About: American Realty Capital Properties Inc (ARCP) by Albert Alfonso

Summary:

- According to a Reuters report, the FBI has opened a criminal probe of American Realty Capital Properties.

- This follows the disclosure of accounting errors by the company.

- This investigation is in addition to a SEC inquiry.

American Realty Capital Properties (NASDAQ:ARCP) just cannot catch a break. Reuters reported that the Federal Bureau of Investigation has opened a criminal investigation into ARCP, according to their sources. The FBI is conducting the investigation along with prosecutors from U.S. Attorney Preet Bharara’s office in New York, according to the Reuters report.

This news comes just days after the company announced a series of accounting errors which had been intentionally not corrected and thus concealed from the public. The amount of money involved, roughly $9.24 million GAAP and $13.60 million AFFO, was relatively small. However, these accounting errors resulted in the resignation of two senior executives, chief financial officer, Brian Block, and chief accounting officer, Lisa McAlister.

Shares of ARCP were trading for as low as $7.85 each on Wednesday, before recovering to $10 per share after CEO David Kay held fairly well received conference call explaining what happened. In the call, Mr. Kay stressed that ARCP’s key metrics were sound. He reaffirmed that the dividend policy will not change, noting that the operating metrics were not impacted and that the NAV is unchanged at $13.25. Nevertheless, the stock continued to fall, closing the week at below $9 per share. In total, ARCP’s stock has fallen 30% since news of the accounting errors first arose, wiping out $4 billion in market value.

Conclusion:

This is quite the shocking development. Not only is the FBI looking into ARCP, but also the Securities and Exchange Commission, which announced its own investigation of the accounting errors late last week. Furthermore, the company was placed on CreditWatch with negative implications by S&P, which risks putting the credit rating into junk territory.

As I noted in my earlier article, accounting issues equal an automatic sell in my book. I sold most of my ARCP holdings on Wednesday, though I still kept some shares, opting instead to sell calls on the remaining position. I now lament that choice as I fear the stock can fall further. An FBI criminal probe is no small matter and represents a clear material risk. What an absolute disaster.

Update: American Realty Capital Properties: The Turmoil Is Only Getting Worse

by Achilles Research

Summary

- ARCP sent shock waves through the analyst community last week after the REIT said its financials should no longer be relied upon and said goodbye to the CFO and CAO.

- ARCP is now also attracting heat from the FBI.

- In addition, RCS Capital Corporation cancels Cole Capital transaction.

Investors in American Realty Capital Properties (NASDAQ:ARCP) need to demonstrate that they have nerves of steel at the moment. After the company reported that it overstated its AFFO last week, and that its Chief Financial Officer and Chief Accounting Officer departed as a result of the accounting scandal, more bad news are seeing the light of day.

First of all, as various news outlets reported, the Federal Bureau of Investigation is putting up some additional heat on ARCP. As Reuters reported:

(Reuters) – U.S. authorities have opened a criminal probe of American Realty Capital Properties in the wake of the real estate investment trust’s disclosure that it had uncovered accounting errors, two sources familiar with the matter said on Friday.

The Federal Bureau of Investigation is conducting the investigation along with prosecutors from U.S. Attorney Preet Bharara’s office in New York, the sources said. Further details of the probe could not be learned.

The involvement of the New York U.S. Attorney’s office is particularly bad news as Preet Bharara takes a tough stance with companies that break the law or push its limits too far. While the criminal probe certainly is bad news and comes in addition to the involvement of the SEC, something else caused massive irritation among ARCP shareholders today: The Cole Capital deal with RCS Capital Corporation (NYSE: RCAP) is in real danger.

According to ARCP’s latest (and angry) press release:

In the middle of the night, we received a letter from RCS Capital Corporation purporting to terminate the equity purchase agreement, dated September 30, 2014, between RCS and an affiliate of ARCP. As we informed RCS orally and in writing over the weekend, RCS has no right and there is absolutely no basis for RCS to terminate the agreement. Therefore, RCS’s attempt to terminate the agreement constitutes a breach of the agreement. In addition, we believe that RCS’s unilateral public announcement is a violation of its agreement with ARCP. The independent members of the ARCP Board of Directors and ARCP management are evaluating all alternatives under the agreement and with respect to the Cole Capital® business, generally. ARCP management and the independent members of the ARCP Board of Directors are committed to doing what is in the best interests of ARCP stockholders and its business, including Cole Capital.

That’s right. Since the FBI now has its fingers in the pie, and the SEC, management at RCS Capital has informed ARCP that it is terminating the deal. Whatever side you are one, you’ve got to admit: American Realty Capital Properties is just falling apart.

The once mighty real estate investment trust has lost a staggering 36% of its market capitalization since shares closed at $12.38 on October 28, 2014, which is a tough pill to swallow for those investors who pledged allegiance to American Realty Capital Properties, despite the turbulence that erupted a week ago.

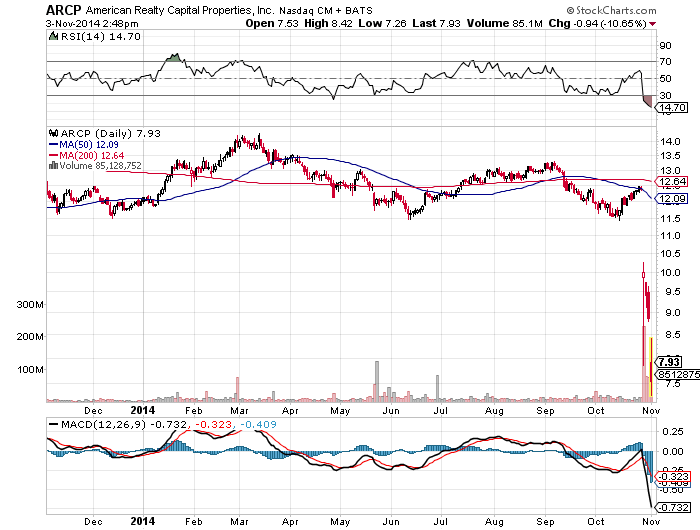

Technical picture

Shares of American Realty Capital Properties are trading extremely weakly today in light of the new information, and I continue to see further downside potential for this REIT in the near term.

It seems as if all the forces of the universe are conspiring to bring American Realty Capital Properties down to its knees, and an investment in this REIT is not recommendable at the moment.

Source: StockCharts.com

Bottom Line:

The American Realty Capital Properties’ story has gotten significantly worse today: In addition to two of the most important executives abruptly leaving the company amid an accounting scandal, the SEC and the FBI are investigating the company, lawyers are very likely going to hit ARCP with litigation, and the latest transaction is in the process of collapsing.

Bulls must either have nerves of steel or clinging to hope. In any case, ARCP’s prospects have gotten much worse today, and I continue to expect further downside potential driven by litigation concerns, potential fines and extremely negative investor sentiment.

American Realty Capital Comes Clean, And I Feel Dirty

by Adam Aloisi

Summary:

- American Realty Capital’s restatement has created rampant volatility in a stock already under the gun.

- Why I decided to sell half of my position in the company.

- Important portfolio takeaways for investors of all kinds.

This is one of the tougher articles I’ve written for Seeking Alpha. Asset allocation and portfolio strategy for income investors has been my focal point of writing over the past three years. I’ve always been of the opinion that talking about how to fish trumps simply giving someone fish to chew on.

Still, I mention equity-income stocks all the time in articles, but it’s rare that I write focus articles. On October third, I wrote, “American Realty Capital Properties: 30% Total Return Next Year“. Less than a month later, I find that post in an inverse position, with American Realty Capital (NASDAQ:ARCP) having dropped around 30% in market value.

First, I will tell readers that I sold a bit more than half of my position as a result of ARCP’s restatement, and still retain shares. However, it is now one of my smallest income portfolio positions and one that I have lost a majority of my conviction in. ARCP, in my mind, has transitioned from being a higher-risk investment into now becoming day-trader fodder, and at least for the near term, highly speculative. I would have been all over this thing during my trading days, but having become more conservative today with less portfolio churn, it has little room in my portfolio.

I considered all options here. I thought about increasing my position, extinguishing it altogether, selling put options at attractive premiums, or potentially doing nothing. Being so supportive of this story over the past year, I was mostly disappointed that I had to put any thought into the matter at all. For a variety of reasons, I came to the conclusion that halving the position — taking a loss, which I needed to do anyway for taxes — was a prudent near-term choice. I will revisit the decision in a month, and could conceivably buy back those shares once wash sale rules have passed.

Though selling during a period of fear and volatility is not typically in my playbook, following this restatement, I have lost confidence in this story. If you follow me, you know that I certainly identified the elevated risk that ARCP brought to real estate investors. Over the past six months, here are some comments that I made in regard to ARCP in several articles:

If you invest in ARCP today, you should expect the unexpected.

Given all the deals and potential for a misstep, there is heightened risk in owning ARCP.

But with the baggage it continues to drag along with it…..it may not necessarily be appropriate for more conservative investors

I do not consider the stock a table pounding buy.

I even compared Nick Schorsch to Monty Hall from “Let’s Make A Deal,” following the Red Lobster purchase and flip-flop on the strip mall IPO-then-sale.

As the year wore on, however, my convictions rose, since the company did not materially change its guidance to investors, despite all the acquisition activity. I figured if there were a stumble, it would have been disclosed earlier this year as the various acquisitions had time to be absorbed into operations.

While there was much criticism over the Cole quasi-divestiture to RCS and lowered guidance, I remained resolute, thinking there wasn’t another buyer, and this at least got Cole out from under the ARCP umbrella.

Of course as we now know, some financial disclosures were not to be relied upon and guidance should have been changed. If there were not so much other controversy with regard to this company, I doubt the stock would have tanked as much as it has. When you have a managerial crisis of confidence already in place and make a restatement announcement, you create panic. If we take this on face value, it does not appear to be a huge restatement, but taken in totality, this is a monumental, perhaps insurmountable, credibility problem. It’s now all aboard for the ambulance-chasing lawyers.

At this point I have decided that it is in my best interest to rip the towel in half and throw it in. I see it as a hedge against further deterioration in this story that I would not necessarily rule out given the loose management style that I and every ARCP investor knew existed.

We’re not talking about some low level accounting bean counter or paper pusher that seems to have perpetrated this; we’re talking about CFO Brian Block, assumedly someone that David Kay and Nick Schorsch had drinks with regularly. So when Kay defended the culture at ARCP on the conference call by uttering, “We don’t have bad people, we had some bad judgment there,” forgive me if I now wonder if he really has a clue how good, sweet, and honest his executives and rank-and-file workers really are. Although the restatements appear isolated to this year’s AFFO, we’ll have to see if anything turns up in 2013. While I’d like to give this company the benefit of the doubt once again, I’m finding myself staring at a slippery slope of hope that another shoe will not drop.

Still, I did not jettison the entire position because these are emotional times, and the glass-is-half-full part of me says the market is overreacting. We are, keep in mind, still talking about a high-quality portfolio of real estate, not a biotech company whose sole drug was deemed inefficacious by the FDA. In the end, however, I had to make a decision for my own portfolio that I deemed appropriate. This was it.

Meanwhile, I would not criticize nor blame someone for selling out here and moving on to more stable pastures. Fellow REIT writer Brad Thomas apparently has. On the flip side, I could see the more adventurous or those with continued conviction buying in now or upping exposure. The “right” thing to do for many investors may be to simply hold through the volatility. As I opined in a past article on ARCP:

But with the considerable sentiment overhang and “show me” attitude of the market, it could take some time and a strong stomach to see it through.

The sentiment “overhang” has basically become something much worse. And at this point I wouldn’t even want to predict how much time it could take for a rebound. Your stomach constitution will need to be stronger than I first suspected.

Portfolio Takeaways

I’ve had more than one reader tell me that the various risks I identified made them conclude that ARCP was not a stock they should own. And given what has happened here, at least for the near-term, that was obviously a prudent decision. We must all come to personal conclusions as to how much risk we are willing to take to attain income and capital growth goals.

For investors of all types, the most important thing to take away from this near-term “disaster” is that diversification and limiting position size is critical. If ARCP amounted to a couple of percent, or less, of a portfolio, the stock’s tank may not be all that impacting. If it was a more concentrated portion of the overall pie, it becomes a more painful near-term event and makes various portfolio maneuver decisions more challenging to come to.

In the end, portfolio management is a personal endeavor that amounts to an inexact science. Whether you think what I’ve done with my ARCP position is right or not is not really all important. The more important thing is whether you are comfortable with the personal portfolio decisions you make or not, why you make them, and whether they are right for your situation.

I’ve used the word “I” more than I normally would in an article. This one was indeed about me and owning up to putting wholesale trust in a management team that apparently I shouldn’t have. And it was a about a decision I really didn’t want to make as a result. Unfortunately, we have to take the bad with the good in the investment world, brush ourselves off, move on, and continue to make personal decisions that are right for our portfolios.

In 2009, 60 percent of buyers were married, 21 percent were single women, 10 percent single men and 8 percent unmarried couples. Thirteen percent of survey respondents were multi-generational households, including adult children, parents and/or grandparents.

In 2009, 60 percent of buyers were married, 21 percent were single women, 10 percent single men and 8 percent unmarried couples. Thirteen percent of survey respondents were multi-generational households, including adult children, parents and/or grandparents. In addition to tapping into their own savings (81 percent), first-time homebuyers used a variety of outside resources for their loan downpayment. Twenty-six percent received a gift from a friend or relative—most likely their parents—and six percent received a loan from a relative or friend. Ten percent of buyers sold stocks or bonds and tapped into a 401(k) fund.

In addition to tapping into their own savings (81 percent), first-time homebuyers used a variety of outside resources for their loan downpayment. Twenty-six percent received a gift from a friend or relative—most likely their parents—and six percent received a loan from a relative or friend. Ten percent of buyers sold stocks or bonds and tapped into a 401(k) fund. The biggest factors influencing neighborhood choice were quality of the neighborhood (69 percent), convenience to jobs (52 percent), overall affordability of homes (47 percent), and convenience to family and friends (43 percent). Other factors with relatively high responses included convenience to shopping (31 percent), quality of the school district (30 percent), neighborhood design (28 percent) and convenience to entertainment or leisure activities (25 percent).

The biggest factors influencing neighborhood choice were quality of the neighborhood (69 percent), convenience to jobs (52 percent), overall affordability of homes (47 percent), and convenience to family and friends (43 percent). Other factors with relatively high responses included convenience to shopping (31 percent), quality of the school district (30 percent), neighborhood design (28 percent) and convenience to entertainment or leisure activities (25 percent).

You must be logged in to post a comment.