election. The forthcoming financial catastrophic detonation will set off a chain of events considered impossible just a few short months ago.

The core elements of this Fourth Turning (debt, civic decay, global disorder) are going to juxtapose and connect, accelerating into a chain reaction of chaos, civil uprising, global war, mass casualties, the fall of empires, and ultimately the destruction of the existing social order (aka Deep State). Hopefully, heroes of Feynman’s stature will arise to help rebuild our country based upon common sense, truthfulness, factual assessment of our situation, and honoring the essential principles of our Constitution. Reality must take precedence over delusions, propaganda, and lies for us to regain our nation. Are we capable of learning the lessons from this major malfunction?

“Flight controllers here looking very carefully at the situation. Obviously, a major malfunction.” – Steve Nesbitt – NASA Mission Control

by

by

by

by

In 2009, 60 percent of buyers were married, 21 percent were single women, 10 percent single men and 8 percent unmarried couples. Thirteen percent of survey respondents were multi-generational households, including adult children, parents and/or grandparents.

In 2009, 60 percent of buyers were married, 21 percent were single women, 10 percent single men and 8 percent unmarried couples. Thirteen percent of survey respondents were multi-generational households, including adult children, parents and/or grandparents. In addition to tapping into their own savings (81 percent), first-time homebuyers used a variety of outside resources for their loan downpayment. Twenty-six percent received a gift from a friend or relative—most likely their parents—and six percent received a loan from a relative or friend. Ten percent of buyers sold stocks or bonds and tapped into a 401(k) fund.

In addition to tapping into their own savings (81 percent), first-time homebuyers used a variety of outside resources for their loan downpayment. Twenty-six percent received a gift from a friend or relative—most likely their parents—and six percent received a loan from a relative or friend. Ten percent of buyers sold stocks or bonds and tapped into a 401(k) fund. The biggest factors influencing neighborhood choice were quality of the neighborhood (69 percent), convenience to jobs (52 percent), overall affordability of homes (47 percent), and convenience to family and friends (43 percent). Other factors with relatively high responses included convenience to shopping (31 percent), quality of the school district (30 percent), neighborhood design (28 percent) and convenience to entertainment or leisure activities (25 percent).

The biggest factors influencing neighborhood choice were quality of the neighborhood (69 percent), convenience to jobs (52 percent), overall affordability of homes (47 percent), and convenience to family and friends (43 percent). Other factors with relatively high responses included convenience to shopping (31 percent), quality of the school district (30 percent), neighborhood design (28 percent) and convenience to entertainment or leisure activities (25 percent).

You must be logged in to post a comment.