Big-Pharma, Chinese and Russian companies, and nefarious characters from around the world all benefited by licensing tech developed at the National Institutes of Health, all paid for by U.S. taxpayers.

Big-Pharma, Chinese and Russian companies, and nefarious characters from around the world all benefited by licensing tech developed at the National Institutes of Health, all paid for by U.S. taxpayers.

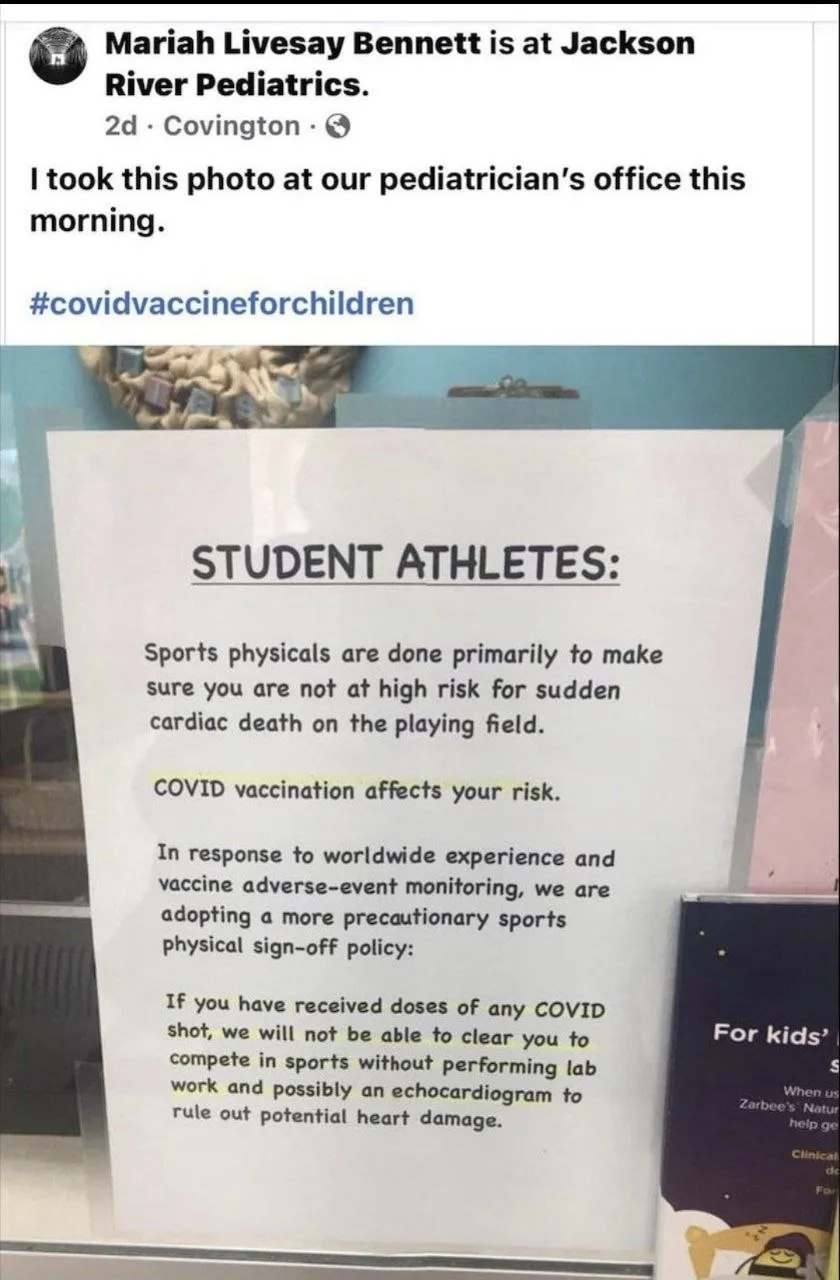

A pediatric practice breaks the awful truth about the risks of COVID “vaccination,” and a truthful lawyer beats the rap against her (“misconduct”)

https://markcrispinmiller.substack.com/p/if-dawn-is-breaking-in-kentucky-and

“The numbers of excess death, disabilities and lost work time since 2021 suggest that we have a pandemic right now that they’re not talking about because it’s the vaccine. If we had these numbers in 2020, it would have been heralded and stamped all over the media”

***

(Raw Egg Nationalist) Natural immunity is just as effective – if not more so – at protecting against COVID-19 Big Pharma vaccines, admits a new study in the Lancet medical journal. The about-face from the 200-year-old publication comes at the same time as the sudden change of heart amongst authorities regarding the origins of the virus.

(Raw Egg Nationalist) Natural immunity is just as effective – if not more so – at protecting against COVID-19 Big Pharma vaccines, admits a new study in the Lancet medical journal. The about-face from the 200-year-old publication comes at the same time as the sudden change of heart amongst authorities regarding the origins of the virus.

(Josh Stylman) It’s seemed evident for a while that the current fiat monetary system is, at best, unstable. At worst, it’s a Ponzi scheme whose time has expired. If that’s the case, I suspect the central bankers and 0.1% know this and might be prepared to usher in the new system before the old one collapses on itself – even as they loot it on the way down with the most significant wealth transfer in human history.

(Brian Shilhavy) A healthcare worker who claims she was injured by the Pfizer COVID vaccine she was required to receive as a condition for employment, and now suffers from CIDP (Chronic Inflammatory Demyelinating Polyneuropathy) which she says has changed her life completely, recently went public to answer a question that apparently others in her social media network have asked her: “What do you think about people who have refused the COVID vaccine?”

(Jim Hoft) Former Clinton adviser and COVID Vaccine critic Naomi Wolf joined Steve Bannon on The War Room on Monday morning. Naomi shared her latest bombshell from her investigation into the Pfizer vaccine documents released by the US government on their COVID vaccine testing. Naomi’s team of investigators, doctors and attorneys identified several US government documents that confirm that Pfizer was adding varying amounts of active ingredient to their experimental COVID vaccines. According to the data, the range of dangerous active ingredient went from 3μg, to 10μg, to 30μg, to 100μg depending on the batch they happened to inject you with.

(Stephanie Seneff and GreenMedInfo) Since December 2020, when several novel unprecedented vaccines against SARS-CoV-2 began to be approved for emergency use, there has been a worldwide effort to get these vaccines into the arms of as many people as possible as fast as possible. These vaccines have been developed “at warp speed,” given the urgency of the situation with the COVID-19 pandemic. Most governments have embraced the notion that these vaccines are the only path towards resolution of this pandemic, which is crippling the economies of many countries.

(Cristina Laila) Governor Gavin Newsom on Thursday unveiled California’s “endemic” virus policy – and it’s going to cost billions and billions, and billions of dollars in pork spending.

The Centers for Disease Control has finally admitted that natural immunity from prior infection exists. But it’s even worse than that for the COVID-19 narrative: The CDC also admits that natural immunity from prior infections is superior to vaccinated immunity alone.

An Airbnb listing hidden deep within western Montana’s woods has been taken down after it discriminated against vaccinated people with “COVID misinformation.”

The information here has been summarized from the website No Jab For Me which provides source links and stands by their information.

Statements in this site are substantiated with facts that will stand in a court of law. Informed Consent requires a flow of information. Click on the hyperlinked sections to direct you to primary sources such as CDC, WHO, FDA documents.

In this interview with The New American magazine’s Senior Editor Alex Newman, lawyer and doctor Richard Fleming offers the documentation proving that the U.S. government and key Americans played a critical role in supporting the research that weaponized viruses to eventually create COVID19 at the Wuhan Institute of Virology. He even names names, such as Ralph Baric at the University of North Carolina, and gives grant numbers from U.S. government institutions. Dr. Fleming argues that the perpetrators must be prosecuted for their crimes, and that all of the necessary evidence is already available.

🇺🇸 The New American:

http://www.thenewamerican.com/

Dr. Richard Fleming, physicist-nuclear cardiologist, issued a warning that experimental covid vaccines are not effective, but could cause Mad Cow disease.

“In the animal model, they develop spongiform and Mad Cow disease,” Fleming said. “We also know 2 weeks afterwards they develop…what causes Alzheimer’s and neurological disorders.”

Fleming warned the effects could take a year and half to show in humans.

Fleming, who in the 1990s discovered inflammation causes cardiovascular disease, said man-made spike proteins in the vaccines also cause inflammation. The Johnson & Johnson vaccine was pulled for its link to blood clots in women.

The vaccines have “no statistically significant benefit,” Fleming said, but cause “inflammation and blood clotting, Lewy bodies [associated with dementia], Mad Cow disease, and nothing to benefit.”

The risk of contracting SARS-CoV-2 infection from contact with a contaminated surface is less than a 1 in 10,000, according to revised CDC guidance.

The Covid 19 (CV-19) headlines out so far this week are downright confusing and contradictory. One says “Covid-19’s Fourth Wave is hitting the U.S Hard.” Another says, “Texas Hits Record Low Covid Cases 3 Weeks After Lifting All Pandemic Restrictions.” What are you to believe? The mainstream media (MSM), CDC and most politicians have been lying about almost everything. The idea they are pushing that only a vaccine is the answer to what many people call a “Plandemic” is a huge lie. Let me prove it.

Please join Greg Hunter of USAWatchdog.com as he posts three videos: An intro- duction video by Hunter along with two “must watch” videos by top experts, so you can be informed about taking a vaccine (or not) or a treatment that can save your life. Big Tech, MSM and the CDC do not want you to hear what these experts have to say.

(Suzanne Hanmer) Several prominent physicians, doctors, Sons of Liberty Media Health and Wellness expert Kate Shemirani, her colleague Dr. Kevin Corbett, and I have postulated that the current experimental mRNA injection for coronavirus, aka COVID-19, could alter one’s genetic code or DNA. Bill Gates stated it, which was included in my video “Human Genome 8 and mRNA Vaccine” on Brighteon.com. It is one reason the term “experimental human genome altering mRNA injection” has been used to describe the jab being foisted onto the mostly unsuspecting public. While many in the media, including Dr. Anthony Fauci and his merry band of chronic liars, and “fact checkers” have declared this claim as false, a video of a TEDx Beacon Street talk by Tal Zaks, chief medical officer of Moderna, Inc., one pharmaceutical company manufacturer of the experimental mRNA technology injection, confirms mRNA injection for COVID-19 can change your genetic code or DNA. This TEDx Beacon Street talk occurred in 2017. H/T to YouTube channel Silview Media Backup Channel.

(Max Blumenthal) The Joseph Biden administration has named Richard Nephew as its Deputy Iran Envoy. As the former Principal Deputy Coordinator of Sanctions Policy for Barack Obama’s State Department, Nephew took personal credit for depriving Iranians of food, sabotaging their automobile industry and driving up unemployment rates. He has described the destruction of Iran’s economy as “a tremendous success,” and lamented during a visit to Russia that food was still plentiful in the country’s capital despite mounting US sanctions.

…If you don’t stay locked in your bedroom in favor of going about your life – still masked, scrubbed and distanced – you’re a fool… “crisis” and desperation have replaced “challenge” and problem solving…

(Rocky Swift) – Japanese supercomputer simulations showed that wearing two masks gave limited benefit in blocking viral spread compared with one properly fitted mask.

The findings in part contradict recent recommendations from the U.S. Centers of Disease Control and Prevention (CDC) that two masks were better than one at reducing a person’s exposure to the coronavirus.

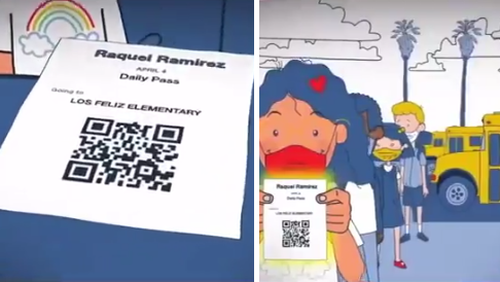

The Los Angeles Unified School District is launching a Microsoft-developed COVID-tracking app for children, which allows students to schedule and view the results of weekly COVID tests, post the results of off-campus COVID tests, and schedule vaccinations.

Shortly after Gov. Abbott’s decision to follow the science and allow the people of his state to be ‘free’ to judge their own risks once again, none other than California Gov. Newsom – desperate to virtue-signal as he fights for political survival amid an imminent recall vote – had a two word response: “Absolutely reckless”

We have two words for Mr. Newsom… can you guess?

(National File) During a recent television appearance on MSNBC, White House Senior COVID Response Advisor Andy Slavitt, who does not possess a medical background admitted the fact that California and other blue states under lockdown cannot record better infection numbers than comparatively free Florida is “just a little beyond our explanation.”

https://twitter.com/Breaking911/status/1362176548661583877?ref_src=twsrc%5Etfw

Officially, China has no specific policy for vaccinated travelers, according to Reuters.

Woman on the Yangtze River Bridge in Wuhan, China… Getty Images

China is reportedly denying entry to individuals who have taken the Pfizer and Moderna vaccines, Adam Curry of the “No Agenda” podcast claimed.

Physicians’ white paper says injection prohibited for the young and at least discouraged for healthy individuals under 70 years of age. ‘Unethical’ to advocate vaccine for persons under 50.

(Patrick Delaney) In an extraordinary recent presentation exposing “the serious and life-threatening disinformation campaign” being waged against the American people and the world, Dr. Simone Gold of the American Frontline Doctors (AFLD) laid out the facts on the Wuhan Virus, safe highly-effective treatments, and particularly what she calls “experimental biological agents,” otherwise referred to as the COVID-19 vaccines.

Continue reading

(Jeffrey A. Tucker) What a glorious thing the reopening is! After nearly a year of darkening times, the light has begun to dawn, at least in the U.S.

Given how incredibly political this pandemic has been from the beginning, many people smell a rat. Is it really the case that the reopening of the American economy, particularly in blue states, is so perfectly timed? Do the science and politics really line up so well?

(John Tanmy) It’s been said off and on over the decades that California is a bellwether of sorts. What happens there is a preview of what’s going to happen elsewhere in the U.S.

“I’m not willing to give up without a fight — I’m just not.” – Annie Rammel, Carlsbad, CA restaurant owner.

In the late 1970s the passage of Proposition 13 foretold a national tax revolt. Californians used a referendum to limit the tax power of grasping politicians in the Golden State, and the push back eventually went national.

A different, more local revolt began last weekend in Carlsbad, CA, a town just north of San Diego. Its restaurant and bar owners decided they’re weren’t going to take it anymore. They’re no longer going to allow witless politicians to destroy what they’ve worked so long to build. They’re going to open their businesses to eager customers.

European equities slumped to near one-month lows on Thursday, as soaring COVID-19 cases across the continent weighed on sentiment. In recent months, virus cases have spiked across Europe, with Spain becoming the first country on the continent to surpass the one million infection mark. At the same time, Italy has just set a record increase in daily cases.

The surge in European coronavirus cases has shifted sentiment lower for businesses, with downside risks emerging for the continent’s economy in the fourth quarter.

Bloomberg, citing a new McKinsey & Co. survey conducted in August, describes a particularly gloomy outlook for Europe’s small and medium-sized businesses, warns that at least half of them could enter into bankruptcy proceedings in the next year if revenues continue to stagnate.

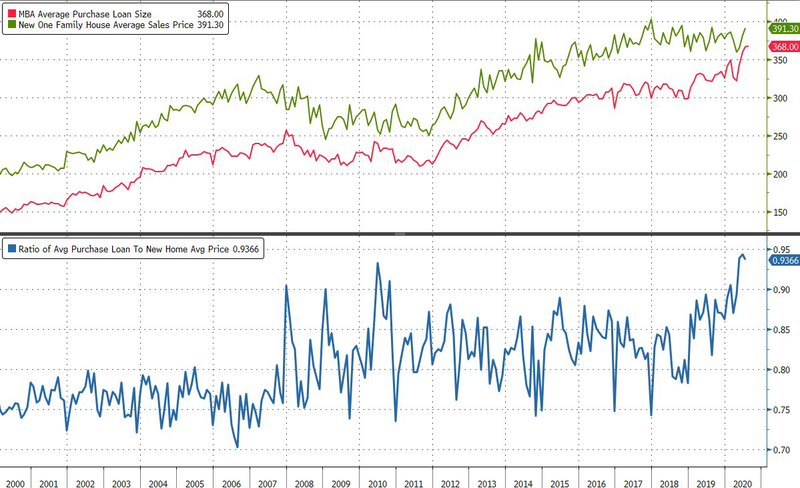

As we noted last month, the US housing market is reflecting the extremes of the economy right now – between those who can’t make ends meet due to the pandemic, and those who are either still employed, are sitting on a pile of equity, or both.

One one end of the spectrum you’ve got affluent borrowers locking in record-low rates, while mortgage originations reached a record $1.1 trillion in the second quarter as rates on 30-year mortgages dipped below 3% for the first time in history in July, according to Bloomberg.

Meanwhile, refis may just be getting started.

There are still nearly 18 million homeowners with good credit and at least 20% equity who stand to cut at least 0.75% off their current rate by refinancing, according to Ben Graboske, president of Black Knight data and analytics.

“We would expect near-record-low interest rates to continue to buoy the market,” he said in a statement Tuesday. –Bloomberg

What’s impressive is that the quarterly spike in new mortgage originations occurred while under nationwide public health measures that restricted home showings, appraisals, and in-person document signings, according to the report. That said, refis accounted for around 70% of home loans issued during the period.

Also notable is that the average loan-to-value ratio is above 90%, as borrowers are having no trouble securing loans with just 10% or less down.

At the other end of the spectrum, mortgage delinquencies are up 450% from pre-pandemic levels, with around 2.25 million mortgages at least 90 days late in July – the most since the credit crisis, according to Black Knight, Inc.

“The money is in the homes and people with college education are still working, but the pain is being felt where people are unemployed,” said Wharton real estate professor, Susan Wachter, adding “COVID-1984 will drive an increase in the already high income-inequality gap, and wealth inequality, actually, which is much more extreme.”

While the unemployment rate fell to 8.4% in August, more than 11 million jobs were still lost in the pandemic, the Labor Department reported last week. Supplemental benefits for the unemployed of $600 a week expired in July and Congress has been at an impasse over a follow-up aid package. –Bloomberg

More findings from Black Knight (via Bloomberg):

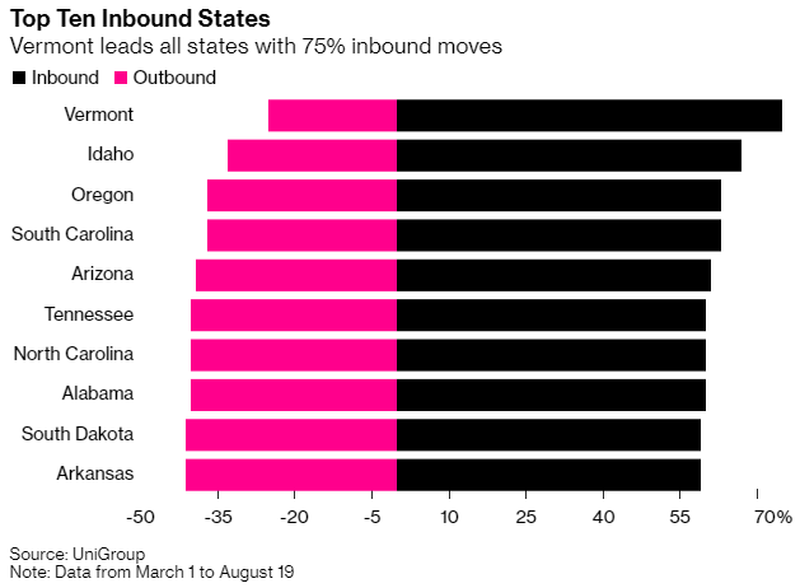

The plandemic-induced summer of escape from New York continues at a moment violent crime is on the rise, restaurant and public venue closures make the city less appealing, public transit is reeling in debt, and remote working set-ups are giving those with means greater mobility.

More worrisome trends… or rather signs of the times signalling that for many the gentrified Big Apple has as one family recently put it reached its “expiration date”. Two separate NY Times reports on Sunday detailed that moving companies are so busy they’re in an unprecedented situation of having to turn people away, while simultaneously the suburbs are witnessing an explosion in demand “unlike any in recent memory”.

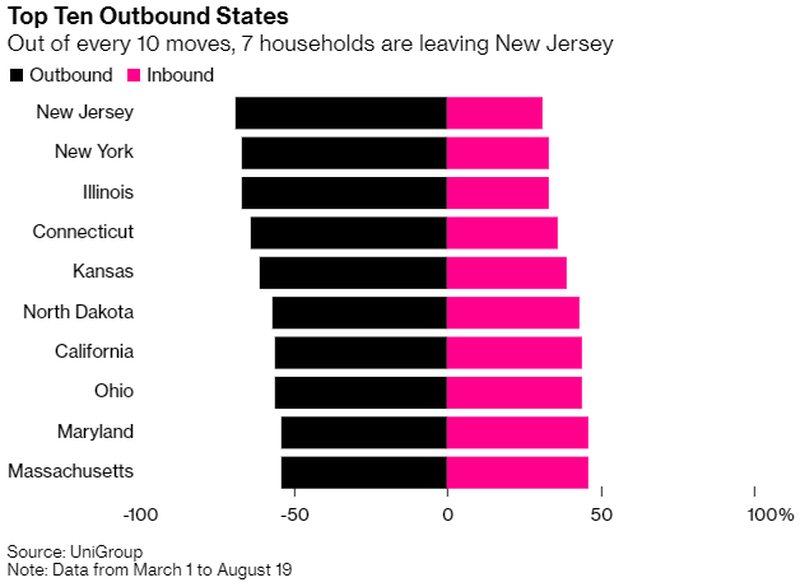

And then there’s fresh data showing that during the plandemic Americans are fast getting the hell out of the more expensive “real estate meccas” of New York and New Jersey.

First, New York City moving are reporting a rush of customers so high it feels like “move out day on a college campus”:

According to FlatRate Moving, the number of moves it has done has increased more than 46 percent between March 15 and August 15, compared with the same period last year. The number of those moving outside of New York City is up 50 percent — including a nearly 232 percent increase to Dutchess County and 116 percent increase to Ulster County in the Hudson Valley.

“The first day we could move, we left,” a dentist was cited as saying of the moment movers were declared an “essential service” by Gov. Cuomo late March. Her family moved to Pennsylvania where they had relatives.

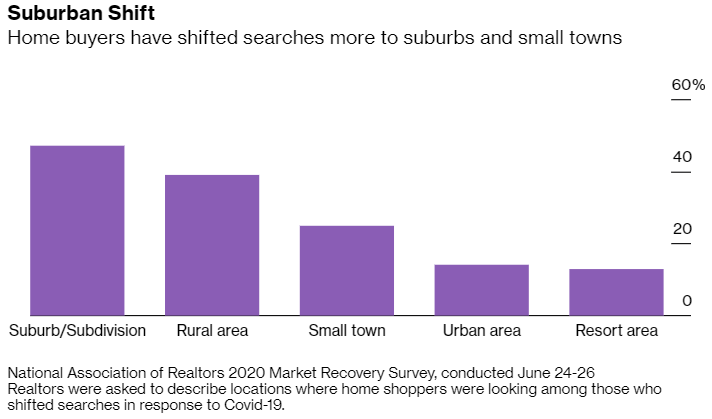

And second, the Times details the unprecedented boom in the suburban real estate as an increasingly online workforce is fed up with closures in the city, losing its appeal and vibrancy.

July alone witnessed a whopping 44% increase in home sales among suburban counties near NYC compared to the same month last year, as the report details:

Over three days in late July, a three-bedroom house in East Orange, N.J., was listed for sale for $285,000, had 97 showings, received 24 offers and went under contract for 21 percent over that price.

On Long Island, six people made offers on a $499,000 house in Valley Stream without seeing it in person after it was shown on a Facebook Live video. In the Hudson Valley, a nearly three-acre property with a pool listed for $985,000 received four all-cash bids within a day of having 14 showings.

Since the pandemic began, the suburbs around New York City, from New Jersey to Westchester County to Connecticut to Long Island, have been experiencing enormous demand for homes of all prices, a surge that is unlike any in recent memory, according to officials, real estate agents and residents.

They’re not just fleeing for the suburbs or upstate, but also to the significantly cheaper and lower cost of living areas of the country like Texas, Florida, South Carolina, and Oregon, or to rural areas.

COVID-1984 is fast reviving American mobility on scales reminiscent of the mid-20th century. Bloomberg describes separately that“Far more people moved to Vermont, Idaho, Oregon and South Carolina than left during the pandemic, according to data provided to Bloomberg News by United Van Lines.”

“On the other hand, the reverse was true for New York and New Jersey, which saw residents moving to Florida, Texas and other Sunbelt states between March and July,” the report finds.

General fear of living in densely populated areas, better enterprise video communications platforms making possible fully remote workplaces which in some cases are ‘canceling’ the traditional office space altogether, and a lack of nightlife or entertainment allure of big cities is driving the exodus.

In addition to the aforementioned states, “Illinois, Connecticut and California, three other states with big urban populations, were also among those losing out during the plandemic,” according to United Van Lines data.

Former hedge fund manager and entrepreneur James Altucher says New York City is dead and it’s not coming back.

Born and bred in New York, Altucher took his family and fled to Florida after the Black Lives Matter riots in June when someone tried to break into his apartment.

Since then, the city has continued to suffer a huge surge in shootings and violent crime as well as an anemic financial recovery from the coronavirus lock down.

Appearing on Fox News Business, Altucher referred to images that were broadcast during the interview showing 6th avenue to be virtually empty.

“We have something like 30 to 50 per cent of the restaurants in New York City are probably already out of business and they’re not coming back,” he pointed out.

Altucher said that despite offices in midtown being allowed to be open, they’re still largely empty because companies like Citigroup, JP Morgan, Google, Twitter and Facebook are encouraging their employees to work remotely from home “for years or maybe permanently.”

“This completely damages not only the economic eco-system of New York City…but what happens to your tax base when all of your workers can now live anywhere they want to in the country?” asked the entrepreneur, noting that many were fleeing to places that are cheaper to live like Nashville, Austin, Miami and Denver.

Warning that the situation was “only going to get worse,” Altucher said that the old New York was not coming back and that creative and business opportunities would now be dispersed throughout the entire country.

“What makes this different now is bandwidth is ten times faster than it was in 2008 so people can work remotely now and have an increase in productivity,” he added.

As we document in the video below, the blame for all this lies firmly at the feet of two people, Governor Cuomo and Mayor de Blasio.

Without anyone left to pay for the city, the Big Apple is headed for a failed state.

The separateness in New York, and by extension much of the nation curled around it from America’s eastern edge, stands out. There are the hyper-wealthy and there are the multi-generational poor. They depend on each other, but with COVID who needs who more has changed.

It’s easy to stress how far apart the rich and the poor live, even though the mansions of the Upper West Side are less than a mile from the crack dealers uptown. The rich don’t ride public transportation, they don’t send their kids to public schools, they shop and dine in very different places with private security to ensure everything stays far enough apart to keep it all together.

But that misses the dependencies which until now have simply been a given in the ecosystem. The traditional view has been the rich need the poor to exploit as cheap labor—textbook economic inequality. But with COVID as the spark, the ticking bomb of economic inequality may soon go off in America’s greatest city. Things are changing and New York, and by extension America, needs to ask itself what it wants to be when it grows up.

It’s snapshot simple. The wealthy and the companies they work for pay most of the taxes. The poor consume most of the taxes through social programs. COVID is driving the wealthy and their offices out of the city. No one will be left to pay for the poor, who are stuck here, and the city will collapse in the transition. A classic failed state scenario.

New York City is home to 118 billionaires, more than any other American city. New York City is also home to nearly one million millionaires, more than any other city in the world. Among those millionaires some 8,865 are classified as “high net worth,” with more than $30 million each.

They pay the taxes. The top one percent of NYC taxpayers pay nearly 50 percent of all personal income taxes collected in New York. Personal income tax in the New York area accounts for 59 percent of all revenues. Property taxes add in more than a billion dollars a year in revenue, about half of that generated by office space.

Now for how the other half lives. Below those wealthy people in every sense of the word the city has the largest homeless population of any American metropolis, which includes 114,000 children. The number of New Yorkers living below the poverty line is larger than the population of Philadelphia, and would be the country’s 7th largest city. More than 400,000 New Yorkers reside in public housing. Another 235,000 receive rent assistance.

That all costs a lot of money. The New York City Housing Authority needs $24 billion over the next decade just for vital repairs. That’s on top of a yearly standard operating cost approaching four billion dollars. A lot of the money used to come from Washington before a multi-billion dollar decline in federal Section 9 funds. So today there is a shortfall and repairs, including lead removal, are being put off. NYC also has a $34 billion budget for public schools, many of which function as distribution points for child food aid, medical care, day care, and a range of social services.

New York’s Governor Andrew Cuomo has seen a bit of the iceberg in the distance. He recently took to MSNBC to beg the city’s wealthy, who fled the coronavirus outbreak, to return. Cuomo said he was extremely worried about New York City if too many of the well-heeled taxpayers who fled COVID decide there is no need to move back.

“They are in their Hamptons homes, or Hudson Valley or Connecticut. I talk to them literally every day. I say. ‘When are you coming back? I’ll buy you a drink. I’ll cook. But they’re not coming back right now. And you know what else they’re thinking, if I stay there, they pay a lower income tax because they don’t pay the New York City surcharge. So, that would be a bad place if we had to go there.”

Included in the surcharge are not only NYC’s notoriously high taxes. The recent repeal of the federal allowance for state and local tax deductions (SALT) costs New York’s high earners some $15 billion in additional federal taxes annually.

“They don’t want to come back to the city,” Partnership for NYC President Kathryn Wylde warned. “It’s hard to move a company… but it’s much easier for individuals to move,” she said, noting that most offices plan to allow remote work indefinitely. “It’s a big concern that we’re going to lose more of our tax base then we’ve already lost.”

While overall only five percent of residents left as of May, in the city’s very wealthiest blocks residential population decreased by 40 percent or more. The higher-earning a neighborhood is, the more likely it is to have emptied out. Even the amount of trash collected in wealthy neighborhoods has dropped, a tell-tale sign no one is home. A real estate agent told me she estimates about a third of the apartments even in my mid-range 300 unit building are empty. The ones for sale or rent attract few customers. She says it’s worse than post-9/11 because at least then the mood was “How do we get NYC back on its feet?” instead of now, when we just stand over the body and tsk tsk through our masks.

Enough New Yorkers are running toward the exits that it has shaken up the greater area’s housing market. Another real estate agent describes the frantic bidding in the nearby New Jersey suburbs as a “blood sport.” “We are seeing 20 offers on houses. We are seeing things going 30 percent over the asking price. It’s kind of insane.”

Fewer than one-tenth of Manhattan office workers came back to the workplace a month after New York gave businesses the green light to return to the buildings they ran from in March. Having had several months to notice what not paying Manhattan office rents might do for their bottom line, large companies are leaving. Conde Nast, the publishing company and majority client in the signature new World Trade Center, is moving out. Even the iconic paper The Daily News (which published the famous headline “Ford to City: Drop Dead” when New York collapsed in 1975 without a federal bailout) closed its physical newsroom to go virtual. Despite the folksy image of New York as a paradise of Mom and Pop restaurants and quaint shops, about 50 percent of those who pay most of the taxes work for large firms.

Progressive pin-up Mayor De Blasio has lost touch with his city. After years of failing to address economic inequality by simply throwing free money to the poor and limiting the ability of the police to protect them, and us, from rising crime, his COVID focus has been on shutting down schools and converting 139 luxury hotels to filthy homeless shelters. Alongside AOC, he has called for higher taxes on fewer people and demanded more federal funds. As for the wealthy who have paid for his failed social justice experiments to date, he says “We don’t make decisions based on a wealthy few. Some may be fair-weathered friends, but they will be replaced by others.”

What others? The concentration of major corporations once pulled talent to the city from across the globe; if you wanted to work for JP Morgan on Wall Street, you had to live here. That’s why NYC has skyscrapers; a lot of people once needed to live and especially work in the same place. Not any more. Technology and work-at-home changes have eliminated geography.

For the super wealthy, New York once topped the global list of desirable places to live based on four factors: wealth, investment, lifestyle and future. The first meant a desire to live among other wealthy people (we know where that’s headed), investment returns on real estate (not looking great, if you can even find a buyer), lifestyle (now destroyed with bars, restaurants, shopping, museums, and theaters closed indefinitely, coupled with rising crime) and…

The future. New York pre-COVID had the highest projected GDP growth of any city. Now we’re left with the question if COVID continues to hollow out the city, who will be left to pay for New York? As one commentator said, NYC risks leading America into becoming “Brazil with Nukes,” a future of constant political and social chaos, with a ruling class content to wall itself off from the greater society’s problems.

(Denise Lones) There are many ways to react about the virus breakout. It doesn’t seem to matter where you go – the news is talking about it everywhere. It is completely normal to feel concerned, unsure, nervous, worried, and more.

However, the reality is that there is not a lot that any of us can do about the virus other than be informed and be aware of the things that we can do to keep ourselves and our families safe. From a business perspective it may seem like there is a lot of doom and gloom out there, but there are many things you could be doing to keep yourself busy and productive.

If you find yourself more home bound than usual, there are some things that you can do to make that time productive. You can:

While it may feel like the world is slowing down and that real estate may come to a screeching halt, that is just not realistic, and it is not worth worrying about. Stop panicking and start taking action to catch up on projects or to help your potential buyers and sellers plan to do the things that they haven’t had time to do. How many times does a seller tell you that they can’t put their home on the market until they paint a room or put away their belongings or do a deep cleaning? This could be the perfect time for them to complete this project that never seems to make it into their regular schedule.

While the rest of the world may be focusing on only the negative try to keep your mind focused on something more positive and productive. Sit down and make a list of all the projects you would love to complete and then start tackling them.

Don’t spend your time focusing on the “what ifs” of this virus. Focus on what you have control over which is making a huge dent in the things you have been putting off. It is normal to worry, but try to put things into a more positive light.

While mom and dad on Main St. still aren’t getting the dire warning that the coronavirus has been offering up to Asia and the rest of the Eastern world over the last several weeks, perhaps a light bulb will finally go off when Jane Q. Public heads to the grocery store and is unable to buy shampoo and toothpaste.

Proctor and Gamble, one of the world’s biggest “everyday product” manufacturers, has now officially warned that 17,600 of its products could be affected and disrupted by the coronavirus. The company’s CFO, Jon Moeller, said at a recent conference that P&G used 387 suppliers across China, shipping more than 9,000 materials, according to CIPS.org.

Moeller said: “Each of these suppliers faces their own challenges in resuming operations.”

And it’s not just everyday consumer goods that are going to feel the impact of the virus.

Smartphones and cars are so far among the consumer products that have been hardest hit from the virus. In fact, according to TrendForce, “forecasts for product shipments from China for the first quarter of 2020 had been slashed, by 16% for smartwatches (to 12.1m units), 12.3% for notebooks (30.7m units) and 10.4% for smartphones (275m units). Cars have dropped 8.1% (19.3m units).”

Their report states: “The outbreak has made a relatively high impact on the smartphone industry because the smartphone supply chain is highly labor-intensive. Although automakers can compensate for material shortage through overseas factories, the process of capacity expansion and shipping of goods is still expected to create gaps in the overall manufacturing process.”

A separate coronavirus analysis by Mintec says that “Chinese demand for copper (it has hitherto been responsible for consuming half the world’s output), will fall by 500,000 tonnes this year, and falls in demand have already impacted prices. From December to January the price of copper fell 9.6%.”

The report notes: “Millions of people have been affected by the travel lock down in Hubei province, the centre of the outbreak. This has been responsible for a glut of jet fuel and diesel on global markets at a time when petroleum supplies were already abundant.”

Other products that have been negatively affected so far include pork, which is up 11% this month, chicken, garlic and dried ginger.

Product supply chain issues could eventually compound hysteria at supermarkets if coronavirus becomes widespread in western countries. Northern Italy, which has seen a small outbreak of coronavirus cases over the last 48 hours, is already experiencing long lines and sold out store shelves.

In the last few weeks, ZeroHedge provided many articles on the evidence of creaking global supply chains fast emerging in China and spreading outwards. Anyone in supply chain management, monitoring the flow of goods and services from China, has to be worried about which regions will be impacted the most (even if the stock market couldn’t care less).

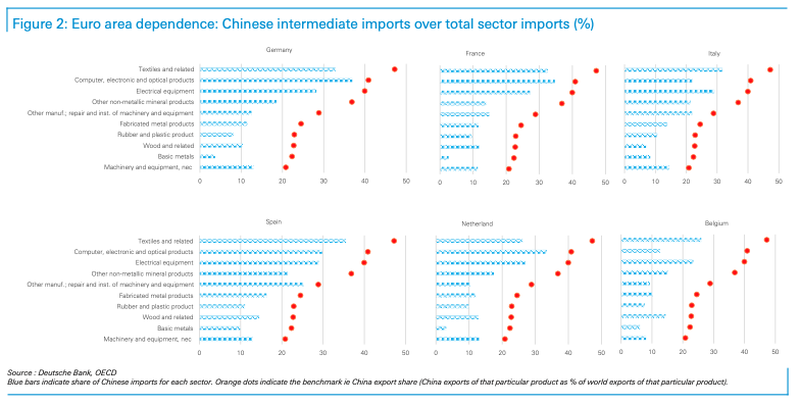

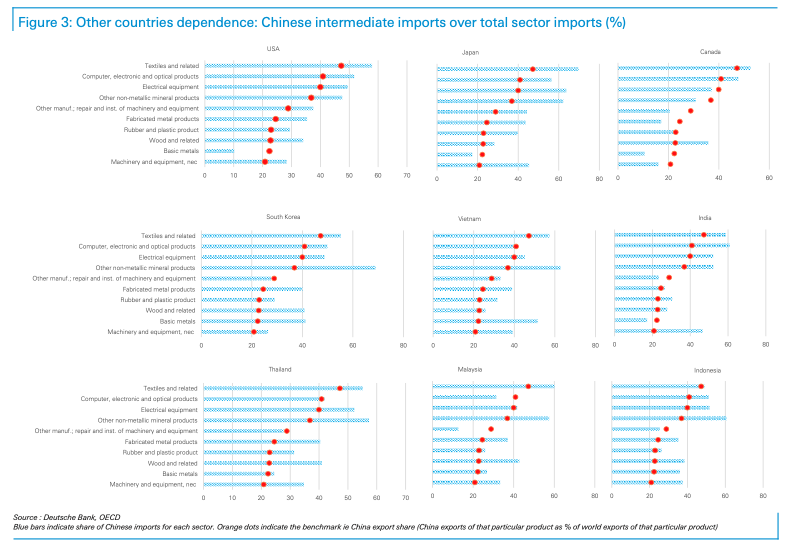

Deutsche Bank’s senior European economist Clemente Delucia and economist Michael Kirker published a note on Thursday titled “The impact of the coronavirus: A supply-chain analysis” identifying the effect of contagion on the rest of the world, mainly focusing on demand and spillover effects into other countries.

The economists constructed a ‘dependency indicator,’ to figure out just how much a country depends on China for the supply of particular imported inputs. It was noted that the more a country depends on China, the more challenging it could be for businesses to find alternative sourcing during a period of supply chain disruptions.

The biggest takeaway from the report is that, surprisingly, the European Union is less directly exposed to a China supply-chain shock than the US, Canada, Japan, and all the major Asian countries (i.e., India, South Korea, Indonesia, Malaysia, Vietnam).

It was determined that in the first wave of supply chain disruptions that “euro-area countries are somewhat less directly dependent on China for intermediate inputs than other major economies in the rest of the world.”

“The euro-area countries have, in general, a dependence indicator below the benchmark. This suggests that euro-area countries have a below-average direct dependence on Chinese imports of intermediate inputs (Figure 2).”

But since China is highly integrated into the global economy, and a supply chain shock would be felt across the world. The second round of disruptions would result in lower world trade growth that would eventually filter back into the European economy.

The US, Japan, Canada, and all the major Asian countries would feel an immediate supply chain shock from China.

Here’s a chart that maps out lower dependency and higher dependency countries to disruption from China.

To summarize, the European Union might escape disruptions from China supply chain shocks in the first round, but ultimately will be affected as global growth would sag. As for the US and Japan, Canada, and all the major Asian countries, well, the disruption will be almost immediate and severe with limited opportunities for companies to find alternative sourcing.

“First of all, our analysis does not take into account non-linearity in the production process. In other words, it does not capture consequences from a stop in production for particular product. It might indicate that given the dependence is smaller, Europe could find it somewhat easier substitute a Chinese product with another. But there is no guarantee this will be the case.”

“Secondly, while our results indicates that the direct impact from supply issues in China could be smaller for the euro area than for other regions in the world, the euro area could be hard-hit by second-round effects. With their higher direct exposure to China, production in other major economies could slow down as a result of disruptions in the supply chain. This not only could cause a shortage in demand for euro-area exports, but it could also impact on the euro-area’s import of intermediate inputs from these other countries (second-round effects). In other words, China has become a relevant player in the world supply chain and production/demand problems in China are spread worldwide through direct and indirect channels.“

News flow this week has indeed suggested the virus is spreading outwards, from East to West, and could get a lot worse ex-China into the weekend.

We believe supply chain disruptions ex-China could become more prevalent in the weeks ahead.

The mistake of the World Health Organization (WHO), governments, and global trade organizations to minimize the economic impact (protect stock markets) of the virus was to allow flights, businesses, and trade to remain open with China. This allowed the virus to start spreading across China’s Belt and Road Initiative (BRI).

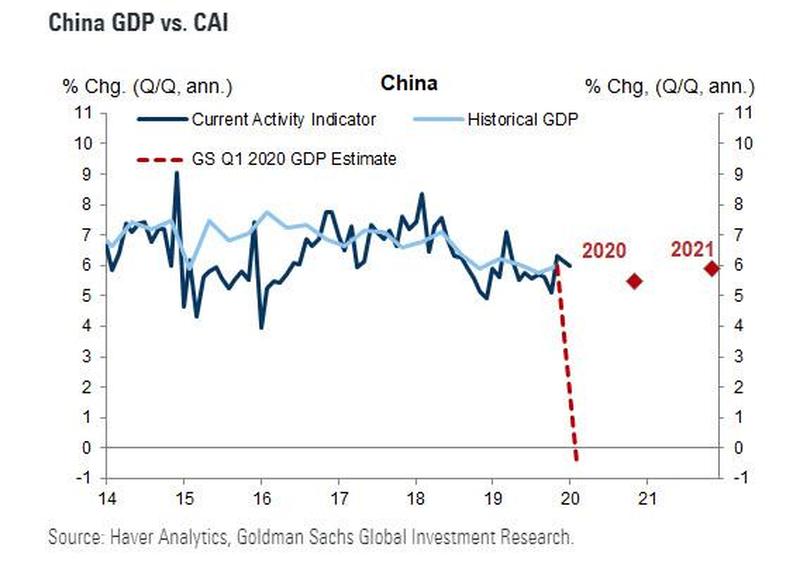

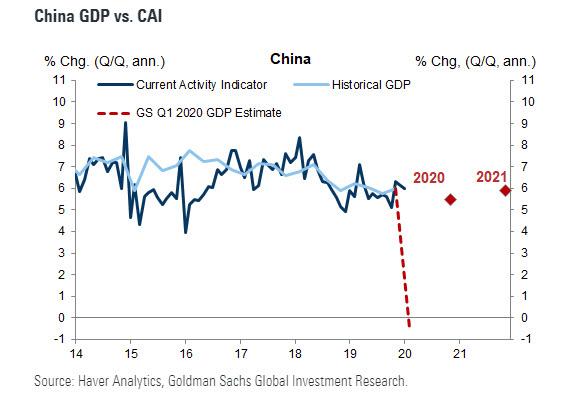

Now that Apple has broken the seal and made it abundantly clear that China’s economic collapse which could push its Q1 GDP negative according to Goldman as the second largest world economy grinds to a halt (as described here last week)…

… will have an adverse impact on countless supply-chains, which in today’s “just in time” delivery environment, are absolutely critical for keeping the global economy running smoothly (for a quick reminder of what happens when JIT supply chains stop functioning read our article from 2012 “”Trade-Off”: A Study In Global Systemic Collapse“), attention on Wall Street has turned to which other US sectors stand to be adversely impacted should the coronavirus pandemic not be contained on short notice and China’s economy crisis transforms into a supply shock.

Conveniently, Goldman Sachs just did this analysis.

New evidence from Bloomberg reveals cracking global supply chains are fast emerging at major Chinese ports with thousands of containers of frozen meat piling up with nowhere to go.

The Covid19 outbreak will remain a dominant issue for 1Q as supply chain shocks are being felt by multinationals on either side of the hemisphere.

Sources told Bloomberg that containers of frozen pork, chicken, and beef (mostly from South America, Europe, and the US) are piling up at Tianjin, Shanghai, and Ningbo ports because of the lack of truck drivers and many transportation networks remain closed.

Seaports in China are quickly running out of room to house the containers and cannot provide enough electricity points to keep existing containers cold. This has forced many vessels to be rerouted to other destinations.

We’ve already noted that Bloomberg’s Stephen Stapczynski recorded footage of an oil tanker parking lot off the Singapore coast last week as refiners in China cut runs as crude consumption has collapsed by more than 4 million barrels per day.

It’s clear that a logistical nightmare is unfolding as two-thirds of the Chinese economy has effectively shut down much of its production capacity, producing a massive “demand shock.”

The impact on the global economy is already dragging down world trade and could force the World Trade Organization (WTO) to slash economic growth forecasts for the year.

The Chinese economy constitutes about 20% of global GDP, and supply chain disruptions across China could cause a cascading effect that could tilt the world into recession.

But it’s not just frozen meats piling up at Chinese ports or a crude glut developing. There’s a high risk that product shortages to Western countries could be 60-90 days out.

Alibaba Group’s CEO Daniel Zhang warned last week that the supply chain disruption, or “shock,” is a “black swan event” for the global economy.

The “black swan” warning was also repeated by Freeport-McMoRan CEO Richard Adkerson several weeks ago after he said the outbreak of the virus in China is a “real black swan event.”

China’s economy is at a standstill and could trigger the next economic crisis, not seen since 2008.

It’s not only Chinese tourists, business travelers, and property buyers who’re not showing up, but also travelers from all over the world who’ve gotten second thoughts about sitting on a plane.

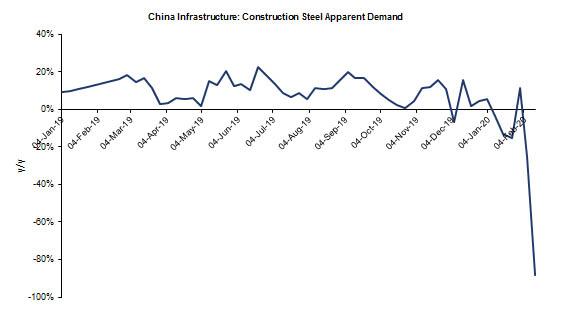

Literally, everything is shutting down. I can’t even fit everything into the title. First, The world’s largest Hotel company by properties announced they will be temporarily closing 1,000 Hotels in China. This amounts to over 70% of their hotels and the CEO said the Hotels that remain open are running under 75% Guest capacity. They expect a huge financial impact. Hilton hotels also announced they will be closing 150 hotels in China along with Best Western. We then move to the recent data compiled by Goldman detailing the true weight of the industrial production halt. Steel demand is Crashing, Construction Steal demand has collapse 88%. Fiat Chrysler warned that they would need to halt production at one of their plants outside of China due to parts shortages and The plant has come to a halt as the problem is not resolved. The company said it is in the process of attaining the product from another source. Last but not least Carnival Corp has warned of a significant financial impact in their upcoming earnings report and they pulled their full-year 2020 forward guidance due to changes.

The supply chain shock emanating from China to other Asia Pacific countries and Europe, could become a major headache for India.

Bloomberg focuses on how an industrial shutdown of China’s economy has already had a profound effect on India’s economy and could get worse.

Pankaj R. Patel, chairman of Zydus Cadila, said prices of medicine in India have exponentially jumped in the last several weeks, thanks to much of the medicine is sourced from China.

The Indian pharmaceutical industry is experiencing massive disruptions that could face shortages starting in April if supplies aren’t replenished in the next couple weeks, Patel warned.

Manufacturers in China have idled plants, and at least two-thirds of the economy is halted. Some factories came online last week with promises of full production by the end of the month, but for most factories, their resumption will likely be delayed. This will undoubtedly lead to medicine shortages in India in the coming months ahead.

A new theme is developing from all this mayhem – that is the reorganization of complex supply chains out of China to a more localized approach to avoid severing. But in the meantime, these complex supply chains in India and across the world will experience massive disruption caused by the shutdown. All of this points to ugly end of globalization:

Pankaj Mahindroo, chairman of the India Cellular and Electronics Association (ICEA), said the wrecking of supply chains in China could soon have a devastating impact on India’s smartphone production.

Mahindroo represents companies including Foxconn, Apple Inc., Micromax Informatics Ltd., and Salcomp India, warned the “impact is already visible… If things don’t improve soon, production will have to be stopped.”

Already, the production of iPhones and Airpods has been reduced in China because of factory shutdowns.

The closure of Foxconn plants in India would be absolutely devastating for Apple.

Apple produces iPhone XR in India. If the production of affordable smartphones is halted or reduced, the Californian based company could see full-year earnings guidance slashed.

Mohnidroo said if things don’t improve in the next couple of weeks, smartphone factories in India could start running out of “critical components like printed circuit boards, camera modules, semiconductors, resistors, and capacitors.”

A spokesperson for Xiaomi Corp.’s India unit said alternative sourcing attempts are underway to mitigate any supply chain disruption from China.

Even before all of this, India’s economy is rapidly decelerating into an economic crisis.

Former Indian Finance Minister Yashwant Sinha warned several months ago that the country is in a “very deep crisis,” witnessing “death of demand,” and the government is “befooling people” with its economic distortions of how growth is around the corner.

Supply chain disruptions are moving from East to West. It’s only a matter of time before production lines are halted in the US because sourcing of Chinese parts is offline. The disruptions of supply chains is the shock that could tilt the global economy into recession.

It’s certainly plausible that the global economy is in the early stages of grinding to a halt. Already, we’ve noted that two-thirds of China’s economy is offline, with major industrial hubs idle and 400 million people quarantined.

The next phase of the supply chain chaos is to spread to regions that are overly reliant on Chinese parts for assembly, such as a Fiat Chrysler Automobiles NV plant in Serbia.

Bloomberg reports Friday morning that the plant is expected to halt operations of its assembly line because of the lack of parts from China as the Covid-19 outbreak worsens.

Turin, Italy-based automaker’s Kragujevac factory in Serbia, which assembles the Fiat 500L, has to bring its production line to a halt due to lack of audio-system and other electric parts sourced from China.

Four of the automaker’s suppliers have been impacted by China’s decision to shut down much of its industrial sector as part of a quarantine that’s expected to take a massive chunk out of GDP growth in the first half.

Fiat Chrysler CEO Mike Manley said four of the company’s suppliers in China had already been affected by the outbreak, including one “critical” maker of parts putting European production at risk.

The evolution of the supply chain disruption emanating from China is spreading outwards and to the West.

Wall Street is blind as a bat, or maybe their hope the Federal Reserve will keep pumping liquidity into the market will numb the pain of one of the most significant shocks expected to hit the global economy in the near term. This is mostly due to the world’s most complex supply chains, which as of late January, have been severed and will start affecting assembly plants in Europe.

The disruption could spread to the US, where many assembly plants source parts from China.

What’s about to hit the global economy was beautifully outlined by former Morgan Stanley Asia chairman Stephen Roach warned several weeks ago that the global economy could already be in a period of vulnerability, where an exogenous shock, such as the Covid-19, could be the trigger for the next worldwide recession.

Mohamed El-Erian, the chief economic adviser to the insurance company Allianz, recently said the economic damage caused by virus outbreak would play out this year.

El-Erian said the economic shock to China and surrounding manufacturing hubs is happening at a time when the global economy is slowing, and interest rates among central banks are near zero, indicating their ammo to fight the downturn is limited.

Freeport-McMoRan CEO Richard Adkerson said in an interview last month that the virus outbreak in China is a “real black swan event” for the global economy.

Alibaba Group’s CEO Daniel Zhang said this week that the virus outbreak in China is developing into a “black swan event” that could have severe consequences for China and the global economy.

When the world’s most complex supply chains break, so does the global economy. It’s only a matter of time before disruption is seen in the US.

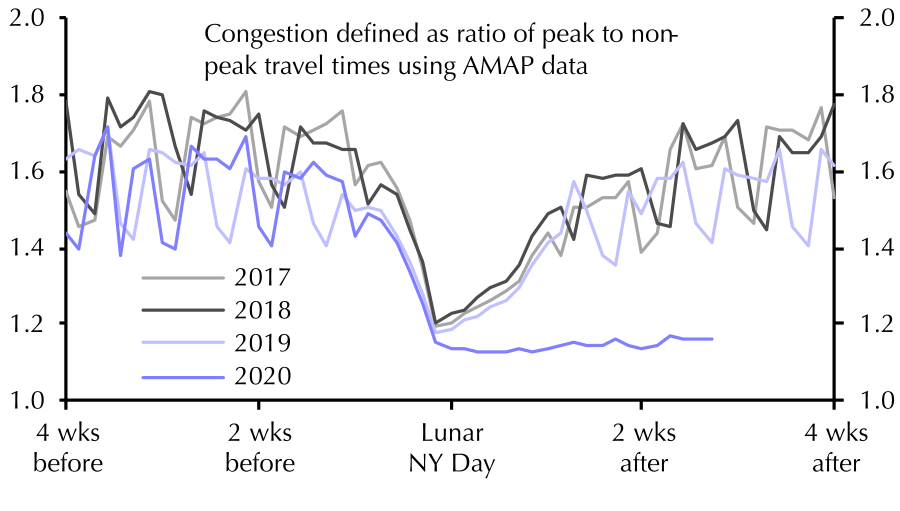

In our ongoing attempts to glean some objective insight into what is actually happening “on the ground” in the notoriously opaque China, whose economy has been hammered by the Coronavirus epidemic, yesterday ZeroHedge showed several “alternative” economic indicators such as real-time measurements of air pollution (a proxy for industrial output), daily coal consumption (a proxy for electricity usage and manufacturing) and traffic congestion levels (a proxy for commerce and mobility), before concluding that China’s economy appears to have ground to a halt.

That conclusion was cemented after looking at some other real-time charts which suggest that there is a very high probability that China’s GDP in Q1 will not only flatline, but crater deep in the red for one simple reason: there is no economic activity taking place whatsoever.

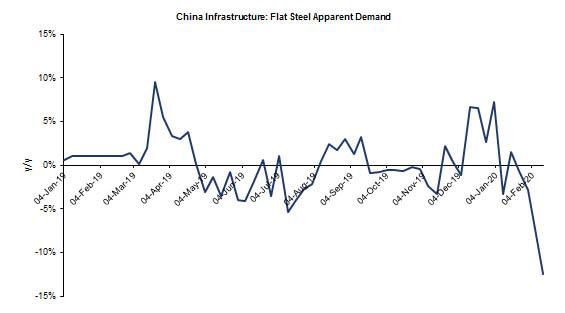

We start with China’s infrastructure and fixed asset investment, which until recently accounted for the bulk of Chinese GDP. As Goldman writes in an overnight report, in the Feb 7-13 week, steel apparent demand is down a whopping 40%, but that’s only because flat steel is down “only” 12% Y/Y as some car plants have ordered their employee to return to work (likely against their will as the epidemic still rages).

However, it is the far more important – for China’s GDP – construction steel sector where apparent demand has literally hit the bottom of the chart, down an unprecedented 88% Y/Y or as Goldman puts it, “construction steel demand is approaching zero.”

But wait, there’s more.

Courtesy of Capital Economics, which has compiled a handy breakdown of real-time China indicators, we can see the full extent of just how pervasive the crash in China’s economy has been, starting with familiar indicator, the average road congestion across 100 Chinese cities, which has collapsed into the New Year and has since failed to rebound.

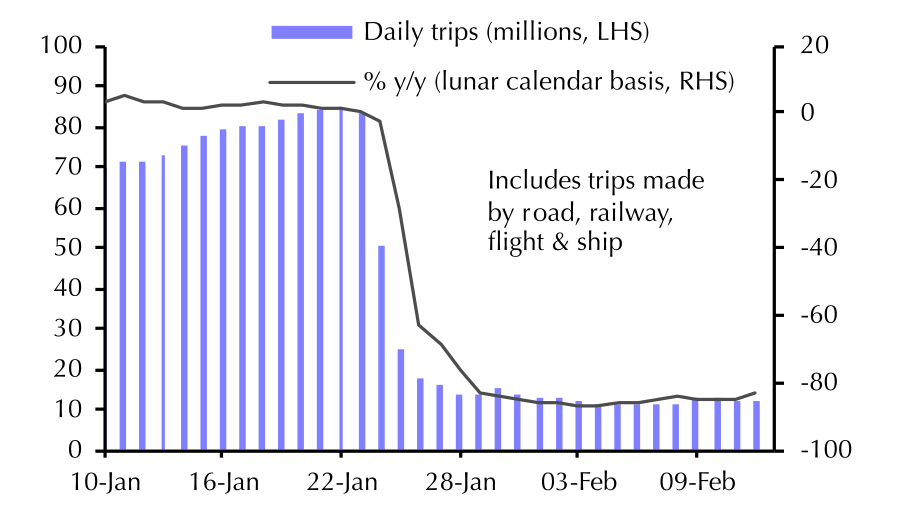

Parallel to this, daily passenger traffic has also flat lined since the New Year and has yet to post an even modest rebound.

And the biggest shocker: a total collapse in passenger traffic (measured in person-km y/y % change), largely due to the quarantine that has been imposed on hundreds of millions of Chinese citizens.

And while we already noted the plunge in coal consumption in power plants as Chinese electricity use has cratered…

… what is perhaps most striking, is the devastation facing the Chinese real estate sector where property sales across 30 major cities have basically frozen.

Finally, and most ominously perhaps, as the economy craters and internal supply chains fray, prices for everyday staples such as food are soaring as China faces not only economic collapse, but also surging prices for critical goods, such as food as shown in the wholesale food price index chart below…

… which in a nation of 1.4 billion is a catastrophic mix.

As the coronavirus pandemic spreads further without containment, and as the charts above continue to flat line, so will China’s economy, which means that not only is Goldman’s draconian view of what happens to Q1 GDP likely optimistic as China now faces an outright plunge in Q1 GDP…

… but any the expectation for a V-shaped recovery in Q2 and onward will vaporize faster than a vial of ultra-biohazardaous viruses in a Wuhan virology lab.

{kind=link}