Just days after Germany reported the highest inflation in generation (with February headline CPI soaring at a 7.6% annual pace and blowing away all expectations), giving locals a distinctly unpleasant deja vu feeling even before the Russian invasion of Ukraine broke what few supply chains remained and sent prices even higher into the stratosphere…

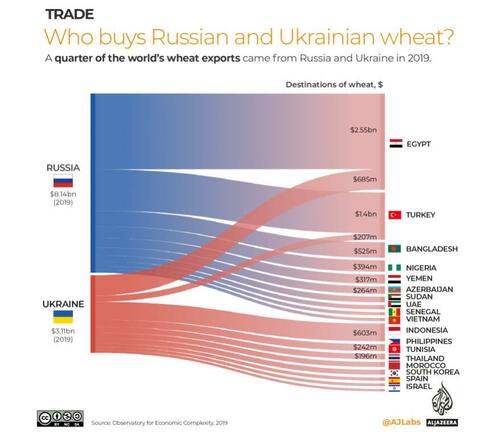

This morning ZeroHedge listed some of the countries that are dangerously (and almost exclusively) reliant on Russia and Ukraine for their wheat imports, highlighting Turkey, Egypt, Tunisia and others…

… which are facing an “Arab Spring” style food crisis (and potential uprising) in the coming weeks unless the Ukraine conflict is resolved.

The U.S. Department of Agriculture’s World Agricultural Supply and Demand Estimates (WASDE) report was released Thursday afternoon and pointed to declining grain supplies that sent grain futures prices higher and will keep food inflation in focus.

VIRGINIA — (CHINESE OWNED) Smithfield Foods, Inc. announced today that its Sioux Falls, SD facility will remain closed until further notice. The plant is one of the largest pork processing facilities in the U.S., representing four to five percent of U.S. pork production. It supplies nearly 130 million servings of food per week, or about 18 million servings per day, and employs 3,700 people. More than 550 independent family farmers supply the plant.

“The closure of this facility, combined with a growing list of other protein plants that have shuttered across our industry, is pushing our country perilously close to the edge in terms of our meat supply. It is impossible to keep our grocery stores stocked if our plants are not running. These facility closures will also have severe, perhaps disastrous, repercussions for many in the supply chain, first and foremost our nation’s livestock farmers. These farmers have nowhere to send their animals,” said Kenneth M. Sullivan, president and chief executive officer, for Smithfield.

“Unfortunately, COVID-19 cases are now ubiquitous across our country. The virus is afflicting communities everywhere. The agriculture and food sectors have not been immune. Numerous plants across the country have COVID-19 positive employees. We have continued to run our facilities for one reason: to sustain our nation’s food supply during this pandemic. We believe it is our obligation to help feed the country, now more than ever. We have a stark choice as a nation: we are either going to produce food or not, even in the face of COVID-19,” he concluded.

In preparation for a full shutdown, some activity will occur at the plant on Tuesday to process product in inventory, consisting of millions of servings of protein. Smithfield will resume operations in Sioux Falls once further direction is received from local, state and federal officials. The company will continue to compensate its employees for the next two weeks and hopes to keep them from joining the ranks of the tens of millions of unemployed Americans across the country.

“We are looking at the machine that feeds society shutting down under controlled demolition”

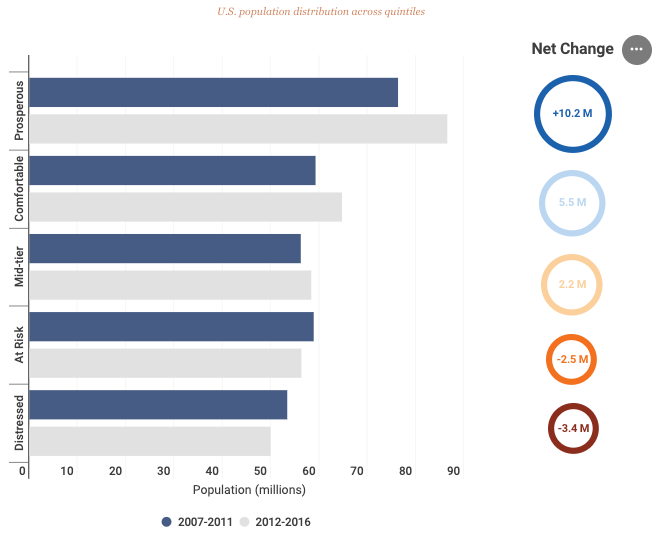

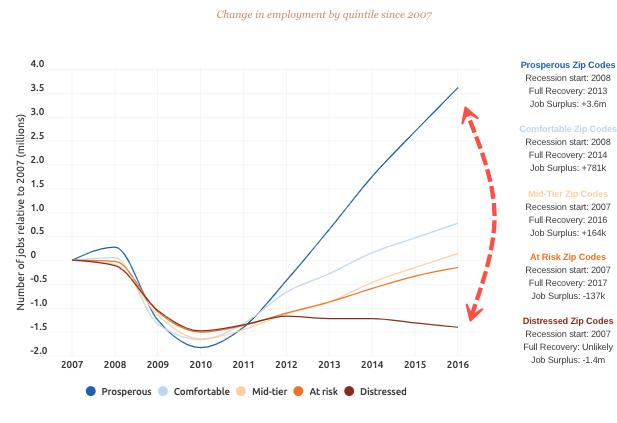

The Economic Innovation Group’s (EIG)Distressed Communities Index(DCI) shows a significant economic transformation (from two distinct periods: 2007-2011 and 2012-2016) that occurred since the financial crisis. The shift of human capital, job creation, and business formation to metropolitan areas reveals that rural America is teetering on the edge of collapse.

Since the crisis, the number of people living in prosperous zip codes expanded by 10.2 million, to a total of 86.5 million, an increase that was much greater than any other social class. Meanwhile, the number of Americans living in distressed zip codes decreased to 3.4 million, to a total of 50 million, the smallest shift of any other social class. This indicates that the geography of economic pain is in rural America.

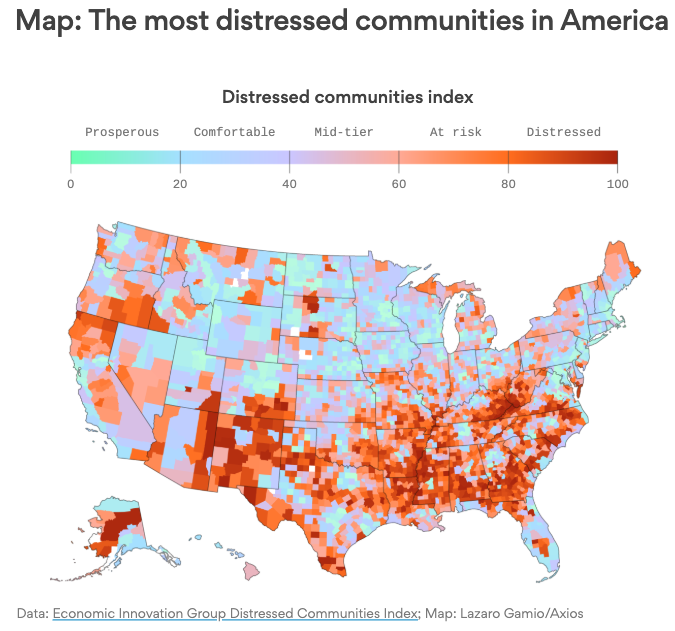

Visualizing the collapse: Economic distress was mostly centered in the Southeast, Rust Belt, and South Central. In Alabama, Arkansas, Mississippi, and West Virginia, at least one-third of the population were located in distressed zip codes.

“While the overall population in distressed zip codes declined, the number of rural Americans in that category increased by nearly 1 million between the two periods. Rural zip codes exhibited the most volatility and were by far the most likely to be downwardly mobile on the index, with 30 percent dropping into a lower quintile of prosperity—nearly twice the proportion of urban zip codes that fell into a lower quintile. Meanwhile, suburban communities registered the greatest stability, with 61 percent remaining in the same quintile over both periods. Urban zip codes were the most robust—least likely to decline and more likely than their suburban counterparts to rise,” the report said.

Prosperous zip codes were the top beneficiaries of the jobs recovery since the financial crisis. All zip codes saw job declines during the recession, each laying off several million jobs from 2007 to 2010. But by 2016, prosperous zip codes had 3.6 million jobs surplus over 2007 levels, which was more than the bottom 80% of distressed zip codes combined. It took five years for prosperous zip codes to replace all jobs lost from the financial crisis; meanwhile, distressed zip codes will never recover.

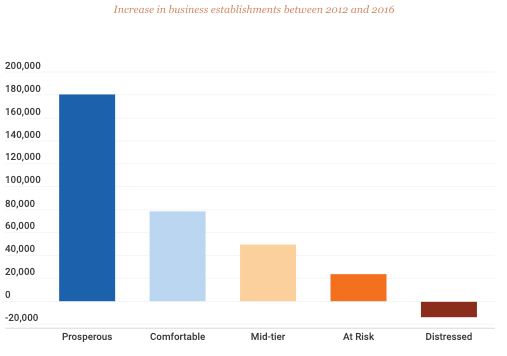

EIG shows that less than 25% of all counties have recovered from business closures from the recession.

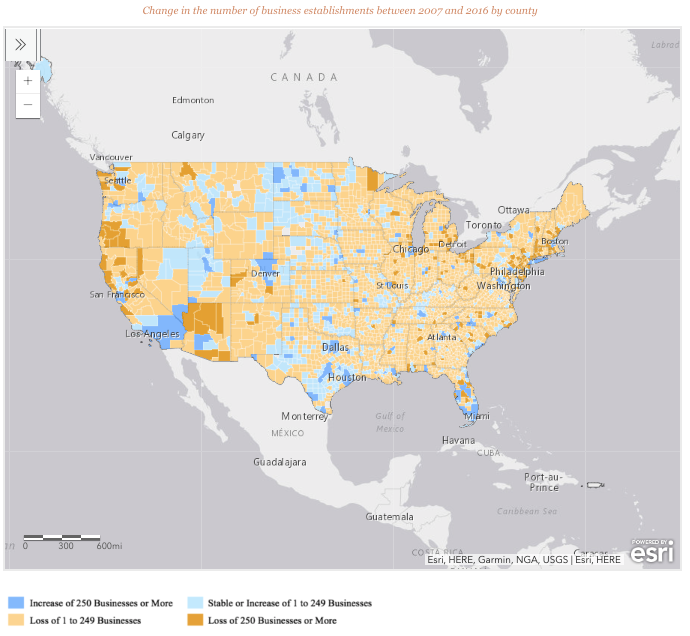

“US business formation has been dismal in both magnitude and distribution since the Great Recession. The country’s population is almost evenly split between counties that have fully replaced (with 161 million residents) and those that have not (with 157.4 million). This divide is due to the fact that highly populous counties—those with more than 500,000 residents—were far more likely to add businesses above and beyond 2007 levels than their smaller peers. Nearly three in every five large counties added businesses on net over the period, compared to only one in every five small one,” the report said.

To highlight the weak recovery and geographic unevenness of new business formation, EIG shows that the entire country had 52,800 more business establishments in 2016 than it did in 2007.

Five counties (Los Angeles, CA; Brooklyn, NY; Harris, TX (Houston); Queens, NY; and Miami-Dade, FL. ) had a combined 55,500 more businesses in 2016 than before the recession. Without those five counties, the US economy would not have recovered.

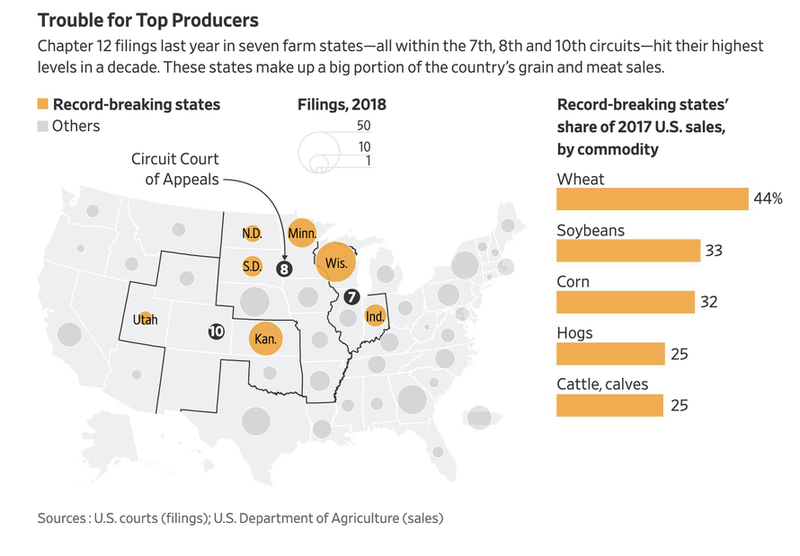

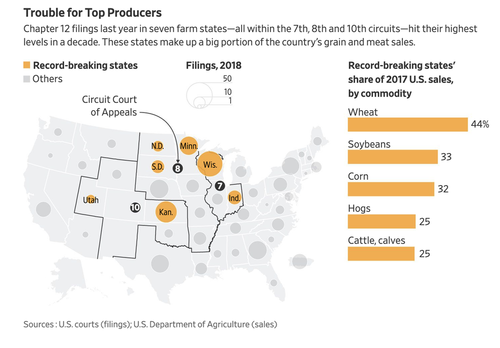

On top of deep structural changes in rural America,JPMorgan told clients last weekthat the entire agriculture complex is on the verge of disaster, with farmers in rural America caught in the crossfire of an escalating trade war.

“Overall, this is a perfect storm for US farmers,” JPMorgan analyst Ann Duignan warned investors.

Farmers are facing tremendous headwinds, including a worsening trade war, collapsing soybean exports to China, global oversupply conditions, and crop yield losses in the Midwest due to flooding. This all comes at a time when farmers are defaulting and missing payments at alarming rates, forcing regional banks to restructure and refinance existing loans.

Today’s downturn of rural America is no different than what happened in the 1920s, 1930s, and the early 1980s.

Debt among American farmers has increased to $409 billion, Agriculture Secretary Sonny Perdue warned Wednesday. That is up from $385 billion last year and is currently at levels not seen since the agricultural recession (farm crisis) of the 1980s, reported Reuters.

“Farm debt has been rising more rapidly over the last five years, increasing by 30% since 2013 – up from $315 billion to $409 billion, according to USDA data, and up from $385 billion in just the last year – to levels seen in the 1980s,” Perdue said in his testimony to the House Agriculture Committee.

Purdue told lawmakers: “Relatively firm land values have kept farmer debt-to-asset levels low by historical standards at 13.5%, and continued low-interest rates have kept the cost of borrowing relatively affordable.”

“But those average values mask areas of greater vulnerability,” he added.

The agricultural sector has experienced tremendous headwinds in the last five years amid deflationary trends in commodity prices, storms damaging crops, and more recent – supply chain disruptions into China due to President Donald Trump’s trade war.

“As producers are not able to cover year to year expenses with operating loans, they are forced into transforming operating loans into term debt which erodes their creditworthiness,” said Luis Ribera, an agricultural economist at Texas A&M University.

“On top of all that then we have the trade war which reduces the demand of US commodities given that tariffs make them more expensive and then depress the prices even more.”

US Department of Agriculture chief economist Robert Johansson said farm exports are expected to drop by as much as $1.9 billion this year, citing the deepening trade war.

China has been a significant buyer of corn, soybeans and other agricultural commodities for at least three decades, but since President Trump launched protectionist policies, Beijing responded by imposing tariffs on American agriculture products which caused trade between both countries to decline. While Beijing has promised to buy hundreds of billions of dollars in agricultural items, it has offered little relief to soybean farmers who are teetering on bankruptcy even with President Trump’s farm bailout money in hand. But as recent trade negotiations might result in an upcoming lasting agreement, it might not be enough to save hundreds of heavily indebted American farms from sliding into bankruptcy.

The number offarmers filing for bankruptcyhas soared to its highest level in a decade. And with high levels of debt, bankruptcies are expected to rise into the 2020s.

Perdue said land values have helped some farmers maintain a low debt-to-asset ratio of 13.5%. However, in the next recession, land values are expected to dip, which could trigger a deleveraging period for farmers on par with the 1980s farm crisis.

Truffles, the darling of the food scene, are not the chocolate treats that bear the same name. Not dessert truffles, true truffles are a rare delight and not an opportunity to be missed. While they are typically considered expensive food, there are ways to get your truffle fix in the United States through avenues such as truffle oil.

There are white and black truffles, and they’re as different as night and day. There are some similarities – they’re both a subterranean fungus that grows in the shadow of oak trees. However, there are over seven different truffle species found all over the world, from the Pacific Northwest to China to North Africa and the Middle East.

Truffles can be found concentrated in certain areas around the world, with the Italian countryside and French countryside being rich places of growth. Black truffles grow with the oak and hazelnut trees in the Périgord region in France. Burgundy truffles can be found throughout Europe in general, like the black summer truffle.

White truffles are typically found in the Langhe and Montferrat areas of northern Italy around the Piedmont region. Additionally, the countrysides of Alba and Asti are popular truffle hunting areas. White truffles are also found in the hill regions of Tuscany in Italy near certain trees.

Not just localized to Europe, however, New Zealand Australia also see truffles growing. The first black truffle produced in theSouthern Hemispherewas in New Zealand in 1993. In Australia, Tasmania was the origin of the first truffle harvests and the largest truffle from Australia, weighing in at 2 pounds, 6 ounces) was harvestedbyMichael and Gwynneth Williams.

In the Pacific Northwest of the U.S., four species of truffles are commercially harvested: the Oregon black truffle, the Oregon spring white, Oregon winter white truffle, and the Oregon brown truffle.

In the South, the pecan truffle is often found alongside fallen pecans. While farmers once discarded them, the gourmet food scene is slowly starting to incorporate them into seasonal dishes.

Depending which country they hail from, they’re sniffed out by specially trained dogs or pigs, then dug up by the “hunter”. They’re located through the natural aroma they release when they interact with certain plants, mammals, and insects. These interactions also encourage new colonies of the truffle fungus to appear through spore dispersal.

White Truffle fresh from the hunt

Both white and black truffles share the same appearance, that of a lumpy potato, but it’s in taste and shelf-life they differ.

Each kind of truffle is firmly in the “umami” category of taste – very earthy and doesn’t need a lot of salt to trip your tastebuds.

The black truffle is far more common, even in haute cuisine. Available for six to nine months a year, it has a stronger taste and pungent aroma that often needs acquiring. I’ve experienced a black truffle-and-olive tapenade, a perfect use for it, because it evokes a black olive-type taste.

Because of the long season and easier odds of being found, black truffles are more affordable. They’re also freezable, making a less-risky purchase for a restaurant, further enabling them to keep prices down.

On the flip-side are white truffles, Earth’s gold. Typically valued at as much as $3,000 per pound, they inspire a big black market. Even legally, they can be outrageous in price.The Atlantic writes, “In 2010, Macau casino tycoon Stanley Ho spent $330,000 on two pieces that weighed 2.87 pounds.”

Internationally, white truffles are big industry. Autumn may yield a truffle experience for you even here. The USA is currently third world-wide for truffle harvest volumes. Stick to truffle towns where restaurants hunt their own, and you maybe be surprised at bargains you find. I was shocked to only spend $20 for my white truffle meal in Croatia.

White truffles cannot be frozen and have a short shelf-life, up to about 10 days. They’re best devoured as soon as possible. Their season is short too – only three to four months each year, September through to as late as January.

I’ve heard of their seasons ending as early as November, though. They’re more elusive to find, often in different forest clusters than their black counterparts. All this computes to costing big bucks.

Even if you dislike black truffles, try fresh white truffles if you ever can. They’re a completely different flavor profile. Instead of black olives, think Parmesan cheese meets mushrooms. It’s a delicate, aromatic flavor – still earthy, but far from overbearing.

Wine and food pairings must let the white truffle take center stage, lest they overpower it. Think polenta with lots of Parmesan and excessive shavings on top.

If you can’t have the real truffle experience, you can buy truffle products flooding the market. These include truffle-infused oils, jams, tapenades, and so forth. Some will use extracts, which are as authentic to the real thing as any extract is. Think orange or lemon or almond extracts. Are they true to the real experience? Not really, but they have their own appeal.

With a growing popularity on the world market, cunning agriculturalists and truffle hunters are trying to farm truffles with mixed results. So far it seems truffles are Earth’s alchemy – a rare treat to remain rare.

Speaking for myself, I was sure I’d hate the pungent fungus, but I felt obligated to try them. Black truffles were a taste I could grow to appreciate, but I’m not a big fan of black olives either. I had decadently expensive dark chocolate-and-black truffle ice cream, though, and that was tasty.

Still, I long for the day I cross paths with white truffles again. The simple dish of polenta and white truffles stands as one of the greatest meals of my life.

There’s a reason they’re sometimes literally worth more than their weight in gold.

(Reuters) – Amazon.com Inc (AMZN.O) said it will cut prices on a range of popular goods as it completes its acquisition of Whole Foods Market Inc (WFM.O), sending shares of rival grocers tumbling on fears that brutal market share battles will intensify.

Amazon’s $13.7 billion purchase of Whole Foods, which will be completed on Monday, has been hanging over a brick-and-mortar retail sector unsure of how to respond to the world’s biggest online retailer.

Shares of Kroger Co (KR.N), the biggest U.S. supermarket operator, closed down 8 percent, while Wal-Mart Stores Inc (WMT.N), the biggest U.S. food seller, closed down 2 percent.

Amazon also said it will start selling Whole Foods brand products on its website, a move that sent down shares of packaged food sellers including Kellogg Co (K.N).

The S&P 500 Food Retail index closed down almost 5 percent as more than $10 billion was wiped off the market value of big food sellers.

Amazon said members of its $99-per-year Prime shopping club would eventually be rolled into Whole Foods’ customer rewards program and be eligible for special offers and discounts.

“There was never any doubt that Amazon would lower prices, and even offer further discounts in-store to Prime members,” said Baird Equity Research analyst Colin Sebastian.

‘LAND GRAB’

Amazon said that starting on Monday it will cut prices on organic grocery staples such as bananas, avocados, brown eggs, farmed salmon and tilapia, baby kale and lettuce, some apples, butter and other products.

“It does not look like they will go kamikaze on pricing,” said Roger Davidson, president of consulting firm Oakton Advisory Group and a former retail executive. “They will lower prices on consequential items to drive traffic and sales but not do a whole store price reduction which could really damage gross margin and potentially wipe out operating margin.”

Lowering prices could stem defections by price-sensitive Whole Foods shoppers, and help the grocer shed its “Whole Paycheck” reputation for high prices that are generally 15 to 25 percent above rivals. It could also bring in new consumers who can then be urged to shop for food and other products online.

“It’s ultimately a nice land grab,” said Bill Bishop of retail consultancy Brick Meets Click, and a way to get customers “thinking about buying healthy food from Amazon.”

FAT PROFITS

The planned price cuts would have been a tough sell to Whole Foods’ investors, who had grown used to fat profits from the upscale chain, but are more in line with Amazon’s broader strategy of sacrificing short-term profit for long-term market dominance.

“Amazon is more focused on driving volume and improving service at the expense of profit margins,” said Sebastian. “Long-term, this strategy works because the absolute profit dollars can still be significant.”

Amazon’s willingness to take lower profit margins ups the ante in the increasingly costly grocery price war.

“In some cases grocery retailers have had to invest between $500 million to $1 billion in order to reduce prices to a level that retained customers and resulted in a net increase in customers,” said Brittain Ladd, who until earlier this year was a senior manager working to globally roll out AmazonFresh, Amazon’s grocery delivery service.

Adding Whole Foods benefits should help Amazon attract more shoppers to its successful Prime scheme, which features two-day shipping for eligible purchases and unlimited streaming of movies and TV shows. Amazon has more than 60 million Prime members, according to analyst estimates.

Whole Foods has rolled out a loyalty program at its smaller, lower-priced 365 by Whole Foods chain, which offers members 10 percent off more than 100 items in the stores. The program is still being tested in the main Whole Foods chain.

Beyond that, some Whole Foods stores will get Amazon Lockers, where customers can receive online orders and make returns.

John Mackey will remain chief executive of Whole Foods and the company will operate as a subsidiary and continue to be headquartered in Austin, Texas, the companies said on Thursday.

When it comes to housing, sometimes it seems we never learn. Just when America appeared to be recovering from the last housing crisis—the trigger, in many ways, for 2008’s grand financial meltdown and the beginning of a three-year recession—another one may be looming on the horizon.

There are at several big red flags.

For one, the housing market never truly recovered from the recession.TruliaChief Economist Jed Kolko points out that, while the third quarter of 2014 saw improvement in a number of housing key barometers, none have returned to normal, pre-recession levels. Existing home sales are now 80 percent of the way back to normal, while home prices are stuck at 75 percent back, remaining undervalued by 3.4 percent. More troubling, new construction is less than halfway (49 percent) back to normal. Kolko also notes that the fundamental building blocks of the economy, including employment levels, income and household formation, have also been slow to improve. “In this recovery, jobs and housing can’t get what they need from each other,” he writes.

Americans are spending more than 33 percent of their income on housing.

Second, Americans continue to overspend on housing. Even as the economy drags itself out of its recession, a spate of reports show that families are having a harder and harder time paying for housing. Part of the problem is that Americans continue to want more space in bigger homes, and not just in the suburbs but in urban areas, as well. Americans more than 33 percent of their income on housing in 2013, up nearly 13 percent from two decades ago, according to newly released data from the Bureau of Labor Statistics (BLS). The graph below plots the trend by age.

Over-spending on housing is far worse in some places than others; the housing market and its recovery remain highly uneven. Another BLS report released last month showed that households in Washington, D.C., spent nearly twice as much on housing ($17,603) as those in Cleveland, Ohio ($9,061). The chart below, from the BLS report, shows average annual expenses on housing related items:

(Bureau of Labor Statistics)

The result, of course, is that more and more American households, especially middle- and working-class people, are having a harder time affording housing. This is particularly the case in reviving urban centers, as more affluent, highly educated and creative-class workers snap up the best spaces, particularly those along convenient transit, pushing the service and working class further out.

Last but certainly not least, the rate of home ownership continues to fall, and dramatically. Home ownership has reached its lowest level in two decades—64.4 percent (as of the third quarter of 2014). Here’s the data, from the U.S. Census Bureau:

(Data from U.S. Census Bureau)

Home ownership currently hovers from the mid-50 to low-60 percent range in some of the most highly productive and innovative metros in this country—places like San Francisco, New York, and Los Angeles. This range seems “to provide the flexibility of rental and ownership options required for a fast-paced, rapidly changing knowledge economy. Widespread home ownership is no longer the key to a thriving economy,” I’ve written.

What we are going through is much more than a generational shift or simple lifestyle change. It’s a deep economic shift—I’ve called it the Great Reset. It entails a shift away from the economic system, population patterns and geographic layout of the old suburban growth model, which was deeply connected to old industrial economy, toward a new kind of denser, more urban growth more in line with today’s knowledge economy. We remain in the early stages of this reset. If history is any guide, the complete shift will take a generation or so.

It’s time to impose stricter underwriting standards and encourage the dense, mixed-use, more flexible housing options that the knowledge economy requires.

The upshot, as the Nobel Prize winner Edmund Phelpshas written, is that it is time for Americans to get over their house passion. The new knowledge economy requires we spend less on housing and cars, and more on education, human capital and innovation—exactly those inputs that fuel the new economic and social system.

But we’re not moving in that direction; in fact, we appear to be going the other way. This past weekend, Peter J. Wallison pointed out in a New York Times op-ed that federal regulators moved back off tougher mortgage-underwriting standards brought on by 2010’s Dodd-Frank Act and instead relaxed them. Regulators are hoping to encourage more home ownership, but they’re essentially recreating the conditions that led to 2008’s crash.

Wallison notes that this amounts to “underwriting the next housing crisis.” He’s right: It’s time to impose stricter underwriting standards and encourage the dense, mixed-use, more flexible housing options that the knowledge economy requires.

During the depression and after World War II, this country’s leaders pioneered a series of purposeful and ultimately game-changing polices that set in motion the old suburban growth model, helping propel the industrial economy and creating a middle class of workers and owners. Now that our economy has changed again, we need to do the same for the denser urban growth model, creating more flexible housing system that can help bolster today’s economy.

The dramatic resurgence of the oil industry over the past few years has been a notable factor in the national economic recovery. Production levels have reached totals not seen since the late 1980s and continue to increase, and rig counts are in the 1,900 range. While prices have dipped recently, it will take more than that to markedly slow the level of activity. Cycles are inevitable, but activity is forecast to remain at relatively high levels.

An outgrowth of oil and gas activity strength is a need for additional workers. At the same time, the industry workforce is aging, and shortages are likely to emerge in key fields ranging from petroleum engineers to experienced drilling crews. I was recently asked to comment on the topic at a gathering of energy workforce professionals. Because the industry is so important to many parts of Texas, it’s an issue with relevance to future prosperity.

Although direct employment in the energy industry is a small percentage of total jobs in the state, the work is often well paying. Moreover, the ripple effects through the economy of this high value-added industry are large, especially in areas which have a substantial concentration of support services.

Employment in oil and gas extraction has expanded rapidly, up from 119,800 in January 2004 to 213,500 in September 2014. Strong demand for key occupations is evidenced by the high salaries; for example, median pay was $130,280 for petroleum engineers in 2012 according to the Bureau of Labor Statistics (BLS).

Due to expansion in the industry alone, the BLS estimates employment growth of 39 percent through 2022 for petroleum engineers, which comprised 11 percent of total employment in oil and gas extraction in 2012. Other key categories (such as geoscientists, wellhead pumpers, and roustabouts) are also expected to see employment gains exceeding 15 percent. In high-activity regions, shortages are emerging in secondary fields such as welders, electricians, and truck drivers.

The fact that the industry workforce is aging is widely recognized. The cyclical nature of the energy industry contributes to uneven entry into fields such as petroleum engineering and others which support oil and gas activity. For example, the current surge has pushed up wages, and enrollment in related fields has increased sharply. Past downturns, however, led to relatively low enrollments, and therefore relatively lower numbers of workers in some age cohorts. The loss of the large baby boom generation of experienced workers to retirement will affect all industries. This problem is compounded in the energy sector because of the long stagnation of the industry in the 1980s and 1990s resulting in a generation of workers with little incentive to enter the industry. As a result, the projected need for workers due to replacement is particularly high for key fields.

The BLS estimates that 9,800 petroleum engineers (25.5 percent of the total) working in 2012 will need to be replaced by 2022 because they retire or permanently leave the field. Replacement rates are also projected to be high for other crucial occupations including petroleum pump system operators, refinery operators, and gaugers (37.1 percent); derrick, rotary drill, and service unit operators, oil, gas, and mining (40.4 percent).

Putting together the needs from industry expansion and replacement, most critical occupations will require new workers equal to 40 percent or more of the current employment levels. The total need for petroleum engineers is estimated to equal approximately 64.5 percent of the current workforce. Clearly, it will be a major challenge to deal with this rapid turnover.

Potential solutions which have been attempted or discussed present problems, and it will require cooperative efforts between the industry and higher education and training institutions to adequately deal with future workforce shortages. Universities have had problems filling open teaching positions, because private-sector jobs are more lucrative for qualified candidates. Given budget constraints and other considerations, it is not feasible for universities to compete on the basis of salary. Without additional teaching and research staff, it will be difficult to continue to expand enrollment while maintaining education quality. At the same time, high-paying jobs are enticing students into the workforce, and fewer are entering doctoral programs.

Another option which has been suggested is for engineers who are experienced in the workplace to spend some of their time teaching. However, busy companies are naturally resistant to allowing employees to take time away from their regular duties. Innovative training and associate degree and certification programs blending classroom and hands-on experience show promise for helping deal with current and potential shortages in support occupations. Such programs can prepare students for well-paying technical jobs in the industry. Encouraging experienced professionals to work past retirement, using flexible hours and locations to appeal to Millennials, and other innovative approaches must be part of the mix, as well as encouraging the entry of females into the field (only 20 percent of the current workforce is female, but over 40 percent of the new entries).

Industry observers have long been aware of the coming “changing of the guard” in the oil and gas business. We are now approaching the crucial time period for ensuring the availability of the workers needed to fill future jobs. Cooperative efforts between the industry and higher education/training institutions will likely be required, and it’s time to act.

Billionaire real estate investor Jeff Greene’s massive Palazzo di Amore in Beverly Hills hit the market today for $195 million, making it America’s new most expensive home for sale.

Set on 25 acres overlooking Los Angeles about five to seven minutes by car to Rodeo Drive, the estate includes a 35,000-square-foot main home plus a 15,000-square-foot entertainment center and a separate guest home, containing a total of 12 bedrooms and 23 bathrooms across the various structures. The massive Mediterranean-style spread also comes with a working vineyard that produces six types of wine. Joyce Rey and Stacy Gottula, both of Coldwell Banker Previews International, are the listing agents.

Building the Palazzo was a seven-and-a-half-year labor of love for Greene. In 2007 the real estate investor, who has a net worth of $3 billion, according to Forbes, purchased the home out of bankruptcy proceedings from the previous owners–a Middle Eastern businessman and his wife–paying a reported $35 million. “I have no logical explanation for why we spent the next seven-and-a-half years building this house,” Greene told Forbes. “But that’s the world of building very detailed custom homes.”

Greene hired mega-mansion builder Mohamed Hadid to do the lion’s share of the design, but remained intimately involved in nearly every decision (along with his wife), pouring in tens of millions to complete the estate. (Finishing touches were just put on last month.) At one point, a Peruvian woodcarver was on site for four months to hand-carve the fireplace mantels, Greene says.

Because the property was purchased out of bankrutpcy, Greene got the deed but not the house plans, he says. The partially-finished palazzo had no driveways, so Greene and Hadid had to design and build one. Same for the swimming pool. The land also came with a curious concrete foundation with nothing on it. At first, Greene and his wife planned to tear it out. Then they changed course to: ”Let’s just build an entertainment complex,” Greene says. Today, that space houses a bowling alley, a 50-seat private screening room, and a ballroom with a DJ booth and a revolving dance floor

Palazzo di Amore would make the ideal setting for some grand entertaining. The first floor of the main house features a chef’s kitchen with a commercial size walk-in refrigerator, plus a secondary staff kitchen, butler’s pantry, two staff rooms, a three-car attached garage and two private offices with separate entry. The living room, dining room, breakfast room, game room, office and family room all open onto grounds that face a waterfall set into the hillside. A separate guest house brings the total livable square footage to 53,000. And the property features garage parking for 27 cars and can accommodate up to 150 cars on site.

Plus, what better way to impress all these hypothetical guests than with your own private wine? When Greene purchased the land in 2007, the vineyards were producing grapes but hadn’t yet been turned into wine. So the billionaire hired three full-time people to turn make the vineyards productive. Now, “Beverly Hills Vineyards” produces between 350 and 500 cases a year of six varietals: Sangiovese, Syrah, Cabernet, Merlot, Rose, and Sauvignon Blanc. “We drink it all the time,” Greene says.

The estate also features facilities for showing off that home-grown wine, with a 3,000-bottle wine cellar as well as a tasting room in the main house; as well as lower-level space for an additional 10,000 bottles (plus barrels) in a temperature-controlled room, flanked by an additional tasting room.

Of course, the home would also make a fabulous private retreat. The private living space on the second floor of the main home contains two wings, one with a guest suite and the 5,000-square-foot master suite, with hand-carved fireplace mantel, Juliet balconies, and his-and-hers baths. The ‘his’ bath features a Turkish-style spa with hand-painted wood panels, a fireplace, and floor-to-ceiling Moroccan tiles. On the opposite wing, there are four additional bedroom suites, including one VIP suite with silk-upholstered walls and a full kitchen. The grounds surrounding the home contain a 128-foot reflecting pool and fountain. Also, a swimming pool, a spa, a barbecue area and a tennis court.

The massive Mediterranean-style spread was originally designed by architect Bob Ray Offenhauser and designer Alberto Pinto. Rey, the listing agent, says she expects the home to sell to a foreign buyer, since all the Los Angeles area homes over $50 million sold this year have gone to foreigners.

To date, the most expensive home sold in the U.S. is the $147 million East Hampton spread picked up by Jana Partners founder Barry Rosenstein earlier this year. The record-setting price tag is based on nation-wide sales of major properties priced around $100 million, Rey says. She cited Copper Beech Farm, the $120 million Greenwich, Conn., property that sold earlier this year, as well as the penthouse at One57, the new luxury condominium towers in Midtown Manhattan, that billionaire Bill Ackman and a group of investors reportedly purchased for north of $90 million. “None of those properties had the land, the amenities that we’re offering here,” Rey says.

As for Greene, who lives in Florida and has a home in Malibu and another house in the Hamptons, he’s simply ready to move on with his life. ”I’m a control freak, and that’s why these projects aren’t good for me,” he says. “It’s just too many years, too long. But hopefully the buyer will come along who will appreciate the fruits of our labor.”

In a recent Wall Street Journal article, several couples across the country are quoted saying that instead of downsizing to a new home, they are choosing to live with their adult children.

This is what many families across the country are doing for both a “peace of mind” and for “higher property values.”

“For both domestic and foreign buyers, the hottest amenity in real estate these days is an in-law unit, an apartment carved out of an existing home or a stand-alone dwelling built on the homeowners’ property,” writes Katy McLaughlin of the WSJ. “While the adult children get the peace of mind of having mom and dad nearby, real-estate agents say the in-law accommodations are adding value to their homes.”

And how much more are these homes worth? In an analysis by Zillow, the homes with this type of living accommodations were priced about 60 percent higher than regular single-family homes.

Local builders are noticing the trend, too. Horsham based Toll Brothers are building more communities that include both large, single-family homes and smaller homes for empty nesters, the company’s chief marketing officer, Kira Sterling, told the WSJ.

Count Dracula, the central character of Irish author Bram Stoker’s classic vampire novel, eagerly left for England in search of new blood, in a story that popularized the Romanian region of Transylvania. Today, house hunters are invited to make the reverse journey now that Romania is a member of the European Union and that restrictions were lifted this year on purchases of local real estate by the bloc’s nationals.

Britain’s Prince Charles, for one, unwinds every year in Zalanpatak. The mud road leading to the remote village stretches for miles, with the clanging of cow bells accompanying tourists making the trek.

Elsewhere in the world, the heir to the British throne occupies great castles and sprawling mansions. In rural Romania, he resides in a small old cottage. His involvement, since 2006, in the restoration of a few local farmhouses has given the hamlet global popularity and added a sense of excitement about Transylvania living.

A living room in Bran Castle, a Transylvania property marketed as Count Dracula’s castle. The home is for sale, initially listed for $78 million.

Transylvania, with a population of more than seven million in the central part of Romania, has a number of high-end homes on the market. And, yes, one is a castle. Bran Castle in Brasov county is marketed as the home of Count Dracula. In reality it was a residence of Romanian Queen Marie in the early 20th century. In 2007, the home was available for $78 million. The sellers are no longer listing a price, said Mark A. Meyer, of Herzfeld and Rubin, the New York attorneys representing the queen’s descendants, but will entertain offers.

Foreign buyers had been focused on Bucharest, where there was speculative buying of apartments after the country joined the EU in 2007. But Transylvania has been luring house hunters away from the capital city.

A guesthouse on the property in Zalanpatak, Transylvania, that is owned by Britain’s Prince Charles. His presence has boosted interest in Romanian real estate.

Transylvania means “the land beyond the forest” and the region is famous for its scenic mountain routes. Brasov, an elegant mountain resort and the closest Transylvanian city to the capital, has many big villas built in the 19th century by wealthy merchants. A 10-room townhouse from that period in the historic city center is listed for $2.7 million. For $500,000, a 2,200-square-foot apartment offers rooftop views of the city and the surrounding mountains.

A seven-bedroom mansion in the nearby village of Halchiu, close to popular skiing resorts, is on the market for $2.4 million. The modern villa features two huge living rooms, a swimming pool, a tennis court and spectacular views of the Carpathian Mountains.

The village, founded by Saxons in the 12th century, has rows of historic houses across the street. Four such buildings were demolished to make way for the mansion, completed in 2010.

A $2.4 million mansion is for sale in Halchiu village.

“Rather than invest a million or more to buy an existing house, the wealthy prefer to build on their own because construction materials and work is cheaper,” said Raluca Plavita, senior consultant at real-estate firm DTZ Echinox in Bucharest.

Non-EU nationals can’t purchase land outright—although they may use locally registered companies to circumvent the restriction—but they can buy buildings freely, said Razvan Popa, real-estate partner at law firm Kinstellar. High-end properties are out of reach for many Romanians, who make an average of $500 in monthly take-home pay.

The country saw a rapid inflation of real-estate prices before 2008, on prospects of Romania’s entry to the EU and the North Atlantic Treaty Organization, as well as aggressive lending by banks. Values then fell by half during the global financial crisis.

The economy is stronger now, with the International Monetary Fund estimating 2.4% growth this year. But the country is still among Europe’s poorest. Its isolation during the dictatorship of Nicolae Ceausescu gave it a bad image.

The interior of the seven-bedroom Halchiu mansion, which was built on the site of four traditional Saxon homes.

“Interest in Romania isn’t comparable with Prague or Budapest where some may be looking to buy a small apartment with a view of Charles Bridge or the Danube,” said Mr. Popa, the real-estate lawyer.

The international publicity around Prince Charles’s properties offers a counterbalance to some of the negative press Romania has received in Western Europe, which is worried about well-educated Romanians moving to other countries to provide inexpensive labor.

The Zalanpatak property is looked after by Tibor Kalnoky, a descendant of a Hungarian aristocratic family. The 47-year-old studied in Germany to be a veterinarian and, after reclaiming family assets in Romania, has managed the prince’s property and has hosted him during his visits.

These occasional visits are enough to attract scores of tourists throughout the year to the formerly obscure village in a Transylvanian valley. The fact that few street signs lead there,that the property offers no Internet or TV and that cellphone signals are absent for miles, seems only to add to the mystery of the place.