Nick Gerli, in his interview with Wealthion, alludes to a number of figures which spell trouble for the residential market. If you own real estate or we’re considering entering the market soon, it’s worth checking out:

End of this cycle is neigh. Prepare you and yours now.

“In real terms, home prices have never been so high. My data goes back over 100 years, so this is something,” Nobel prize-winning economist Robert Shiller told CNBC’s “Trading Nation.”

Shiller is the co-founder of the S&P CoreLogic Case-Shiller home price index. He is worried about a housing bubble forming where the “Wild West” mentality pushes prices higher. He also is concerned about stocks and cryptocurrencies.

Glenn Kelman, CEO at Redfin, spoke with Bloomberg Radio’s Denise Pellegrini on Wednesday about the state of the US housing market. He said the latest surge in home prices could subside.

The Federal Reserve continued to increase its holdings of mortgage-backed securities by the tune of $40 billion per month, fueling a housing bubble with record-low mortgage rates and low inventory.

Even as the housing sector has more than recovered from the downturn, Chair Jerome Powell continues pedal to the metal with MBS purchases. According to the National Association of Realtors (NAR), this has resulted in the median price for a single-family home to soar the most on record in the first quarter.

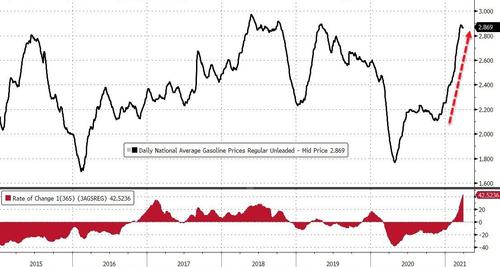

Don’t worry, there’s no inflation – apart from in gas and home prices. According to AAA, gas prices at the pump are back near their highest in 6 years, up a stunning 42% YoY…

The housing boom unleashed by the Federal Reserve during the pandemic was built on historically low mortgage rates (thanks Powell), low inventory, city-dwellers moving to rural areas, and remote-work phenomenon. In the latest installment of the desperate frenzy of buyers fleeing for suburban life in California, one home received 122 offers in just two days.

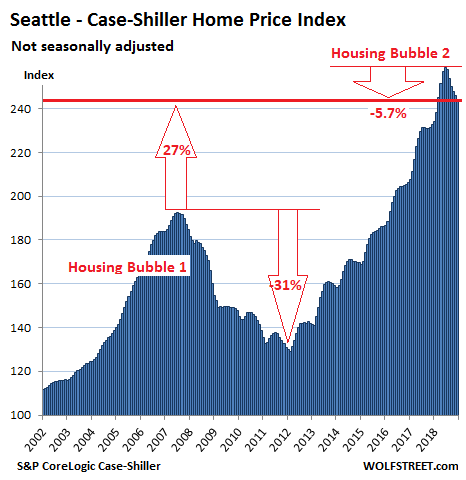

San Francisco Bay Area & Seattle lead with biggest multi-month drops since 2012; San Diego, Denver, Portland, Los Angeles decline. Others have stalled. A few eke out records.

San Francisco and San Diego are catching the Seattle cold, and others are sniffling too, as the most splendid housing bubbles in America are starting to run into reality.

House prices in the Seattle metro dropped 0.6% in December from November, according toS&P CoreLogic Case-Shiller Home Price Index, released this morning, and have fallen 5.7% from the peak in June 2018, the biggest six-month drop since the six-month drop that ended in February 2012 as Housing Bust 1 was bottoming out. The index is now at the lowest level since February 2018. After the breath-taking spike into June, the index is still up 5.1% year-over-year, and is 27% higher than it had been at the peak of Seattle’s Housing Bubble 1 (July 2007):

So Seattle’s Housing Bubble 2 is unwinding, but more slowly than it had inflated. Many real estate boosters simply point at the year-over-year gain to say that nothing has happened so far — which makes it a picture-perfect “orderly decline.”

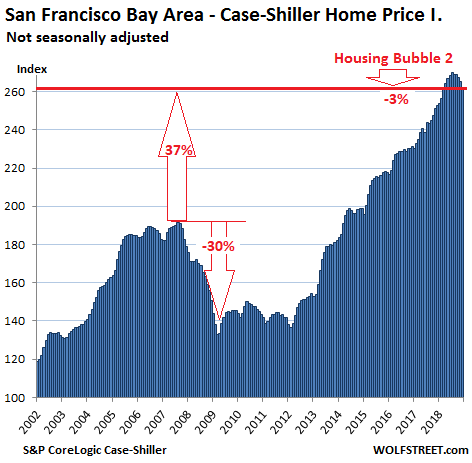

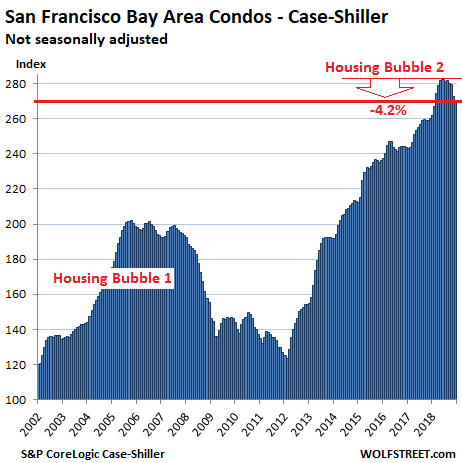

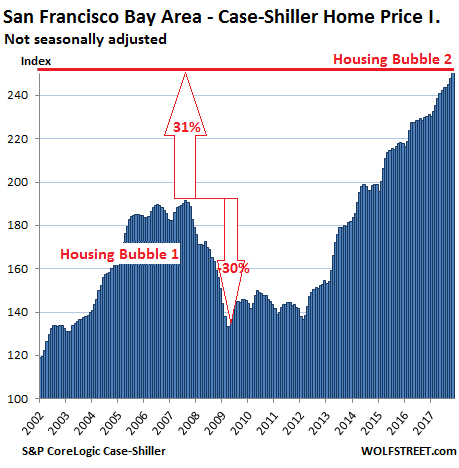

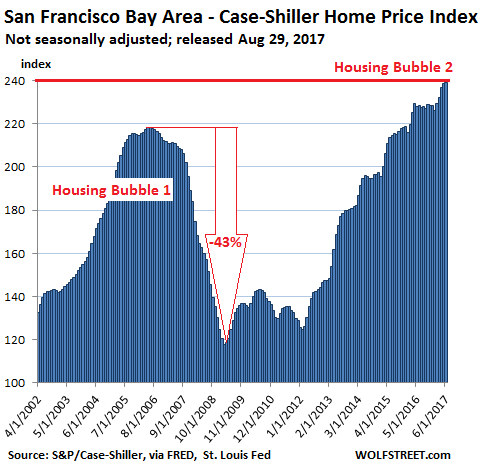

San Francisco Bay Area:

The Case-Shiller index for “San Francisco” includes five counties: San Francisco, San Mateo (northern part of Silicon Valley), Alameda, Contra Costa (both part of the East Bay ), and Marin (part of the North Bay). In December, the index for single-family houses fell 1.4% from November, the steepest month-to-month drop since January 2012. The index is now down 3% from its peak in July, the biggest five-month drop since March 2012.

Given the surge in early 2018, the index is still up 3.6% from a year ago and remains 37% above the peak of Housing Bubble 1, fitting into the theme of a perfect orderly decline:

Case-Shiller also has separate data for condo prices in the five-county San Francisco Bay Area, and this index fell 0.9% in December from November, after an blistering 2.4% drop in the prior month. From the peak in June 2018, the index has now dropped 4.2%, the steepest six-month drop since February 2012:

The Case-Shiller Home Price Index is a rolling three-month average; this morning’s release tracks closings that were entered into public records in October, November, and December. By definition, this causes the index to lag more immediate data, such as median prices, by several months.

The index is based on “sales pairs,” comparing the sales price of a house in the current month to the prior transaction of the same house years earlier (methodology). This frees the index from the issues that plague median prices and average prices — but it does not indicate prices.

It was set at 100 for January 2000; a value of 200 means prices as tracked by the index have doubled since the year 2000. Every index on this list of the most splendid housing bubbles in America, except Dallas and Atlanta, has more than doubled since 2000.

The index is a measure of inflation — of house-price inflation. It tracks how fast the dollar is losing purchasing power with regards to buying the same house over time.

So here are the remaining metros on this list of the most splendid housing bubbles in America.

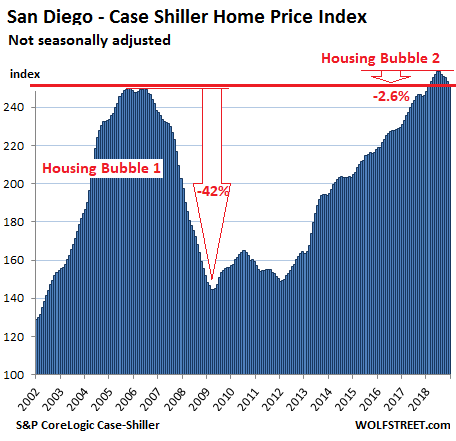

San Diego:

House prices in the San Diego metro declined 0.7% in December from November and are now down 2.6% from the peak in July, the biggest five-month drop since March 2012, leaving the index at the lowest level since February 2018, and just one hair above the peak of Housing Bubble 1:

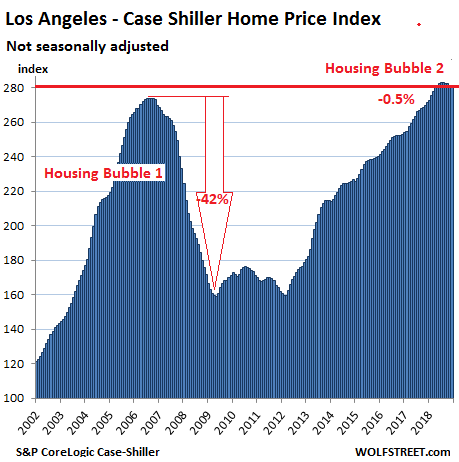

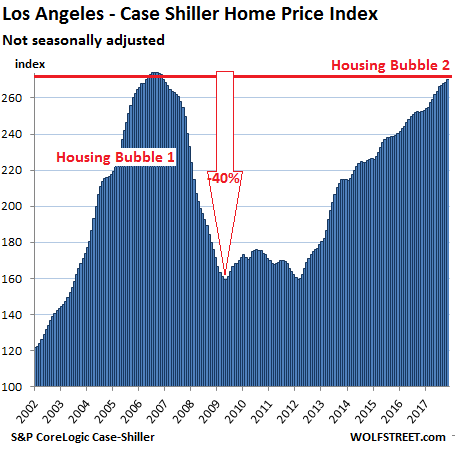

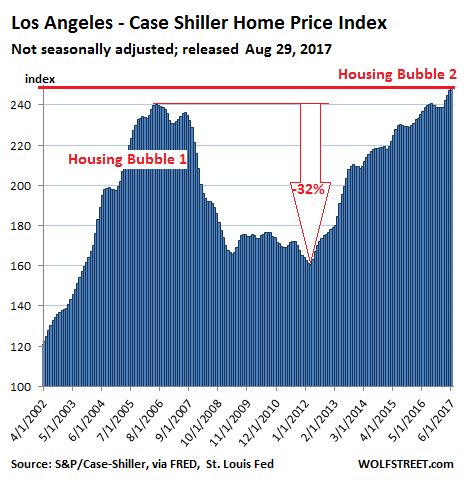

Los Angeles:

The Case-Shiller index for the Los Angeles metro was about flat in December with November but down 0.5% from the peak in August — don’t laugh, the largest four-month decline since March 2012. What this shows is just how relentless Housing Bubble 2 has been. The index is up 3.7% year-over-year:

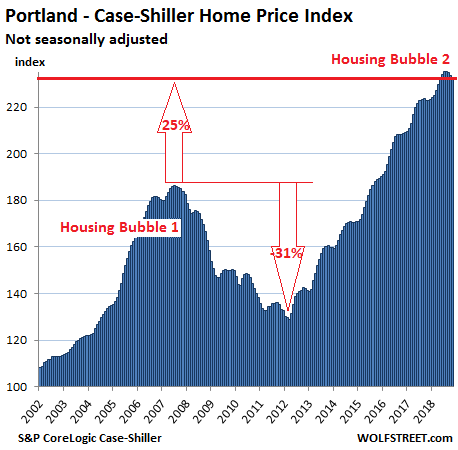

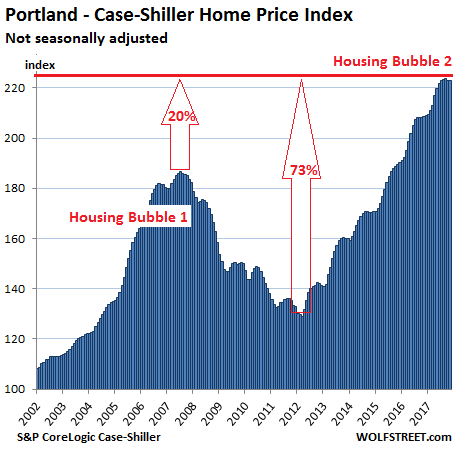

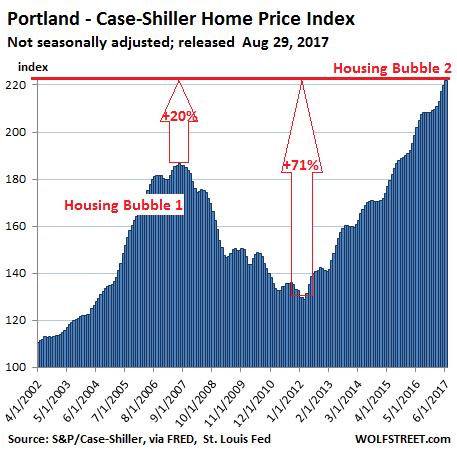

Portland:

The Case-Shiller Index for the Portland metro inched down in December from November for the fifth month in a row and is now down 1.4% from the peak in July 2018. And that was the steepest five-month drop since March 2012. Year-over-year, the index was up 3.9%:

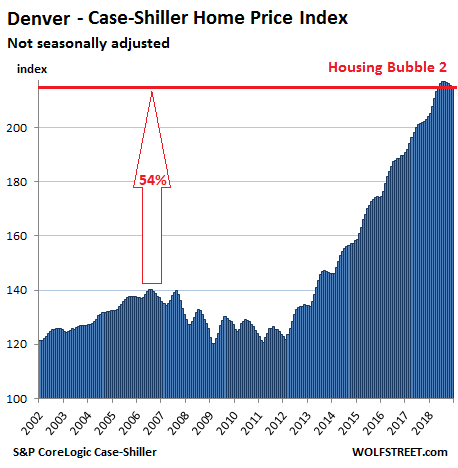

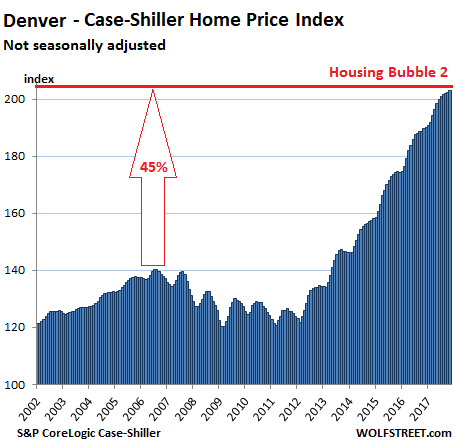

Denver:

House prices in the Denver metro edged down in December from November for the fourth month in a row, after an uninterrupted 33-month run of monthly increases. The four-month drop amounted to 0.9%, which, you guessed it, was the steeped such drop since March 2012. The index is at the lowest level since May 2018 but is still up 5.5% year-over-year:

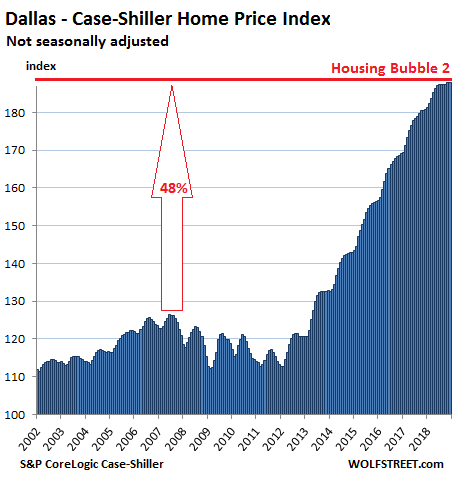

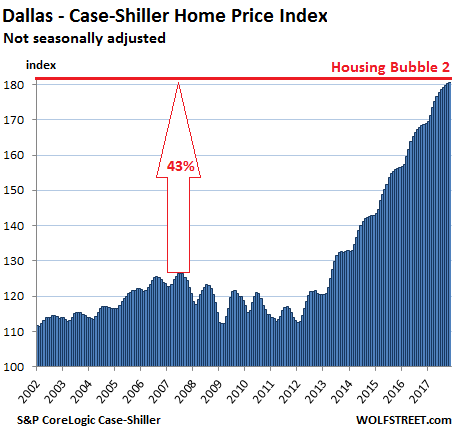

Dallas-Fort Worth:

The Case-Shiller Index for the Dallas-Fort Worth metro in December ticked up by less than a rounding error to a new record, leaving it essentially flat for the seventh month in a row. The index is up 4.0% year-over-year:

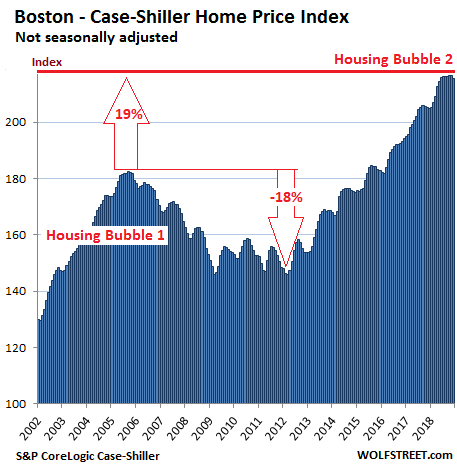

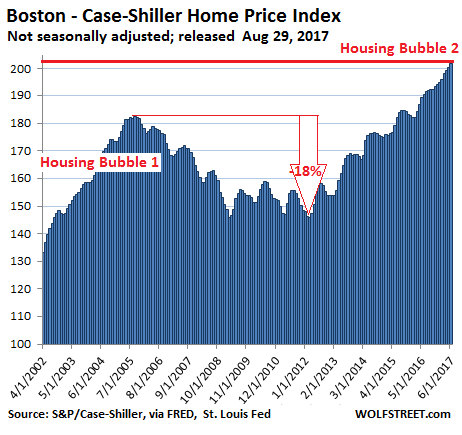

Boston:

In the Boston metro, house prices dipped 0.5% in December from a record in November and are now back where they’d been in June. The Case-Shiller Index is up 5.3% from a year ago:

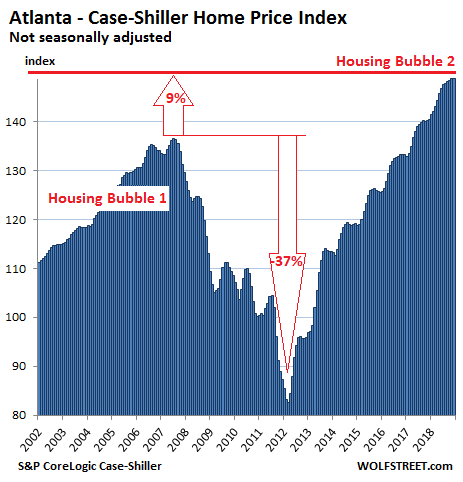

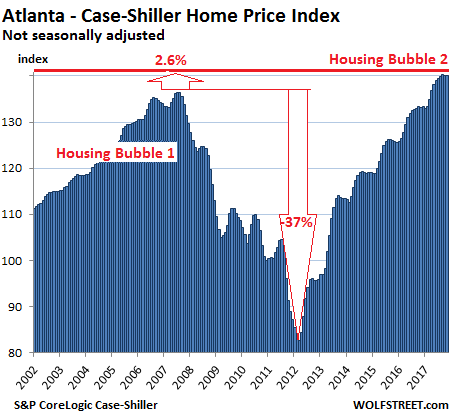

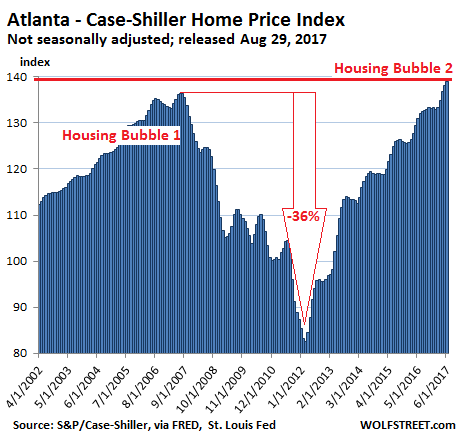

Atlanta:

The Case-Shiller Home Price Index for the Atlanta metro inched up a smidgen in December, to a new record, and is up 5.9% from a year ago:

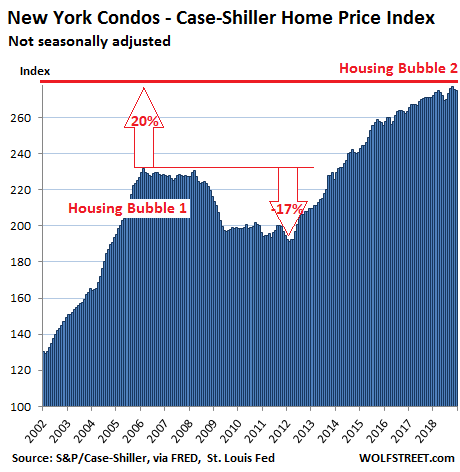

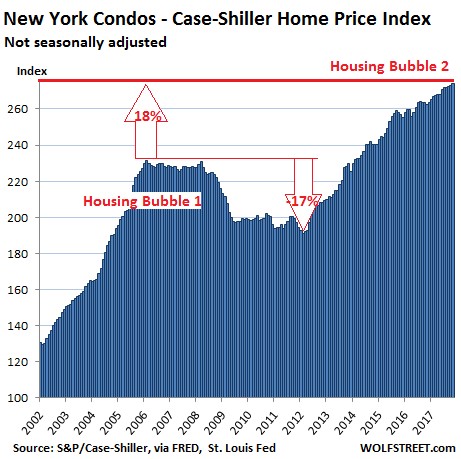

New York City Condos:

The Case-Shiller index for condo prices in the New York City metro ticked down in December for the second month in a row after a mighty bounce in September and an uptick in October. This index can be volatile, but after all these bounces and declines, the index was up just 1.5% from a year ago, the smallest year-over-year price gain on this list of the most splendid housing bubbles in America:

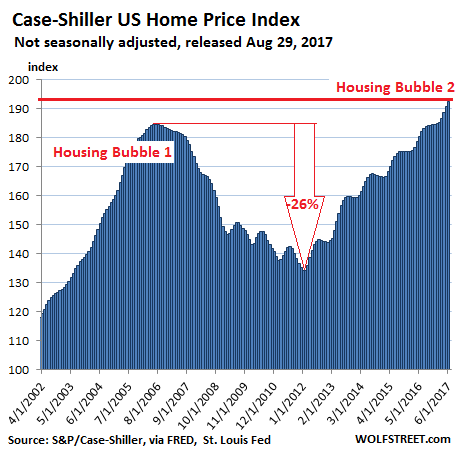

On a national basis, these individual markets get averaged out with other markets that didn’t quite qualify for this list since their housing bubble status has not reached the ultimate splendidness yet. Some of those markets, such as the huge metro of Chicago, remain quite a bit below their Housing Bubble 1 peaks and are now declining, while others are shooting higher.

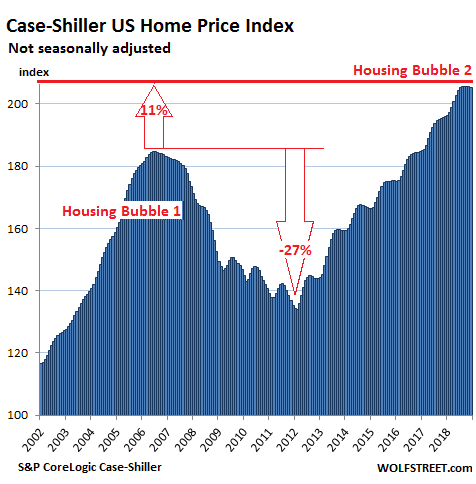

So the Case-Shiller National Home Price Index has been about flat since July, but is still up 4.7% year-over-year and is 11% higher than it had been at its prior peak in July 2006 during Housing Bubble 1:

It always boils down to this: Regardless of how thin you cut a slice of bologna, there are always two sides to it. When home prices drop after a housing bubble, there are many losers. But here are the winners – including a whole generation. Listen to my latest podcast, an 11-minute walk on the other side…

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate “beer money.” I appreciate it immensely. Click on the beer mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article?Sign up here.

Now that Housing Bubble #2 Is Bursting… How Low Will It Go?

Unless the Fed is going to start buying millions of homes outright, prices are going to fall to what buyers can afford.

There are two generalities that can be applied to all asset bubbles:

1. Bubbles inflate for longer and reach higher levels than most pre-bubble analysts expected

2. All bubbles burst, despite mantra-like claims that “this time it’s different”

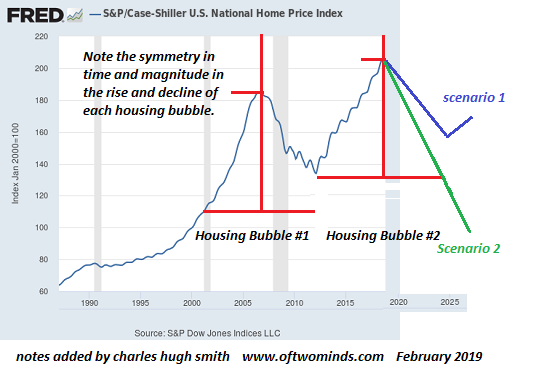

The bubble burst tends to follow a symmetrical reversal of very similar time durations and magnitudes as the initial rise. If the bubble took four years to inflate and rose by X, the retrace tends to take about the same length of time and tends to retrace much or all of X.

If we look at the chart of the Case-Shiller Housing Index below, this symmetry is visible in Housing Bubble #1 which skyrocketed from 2003-2007 and burst from 2008-2012.

Housing Bubble #1 wasn’t allowed to fully retrace the bubble, as the Federal Reserve lowered interest rates to near-zero in 2009 and bought $1+ trillion in sketchy mortgage-backed securities (MBS), essentially turning America’s mortgage market into a branch of the central bank and federal agency guarantors of mortgages (Fannie and Freddie, VA, FHA).

These unprecedented measures stopped the bubble decline by instantly making millions of people who previously could not qualify for a privately originated mortgage qualified buyers. This vast expansion of the pool of buyers (expanded by a flood of buyers from China and other hot-money locales) drove sales and prices higher for six years (2012-2018).

As noted on the chart below, this suggests the bubble burst will likely run from 2019-2025, give or take a few quarters.

The question is: what’s the likely magnitude of the decline? Scenario 1 (blue line) is a symmetrical repeat of Housing Bubble #2: a retrace of the majority of the bubble’s rise but not 100%, which reverses off this somewhat higher base to start Housing Bubble #3.

Since the mainstream consensus denies the possibility that Housing Bubble #2 even exists (perish the thought that real estate prices could ever–gasp–drop), they most certainly deny the possibility that prices could retrace much of the gains since 2012.

More realistic analysts would probably agree that if the current slowdown (never say recession, it might cost you your job) gathers momentum, some decline in housing prices is possible. They would likely agree with Scenario 1 that any such decline would be modest and would simply set the stage for an even grander housing bubble #3.

But there is a good case for Scenario 2, in which price plummets below the 2012 lows and keeps on going, ultimately retracing the entire housing bubble gains from 2003.

Why is Scenario 2 not just possible but likely? There are no more “saves” in the Fed’s locker. Dropping interest rates to zero and buying another trillion in MBS won’t have the same positive effects they had in 2009-2018. Those policies have run their course.

Among independent analysts, Chris Hamilton is a must-read for his integration of demographics and economics. Please read (via Zero Hedge)Demographics, Debt, & Debasement: A Picture Of American Insolvencyif you want to understand why near-zero interest rates and buying mortgage-backed securities isn’t going to spark Housing Bubble #3.

Millennials are burdened with $1 trillion in student loans and most don’t earn enough to afford a home at today’s nosebleed prices. When the Fed drops the Fed Funds Rate to zero, it doesn’t follow that mortgage rates drop to zero. They drop a bit, but not enough to transform an unaffordable house into an affordable one.

Buying up $1 trillion in sketchy mortgages worked in 2009 because it bailed out everyone who was at risk of absorbing huge losses as a percentage of those mortgages defaulted. The problem now isn’t one of liquidity or iffy mortgages: it’s the generation that would like to buy homes finds they don’t earn enough, and their incomes are not secure enough, to gamble everything on an overpriced house that chains them to a local economy they might want to leave if opportunities arise elsewhere.

In other words, the economy has changed, and the sacrifices required to buy a house in hot markets at today’s prices make no sense. The picture changes, of course, in areas where 2X or 3X a typical income will buy a house, and 1X a pretty good income will buy a house.

Unless the Fed is going to start buying millions of homes outright, prices are going to fall to what buyers can afford. As China’s debt bubble implodes, the Chinese buyers with cash (probably not even cash, just money borrowed in China’s vast unregulated Shadow Banking System) who have propped up dozens of markets from France to Vancouver will vanish, leaving only the unwealthy as buyers.

The only question of any real interest is how low prices will drop by 2025. We’re so accustomed to being surprised on the upside that we’ve forgotten we can surprised on the downside as well.

(Ben Jones) A report from theOrange County Registerin California. “When 2018 started, the housing buzz was ‘where’s the supply?’ Now with the year almost complete, the industry now wonders ‘where did all the buyers go?’ Ponder that in housing-starved Southern California, builders have the largest standing supply of completed homes to sell in six years. Yes, newly constructed residences are a pricey niche that’s not for everyone. Still, the change of momentum is remarkable.”

“Housing tracker MetroStudy reports that at the end of the third quarter, 3,401 new homes were finished but unsold in the four-county region covered by the Southern California News Group. That’s up 428 homes in 12 months, or 14 percent, and was the highest inventory level since 2012’s second quarter.”

“But this year, house hunters have pulled back — for both new and existing residences. If you need a stark measurement of the buyer reluctance, look at this: CoreLogic reported Southern California home sales of all types in September suffered their largest year-over-year decline in nearly eight years.”

“It adds up to a situation where not too long ago local builders had many buyers waiting months for homes to be completed. Today, most housing projects offer new homes ready for immediate occupancy — with special pricing, no less.”

“Look at the market upheaval in Orange County. It’s got the region’s biggest boost in new-home supply, according to MetroStudy. As of Sept. 30, O.C. had 1,074 finished residences for sale, up 277 or 35 percent in a year. It’s O.C.’s largest new-home inventory in nearly 12 years.”

“Builders, faced with their own industry competition, also are up against homeowners in the region who rushed to list their homes. As that new-home supply swelled in the third quarter, Southern California owners averaged 35,333 listings, according to ReportsOnHousing. That’s 4,568 more existing homes on the market than a year earlier — or 10 times the growth of unsold new homes.”

“Yet this is an autumn period when many owners typically take homes off the market. Who knew that 2018 would be the year when house hunters had too many homes to choose from?”

FromCurbed Los Angeles. “The number of homes for sale in the Los Angeles area climbed more than 30 percent in October, according to Zillow. That suggests the region’s sky-high home prices could continue to fall, as they did in September.”

“During the month of October, inventory (the total number of houses and condos on the market) in Los Angeles and Orange counties jumped nearly 32 percent above levels recorded in October of last year. A bump in the number of homes available for sale often corresponds with falling prices, since sellers have more competition when listing their homes and are less likely to be overwhelmed with offers above asking price.”

“The spike in the number of homes available for purchase mirrors—and far exceeds—a nationwide trend. Across the country, inventory went up 3 percent since last year, marking the first yearly increase since 2014.”

“‘This is a phenomenon we’re seeing in several pricey markets throughout the country,’ says Zillow economist Aaron Terrazas. He points out that inventory has also risen by double digit percentages in San Francisco, Seattle, and San Jose.”

“Terrazas tells Curbed that much of the inventory growth in LA and other markets is driven by homes that take longer to sell, suggesting that buyers may be less willing to pay bloated prices.”

“‘This is a reflection of how poor affordability is in those areas,’ says Terrazas. ‘Buyers are starting to pull back a little bit from where they were a year ago.’”

Hong Kong homeowners who bought flats in the last several months have seen their value decline as much as 20% in a matter of recent weeks, according to HSBC, sending values into negative equity which had only left the region from the prior downturn that ended in early 2017, reports theSouth China Morning Post.

Hong Kong’s famously expensive property market has started to feel the strain lately from a fall in demand caused by rising interest rates, a struggling stock market and fears about the impact of the US-China trade war. Negative equity occurs when a home loan exceeds the market value of the property, and has not been seen in Hong Kong since early 2017. –SCMP

“Theoretically, buyers who obtained a mortgage of 90 per cent of the flat’s value will fall into negative equity once home prices have dropped more than 10 per cent,” said Chief Vice-President at mReferral Mortgage Brokerage Services, Sharmaine Lau.

The largest losses are likely to be flat owners who paid sky-high prices for tiny apartments in older tenements, according to industry watchers, who add that banks tend to become very conservative in valuing such properties when the real estate market takes a turn for the worse.

“Lower valuations will first apply to flats that have less marketability. Banks’ valuations, which are supported by surveyors, are made in line with market conditions,” said Cushman and Wakefield head of valuation and advisory services for the Asia-Pacific region, Chiu Kam-kuen.

Meanwhile, SCMP was able to find apartments at older housing developments which are now valued at HSBC far below their recent selling prices.

A 234 square foot unit at 36-year-old Lee Bo Building in Tuen Mun, which was sold for HK$3.82 million on October 8, is now valued 20 per cent lower at HK$3.08 million. In North Point, a 128 square foot unit at 41-year-old Yalford Building, sold on August 29 for HK$3.1 million, is also valued a fifth lower now by the bank, at HK$2.48 million.

In Kowloon, a 210 square foot unit at 34-year-old Hong Fai Building in Cheung Sha Wan sold for HK$3.87 million on June 20 is already down about 13 per cent, according to HSBC, at HK$3.38 million.

The spectre of negative equity is only going to get worse, according to Louis Chan, Asia-Pacific vice-chairman and chief executive for residential sales at Centaline Property.

“More homeowners will fall into negative equity next year as flat prices may decline by 10 per cent,” he said. –SCMP

The precipitous drop may force companies such as the Hong Kong Mortgage Corporation (HKMC) to adjust their mortgage insurance program in light of market developments.

Under the program, buyers of flats worth less than HK$4.5 million can get mortgage loans of up to 90 per cent of the unit’s value, capped at HK$3.6 million, while for flats priced between HK$4.5 million and HK$6 million the maximum loan-to-value ratio is 80 per cent, capped at HK$4.8 million.

In the first quarter of 2018, HKMC said 6,955 applicants secured HK$26.86 billion in home loans under the mortgage insurance program. In 2017, a total of HK$32.3 billion in mortgages were granted to 8,829 applicants, up from HK$24.6 billion of 7,145 successful in 2016. –SCMP

Negative equity reached its peak in Hong Kong in 2003 following an outbreak of Severe Acute Respiratory Syndrome (SARS) which sent already-teetering home values plummeting. According to the HKMA, over 105,000 households found themselves in negative equity at the time – all of which were above water as of the first quarter of last year.

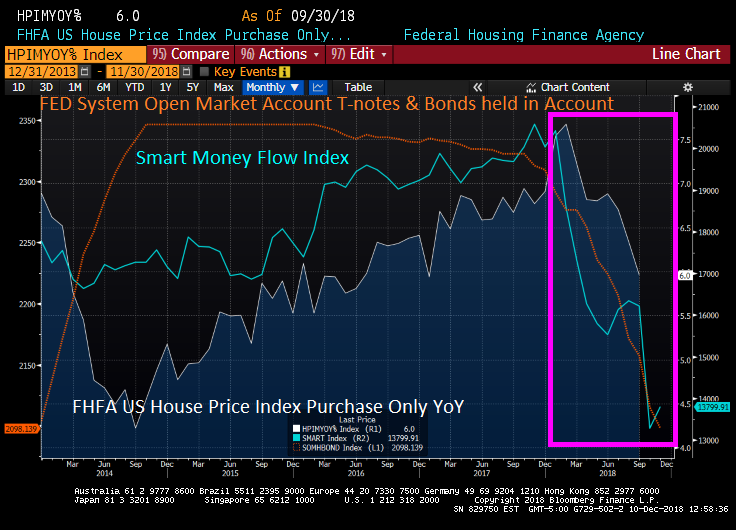

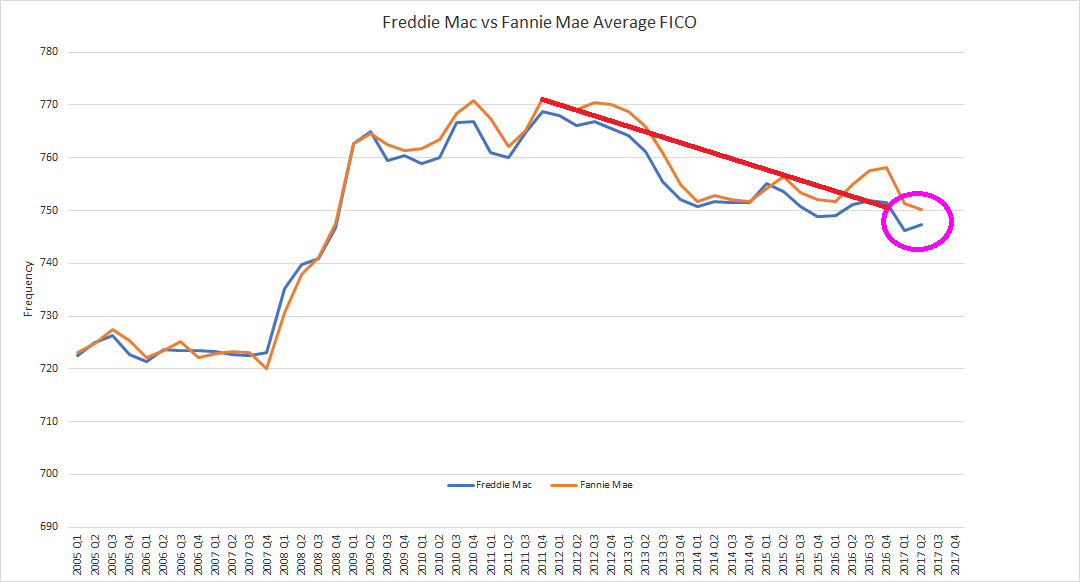

Fannie Mae and Freddie Mac, the mortgage giants in seemingly perpertual conversatorship with the FHFA, have mortgage loans that are even more risky in terms of loan-to-value (LTV) ratios than during the catastrophic housing bubble of the 2000s.

The “good” news is that the average FICO (credit) score for Fannie and Freddie loan purchases is above those from the housing bubble. But the trend is worrisome.

In terms of Debt-to-income ratios (or Detes as Tom Haverford would say), the Detes are below housing bubble levels, but have been rising since the end of 2008.

The housing market indicated that a crisis was coming in 2008. Is the same thing happening once again in 2018?

For several years, the housing market has been one of the bright spots for the U.S. economy. Home prices, especially in the hottest markets on the east and west coasts, had been soaring. But now that has completely changed, and home sellers are cutting prices at a pace that we have not seen since the last recession. In case you are wondering, this is definitely a major red flag for the economy. According toCNBC, home sellers are “slashing prices at the highest rate in at least eight years”…

After three years of soaring home prices, the heat is coming off the U.S. housing market. Home sellers are slashing prices at the highest rate in at least eight years, especially in the West, where the price gains were hottest.

It is quite interesting that prices are being cut fastest in the markets that were once the hottest, because that is exactly what happened during the subprime mortgage meltdown in 2008 too.

According toRedfin, more than one out of every four homes for sale in America had a price drop within the most recent four week period…

In the four weeks ended Sept. 16, more than one-quarter of the homes listed for sale had a price drop, according to Redfin, a real estate brokerage. That is the highest level since the company began tracking the metric in 2010. Redfin defines a price drop as a reduction in the list price of more than 1 percent and less than 50 percent.

That is absolutely crazy.

I have never even heard of a number anywhere close to that in a 30 day period.

Of course the reason why prices are being dropped is because homes are not selling. The supply of homes available for saleis shooting up, and that is good news for buyers but really bad news for sellers.

It could be argued that home prices needed to come down because they had gotten ridiculously high in recent months, and I don’t think that there are too many people that would argue with that.

But is this just an “adjustment”, or is this the beginning of another crisis for the housing market?

Just like a decade ago, millions of American families have really stretched themselves financially to get into homes that they really can’t afford. If a new economic downturn results in large numbers of Americans losing their jobs, we are once again going to see mortgage defaults rise to stunning heights.

The general burden of the American worker is the daily task of squaring the difference between the booming economy reported by the government bureaus and the dreary economy reported in their biweekly paychecks. There is sound reason to believe that this task, this burden of the American worker, has been reduced to some sort of practical joke. An exhausting game of chase the wild goose.

How is it that the economy’s been growing for nearly a decade straight, but the average worker’s seen no meaningful increase in their income? Have workers really been sprinting in place this entire time? How did they end up in this ridiculous situation?

The fact is, for the American worker, America’s brand of a centrally planned economy doesn’t pay. The dual impediments of fake money and regulatory madness apply exactions which cannot be overcome. There are claims to the fruits of one’s labors long before they’ve been earned.

The economy, in other words, has been rigged. The value that workers produce flows to Washington and Wall Street, where it’s siphoned off and miss-allocated to the cadre of officials, cronies, and big bankers. What’s left is spent to merely keep the lights on, the car running, and food upon the table.

And unfortunately, things are likely to only go downhill from here.

[T]here came another folly of government intervention in 1930 transcending all the rest in significance. In a world staggering under a load of international debt which could be carried only if countries under pressure could produce goods and export them to their creditors, we, the great creditor nation of the world, with tariffs already far too high, raised our tariffs again. The Hawley-Smoot Tariff Act of June 1930 was the crowning folly of the who period from 1920 to 1933….

Protectionism ran wild all over the world. Markets were cut off. Trade lines were narrowed. Unemployment in the export industries all over the world grew with great rapidity, and the prices of export commodities, notably farm commodities in the United States, dropped with ominous rapidity….

The dangers of this measure were so well understood in financial circles that, up to the very last, the New York financial district retained hope the President Hoover would veto the tariff bill. But late on Sunday, June 15, it was announced that he would sign the bill. This was headline news Monday morning. The stock market broke twelve points in the New York Time averages that day and the industrials broke nearly twenty points. The market, not the President, was right.

Even though the stock markethas been booming, everything else appears to indicate that the U.S. economy is slowing down.

If home prices continue to fall precipitously, that is going to put even more pressure on the system, and it won’t be too long before we reach a breaking point.

We have a decidedly nuanced view ofReal Estate: Whilenot neccessarily a bubble, it has been the prime driver of the economy since rates were slashed to half century lows 3 years ago.

The early stages of a housing cycle are fun for pretty much everyone. Homeowners see their equity start to rise and feel smart for having bought, home seekers have to pay up, but not too much, and fully expect their new home to keep appreciating. People with modest incomes feel a bit of pinch but can still afford to stick around.

But later on the bad starts to outweigh the good. Existing homeowners still enjoy the ride but would-be buyers find themselves priced out of their top-choice neighborhoods. And residents who aren’t tech millionaires find that they can no longer afford to live where they work. Consider the plight of a teacher or cop pretty much anywhere in California these days:

Drew Barclay has a master’s degree in education and three years of experience as an English teacher, but, like most new teachers in Davis, he can’t afford to live there.

Instead, Barclay, 31, shares a rental in Sacramento that costs him $950 a month — about 40 percent of the $2,550 he brings home each month after taxes.

He is so certain that he won’t be able to qualify for a loan for a home in Davis on his $47,000 annual salary that he hasn’t bothered to house hunt. The median price for a house in the city in March was $682,500, according to tracking firm CoreLogic. Renting also is prohibitive, with the average rent in Davis about $2,500 a month, according to Zillow, a real estate website.

Davis Joint Unified officials hope to get a little help from state legislators. Last week, the state Senate voted 24-8 to waive the annual school district parcel tax of $620 for teachers and other employees of the Yolo County school district.

Davis school board member Alan Fernandes said that about two-thirds of the district’s teachers live outside Davis where housing is less expensive. He said the bill would encourage more of the district’s teachers to live in the community they serve.

Davis Joint Unified regularly passes parcel taxes to keep class sizes down and to support classroom programs. In 2016, 71 percent of Davis voters approved Measure H, a yearly tax of $620 on each parcel of taxable real property in the district for eight years. The measure raises $9.5 million a year to support math, reading and science programs and reduced class sizes for elementary grades.

But the roughly $50 a month exemption isn’t likely to help Davis Joint Unified teachers enough to make buying a house affordable. The teachers are some of the lowest-paid educators in the region, with some of the highest health care costs.

Barclay said he knows teachers 10 or 15 years older than he is who are renting rooms in other educators’ homes to get by. He said some teachers have weekend jobs to make enough money to pay their bills.

“Because I’m fairly certain I can’t put down permanent roots here, I don’t see this position as a permanent one,” Barclay said of his job as an English teacher at Davis Senior High School.

California school districts have responded by offering signing bonuses, housing stipends, computers and free tuition to educators who sign up with their districts.

When housing costs reach this point there’s no real fix. Raise taxes to increase teacher pay and there’s political trouble. Cut back on other services and the quality of life declines. “Streamline” the schools and educational outcomes and teacher morale plummet.

There’s a limit, in other words, to the ascent of home prices beyond which the system starts to break down. And when the people who make a town run smoothly – teachers, firefighters, cops, sanitation workers – can no longer afford to live there, that town has clearly crossed the line.

Based on the Case-Shiller home price index, which is now back to its 2007 housing bubble peak, there are a lot more Davis, CAs out there, with all the pathologies that that implies.

A housing bubble, of course, is just a symptom of a bigger problem. Easy money distorts the workings of a market economy by causing the prices of many assets to soar beyond all reason, enriching the owners and impoverishing the users. Typically, when housing reaches this point so have stocks and other financial assets,CEO salaries, corporate concentration, political corruption and a long list of other evils that feed on low interest rates and lax lending standards. The confluence of resulting problems then brings the cycle to a noisy end.

The housing market is starting to overheat. Again.

According to the latest BLS data, average hourly wages for all US workers in November rose at a relativelybrisk 2.7% relative to the previous year, if below the Fed’s “target” of 3.5-4.5% as countless economists are unable to explain how 4.1% unemployment, and “no slack” in the economy fails to boost wage growth. Another problem with tepid wage growth, in addition to crushing the Fed’s credibility, is that it keeps a lid on how much overall price levels can rise by, i.e. inflation. Meanwhile, with record global debt, it has been the Fed’s imperative to boost inflation at any cost to inflate away the debt overhang, however weak wages have made this impossible.

Well, not really.

Because a quick look at US housing shows that while wages may be growing at roughly 2.7%, according to thelatest Case Shiller data, 18 of 20 metro areas in the US saw home prices grow at a higher pace, while 16 of 20 major U.S. cities experienced home price growth of 5.4% or higher, double the average wage growth, and something which even the NAR has been complaining about with its chief economist Larry Yun warning that as the disconnect between prices and wages becomes wider, homes become increasingly unaffordable for most Americans.

Confirming the recent jump in home prices, at the national level in February home prices for the Top 20 metro areas soared 6.8% YoY according to Case Shiller, the fastest rate since June 2014…

… and hitting a new all time high nationwide.

And while this should not come as a surprise – considering we have pointed it out on numerous occasions in the past – one look at the chart below confirms that something very troubling is taking place in San Francisco, which has either become “Vancouver South” when it comes to Chinese hot money laundering, or the second housing bubble has finally arrived on the West Coast. And while according to Case-Shiller data, home prices in San Francisco rose “only” 10.1% Y/Y, a more accurate breakdown of San Fran housing prices fromParagon Real Estateindicates a record 24% annual increase in San Francisco home prices, which increased by $110,000 in just the past quarter.

Behold: a housing bubble…

Also worth keeping an eye on: price appreciation in Sin City has quietly surged in recent months, and in February home prices jumped 11.6% Y/Y, the highest annual increase in years. Considering Las Vegas was the epicenter of the last housing bubble when prices exploded higher only to crash, it may be a good idea to keep a close eye on price tendencies in this metro area for a broader confirmation of the second housing bubble, than just the microcosm that is San Francisco.

* * *

Meanwhile, for those looking to buy for the first time, conditions have never been worse. Growth in property values is outpacing wage gains and limiting affordability, representing a major headwind for first-time buyers, and the broader market.

Finally, putting the above data in context, here are twocharts courtesy of real-estate expert Mark Hanson, the first of which shows how much household income increase is needed to buy the median priced home in key US cities…

… while the next chart shows the divergence between actual household income, and the income needed to buy the median priced house.

This home on Plymouth Drive in Sunnyvale, Calif. recently set the highest price per square foot ever recorded by the Multiple Listing Service. The two bedroom, two bath home – 848 square feet in size – sold in two days for $2 million. It had been listed for $1.45 million. That means it sold for $2,358 per square foot, which is the highest price per square foot in Sunnyvale recorded by MLS Listings which has data going back to Jan. 1, 2000.

SUNNYVALE — The small, unassuming home in the Cherry Chase neighborhood was on the market just two days before it sold for $2 million, a whopping $550,000 over its asking price.]

In this red-hot real estate market, the price tag barely caused a stir. What did was the other number that turned the home into another Bay Area record-breaker: It sold for the highest square-foot price recorded in Sunnyvale — a stunning $2,358, according to MLSListings, which tracks homes sales going back to 2000.

The jaw-dropping price tag suggests Sunnyvale, which has traditionally been less expensive than neighboring cities Cupertino or Palo Alto, is becoming a real estate destination in itself.

“I was blown away by it,”Doug Larson of Coldwell Banker, the real estate agent who sold the home, said of the price it fetched.

There’s nothing particularly breathtaking about the modest, one-story house on quiet, tree-lined Plymouth Drive. But it sits nestled at the center of one of the country’s most expensive real estate markets. As prices continue to increase throughout the Bay Area,pushing out even some highly paid tech workers, experts say more residents are flocking to relatively affordable Sunnyvale, driving up prices there.

“It’s become the new hot market,” said Jim Harrison, president and CEO of MLSListings.

Homes in Sunnyvale sold for a median price of $1.57 million in January, according to Zillow. That’s affordable compared to neighboring Cupertino, with a median sale price of $2.2 million, or Palo Alto, with a median price of $3 million.

But it may not stay that way for long. So far this year, homes in Sunnyvale are selling for an average of 28 percent over their listed price and are spending just nine days on the market, Harrison said. A four-bedroom, two-bath, 2,000 square foot house in the city recentlysold for close to $800,000 over its listing price, fetching $2.47 million.

The Plymouth Drive house is small by comparison, just 848 square feet, which contributed to its high per-square-foot price. But it’s on a large lot — 6,000 square feet. That makes it a prime candidate for the new owner to tear it down and build something else, Harrison said.

Realtor Juliana Lee of Keller Williams, who represents the buyer of the Plymouth Drive home, declined to comment on behalf of herself and her client.

Listing photos of the home show a small, beige house with a huge backyard, hardwood floors and a large front window with white shutters. Before the sale, the most expensive per-square-foot price recorded in Sunnyvale was $2,175, according to MLSListings. That was for a 1,839-square-foot, two-bedroom home on a 36,155 square foot lot, which sold for $4 million.

Sunnyvale has become popular in part because of its proximity to Silicon Valley’s tech jobs, said realtor James Morris of James Morris Homes, which has offices in San Jose and Saratoga. LinkedIn is headquartered in the city, Apple is just next door in Cupertino, and Google is on the other side in Mountain View.

Millennials don’t want to endure long commutes on the Bay Area’s clogged freeways, Morris said.

“They will pay that premium to be close to their jobs and not have to drive,” he said.

When Larson put the Plymouth Drive house on the market on Feb. 7, he asked for $1.45 million and assumed his client would get about $1.6 million. The next day, he opened the house for a realtor tour so the community’s agents could check out the property and determine if it was something their clients might want. It generated a lot of interest, Larson said, with some agents indicating they had buyers willing to offer as much as $1.8 million.

Friday morning, a realtor called Larson and told him she was sending over an offer. Larson told her his client wasn’t accepting offers until the following Wednesday, but the persistent realtor refused to take no for an answer and sent her client’s offer that afternoon.

It was too tempting to pass up — $2 million, all cash, closing in 10 days. The seller was shocked.

“She said, ‘What?’” Larson said. “She was as taken aback as I was.”

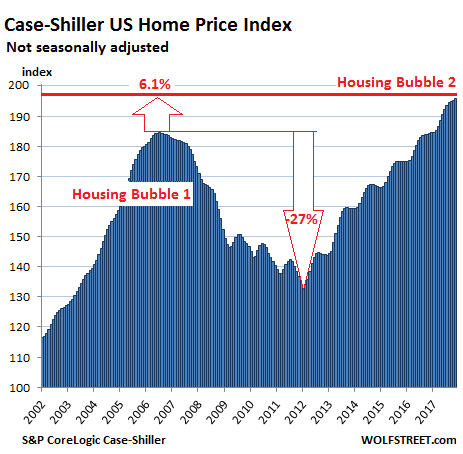

Just after Wolf Richter reported on the minuscule 1.4% year-over-year growth of per-capita “real” disposable income and the lowest saving rate in 12 years —for the lucky ones— there’s another asset-bubble doozie: The S&P CoreLogic Case-Shiller National Home Price Index for November, released this morning, rose 6.2% year-over-year (not-seasonally-adjusted). The index has now surpassed by 6.1% what was afterwards called the crazy peak of Housing Bubble 1 in July 2006 and is up 46% from the bottom of Housing Bust 1:

Real estate prices are a result of local dynamics but are also impacted by national and global factors, including monetary policies and foreign non-resident investors trying to get their money out of harm’s way. This causes local housing bubbles, operating on their own schedules. When enough of them occur simultaneously, it becomes a national housing bubble. See chart above.

The Case-Shiller Index is based on a rolling three-month average; today’s release was for September, October, and November data. Instead of median prices, the index uses “home price sales pairs,” for example for a house that sold in 2010 and then again in 2017. The index provider incorporates other factors and uses algorithms to adjust the price movement into an index data point. The index was set at 100 for January 2000. An index value of 200 means prices as figured by the algorithm have doubled since then.

Here are the most magnificent leaders among the housing bubbles in major metro areas:

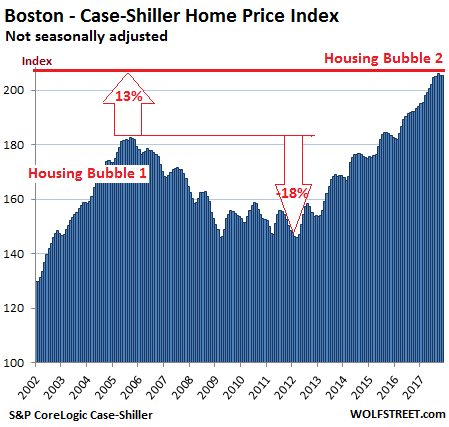

Boston:

The index for the Boston metro area edged down again on a monthly basis, the second decline in a row after 22 months in a row of increases. It has essentially been flat for four months but is still up 6.3% year-over-year. The slight monthly decline could be within the normal seasonal variations but there were no seasonal variations during the relentless surge in 2016 and 2015. During Housing Bubble 1, from January 2000 to October 2005, the index for Boston soared 82% before plunging. The index now exceeds the peak of Housing Bubble 1 by 12.5%:

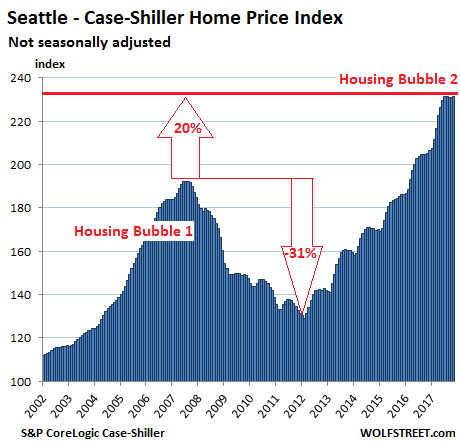

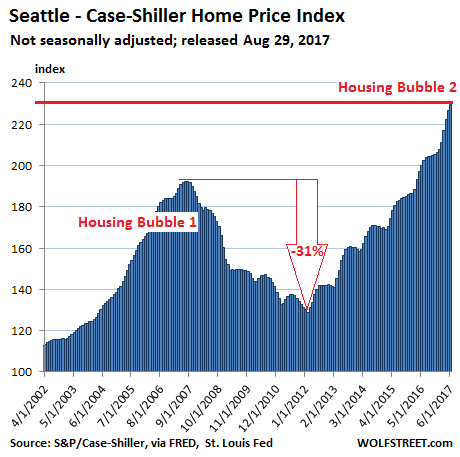

Seattle:

The Case-Shiller home price index for the Seattle metro ticked up a smidgen on a month-to-month basis, after the first two back-to-back declines since the end of 2014! It has now been flat for the past five months. However, flat spots or slight declines in the index this time of the year were not unusual before 2015. The index is up 12.7% year-over-year, 20% from the peak of Housing Bubble 1 (July 2007), and 79% from the bottom of Housing Bust 1 in February 2011:

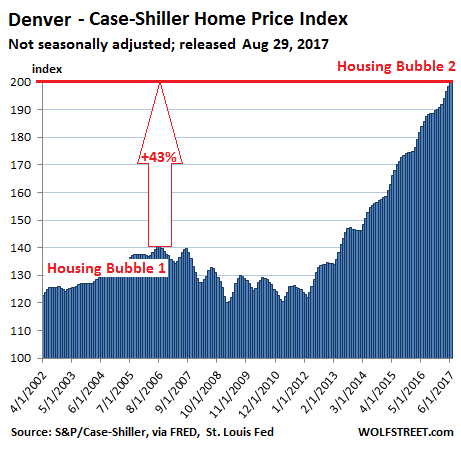

Denver:

The index for the Denver metro ticked up again on a monthly basis, the 25th increase in a row. It is up 7.0% year-over-year and has surged 45% above the prior peak in July 2006. Instead of the craziness of Housing Bubble 1, Denver experienced more “normal” home-price increases, and was therefore also spared the ravages of Housing Bust 1. But in 2012, Housing Bubble 2 erupted in full force:

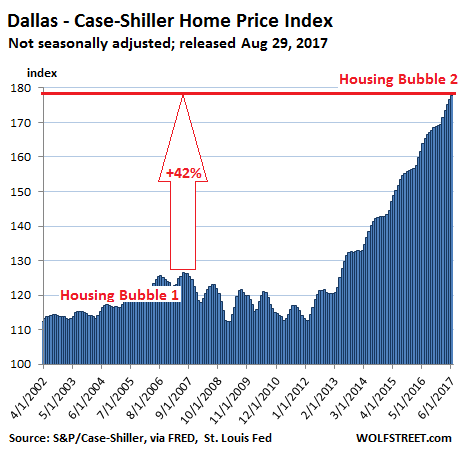

Dallas-Fort Worth:

The index for the Dallas-Fort Worth metro ticked up again on a monthly basis — the 46th month in a row of increases. It is up 7.0% year-over-year and 43% from the prior peak in June 2007. Like Denver, Dallas experienced saner times during Housing Bubble 1. But prices began to surge relentlessly in 2012:

Atlanta:

The home price index for the Atlanta metro has now been flat (actually down a tiny bit) for three months in a row, in line with prior seasonal declines, but is still up 5.2% year-over-year and 2.6% above the peak of Housing Bubble 1 in July 2007. From that peak, the index plunged 37%. It’s now up 70% since February 2012:

Portland:

The Case-Shiller index for Portland was flat in November, and has now been flat or slightly down for five months in a row, and for now still in the range of normal seasonal patterns. The index is up 6.9% year-over-year and has skyrocketed 73% in five years. It’s 20% above the crazy peak of Housing Bubble 1 and has ballooned 123% since 2000:

San Francisco Bay Area:

The index for “San Francisco” covers the county of San Francisco plus four other Bay Area counties — Alameda, Contra Costa, Marin, and San Mateo (the northern part of Silicon Valley). It jumped 1.4% for the month, after jumping 1.2% in the prior month. It’s up 9.1% year-over-year, up 31.3% from the insane peak of Housing Bubble 1, and up 85% from the end of Housing Bust 1. The index has surged 151% since 2000:

Los Angeles:

Home prices in the Los Angeles metro, as tracked by the index, rose 0.7% for the month, and 7.0% year-over-year. LA’s Housing Bubble 1 was in a category of its own in its steepness on both sides, with home prices skyrocketing 174% from January 2000 to July 2006, before collapsing and surrendering much of the gains. The index has skyrocketed since Housing Bust 1 and is now within a smidgen of the prior insane peak:

New York City Condos:

Case-Shiller has a special index for New York City’s condo because this is such a vast market. And this index rose another notch in November and is up 4.4% year-over-year. The index soared 131% from 2000 to February 2006 during Housing Bubble 1, barely deflated during the bust before QE unleashed money from around the world which then re-floated Wall Street more than anything else. The index is 18% above the peak of Condo Bubble 1 and has nearly tripled over the past 17 years:

This is asset-price inflation at work — now that “homes” have become a global asset class. These homes didn’t get 50% bigger or 50% nicer over the past few years. Instead the purchasing power of the dollar with regards to these assets has been purposefully demolished by the Fed’s monetary policies that resulted in practically no wage inflation, moderate consumer price inflation, but massive asset-price inflation. Asset-price inflation without corresponding wage inflation means that the value of labor (wages earned) with regards to homes and other assets has been crushed — a phenomenon now hypocritically called the “affordability crisis” in many big urban areas in the US.

Following yesterday’sdisastrous drop in existing home sales(due to record low supply), new home sales plunged 9.3% MoM after November saw its biggest surge since Jan 1992, revised dramatically lower.

The November 17.5% spike was revised dramatically down to 15.0% spike – the highest since 1993 but December’s 9.3% plunge was already worse than the expected 7.9% giveback…

Biggest MoM drop since Aug 2016.

In fact the downward revisions are huge… October from 624K to 599K; November from 733K to 689K

As good as it gets?

While the blame is immediately laid on weather, the regional drops show that is simply not correct:

Purchases fell in all four U.S. regions, led by a 10 percent drop in the Midwest and a 9.8 percent slide in the South.

Median Home Prices reached a new record high…at $335,400

As Bloomberg notes, new-home sales, tabulated when contracts get signed, account for about 10 percent of the market. They’re considered a timelier barometer than purchases of previously owned homes, which are calculated when contracts close and are reported by the National Association of Realtors.

But the ongoing lack of supply remains the most notable aspect in the US housing ‘recovery’.

Alhambra’s Jeffrey Snider notescritically that it’s what’s going on underneath the headline that really matters (as always). The reluctance of Americans to sell their houses has become such a contradiction to the attempt to paint the housing market, and therefore the overall economic condition, as healthy, even robust. Prices are rising, in some places quickly. Yet, inventory of available-for-sale homes continues to decline, sharply once again in December.

It’s a glaring dichotomy that ever the NAR’s Chief Economist, Larry Yun, has been forcedto grudgingly address.

Existing sales concluded the year on a softer note, but they were guided higher these last 12 months by a multi-year streak of exceptional job growth, which ignited buyer demand. At the same time, market conditions were far from perfect. New listings struggled to keep up with what was sold very quickly, and buying became less affordable in a large swath of the country. These two factors ultimately muted what should have been a stronger sales pace.

It’s the “exceptional job growth” premise that leads toward only confusion. It’s one of those terms, like “globally synchronized growth” or “economic boom”, that refers quite differently to only the mainstream depiction of the economy, the one that has been consistently overoptimistic about things for a decade. The actual data suggests an entirely separate set of circumstances, which is where all this misunderstanding comes in.

In truth, falling inventory is quite easily explained, and in a way that is perfectly consistent with labor market and national (labor) income statistics as they are. The BLS outside of the unemployment rate, which, for the nth time doesn’t include Americans who would work if there was work, actually has been describing a consistently and persistently slowing labor market. The timing of where that started matches with where resale inventory began to contract.

There is actually a big difference between an average payroll gain of 150k and 250k; the latter is barely minimal, while the former is what panicked the Fed into launching QE3 in 2012. Last year was by every reasonable measure not even close to a good one for American workers.

The primary effect of sluggish, constrained payroll expansion, along with parallel effects in other labor factors, is weakened aggregate income. Even people who are working start to become uncertain or even fearful when the jobs market as a whole slows down – and not just slows, but continues to decelerate year after year (after year). This trend will be starting its fourth year. At that length, workers and prospective workers become quite certain about their general uncertainty.

If your ground-level view of the jobs environment and therefore economy is far more unsteady and dour than exceptional, you are not going to be as sure about selling your existing home to move up, taking on a larger monthly payment in the process. The more people like you who pass on the opportunity to cash in on higher prices, the more that says this is a widespread view quite different from the narrative established in consumer sentiment surveys and what news outlets write about in their headlines.

The economy is what actually happens, not what people think other people think Economists say is happening. Talk isn’t cheap, it’s wayovervalued.

A little over a year ago, home prices finally surpassed their prior all-time highs, reached during the heyday of the housing bubble back in 2006.

But with home prices in 80% of US cities are growing twice as fast as wages, working-class families across the US are finding it increasingly difficult to support their families – let alone afford a home. But fortunately, this hasn’t been a problem for institutional investors like Blackstone, which are presently enjoying the luxury of a controversial valuation assessment known as a Broker Price Opinion – or BPO.

As the Wall Street Journalexplains, Congress prohibited the use of BPOs to underpin traditional mortgages as part of Dodd-Frank. But, fortunately for private-equity firms and their limited partners, that prohibition doesn’t apply to investors buying tens of thousands of homes.

Blackstone and its lender, Deutsche Bank AG, settled on a sort of drive-by valuation done by real-estate agents that are more cursory and cost far less than traditional appraisals.

Congress outlawed the use of such assessments, called broker price opinions, or BPOs, to value properties for traditional mortgages. But the prohibition, enacted as part of postcrash financial regulation, doesn’t apply to investors buying tens of thousands of houses.

Now these perfunctory valuations abound, underpinning tens of billions of dollars of home deals. Sometimes the process is outsourced to India, where companies charge real-estate agents a few dollars to come up with U.S. home values by consulting Google Earth and real-estate websites.

That’s right: Shoddy satellite photos and workers at call centers in India – thousands of miles away from the homes they’re evaluating – are making up prices for homes that are then used to value collateral used in bond offerings. In fact, BPOs have been used to value collateral in the more than $20 billion of bonds sold by institutional landlord. They’re also thefast-growing business of lending to individual house flippers. Banks request them when considering whether to foreclose or negotiate repayment plans with delinquent homeowners.

Their popularity shows how Wall Street is finding ways to adapt to government efforts to crack down on some of the excesses that contributed to the housing crisis. Whileauthorities in Canada and Australiahave passed laws to curb speculation in their respective housing markets, US regulators have been unwilling to challenge BPOs – though the SEC is investigating whether certain rental-home companies used these shoddy valuations to distort the value of bonds tied to the deal. Critics say BPOs are ill-suited to gauge home values and could leave debt holders with less collateral than they thought.

So what are the risks, exactly? Well, inaccurate pricing information could result in abrupt and unexpected losses for investors when a more thorough appraisal is sought.

“BPOs are a creature of financial institutions that want deals to close fast, and so they don’t have to use an appraiser,” said Donald Epley, a retired University of South Alabama professor who helped write national appraisal standards after the 1980s savings-and-loan collapse. “You’re just dumbing down the standards to make the loan.”

Some credit rating firms have realized that these valuations aren’t reliable, and have stopped accepting them, or sought a second opinion.

When Fannie Mae last year guaranteed about $1 billion of Invitation Homes debt, it accepted BPOs for the 7,204 houses serving as collateral. Assuming a typical appraisal price of $450 and the $95 that Invitation Homes pays per BPO, the company saved about $2.6 million.

Credit-rating firms usually discount BPO values when grading rent-backed bonds. Kroll Bond Rating Agency has trimmed them by about 10% and uses the lower of the reduced BPOs and the amounts spent buying and renovating the homes.

“We’re never taking BPOs at face value,” said Kroll’s Daniel Tegen.

With many institutional investors expect, as Goldman Sachs put it, “a strong and synchronous global expansion” during the coming year, housing bears are difficult to come by. But Bloomberg managed to find one: James Stack, an investor who manages $1.3 billion for high net worth individuals, says that his “Housing Bubble Bellwether Barometer” is flashing red again. Stack predicted the housing crash back in 2005, just as home prices were reaching their peak.

His assessment of the market should send a chill down the spine of foreign investors who have poured money into New York City, San Francisco and other hot urban housing markets that have led the recovery in home valuations.

“It is 2005 all over again in terms of the valuation extreme, the psychological excess and the denial,” said Stack, whose fireproof files of newspaper articles on bear markets date back to 1929. “People don’t believe housing is in a bubble and don’t want to hear talk about prices being a little bit bubblish.”

Despite the torrid rally in home prices, Stack is one of the few real-estate market observers who foresee a sizable correction in prices. Indeed, as the vital spring selling season approaches, there are plenty of reasons for buyers to be optimistic – not the least of which is the “wealth effect” stemming from gains in equity prices. A backup in home building following the recession has left a paucity of inventory just as the housing needs of two generations – millennials who are buying their first homes and Baby Boomers who are downsizing in retirement – are shifting.

But there’s a structural mismatch between different tiers of the housing market that are poised to create problems for home builders.

There are plenty of reasons to be optimistic. The housing needs of two massive generations – millennials aging into home ownership and baby boomers getting ready for retirement – are expected to fuel demand for years to come if employment remains strong. Sales in master-planned communities, many of which target buyers who are at least 55, reached a record last year, according to John Burns Real Estate Consulting. Last month, a gauge of confidence from the National Association of Home Builders/Wells Fargo rose to the highest level in 18 years, and starts of single-family homes in November were the strongest in a decade.

“As soon as homes are finished, they’re flying off the shelf,” said Matthew Pointon, Capital Economics Ltd.’s U.S. property economist.

Home builders, which have focused on pricier homes since the market bottomed in 2012, are now getting ready for a wave of first-time buyers left with little to choose from on the existing-home market. Investors are rushing to builders of starter homes, because lower-priced homes in the U.S. are in the shortest supply. Shares of LGI Homes Inc., which targets renters with ads that trumpet monthly payments instead of prices, rose 161 percent last year. D.R. Horton Inc., the biggest builder, powered by its fast-selling Express entry-level brand, gained 87 percent.

Home builder stocks rallied 75% last year, outpacing the S&P 500’s best performance since the once-in-a-generation return in 2013. That gain made home builders one of the best-performing subsets of the market.

While demand for low-income homes remains robust, home builders have so far been fixated on housing stock for high-income earners – particularly in hot markets like San Francisco, New York City and Washington DC. Meanwhile, the SEC requested information in May from Radian Group about the BPO’s it provided for rent-backed bonds.

Of course, its premature to say that this will have any kind of tangible impact on the market. But it should certainly make investors think twice about valuations.

This is how monetary policies have crushed the value of labor.

For the good folks who hope fervently that the Fed doesn’t have reasons to raise rates or unwind QE because there isn’t enough inflation, here is an update on one aspect of inflation – asset price inflation, and particularly house price inflation – where the value of your hard-earned dollars has collapsed over a given number of years to where it takes a whole lot more dollars to pay for the same house.

So here are some visuals of amazing house price bubbles, city by city. Bubbles really aren’t hard to recognize, if you want to recognize them. What’s hard to predict accurately is when they will burst. Normally the Fed doesn’t want to acknowledge them. But now it has its eyes focused on them.

The S&P CoreLogic Case-Shiller National Home Price Index for June was released today. It jumped 5.8% year-over-year, not seasonally adjusted, once again outpacing growth in household incomes, as it has done for years. At 192.6, the index has surpassed by 5% the peak in May 2006 of crazy Housing Bubble 1, which everyone called “housing bubble” after it imploded (data viaFRED, St. Louis Fed):

The Case-Shiller Index is based on a rolling-three month average; today’s release was for April, May, and June data. Instead of median prices, it uses “home price sales pairs,” for example, a house sold in 2011 and then again in 2017. Algorithms adjust this price movement and add other factors. The index was set at 100 for January 2000. An index value of 200 means prices have doubled in the past 17 years, which is what most of the metros in this series have accomplished, or are close to accomplishing.

Real estate is local. Therefore real estate bubbles are local. If enough local bubbles balloon at the same time, it becomes a national housing bubble. As the above chart shows, the US national Housing Bubble 2 now exceeds the crazy levels of Housing Bubble 1, and in all ten major metro areas, home prices are setting new records.

In the Boston metro, the home price index is now 11% above the peak of Housing Bubble 1 (Nov 2005):

Home prices in the Seattle metro have spiked over the past year, pushing the index 20% above the peak of Housing Bubble 1 (Jul 2007):

Then there’s Denver’s very special house price bubble. The index has soared a stunning 43% above the peak of Housing Bubble 1 (Aug 2006):

People in the Dallas-Fort Worth metro felt left out during Housing Bubble 1, when prices rose only 13% in five years, while folks in other parts of the country were getting rich just sitting there. They also skipped much of the house price crash. But they know how to party when time comes. The index has now surged by 42% from the peak in June 2007:

The Atlanta metro, where home prices had plunged 36% after Housing Bubble 1, has now finally squeaked past the prior peak by 2%, with a near-perfect V-shaped bubble recovery:

Portland’s home prices have kicked butt since 2012, with the index soaring 71% in five years – not that homes were cheap in Portland in 2012. Portland’s house price bubble is now 20% above the peak of Housing Bubble 1:

The San Francisco Case-Shiller Index, which covers the five-county Bay Area and not just San Francisco, is now 10% above the insane peak of Housing Bubble 1. During the last housing crash, the index plunged 43%. Eight years of global monetary craziness has sent liquidity from around the world sloshing knee-deep through the streets, which has performed miracles:

Los Angeles home prices performed similar feat, doubling from 2002 to July 2006, before giving up two-thirds of those gains, then soaring once again. The index is now 3% above the peak of totally insane Housing Bubble 1:

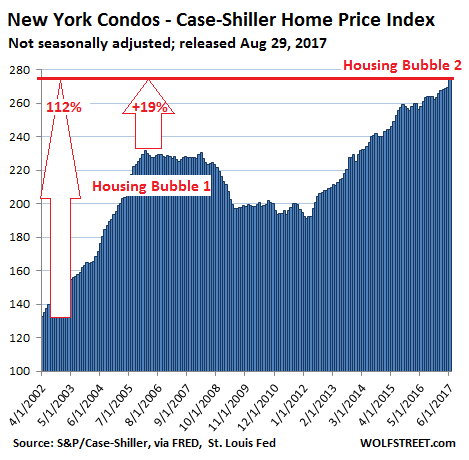

New York City condo bubble never saw the crash in its full bloom. Prices are now 19% above the peak of the prior bubble (Feb. 2006). Over the past 15 years, the index has soared 112%:

While the monetary policies of the past eight years have had no impact on wage inflation in the US, and only moderate impact on consumer price inflation, they’ve been a rip-roaring success in creating asset price inflation.

Asset price inflation means that the dollar loses its value when it comes to buying assets. Wage earners, when they’re trying to buy assets today – not just homes but any type of asset, including buying into retirement plans – are finding out that their labor is buying only a fraction of the assets that their labor could buy eight years ago. This is how these monetary policies have crushed the value of labor.

A really long, long time ago, well before most of today’s wall street analysts made it through puberty, the entire international financial system almost collapsed courtesy of a mortgage lending bubble that allowed anyone with a pulse to finance over 100% of a home’s purchase price…with pretty much no questions asked.

And while the millennial titans of high finance today may consider a decade-old case study on mortgage finance to be about as useful as a Mark Twain novel when it comes to underwriting mortgage risk, they may want to considered at least taking a look at the ancient finance scrolls from 2009 before gleefully repeating the sins of their forefathers.

Alas, it may be too late. AsBlack Knight Financial Servicespoints out, down payments, the very thing that is supposed to deter rampant housing speculation by forcing buyers to have ‘skin in the game’, are once again disappearing from the mortgage market. In fact, just in the last 12 months, 1.5 million borrowers have purchased a home with less than 10% down, a 7-year high.

– Over the past 12 months, 1.5M borrowers have purchased a home by putting down less than 10 percent, which is close to a seven-year high in low down payment purchase volumes

– The increase is primarily a function of the overall growth in purchase lending, but, after nearly four consecutive years of declines, low down payment loans have ticked upwards in market share over the past 18 months

– Looking back historically, we see that half of all low down payment lending (less than 10 percent down) in 2005-2006 involved piggyback second liens rather than a single high LTV first lien mortgage

– The low down payment market share actually rose through 2010 as the GSEs and portfolio lenders pulled back, the PLS market dried up, and FHA lending buoyed the purchase market as a whole

– The FHA/VA share of purchase lending rose from less than 10 percent during 2005-2006 to nearly 50 percent in 2010

– As the market normalized and other lenders returned, the share of low-down payment lending declined consistent with a drop in the FHA/VA share of the purchase market

On the bright side, at least Yellen’s interest rate bubble means that today’s housing speculators don’t even have to rely on introductory teaser rates to finance their McMansions...Yellen just artificially set the 30-year fixed rate at the 2007 ARM teaser rate…it’s just much easier this way.

“The increase is primarily a function of the overall growth in purchase lending, but, after nearly four consecutive years of declines, low down payment loans have ticked upward in market share over the past 18 months as well,” said Ben Graboske, executive vice president at Black Knight Data & Analytics, in a recent note. “In fact, they now account for nearly 40 percent of all purchase lending.”

At that time half of all low down payment loans being made involved second loans, commonly known as “piggyback loans,” but today’s mortgages are largely single, first liens, Graboske noted.

The loans of the past were also far riskier – mostly adjustable-rate mortgages, which, according to the Black Knight report, are virtually nonexistent among low down payment mortgages today. Instead, most are fixed rate. Credit scores of borrowers taking out these loans today are also about 50 points higher than those between 2004 and 2007.

Finally, on another bright note, tax payers are just taking all the risk upfront this time around…no sense letting the banks take the risk while pretending that taxpayers aren’t on the hook for their poor decisions…again, it’s just easier this way.

The pending home sales index, an estimate of existing home sales, has accurately provided the direction of the monthly home resale reports.

The survey is down for the second month, providing further evidence of a housing slowdown.

TheEconodayconsensus estimate was for the index to rise 0.5%. Instead, the pending home sales index declined 1.3%.

“Spring sales data have not been favorable for the housing sector. Pending home sales are down for a second straight month, 1.3 percent lower in April to an index of 109.8 which is 3.3 percent below this time last year. This index tracks contract signings for resales and the results point to weakness for final sales in May and June. Final resales contracted in April as did new home sales while the month’s housing starts were also weak. Spring is the big season for housing and these are not the results of a sector that will be leading the 2017 economy.”

Pending home sales had been expected to rise slightly in April after declining 0.8 percent in March. Instead, the National Association of Realtors’® (NAR’s) Pending Home Sale Index (PHSI) slumped for the second straight month, dropping 1.3 percent. The PHSI, based on contracts signed for existing home purchases, fell from 111.3 (revised from 111.4) in March to 109.8.

The April dip put the Index 3.3 percent below its level in April 2016. This was the first year-over-year decline since last December and the largest since the Index fell 7.1 percent in June 2014.

Lawrence Yun, NAR chief economist, said the fading contract activity in the normally active spring market is due to significantly weak supply levels. These, in turn, are spurring deteriorating affordability conditions. “Much of the country for the second straight month saw a pullback in pending sales as the rate of new listings continues to lag the quicker pace of homes coming off the market,” he said. “Realtors are indicating that foot traffic is higher than a year ago, but it’s obviously not translating to more sales.”

Yun added, “Prospective buyers are feeling the double whammy this spring of inventory that’s down 9.0 percent from a year ago and price appreciation that’s much faster than any rise they’ve likely seen in their income.”

The economist sees little evidence that the record low levels of inventory will improve anytime soon. Homebuilding activity remains below the necessary levels and too few homeowners are listing their home for sale.

“The unloading of single-family homes purchased by real estate investors during the downturn for rental purposes would also go a long way in helping relieve these inventory shortages,” said Yun. “To date, there are no indications investors are ready to sell. However, they should be mindful of the fact that rental demand will soften as the overall population of young adults starts to shrink in roughly five years.”

NAR expects that existing home sales will increase about 3.5 percent from 2016 to 5.64 million units and the national median existing-home price is expected to increase around 5 percent. In 2016, existing sales increased 3.8 percent and prices rose 5.1 percent.

The decline of sales was nearly nationwide in scope and all four regions are now running lower index numbers than the previous April. The West was the only region enjoying a month-over-main gain. The PHSI in the Northeast decreased 1.7 percent to an index of 97.2, now 0.6 percent lower than the previous April. In the Midwest, the index fell 4.7 percent to 104.4, a decline of 6.1 percent year-over-year.

Supply Issue?

In addition to the decline this month, the Pending Home Sales Index for March was revised lower, from -0.8 % to -0.9 %. The second quarter recovery thesis is dying on the vine.

Once again Yun blames supply. And once again Yun is wrong. If supply was triple and prices remained the same, sales would not be skyrocketing.

Of course, if supply tripled and sales did not soar, prices would drop. That is the real issue. Prices are above what buyers can afford to pay.

Although the number of resales is well below the bubble years, the median price isn’t.

Median Home Prices 1963-Present:

More Trapped Home Buyers:

New home sales are recorded at signing. Existing home sales are recorded at closing.

Thus, the March report has negative implications for April and May, while the April report has negative implications for resales in May and June.

Looking ahead, existing home buyers in the last two to three years overpaid. In some areas, notably California, home buyers overpaid dramatically.

Another round of trapped home buyers unable to sell their homes is right around the corner.

Two days agowe looked at the latest troubling developmentin US home price trends: a new bubble appears to be emerging in all the “usual suspect” places. As we noted on Thursday, “home prices in markets that bubbled over back in 2006/2007, like Las Vegas and San Francisco, got cut in half in 2009 but have since doubled again of their lows. Meanwhile, markets like Denver and Dallas that didn’t participate as much in the 2007 mania are now surging to all-time highs, with Dallas prices up 55% over the past 5 years.”

TheWall Street Journal addedthat some of the home buying behaviors of consumers, like paying prices well above appraisal values and waiving home inspections, are starting to be eerily reminiscent of 2006:

In some markets, bidding wars are breaking out. Agents said some buyers are kicking in extra cash when properties don’t appraise for the asking price, and some are waiving their right to home inspections.

“It can’t be sustained,” said David Berson, chief economist at Nationwide Insurance and a former chief economist at mortgage giant Fannie Mae, referring to the frenzied buying. “It can’t go on forever.”

Other signs of overexuberance have emerged, including surging levels of licensed Realtors all chasing a quick buck.

The number of licensed Realtors has jumped by nearly 25% since 2012, hitting a nine-year high in 2016 and sitting just 9% below the peak in 2006, according to real-estate consultant John Burns. In Denver, homes are selling briskly. The median number of days that homes spent on the market declined to eight in the first three months of the year from 61 in 2012, according to Redfin. Home prices rose 8.5% in Denver over the year ended in February, according to Case-Shiller.

Nicki Thompson, an agent in Denver, said she recently had a listing that was on the market for two weekends at $1.2 million and she received multiple all-cash offers above the listing price.

“It’s just crazy,” she said.

And for a practical example of just how crazy it truly is,take this renovated 2-bedroom, 1,948 sq. ft house first built in 1951 in the Eagle Rock section of Los Angeles, which was listed in mid-March for $699,000, was estimated by Redfin at $780,000, andsold yesterday for $980,888(more than $500/sq foot) and 40% above asking, just over a month after it was first listed.

In the 1960s-80s drums played on some of the most famous pop songs known (Good Vibrations, Mrs. Robinson, A Little Less Conversation, to name a few) were built in this garage in our beloved Eagle Rock. A. F. Blaemire and his wife, Kirsten, filled this home with music and creativity for decades, and now it’s ready for its next inspired owner! With freshly refinished hardwood floors and repainted interior, 5208 Monte Bonito is a blank canvas with great potential. The rooms are bright and spacious, including a downstairs recreation room perfect for a jam room, art studio, den (or all of the above!). The two-car garage has direct access to the house and an additional storage room. The back yard has plenty of space for entertaining and gardening – there is already an avocado tree, an orange tree, and a pitaya to get you started! Views of the Eagle Rock from the master bedroom, and sunset views from the front porch make this the ideal setting to call home.

Then again, maybe not.

So what do you get for just under a million in LA these days? Not much: two bedrooms, less than two bathrooms, a 2 car garage, a decorative fireplace, a rec room, and a 7,195 sq foot lot.

Here are some photos showing what a “million dollar house” looks like in the latest US housing bubble.

A recent poll found that two-thirds of metropolitan Vancouver residents believe “foreigners investing” is a main cause of high housing costs, and 70 per cent said the government should work to improve affordability.

One month ago, when describing the latest in an endless series of Vancouver real estate horror stories, in this case an abandoned, rotting home (which is currently listed for a modest$7.2 million), we explained the simple money-laundering dynamic involving Chinese “investors” as follows.

Chinese investors smuggle out millions in embezzled cash, hot money or perfectly legal funds, bypassing the $50,000/year limit in legal capital outflows.

They make “all cash” purchases, usually sight unseen, using third parties intermediaries to preserve their anonymity, or directly in person, in cities like Vancouver, New York, London or San Francisco.

The house becomes a new “Swiss bank account”, providing the promise of an anonymous store of value and retaining the cash equivalent value of the original capital outflow.

We also explained that hundreds if not thousands of Vancouver houses, have become a part of the new normal Swiss bank account: “a store of wealth to Chinese investors eager to park “hot money” outside of their native country, and bidding up any Canadian real estate they could get their hands on.”

This realization has now fully filtered down to the local population, and as the National Post writes in its latest troubling look at the “dark side” of Vancouver’s real estate market, it cites wholesaler Amanda who says that “Vancouver seems to be evolving from a residential city into almost like a lock box for money… but I have to live among the empty houses. I’m a resident, not just an investor.”

The Post article, however, is not about the use of Vancouver (or NYC, or SF, or London) real estate as the end target of China’s hot money outflows – by now most are aware what’s going on. It focuses, instead, on those who make the wholesale selling of Vancouver real estate to Chinese tycoons who are bidding up real estate in this western Canadian city to a point where virtually no domestic buyer can afford it, and specifically the job that unlicensed “wholesalers” do in spurring and accelerating what is currently the world’s biggest housing bubble.

A bubble which, the wholesalers themselves admit, will inevitably crash in spectacular fashion.

Vancouver’s real estate market has been very good to Amanda. She’s not a licensed realtor, but buying and selling property is her full-time job.

She started about eight years ago as an unlicensed “wholesaler” in Vancouver.

She would approach homeowners and make unsolicited offers for private cash deals. Amanda made a 10-per-cent fee on each purchase by immediately assigning the contract to a background investor. It is seen as the lowest job in property investment, but it is low risk and very profitable. Amanda has done so well that she now owns two homes in Vancouver and develops property in the U.S.

Unlicensed wholesaling is an illicit and predatory business that is quickly growing in Metro Vancouver because enforcement is virtually non-existent.

It’s similar to a tactic currently being examined by B.C. real estate authorities known as “assignment flipping,” which involves legally but secretly trading homes on paper to enrich realtors and circles of investors.

However, unlicensed wholesaling is completely unregulated. Amanda estimates hundreds of wholesalers are scouring Metro Vancouver’s never-hotter speculative market — not including the realtors who are secretly wholesaling for themselves.

Amanda decided to step away from the easy money for moral reasons.

She’s most concerned that wholesalers are targeting B.C.’s vulnerable seniors who don’t understand the value of their old homes. She is also worried about offshore money being laundered, and the resulting vacant homes.

Because wholesalers are unlicensed, they have no obligation to identify their background investors or reveal the source of funds to Canadian authorities who fight money laundering.

“Vancouver seems to be evolving from a residential city into almost like a lock box for money,” Amanda said. “But I have to live among the empty houses. I’m a resident, not just an investor.”

Amanda said she believes that unethical and ignorant investors are driving B.C.’s housing market at full speed towards a crash. For these reasons, and with the condition that we not use her real name, she came forward to reveal how wholesalers operate.

The calling cards of wholesalers — hand-written flyers offering homeowners “confidential” and “discreet” cash sales — started flooding west side Vancouver homes over the past 18 months. With the dramatic surge in home prices, wholesalers now are spreading into neighborhoods across Metro Vancouver and Vancouver Island.