The 2023 housing market continues its correction, with home prices now falling month over month and year over year according to the National Association of Realtors. On top of that foreclosure starts increased 20% month over month and 22% year over year, and more importantly the speed of the foreclosure process through completion increased 12% quarter over quarter. Additionally JP Morgan sent out a note informing us that lending conditions have now tightened faster than they did during the great financial crisis, with the full effects not being felt until late 2023 or early 2024.

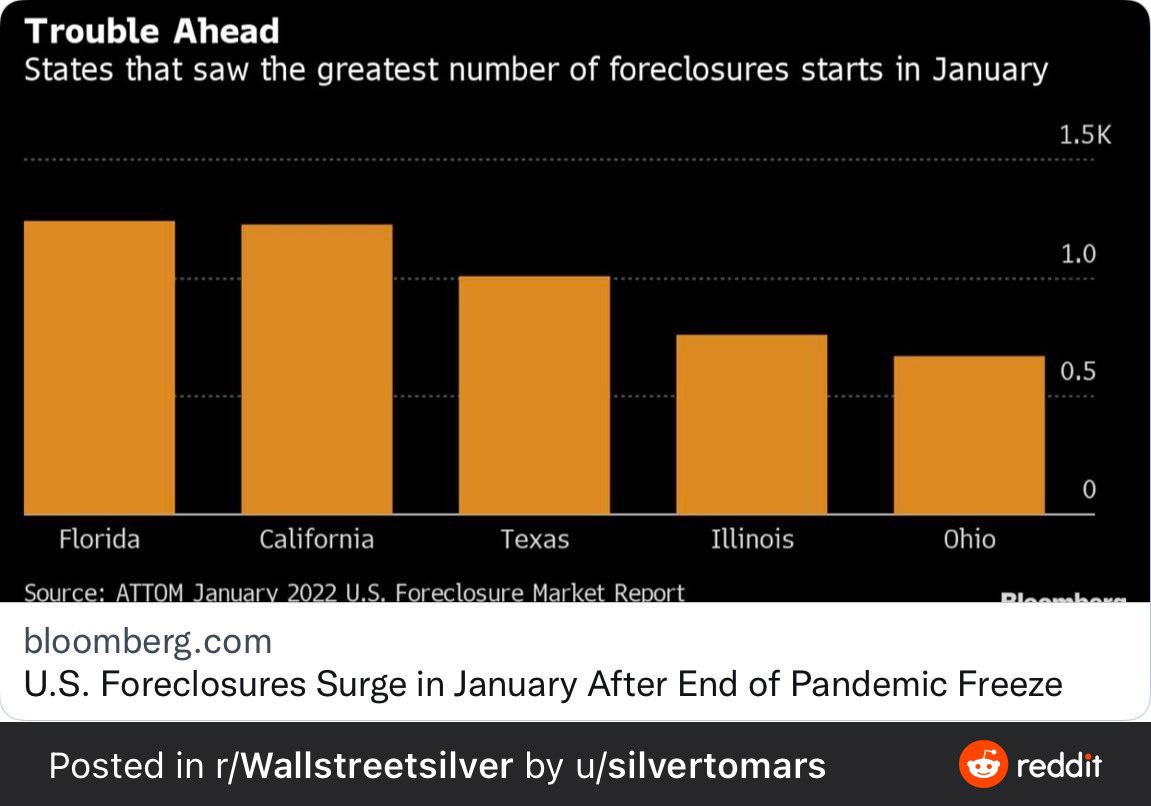

(Alexandre Tanzi) Foreclosures on homes in the U.S. surged in January after a pandemic moratorium ended, though they remained well below pre-Covid levels, according to new data from RealtyTrac.

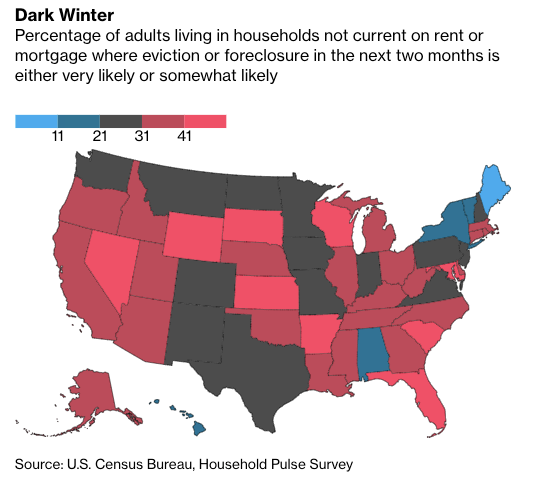

A dark covid winter is descending on the working-poor of America as millions of adults face eviction or foreclosure in the next few months. Bloomberg, citing a survey that was conducted on Nov. 9 by the U.S. Census Bureau, shows 5.8 million adults face eviction or foreclosure come Jan. 1. That accounts for 32.5% of the 17.8 million adults currently behind rent or mortgage payments.

(John Myers) Gov. Gavin Newsom’s administration said Friday it would begin work on transferring $331 million back into a special fund designed to help California homeowners hit hard by the recession-era mortgage crisis, money that the courts have ruled was wrongly used to help balance the state budget.

The California Supreme Court refused earlier this week to hear an appeal by the administration disputing lower court rulings that found the state mistakenly used a portion of the money — paid by large banks and lenders as part of a nationwide legal agreement in 2012 — to pay off housing bonds. In some cases, those bonds were enacted a decade before the mortgage settlement. In all, three years of state budget expenses were covered by a portion of what California received from the mortgage settlement.

The decision to use the money was championed by Newsom’s predecessor, former Gov. Jerry Brown. Legislators subsequently ratified the plan, and last year went even further: They passed legislation seeking to block a court ruling to repay more than $331 million into a fund originally designed for statewide homeowner assistance efforts. Groups that waged a five-year court battle over the funds expressed relief that the legal fight was finally over.

“Truth prevails,” said Faith Bautista, president and chief executive of the National Asian American Coalition. “They’re now facing the reality that the money belonged to the homeowners in distress.”

While the money in question was undoubtedly tempting at the time it was diverted — California’s budget was still reeling from successive years of back-to-back deficits — the state’s coffers are now overflowing. The budget signed by Newsom last month includes $19.2 billion in cash reserves, making the repayment of the mortgage settlement money limited only by how fast state leaders can take action. The Legislature will return next month for the final weeks of its 2019 session.

The money diverted to state budget needs was a small portion of what both California homeowners and the government received from the national settlement agreed to by 49 states in 2012. Those states, along with the federal government and the District of Columbia, had earlier filed suit against the nation’s five largest mortgage servicers: Ally (formerly known as GMAC), Bank of America, Citigroup, J.P. Morgan Chase and Wells Fargo. The legal action alleged a number of federal law violations, and the financial institutions agreed to pay more than $20 billion to homeowners affected by the mortgage crisis. The companies also agreed to pay the states a total of $2.5 billion.

California’s share of the state payments was $410 million, to be used for a variety of services directed by then-Atty. Gen. Kamala Harris. But most of the money was used instead for budget-balancing items which, while related to housing, were long-term costs that further shrank the funds available for basic government services. A coalition including representatives for Asian American and Latino communities sued the state in 2014 over its decision to use the money to help erase a projected budget deficit. A Sacramento judge ruled for the coalition in 2015 and the 3rd District Court of Appeal agreed with that ruling last year.

In April, the same appeals court again rebuked state officials.

“It is the judicial branch that has the constitutional authority to interpret statutes,” the three-judge panel wrote in its ruling, stating that the mortgage settlement “money was unlawfully diverted from a special fund in contravention of the purposes for which that special fund was established.”

On Wednesday, the California Supreme Court refused Newsom’s request to hear the case, allowing the appeals ruling to stand.

“Now that the Supreme Court has issued its decision in this matter, we will move forward to implement the ruling,” said H.D. Palmer, a spokesman for the California Department of Finance.

Bautista, whose Daly City-based group works with low-income communities of color across the state, said she hopes the $331 million will be supplemented by money from the nation’s leading lenders to offer services such as down payment assistance for those who went through foreclosure during the housing crisis and want to again own a home. She said other services, including financial literacy efforts and those helping Californians with low credit scores, should also be considered. And she urged Newsom to make such efforts part of his larger discussion about the state’s housing crisis.

“People are hurting in East L.A., Riverside, the Central Valley,” Bautista said. “Let’s pick what’s best and use the money wisely.”

Neil Barofsky, an attorney who represented the groups that fought the cash diversion in the courts, said it was disappointing that state officials spent so many years on “frivolous appeals,” culminating in what he called the “ginned- up legislative action” last year designed to block repayment of the money and the appeals court ruling.

“We understand it was a desperate time for the state when this happened,” he said. “But once we returned to surpluses, the idea that they would just keep fighting this has been breathtaking.”

One month ago we discussed why according to the recent data, the “Housing Market Headed For “Broadest Slowdown In Years.” Fast forward to today, when we received the latest confirmation that the US housing market appears to have recently hit a downward inflection point: according to the just released July 2018 U.S. Foreclosure Market Report released byATTOM Data Solutions, foreclosure starts in July increased by 1% from a year ago — the first year-over-year increase following 36 consecutive months of decreases.

Foreclosures rose from a year ago in 96 of the 219 metropolitan statistical areas, or 44% of the markets analyzed in the report; 33 of those areas posted their third straight monthly increase. A total of 30,187 U.S. properties started the foreclosure process for the first time in July, up 1 percent from the previous month and while the increase was less than 1% from a year ago, it marked the first annual increase in exactly 3 years.

21 states posted a year-over-year increase in foreclosure starts in July, including Florida (up 35 percent); California (up 3 percent); Texas (up 7 percent); Illinois (up 7 percent); and Ohio (up 2 percent).

Metro areas posting year-over-year increases in foreclosure starts in July included Los Angeles, California (up 20 percent); Houston, Texas (up 76 percent); Philadelphia, Pennsylvania (up 10 percent); Miami, Florida (up 29 percent); and San Francisco, California (up 10 percent).

“The increase in foreclosure starts is not just a one-month anomaly in many local markets given that July represented the third consecutive month with a year-over-year increase in 33 metro areas, including Los Angeles, Miami, Houston, Detroit, San Diego and Austin,” said Daren Blomquist, senior vice president with ATTOM Data Solutions.

“Gradually loosening lending standards over the past few years have introduced a modicum of risk back into the housing market, and that additional risk is resulting in rising foreclosure starts in a diverse set of markets across the country. Most susceptible to rising foreclosure starts are affordability-challenged markets where home buyers are more financially stretched and markets with some type of trigger event such as a natural disaster or large-scale layoffs.”

The data comes shortly after aseparate reportfound that there has been a plunge of sales in ultra-luxury real estate in New York City, where apartments that cost $5 million or more have seen their sale plunge more than 31% in the first 6 months of the year.

The surprising reversal in the US housing sector comes at a time when the US economy is reportedly firing on all four cylinders, with the stock market at all time highs and not long after the Department of Commerce revised income and spending data to “discover” that US households had actually saved twice as much as previously expected. Which begs the question: is the rise in interest rates a sufficiently adverse development to offset all the other favorable trends in the economy, or is something more sinister – and unknown – taking place in the US economy.

As a reminder it is housing – and not financial markets or stocks – that has traditionally been the most relevant, and aspirational, asset for the US middle class and as such is the best indicator of economic prosperity (or lack thereof) for a majority of the US population. And recent trends are anything but optimistic.

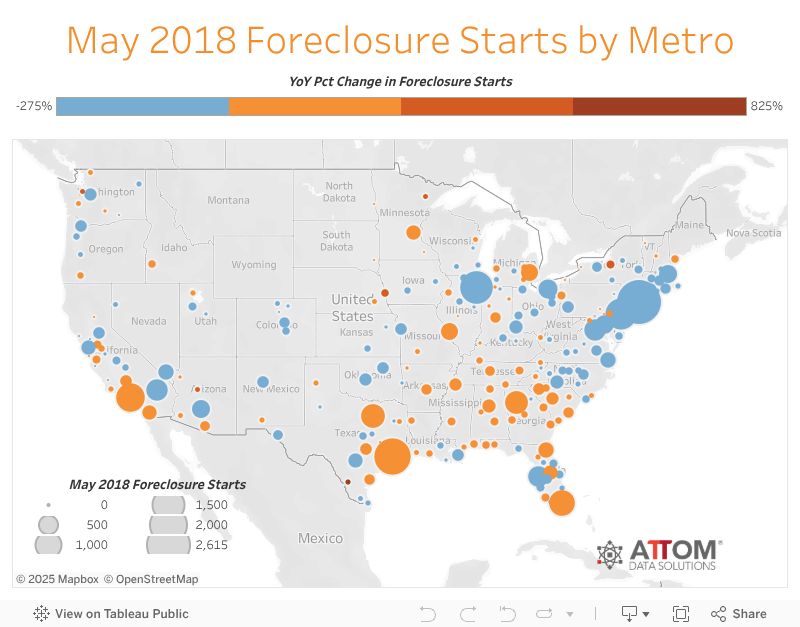

Counter to the national trend, several housing markets saw foreclosure starts rise year over year last month, according to a new report from ATTOM Data Solutions, a real estate data firm.

Forty-three percent of local markets saw an annual increase in May in foreclosure starts. Foreclosure starts were most on the rise in Houston, which saw a 153 percent jump from a year ago. Hurricane Harvey struck the Houston metro area in August 2017, tying with Hurricane Katrina as the costliest tropical cyclone on record, and has contributed to many recent foreclosures in the area. Other areas that are seeing foreclosure starts rise: Dallas-Fort Worth (up 46% year over year); Los Angeles (up 14 percent); Atlanta (up 7 percent); and Miami (up 4 percent).

A total of 33,623 U.S. properties started the foreclosure process in May, which is down 6 percent from a year ago. But a number of states—23 states and the District of Columbia—posted a year-over-year increase in foreclosure starts in May.

Overall, the metro areas with the highest foreclosure rates in May were: Flint, Mich.; Atlantic City, N.J.; Trenton, N.J.; Philadelphia; and Columbia, S.C.

View the chart below to see foreclosure starts by metro area.

Home ownership is at a 48-year low, driven in part by a shocking pattern of foreclosure that put 9.4 million out of their homes during the recent recession, according to a Harvard survey.

In its “State of the Nation’s Housing 2016,” Harvard said that “the U.S. homeownership rate has tumbled to its lowest level in nearly a half-century.”

Figures from the St. Louis Fed showed a home ownership rate of 63.5 percent. The last time it was lower was in 1967.

“A critical but often overlooked factor is the role of foreclosures in depleting the ranks of homeowners. Indeed, CoreLogic estimates that more than 9.4 million homes (the majority owner-occupied) were forfeited through foreclosures, short sales, and deeds-in-lieu of foreclosure from the start of the housing crash in 2007 through 2015,” said the report.

The report also noted that the number of people using at least 30 percent of their income for housing rose, as our Joseph Lawler reported this week. It said, “40.9 million Americans, both homeowners and renters, spend more than 30 percent of their income on housing, including 19.8 million who spend over half of their income for housing.”

At the same time, said Harvard, the drive for the American Dream has been braked by low incomes, higher prices and bad credit.

Harvard:

“Just as exits from homeownership have been high, transitions to owning have been low. Tight mortgage credit is one explanation, with essentially no home purchase loans made to applicants with subprime credit scores (below 620) since 2010 and a sharp retreat in lending to applicants with scores of 620–660 compared with the early 2000s. And given that the homeownership rate tends to move in tandem with incomes, the 18 percent drop in real incomes among 25–34 year olds and the 9 percent decline among 35–44 year olds between 2000 and 2014 no doubt played a part as well.”

It’s 9:30 a.m. on a recent sunny Friday, and 60 people have crammed into an airport hotel conference room in Northern Virginia to hear Kevin Shortle, a veteran real estate professional with a million-watt smile, talk about “architecting a deal.”

Some have worked in real estate before, flipping houses or managing rentals. But the deals Shortle, lead national instructor for a company called Note School, is describing are different: He teaches people how to buy home notes, the building blocks of housing finance.

While titles and deeds establish property ownership, notes — the financial agreements between lenders and home buyers — set the terms by which a borrower will pay for the home. Financial institutions have long passed them back and forth as they re-balance their portfolios.

But the trade in delinquent notes has exploded in the post-financial-crisis world. As government entities like Fannie Mae and Freddie Mac have struggled with the legacies of the housing bust, they’ve sold billions of dollars’ of delinquent notes to big institutional investors, who resell them in turn.

A sign outside a foreclosed home for sale in Princeton, Ill, in January 2014.

And people like the ones in the Sheraton now pay good money to learn how to pursue what Note School calls “rich rewards.” The result: a marketplace where thousands of notes are bought and sold for a fraction of the value of the homes they secure.

A buyer can renegotiate with the homeowner, collecting steady cash. Or she might offer a “cash for keys” payout and seek a tenant or new owner. If all else fails, she can foreclose.

For some housing market observers, the churn in notes is a sign that the financial crisis hasn’t fully healed — and a fresh source of potential abuses. But the people listening to Shortle saw opportunity as he explained how they can “be the bank” for people with mortgage-payment problems.

“You can make a lot of money in the problem-solving business,” Shortle said.

How home notes move through a healing housing market

Since most people buy homes using mortgage financing, notes can be thought of as another name for mortgage agreements. After the home purchase closes, banks and other lenders usually sell them to government entities like Fannie Mae, Freddie Mac, and the Federal Housing Administration.

The housing market has improved since the bust, but hasn’t healed fully. There were 1.4 million foreclosures in 2015, according to real estate data firm RealtyTrac, and more than 17% of all transactions last year were deemed “distressed” — more than double pre-bust levels — in some way.

As the dust has settled, government agencies have begun selling delinquent notes to big institutional investors like Lone Star Funds, Goldman Sachs GS, +2.76% and Fortress Investments FIG, +3.96% as well as some community nonprofits, in bulk. The agencies have sold more than $28 billion in distressed loans since 2012, according to government data.

The big investors then sell some to buyers such as Colonial Capital Management, which is run by the same people who run Note School. Colonial, which buys about 2,000 notes a year, sells most of them one by one to people like the ones who gathered in the Virginia Sheraton.

It’s difficult to know how much this happens and what it has meant for homeowners.

Anyone who buys notes from the government must follow reporting requirements that include information on how the loans perform. Those requirements stay with the notes if they’re resold; they expire four years after the government’s initial sale. But nobody tracks note sales that weren’t made by the government, and even the government’s records don’t link outcomes and note owners.

March data from the Federal Housing Administration only hint at a broad view of how post-sale loans perform. The FHA has sold roughly 89,000 loans since 2012; less than 11% of those homeowners now pay their mortgages on time. Many are simply classified as “unresolved.” More than 34% had been foreclosed upon.

Fannie Mae and Freddie Mac, which began selling notes in 2014, were supposed to report similar data by the end of March. A spokeswoman for the agencies’ regulator said she did not know when that report, still incomplete, would be submitted.

And not all notes are initially sold by the government, making comprehensive oversight of the marketplace even harder. Banks and other lenders often sell notes directly; Colonial doesn’t buy notes from the government, according to Eddie Speed, founder of both Note School and Colonial.

For investors, a cleaner deal than the world of ‘tenants and toilets’

Note buying has attractions for both investors and the communities where the homeowners live.

Delinquent notes can be bought cheaply, often for about a third of a home’s market value. Note buyers get an investment that’s more like a financial asset — and less dirty than the landlord’s world of “tenants and toilets.”

Meanwhile, investors can often afford to cut homeowners a significant break, avoiding foreclosure while still making a profit.

And there’s government money for the taking in the name of helping homeowners. Since the housing crisis, the federal government has allocated nearly $10 billion to states deemed hardest-hit by the bust. Those states funnel the money to borrowers, often to help them reach new agreements with their lenders.

That can help municipalities that lose out on property taxes when homeowners don’t make payments, and which benefit from having more involved owners, Speed says.

Eddie Speed

When Tj Osterman, 38, and Rick Allen, 36, who have worked together as real-estate investors for about 10 years in the Orlando area, first explored note buying, they thought it little different than flipping abandoned houses.

But when they realized homeowners were often still in the picture, they changed their approach to try to work with them. Some of their motivation came from personal experience: Allen went through foreclosure in 2007. “It was a tough time,” he said. “I wish there was someone like me who said, let’s help you keep your house.”

They can buy notes cheaply enough that they can reduce the principal owed by homeowners “as much as 50%, and still turn a nice profit, pay back taxes, [and] get these people feeling good about themselves again,” said Osterman.

They now have a goal of helping save 10,000 homeowners from foreclosure. “I’m so addicted to the socially responsible side of stuff,” Osterman said. “We talk with borrowers like human beings and underwrite to real-world standards.”

‘There’s a system out there that’s broken’

Some housing observers have concerns about drawing nonprofessionals into an often-opaque market. A recent example Shortle used as a case study during the Virginia seminar helps explain why.

A note on an Atlanta-area home was being sold for $24,360; according to estimates from Zillow and local agents, its market value was between $50,000 and $70,000.

Some back taxes were owed, and a payment history showed that while the homeowner was making erratic or partial payments on her $500 monthly mortgage, she hadn’t quit. She had some equity built up in the house, another sign of commitment.

Real-estate investment firm Stonecrest sold her the home in 2012; she had used Stonecrest’s own financing at 9%. Her payment record was spotless until 2014. Stonecrest sold the note to Colonial in 2015 and Colonial offered it for resale in early 2016.

Most notes underpin mortgages. But this one was linked to a land contract, a financial agreement more typical when the seller is offering financing. Land contracts are sometimes criticized for being almost predatory: If a buyer skips a payment, the house and all the money he’s put toward it can be taken away.

And buyers don’t hold the deeds to the home, so the homes can be taken more quickly if they’re delinquent. Note School often steers students to scenarios where government programs like Hardest Hit can be tapped, but those programs don’t apply to land contracts.

Shortle walked his class through different strategies. The new note owner could foreclose; they could also induce the home buyer to walk. “It may be time to give this person a little cash for keys to move on,” he told the class. “They can’t afford it.”

Other data indicated that the house would rent for roughly $750. It might make sense, Shortle suggested, to remove the homeowner, fix up the house, rent it out, then sell the entire arrangement to a cash investor.

If a new note owner took that tack, the note would change hands four times in about as many years—even as the homeowner changed just once. The homeowner might never notice.

Some analysts see evidence of a still-hurting housing market behind all that activity.

By diffusing distressed loans out into a broader marketplace, lenders avoid the negative publicity that comes with foreclosing on delinquent homeowners. That masks “a layer of distress in the housing market that’s being overlooked,” said Daren Blomquist, vice president at RealtyTrac.

“This has been a way to push aside the crisis and sweep it under the rug,” Blomquist told MarketWatch.

Some analysts see evidence of a still-hurting housing market behind all that activity.

By diffusing distressed loans out into a broader marketplace, lenders avoid the negative publicity that comes with foreclosing on delinquent homeowners. That masks “a layer of distress in the housing market that’s being overlooked,” said Daren Blomquist, vice president at RealtyTrac.

“This has been a way to push aside the crisis and sweep it under the rug,” Blomquist told MarketWatch.

Osterman, left, and Allen

Note investors say they can offer a service others can’t or won’t. “There’s a real issue with how we’re treating hardships,” said Osterman. “There’s a system out there that’s broken and needs to be disrupted in a good way.”

Note School’s founder says the goal is a ‘win-win’

While newer investors like Osterman and Allen have a sense of mission forged during the recent housing crisis, Speed has been in the note business for more than 30 years. He is adamant that it’s in Note School’s best interest to teach students to observe regulation and treat homeowners respectfully. There’s no reason it can’t be a “win-win,” he said.

‘”We’re not teaching people to go and do ‘Wild West investing.’

Colonial Funding doesn’t make buyers of its notes go through Note School, but it does require them to work with licensed mortgage servicers. Note School offers connections to armies of vendors offering services for every step of the process: people who will assess the property’s real market value, “door-knockers” who will hand-deliver letters to homeowners, title research companies, insurers, and more.

“We’ve been in the note buying business for 30 years,” said Speed. “We’re not teaching people to go and do ‘Wild West investing.’”

Speed believes buying distressed notes is a process tailor-made for people with an entrepreneurial approach to doing well by solving problems — and maintains that he is mindful of the postcrisis environment in which they work.

“I’m walking into where the disaster has already happened,” he said. “If I walk into a loan where the customer has vacated, they probably want out. Common sense tells us if the borrower can deed it over to the lender and walk away with dignity, that seems like a good deal for him. We’re trying to do everything we can to reach resolution.”

Distressed homeowners who, with their lender’s approval, arrange a short sale of their property — for less than they owe — can’t be sued for the balance of their debt, the state Supreme Court ruled Thursday.

The unanimous decision protects borrowers who increasingly resorted to short sales as property values fell at the end of the last decade. The Legislature amended state law in 2012 to provide them explicit protection against deficiency judgments, but a lawyer for the borrower in Thursday’s case said that about 200,000 Californians had conducted short sales in the previous five years and were potentially affected by the ruling.

“The little guy won today,” said the attorney, Andrew Stilwell.

His client, Carol Coker, borrowed $452,000 in 2004 to buy a condominium in San Diego County. She fell behind on her payments, and in March 2010 JPMorgan Chase Bank, which then held the loan, sent her a default notice and began foreclosure proceedings.

The bank then agreed to allow Coker to sell the condo to another buyer for $400,000, collect the proceedings and release its lien on the property. But after the sale, the bank billed her for the $116,000 balance due on her loan.

The state law at the time, originally enacted in 1933 and amended in 1989, prohibited a bank from seeking a deficiency judgment, for the balance due on its loan, after the bank itself foreclosed on a home. But the law did not address short sales, which were rare until the late 2000s, and JPMorgan Chase argued that the anti-deficiency rule did not apply to those cases.

But the court said the rationale of the law applied equally to short sales.

“For more than half a century, this court has understood the statute to limit a lender’s recovery on a standard purchase-money loan to the value of the security,” Justice Goodwin Liu said in the 7-0 decision.

Liu said the law was intended to maintain economic stability and protect property buyers from severe losses during periods of economic decline.

Coker’s short sale of the condo — which she bought as a residence, rather than an investment — “did not change the standard purchase-money character of her loan,” Liu said. He said the short sale, “like a foreclosure sale, allowed Chase to realize and exhaust its security” in the property.

Stilwell said the ruling would also affect cases in federal Bankruptcy Courts in California, which rely on state laws affecting creditors and debtors.

“The Supreme Court shut the door on banks trying to go too far to take advantage of the poor, the middle class, people who couldn’t afford what they got into in this real estate debacle,” he said.

The bank’s lawyers referred inquiries to bank headquarters in New York, which could not be reached for comment late Thursday.

RealtyTrac’s Q1 2015 Zombie Foreclosure Report, found that as of the end of January 2015, 142,462 homes actively in the foreclosure process had been vacated by the homeowners prior to the bank repossessing the property, representing 25 percent of all active foreclosures.

The total number of zombie foreclosures was down 6 percent from a year ago, but the 25 percent share of total foreclosures represented by zombies was up from 21 percent a year ago.

“While the number of vacated zombie foreclosures is down from a year ago, they represent an increasing share of all foreclosures because they tend to be the problem cases still stuck in the pipeline,” said Daren Blomquist vice president at RealtyTrac. “Additionally, the states where overall foreclosure activity has been increasing over the past year — counter to the national trend — tend to be states with a longer foreclosure process more susceptible to the zombie problem.”

“In states with a bloated foreclosure process, the increase in zombie foreclosures is actually a good sign that banks and courts are finally moving forward with a resolution on these properties that may have been sitting in foreclosure limbo for years,” Blomquist continued. “In many markets there is plenty of demand from buyers and investors to snatch up these distressed properties as soon as they become available to purchase.”

Florida, New Jersey, New York have most zombie foreclosures

Despite a 35 percent decrease in zombie foreclosures compared to a year ago, Florida had the highest number of any state with 35,903 — down from 54,908 in the first quarter of 2014. Zombie foreclosures accounted for 26 percent of all foreclosures in Florida.

Zombie foreclosures increased 109 percent from a year ago in New Jersey, and the state posted the second highest total of any state with 17,983 — 23 percent of all properties in foreclosure.

New York zombie foreclosures increased 54 percent from a year ago to 16,777, the third highest state total and representing 19 percent of all residential properties in foreclosure.

Illinois had 9,358 zombie foreclosures at the end of January, down 40 percent from a year ago but still the fourth highest state total, while California had 7,370 zombie foreclosures at the end of January, up 24 percent from a year ago and the fifth highest state total.

“We are now in the final cycle of the foreclosure crisis cleanup, in which we are witnessing a large final wave of walkaways,” said Mark Hughes, Chief Operating Officer at First Team Real Estate, covering the Southern California market. “This has created an uptick in vacated or ‘zombie’ foreclosures and the intrinsic neighborhood issues most of them create.

“A much longer recovery, a largely veiled underemployment issue, and growing examples of faster bad debt forgiveness have most likely fueled this last wave of owners who have finally just walked away from their American dream,” Hughes added.

Other states among the top 10 for most zombie foreclosures were Ohio (7,360), Indiana (5,217), Pennsylvania (4,937), Maryland (3,363) and North Carolina (3,177).

“Rising home prices in Ohio are motivating lending servicers to commence foreclosure actions more quickly and with fewer workout options offered to delinquent homeowners, creating immediate vacancies earlier in the foreclosure process,” said Michael Mahon, executive vice president at HER Realtors, covering the Ohio housing markets of Cincinnati, Dayton and Columbus. “Delinquent homeowners need to understand how prices have increased in recent months, and how this increase in equity may provide positive options for them to avoid foreclosure.”

Metros with most zombie foreclosures: New York, Miami, Chicago, Tampa and Philadelphia. The greater New York metro area had by far the highest number of zombie foreclosures of any metropolitan statistical area nationwide, with 19,177 — 17 percent of all properties in foreclosure and up 73 percent from a year ago.

Zombie foreclosures decreased from a year ago in Miami, Chicago and Tampa, but the three metros still posted the second, third and fourth highest number of zombie foreclosures among metro areas nationwide: Miami had 9,580 zombie foreclosures,19 percent of all foreclosures but down 34 percent from a year ago; Chicago had 8,384 zombie foreclosures, 21 percent of all foreclosures but down 35 percent from a year ago; and Tampa had 7,838 zombie foreclosures, 34 percent of all foreclosures but down 25 percent from a year ago.

Zombie foreclosures increased 53 percent from a year ago in the Philadelphia metro area, giving it the fifth highest number of any metro nationwide in the first quarter of 2015. There were 7,554 zombie foreclosures in the Philadelphia metro area as of the end of January, 27 percent of all foreclosures.

Other metro areas among the top 10 for most zombie foreclosures were Orlando (3,718), Jacksonville, Florida (2,368), Los Angeles (2,074), Las Vegas (1,832), and Baltimore, Maryland (1,722).

Metros with highest share of zombie foreclosures: St. Louis, Portland, Las Vegas

Among metro areas with a population of 200,000 or more and at least 500 zombie foreclosures as of the end of January, those with the highest share of zombie foreclosures as a percentage of all foreclosures were St. Louis (51 percent), Portland (40 percent) and Las Vegas (36 percent).

Metros with biggest increase in zombie foreclosures: Atlantic City, Trenton, New York

Among metro areas with a population of 200,000 or more and at least 500 zombie foreclosures as of the end of January, those with the biggest year-over-year increase in zombie foreclosures were Atlantic City, New Jersey (up 133 percent), Trenton-Ewing, New Jersey (up 110 percent), and New York (up 73 percent).

According to RealtyTrac, the first wave of 7.3 million homeowners who lost their home to foreclosure or short sale during the foreclosure crisis are now past the seven-year window they conservatively need to repair their credit and qualify to buy a home as we begin 2015.

In addition, more waves of these potential boomerang buyers will be moving past that seven-year window over the next eight years corresponding to the eight years of above-normal foreclosure activity from 2007 to 2014.

“The housing crisis certainly hit home the fact that home ownership is not for everyone, but those burned during the crisis should not immediately throw the baby out with the bathwater when it comes to their second chance at home ownership,” said Chris Pollinger, senior vice president of sales at First Team Real Estate, covering the Southern California market which has more than 260,000 potential boomerang buyers. “Home ownership done responsibly is still one of the best disciplined wealth-building strategies, and there is much more data available for home buyers than there was five years ago to help them make an informed decision about a home purchase.”

Nearly 7.3 million potential boomerang buyers nationwide will be in a position to buy again from a credit repair perspective over the next eight years.

Markets with the most potential boomerang buyers over the next eight years among metropolitan statistical areas with a population of at least 250,000.

Markets with the highest rate of potential boomerang buyers as a percentage of total housing units over the next eight years among metro areas with at least 250,000 people.

Markets most likely to see the boomerang buyers materialize are those where there are a high percentage of housing units lost to foreclosure but where current home prices are still affordable for median income earners and where the population of Gen Xers and Baby Boomers — the two generations most likely to be boomerang buyers — have held steady or increased during the Great Recession.

There were 22 metros among those with at least 250,000 people where this trifecta of market conditions is in place, making these metros the most likely nationwide to see a large number of boomerang buyers materialize in 2015 and beyond.

When it comes to housing, sometimes it seems we never learn. Just when America appeared to be recovering from the last housing crisis—the trigger, in many ways, for 2008’s grand financial meltdown and the beginning of a three-year recession—another one may be looming on the horizon.

There are at several big red flags.

For one, the housing market never truly recovered from the recession.TruliaChief Economist Jed Kolko points out that, while the third quarter of 2014 saw improvement in a number of housing key barometers, none have returned to normal, pre-recession levels. Existing home sales are now 80 percent of the way back to normal, while home prices are stuck at 75 percent back, remaining undervalued by 3.4 percent. More troubling, new construction is less than halfway (49 percent) back to normal. Kolko also notes that the fundamental building blocks of the economy, including employment levels, income and household formation, have also been slow to improve. “In this recovery, jobs and housing can’t get what they need from each other,” he writes.

Americans are spending more than 33 percent of their income on housing.

Second, Americans continue to overspend on housing. Even as the economy drags itself out of its recession, a spate of reports show that families are having a harder and harder time paying for housing. Part of the problem is that Americans continue to want more space in bigger homes, and not just in the suburbs but in urban areas, as well. Americans more than 33 percent of their income on housing in 2013, up nearly 13 percent from two decades ago, according to newly released data from the Bureau of Labor Statistics (BLS). The graph below plots the trend by age.

Over-spending on housing is far worse in some places than others; the housing market and its recovery remain highly uneven. Another BLS report released last month showed that households in Washington, D.C., spent nearly twice as much on housing ($17,603) as those in Cleveland, Ohio ($9,061). The chart below, from the BLS report, shows average annual expenses on housing related items:

(Bureau of Labor Statistics)

The result, of course, is that more and more American households, especially middle- and working-class people, are having a harder time affording housing. This is particularly the case in reviving urban centers, as more affluent, highly educated and creative-class workers snap up the best spaces, particularly those along convenient transit, pushing the service and working class further out.

Last but certainly not least, the rate of home ownership continues to fall, and dramatically. Home ownership has reached its lowest level in two decades—64.4 percent (as of the third quarter of 2014). Here’s the data, from the U.S. Census Bureau:

(Data from U.S. Census Bureau)

Home ownership currently hovers from the mid-50 to low-60 percent range in some of the most highly productive and innovative metros in this country—places like San Francisco, New York, and Los Angeles. This range seems “to provide the flexibility of rental and ownership options required for a fast-paced, rapidly changing knowledge economy. Widespread home ownership is no longer the key to a thriving economy,” I’ve written.

What we are going through is much more than a generational shift or simple lifestyle change. It’s a deep economic shift—I’ve called it the Great Reset. It entails a shift away from the economic system, population patterns and geographic layout of the old suburban growth model, which was deeply connected to old industrial economy, toward a new kind of denser, more urban growth more in line with today’s knowledge economy. We remain in the early stages of this reset. If history is any guide, the complete shift will take a generation or so.

It’s time to impose stricter underwriting standards and encourage the dense, mixed-use, more flexible housing options that the knowledge economy requires.

The upshot, as the Nobel Prize winner Edmund Phelpshas written, is that it is time for Americans to get over their house passion. The new knowledge economy requires we spend less on housing and cars, and more on education, human capital and innovation—exactly those inputs that fuel the new economic and social system.

But we’re not moving in that direction; in fact, we appear to be going the other way. This past weekend, Peter J. Wallison pointed out in a New York Times op-ed that federal regulators moved back off tougher mortgage-underwriting standards brought on by 2010’s Dodd-Frank Act and instead relaxed them. Regulators are hoping to encourage more home ownership, but they’re essentially recreating the conditions that led to 2008’s crash.

Wallison notes that this amounts to “underwriting the next housing crisis.” He’s right: It’s time to impose stricter underwriting standards and encourage the dense, mixed-use, more flexible housing options that the knowledge economy requires.

During the depression and after World War II, this country’s leaders pioneered a series of purposeful and ultimately game-changing polices that set in motion the old suburban growth model, helping propel the industrial economy and creating a middle class of workers and owners. Now that our economy has changed again, we need to do the same for the denser urban growth model, creating more flexible housing system that can help bolster today’s economy.

This new class action against Ocwen addresses the marked-up default services fees that Ocwen is charging homeowners, particularly distressed homeowners, as part of a scheme of self-dealing with companies such as Altisource, and with the involvement of William C. Erbey, Executive Chairman, who has a leadership role on the Board of Ocwen and Altisource:

Weiner v Ocwen Financial Corporation a Florida Corporation COMPLAINT. Weiner v. Ocwen Fin. Corp. and Ocwen Loan Servicing, LLC, No 2:14-cv-02597 (E.D.Cal.), filed Nov. 5, 2014.

52. Ocwen’s scheme works as follows: Ocwen directs Altisource to order and coordinate default-related services, and, in turn, Altisource places orders for such services with third-party vendors. The third-party vendors charge Altisource for the performance of the default-related services, Altisource then marks up the price of the vendors’ services, in numerous instances by 100% or more, before “charging” the services to Ocwen. In turn, Ocwen bills the marked-up fees to homeowners.

58.Thus, the mortgage contract discloses to homeowners that the servicer will pay for default-related services when reasonably necessary, and will be reimbursed or “paid back” by the homeowner for amounts “disbursed.” Nowhere is it disclosed to borrowers that the servicer may engage in self-dealing to mark up the actual cost of those services to make a profit. Nevertheless, that is exactly what Ocwen does.

[Ed.: Explanation of Modern Relationship Between Loan Servicers and Home Loan Borrowers]

America’s Lending Industry Has Divorced itself from the Borrowers it Once Served

18. Ocwen’s unlawful loan servicing practices exemplify how America’s lending industry has run off the rails.

19. Traditionally, when people wanted to borrow money, they went to a bank or a “savings and loan.” Banks loaned money and homeowners promised to repay the bank, with interest, over a specific period of time. The originating bank kept the loan on its balance sheet, and serviced the loan — processing payments, and sending out applicable notices and other information — until the loan was repaid. The originating bank had a financial interest in ensuring that the borrower was able to repay the loan.

20. Today, however, the process has changed. Mortgages are now packaged, bundled, and sold to investors on Wall Street through what is referred to in the financial industry as mortgage backed securities or MBS. This process is called securitization. Securitization of mortgage loans provides financial institutions with the benefit of immediately being able to recover the amounts loaned. It also effectively eliminates the financial institution’s risk from potential default. But, by eliminating the risk of default, mortgage backed securities have disassociated the lending community from homeowners.

21. Numerous unexpected consequences have resulted from the divide between lenders and homeowners. Among other things, securitization has led to the development of an industry of companies which make money primarily through servicing mortgages for the hedge funds and investment houses who own the loans.

22. Loan servicers do not profit directly from interest payments made by homeowners. Instead, these companies are paid a set fee for their loan administration services. Servicing fees are usually earned as a percentage of the unpaid principal balance of the mortgages that are being serviced. A typical servicing fee is approximately 0.50% per year.

23. Additionally, under pooling and servicing agreements (“PSAs”) with investors and note holders, loan servicers assess fees on borrowers’ accounts for default-related services. These fees include, inter alia, Broker’s Price Opinion (“BPO”) fees, appraisal fees, and title examination fees.

24. Under this arrangement, a loan servicer’s primary concern is not ensuring that homeowners stay current on their loans. Instead, they are focused on minimizing any costs that would reduce profit from the set servicing fee, and generating as much revenue as possible from fees assessed against the mortgage accounts they service. As such, their “business model . . . encourages them to cut costs wherever possible, even if [that] involves cutting corners on legal requirements, and to lard on junk fees and in-sourced expenses at inflated prices.”3

25. As one Member of the Board of Governors of the Federal Reserve System has explained: While an investor’s financial interests are tied more or less directly to the performance of a loan, the interests of a third-party servicer are tied to it only indirectly, at best. The servicer makes money, to oversimplify it a bit, by maximizing fees earned and minimizing expenses while performing the actions spelled out in its contract with the investor. . . . The broad grant of delegated authority that servicers enjoy under pooling and servicing agreements (PSAs), combined with an effective lack of choice on the part of consumers, creates an environment ripe for abuse.4 (citing See Sarah Bloom Raskin, Member Board of Governors of the Federal Reserve System, Remarks at the National Consumer Law Center’s Consumer Rights Litigation Conference, Boston Massachusetts, Nov. 12, 2010, available at http://www.federalreserve.gov/newsevents/speech/raskin20101112a.htm (last visited Jan. 23, 2012).

If you really would rather own the property than the note, take a few lessons in fraud from Owen Financial Corp. According to allegations from New York’s financial regulator, Benjamin Lawsky, the lender sent “thousands” of foreclosure “warnings” to borrowers months after the window of time had lapsed during which they could have saved their homes[1]. Lawskey alleges that many of the letters were even back-dated to give the impression that they had been sent in a timely fashion. “In many cases, borrowers received a letter denying a mortgage loan modification, and the letter was dated more than 30 days prior to the date that Ocwen mailed the letter.”

The correspondence gave borrowers 30 days from the date of the denial letter to appeal, but the borrowers received the letters after more than 30 days had passed. The issue is not a small one, either. Lawskey says that a mortgage servicing review at Ocwen revealed “more than 7,000” back-dated letters.”

In addition to the letters, Ocwen only sent correspondence concerning default cures after the cure date for delinquent borrowers had passed and ignored employee concerns that “letter-dating processes were inaccurate and misrepresented the severity of the problem.” While Lawskey accused Ocwen of cultivating a “culture that disregards the needs of struggling borrowers,” Ocwen itself blamed “software errors” for the improperly-dated letters[2]. This is just the latest in a series of troubles for the Atlanta-based mortgage servicer; The company was also part the foreclosure fraud settlement with 49 of 50 state attorneys general and recently agreed to reduce many borrowers’ loan balances by $2 billion total.

Most people do not realize that Ocwen, although the fourth-largest mortgage servicer in the country, is not actually a bank. The company specializes specifically in servicing high-risk mortgages, such as subprime mortgages. At the start of 2014, it managed $106 billion in subprime loans. Ocwen has only acknowledged that 283 New York borrowers actually received improperly dated letters, but did announce publicly in response to Lawskey’s letter that it is “investigating two other cases” and cooperating with the New York financial regulator.

WHAT WE THINK: While it’s tempting to think that this is part of an overarching conspiracy to steal homes in a state (and, when possible, a certain enormous city) where real estate is scarce, in reality the truth of the matter could be even more disturbing: Ocwen and its employees just plain didn’t care. There was a huge, problematic error that could have prevented homeowners from keeping their homes, but the loan servicer had already written off the homeowners as losers in the mortgage game. A company that services high-risk loans likely has a jaded view of borrowers, but that does not mean that the entire culture of the company should be based on ignoring borrowers’ rights and the vast majority of borrowers who want to keep their homes and pay their loans. Sure, if you took out a mortgage then you have the obligation to pay even if you don’t like the terms anymore. On the other side of the coin, however, your mortgage servicer has the obligation to treat you like someone who will fulfill their obligations rather than rigging the process so that you are doomed to fail.

Do you think Lawskey is right about Ocwen’s “culture?” What should be done to remedy this situation so that note investors and homeowners come out of it okay?

Thank you for reading the Bryan Ellis Investing Letter!

— Ocwen posts open letter and apology to borrowers Pledges independent investigation and rectification October 27, 2014 10:37AM

Ocwen Financial (OCN) has taken a beating after the New York Department of Financial Services sent a letter to the company on Oct. 21 alleging that the company had been backdating letters to borrowers, and now Ocwen is posting an open letter to homeowners.

Ocwen CEO Ron Faris writes to its clients explaining what happened and what steps the company is taking to investigate the issue, identify any problems, and rectify the situation.

Click here to read the full text of the letter.

“At Ocwen, we take our mission of helping struggling borrowers very seriously, and if you received one of these incorrectly-dated letters, we apologize. I am writing to clarify what happened, to explain the actions we have taken to address it, and to commit to ensuring that no borrower suffers as a result of our mistakes,” he writes.

“Historically letters were dated when the decision was made to create the letter versus when the letter was actually created. In most instances, the gap between these dates was three days or less,” Faris writes. “In certain instances, however, there was a significant gap between the date on the face of the letter and the date it was actually generated.”

Faris says that Ocwen is investigating all correspondence to determine whether any of it has been inadvertently misdated; how this happened in the first place; and why it took so long to fix it. He notes that Ocwen is hiring an independent firm to conduct the investigation, and that it will use its advisory council comprised of 15 nationally recognized community advocates and housing counselors.

“We apologize to all borrowers who received misdated letters. We believe that our backup checks and controls have prevented any borrowers from experiencing a foreclosure as a result of letter-dating errors. We will confirm this with rigorous testing and the verification of the independent firm,” Faris writes. “It is worth noting that under our current process, no borrower goes through a foreclosure without a thorough review of his or her loan file by a second set of eyes. We accept appeals for modification denials whenever we receive them and will not begin foreclosure proceedings or complete a foreclosure that is underway without first addressing the appeal.”

Faris ends by saying that Ocwen is committed to keeping borrowers in their homes.

“Having potentially caused inadvertent harm to struggling borrowers is particularly painful to us because we work so hard to help them keep their homes and improve their financial situations. We recognize our mistake. We are doing everything in our power to make things right for any borrowers who were harmed as a result of misdated letters and to ensure that this does not happen again,” he writes.

Last week the fallout from the “Lawsky event” – so called because of NYDFS Superintendent Benjamin Lawsky – came hard and fast.

Compass Point downgraded Ocwen affiliate Home Loan Servicing Solutions (HLSS) from Buy to Neutral with a price target of $18.

Meanwhile, Moody’s Investors Service downgraded Ocwen Loan Servicing LLC’s servicer quality assessments as a primary servicer of subprime residential mortgage loans to SQ3 from SQ3+ and as a special servicer of residential mortgage loans to SQ3 from SQ3+.

Standard & Poor’s Ratings Services lowered its long-term issuer credit rating to ‘B’ from ‘B+’ on Ocwen on Wednesday and the outlook is negative.

—- Ocwen Writes Open Letter to Homeowners Concerning Letter Dating Issues October 24, 2014

Dear Homeowners,

In recent days you may have heard about an investigation by the New York Department of Financial Services’ (DFS) into letters Ocwen sent to borrowers which were inadvertently misdated. At Ocwen, we take our mission of helping struggling borrowers very seriously, and if you received one of these incorrectly-dated letters, we apologize. I am writing to clarify what happened, to explain the actions we have taken to address it, and to commit to ensuring that no borrower suffers as a result of our mistakes.

What Happened Historically letters were dated when the decision was made to create the letter versus when the letter was actually created. In most instances, the gap between these dates was three days or less. In certain instances, however, there was a significant gap between the date on the face of the letter and the date it was actually generated.

What We Are Doing We are continuing to investigate all correspondence to determine whether any of it has been inadvertently misdated; how this happened in the first place; and why it took us so long to fix it. At the end of this exhaustive investigation, we want to be absolutely certain that we have fixed every problem with our letters. We are hiring an independent firm to investigate and to help us ensure that all necessary fixes have been made.

Ocwen has an advisory council made up of fifteen nationally recognized community advocates and housing counsellors. The council was created to improve our borrower outreach to keep more people in their homes. We will engage with council members to get additional guidance on making things right for any borrowers who may have been affected in any way by this error.

We apologize to all borrowers who received misdated letters. We believe that our backup checks and controls have prevented any borrowers from experiencing a foreclosure as a result of letter-dating errors. We will confirm this with rigorous testing and the verification of the independent firm. It is worth noting that under our current process, no borrower goes through a foreclosure without a thorough review of his or her loan file by a second set of eyes. We accept appeals for modification denials whenever we receive them and will not begin foreclosure proceedings or complete a foreclosure that is underway without first addressing the appeal.

In addition to these efforts we are committed to cooperating with DFS and all regulatory agencies.

We Are Committed to Keeping Borrowers in Their Homes Having potentially caused inadvertent harm to struggling borrowers is particularly painful to us because we work so hard to help them keep their homes and improve their financial situations. We recognize our mistake. We are doing everything in our power to make things right for any borrowers who were harmed as a result of misdated letters and to ensure that this does not happen again. We remain deeply committed to keeping borrowers in their homes because we believe it is the right thing to do and a win/win for all of our stakeholders.

We will be in further communication with you on this matter.

Sincerely, Ron Faris CEO

YOU DECIDE — Ocwen Downgrade Puts RMBS at Risk

Moody’s and S&P downgraded Ocwen’s servicer quality rating last week after the New York Department of Financial Services made “backdating” allegations. Barclays says the downgrades could put some RMBS at risk of a servicer-driven default.

You must be logged in to post a comment.