“We just aren’t sure where they’ve gone.”

Tag Archives: Education

Los Angeles Schools To Launch 24/7 Tracking App And Weekly Virus Testing So Children Can Attend Classes

The Los Angeles Unified School District is launching a Microsoft-developed COVID-tracking app for children, which allows students to schedule and view the results of weekly COVID tests, post the results of off-campus COVID tests, and schedule vaccinations.

NYU Prof: “Hundreds, If Not Thousands” Of Universities Will Soon Be “Walking-Dead”

As colleges attempt to recover from the pandemic and prepare for future semesters, a New York University professor estimates that the next 5-10 years will see one to two thousand schools going out of business.

Scott Galloway, professor of marketing at the New York University Leonard N. Stern School of Business told Hari Sreenivasan on PBS’ “Amanpour and Co.” that many colleges are likely to suffer to the point of eventual extinction as a result of the coronavirus.

He sets up a selection of tier-two universities as those most likely not to walk away from the shutdown unscathed. During the pandemic, wealthy companies have not struggled to survive. Similarly, he says, “there is no luxury brand like higher education,” and the top names will emerge from coronavirus without difficulty.

“Regardless of enrollments in the fall, with endowments of $4 billion or more, Brown and NYU will be fine,” Galloway wrote in a blog post.

“However, there are hundreds, if not thousands, of universities with a sodium pentathol cocktail of big tuition and small endowments that will begin their death march this fall.”

“You’re gonna see an incredible destruction among companies that have the following factors: a tier-two brand; expensive tuition, and low endowments,” he said on “Amanpour and Co.,” because “there’s going to be demand destruction because more people are gonna take gap years, and you’re going to see increased pressure to lower costs.”

Approximating that a thousand to two thousand of the country’s 4,500 universities could go out of business in the next 5-10 years, Galloway concludes, “what department stores were to retail, tier-two higher tuition universities are about to become to education and that is they are soon going to become the walking dead.”

Another critical issue underlying the financial difficulties families and universities both face is the possibility that the quality of higher education has decreased.

Galloway argues that an education in the U.S. is observably unsatisfactory for the amount that it costs, given that if you “walk into a class, it doesn’t look, smell or feel much different than it did 40 years ago, except tuition’s up 1,400 percent,”he said during an interview with Dr. Sanjay Gupta.

And the pandemic, according to Galloway, has served to expose the quality of higher education.

Why Are So Many Top-Tier College Girls Turning To ‘Soft Prostitution’?

Are you a rich guy who wants to bang debt-laden college girls with all your extra money?

Are you a struggling college girl facing decades of six-figure debt so you can follow your unsinkable dreams?

Great news; thanks to the internet, your bases are covered! As we’ve previously reported (here and here), ‘soft prostitution’ may have been going on for a long time – but its normalization is relatively new – and undoubtedly linked to the $1.5 trillion+ student debt problem.

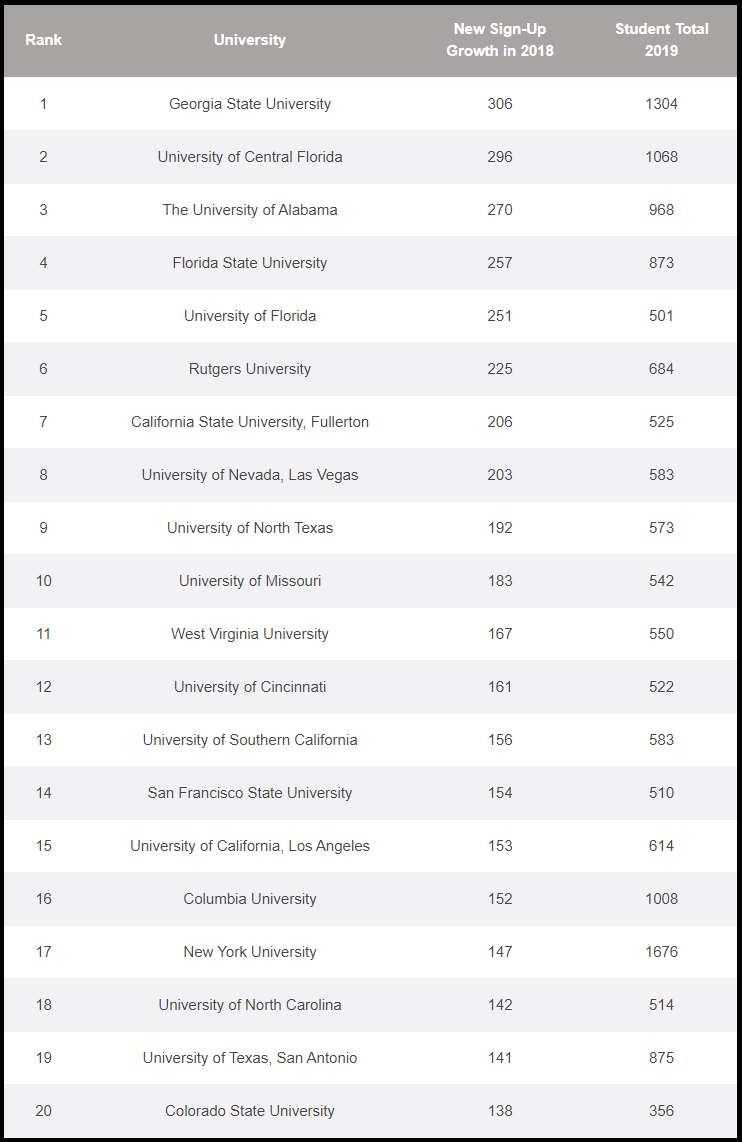

As an example, according to ‘sugar daddy / sugar baby’ website SeekingArrangement, there are 1,304 students at Georgia State University signed up to be Sugar Babies right now – up from just 306 in 2018.

Given that there are 15,277 female students at Georgia State, – nearly one in ten girls at Georgia State are willing to whore themselves out to make ends meet.

Of this list, several universities are considered top-tier – such as UCLA, University of Southern California, Columbia and New York University.

According to Seeking.com, “Sugar Babies do not want to be in monotonous, traditional relationships prescribed by society — that no longer works today. Rather, she is seeking a modern relationship — one that is different and matches her ambition and drive — with a romantic partner who can play the traditional role of provider or gentleman, without placing unreasonable limitations on personal growth,” according to the website.

Overall, there are 2.7 million US students signed up and 4.7 million worldwide.

According to the website, “Students registered on SeekingArrangement get help paying for tuition and even more benefits.Finding the right Sugar Daddy can help students gain access to the right network and opportunities. College Sugar Babies can also get help paying for other college-related costs, such as books and housing.”

And while the site claims 4.5 million students across the globe, SeekingArrangement says it has 20 million members worldwide – of which students are most common.

What do they Sugar Babies do with the money they earn with their vaginas? 30% is spent on tuition and other school related expenses, while 25% goes towards living expenses.

Meanwhile, the average Sugar Daddy is 41-years-old and has an annual income of $250,000. Most common professions are Tech Entrepreneur and CEO are their two top occupations, followed by Developer, Financier, Lawyer and Physician.

As for cities – New York tops the list, followed by London, Toronto and Los Angeles.

Follow your dreams people.

Majority Of Recent College Grads Don’t Have Jobs Lined Up, Survey Shows

This doesn’t bode well for the labor market.

Less Than 25% Of College Graduates Can Answer These 4 Simple Money Questions

Americans have become numb to financial intelligence. This is no more evident than a recent Sallie Mae survey, which indicated that college graduates can’t even answer simple questions about financial concepts, such as interest.

The statistics are not looking good for the United States, a nation deeply indebted, addicted to consumerism, and woefully ignorant about it all. Not long ago, SHTFPlanreported that a mere 1 in 10 Americans is actually capable of getting an A on a basic financial security test.

And even college graduates, who are likely tens of thousands (if not more) dollars in debt because of school, learned little to nothing about handling their personal finances. The big red flag comes from consumer banking firm Sallie Mae. The firm released its new “Majoring in Money” study which asked hundreds of current and recently graduated college students up to age 29 about basic financial concepts. The results are worrisome.

Sallie Mae asked these individuals four questions related to credit and interest, and fewer than one in four got all four of these correct.

1. Interest accumulation:

Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow?

a. More than $102

b. Exactly $102

c. Less than $102

d. Not sure2. Effects of payment behavior on credit cost:

Assuming the following individuals have the same credit card with the same interest rate and balance, which will pay the most in interest on their credit card purchases over time?

a. Joe, who makes the minimum payment on his credit card bill every month

b. Jane, who pays the balance on her credit card in full every month

c. Joyce, who sometimes pays the minimum, sometimes pays less than the minimum and missed one payment on her credit card bill

d. All of them will pay the same amount in interest over time

e. Not sure3. Impact of repayment term on cost of credit:

Imagine that there are two options when it comes to paying back a loan and both come with the same interest rate. Provided you have the needed funds, which option would you select to minimize your total costs over the life of the loan (i.e., all of your payments combined until the loan is completely paid off)?

a. Option 1 allows you to take 10 years to pay back the loan

b. Option 2 allows you to take 20 years to pay back the loan

c. Both options have the same out-of-pocket cost over the life of the loan

d. Not sure4. Interest terminology:

Which of the following best defines the term “interest capitalization”?

a. The type of interest charged on high-balance loans

b. The addition of unpaid interest to the principal balance of a loan

c. Interest that is charged when you postpone payments on your loan

The fact that we have an entire generation, largely college educated, who cannot answer these questions does not bode well for our future as a society. Not knowing the answers to these could end up costing people a lot of money down the road. According to Market Watch, 83% of college grads carry a credit card as revealed by Sallie Mae, but only about six in 10 say they pay the balance(s) in full and on time each month. Coupled with the fact that nearly seven in 10 college students take out student loans, graduating with an average of nearly $30,000 in debt, the decline in financial intelligence is evident.

There are ways to learn the basics of personal finance. Dave Ramsey’s Total Money Makeover book was of the most help to many people, and Ramsey is perhaps the most well-known personal finance guru out there. He takes a strick “no debt” approach that has worked not only for himself, buy countless others. He also offers an easy to follow guide which he’s dubbed “the baby steps” that will get people on the path to financial freedom.

Other resources are those such as Robert Kiyosaki’s Rich Dad, Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle Class Do Not!

Both books are excellent resources that teach the very basics about money and personal finance that no one is learning about in their public school educations.

* * *

The answers are 1: A, 2: C, 3: A, and 4: B

College (As We Knew It) Is Broken In America

The system of higher education in the United States is being rebuilt from the foundation and we’ve only just started to see the impact of this dramatic transformation.

- The way students and parents pay for college is changing

- The methods and the places students learn are changing (and have been for a while)

- Our culture is changing to finally accept that “traditional” 4-year college isn’t the answer for everyone

(Alex Mitchell) But before we talk about all of the changes that are happening in higher education right now, let’s talk about why college is, to put it simply, broken in the United States.

College is Broken.

It’s impossible to miss the many ways college is broken today. And I’m not just talking about the high profile bribery scandal that broke several weeks ago.

While parents paying hundreds of thousands to millions of dollars to guarantee college admission through a “side door” is concerning, it pales in comparison to these other indicators of college broken-ness.

1. Student Loans Are Crippling Tens of Millions

44.2 Million Americans currently are carrying close to $1.5 Trillion in student loan debt (this is ~20% of the US adult population).

Even more astonishing, over 11% of these loans are delinquent (90+ days without payment or in default).

This delinquency rate is >5x the credit card delinquency rate!

Student loans have become such a burden that companies have been started to offer student loan repayment as a fringe benefit: Goodly.

Shout out to Goodly for helping the many already in debt, but we need to stop the problem at the source too!

Sources: Federal Reserve, Bloomberg

2. Tuition Increases Are Relentless

From 1988 to 2008, tuition increased on average by 3.5% per year. From 2008 to 2018, tuition continued to increase at a still-suffocating 3% per year.

In 1998, tuition at a private 4-year college was 77% of the average male income in the United States.

By 2016, this had increased to 116%.

On the public college side, the increase is even more dramatic. In 1998, the costs averaged 29% of the average male income in the United States,increasing to 52% in 2016.

Incomes simply have not kept pace with tuition increases.

Source: ProCon.org

3. Incentives Are Distorted Between Colleges and Students

Students continue to attend college and continue to take on these significant loans because they believe they are making a good investment. College graduates earn substantially more than High School graduates over the course of their career, right? Correct, but…

The fundamental problem is that if the college they attend turns out to be a bad investment, as a growing number of private 4-year colleges do, only the student pays this penalty (and they pay a BIG, often lifelong, one).

The college already got paid by either the government or the student loan company and there is simply no penalty for their lack of performance in student education and career placement (save for some very limited publicly funded university penalties).

There are also no meaningful incentives from the government to provide education in areas where jobs are in the highest demand.

The only true incentive these colleges have is one that is too distant for many: The ability to continue to recruit new students who will pay their ever-increasing tuition rates.

How College is Changing Right Now

Where And How You Learn

- MOOCs: Massive Open Online Courses aren’t new, but the depth of courses they offer continues to increase dramatically. Between EdX, Coursera, Khan Academy, and Udacity you can learn almost anything from anywhere for free.

- Code Schools (v2!): Code Schools have already gone through one wave of evolution with ineffective programs and schools failing, new models for sustainable funding and profitability emerging and consolidation accelerating.

- Technical Trade Schools: Technical school used to mean learning a trade like Carpentry or studying as an Electrician’s apprentice. This concept has been reinvigorated with companies like NextGenT that offer many technical certificate programs in high demand fields like cybersecurity.

How You Pay

- ISAs: Income Share Agreements. Instead of paying tuition up front, a student agrees to pay a percentage of their future income to the school or lender. There is usually an income “floor” that the student must be above in order for the income share to take effect after graduation. There is also usually a repayment “ceiling” (so the former student doesn’t end up paying an obscene amount if they get a high-salary position immediately out of school). Companies like Vemo Education have started to bring this payment model to significant numbers of both code schools and traditional 4-year colleges.

- Get Paid to Learn: Several companies are taking the idea of the ISA a step further. In addition to paying nothing upfront, these companies are actually paying you a salary to learn. They are betting on high demand career fields like software development and data science and trying to make it as easy as possible for top candidates to join their schools. Several “get paid to learn” companies include Lambda School, Modern Labor, and CareerKarma.

Cultural Changes and Pressures

- Reducing the 4 Year College “Pressure”: It’s taken a long time, and particularly affluent parts of our country are still pretty resistant, but code schools and alternative higher education options have begun to gain acceptance as a better option for meaningful percentages of high school graduates.

Thank you for reading. If you’re enjoying this post so far, I think you would enjoy my new book, Disrupt Yourself. For a limited time, I’m offering a free pre-release chapter.

Claim yours now here: I want a free chapter of Disrupt Yourself!

Prediction: College in 10 Years…

- Mid-tier private colleges cease to exist

- Code schools will (continue to) consolidate dramatically

- All colleges remaining offer ISAs and many offer “get paid to learn” options

- Community College still exists as the low cost higher education option and may even grow in influence and size

- A small set of top code schools achieve “Ivy League” status and diversify to offer robust curriculum for developers, data scientists, designers, product managers and more (essentially the tech company talent stack)

- Student loan debt collapses in value as defaults skyrocket

Prediction: College in 20 Years…

- Ivy League and top research universities are only “old guard” that remain

- Community college is free everywhere in the USA as a guaranteed, robust, public secondary education (in many states this is the case already)

- All colleges that remain offer both ISAs and “you get paid to learn” options

- Code schools look like colleges and colleges look like code schools to the point where they are hard to differentiate

College is Changing and It’s a Good Thing

College is broken today.

But fortunately, many startups, companies, and public figures are starting to pay attention and build the next generation of higher education.

It’s going to be disruptive, it’s going to be scary (at times), but with the right minds focused on this huge problem, our country will build a secondary education system that has:

- Free options that are robust (Community College)

- Stronger alignment with high-demand careers

- True incentive alignment between students and education providers

- Little to no debt for students (!)

***

Warren Proposes $640 Billion Student Debt Forgiveness, Free College

“It’s a problem for all of us”

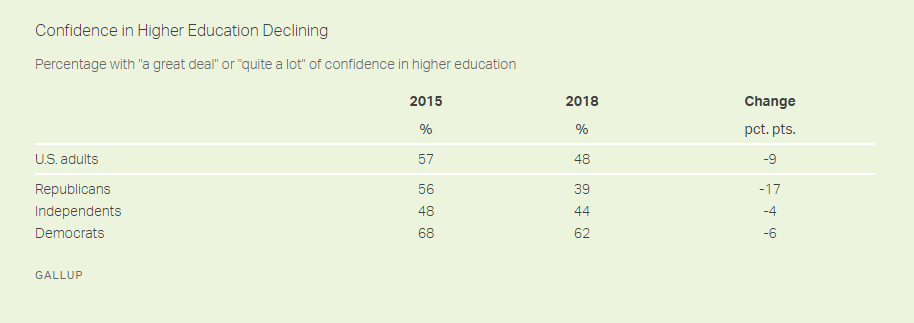

Confidence In Higher Education Plummets

Confidence in higher education in the United States has dropped significantly since 2015, according to polling company Gallup, which notes that it’s the worst-performing institution they measure.

The crisis in confidence coincides with a similar decline in the public’s view that higher education is affordable and available to those who need it, according to the report – suggesting that affordability and access are linked to the faith people have in the institution of higher learning.

The waning confidence in higher education isn’t limited to the general public either; academics have begun to lose faith as well.

Concerns about the future of higher education also exist within academia. College and university trustees and board members — many of whom are intimately familiar with higher ed’s services, operations and impact — remain concerned about the industry’s future, despite being more confident in their own institution’s future. The AGB 2018 Trustee Index, a recent study conducted by the Association of Governing Boards and Gallup, finds that three in four trustees (74%) are concerned or very concerned about the future of higher education in the U.S. Their concerns remain focused largely on one main challenge: affordability. –Gallup

What do college and university trustees point to as the top issues causing the drop in public confidence? Negative media reports about student debt (72%) and news reports on the cost of tuition (64%). To that end, more than half of trustees (58%) say their top concern about the future of higher education is the cost.

When it comes to affordability, the National Center for Education Statistics estimates that the total cost of tuition, fees and living expenses rose 28% between 2005/2006 – 2015/2016 in the United States after account for inflation, while enrollment across all higher education sectors dropped by 1.4% in 2018, which Gallup says is consistent with recent trends.

Many colleges, universities and even states are attempting to address affordability concerns and related enrollment decreases by freezing or reducing tuition costs. For the seventh year in a row, Purdue University has frozen its tuition rates. Western Governors University has bucked the enrollment trend in higher education for a variety of reasons, including because of its commitment to keep costs contained. In the past five years, WGU has increased the cost of annual tuition by only $600, while total enrollment has more than doubled, to over 100,000 students. –Gallup

The solution?

Restoring confidence in higher education – and boosting enrollment – can be accomplished by restoring affordability while improving the quality of higher education, according to the report.

A 2015 Gallup report revealed a clear relationship between student debt levels and graduates’ perceptions that their degree was ‘worth it.’ Graduates drowning in student loan debt were obviously less likely to consider their education a worthwhile investment.

However, and fortunately for higher education, a high-quality experience in school blunted the negative effect of student debt on graduates’ beliefs that their undergraduate experience was worthwhile, proving that the significant investment can be worth it for some grads. The AGB 2018 Trustee Index also shows that trustees have been asked to make changes to the academic programs offered at their institution to better respond to 21st-century needs. Half of trustees say senior administrators have asked them to increase or introduce STEM programs, and about one-third say they have been asked to increase or introduce applied or experiential learning programs. –Gallup

While the American public largely still believes that higher education is the way to achieve a better life through higher-paying jobs, institutions must figure out how to provide a quality education without saddling grads with debt that takes decades to pay off.

‘Tuition Insurance’ Industry Is Booming As Cost Of College Skyrockets

Not only is tuition insurance now a thing, but the industry is absolutely booming. The Wall Street Journal reports that 70,000 policies were written across the United States over the course of the last year, which was up from just 20,000 policies that were written five years ago.

But the reported rise in students attending universities with disabilities as a result of mental health disorders – combined with the rapidly rising cost of tuition – has caused the birth of an industry that doesn’t look like it has any plans of slowing down.

Just as it is in any industry that is attracting large quantities of cash, money making derivatives and alternative products tend to pop up. This was notably the case in the world of cryptocurrency, when we reported back in July that the crypto-insurance industry not only existed, but similarly, was also blooming.

But the reported rise in students attending universities with disabilities as a result of mental health disorders – combined with the rapidly rising cost of tuition – has caused the birth of an industry that doesn’t look like it has any plans of slowing down.

Just as it is in any industry that is attracting large quantities of cash, money making derivatives and alternative products tend to pop up. This was notably the case in the world of cryptocurrency, when we reported back in July that the crypto-insurance industry not only existed, but similarly, was also blooming.

The article notes that a lot of schools already carry a reimbursement policy, but that usually doesn’t apply to the second half of any given semester. For example, the policy at Vanderbilt University, where students are paid back up until about halfway through the semester, at which point they no longer entitled to reimbursement. Vanderbilt charges about $59,000 for tuition and housing, according to the article, and tuition insurance there is about $530. In general, the article notes that tuition insurance generally costs about 1% of tuition:

Several companies provide tuition insurance, Most policies charge in the neighborhood of 1% of the cost of school. A semester that runs $30,000 would cost about $300. At least 200 schools now work with insurers, offering the coverage to families when the pay the tuition bill.

Liberty Mutual Insurance started offering tuition-reimbursement policies this year, in part because of consumer demand. When a student drops out mid-semester parents are often “very surprised to learn that you may not get anything back,” said Michelle Chevalier, a senior director at Liberty Mutual.

In addition to the rising cost of college, a growing number of mental health issues with students are also driving the demand for this insurance. Insurance plans don’t usually cover academic or disciplinary related drop-outs. The article notes:

Plans don’t typically cover students who drop out for academic or disciplinary reasons but will for medical reasons. Generally, insurers don’t ask about pre-existing conditions, either mental or physical. The idea, GradGuard’s Mr. Fees said, is: “If a student is healthy enough to start to a semester, they qualify.”

Insurers say that the number of claims they receive citing mental health incidents has risen. As many as one in four students at some elite U.S. colleges are now classified as disabled, largely because of mental-health issues such as depression or anxiety, according to the National Center for Education Statistics and interviews with schools.

Carmen Duarte, a spokesperson for A.W.G. Dewar, Inc. which has been offering tuition-reimbursement policies since the 1930, said claims have remained flat for physical-health incidents but increased for mental-health reasons.

The interesting thing, however, is while everybody is talking about tuition insurance and the purposes that it serves, nobody stops to ask why college tuitions on an inflation adjusted basis have skyrocketed so much.

It seems that only a couple, non-mainstream analysts want to actively address the fact that providing student loans for nearly everybody, running up a nationwide $1.5 trillion tab, could possibly be creating an artificial demand that is allowing colleges to take advantage of guaranteed money and hike up the price of tuition. It’s once again an example of the government getting involved and disabling the key benefits of free market capitalism.

A genuine demand slow down for university enrollment could be beneficial, as it would encourage colleges to compete, lower prices and ensure a higher quality of education that they could pitch to entice new enrollees.

But this artificial bubble created by the influx of student loans and the idea that “everybody has the right to go to college” has done just the opposite: created such sky-high tuition prices that derivative industries like tuition insurance have been born, and will likely continue to flourish.

One Million Americans Default On Their Student Loans Each Year, Report Reveals

More than one million American student loan borrowers default on their debt each year, a new report says.

That means by 2023, approximately 40 percent of borrowers are expected to default.

That is according to a new report by the Urban Institute, a nonprofit research organization dedicated to developing evidence-based insights on critical socioeconomic issues. Researchers found about 250,000 student loan borrowers see their debts go into default every quarter, and an additional 20,000 to 30,000 borrowers default on their rehabilitated student loans.

“My results indicate that the likelihood of student loan default is positively correlated with holding other collections debt (e.g., medical, utilities, retail, or bank debt). About 59 percent of borrowers who defaulted on their student loans within four years had collections debt in the year before entering student loan repayment (compared with 24 percent among non-defaulters). Those who will default on their student loans are more likely to reside in neighborhoods that have more residents of color and fewer adults with a bachelor’s degree or higher, but a borrower’s personal credit profile is a stronger predictor of default than the neighborhood where she resides,” said Kristin Blagg, a research associate in the Education Policy Program at the Urban Institute.

The average defaulter is more likely to live in Hispanic and black neighborhoods, Blagg found. Her previous research has shown that minorities are more burdened by their education debt because their parents have a lower net wealth as well as higher rates of unemployment. These neighborhoods also have a median income of around $50,000, compared with $60,000 for non-defaulters.

The Urban Institute made a startling discovery: Those with the smallest loan balances had a higher probability of not paying off their debt. In fact, 1 in 3 people who had a student loan balance less than $5,000 defaulted within four years, compared with 15 percent of borrowers who owed more than $35,000.

This is because students who dropped out of college have less debt, but are easily burdened by debt since they do not have the benefit of a degree, said Mark Kantrowitz, a student loan expert, who spoke with CNBC.

Also, Kantrowitz said, “They often lack awareness of options for dealing with the debt, such as deferments, forbearances, income-driven repayment and loan forgiveness.”

The report then describes the relationship between a borrower’s credit profile and student loan default in a nationally representative sample of student loan borrowers, over the first four years of repayment. It found that by the time the student loan falls into the default, the borrower will see their credit score plunge by 60 points, to an average of around 550. Borrowers who stay current, usually have credit scores in the high 600s.

As we have mentioned, millennials are delaying marriage, home-buying and having kids (pretty much delaying the American dream), simply because of their gig-economy job(s) cannot cover debt servicing payments of their loans.

“Negative effects of student loan default can be wage garnishments, tax offsets, and other methods of loan collections,” said Elaine Griffin Rubin, senior contributor and communications specialist at Edvisors. “In addition, some states suspend or revoke state-issued professional licenses, and some states suspend a driver’s license because of a defaulted loan.”

To make the situation worse, defaulting on student loans increases the balance, likely due to collection fees and the accumulation of interest. Kantrowitz said a borrower could expect their balance to jump by over 10 percent after default.

These myriad consequences that come with a default can be hard to recover from, Kantrowitz said.

“At best, it delays participation in the American Dream,” he said. “At worst, they are shut out permanently.”

Student debt is a crisis that many Americans will not be able to recover from. The College Board, a non-profit organization, says the average cost of a U.S. degree is $34,740 a year at a private college, minus living costs.

Graduates of the Class of 2016 owe a staggering $37,000 each in student loans. Total Student Loans Owned and Securitized, Outstanding (SLOAS) has surpassed the $1.5 trillion mark in Q2 2018, which is second only to home mortgages among categories of consumer debt and the main reason Americans’ household debt has swelled to a record high.

Credit bubbles are all the same. It just happens that the life cycle of the student debt bubble is nearing a deleveraging period. According to both Keynesian and monetarist theory, when the student debt bubble cracks, the state should intervene directly, and bailout the millennials who made terrible life decisions in accumulating massive amounts of debt for a worthless liberal arts degree, simply because the myth of going to college would usher in a high paying job. As it has become increasingly evident, that is not the case in today’s gig-economy. The failing education system has duped millennials, they have now realized that the greatest con of all time is college.

Which American College Degrees Get The Highest Salaries?

If you’re a college graduate, you likely went to school to pursue an important passion of yours.

But as we all know, what we major in has consequences that extend far beyond the foundation of knowledge we build in our early years. As Visual Capitalist’s Jeff Desjardins notes, any program we choose to enroll in also sets up a track to meet future friends, career opportunities, and connections.

Even further, the college degree you choose will partially dictate your future earning potential – especially in the first decade after school. If jobs in your field are in high demand, it can even set you up for long-term financial success, enabling you to pay off costly student loans and build up savings potential.

DATA BACKGROUNDER

Today’s chart comes to us from Reddit user /r/SportsAnalyticsGuy, and it’s based on PayScale’s year-long survey of 1.2 million users that graduated only with a bachelor degree in the United States. You can access the full set of data here.

(

(The data covers two different salary categories:

Starting median salary: The median of what people were earning after they graduated with their degree.

Mid-career Percentiles: Salary data from 10 years after graduation, sorted by percentile (10th, 25th, Median, 75th, and 90th)

In other words, the starting median salary represents what people started making after they graduated, and the rest of the chart depicts the range that people were making 10 years after they got their degree. Lower earners (10th percentile) are the lower bound, and higher earners (90th) are the upper bound.

COLLEGE DEGREES, BY SALARY

What college majors win out?

Here’s the top 20 majors from the data set, sorted by mid-career median salary (10 years in):

Based on this data, there are a few interesting things to point out.

The top earning specialization out of college is for Physician Assistants, with a median starting salary of $74,300. The downside of this degree is that earning potential levels out quickly, only showing a 23.4% increase in earning power 10 years in.

In contrast, the biggest increases in earning power go to Math, Philosophy, Economics, Marketing, Physics, Political Science, and International Relations majors. All these degrees see a 90% or higher increase from median starting salary to median mid-career salary.

In absolute terms, the majors that saw the highest median mid-career salaries were all along the engineering spectrum: chemical engineering, computer engineering, electrical engineering, and aerospace engineering all came in above $100,000. They also generally had very high starting salaries.

As a final note, it’s important to recognize that this data does not necessarily correlate to today’s degrees or job market. The data set is based on people that graduated at least a decade ago – and therefore, it does not necessarily represent what grads may experience as they are starting their careers today.

Fed Finds Wealth Advantage For College Grads Is Vanishing

Four years ago, in one of its taxpayer subsidized research papers, the San Fran Fed asked “is it still worth going to college“, looking at the trade off between the “investment” of tens of thousands of dollars in student loans relative to the pick up in earnings potential over one’s lifetime. It found that the answer is “yes” because “the value of a college degree remains high, and the average college graduate can recover the costs of attending in less than 20 years.” In other words by the time one is 42, one’s student loans will be paid off, assuming of course that one can still find a job. And, staying in this idealized world, the difference between earnings continues to grow “such that the average college graduate earns over $800,000 more than the average high school graduate by retirement age.”

Four years later, the New York decided to rerun the same analysis, which it described in a recent blog post “The College Boost: Is the Return on a Degree Fading?”, and came to a starkly bleaker conclusion.

As DataTrek’s Nick Colas summarizes the Fed’s study, the net income and net worth benefits of a college or grad school degree are rapidly diminishing. Specifically, the NY Fed economists looked at two broad demographic cohorts (whites and African Americans), segmenting changes in expected income between those people born each decade between the 1930s and the 1980s. Their findings:

- White workers with a 4-year degree born from the 1930s to the 1970s saw a +57–72% pickup in income over their non-college educated counterparts. Those born in the 1980s only saw a +43% improvement, however.

- African American college grads born in the 1980s are, however, still seeing income differentials in line with older cohorts (+71% versus +66 – 76% for those born in the 1940s to 1970s).

The data looks similar for those workers with a graduate degree. For white workers born in the 1980s, the differential to their peers without an advanced degree is +54%, lower than the +80–108% of older cohorts. For African Americans, the benefits of a graduate education remain consistently high (+73–125% more than those without a grad school degree) across all age groups.

Where things look really bad is when you look at total wealth differentials between the age groups. These include both financial assets and non-financial, such as home ownership.

- On that count, white families with a college educated household member who was born in the 1980s is +42% better off for their sheepskin, versus +134–247% for those born in the 1930s to the 1980s. Moreover, the older the graduate, the better the differential.

- The news is even worse for African American households, where those born in the 1980s are only +6% better off than their non-college educated peers. Those differences were +126% to +253% for those born in the 1940s to the 1970s.

Exactly the same thing holds true when applied to graduate degrees: earlier born households accumulate much more wealth than later ones when compared to those who did not earn such a degree.

Key takeaway: to us, this looks like a solid data-driven indictment of the rising cost of US education, with its concurrent increase in student debt (and one that is vastly different from the far rosier take by the San Fran Fed in 2014). A college and/or graduate degree does mean higher wages. But it also means more educational debt, which delays both savings and home ownership.

The notion that younger demographic college graduate cohorts will deliver out sized economic growth, as their parents did when they were younger, seems suspect at best.

The Exorbitant Cost Of Getting Ahead In Life

Some 84 percent of Americans claim that a higher education is a very or extremely important factor for getting ahead in life, according to the National Center for public policy and Higher Education.

So, it’s worth the exorbitant cost, but not everyone can pay, and outsized costs in the U.S. are giving much of the rest of the developed world the higher education advantage.

According to the U.S. Bureau of Labor Statistics (BLS), people with a Bachelor’s Degree earn around 64 percent more per week than those with a high school diploma, and around 40 percent more than those with an Associate’s Degree. In turn, those with an Associate’s degree earn around 17 percent more than those with a high school diploma.

The Federal Reserve Bank of New York says that college graduates overall earn 80 percent more than those without a degree.

There’s also job security to consider.

Individuals with college degrees have a lower average unemployment rates than those with only high school educations. Among people aged 25 and over, the lowest unemployment rates occur in those with the highest degrees.

From this perspective, it’s no surprise that students are willing to bite the bullet and take on a ton of debt to finance education.

About three-fourths of students who attend four-year colleges graduate with loan debt. And this number is up from about half of students three decades ago.

The average student loan debt for Class of 2017 graduates was $39,400, up 6 percent from the previous year. Over 44 million Americans now hold over $1.5 trillion in student loan debt, according to Student Loan Hero.

According to College Board, the average cost of tuition and fees for the 2017–2018 school year was $34,740 at private colleges, $9,970 for state residents at public colleges, and $25,620 for out-of-state residents attending public universities.

The U.S. is one of the most expensive places to go obtain a higher education, but there are pricier venues, too.

If you want a free higher education, try Europe—specifically Germany and Sweden. Denmark, too, doles out an allowance of about $900 a month to students to cover their living expenses. But don’t try to study in the UK on the cheap. The UK is the most expensive country in Europe, with college tuition coming in at an average of $12,414.

In Australia, graduates don’t pay anything on their loans until they earn about $40,000 a year, and then they only pay between 4 percent and 8 percent of their income, which is automatically deducted from their bank accounts, reducing the chances of default.

For Japan—a country that sees more than half of its population go to college—the highly respected University of Tokyo only costs about $4,700 a year for undergraduates, thanks to government subsidies. The Japanese government spends almost $8,750 a year per student because it sees the massive value in having a highly educated citizenry.

For Americans, while student loans may still be a good investment overall, the idea of taking a lifetime to pay off the debt may become increasingly unattractive. And it’s only going to get worse, according to JPMorgan, which predicts that by 2035 the cost of attending a four-year private college will top $487,000.

Margin Calls Mount On Loans Against Stock Portfolios Used To Buy Homes, Boats, “Pretty Much Everything”

Take the Ultimate Vacation on Tropical Island Paradise Super yacht

In a securities-based loan, the customer pledges all or part of a portfolio of stocks, bonds, mutual funds and/or other securities as collateral. But unlike traditional margin loans, in which the client uses the credit to buy more securities, the borrowing is for other purchases such as real estate, a boat or education.

The result was “dangerously high margin balances,” said Jeff Sica, president at Morristown, N.J.-based Circle Squared Alternative Investments, which oversees $1.5 billion of mostly alternative investments. He said the products became “the vehicle of choice for investors looking to get cash for anything.” Mr. Sica and others say the products were aggressively marketed to investors by banks and brokerages.

From the Wall Street Journal article: Margin Calls Bite Investors, Banks

Today’s article from the Wall Street Journal on investors taking out large loans backed by portfolios of stocks and bonds is one of the most concerning and troubling finance/economics related articles I have read all year.

Many of you will already be aware of this practice, but many of you will not. In a nutshell, brokers are permitting investors to take out loans of as much as 40% of the value from a portfolio of equities, and up to a terrifying 80% from a bond portfolio. The interest rates are often minuscule, as low as 2%, and since many of these clients are wealthy, the loans are often used to purchase boats and real estate.

At the height of last cycle’s credit insanity, we saw average Americans take out large home loans in order to do renovations, take vacations, etc. While we know how that turned out, there was at least some sense to it. These people obviously didn’t want liquidate their primary residence in order to do these things they couldn’t actually afford, so they borrowed against it.

In the case of these financial assets loans, the investors could easily liquidate parts of their portfolio in order to buy their boats or houses. This is what a normal, functioning sane financial system would look like. Rather, these clients are so starry eyed with financial markets, they can’t bring themselves to sell a single bond or share in order to purchase a luxury item, or second home. Of course, Wall Street is encouraging this behavior, since they can then earn the same amount of fees managing financial assets, while at the same time earning money from the loan taken out against them.

I don’t even want to contemplate the deflationary impact that this practice will have once the cycle turns in earnest. Devastating momentum liquidation is the only thing that comes to mind.

So when you hear about margin loans against stocks, it’s not just to buy more stocks. It’s also to buy “pretty much everything…”

From the Wall Street Journal:

Loans backed by investment portfolios have become a booming business for Wall Street brokerages. Now the bill is coming due—for both the banks and their clients.

Among the largest firms, Morgan Stanley had $25.3 billion in securities-based loans outstanding as of June 30, up 37% from a year earlier. Bank of America, which owns brokerage firm Merrill Lynch, had $38.6 billion in such loans outstanding as of the end of June, up 14.2% from the same period last year. And Wells Fargo & Co. said last month that its wealth unit saw average loans, including these loans and traditional margin loans, jump 16% to $59.3 billion from last year.

In a securities-based loan, the customer pledges all or part of a portfolio of stocks, bonds, mutual funds and/or other securities as collateral. But unlike traditional margin loans, in which the client uses the credit to buy more securities, the borrowing is for other purchases such as real estate, a boat or education.

Securities-based loans surged in the years after the financial crisis as banks retreated from home-equity and other consumer loans. Amid a years long bull market for stocks, the loans offered something for everyone in the equation: Clients kept their portfolios intact, financial advisers continued getting fees based on those assets and banks collected interest revenue from the loans.

This is the reason Wall Street loves these things. You earn on both sides, while making the financial system much more vulnerable. Ring a bell?

The result was “dangerously high margin balances,” said Jeff Sica, president at Morristown, N.J.-based Circle Squared Alternative Investments, which oversees $1.5 billion of mostly alternative investments. He said the products became “the vehicle of choice for investors looking to get cash for anything.” Mr. Sica and others say the products were aggressively marketed to investors by banks and brokerages.

Even before Wednesday’s rally, some banks said they were seeing few margin calls because most portfolios haven’t fallen below key thresholds in relation to loan values.

“When the markets decline, margin calls will rise,” said Shannon Stemm, an analyst at Edward Jones, adding that it is “difficult to quantify” at what point widespread margin calls would occur.

Bank of America’s clients through Merrill Lynch and U.S. Trust are experiencing margin calls, but the numbers vary day to day, according to spokesman for the bank. He added the bank allows Merrill Lynch and U.S. Trust clients to pledge investments in lieu of down payments for mortgages.

Clients may be able to borrow only 40% or less of the value of concentrated stock positions or as much as 80% of a bond portfolio. Interest rates for these loans are relatively low—from about 2% annually on large loans secured by multi million-dollar accounts to around 5% on loans less than $100,000.

80% against a bond portfolio. Yes you read that right. Think about how crazy this is with China now selling treasuries, and U.S. government bonds likely near the end of an almost four decades bull market.

About 18 months ago, he took out a $93,000 loan through Neuberger Berman, collateralized by about $260,000 worth of stocks and bonds, and used the proceeds to buy his share in a three-unit investment property in the Bushwick section of Brooklyn, N.Y. He says that his portfolio, up about 3% since he took out the loan, would need to fall 25% before he would worry about a margin call.

Regulators earlier this year had stepped up their scrutiny of these loans due to their growing popularity at brokerages. The Financial Industry Regulatory Authority put securities-based loans on its so-called watch list for 2015 to get clarity on how securities-based loans are marketed and the risk the loans may pose to clients.

“We’re paying careful attention to this area,” said Susan Axelrod,head of regulatory affairs for Finra.

I think the window for “paying close attention” closed several years ago.

All I have to say about this is, good lord.

Energy Workforce Projected To Grow 39% Through 2022

b

b

The dramatic resurgence of the oil industry over the past few years has been a notable factor in the national economic recovery. Production levels have reached totals not seen since the late 1980s and continue to increase, and rig counts are in the 1,900 range. While prices have dipped recently, it will take more than that to markedly slow the level of activity. Cycles are inevitable, but activity is forecast to remain at relatively high levels.

An outgrowth of oil and gas activity strength is a need for additional workers. At the same time, the industry workforce is aging, and shortages are likely to emerge in key fields ranging from petroleum engineers to experienced drilling crews. I was recently asked to comment on the topic at a gathering of energy workforce professionals. Because the industry is so important to many parts of Texas, it’s an issue with relevance to future prosperity.

Although direct employment in the energy industry is a small percentage of total jobs in the state, the work is often well paying. Moreover, the ripple effects through the economy of this high value-added industry are large, especially in areas which have a substantial concentration of support services.

Employment in oil and gas extraction has expanded rapidly, up from 119,800 in January 2004 to 213,500 in September 2014. Strong demand for key occupations is evidenced by the high salaries; for example, median pay was $130,280 for petroleum engineers in 2012 according to the Bureau of Labor Statistics (BLS).

Due to expansion in the industry alone, the BLS estimates employment growth of 39 percent through 2022 for petroleum engineers, which comprised 11 percent of total employment in oil and gas extraction in 2012. Other key categories (such as geoscientists, wellhead pumpers, and roustabouts) are also expected to see employment gains exceeding 15 percent. In high-activity regions, shortages are emerging in secondary fields such as welders, electricians, and truck drivers.

The fact that the industry workforce is aging is widely recognized. The cyclical nature of the energy industry contributes to uneven entry into fields such as petroleum engineering and others which support oil and gas activity. For example, the current surge has pushed up wages, and enrollment in related fields has increased sharply. Past downturns, however, led to relatively low enrollments, and therefore relatively lower numbers of workers in some age cohorts. The loss of the large baby boom generation of experienced workers to retirement will affect all industries. This problem is compounded in the energy sector because of the long stagnation of the industry in the 1980s and 1990s resulting in a generation of workers with little incentive to enter the industry. As a result, the projected need for workers due to replacement is particularly high for key fields.

The BLS estimates that 9,800 petroleum engineers (25.5 percent of the total) working in 2012 will need to be replaced by 2022 because they retire or permanently leave the field. Replacement rates are also projected to be high for other crucial occupations including petroleum pump system operators, refinery operators, and gaugers (37.1 percent); derrick, rotary drill, and service unit operators, oil, gas, and mining (40.4 percent).

Putting together the needs from industry expansion and replacement, most critical occupations will require new workers equal to 40 percent or more of the current employment levels. The total need for petroleum engineers is estimated to equal approximately 64.5 percent of the current workforce. Clearly, it will be a major challenge to deal with this rapid turnover.

Potential solutions which have been attempted or discussed present problems, and it will require cooperative efforts between the industry and higher education and training institutions to adequately deal with future workforce shortages. Universities have had problems filling open teaching positions, because private-sector jobs are more lucrative for qualified candidates. Given budget constraints and other considerations, it is not feasible for universities to compete on the basis of salary. Without additional teaching and research staff, it will be difficult to continue to expand enrollment while maintaining education quality. At the same time, high-paying jobs are enticing students into the workforce, and fewer are entering doctoral programs.

Another option which has been suggested is for engineers who are experienced in the workplace to spend some of their time teaching. However, busy companies are naturally resistant to allowing employees to take time away from their regular duties. Innovative training and associate degree and certification programs blending classroom and hands-on experience show promise for helping deal with current and potential shortages in support occupations. Such programs can prepare students for well-paying technical jobs in the industry. Encouraging experienced professionals to work past retirement, using flexible hours and locations to appeal to Millennials, and other innovative approaches must be part of the mix, as well as encouraging the entry of females into the field (only 20 percent of the current workforce is female, but over 40 percent of the new entries).

Industry observers have long been aware of the coming “changing of the guard” in the oil and gas business. We are now approaching the crucial time period for ensuring the availability of the workers needed to fill future jobs. Cooperative efforts between the industry and higher education/training institutions will likely be required, and it’s time to act.