(Sundance) The apoplectic response to Joe Manchin’s rebuke of Biden’s Build Back Better deal in general, and specifically, their reaction to losing the climate change agenda within it, points toward the original intent of COVID-19 in the first place. Continue reading

Tag Archives: World Economic Forum

Don’t Count On A Major Slowdown In U.S. Oil Production Growth

Summary

- The presumption that North American shale oil production is the “swing” component of global supply may be incorrect.

- Supply cutbacks from other sources may come first.

- Growth momentum in North American unconventional oil production will likely carry on into 2015, with little impact from lower oil prices on the next two quarters’ volumes.

- The current oil price does not represent a structural “economic floor” for North American unconventional oil production.

The recent pull back in crude oil prices is often portrayed as being a consequence of the rapid growth of North American shale oil production.

The thesis is often further extrapolated to suggest that a major slowdown in North American unconventional oil production growth, induced by the oil price decline, will be the corrective mechanism that will bring oil supply and demand back in equilibrium (given that OPEC’s cost to produce is low).

Both views would be, in my opinion, overly simplistic interpretations of the global supply/demand dynamics and are not supported by historical statistical data.

Oil Price – The Economic Signal Is Both Loud and Clear

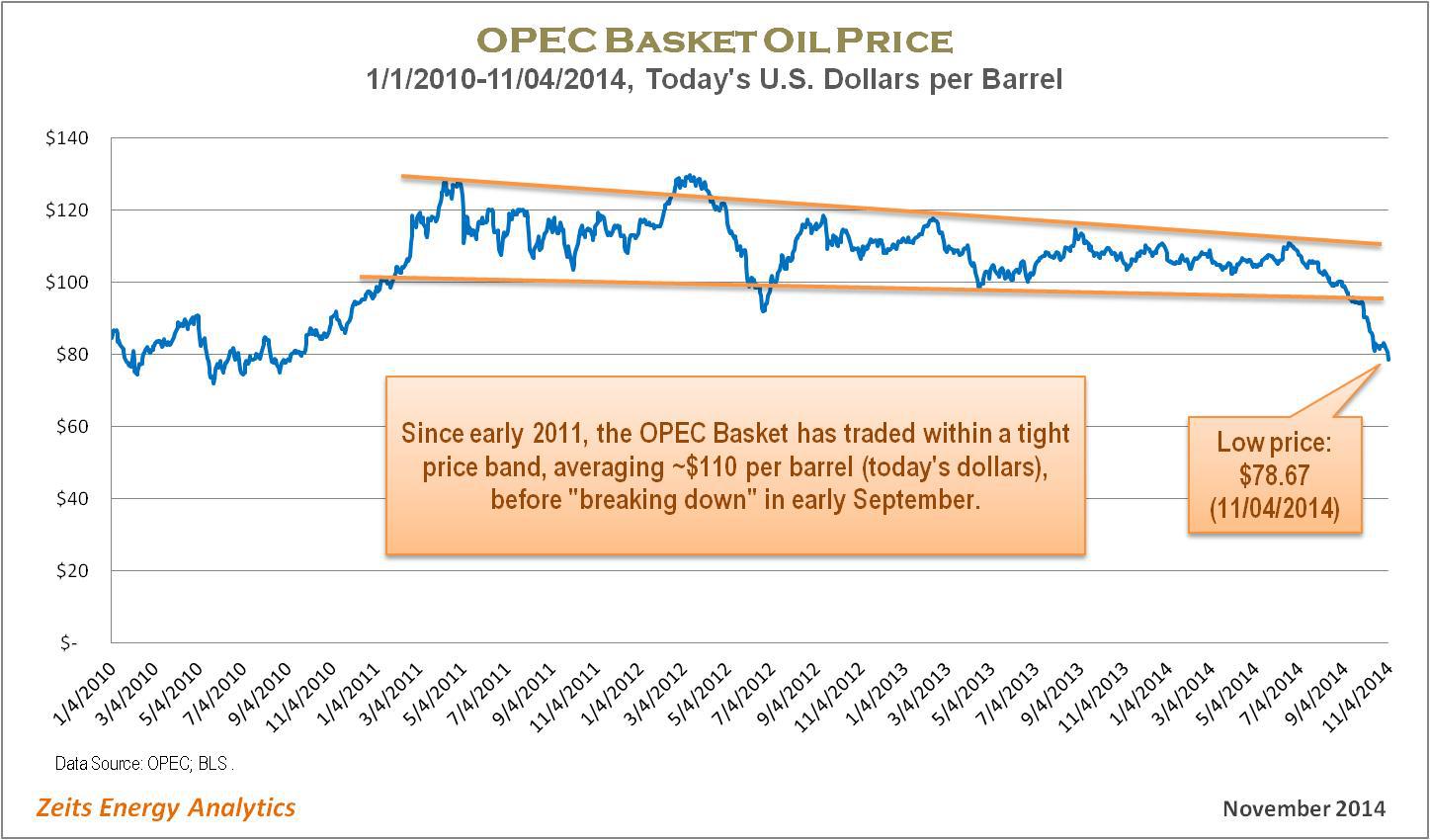

The current oil price correction is, arguably, the most pronounced since the global financial crisis of 2008-2009. The following chart illustrates very vividly that the price of the OPEC Basket (which represents waterborne grades of oil) has moved far outside the “stability band” that seems to have worked well for both consumers and producers over the past four years. (It is important, in my opinion, to measure historical prices in “today’s dollars.”)

(Source: Zeits Energy Analytics, November 2014)

(Source: Zeits Energy Analytics, November 2014)

Given the sheer magnitude of the recent oil price move, the economic signal to the world’s largest oil suppliers is, arguably, quite powerful already. A case can be made that it goes beyond what could be interpreted as “ordinary volatility,” giving the hope that the current price level may be sufficient to induce some supply response from the largest producers – in the event a supply cut back is indeed needed to eliminate a transitory supply/demand imbalance.

Are The U.S. Oil Shales The Culprit?

It is debatable, in my opinion, if the continued growth of the U.S. onshore oil production can be identified as the primary cause of the current correction in the oil price. Most likely, North American shale oil is just one of several powerful factors, on both supply and demand sides, that came together to cause the price decline.

The history of oil production increases from North America in the past three years shows that the OPEC Basket price remained within the fairly tight band, as highlighted on the graph above, during 2012-2013, the period when such increases were the largest. Global oil prices “broke down” in September of 2014, when North American oil production was growing at a lower rate than in 2012-2013.

(Source: OPEC, October 2014)

(Source: OPEC, October 2014)

If the supply growth from North America was indeed the primary “disruptive” factor causing the imbalance, one would expect the impact on oil prices to become visible at the time when incremental volumes from North America were the highest, i.e., in 2012-2013.

Should One Expect A Strong Slowdown in North American Oil Production Growth?

There is no question that the sharp pullback in the price of oil will impact operating margins and cash flows of North American shale oil producers. However, a major slowdown in North American unconventional oil production growth is a lot less obvious.

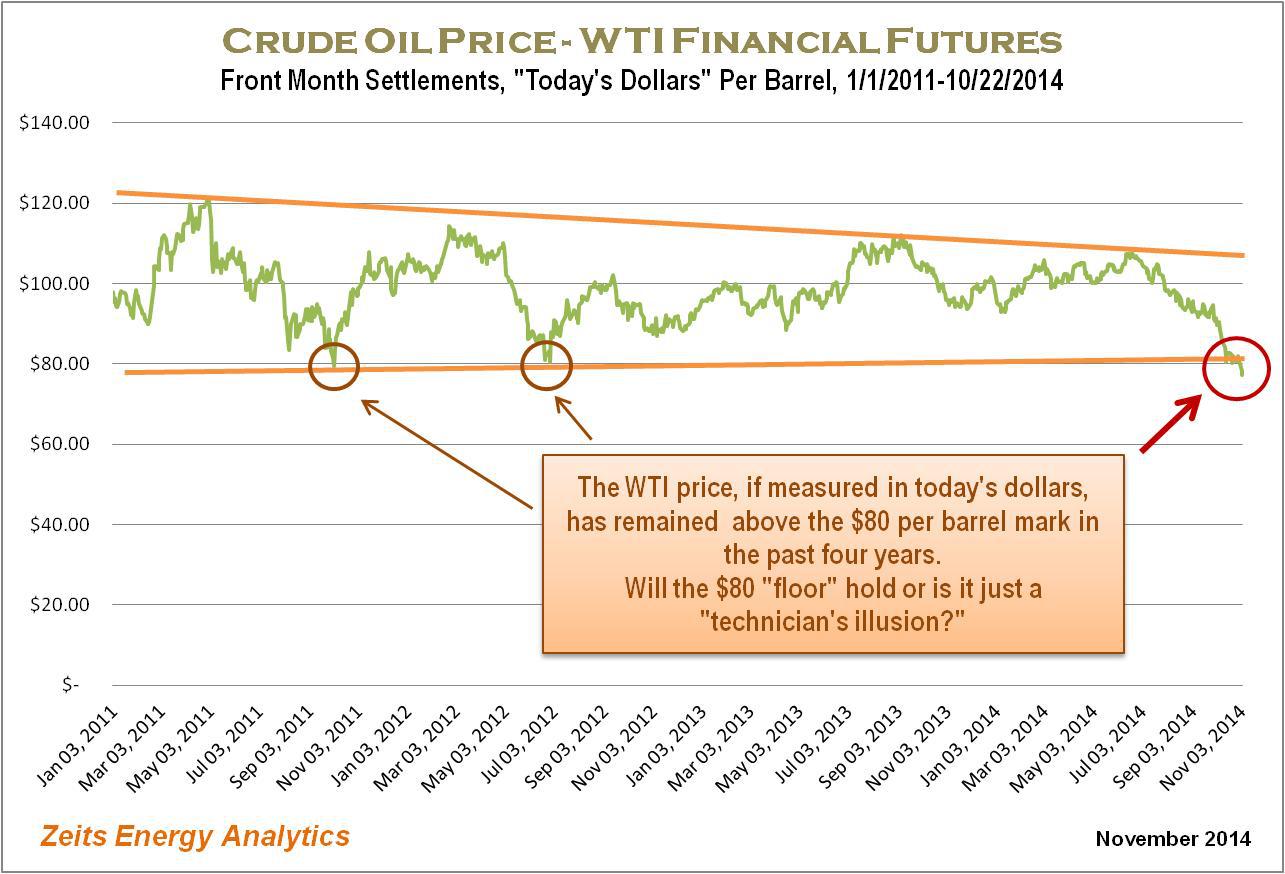

First, the oil price correction being seen by North American shale oil producers is less pronounced than the oil price correction experienced by OPEC exporters. It is sufficient to look at the WTI historical price graph below (which is also presented in “today’s dollars”) to realize that the current WTI price decline is not dissimilar to those seen in 2012 and 2013 and therefore represents a signal of lesser magnitude than the one sent to international exporters (the OPEC Basket price).

(Source: Zeits Energy Analytics, November 2014)

(Source: Zeits Energy Analytics, November 2014)

Furthermore, among all the sources of global oil supply, North American oil shales are the least established category. Their cost structure is evolving rapidly. Given the strong productivity gains in North American shale oil plays, what was a below-breakeven price just two-three years ago, may have become a price stimulating growth going into 2015.

Therefore, the signal sent by the recent oil price decline may not be punitive enough for North American shale oil producers and may not be able to starve the industry of external capital.

Most importantly, review of historical operating statistics provides an indication that the previous similar WTI price corrections – seen in 2012 and 2013 – did not result in meaningful slowdowns in the North American shale oil production.

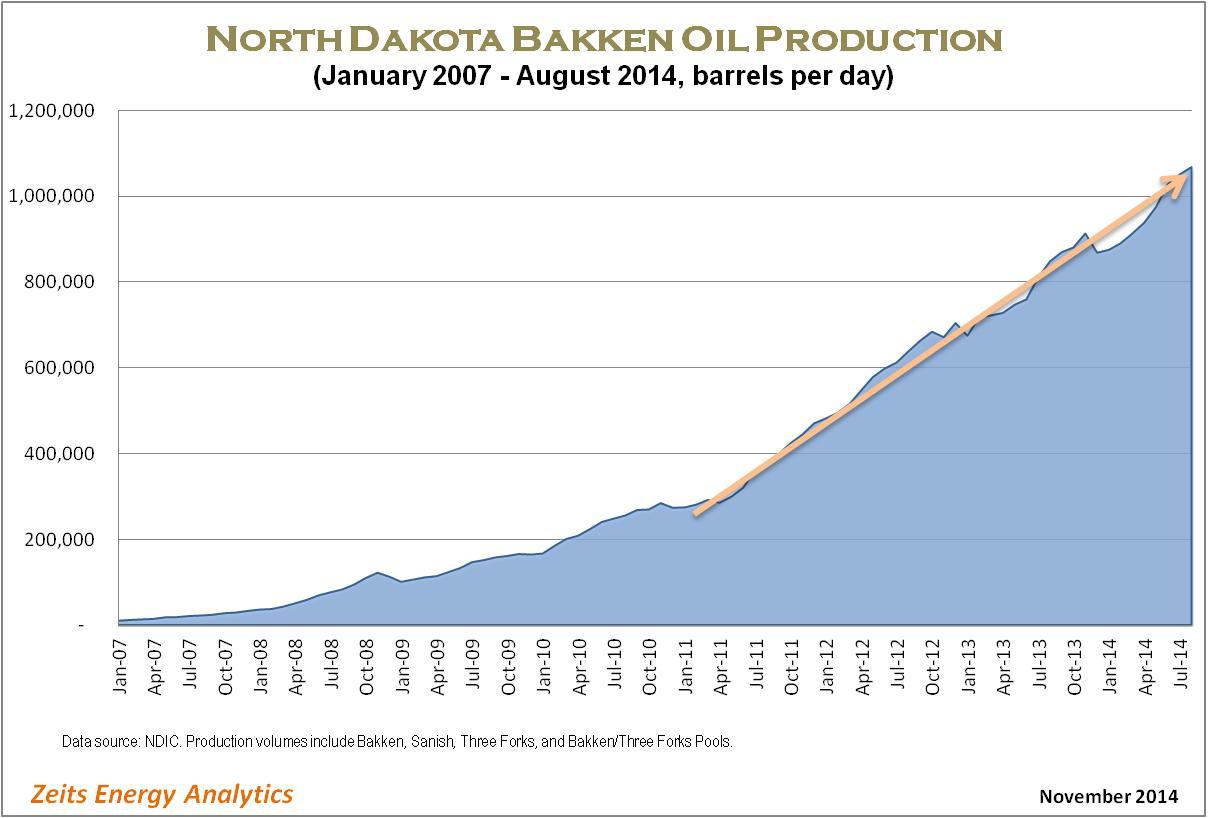

The following graph shows the trajectory of oil production in the Bakken play. From this graph, it is difficult to discern any significant impact from the 2012 and 2013 WTI price corrections on the play’s aggregate production volumes. While a positive correlation between these two price corrections and the pace of production growth in the Bakken exists, there are other factors – such as takeaway capacity availability and local differentials – that appear to have played a greater role. I should also note that the impact of the lower oil prices on production volumes was not visible in the production growth rate for more than half a year after the onset of the correction.

(Source: Zeits Energy Analytics, November 2014)

(Source: Zeits Energy Analytics, November 2014)

Leading U.S. Independents Will Likely Continue to Grow Production At A Rapid Pace

Production growth track record by several leading shale oil players suggests that U.S. shale oil production will likely remain strong even in the $80 per barrel WTI price environment. Several examples provide an illustration.

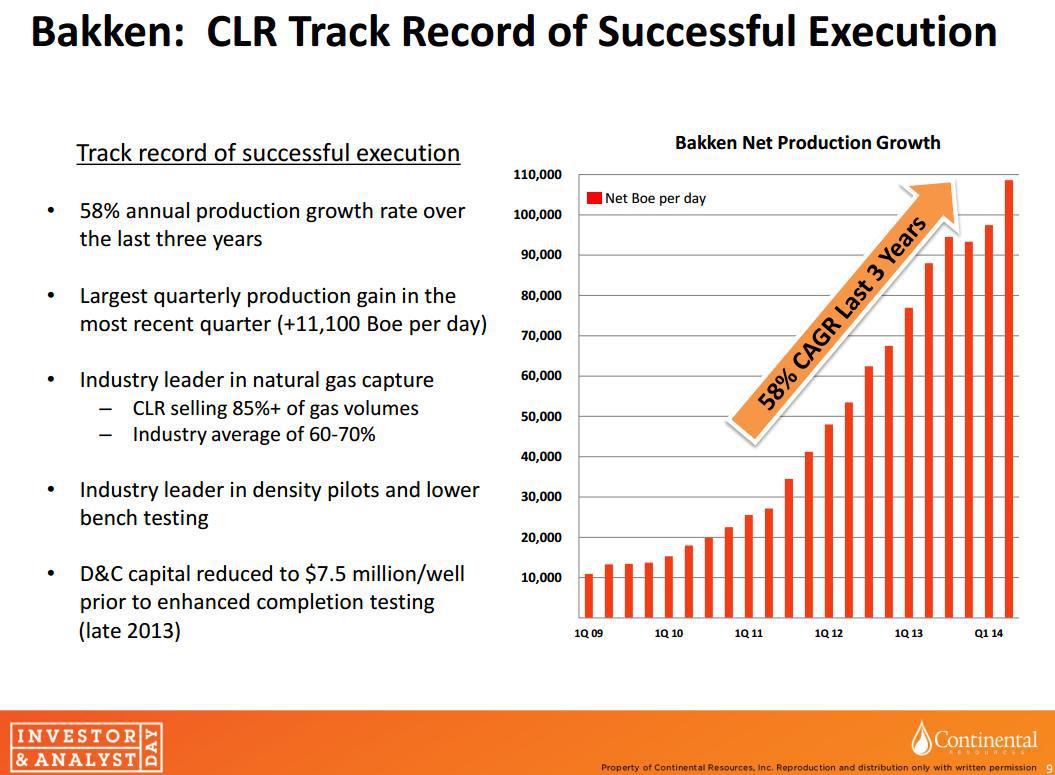

Continental Resources (NYSE:CLR) grew its Bakken production volumes at a 58% CAGR over the past three years (slide below). By looking at the company’s historical production, it would be difficult to identify any impact from the 2012 and 2013 oil price corrections on the company’s production growth rate. Continental just announced a reduction to its capital budget in 2015 in response to lower oil prices, to $4.6 billion from $5.2 billion planned initially. The company still expects to grow its total production in 2015 by 23%-29% year-on-year.

(Source: Continental Resources, October 2014)

(Source: Continental Resources, October 2014)

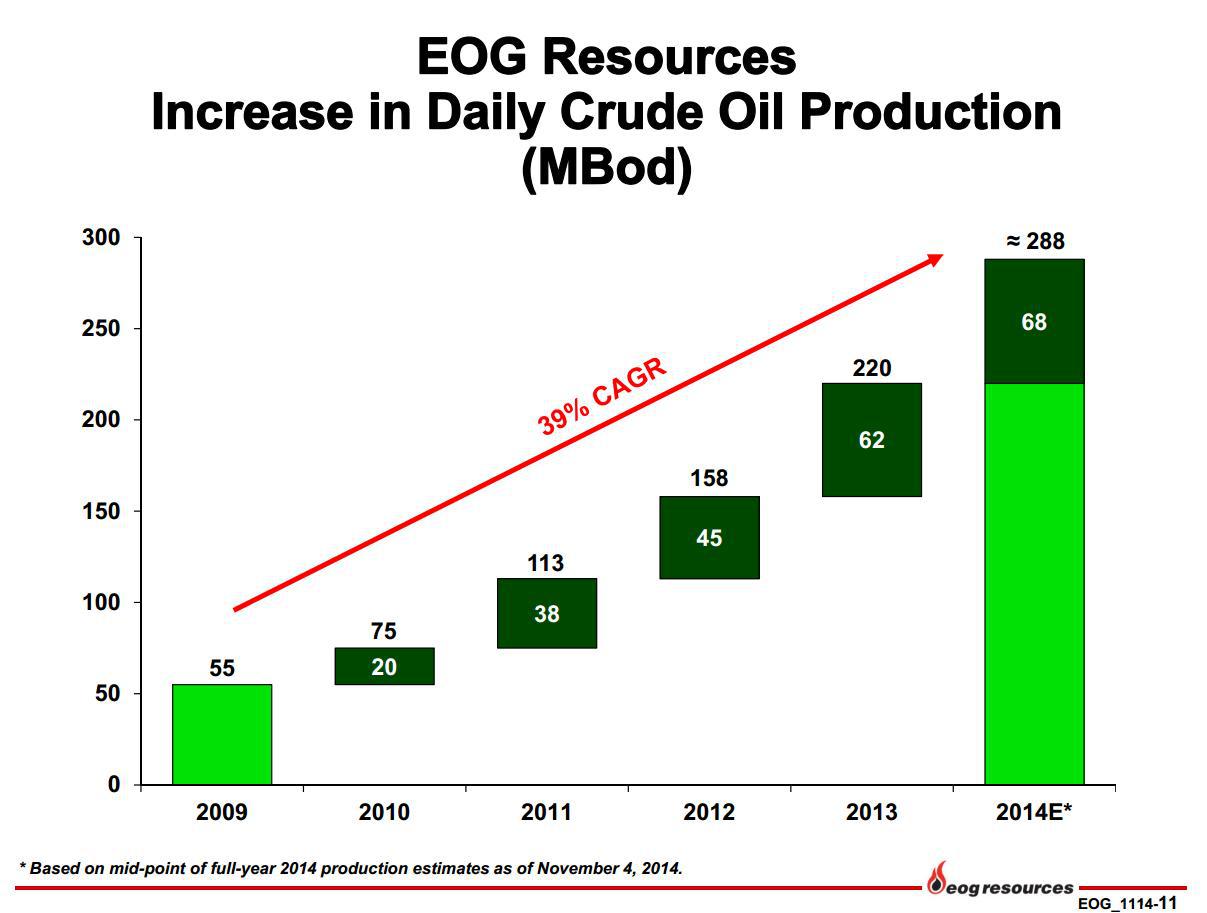

EOG Resources (NYSE:EOG) expects that its largest core plays (Eagle Ford, Bakken and Delaware Basin) will generate after-tax rates of return in excess of 100% in 2015 at $80 per barrel wellhead price. EOG went further to suggest that these plays may remain economically viable (10% well-level returns) at oil prices as low as $40 per barrel. The company expects to continue to grow its oil production at a double-digit rate in 2015 while spending within its cash flow. EOG achieved ~40% oil production growth in 2012-2013 and expects 31% growth for 2014. While a slowdown is visible, it is important to take into consideration that EOG’s oil production base has increased dramatically in the past three years and requires significant capital just to be maintained flat. Again, one would not notice much impact from prior years’ oil price corrections on EOG’s production growth trajectory.

(Source: EOG Resources, November 2014)

(Source: EOG Resources, November 2014)

Anadarko Petroleum’s (NYSE:APC) U.S. onshore oil production growth story is similar. Anadarko increased its U.S. crude oil and NLS production from 100,000 barrels per day in 2010 to close to almost 300,000 barrels per day expected in Q4 2014. Anadarko has not yet provided growth guidance for 2015, but indicated that the company’s exploration and development strategies remain intact. While recognizing a very steep decline in the oil price, Anadarko stated that it wants “to watch this environment a little longer” before reaching conclusions with regard to the impact on its future spending plans.

(Source: Anadarko Petroleum, October 2014)

(Source: Anadarko Petroleum, October 2014)

Devon Energy (NYSE:DVN) posted company-wide oil production of 216,000 barrels per day in Q3 2014. While Devon will provide detailed production and capital guidance at a later date, the company has indicated that it sees 20% to 25% oil production growth and mid‐single digit top‐line growth “on a retained‐property basis” (pro forma for divestitures) in 2015.

The list can continue on.

In Conclusion…

Based on preliminary 2015 growth indications from large shale oil operators, North American oil production growth in 2015 will likely remain strong, barring further strong decline in the price of oil.

No slowdown effect from lower oil prices will be seen for at least six months from the time operators received the “price signal” (August-September 2014).

Given the effects of the technical learning curve in oil shales and continuously improving drilling economics, the current ~$77 per barrel WTI price is unlikely to be sufficient to eliminate North American unconventional production growth.

North American shale oil production remains a very small and highly fragmented component of the global oil supply.

The global oil “central bank” (Saudi Arabia and its close allies in OPEC) remain best positioned to quickly re-instate stability of oil price in the event further significant decline occurred.

World Resistance Report: Davos Class Jittery Amid Growing Warnings of Global Unrest

World of Resistance Report: Davos Class Jittery Amid Growing Warnings of Global Unrest

By: Andrew Gavin Marshall

Originally posted on 4 July 2014 at Occupy.com

In Part 1 of the WoR Report, I examined the “global political awakening” as articulated by arch-imperial strategist Zbigniew Brzezinski. In Part 2 published last week I took a more detailed look at the ways global inequality and injustice relate to the coming era of instability and social unrest. Here, in Part 3, I explore the warnings on inequality and revolt now coming from one of the premier institutions of the global oligarchy: the World Economic Forum.

As an annual gathering of thousands of leading financial, corporate, political and social oligarchs in Davos, Switzerland, the World Economic Forum (WEF) has taken a keen interest in recent years discussing the potential for social upheaval as a result of mass inequality and poverty. A WEF report released in November of 2013 warned that a “lost generation” of unemployed youth in Europe could potentially pull the Eurozone apart. One of the report’s authors, the CEO of Infosys, commented that “unless we address chronic joblessness we will see an escalation in social unrest,” noting that youth especially “need to be productively employed, or we will witness rising crime rates, stagnating economies and the deterioration of our social fabric.” The report added: “A generation that starts its career in complete hopelessness will be more prone to populist politics and will lack the fundamental skills that one develops early on in their career.”

In short, if the global ruling class – known affectionately as the Davos Class – doesn’t quickly find ways to accommodate the continent’s increasingly unemployed and “lost” youth, those people will potentially turn to “populist politics” of resistance that directly challenge the global political and economic order. For the individuals and interests represented at the World Social Forum, this poses a monumental and, increasingly, an existential threat.

The World Economic Forum’s Global Competitiveness Report for 2013-2014, entitled “Assessing the Sustainable Competitiveness of Nations,” noted that the global financial crisis and its aftermath “brought social tensions to light” as economic growth was not translated into positive benefits for much or most of the planet’s population. Citing the Arab Spring, growing unemployment in Western economies and increasing income inequality, there was growing recognition that dangerous upheaval could be on the way. The report noted: “Diminishing economic prospects, sometimes combined with demand for more political participation, have also sparked protests in several countries including, for example, the recent events in Brazil and Turkey.”

The WEF report wrote that “if economic benefits are perceived to be unevenly redistributed within a society,” this could frequently result in “riots or social discontent” such as the Arab Spring revolts, protests in Brazil, the Occupy Wall Street movement, and other recent examples. The report concluded that numerous nations were at especially high risk of social unrest, including China, Indonesia, Turkey, South Africa, Brazil, India, Peru and Russia, among others.

In early 2014, the World Economic Forum released the 9th edition of its Global Risks report, published to inform the debate, discussion and planning of attendees and guests at the annual WEF meeting in Davos. The report was produced with the active cooperation of major universities and financial corporations, including Marsh & McLennan Companies, Swiss Re, Zurich Insurance Group, National University of Singapore, University of Oxford, and the University of Pennsylvania’s Wharton Risk Management and Decision Processes Center. It included a large survey conducted in an effort to assess the major perceived risks to the global order atop which the Davos Class sits.

The report noted that the “most interconnected” risks were fiscal crises, structural unemployment and underemployment, all of which link to “rising income inequality and political and social instability.” The young generation now coming of age globally, noted the WEF, “faces high unemployment and precarious job situations, hampering their efforts to build a future and raising the risk of social unrest.” This “lost generation” faces not only high unemployment and underemployment, but also major educational challenges since “traditional higher education is ever more expensive and its payoff more doubtful.”

Perceiving the innovations and skills of today’s generation which are enabling the growing foment, the Forum noted:

“In general, the mentality of this generation is realistic, adaptive and versatile. Smart technology and social media provide new ways to quickly connect, build communities, voice opinion and exert political pressure… [youth are] full of ambition to make the world a better place, yet feel disconnected from traditional politics and government – a combination which presents both a challenge and an opportunity in addressing global risks.”

The Global Risks 2014 report cited a global opinion survey on the “awareness, priorities and values of global youth,” which the authors refer to as “generation lost.” This generation, noted the survey, “think independently of this basic fallback system of the older generation – governments providing a safety net,” which “points to a wider distrust of authorities and institutions.” The “mindset” of today’s youth has been additionally shaped by the repercussions and apparent failures to deal with the global financial crisis, as well as increasing revelations about U.S. intelligence agencies engaging in massive digital spying. For a generation largely mobilized through social media, online spying has held particular relevance, as “the digital revolution gave them unprecedented access to knowledge and information worldwide.”

Protests and anti-austerity movements were able to “give voice to an increasing distrust in current socio-economic and political systems,” with youth making up significant portions of “the general disappointment felt in many nations with regional and global governance bodies such as the EU and the International Monetary Fund.” The youth “place less importance on traditionally organized political parties and leadership,” which creates a major “challenge for those in positions of authority in existing institutions” as they try “to find ways to engage the young generation,” adds the report.

According to the World Bank, more than 25% of the world’s youth, or some 300 million people, “have no productive work.” On top of this, “an unprecedented demographic ‘youth bulge’ is bringing more than 120 million new young people on to the job market each year, mostly in the developing world.” This fact “threatens to halt economic progress, creating a vicious cycle of less economic activity and more unemployment,” which “raises the risk of social unrest by creating a disaffected ‘lost generation’ who are vulnerable to being sucked into criminal or extremist movements.”

Noting that more than 1 billion people currently live in slums – a number that has been steadily increasing as income inequality rises – the report stated that “this growing population of urban poor is vulnerable to rising food prices and economic crises, posing significant risks of chronic social instability.” Growing income inequality is now being termed a “systemic risk,” according to the WEF. And in a stark admission from that institution representing the world’s major profiteers of global capitalism, the report acknowledged that globalization “has been associated with rising inequality between and within countries” and that “these factors render poor people and poor countries vulnerable to systemic risks.”

The four major “emerging market” BRIC nations of Brazil, Russia, India and China “now rank among the 10 largest economies worldwide.” But slow political reforms within these countries, coupled with external economic shocks (like financial crises caused by Western nations and their corporate institutions) could aggravate the “existing undertones of social unrest.” Within the BRIC nations and other emerging market economies, “popular discontent with the status quo is already apparent among rising middle classes, digitally connected youths and marginalized groups,” the report went on. Collectively, these groups “want better services (such as healthcare), infrastructure, employment and working conditions,” as well as “greater accountability of public officials, better protected civil liberties and more equitable judicial systems.” Further, a “greater public awareness of widespread corruption have sharpened popular complaints.”

Both Brazil and Turkey have made universal healthcare systems a constitutional obligation, which was a stated ambition of other emerging market nations such as India, Indonesia and South Africa. The failure to create these healthcare systems “may arouse social unrest,” warned the WEF. The World Economic Forum’s chief economist, Jennifer Blanke, stated: “The message from the Arab Spring, and from countries such as Brazil and South Africa is that people are not going to stand for it any more.” David Cole, the group chief risk officer of Swiss Re (one of the contributing companies to the WEF report) commented: “The members of generation lost are not lost because they have tuned out. They are highly tuned in. They are lost because they are being left out or they are deciding to leave.” http://www.theguardian.com/business/2014/jan/16/income-gap-biggest-risk-global-community-world-economic-forum

The World Economic Forum’s Risk report for 2014 was primarily concerned with “the breakdown of social structures” and “the decline of trust in institutions.” It warned of risks of “ideological polarization, extremism – in particular those of a religious or political nature – and intra-state conflicts such as civil wars.” All of these issues relate directly “to the future of the youth.”

It’s an interesting paradox for an organization to see the greatest threat to its ideological and social power being “the future of the youth” when it has already written off the present generation as “lost.” However, this is a view shared not only by the World Economic Forum but, increasingly, by other powerful institutions creating something of an echo chamber through the mainstream media. The head of the IMF has warned that youth unemployment in poor nations was “a kind of time bomb,” and the head of the International Labor Organization (ILO) warned in 2011 that the “world economy” was unable “to secure a future for all youth,” thus undermining “families, social cohesion and the credibility of policies.” While there was “already revolution in the air in some countries,” as reported in the Globe and Mail, the dual crises of unemployment and poverty were “fuel for the fire.”

In April of 2014, the World Economic Forum on Latin America reported that the primary challenge for the region was “to reduce inequality,” noting that between 70 and 90 million people in Latin America had entered what were referred to as the “consuming classes,” or “middle classes,” over the previous decade. However, Marcelo Cortes Neri, Brazil’s Minister of Strategic Affairs, explained, “When we talk about middle class we think of the U.S. middle class, with two cars and two dogs and a swimming pool. That is not Latin American middle class or the world middle class.”

He added that the emerging so-called “middle class” in Latin America and elsewhere “could become a problem for governance,” commenting: “They are the ones that put pressure for better levels of education and healthcare; they are the ones that go to the streets to demand rights.” Neri then posed the question: “How prepared is Latin America to have a robust middle class?” In particular, youth between the ages of 15 and 29 raised specific concerns for Latin America’s elite, with Neri warning: “This is the group I am most worried about. They have very high expectations and so the probability they will get frustrated is enormous.”

When one of the world’s most influential organizations representing the collective interests of the global oligarchy openly acknowledges that globalization has increased inequality, and in turn, that inequality is fueling social unrest around the world manifesting the greatest potential threat to those oligarchic interests, we can safely say we’re entering a new era of global instability and resistance.

Andrew Gavin Marshall is a researcher and writer based in Montreal, Canada. He is project manager of The People’s Book Project, chair of the geopolitics division of The Hampton Institute, research director for Occupy.com’s Global Power Project and World of Resistance Report, and host of a weekly podcast show with BoilingFrogsPost.

You must be logged in to post a comment.