https://www.thedailydoom.com/p/the-deeper-dive-where-are-we

Summery article about the following podcast from December 5th, 2023 that describes everything leading up to today’s frozen real estate market and probable circumstances that will break the ice wall during 2024 and 2025.

Tag Archives: housing market

The Move In Mortgage Rates From 7% To 11% Will Be More Painful Than The Move From 3% To 7%.

National Average U.S. Homeowner Equity Drops For First Time Since 2012

The housing bull market has peaked for now. Recent home price declines are leading to decreased tappable equity for homeowners.

Foreclosures JUMP as Lending Tightens to New All Time RECORD

The 2023 housing market continues its correction, with home prices now falling month over month and year over year according to the National Association of Realtors. On top of that foreclosure starts increased 20% month over month and 22% year over year, and more importantly the speed of the foreclosure process through completion increased 12% quarter over quarter. Additionally JP Morgan sent out a note informing us that lending conditions have now tightened faster than they did during the great financial crisis, with the full effects not being felt until late 2023 or early 2024.

US January YoY Home Sales Down Record 37%, Median Price Up 1.5%, Lowest Since 2012

Existing home sales had fallen for a record 11 straight months ahead of this morning’s print for January, which consensus expected to reveal a 2% MoM rebound. However, existing home sales for January actually tumbled 0.7% MoM (well below the 2.0% jump expected) and the record 12th straight monthly decline with December’s 1.5% decline actually revised even worse to -2.2% MoM…

San Francisco Bay Area Housing Market Crashes, Prices Plunge 35% from Crazy Peak: Where’s Demand Supposed to Come From?

In the first 10 months of Housing Bust 2 (now), the median price plunged a lot faster than in the first 10 months of Housing Bust 1 (2007-11).

About 1 In 12 Mortgaged Homes Purchased in 2022 Have Already Slipped Underwater

A clear bifurcation of risk emerged between mortgaged homes purchased relatively recently versus those bought early in or prior to the pandemic: Black Knight

(Connie Kim) Home price corrections exposed a growing pocket of equity risk concentrated among purchase mortgages originated in 2022, Black Knight said in its latest mortgage monitor report. Of all homes purchased with a mortgage in 2022, 8% are now at least marginally underwater.

Of the 450,000 underwater borrowers at the end of the third quarter, nearly 60% of the mortgages originated in the first nine months of 2022, according to Black Knight. In total, 5% of all mortgages originated so far this year are now marginally underwater, with another 20% in low equity positions.

72% Of Millennials Have Regrets About Homes They Overpaid Or Settled For In 2021 And 2022

As new inventory is finally starting to hit the market and demand has temporarily slowed down thanks to rising rates, the housing expansion between March 2020 and now is still very likely to go down in history as blowing unprecedented amounts of air into an unprecedented bubble.

And now we have the data to show it. Continue reading

Blackstone Prepares A Record $50 Billion To Snap Up Real Estate During The Coming Crash

The past two months have seen a barrage of negative news coverage focusing on the US housing market…

3rd Look at Local Housing Markets in June, Sales Down Sharply, Inventory “Surged”

Today, in the Calculated Risk Real Estate Newsletter: 3rd Look at Local Housing Markets in June, Sales Down Sharply, Inventory “Surged”

A brief excerpt: Continue reading

Sharp Decline in Pending Sales, Inventory Surges In California

“Real Estate Tech” in Existential Crisis

“Real Estate Tech” in Existential Crisis as Housing Sours, Stocks Plunge, New Money Out of Reach: Redfin & Compass Try to Survive by Cutting Staff. Opendoor, Zillow Sag

In short, the party ran out of bamboozle.

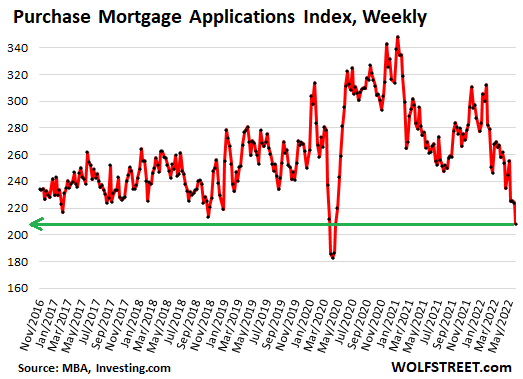

Housing Bubble Getting Ready to Pop: Mortgage Applications to Purchase a Home Drop to Lockdown Lows, “Bad Time to Buy” Hits Record amid Sky-High Prices, Spiking Mortgage Rates

(Wolf Richter) This just keeps getting worse: Applications for mortgages to purchase a home dropped 7% for the week, and were down 21% from a year ago, the Mortgage Bankers Association reported today. An indicator of future home sales: Potential homebuyers try to get pre-approved for a mortgage, lock in a mortgage rate, and then start house-hunting.

Mortgage rates have soared this year, and home prices have soared for years to ridiculous levels, causing layers and layers of potential buyers to abandon the market, amid “worsening affordability challenges,” as the MBA called it. And these applications to purchase a home hit the lowest point since the depth of the lockdown in April 2020 (data via Investing.com):

The MBA’s Purchase Mortgage Applications Index has now dropped below the lows of late 2018. By November 2018, the Fed had been hiking rates for years (slowly), and its QT was in full swing, and mortgage rates had edged above 5%, which was enough to begin shaking up the housing market. Home sales volume slowed, prices began to come down in some markets, and stocks were selling off. But with inflation below the Fed’s target, and with Trump, who’d taken ownership of the Dow, constantly throwing darts at Powell, the Fed signaled in December 2018 that it would cave, and instantly mortgage rates began to fall, and volume and prices took off again.

Today, raging inflation is the #1 economic issue, and the Fed is chasing after it, with backing from the White House, and so this issue in the housing market is just going to have to play out.

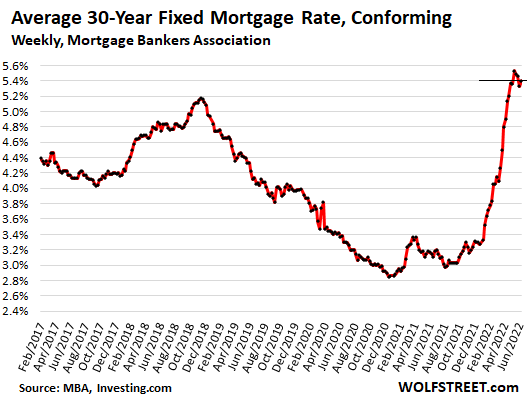

Holy-Moly Mortgage Rates.

The average 30-year fixed mortgage rate with conforming balances and 20% down rose to 5.40% this week, according to the MBA today, having been in this 5.4% range, plus or minus a little, since the end of April, the highest since 2009.

I call them holy-moly mortgage rates because that’s the reaction you get when you apply this rate to figure a mortgage payment for a home at current prices and then accidentally look at the resulting mortgage payment (data via Investing.com):

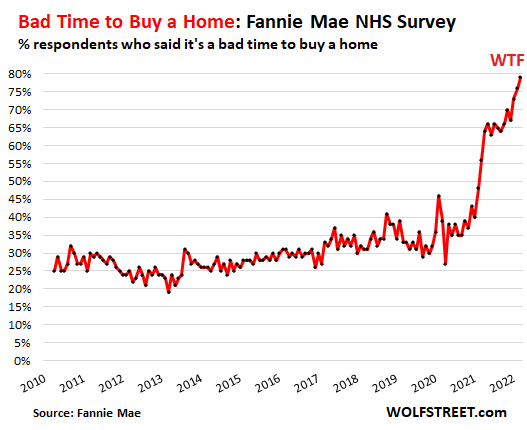

“Bad time to buy a home.”

Turns out, sky-high home prices to be financed with holy-moly mortgage rates, plus uncertainty about the economy, dropping stock prices, and inflation eating everyone’s lunch make a toxic mix for homebuyers.

The percentage of people who said that now is a “bad time to buy” a home jumped to 79%, another record-worst in the data going back to 2010, according to Fannie Mae’s National Housing Survey for May. Sentiment has been deteriorating since February 2021:

“Consumers’ expectations that their personal financial situations will worsen over the next year reached an all-time high in the May survey, and they expressed greater concern about job security,” according to Fannie Mae’s report.

“These results suggest to us that increased mortgage rates, high home prices, and inflation will likely continue to squeeze would-be home buyers – as well as those potential sellers with lower, locked-in mortgage rates – out of the market, supporting our forecast that home sales will slow meaningfully through the rest of this year and into next,” said Fannie Mae.

Sagging stock prices keep getting blamed.

The stock market is on the front pages every day. Only a small percentage of Americans own any significant amount of equities, but that doesn’t matter. Stock market declines, with many high-flying stocks plunging 70% or 80% or even 90% since February 2021, have rattled a lot of nerves. Which is in part why Fannie Mae pointed out, “consumers’ expectations that their personal financial situations will worsen over the next year reached an all-time high.”

The MBA also had previously pointed at the financial markets as one of the reasons for the plunge in purchase mortgage applications.

In the tech and social media sector, the big declines in stock prices have now triggered the first hiring freezes and a few layoffs. And this too – just the idea of nirvana being somehow over – is shaking up some folks.

Sharp increases in stock portfolios, stock options from employers, or cryptos empowered potential homebuyers and enabled many to borrow against their portfolios to come up with down payments. This option has either vanished or is looking very shaky for many.

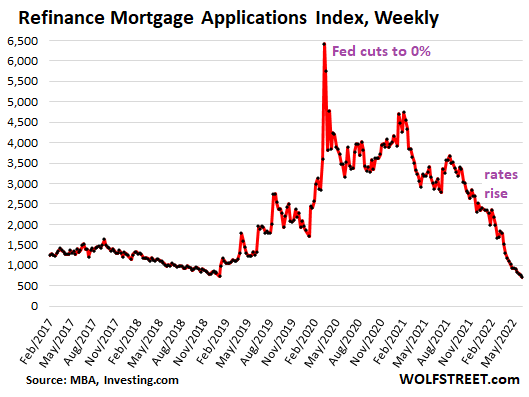

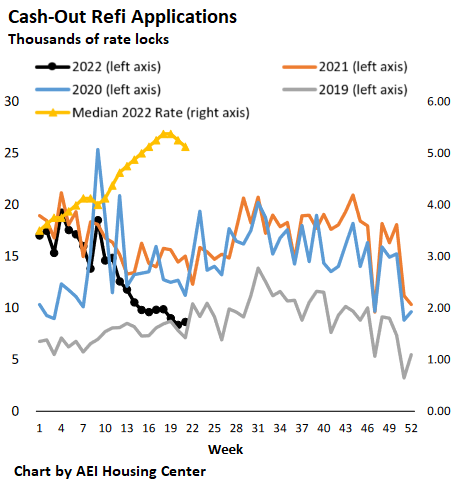

Refi applications collapsed to lowest since year 2000.

Applications for mortgages to refinance an existing mortgage dropped another 6% for the week, and have collapsed by 75% from a year ago, to the lowest level since the year 2000, according to the MBA’s Refinance Mortgage Applications Index. The MBA obtains this data from a weekly survey of mortgage bankers.

With these holy-moly mortgage rates, just about the only reason to refinance is to extract cash from the home via a cash-out refi (data via Investing.com):

Cash-Out Refi mortgage applications.

According to the AEI Housing Center, which tracks mortgage applications by the number of rate locks, no-cash-out refi applications have collapsed by 92% from a year ago. But cash-out refi applications are primarily driven by the desire to extract cash from a home, with mortgage rates being a secondary issue – and so they continue but a slower pace.

Cash out refi applications in week through May 30 (black line) plunged by 42% from the same week in 2021 and have stabilized roughly level with 2019:

A cash-out refi provides a big lump sum for the homeowner to spend on all kinds of things, from cars to home improvement projects. They are also used to pay off high-cost debts, such as credit cards so that these credit cards can then be used for more purchases. The plunge in cash-out refi reduces the availability of these lump-sums, and therefore reduces the stimulus to the economy they provide.

No-cash-out refi mortgages at lower mortgage rates also boost consumer spending, as the lower rates reduce payments that then leave some extra every month to spend on other stuff. But the spike in mortgage rates, and the subsequent 92% collapse of no-cash-out refi mortgage applications ends this program.

Source: by Wolf Richter | Wolf Street

***

George Gammon: Thinking of buying a house? Stop and watch this first – MS

US housing implosion about to start – Market Sanity

Bank of America declares ‘technical recession’ – NTD

Inflation, consumer woe add to worries that recession is already here – CNBC

“Warning flags are everywhere” – ECB, inflation and U.S. stocks – QTR

Bond market rout so severe double-digit losses are the norm – Yahoo!

Get ready for currency collapses – King World News

Housing Market: Could This Be Worse Than 2008?

“Conditions are changing really fast”

Nick Gerli, in his interview with Wealthion, alludes to a number of figures which spell trouble for the residential market. If you own real estate or we’re considering entering the market soon, it’s worth checking out:

“Major Turning Point” – US Housing Inventory Rises For First Time Since 2019

“Sellers are fueling this turnaround in inventory, with newly listed homes entering the market at a rate not seen since 2019.”

Are Real Estate Prices About To Crash?

No however, difficult is the way, narrow is the gate and in service to each other we will remain free.

Is Housing a Bubble That’s About to Crash?

(Charles Hugh Smith) We are all prone to believing the recent past is a reliable guide to the future. But in times of dynamic reversals, the past is an anchor thwarting our progress, not a forecast.

Are we heading into another real estate bubble / crash? Those who say “no” see the housing shortage as real, while those who say “yes” see the demand as a reflection of the Federal Reserve’s artificial goosing of the housing market via its unprecedented purchases of mortgage-backed securities and “easy money” financial conditions.

Cracks Appear In Housing Market As Sellers Begin To Lower Asking Prices

Over the last several weeks, readers have become aware of an emerging housing affordability crisis as US mortgage rates continued their near-vertical ascent, risks jeopardizing the housing market boom. The 30 Year fixed mortgage rate has jumped a staggering 177bps this year, reaching the highest since 1Q10, with Bankrate data showing mortgage rates are above 5%.

Rate Hikes Jeopardize Much More Than Just American Home Ownership

(J.G. Collins) Someone once said that you never actually “buy” a home. Instead, you merely commit to paying an annuity: the mortgage.

That’s largely true. The price and “value” of homes for the overwhelming majority of homeowners is a function of home buyers’ ability to make payments.

And with the Federal Reserve signaling further interest rate hikes, home buyers and sellers—and assorted others who use credit—will incur knock-on effects from those increases.

Biggest Housing Affordability Shock In History Incoming

30 Year fixed mortgage rates have jumped 160bp this year, reaching the highest since November 2018, with the latest Freddie Mac data showing an acceleration in mortgage rates which jumped a quarter point in just the past week, from 4.42% to 4.67%. This is an even bigger increase than we discussed in our recent housing comment.

And while the benchmark 10y Treasury yield has also risen, the increase is “only” 94bp. In other words, there has also been a significant widening in mortgage spreads, by 66bp to 243bp. This could be explained by the Fed’s accelerated pivot from QE to QT, the latter of which we expect will be announced at the next FOMC meeting in May.

As discussed one week ago in “Housing Affordability Is About To Crash The Most On Record“, the move higher in rates means that an already record affordability shock will be even worse! Continue reading

Welcome to the Death Zone

Do you own a house? Do you rent?

Bidding Wars For Homes Fall To Lowest Level This Year

(Jacob Passy) The frequency of bidding wars on homes has dropped to the lowest level this year — the latest sign that the housing market may be cooling and reverting back to its usual seasonal patterns.

While home buyers are still more likely than not to face a bidding war on a property they wish to purchase, competition in the nation’s housing market is cooling. GETTY IMAGES/ISTOCKPHOTO

A new report from Redfin RDFN, -2.39% found that 58.8% of the offers on homes written by the company’s real-estate agents faced competition in August. That’s down from 62.1% the month prior and a peak of 74.3% reached back in April. Redfin defines a bidding war as any situation where there are at least two competing bids on a home.

The Cheapest Housing Lots For Sale In San Francisco Are Entirely Under Water

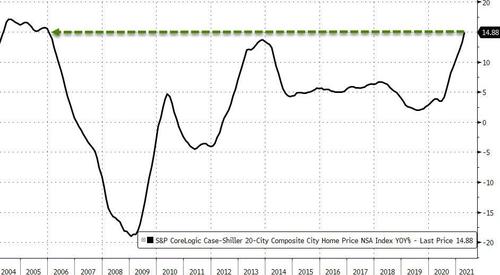

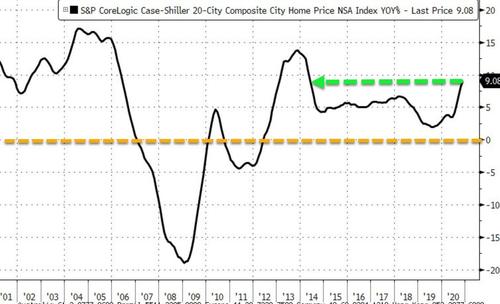

U.S. Home Prices Just Accelerated At Their Fastest Pace On Record

According to the Case-Shiller indices, home prices in America’s 20 largest cities have exploded at 14.88% YoY in April – the highest since Nov 2005…

Home Prices Soar 18% To All Time High; A Record 58% Of Houses Sell Within Two Weeks Of Listing

As if the official government data on soaring home prices wasn’t crazy enough, the latest monthly data from RedFin shows that in April, homes sold at their fastest pace on record with nearly half off-market within one week.

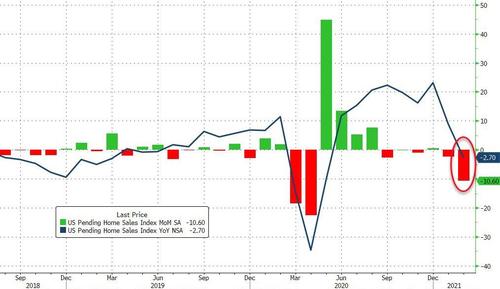

Pending Home Sales Drop For 2nd Month In A Row; Weather, Rates, Inventory Blamed

Following the unexpected plunge in new- and existing-home sales, analysts expected a 3.0% MoM drop in pending home sales to round out the dismal housing data in February. Instead – mimicking the huge drops in other segments of the housing market, pending home sales crashed 10.6% MoM (the biggest drop since April). Worse still, pending home prices are now back down 2.7% YoY…

That completes the triple whammy of collapse in the home sales market…

Source: Bloomberg

Source: Bloomberg

U.S. Home Prices Are Soaring At The Fastest Pace In 7 Years

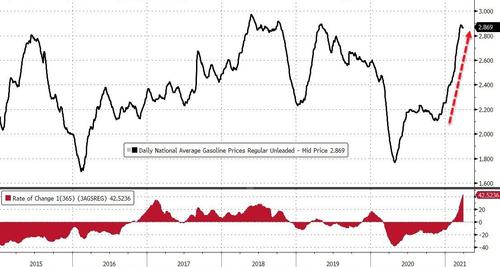

Don’t worry, there’s no inflation – apart from in gas and home prices. According to AAA, gas prices at the pump are back near their highest in 6 years, up a stunning 42% YoY…

Source: Bloomberg

Source: Bloomberg

Continue reading

Red Hot: Sacramento House Receives 122 Offers In Two Days

The housing boom unleashed by the Federal Reserve during the pandemic was built on historically low mortgage rates (thanks Powell), low inventory, city-dwellers moving to rural areas, and remote-work phenomenon. In the latest installment of the desperate frenzy of buyers fleeing for suburban life in California, one home received 122 offers in just two days.

U.S. Home Prices Soar At The Fastest Pace In 7 Years

After surged in October, US home prices (as measured by S&P CoreLogic Case-Shiller index of property values) was expected to accelerate further as a low inventories of listings and solid demand, fueled by cheap borrowing costs, have given sellers more leeway to raise asking prices. And it did not disappoint as November (the latest data) showed the 20-City Composite Home Price Index soared 9.08% YoY… the fastest pace since May 2014.

Top Housing Markets For 2021

The Fed Can No Longer Exit The Mortgage Market Without Causing a Housing Crisis

Liquidity must remain high, mortgage rates must remain suppressed and forbearance must be extended or poof, there goes the housing market. Continue reading

A Tale Of Two Housing Markets: Mortgage Delinquencies Spike 450%, Yet Refis Boom With Low-Principal Loans

As we noted last month, the US housing market is reflecting the extremes of the economy right now – between those who can’t make ends meet due to the pandemic, and those who are either still employed, are sitting on a pile of equity, or both.

One one end of the spectrum you’ve got affluent borrowers locking in record-low rates, while mortgage originations reached a record $1.1 trillion in the second quarter as rates on 30-year mortgages dipped below 3% for the first time in history in July, according to Bloomberg.

Meanwhile, refis may just be getting started.

There are still nearly 18 million homeowners with good credit and at least 20% equity who stand to cut at least 0.75% off their current rate by refinancing, according to Ben Graboske, president of Black Knight data and analytics.

“We would expect near-record-low interest rates to continue to buoy the market,” he said in a statement Tuesday. –Bloomberg

What’s impressive is that the quarterly spike in new mortgage originations occurred while under nationwide public health measures that restricted home showings, appraisals, and in-person document signings, according to the report. That said, refis accounted for around 70% of home loans issued during the period.

Also notable is that the average loan-to-value ratio is above 90%, as borrowers are having no trouble securing loans with just 10% or less down.

At the other end of the spectrum, mortgage delinquencies are up 450% from pre-pandemic levels, with around 2.25 million mortgages at least 90 days late in July – the most since the credit crisis, according to Black Knight, Inc.

“The money is in the homes and people with college education are still working, but the pain is being felt where people are unemployed,” said Wharton real estate professor, Susan Wachter, adding “COVID-1984 will drive an increase in the already high income-inequality gap, and wealth inequality, actually, which is much more extreme.”

While the unemployment rate fell to 8.4% in August, more than 11 million jobs were still lost in the pandemic, the Labor Department reported last week. Supplemental benefits for the unemployed of $600 a week expired in July and Congress has been at an impasse over a follow-up aid package. –Bloomberg

More findings from Black Knight (via Bloomberg):

- More borrowers with ability to refinance are using their equity to get cash. About $44.5 billion in equity was tapped through cash-out refinancing in the second quarter, the most in more than a decade.

- Markets with the biggest delinquency increases in July were Miami, Las Vegas, Orlando, New York and New Orleans.

- The number of homeowners in forbearance continued to fall last week and is down by 1 million from its May peak. But the July 31 expiration of extra unemployment benefits means this month “may provide the true test,” Black Knight said in a Sept. 4 report.

- Homeowners with less equity and lower credit quality were more than twice as likely to have entered forbearance plans. About 11.5% of loans by the Federal Housing Administration and Department of Veterans Affairs were in forbearance last week, compared with 5.1% for Fannie Mae and Freddie Mac borrowers, who have better credit and more equity in their houses.

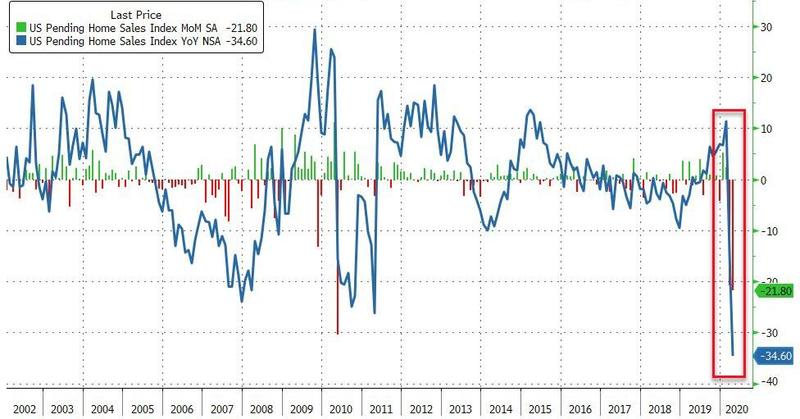

Pending Home Sales Plummet 35% YoY – Biggest Drop Ever As Buyers Forfeit Deposits

Existing home sales collapsed but new home sales rebounded in April, which leaves pending home sales to break the tie and analysts expected a 17.3% MoM drop. However, pending home sales disappointed notably with a 21.8% MoM collapse, sending YoY sales crashing 34.6% – the most ever…

“The housing market is temporarily grappling with the coronavirus-induced shutdown,” which reduced listings and purchases, Lawrence Yun, NAR’s chief economist, said in a statement.

So while all sorts of narratives about lower rates were puked out to defend new home sales outlier data, it seems pending home sales did not get the message…

Every region crashed…

- Northeast fell 14.5%; Feb. rose 2.8%

- Midwest fell 22%; Feb. rose 4.2%

- South fell 19.5%; Feb. fell 0.2%

- West fell 26.8%; Feb. rose 5.1%

That is the lowest level of pending home sales since records began in 2001…

Weekly Mortgage Applications Point To A Remarkable Recovery In Home Buying

If mortgage demand is an indicator, buyers are coming back to the housing market far faster than anticipated, despite coronavirus shutdowns and job losses.

(CNBC) Mortgage applications to purchase a home rose 6% last week from the previous week, according to the Mortgage Bankers Association’s seasonally adjusted index. Purchase volume was just 1.5% lower than a year ago, a rather stunning recovery from just six weeks ago, when purchase volume was down 35% annually.

“Applications for home purchases continue to recover from April’s sizable drop and have now increased for five consecutive weeks,” said Joel Kan, an MBA economist. “Government purchase applications, which include FHA, VA, and USDA loans, are now 5 percent higher than a year ago, which is an encouraging turnaround after the weakness seen over the past two months.”

As states reopen, so are open houses, and buyers have been coming out in force, if masked. Record low mortgage rates, combined with strong pent-up demand from before the pandemic and a new desire to leave urban down towns due to the pandemic, are driving buyers back to the single-family home market. It remains to be seen if this is simply the pent-up demand or a long-term trend.

Buoying buyers, the average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances of up to $510,400 decreased to 3.41% from 3.43%. Points including the origination fee increased to 0.33 from 0.29 for 80 percent loan-to-value ratio loans.

Low rates are not, however, giving current homeowners much incentive to refinance. Those applications fell 6% for the week but were still 160% higher than one year ago, when interest rates were 92 basis points higher. That is the lowest level of refinance activity in over a month.

“The average loan amount for refinances fell to its lowest level since January — potentially a sign that part of the drop was attributable to a retreat in cash-out refinance lending as credit conditions tighten,” said Kan. “We still expect a strong pace of refinancing for the remainder of the year because of low mortgage rates.”

Federal regulators this week changed lending guidelines for Fannie Mae and Freddie Mac, allowing refinances on loans that were or still are in the government’s mortgage bailout, part of the coronavirus relief package. Those loans can be refinanced once borrowers have made at least three regular monthly payments. Given tough economic conditions and rising unemployment, more borrowers may be looking to save money on their monthly payments.

Weaker refinance demand pushed total mortgage application volume down 2.6% for the week.

The refinance share of mortgage activity decreased to 64.3% of total applications from 67% the previous week. The share of adjustable-rate mortgage activity increased to 3.2% of total applications.

Consumer Confidence In Housing Falls To Lowest Level Since Subprime Crash

The economic free fall from Covid-19 is taking its toll on what had been very strong housing demand and sentiment just a few months ago.

After falling sharply in March, housing confidence among consumers took an even deeper dive in April, according to the Fannie Mae Home Purchase Sentiment Index. It was the lowest level since November 2011. Back then, the market was reeling from the subprime mortgage crisis, with home prices cratering and foreclosures rampant.

Consumers suddenly have a much more pessimistic view of buying and selling conditions. In addition, more consumers said their household income is now significantly lower than it was a year ago.

“Individuals’ heightened uncertainty about job security, as registered in the survey over the last two months, is likely weighing on prospective home buyers, who may be more wary of the substantial, long-term financial commitment of a mortgage,” said Doug Duncan, chief economist at Fannie Mae.

This comes even as interest rates are hovering near record lows. And that is helping to keep buyer sentiment slightly ahead of seller sentiment: 46% of those surveyed said it was a bad time to buy a home, while 65% said it’s a bad time to sell a home.

“We expect that the much steeper decline in selling sentiment relative to buying sentiment will soften downward pressure on home prices,” added Duncan.

On average, consumers said they expect home prices to fall 2% over the next 12 months, the lowest expected growth rate in the survey’s history, which dates to 2010.

Home sales have already fallen sharply, and active listings were down 15% annually in April, according to realtor.com. Sellers also pulled their homes from the market, as social distancing measures went into place.

Signs of a rebound?

The numbers are expected to get worse in May, but there is still some demand in the market. Agents in states that are starting to reopen are hosting open houses again, and online searches are rising.

Three in 4 potential sellers said they are preparing to sell their homes following the end of stay-at-home orders, according to a new survey from the National Association of Realtors.

“After a pause, home sellers are gearing up to list their properties with the reopening of the economy,” said Lawrence Yun, NAR’s chief economist. “Plenty of buyers also appear ready to take advantage of record-low mortgage rates and the stability that comes with these locked-in monthly payments into future years.”

Home buying and selling will likely vary dramatically by location, as some harder-hit areas stay closed while others reopen. Sales will still be limited by the tight supply of homes for sale. Even before the pandemic struck, the market was incredibly lean.

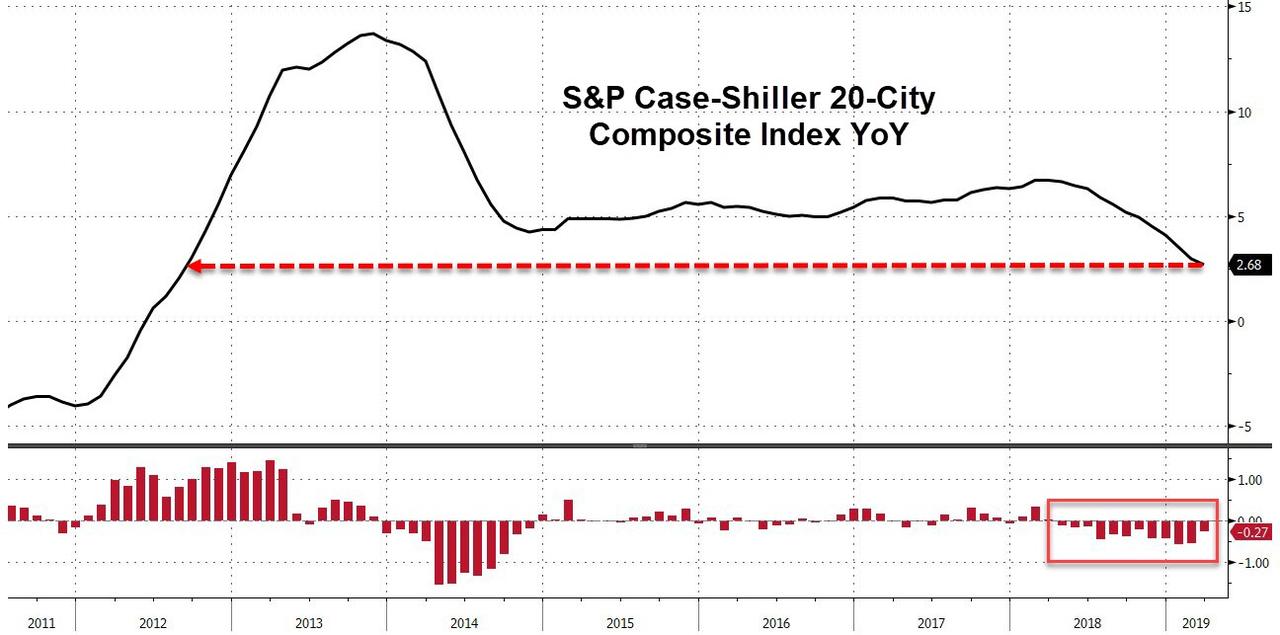

US Home Price Gains Slump For 12th Straight Month, Weakest In 7 Years

Case-Shiller’s March home price index showed yet another deceleration in growth – the 12 months in a row of slowing equals the 2014 growth scare’s length but is the weakest growth since July 2012.

After February’s 20-City Composite 3.00% YoY print, expectations were for 2.55% growth in March and it surprised very modestly with a 2.68% YoY print (still the lowest in 7 years)…

Nationally, home-price gains slowed to a 3.7% pace.

“Given the broader economic picture, housing should be doing better,” David Blitzer, chairman of the S&P index committee, said in a statement.

“Measures of household debt service do not reveal any problems and consumer sentiment surveys are upbeat. The difficulty facing housing may be too-high price increases,” which continue to outpace inflation, he said.

While all 20 cities in the index showed year-over-year gains, five were below 2%: Chicago, Los Angeles, San Diego, San Francisco and Seattle, which a year ago posted a 13% increase. Las Vegas led the nation in March with an 8.2% gain, followed by Phoenix.

Existing Home Sales Tumble YoY For 14th Month – Worst Run Since Housing Crisis

Existing home sales were the odd one out in March (falling as new- and pending-home-sales spiked) but expectations were for a catch-up rebound in April, but did not, dramatically missing the expectation of a 2.7% rise by dropping (again) by 0.4% MoM…

This 0.4% decline comes after existing home sales fell 4.9% MoM in March with a tumbling mortgage rate seemingly not affecting the secondary market…

Single-family units fell 1.1% MoM but Condos/Co-ops jumped 5.6% in April (erasing March’s 5.3% drop).

Supply increased from 3.8 to 4.2 months (the highest since Oct 2018) as median prices jumped to their highest since July 2018.

Only The West saw an increase in sales (up 1.8% MoM) in April, with the Northeast worst, down 4.5% MoM.

Worse still, existing home sales are still down 4.4% year-over-year…

This is the 14th month in a row of annual declines – the longest stretch since the housing crisis over a decade ago…but that’s probably nothing!

Real Estate On New York City’s “Billionaire’s Row” 40% Unsold Due To “Unrealistic” Prices

The area known as “Billionaire’s Row” in Manhattan is becoming one of the biggest real estate gluts in all of the city. 40% of apartments in the area are now sitting unsold in towers that top out at 100 stories, according to the New York Post.

Only half a decade after the One57 building became the city’s first “supertall” residential skyscraper, only 84 of its 132 condos have been purchased. This means that more than a third of them are still on the market and none of them are under contract.

The story is the same down the road – six nearby buildings have as much of 80% of their units available, according to data, with the total value of all unsold inventory estimated to be between $5 billion and $7 billion.

And the supply glut is only going to get worse, as Central Park Tower, at 217-225 W. 57th St. is set to put an additional 179 apartments on the market next year. No deals for the new building have closed, which means if it opened today it would push the overall unsold percentage in the area to nearly 65%. Listings online show asking prices for units between $2.1 million and $64 million. Brokers are blaming the high prices for the sales drought.

Top broker Dolly Lenz said:

“When people come here from other parts of the country and from around the world, the first thing they want to see is Billionaires’ Row. We toured them through the properties but many felt they were too pricey for the market — $7,000, $8,000 and $10,000 a square foot.”

Lenz also said that these prices were caused by a combination of costs of property, construction, financing and high-end marketing, in addition to developers who have clauses in their contracts that keep lenders from forcing them to drop prices.

Many brokers feel pessimistic, expressing that the drought in Billionaire’s Row could telegraph a coming drought for the entire market. The Post provided a host of pessimistic quotes from brokers:

- “Empty buildings are never good for the city,” one broker said.

- “This happened in 1988 to 1992, when there were a glut of condos that didn’t sell. They were smaller and less expensive, but it led to bad times.”

- Another broker said the prospects for selling the vacant apartments were grim.

- “They are priced out of the constellation of buyers out there now,” the broker said.

- “It’s all a function of price. You can do the most spectacular marketing and offer the most incredible amenities, but it all comes down to price.”

- “There’s a whole food chain that relies on people living in these buildings,” one broker said.

One local resident said of the vacancies:

“To find out that people aren’t living in the condos is just, ugh. I wish this was all affordable housing. This really upsets me. So many are struggling in the city.”

An Extell spokeswoman disputed some data provided in the article, stating that One57 “is over 85 percent sold in units and over 90 percent sold in value.”

About one month ago, we reported that Manhattan’s housing market was on its “worst cold streak in 30 years”. We also took note of the rising prices that are pricing potential buyers – even the billionaires – out of the market.

By one broker’s count, Q1 marked the sixth straight quarterly drop in sales volume, the worst streak in at least 30 years.

Per the FT, sales tumbled by 11%, according to broker Stribling & Associates, by 5%, according to Corcoran, and by 2.7% for co-ops and condominium apartments, according to Douglas Elliman and real estate appraisal firm Miller Samuel.

While the average sales price for new developments climbed a staggering 89.4% to $7.6 million, that figure was exaggerated by a single purchase: Ken Griffin’s purchase of a $240 million penthouse at 220 Central Park South, which, according to some, was the most expensive home ever sold in America. But depending on the report, the median sales price ranged from 2% lower to 3.2% higher. And although the entry level market in Manhattan – that is, apartments priced at $1 million and below – had held up for most of the past year, it has recently started to suffer.

“It’s like a layer cake,” Jonathan Miller, CEO of Miller Samuel, told CNBC. “When you have softening at the top, it starts to melt into the next layer and the next layer after that, because those buyers further down have to compete on price.”

According to one broker, sellers with unrealistic expectations are the biggest barrier to sales, because they’re refusing to adjust for the fact that listings have been piling up and sitting on the market for longer periods, giving buyers more room to negotiate, and more options.

Inventory has climbed 9% over the past nine months, and there’s a glut in new developments that’s only going to get worse.

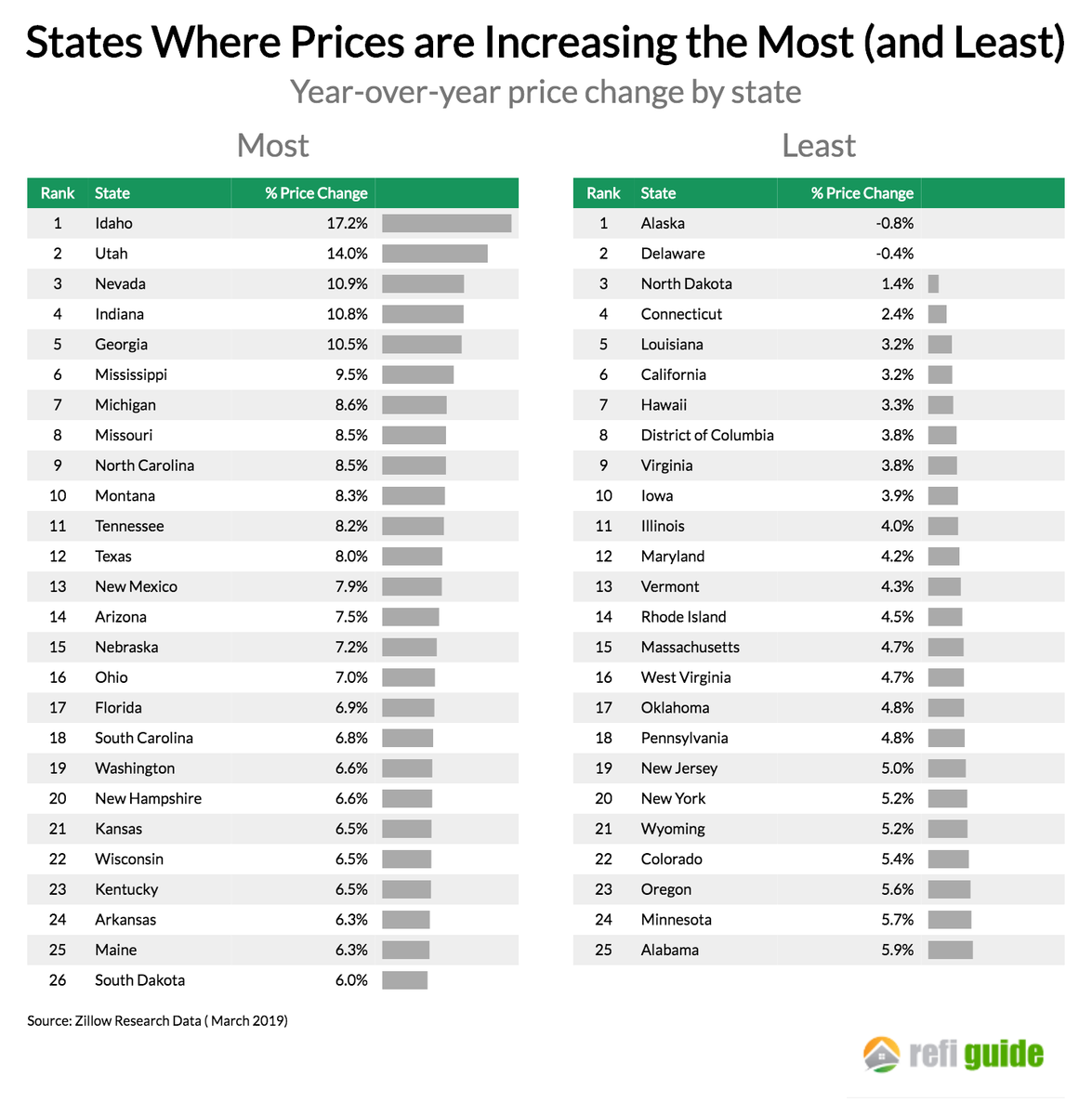

Where Home Prices Are Rising the Fastest (Slowest) In America

Since the end of the great recession, home prices in America have rebounded substantially. Since the dark days of 2009, prices have steadily climbed and are up over 50% on average from the lowest point.

This is great news for homeowners whose homes may be worth more than their pre-recession values, but less great news for homebuyers who can afford less house for the dollar. What’s more is that in some places, home prices have spiked much faster than average, while in other places, home prices have remained depressed.

So where in America are home prices increasing the fastest and the slowest? In light of fluctuating mortgage interest rates, tax reform that’s limited many homeowner deductions, and an affordability crisis in many urban areas, along with Priceonomics customer RefiGuide.org thought we’d dive deeper into the home price data published, aggregated and made available by Zillow.

Over the last year, the median home prices increased the fastest at the state level in Idaho, where prices increased by a staggering 17.2%. In just two states did home prices actually fall last year (Alaska and Delaware). The large cities with the fastest home appreciation were Newark, Dallas, and Buffalo where prices increased more than 15% in each place. The large city where prices decreased the fastest was Seattle, where home prices actually fell 2.4%.

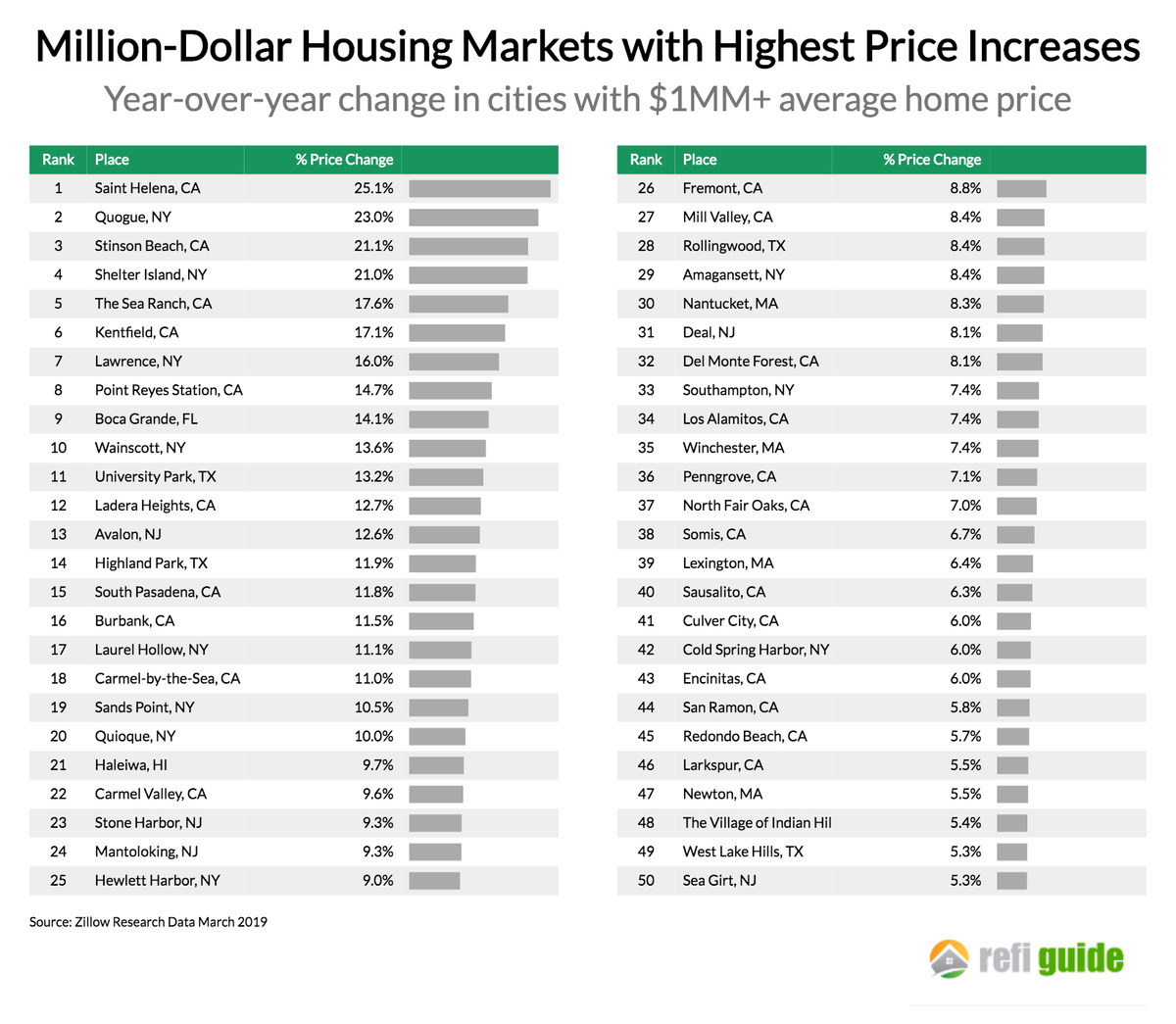

Lastly, we looked at the expensive markets (where homes cost more than a million dollars) that had the highest price appreciation. St. Helena, CA, Quogue, NY and Stinson Beach, CA all had prices increase over 20% last year.

***

For this analysis, we looked at data from the beginning of March 2019 compared to prices one year earlier. We looked at Zillow’s seasonally adjusted median price estimate as published by Zillow Research Data.

Nationally, home prices increased 7.2% last year or about $15,000 more than the year before. However, in some states prices spiked much more than that.

Idaho leads the country with home prices increasing by 17.2% last year, driven by strong demand in the Boise market. In Utah the impact of a thriving economy and growing population is that prices increased 14% in just one year. Nevada, likewise is seeing strong home price growth as people migrate from California and the state’s low taxes are more favorable under the most recent tax reform. Alaska and Delaware have the distinction of being the only states where home prices fell over the last year.

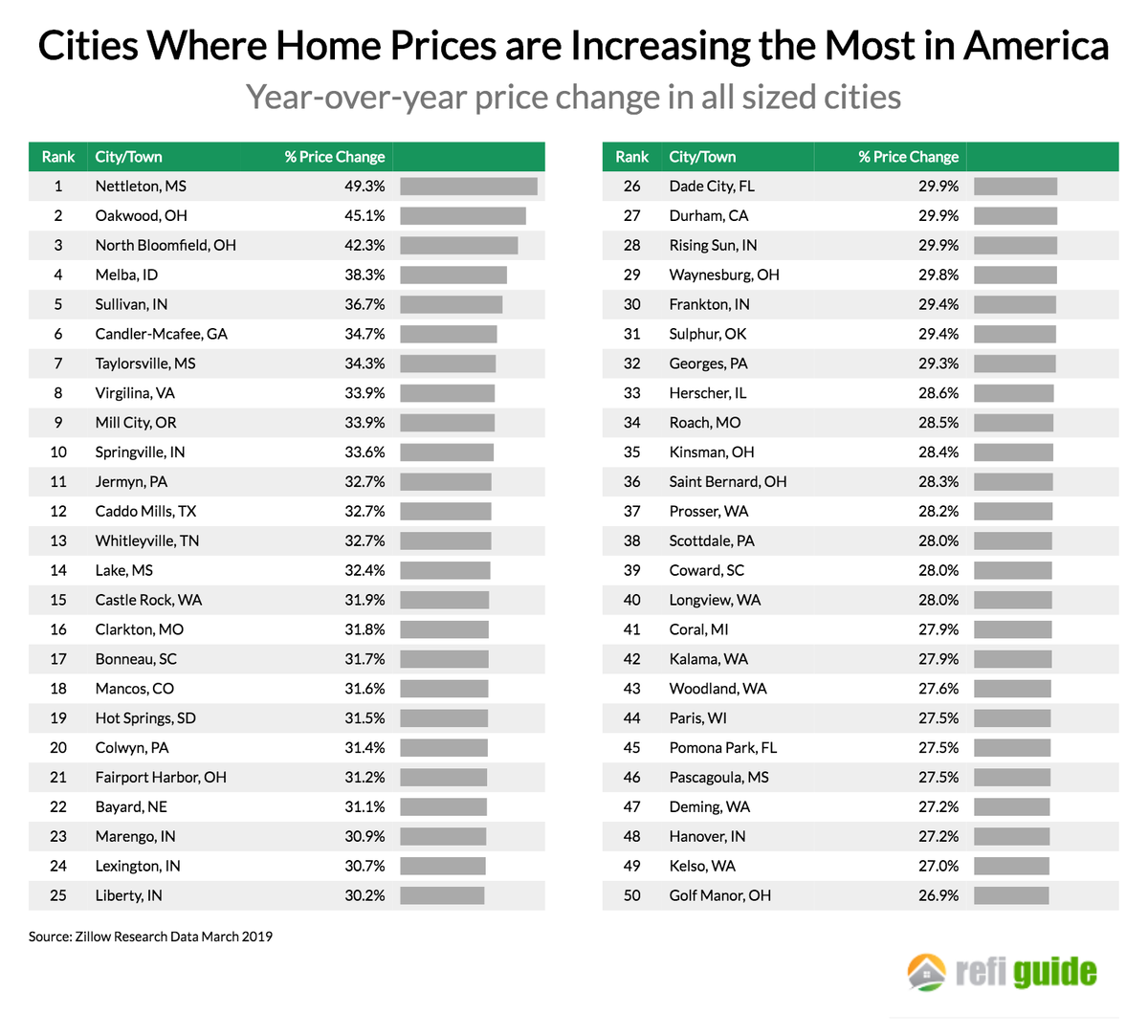

Next, we looked at home prices in the top one hundred largest housing markets, as measured by population. Which cities were experiencing rapid home equity appreciation and which ones are not?

At the city level, home prices have increased the fastest in Newark, NJ where prices have increased more than 17% as buyers who are priced out of New York City have purchased in this area. Dallas, a city with a strong economy and low taxes has seen home prices increase nearly 17% as well.

Notably, some of the most expensive and desirable cities like Seattle, Oakland and Portland have seen their prices decrease in the last year. Each of these locations has experienced price appreciation during this decade, however.

Were there any smaller cities and towns that experienced home prices rising faster than the big cities? Below shows the fifty places in the United States where home prices increased the most this last year:

Across the Midwest and South, numerous smaller cities experienced price appreciation much greater than 25% last year. In Nettleton, MS prices increased 49% in just one year! Notably, almost none of these high-price growth cities are located on the coasts.

Lastly, what are expensive places to buy a home in America that are just getting more expensive? To conclude we looked at locations where the median home price was over one million dollars and the prices keep rising:

In this rarefied group, prices increased the most in Saint Helena, CA. In this tony town in Napa Valley, prices increased over 25% last year. In second place was Quogue, NY a town in the Hamptons. In fact, 9 out of the top 10 expensive cities with high price appreciation are in California or New York. More specifically, many of these locations are in the vicinity of San Francisco and New York City, the two very large economic engines that are driving home prices.

***

After nearly a decade of vibrant stock market and real estate returns, this year home prices have continued to climb at a steady clip. In only two states in America did prices actually fall, and in five states prices grew more than 10% in a year. As the economy has continued roaring, places that were once known for being affordable like Idaho, Utah, and Nevada have seen home prices spike. While expensive cities like Seattle, Portland and Oakland have seen prices level off in the last year, and places like Newark, Dallas and Buffalo have become less affordable. In this stage of American economic expansion, the once affordable places are seeing their prices escalate.

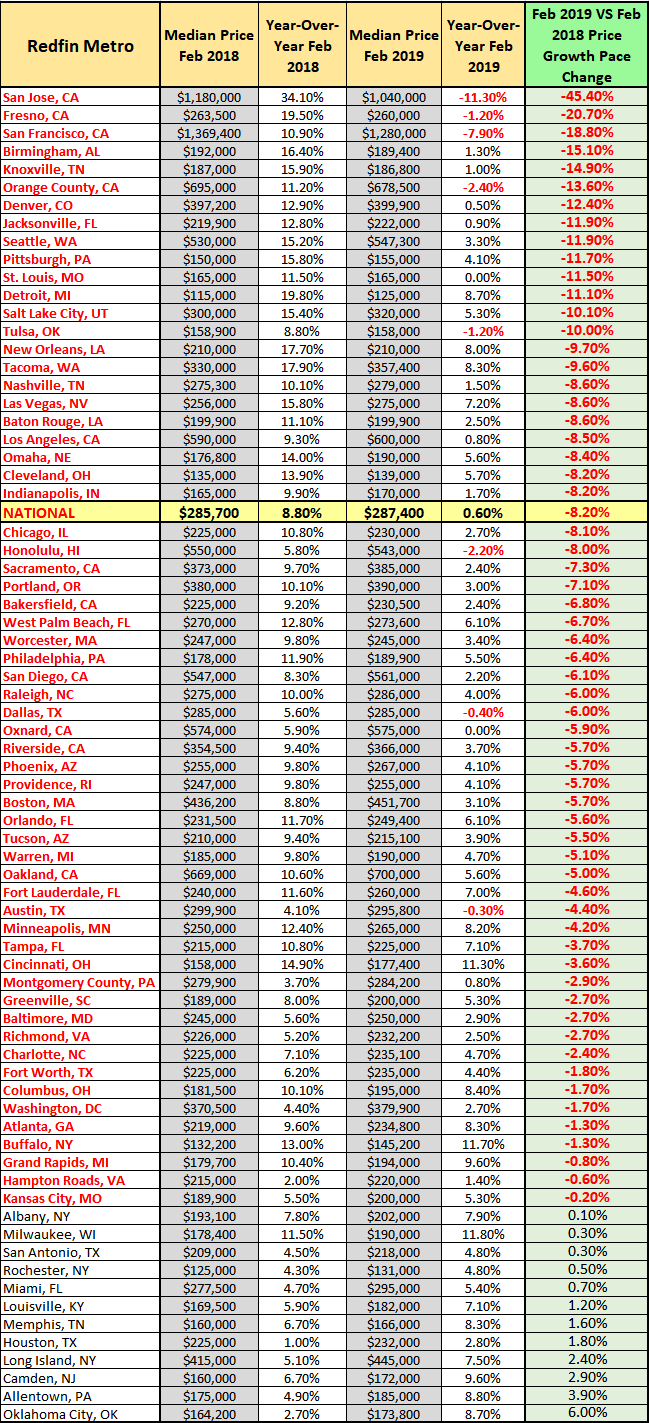

US Housing Hits A Brick Wall: “The House Price Deceleration Is Staggering”

(by Mark Hanson) RedFin puts out a monthly home sales report, which contains a lot of great data. The chart below shows Feb 2018 year-over-year price growth, which was off the charts, compared to Feb 2019 year-over-year growth, which was very weak.

This y/y growth deceleration is staggering, especially in the high-flying regions.

Very few regions escaped a significant deceleration with some prominent regions like San Jose and San Francisco even getting crushed on a year-over-year absolute basis.

The only thing that even comes close to this sharp of deceleration was circa-2007.

It was data like these I have been tracking that led to my call last year that there was no way the Fed could continue to hike in 2019.

For certain housing and related names, this is a killer unless prices re-accelerate quickly.

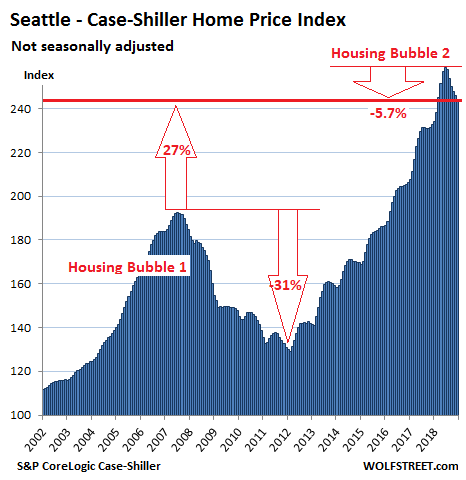

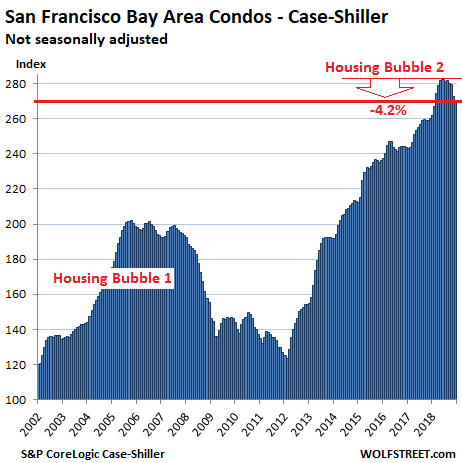

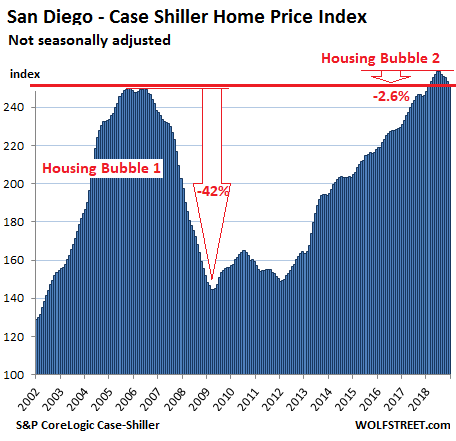

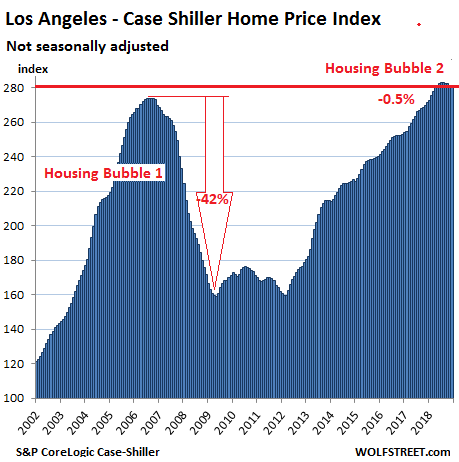

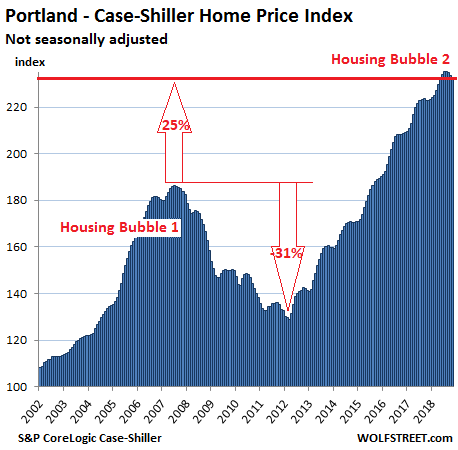

The Most Splendid Housing Bubbles in America Get Pricked

San Francisco Bay Area & Seattle lead with biggest multi-month drops since 2012; San Diego, Denver, Portland, Los Angeles decline. Others have stalled. A few eke out records.

San Francisco and San Diego are catching the Seattle cold, and others are sniffling too, as the most splendid housing bubbles in America are starting to run into reality.

House prices in the Seattle metro dropped 0.6% in December from November, according to S&P CoreLogic Case-Shiller Home Price Index, released this morning, and have fallen 5.7% from the peak in June 2018, the biggest six-month drop since the six-month drop that ended in February 2012 as Housing Bust 1 was bottoming out. The index is now at the lowest level since February 2018. After the breath-taking spike into June, the index is still up 5.1% year-over-year, and is 27% higher than it had been at the peak of Seattle’s Housing Bubble 1 (July 2007):

So Seattle’s Housing Bubble 2 is unwinding, but more slowly than it had inflated. Many real estate boosters simply point at the year-over-year gain to say that nothing has happened so far — which makes it a picture-perfect “orderly decline.”

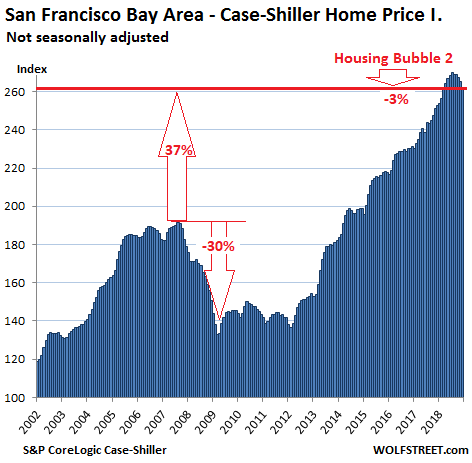

San Francisco Bay Area:

The Case-Shiller index for “San Francisco” includes five counties: San Francisco, San Mateo (northern part of Silicon Valley), Alameda, Contra Costa (both part of the East Bay ), and Marin (part of the North Bay). In December, the index for single-family houses fell 1.4% from November, the steepest month-to-month drop since January 2012. The index is now down 3% from its peak in July, the biggest five-month drop since March 2012.

Given the surge in early 2018, the index is still up 3.6% from a year ago and remains 37% above the peak of Housing Bubble 1, fitting into the theme of a perfect orderly decline:

Case-Shiller also has separate data for condo prices in the five-county San Francisco Bay Area, and this index fell 0.9% in December from November, after an blistering 2.4% drop in the prior month. From the peak in June 2018, the index has now dropped 4.2%, the steepest six-month drop since February 2012:

The Case-Shiller Home Price Index is a rolling three-month average; this morning’s release tracks closings that were entered into public records in October, November, and December. By definition, this causes the index to lag more immediate data, such as median prices, by several months.

The index is based on “sales pairs,” comparing the sales price of a house in the current month to the prior transaction of the same house years earlier (methodology). This frees the index from the issues that plague median prices and average prices — but it does not indicate prices.

It was set at 100 for January 2000; a value of 200 means prices as tracked by the index have doubled since the year 2000. Every index on this list of the most splendid housing bubbles in America, except Dallas and Atlanta, has more than doubled since 2000.

The index is a measure of inflation — of house-price inflation. It tracks how fast the dollar is losing purchasing power with regards to buying the same house over time.

So here are the remaining metros on this list of the most splendid housing bubbles in America.

San Diego:

House prices in the San Diego metro declined 0.7% in December from November and are now down 2.6% from the peak in July, the biggest five-month drop since March 2012, leaving the index at the lowest level since February 2018, and just one hair above the peak of Housing Bubble 1:

Los Angeles:

The Case-Shiller index for the Los Angeles metro was about flat in December with November but down 0.5% from the peak in August — don’t laugh, the largest four-month decline since March 2012. What this shows is just how relentless Housing Bubble 2 has been. The index is up 3.7% year-over-year:

Portland:

The Case-Shiller Index for the Portland metro inched down in December from November for the fifth month in a row and is now down 1.4% from the peak in July 2018. And that was the steepest five-month drop since March 2012. Year-over-year, the index was up 3.9%:

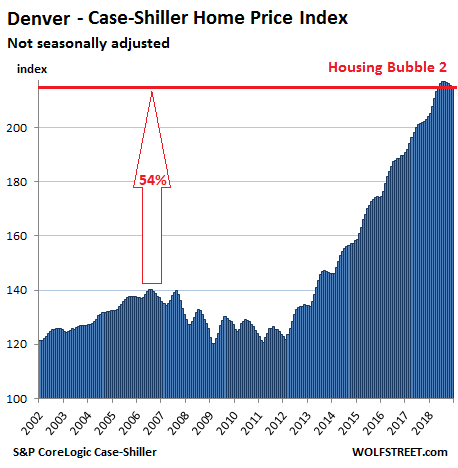

Denver:

House prices in the Denver metro edged down in December from November for the fourth month in a row, after an uninterrupted 33-month run of monthly increases. The four-month drop amounted to 0.9%, which, you guessed it, was the steeped such drop since March 2012. The index is at the lowest level since May 2018 but is still up 5.5% year-over-year:

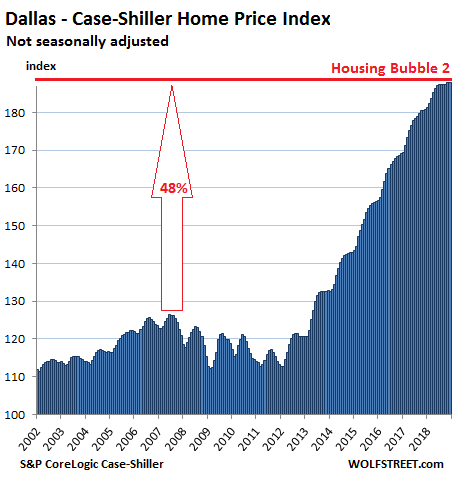

Dallas-Fort Worth:

The Case-Shiller Index for the Dallas-Fort Worth metro in December ticked up by less than a rounding error to a new record, leaving it essentially flat for the seventh month in a row. The index is up 4.0% year-over-year:

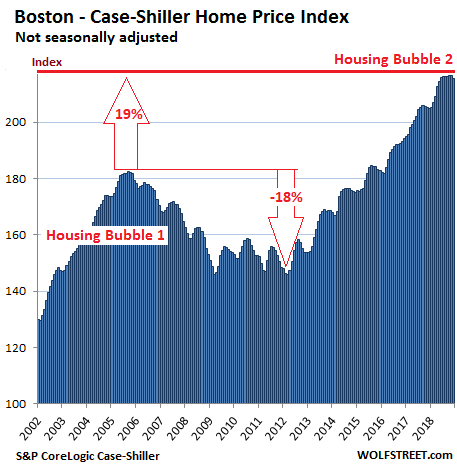

Boston:

In the Boston metro, house prices dipped 0.5% in December from a record in November and are now back where they’d been in June. The Case-Shiller Index is up 5.3% from a year ago:

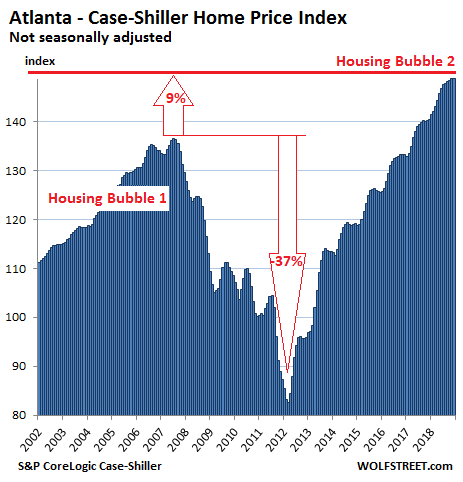

Atlanta:

The Case-Shiller Home Price Index for the Atlanta metro inched up a smidgen in December, to a new record, and is up 5.9% from a year ago:

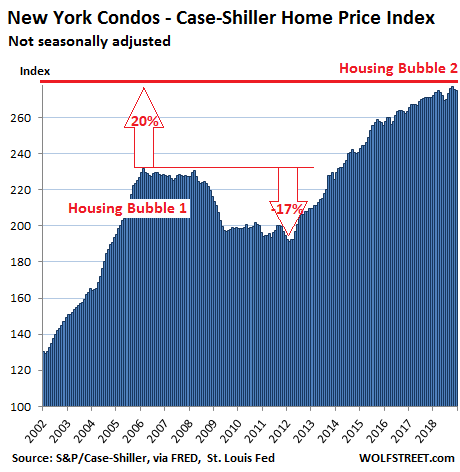

New York City Condos:

The Case-Shiller index for condo prices in the New York City metro ticked down in December for the second month in a row after a mighty bounce in September and an uptick in October. This index can be volatile, but after all these bounces and declines, the index was up just 1.5% from a year ago, the smallest year-over-year price gain on this list of the most splendid housing bubbles in America:

On a national basis, these individual markets get averaged out with other markets that didn’t quite qualify for this list since their housing bubble status has not reached the ultimate splendidness yet. Some of those markets, such as the huge metro of Chicago, remain quite a bit below their Housing Bubble 1 peaks and are now declining, while others are shooting higher.

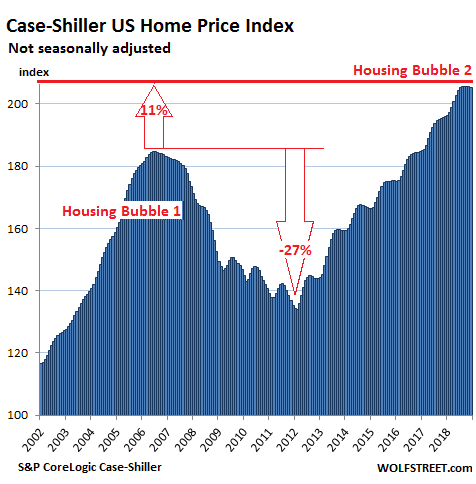

So the Case-Shiller National Home Price Index has been about flat since July, but is still up 4.7% year-over-year and is 11% higher than it had been at its prior peak in July 2006 during Housing Bubble 1:

It always boils down to this: Regardless of how thin you cut a slice of bologna, there are always two sides to it. When home prices drop after a housing bubble, there are many losers. But here are the winners – including a whole generation. Listen to my latest podcast, an 11-minute walk on the other side…

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate “beer money.” I appreciate it immensely. Click on the beer mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

Housing Market Crisis 2.0: The Jury Is In For 2018-2019

Summary

Here is a play-by-play review of a housing crisis that began exploding one story at a time last summer.- What is different this time from last is that the 2007-2009 crisis started in the US and pretty much stayed in the US.

- This one is developing all over the world simultaneously – in the US, Canada, Australia, the UK, etc.

(by David Haggith) As happened with the first housing market crash that began in 2007 but didn’t become widely recognized until mid-2008, the present housing crisis began exploding one story at a time last summer, and this blog was perhaps the first to state that summer’s change was the turning point from decades of ascent into a collapse in housing sales and prices. I said the same thing back in 2007, and people didn’t believe me then either.

The present housing market crash, like the last, was created by the Federal Reserve artificially pressing mortgage rates down, then down further, and then down as deep they dared push for years and years. Falling interest allowed people with flat incomes to keep purchasing increasingly expensive homes. Since people buy payments more than house prices, housing prices kept rising as payments were kept in line via these artificial interest reductions.

The Fed’s ill-conceived plan, however, was never sustainable prior to the last housing market crash and is not now. I’ve said throughout the Great Recession and ensuing years that, sooner or later, we’d get to the point where the Fed would have to raise rates, and I’ve said its quantitative tightening will certainly raise rates as much as it increases its stated interbank lending interest targets. I’ve also said that, by the time the Fed started raising rates, housing prices would be unaffordable without the Fed’s artificially lowered interest; therefore, the market would have to crash all over again because, all over again, people would find themselves underwater on their mortgages.

And now, here we are. US banks have not started to go down, but they are feeling serious pressure as this article will point out, while eight months of statistics now prove housing is relentlessly falling with NO hint of letting up. As I wrote in my first Premium Post, “2019 Economic Headwinds Look Like Storm of the Century,” Housing Market Crash 2.0 is one of the numerous forces that will be knocking the US economy down in 2019. The rest of the global economy is already down further than the US.

The principal driver in Housing Market Crash 2.0 is the Federal Reserve’s Great Recovery Rewind (the downsizing of its balance sheet, which tightens financial conditions). This, I said two years ago, would cause mortgage rates to start rising one year ago, and you can now see that mortgage rates did exactly that all of last year:

Mortgage rates rose only a minuscule blip when the Fed started with a tiny rolloff (tightening) near the end of 2017, even as I had said the Fed’s unwind would not likely cause any serious damage to the economy until January 2018. Rates, however, immediately ramped up steeply when the Fed doubled its roll-off rate in January (which was when I said the balance sheet unwind would start to have serious market impacts). This has hit stocks, bonds, and housing the worst… so far.

Since the housing market is one of the major areas where Americans store wealth and since it is an industry that buys products and labor from a multitude of other industries, a decline in housing impacts the economy more than any other industry.

US Housing Market Crash 2.0

Here is the path US housing prices had been following until the market rolled over:

And here is a play-by-play of how the housing market crash has gone since I made my brazen 2018 summer proclamation that it had arrived on schedule:

June-July, 2018: Average housing demand in the US was reported to have fallen 9.6 percent in June YoY, while the number of listings increased. Overall, 15% fewer offers were made on homes, which is probably why the inventory grew. In many major markets, however, inventory declined. Agents in So. Cal reported bidding wars were cooling down. Where homes had been getting 10-15 offers (causing a bidding war), they were now just getting one or two.

Prices continued to climb or remained high because sales have to slump a lot before sellers become willing to accept the harsh reality that their homes, in which they have so much of their wealth invested, are not worth as much as they were. As inventory rises, buyers become more choosy and make offers on only the best-priced homes, rather than bid prices up. As a result, prices stall so do buyers until eventually their waiting overcomes seller inertia and sellers start to move down to find the more deeply coalesced pool of buyers.

In affluent areas, however, prices already began to fall. In part, this jolt down at the top was due to the Trump Tax Cuts, which funded some cuts by curbing deductions for mortgage interest and particularly for property tax. That hit areas like Manhattan, Westchester County, New Jersey, and Connecticut the hardest because of their high property taxes that had been paid on behalf of the wealthy via income-tax breaks. (Property-tax bills in Westchester County, one of the highest in the nation, commonly hit $50,000 per year or more.)

On a quarterly basis, purchases nationally plunged 18% in the second quarter.

August 2018: Near the end of summer, reports like the following started to appear for the first time in almost a decade:

“We all think next year is going to be a tough year for real estate sales,” said Matthew Roach, a property attorney in Yorktown Heights, New York…. Some buyers are saying, “‘Look, I’m not going to spend more than $35,000 in taxes,’ ” said Angela Retelny, a broker at Compass. “Houses … have to be reduced – because their taxes are just way too high for the price range….” The state of the market is such that you’re seeing “dramatic price reductions every single day – every hour, pretty much,” she said.”

But it was not just high-end markets that hit the skids. Farms in the midwest had been seeing rising bankruptcies for a few years and finally broke above the peak they hit in the last housing market crash:

The rise in farm bankruptcies, however, had little to do with mortgage rates or housing prices, and everything to do with commodity prices (particularly dairy); however, as goes the farm business, so goes the sale of the farm. More people selling in distressed conditions coupled to fewer people interested in buying into a failing industry equals tougher sales; and, so, this distress was certain to flow out into declining sales and prices. (Fire sales of land and equipment due to distress last summer are now well underway.)

The impact hit first in delinquent Ag. loans in the upper midwest, which rose (when measured against the farm capital backing those loans) to strike a level worse than what was seen in the pit of the Great Recession. The Kansas City Fed predicted farm income would worsen into 2019. The Trump Trade War certainly isn’t helping.

(During this same time, my wife and I – putting my belief in a housing market crash to practice – listed our farm in the hope of selling near the peak, possibly renting and then buying back in at a lower price in a couple of years. We hope to retire our mortgage so that we can more easily retire five years from now. We both have jobs that are fairly recession proof, so we’re not too concerned about needing to grow our own food. Still, if we can’t sell at near-peak value, we’ll happily hold on here since the farm produces relatively passive income. (We let other people rent agricultural use and do 90% of the work.) If things ever did go extremely bad, we can grow a huge amount of food in a valley that always has abundant mountain water. So, we’ll be happy to sell at peak value, but happy to sit it out here if we’re already too late to get that value.)

September 2018: By the end of summer on the east coast, some markets like Connecticut saw a rise in people choosing to wait out the foreseeable housing market crash by renting, even at $10,000 a month for higher-end homes, in hopes of buying low at the bottom of the market in a not-too-distant future. Several east-coast counties saw rentals rising sharply as sales fell just as sharply. Owners also began choosing to rent out homes rather than sell them at a loss because losses on a primary residence are not deductible; but if a home has been rented for two years, it can be converted into an investment property so that, at least, the loss can be deducted from taxes. (They may have also hoped that, by renting, they could wait out the decline in prices.)

Todd David Miller, a vice president of sales at the Higgins Group, said that of the $57 million in sales his team has done so far this year, primarily in the towns of Westport and Fairfield, almost all of the sellers have either moved out of state or are renting in the area. Those who are staying in the area are gravitating toward home rentals near the beach.

“These are mainly higher-end transactions, and the majority of them had to sell at a loss,” Mr. Miller said. “They don’t want to put any more money into real estate right now….”

“We’re going through this era of uncertainty. And what do buyers do when the near-term seems uncertain? They pause. People are just nervous that values will continue to decline, and for that reason, more people are opting to rent, if they are not forced to buy”, Miller said.

October 2018: New home sales were expected to start rising again in October but, instead, fell miserably (8.9% MoM). That marked the seventh month of missed expectations. The midwest led the slump that month, falling a hard 22%, but the fall was bad in all parts of the US. At this point, median prices began dropping nationally, too (down 3. 6%). As a result of a backlog from declining sales, inventory began to soar (climbing 7.4 in one month). Sentiment, too, had taken a bad plunge by October with the number of people who said they planned to buy a house in the next twelve months falling by half over the past year.

Sales of new U.S. single-family homes tumbled to a more than 2-1/2-year low in October amid sharp declines in all four regions, further evidence that higher mortgage rates were hurting the housing market.

The Fed crush was fully on.

November 2018: By November, mortgage rates across the United States had hit their highest level since the Great Recession 8-1/2 years earlier. As a result, new mortgage applications across the US fell to their lowest level since December 2014. Since refinancing mostly happens when mortgage interest is lower than it was when a mortgage was taken out, refis hit their lowest point since the year 2000. So, clearly, the Fed has crushed mortgage activity.

By this point, year-on-year sales had fallen for eight straight months across the nation. The west coast – with Seattle leading the earlier procession in sales and prices – had long been one of the nation’s hottest markets, which is why I stated at the start of last summer the housing market’s initial decline in Seattle was a “bellwether” for the whole US market. While my one crow on a wire (detractor) insisted I didn’t know a thing, time has proven my summer proclamation that Housing Market Crash 2.0 had begun to be dead on with Seattle leading the recession in sales and prices:

Since that proclamation, inventories in the region have soared due to a buildup from declining sales. Lending limits have increased due to falling prices and less assurance on the part of banks that collateral will hold its value or that repossessions won’t be the next wave. King County where Seattle is located has led the decline to where the number of single-family homes on the market has doubled in just a year.

Since my summer declaration, King County has recorded a bruising fall. In just half a year, the median price plunged from its peak of $726,000 last spring to $644,000 in November. According to Mike Rosenberg, a Seattle Times real estate reporter, this was the fastest price drop anywhere in the nation (over 11% in half a year – a crushing reversal from years before when rises 10% in a full year were seen as evidence of a superheated market; so, doesn’t that make this flash-frozen fall?) The last drop that steep was back at the start of the Great Recession in 2008! Not a time for housing anyone wants to compare to.

In Southern California, home sales in November plunged 12% YoY. In California, however, prices remain above their 2008 summit and have so far largely resisted following sales down. Nevertheless, Bank of America proclaimed, “We are calling it: existing home sales have peaked.”

LA Times noted if volatility in the stock market and Washington significantly affects consumer confidence and business investment decisions in 2019, the housing market could be due for significant correction into 2020…. Richard K. Green, director of the USC Lusk Center for Real Estate, told the LA Times, he is very pessimistic about the housing situation in Southern California. Green warns prices could plunge 5% to 10% into 2020, even with the current level of economic growth.

Things looked just as stark in Las Vegas by November where, out of the 10,000 homes on the market, 7,000 of those had not received a single offer, a figure 50% worse than the year before. Realtors started warning sellers not to panic, which, in itself, easily becomes a self-fulfilling warning. In the last few years, Las Vegas had risen to become one of the most overvalued markets in the nation. It looks like prices have finally peaked now that they have risen out of site on the back of low-interest loans and now that interest is higher and now that the Trump Tax cuts have stripped away some of the benefits of home ownership in favor of a larger general deduction that goes equally to renters or buyers.

By the end of November, the US Census Bureau reported that new home sales had rolled off a cliff. New homes sitting on the market were at their highest point in five years, and unsold supply per quarter was growing at an alarming annualized rate of 33% (meaning should it continue).

In another sign the market has turned under, housing flips have flopped in the Chicago area. The flipper boom has nearly gone bust. With properties taking longer to sell, higher interest on loans to acquire and repair those fixers eats up more profit and increases the risk involved in flipping homes. With profits sometimes now shifting into reverse, flippers are backing out of the market. The number of homes turned around by flippers in the Chicago area went from a high of 7,600 in the first three quarters of 2017 to 4,000 in the first three quarters of 2018. Across the nation, the number of homes flipped dropped 12%.

December 2018: The median price of a home in Manhattan fell below the one-million-dollar market for the first time in four years, and it took 15% longer to sell even at those lower prices. Again, real estate agents noted that the Trump Tax Cuts were making the situation worse, but particularly in high-end markets.

Relief started spreading to the boroughs, too. Most of Brooklyn’s trendiest neighborhoods saw more than a fifth of sellers pressed to lower their asking price. And in the pricey Hamptons, home purchases in the 4th quarter of 2018 crashed a full 35%, the biggest quarterly fall since … you guessed it, the Great Recession in 2009!

Inventory is piling up across the city, and that’s good news for buyers in search of a bargain. For sellers with dreams of making a big profit, it’s time for a reality check.

Most of us don’t care what banksters are paying (or getting) for a home near their Wall Street office, but the massive year-end plunge in NYC and its surrounds is further evidence that the fall in home prices is not only unabated but worsening. What started showing up at the top of the market in the hottest markets like Seattle last summer is now, as I said would be the case, trending down to lower sectors just as seen in the spread from Manhattan to the boroughs.

This is all terrible news for my crow. If he had any integrity, he’d cannibalize and eat crow. Of course, neither crows nor trolls ever have integrity. However, for those who would like to become first-time home buyers someday, this is news to crow about. How you look at it depends on where you’re standing. Someone might even be able to become a first-time home buyer in Manhattan in a couple of years if the Fed doesn’t quickly spin on its heels and reverse its Great Recovery Rewind, as it is already sounding ready to do.

Nationally, sales dropped 11% in December, but the most valuable thing about December stats is that we get a final tally to reveal how the entire year went. A total of 5.34 million homes sold in 2018, proving the year to have the largest annual drop (about 10%) in total home sales since … you guessed it … the bottom of the Great Recession eight years ago.

Business Insider summarized 2018 as the year that…

The US housing market took a dark turn … as homebuying fell off a cliff and mortgage lenders saw a steep decline in applications, originations,and profits. Interest rates are partly to blame for the slide in housing, but that’s only half of the equation, according to analysts. It’s too soon to panic, but a deeper drought in housing is bad news for just about everybody, not just the banks. Significant housing declines have foreshadowed nine of the 11 post-war US recessions, according to UBS…. The decline has been broad, affecting every region in the US.

2018-2019 Housing Market Crash 2.0 appears inevitable, given how far off the cliff we’ve already fallen and how fast we’re going down.

And here is where home-buying sentiment now lies:

So, eat crow, Crow. In short, sentiment across the nation is as bad as it has ever been. It looks like how people feel after they’ve already fallen off a cliff.

How hard is Housing Market Crash 2.0 hitting banks?

At Wells Fargo, mortgage banking revenues fell 50% to $467 million in the fourth quarter, while originations declined 28% to $38 billion. JPMorgan, meanwhile, saw mortgage income fall to $203 million, a 46% drop from the same period last year. Originations fell 30% to $17.2 billion.

that’s Fifty percent!

Looking forward: Pending sales are a forward-looking indicator. Due to the lag of a month or two between a pending contract and closing, the direction of movement in pending sales tells us where we’ll most likely be in final sales a month or two down the road. November’s pending sales told us that sales in January when all reporting is completed in February will likely be down to their lowest since May 2014. And December’s sales, which were way down in November’s pending report, already came in worse way worse than November’s actuals, falling a whopping 2.2% from where they were in an already bad November. So, we can expect January’s to do no better once all reports are in.

Real estate bimbos had expected a 0.5% rise in December! Of course, they were also ebulliently predicting a warm spring market for 2019 and recently were forced by facts to temper their predictions. In my opinion, real-estate sales people (as a group, not all individuals) fit somewhere among the following groups for lying: 1) transportation sales people (car dealers and horse traders); 2) banksters; 3) stock brokers; and 4) politicians.

Graph by Wolf Street

Graph by Wolf Street

“It’s been dripping down, down, down,” NAR chief economist Lawrence Yun said…. “Frustrating that the housing market is not recovering.”

Wolf Street

Pending sales strongly indicate that Housing Market Crash 2.0 is still fully on track for 2019. Moreover, year-on-year declines have been worsening each month since the start of October even though interest rates improved in November. That, to me, supports my view that the Fed has already gone too far to stop the damage, even if it quits tightening altogether.On a longer-term perspective, consider the demographics: School-debt-ridden, under-employed millennials, who are more into buying experiences in life than things, are not inclined to buy homes that are in the housing-bubble price zone. Neither are baby-boomers looking to retire, which often involves downsizing.

None of this bothers me because my wife and I have the best of all worlds – very low fixed interest, a home we bought at the bottom of the market last time around, a chance to sell now high or stay and keep reaping the rewards of living in a beautiful place.

I benefited from the last crash. I hope others are able to reap the same reward by turning the next bottom into their blessing. It’s all about seeing clearly what is coming so you can sell high and buy low. It is what can happen to those who see reality clearly and don’t live in economic denial like my crow who could only see what he wanted to see in praise of his choice for president. My lone crow on a wire, who scoffed at a good call because he didn’t like it, now looks like the fool I warned last summer he would prove to be. He has fallen off the wire because he hasn’t a leg left to stand on. All reports everywhere have come in against consistently month after month for over half a year.

(I’m not advising anyone as everyone’s particular situation is different – just saying what I’ve done, what I’m doing and why. I’m saying what I believed would happen and is now happening so you can weigh all risks and possible rewards for yourself in your own context and your own ability to take risk in order to do as you feel best.)

Here is a picture of where we are in our developing 2018-2019 housing market crash:

After 2018, we look about like this. 2018 pushed us just over the edge into a housing market crash that is as likely to continue sliding as the house in this picture at the top of a bluff that is giving way. (And I’ve seen places in Seattle that look exactly like that.)

Canada Housing Market Crash

One major difference between Housing Market Crash 2.0 and the last time is that this one is already global. The last one started in the US and mostly stayed in the US. This one is rapidly building in several nations because it is part of the bursting of the “Everything Bubble.”

Vancouver, June-July, 2018: Residential property sales fell 14.6% from June 2018 to July but a massive 30.1% from a year before. The 2,070 transactions that took place were the fewest since the end of the last millennium. Buyers and sellers were both reportedly sitting things out in confusion as to whether recent price gains would continue or whether the housing bubble had already burst. (As of August, prices had not started to drop.)

Sales of detached properties in July decreased 32.9% from a year before, and apartments dropped 26.5%. In fact, July’s sales were 29.3% below the 10-year average for July. Much of the plunge was attributed to Vancouver’s new law aimed at shutting out absentee Asian buyers that were ramming up housing prices while leaving the homes abandoned to become derelict in high-end neighborhoods. So, the decline is, in large part, intentional; but, if declining sales bring down prices, the dangers of falling prices to people who find themselves underwater and to their banks remain just as high.

The topping of the Canadian housing market looked like this:

Canadian market looks like a bus crashing into a brick wall.

Canadian market looks like a bus crashing into a brick wall.

January 2019: The B.C. Real Estate Association claimed the huge drop in British Columbia housing sales was due to mortgage stress testing. In spite of the plunge, prices are holding in the province, though no longer rising since last spring. Inventory is building to a level that will probably force prices down by or before summer.

Australia Housing Market Crash

Australia is faring even worse. Melbourne housing prices have plummeted at their fastest quarterly pace ever recorded! Less than two months ago, Australian housing regulators were warned to prepare “contingency plans for a severe collapse in the housing market” that could lead to a “crisis situation.” The Australian market peaked back in October 2017. It’s been downhill ever since with momentum now hitting break-neck speed. Sidney prices are down 12% from their peak.

Experts have been left stunned after Aussie house prices plunged at “the fastest rate of decline ever seen”. And there’s more pain to come…. “We have seen the downturn accelerate over the last three months. At 4 per cent down in Melbourne that’s the fastest rate of decline we’ve ever seen of any rolling three-month period, and Sydney is virtually (the fastest outside) a really brief period in the ’80s.” Sydney’s total decline is now the worst since [CoreLogic] began collecting records in 1980… One analyst has even tipped falls of up to 30 per cent, based on the revelation from the banking royal commission that almost all mortgages written between 2012 and 2016 … over-assess borrowing capacity.

News.com.au

The defaults will be cascading in soon. While Melbourne and Sidney are in an all-out housing crash, other cities in Australia are feeling the pinch, too. Every capital city marked declines, except Canberra. As in the US and Canada, the most expensive end of the market is taking the biggest fall first. Melbourne and Sidney, however, constitute half the value of Australia’s total housing market; so a drop in only those two cities if the plunge were isolated could still be devastating to Australian banks.

Hong Kong Housing Market Crash

Even the world’s hottest housing market is in decline. In stock market terms, one could say it has “entered a correction.” After its longest streak of falling values since 2016, the price of existing homes is down almost 10% from their August peak. This is actually seen by many, including some Chinese government officials, as relief to a market that had long run too hot.

The article above would have been one of my Premium Posts. Such articles are long to readbut are intended to present the most comprehensive overviews you’ll find anywhere. I chose to make this one available to all for two reasons: 1) to show the depth and breadth of Premium Post articles so readers can assess what they are like; and 2) because it concludes an argument made last summer over a prediction made almost two years ago for last summer.

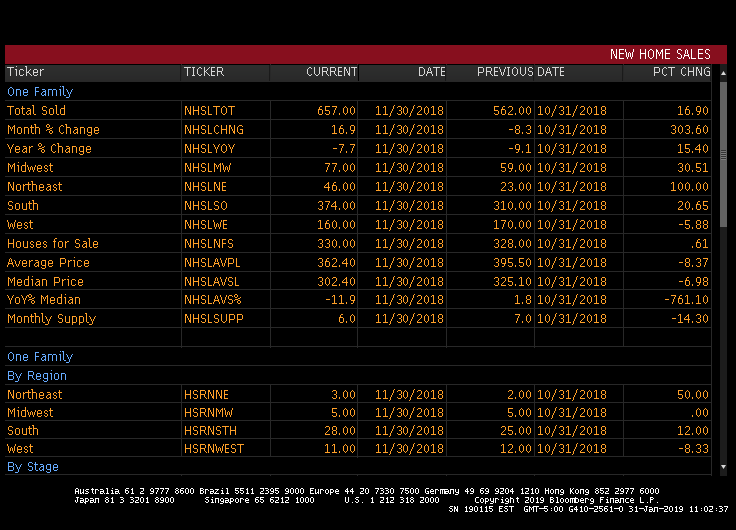

US New Home Sales Fall 7.7% YoY In November, But Rise 16.9% MoM, Most Since 1992 (Months Supply Still Elevated, Median Price Falls)

Let’s start with the +16.9% MoM number, a more cheery, pop the champagne bottle headline.

But on a YoY basis, new home sales fell 7.7% in November.

Months supply of new home sales fell in November, but are still at elevated levels.

And the median price of new home sales fell in November as The Fed’s normalization grabs the housing market with its icy grip.

“The weather started getting rough, the tiny ship was tossed….”

Source: by Anthony B. Sanders | Confounded Interest

***

November New Home Sales Surge By The Most Since 1992

…as the median price plunged to $302,400 – the lowest since Feb 2017…

US Pending Home Sales Fall 9.5% YoY In December To Lowest Level Since 2014 As Fed Unwinds

As The Federal Reserve continues to unwind its balance sheet, pending home sales YoY declined 9.5% YoY, the worst since 2014.\

Pending home sales got a big boost from The Fed’s third round of asset purchases (QE3), but PHS are feeling the pain of The Fed’s unwind.

***

US Pending Home Sales Crash Most In 5 Years

Following Case-Shiller’s report that home price gains are the weakest in four years, Pulte Homes’ CEO admission that 2019 will be a “challenging year,” and existing home sales carnage, Pending Home Sales were expected to very modestly rebound in December.

But they didn’t!

Pending home sales dropped 2.2% MoM (versus a 0.5% expected rise) to the lowest since 2014…

This is the 12th month in a row of annual sales declines… and the biggest annual drop in 5 years…

Yet another sign the housing market is struggling amid elevated property prices and borrowing costs – but there’s always hope…

“The stock market correction hurt consumer confidence, record high home prices cut into affordability and mortgage rates were higher in October and November for consumers signing contracts in December,” NAR Chief Economist Lawrence Yun said in a statement.

But with mortgage rates declining recently and the Fed less likely to raise borrowing costs, “the forecast for home transactions has greatly improved.”

Finally, the Realtors group forecasts a decline in annual home sales to 5.25 million this year from 5.34 million in 2018, which would mark the first back-to-back drops since the last recession.

Global Housing Markets From Hong Kong To Sydney Join Global Rout

It’s not just stocks: the global housing market is in for a rough patch, which has turned ugly for many homeowners and investors from Vancouver to London, with markets in Singapore, Hong Kong, and Australia already showing increased signs of softening.

Macro factors have triggered a global economic slowdown that is unraveling luxury marketplaces worldwide, according to Bloomberg. As a result, a turning point has been reached, with home prices globally now under pressure, and rising mortgage rates leading to depressed consumer optimism, while also triggering a housing affordability crisis, S&P Global Ratings said in a December report. To make matters worse, a simultaneous drop in house prices globally could lead to “financial and macroeconomic instability,” the IMF warned in a report last April.

While each metropolis globally has its distinct characteristics of what triggered its real estate slowdown, there are a few common denominators at play: rising borrowing costs, quantitative tightening, a crackdown on money laundering and increased government regulation, emerging market capital outflows and volatile financial markets. Bloomberg notes that there is also declining demand from Chinese buyers, who were the most powerful force in many housing markets globally over the course of this cycle.

“As China’s economy is affected by the trade war, capital outflows have become more difficult, thus weakening demand in markets including Sydney and Hong Kong,” said Patrick Wong, a real estate analyst at Bloomberg Intelligence.

One of the first dominoes to fall has been in Hong Kong, home values in the city have plummeted for 13 weeks straight since August, the longest losing streak since the 2008 financial crash, data from Centaline Property Agency show. Homeowners and investors have taken great caution due to a jump in borrowing costs, a looming vacancy tax, and the trade war that has derailed economic growth in mainland China.

“The change in attitude can be explained by a slowing mainland economy,” said Henry Mok, JLL’s senior director of capital markets. “Throw in a simmering trade war between China and the U.S., the government has taken actions to restrict capital outflows, which in turn has increased difficulties for developers to invest overseas.”