Over the last year, sales of Chinese property stocks are down almost 25%. To put this in perspective, this is worse than 2008 when sales fell by ~20%. China also cut interest rates on $5.6 trillion of mortgages with their HY real estate index down 80%+.

China’s real estate market is beyond recession territory.

(Catherine Yang) China Evergrande Group announced on Sept. 28 that its chairman and founder has been suspected of committing crimes, confirming reports that Hui Ka Yan was under police surveillance.

(Redacted News) China and Saudi Arabia just dealt a throat punch to the U.S. dollar. This first week of April we got our clearest sign yet that America is in serious economic trouble after China and Saudi Arabia filed new agreements on oil and trade. But the biggest problem came from the Crown Prince who said he’s done trying to please The United States.

Steve Cortes was on Steve Bannon’s War Room Monday. He discussed growing evidence of China’s failing economy which impacts the US economy greatly. To put it mildly, China’s economy is falling apart.

An aerial view shows the 39 buildings developed by China Evergrande Group that authorities have issued a demolition order on in Hainan Province, China, on Jan. 6, 2022. (Aly Song/Reuters)

(Daily Veracity) Similar to Japan’s devastating 80% market crash in the 1990s, China’s economy is about to experience the biggest crash in history that will take decades to recover from.

China’s factory-gate prices grew at the fastest pace in almost 26 years in September, adding to global inflation risks and putting pressure on local businesses to start passing on higher costs to consumers.

SHANGHAI, Sept 29 (Reuters) – China’s vast Belt and Road Initiative (BRI) is in danger of losing momentum as opposition in targeted countries rises and debts mount, paving the way for rival schemes to squeeze Beijing out, a new study showed on Wednesday.

Pictured are travelers walking past a map displaying CCP targets of conquest

An alarming briefing by a top Australian general to his troops leaked by an anonymous source warns of a “high likelihood” of war with Communist China.

(Jamie White) According to the confidential briefing obtained by the Sydney Morning Herald on Tuesday, Australian Defense Force (ADF) adviser Major-General Adam Findlay said last year that China was already engaged in “grey zone” warfare.

Yesterday ZeroHedge discussed why western Corporations are terrified to confront China, even if it means losing on those all-important virtue signaling brownie points which are all that matter in Western society today: as a reminder, the stock of H&M, Nike and Adidas came under fire on Chinese social media on Thursday after Beijing’s propaganda offensive against Swedish fashion brand H&M sparked by the company’s expression of concern about labor conditions in Xinjiang. The sportswear companies were the latest to be caught up in a backlash prompted by a government call to stop foreign brands from tainting China’s name as internet users found statements they had made in the past on Xinjiang.

On Friday, as the Xinjiang spat escalated, China showed just how easy it is for Western companies to literally disappear when outlets belonging to Sweden’s H&M (Hennes & Mauritz AB) – the fashion retailer that found itself at the center of an escalating spat over human rights in Xinjiang – did not to show up on Apple Maps and Baidu Maps searches in China.

Tensions spiked in the South China Sea and near Taiwan over this past weekend and have continued boiling since, after Chinese PLA aircraft made repeat in incursions into Taiwan’s claimed airspace. In response Taiwan’s Air Force scrambled jets in its own ‘show of strength’ deterrence message, and with the US aircraft carrier USS Roosevelt in the region, China’s Defense Ministry subsequently warned Taipei on Thursday that “independence means war”.

A new report in FT that broke overnight now reveals that the Sunday incident was even more alarming for the prospect of direct conflict than previously thought. FT cites unnamed intelligence sources to report that “Chinese military aircraft simulated missile attacks on a nearby US aircraft carrier during an incursion into Taiwan’s air defense zone three days after Joe Biden’s inauguration, according to intelligence from the US and its allies.”

File image of Taiwan Air Force F-16 monitoring a Chinese H-6 bomber, via Taiwan’s Defense Ministry

(by Graham Allison) China has now displaced the U.S. to become the largest economy in the world. Measured by the more refined yardstick that both the IMF and CIA now judge to be the single best metric for comparing national economies, the IMF Report shows that China’s economy is one-sixth larger than America’s ($24.2 trillion versus the U.S.’s $20.8 trillion). Why can’t we admit reality? What does this mean?

On Thursday, China for the first time sold dollar-denominated bonds directly to US buyers and with the Chinese 10Y offering a record 2.5% pickup in yield compared to 10Y Treasuries, it’s hardly a surprise that demand was off the charts.

The $6 billion bond offering which took place in Hong Kong, drew record demand, in part due to the attractive yield offered by Chinese paper and in part due to China’s impressive recovery from the coronavirus, with an orderbook more than $27 billion, or roughly $10 billion more than an offering of the same size last November, according to the FT, which added about 15% of the offering went to American investors.

The $6BN USD-denominated bond offering was as follows:

$1.25BN in 3-year dollar bonds at 0.425%

$2.25BN 5-year dollar bonds at 0.604%

$2BN 10-year dollar bonds at 1.226%

$500MM 30-year dollar bonds at 2.310%

The yield on the 10-year bond was about 0.5% above the equivalent US Treasury, and helped the bond sales receive “a strong reception from US onshore real money investors”, said Samuel Fischer, head of China onshore debt capital markets at Deutsche Bank, which helped arrange the deal. Other arrangers of the bond sale included Standard Chartered, Bank of America, Citigroup, Goldman Sachs and JPMorgan.

What was unique about today’s offering is that unlike previous issuance, “the debt was sold under a mechanism that gave institutional investors in the US the chance to buy in.”

Somewhat surprising is that frictions between Beijing and Washington had no impact “at all” on demand from US buyers, which included an American pension fund, one banker told the FT. In fact, the strategic timing of the bond sale which was arranged by the Chinese government just weeks before Americans head to the polls for the presidential election was meant to show “how tightly the financial systems of the two countries are linked, despite a trade war and tensions over technology and geopolitics.”

“This is the investor community showing confidence in [China’s] recovery,” said another banker on the sale, who added that “US investor participation in Chinese paper is not reduced by any means.”

Analyst responses were broadly enthusiastic about the offering:

Hayden Briscoe, head of fixed income for Asia Pacific at UBS Asset Management, said the bonds would help “set the benchmark” for Chinese corporates such as petrochemical groups Sinopec and Sinochem, which also borrow in dollars. “A lot of their expenses are in US dollars, and they borrow in the dollar market to match funds to that.”

He added that the bonds benefited from strong demand partly due to their scarcity value. “There’s so few of them and they suit sovereign wealth fund type buyers — they tend to just disappear.”

White House trade adviser Peter Navarro said on Monday the trade deal with China is “over,” and he linked the breakdown in part to Washington’s anger over Beijing’s not sounding the alarm earlier about the coronavirus outbreak.

“It’s over,” Navarro told Fox News in an interview when asked about the trade agreement. He said the “turning point” came when the United States learned about the spreading coronavirus only after a Chinese delegation had left Washington following the signing of the Phase 1 deal on Jan. 15.

“It was at a time when they had already sent hundreds of thousands of people to this country to spread that virus, and it was just minutes after wheels up when that plane took off that we began to hear about this pandemic,” Navarro said.

U.S.-China relations have reached their lowest point in years since the coronavirus pandemic that began in China hit the United States hard. President Donald Trump and his administration repeatedly have accused Beijing of not being transparent about the outbreak.

Trump on Thursday renewed his threat to cut ties with China, a day after his top diplomats held talks with Beijing and his trade representative said he did not consider decoupling the U.S. and Chinese economies a viable option.

Navarro has been one of the most outspoken critics of China among Trump’s senior advisers.

In other news, Catherine Austin Fitts provides a big picture update with Greg Hunter …

In the last few weeks, ZeroHedge provided many articles on the evidence of creaking global supply chains fast emergingin China and spreading outwards. Anyone in supply chain management, monitoring the flow of goods and services from China, has to be worried about which regions will be impacted the most (even if the stock market couldn’t care less).

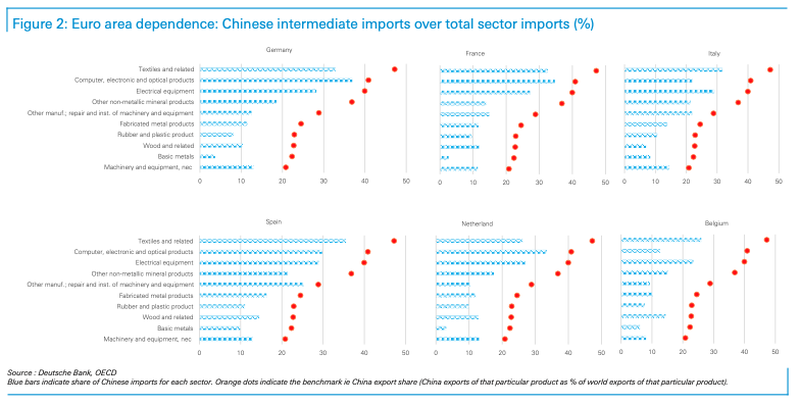

Deutsche Bank’s senior European economist Clemente Delucia and economist Michael Kirker published a note on Thursday titled “The impact of the coronavirus: A supply-chain analysis” identifying the effect of contagion on the rest of the world, mainly focusing on demand and spillover effects into other countries.

The economists constructed a ‘dependency indicator,’ to figure out just how much a country depends on China for the supply of particular imported inputs. It was noted that the more a country depends on China, the more challenging it could be for businesses to find alternative sourcing during a period of supply chain disruptions.

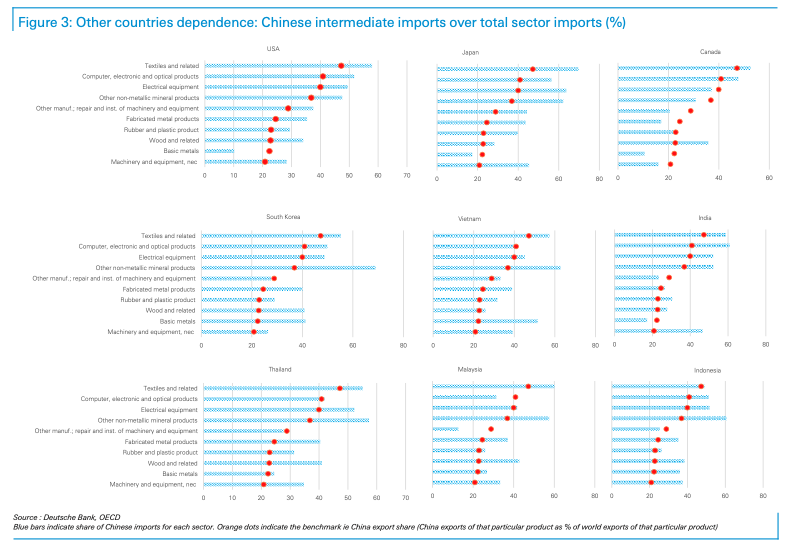

The biggest takeaway from the report is that, surprisingly, the European Union is less directly exposed to a China supply-chain shock than the US, Canada, Japan, and all the major Asian countries (i.e., India, South Korea, Indonesia, Malaysia, Vietnam).

It was determined that in the first wave of supply chain disruptions that “euro-area countries are somewhat less directly dependent on China for intermediate inputs than other major economies in the rest of the world.”

“The euro-area countries have, in general, a dependence indicator below the benchmark. This suggests that euro-area countries have a below-average direct dependence on Chinese imports of intermediate inputs (Figure 2).”

But since China is highly integrated into the global economy, and a supply chain shock would be felt across the world. The second round of disruptions would result in lower world trade growth that would eventually filter back into the European economy.

The US, Japan, Canada, and all the major Asian countries would feel an immediate supply chain shock from China.

Here’s a chart that maps out lower dependency and higher dependency countries to disruption from China.

To summarize, the European Union might escape disruptions from China supply chain shocks in the first round, but ultimately will be affected as global growth would sag. As for the US and Japan, Canada, and all the major Asian countries, well, the disruption will be almost immediate and severe with limited opportunities for companies to find alternative sourcing.

“First of all, our analysis does not take into account non-linearity in the production process. In other words, it does not capture consequences from a stop in production for particular product. It might indicate that given the dependence is smaller, Europe could find it somewhat easier substitute a Chinese product with another. But there is no guarantee this will be the case.”

“Secondly, while our results indicates that the direct impact from supply issues in China could be smaller for the euro area than for other regions in the world, the euro area could be hard-hit by second-round effects. With their higher direct exposure to China, production in other major economies could slow down as a result of disruptions in the supply chain. This not only could cause a shortage in demand for euro-area exports, but it could also impact on the euro-area’s import of intermediate inputs from these other countries (second-round effects). In other words, China has become a relevant player in the world supply chain and production/demand problems in China are spread worldwide through direct and indirect channels.“

News flow this week has indeed suggested the virus is spreading outwards, from East to West, and could get a lot worse ex-China into the weekend.

The mistake of the World Health Organization (WHO), governments, and global trade organizations to minimize the economic impact (protect stock markets) of the virus was to allow flights, businesses, and trade to remain open with China. This allowed the virus to start spreading across China’s Belt and Road Initiative (BRI).

Enjoy a riveting weekly news wrap up with Greg Hunter…

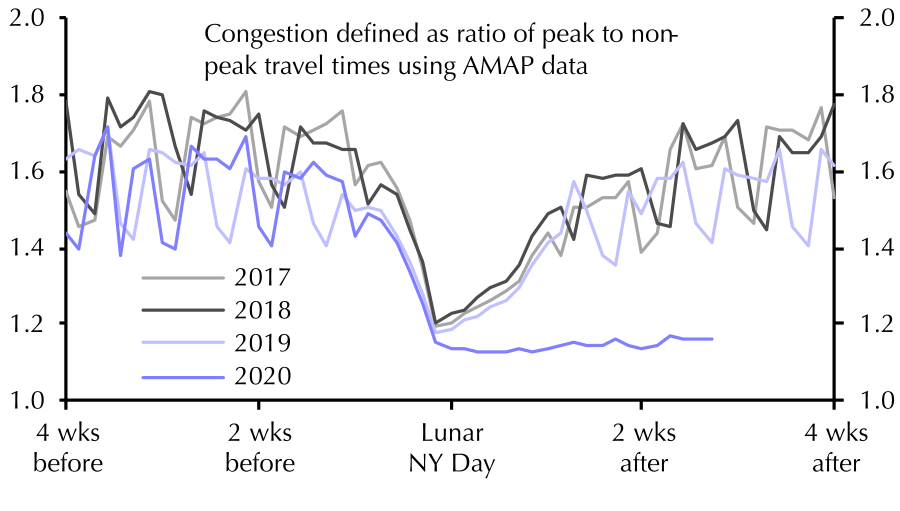

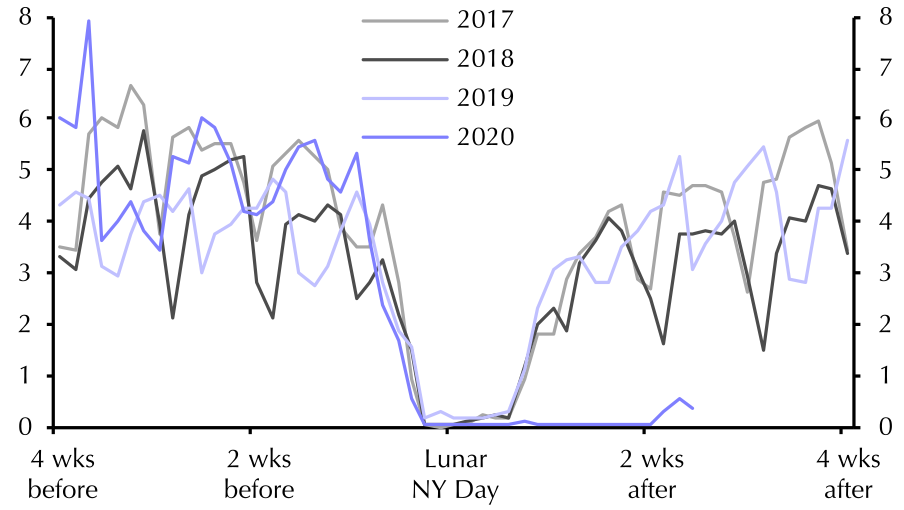

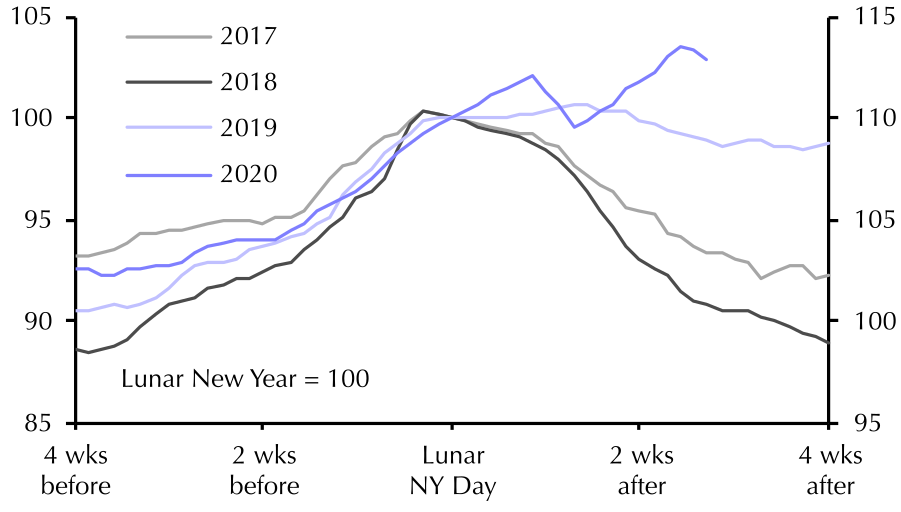

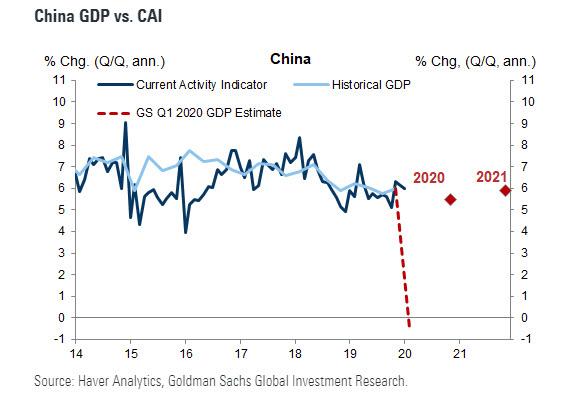

In our ongoing attempts to glean some objective insight into what is actually happening “on the ground” in the notoriously opaque China, whose economy has been hammered by the Coronavirus epidemic, yesterday ZeroHedge showed several “alternative” economicindicators such as real-time measurements of air pollution (a proxy for industrial output), daily coal consumption (a proxy for electricity usage and manufacturing) and traffic congestion levels (a proxy for commerce and mobility), before concluding that China’s economy appears to have ground to a halt.

That conclusion was cemented after looking at some other real-time charts which suggest that there is a very high probability that China’s GDP in Q1 will not only flatline, but crater deep in the red for one simple reason: there is no economic activity taking place whatsoever.

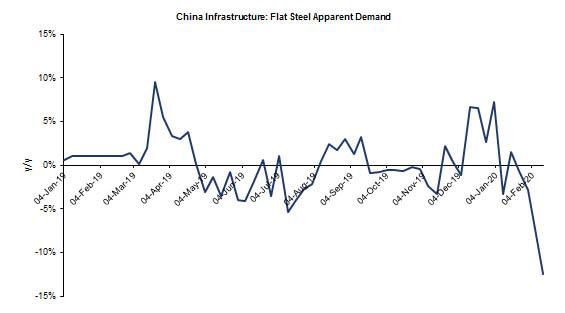

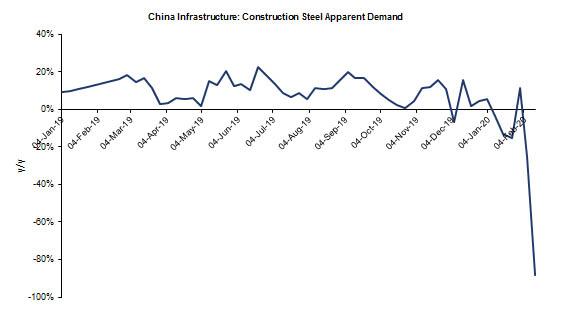

We start with China’s infrastructure and fixed asset investment, which until recently accounted for the bulk of Chinese GDP. As Goldman writes in an overnight report, in the Feb 7-13 week, steel apparent demand is down a whopping 40%, but that’s only because flat steel is down “only” 12% Y/Y as some car plants have ordered their employee to return to work (likely against their will as the epidemic still rages).

However, it is the far more important – for China’s GDP – construction steel sector where apparent demand has literally hit the bottom of the chart, down an unprecedented 88% Y/Y or as Goldman puts it, “construction steel demand is approaching zero.”

But wait, there’s more.

Courtesy of Capital Economics, which has compiled a handy breakdown of real-time China indicators, we can see the full extent of just how pervasive the crash in China’s economy has been, starting with familiar indicator, the average road congestion across 100 Chinese cities, which has collapsed into the New Year and has since failed to rebound.

Parallel to this, daily passenger traffic has also flat lined since the New Year and has yet to post an even modest rebound.

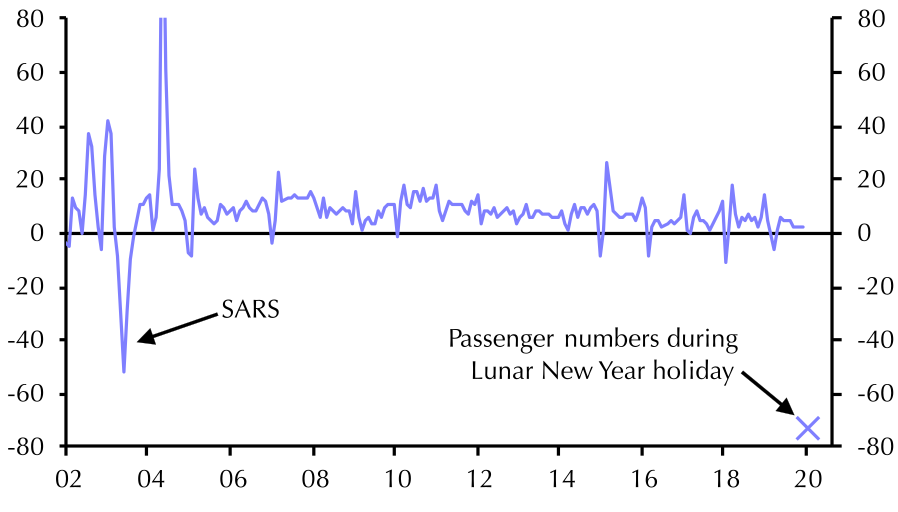

And the biggest shocker: a total collapse in passenger traffic (measured in person-km y/y % change), largely due to the quarantine that has been imposed on hundreds of millions of Chinese citizens.

And while we already noted the plunge in coal consumption in power plants as Chinese electricity use has cratered…

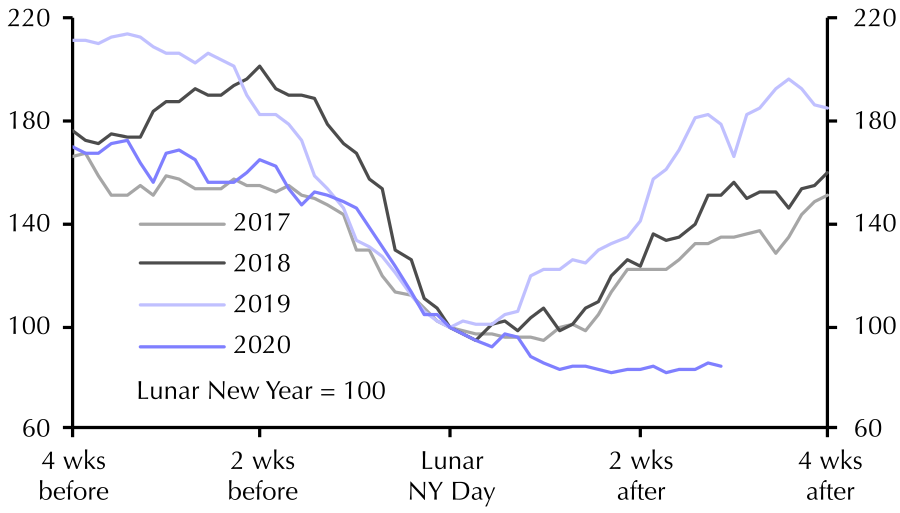

… what is perhaps most striking, is the devastation facing the Chinese real estate sector where property sales across 30 major cities have basically frozen.

Finally, and most ominously perhaps, as the economy craters and internal supply chains fray, prices for everyday staples such as food are soaring as China faces not only economic collapse, but also surging prices for critical goods, such as food as shown in the wholesale food price index chart below…

… which in a nation of 1.4 billion is a catastrophic mix.

As the coronavirus pandemic spreads further without containment, and as the charts above continue to flat line, so will China’s economy, which means that not only is Goldman’s draconian view of what happens to Q1 GDP likely optimistic as China now faces an outright plunge in Q1 GDP…

… but any the expectation for a V-shaped recovery in Q2 and onward will vaporize faster than a vial of ultra-biohazardaous viruses in a Wuhan virology lab.

Ending the limited quarantine and falsely proclaiming China safe for visitors and business travelers will only re-introduce the virus to workplaces and infect foreigners.

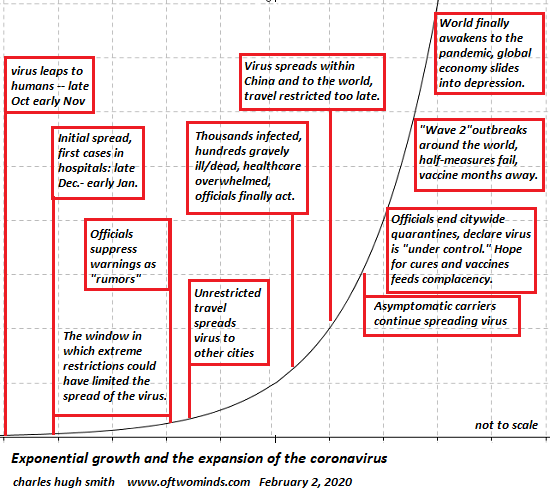

(Charles Hugh Smith) China faces an inescapably fatal dilemma: to save its economy from collapse, China’s leadership must end the quarantines soon and declare China “safe for travel and open for business” to the rest of the world.

But since 5+ million people left Wuhan to go home for New Years, dispersing throughout China, the virus has likely spread to small cities, towns and remote villages with few if any coronavirus test kits and few medical facilities to administer the tests multiple times to confirm the diagnosis. (It can take multiple tests to confirm the diagnosis, as the first test can be positive and the second test negative.)

As a result, Chinese authorities cannot possibly know how many people already have the virus in small-town / rural China or how many asymptomatic carriers caught the virus from people who left Wuhan. They also cannot possibly know how many people with symptoms are avoiding the official dragnet by hiding at home.

No data doesn’t mean no virus.

If the virus has already been dispersed throughout China by asymptomatic carriers who left Wuhan without realizing they were infected with the pathogen, then regardless of whatever official assurances may be announced in the coming days/weeks, it won’t be safe for foreigners to travel in China nor will it be safe for Chinese workers to return to factories, markets, etc.

But if China doesn’t “open for business” with unrestricted travel soon, its economy will suffer calamitous declines as fragile mountains of debt and leverage collapse and supply chain disruptions push global corporations to find permanent alternatives elsewhere.

Here’s the fatal dilemma: maintaining the quarantine long enough to truly contain it (which requires extending it to the entire country) will be fatal to China’s economy.

But ending the limited quarantine and falsely proclaiming China safe for visitors and business travelers will only re-introduce the virus to workplaces and infect foreigners who will return home as asymptomatic carriers, spreading the virus in their home nations.

Falsely declaring China safe will endanger everyone credulous enough to believe Chinese officials, and destroy whatever thin shreds of credibility China may yet have in the global economy and community. That will set off chains of causality that will destroy China’s economy just as surely as a three-month nationwide quarantine.

Who will be foolish enough to believe anything Chinese officials proclaim after foreigners who accepted the false assurances of safety return home with the coronavirus?

Air freight takes 12 to 24 hours, add another few hours for packaging, handling and last-mile delivery and that leaves 6+ days for the virus to spread to anyone who touches goods handled by an symptomatic carrier. Maybe the odds of catching the virus via surfaces are low, but maybe not. No one knows, including anyone rash enough to claim that the risk is negligible.

Bloombergcited a new report via China Merchants Securities (CMSC) that said new apartment sales crashed 90% in the first week of February over the same period last year. Sales of existing homes in 8 cities plunged 91% over the same period.

Wuhan, Hubei, China Sunrise

“The sector is bracing for a worse impact than the 2003 SARS pandemic,” said Bai Yanjun, an analyst at property-consulting firm China Index Holdings Ltd. “In 2003, the home market was on a cyclical rise. Now, it’s already reeling from an adjustment.”

Long before the coronavirus outbreak, China’s housing market has been on shaky grounds amid declining demand, stricter mortgage requirements, and price discounts.

The latest shock: two-thirds of China’s economy has come to a standstill, could generate enough pessimism to pop the country’s massive housing bubble.

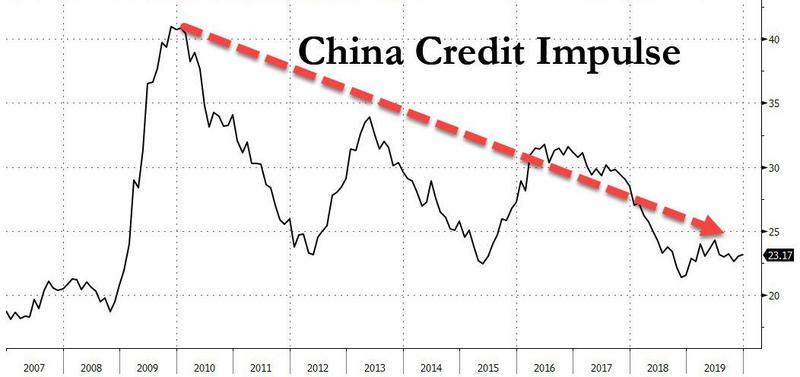

The CPC failed to stimulate the economy last year, with credit impulse not turning up as expected. The virus outbreak has allowed the CPC to scapegoat the slowdown and the inevitable crash.

Real estate transactions have been forbidden in many cities. This means fire sales could be seen once selling restrictions end.

E-House China Enterprise Holdings Ltd.’s research institute said four units per day were being sold in Beijing last week, and this is down from several hundred per day during the same period in the previous year.

China International Capital Corp. analyst Eric Zhang said demand could pick back up in April, assuming the virus outbreak is under control.

The downturn in China’s property market could get a lot worse, and without proper liquidity from the central bank, once selling restrictions end, it could trigger a liquidity gap where housing prices face a deep correction.

But remember, the CPC can now blame the virus for a housing market crash or a downturn in the economy.

Soon the only food that will be affordable in China, is coronabat stew.

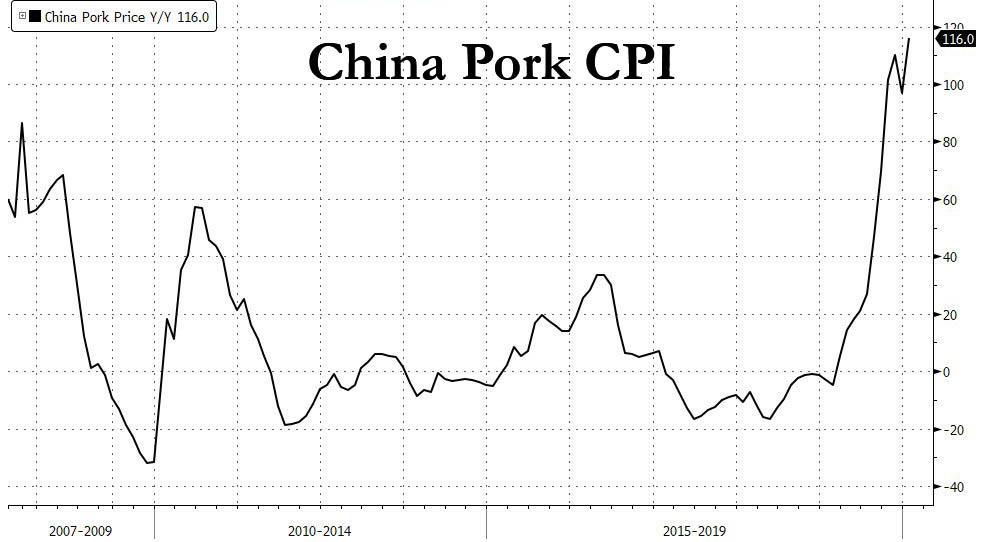

With over 400 million people across dozens of Chinese cities living in lock down as a result of the Coronavirus pandemic, crippling global supply chains and grinding China’s economy to a halt, it is easy to forget that China has been battling another major viral epidemic for the past two years: namely the African Swing Fever virus, aka “pig ebola” which killed off over half of China’s pig population in the past year, sending pork prices soaring, and unleashing a tidal wave of inflation.

Well, earlier today, the world got a stark reminder of this when China reported that in January, its CPI jumped by whopping 5.4% Y/Y, the highest print in nine years…

… driven by a surge in pork prices, which reversed a rare drop in December when the slid by 5.6%, rising 8.5% in just ont month, and a record 116% compared to a year ago.

This unprecedented surge in pork CPI meant that China’s food CPI rose a record 20.6% in January, also the highest on record, as China’s population, now ordered to live under self-imposed quarantine, suddenly finds it can no longer afford to buy food.

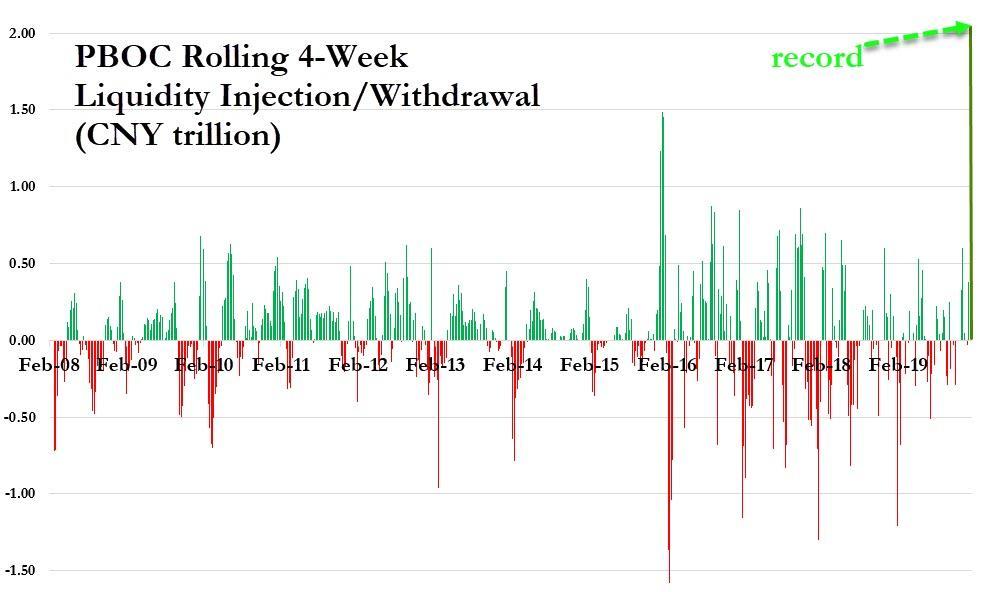

Needless to say, this is suddenly a major problem for China, whose central bank has in the past two weeks unleashed an unprecedented liquidity tsunami, including the biggest ever reverse repo injection…

… in hopes of stabilizing the stock market. Well, oops, because some of this liquidity now appears to be making its way into the broader economy, and is making already scarce food (aside from bat stew of course) even more un-affordable, and the already depressed and dejected Chinese population even more hungry, and angry.

There was one silver lining in today’s data: after spending half a year in deflation, China’s Production Prices, a proxy for industrial profits and overall price leverage, finally printed in the positive, rising 0.1% Y/Y, and better than the expected 0.0%

So far so good, however, with China’s economy now on indefinite lock down, expect the correlation shown in the chart above to break any moment now, with industrial profits crashing as a result of the coronavirus putting countless Chinese factories on lock down at least until the coronavirus is contained. When that happens is anyone’s guess, but one thing is certain: at the rate food prices are exploding, soon the only food China’s population will be able to afford will be the experimental bats used by the Wuhan Institute of Virology, one of which may or may not have been accidentally sold to the local fish market last December triggering what is now the worst viral pandemic in decades.

Just as concerning, if only for Beijing, is that if the surge in food prices isn’t “contained” very soon the arms of the PBOC will be tied and any hopes that China will reflate its economy – and the world – to offset the economic crunch resulting from the coronavirus, will be weaponized and vaporize right through the HVAC, just like any number of manmade viruses currently being developed in Wuhan, as pretty soon China’s population – starving and quarantined – will have no choice but take matters into its own hands.

Something is seriously starting to break in China’s financial system.

Smog is seen over the city against sky during a haze day in Tianjin, China (Stringer Network)

Three days after we described theself-destructive doom loop that is tearing apart China’s smaller banks,where a second bank run took place in just two weeks – an unprecedented event for a country where until earlier this year not a single bank was allowed to fail publicly and has now hadno less than five bankhigh profile nationalizations/bailouts/runs so far this year – the Chinese bond market is bracing itself for an unprecedented shock: a major, Fortune 500 Chinese commodity trader is poised to become the biggest and highest profile state-owned enterprise to default in the dollar bond market in over two decades.

Before a complete fracturing of the US and Chinese economies, there have already been numerous signs of decoupling that are currently taking place behind the scenes.

But before we tell you about the decoupling and the latest evidence we’ve found. You must be asking: Where are we in the trade war? Beginning innings? Imminent trade deal?

The flurry of trade headlines from the US and China over the last 15 or so months have certainly been confusing. The fact is, there’s so much fake trade news that it’s hard to tell exactly the progress between both countries.

But what’s certain is that the trade war is in the beginning innings and nowhere near being resolved. Yes, there’s a Phase 1 deal being floated around, but that’s only for President Trump to save Midwest farmers and to create positive sentiment ahead of the 2020 election to pump the stock market.

In reality, the trade war is a winner take all game, it’s really about empire, and how Washington is attempting to prevent China from becoming the next global superpower. Hence the reason for tariffs, which is an attempt by President Trump, the Pentagon, and US corporate elites to limit China’s ascension.

The decoupling will be slow at first, then rapid. We’re already seeing small to medium-sized Chinese companies being denied IPOs on Nasdaq. President Trump has already banned Haweui access to key US markets. And now, the next evidence that the decoupling is gaining momentum comes from the US Department Of The Interior.

The Department has grounded its entire fleet of 800 drones for fear that Chinese hackers could spy on critical infrastructure, reported The Wall Street Journal.

“Secretary Bernhardt is reviewing the Department of the Interior’s drone program. Until this review is completed, the Secretary has directed that drones manufactured in China or made from Chinese components be grounded unless they are currently being utilized for emergency purposes, such as fighting wildfires, search and rescue, and dealing with natural disasters that may threaten life or property,” the Department told The Verge via an email statement.

US officials worry that the Department is relying too heavily on Chinese drones and has put critical infrastructure at risk of being spied on by the Chinese.

Last month a bipartisan bill was introduced that would limit federal agencies from purchasing Chinese drones.

Several years ago, the Department of Homeland Security warned federal agencies from purchasing Chinese drones, specifically ones made by Shenzhen-based SZ DJI Technology Co., Ltd.

A DJI spokesperson told The Verge in a statement that the latest grounding of their drones by the Department Of The Interior is rather “disappointing.”

“We are aware the Department of Interior has decided to ground its entire drone program and are disappointed to learn of this development…As the leader in commercial drone technology, we have worked with the Department of Interior to create a safe and secure drone solution that meets their rigorous requirements, which was developed over the course of 15 months with DOI officials, independent cybersecurity professionals, and experts at NASA. We will continue to support the Department of Interior and provide assistance as it reviews its drone fleet so the agency can quickly resume the use of drones to help federal workers conduct vital operations,” the DJI spokesperson said.

The Department’s decision to ground Chinese drones is a clear trend of what’s to come in the year ahead: more groundings across a wide array of agencies.

Just wait until the groundings start hitting state and local municipalities and lower-level agencies. It’s going to be a nightmare.

Nevertheless, when the government starts banning certain Chinese products from consumers, you’ll know the great decoupling between the US and China is imminent.

For this to all happen, the Trump administration will need to ramp up Sinophobia propaganda to convince the American people that decoupling is the right move.

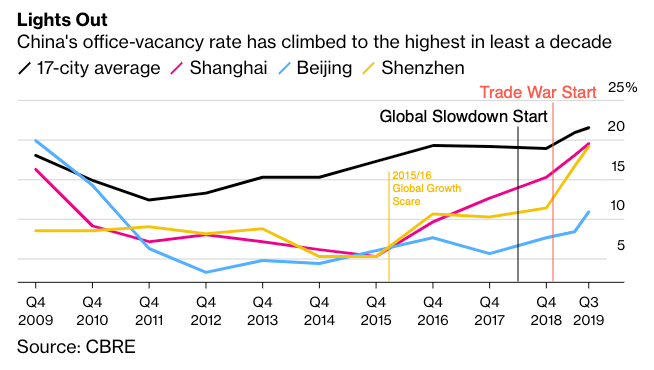

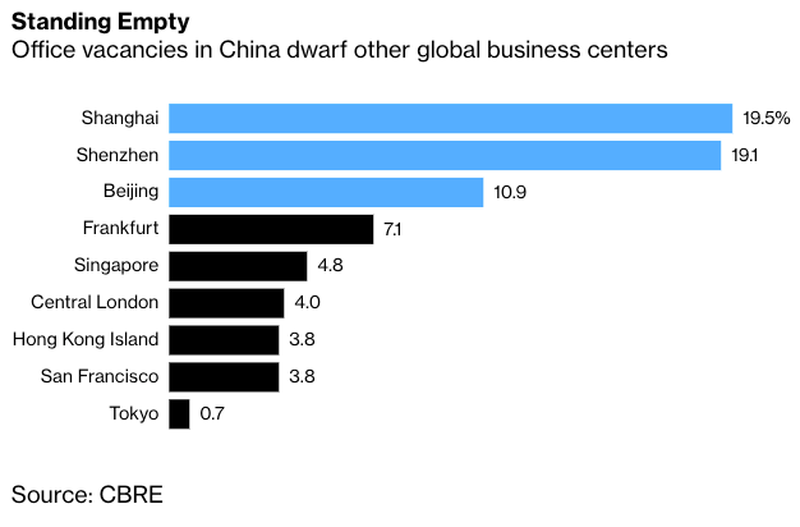

A darkening outlook for China’s economy continues to materialize week by week.

New data from commercial property group CBRE warns the country’s office vacancy rate has just surged to the highest since the financial crisis of 2007–2008, first reported by Bloomberg.

CBRE said the vacancy rate for commercial office space in 17 major cities rose to 21.5% in 3Q19, a level not seen since the global economy was melting down in 2008.

Sam Xie, CBRE’s head of research in China, said the recent “spike” in vacancies is one of the worst since the last financial crisis.

Catherine Chen, Cushman & Wakefield’s head of research for Greater China, toldFinancial Timesthat soaring commercial office vacancies in China was mainly due to dwindling demand, but not oversupplied conditions.

“Contributing factors included slower expansion of co-working operators and financial services companies, and a general cost-saving strategy adopted by most tenants given ongoing trade tensions and economic growth slowdown,” she added.

Henry Chin, head of research for Asia Pacific at CBRE, told Financial Times that macroeconomic headwinds relating to the trade war between the US and China were also a significant factor in rising office vacancies.

As shown in the Bloomberg chart below, using CBRE data, Shanghai and Shenzhen had the highest office vacancies than any other city, and both had around 20% of office spaces dormant.

And with the global economy in a synchronized slowdown, global growth estimates are now printing at 3%, the slowest pace since the financial crisis. The Chinese economy will likely continue to slow, and could see domestic growth under 6% this year. This suggests that China’s office space vacancies will continue to rise through year-end.Office Vacancies In China Hit Decade High Amid Economic Turmoil

Chinese police searched the house of Zhang Qi, 57, the former mayor of Danzhou, and found a large amount of cash, as well as 13.5 tons of gold in ingots in a secret basement of his home, according tolocal media.

In addition to the mayoral post, Qi held others including Secretary of the Communist Party.

According to unofficial reports, in addition to the $625 million worth of gold, cash worth 268 billion yuan ($37 billion) was discovered[ZH: seems highs to us].

The video prompted some witty social media responses…

Luxurious real estate with a total area of several thousand square meters, which the former city manager had been reportedly hiding, was the icing on the cake in this massive haul for the Chinese Anti-Corruption Committee.

Qi was investigated by the Central Commission for Discipline Inspection (CCDI), the party’s internal disciplinary body, and the National Supervisory Commission, the highest anti-corruption agency of China, in September 2019.

According to China’s anti-corruption laws, Qi will be executed.

(Nathan Su) Newly discovered deep ties between the chief investment officer (CIO) of the California Public Employees Retirement System (CalPERS) and the Chinese government, along with CalPERS’s China investment holdings, have provoked controversy about the operations of the largest public retirement fund in the United States.

CalPERS manages more than $350 billion for public employees either retired from or currently working for most of the state and local public agencies in California.

The fund holds tens of millions of shares in equities of Chinese companies. Among other things, these companies develop advanced weapons for China’s People’s Liberation Army (PLA), and, according to one expert, are involved in unethical business practices and human rights abuses, including the concentration camps holding Uyghurs in Xinjiang.

According to a 2017 report by People’s Daily, the official mouthpiece of the Chinese Communist Party (CCP), CalPERS’s current CIO, Yu “Ben” Meng, as of 2015 was a participant in the Chinese government’s prestigious headhunting program called the Thousand Talents Plan (TTP).

We are told China’s economy is hurting, the “trade wars” are working and bringing China to it’s knees. From where I sit nothing could be further from the truth.

Currently China holds well north of $1 TRILLION in U.S. Treasuries – debt – that you and I, the tax payers of this country, send interest payments to month after month for them to continue holding our debt. It’s like the mortgage on your house, student loan or car note you have but instead of you getting anything for the debt payment you get to know the warmongers are going to purchase more bombs, weapons of all kinds and create more destruction. China, on the other hand, takes the payment and is building out the Belt and Road Initiative around the world. So, while we are working like slaves to pay our taxes, China is using our labor (taxes) paid to them to build a better global economic and financial system that does not include you and I. Pretty cool, aye?

While this is happening on one side of China’s national ledger sheet, on the other side something completely different is happening.

China reentered the gold market seven months ago, in December 2018 and has added a little less than 74 tons to their official gold holdings of approximately 1,935+ tons of gold. Please keep in mind this does not count the known 80-100 tons per annum that is flowing in from Russia. While this is not a large volume of gold in the grand scheme, this has been going on since 2016 so we are now talking about upwards of 240 – 300 additional tons. This changes their “official” gold holdings from approximately 1,935 tons to somewhere north of 2,175+. It could be as high as 2,235 or more tons of gold.

With more and more central banks continuing to add to their gold hoards did China see the pipeline tightening? China made their exit from the market in October 2016, the same month the yuan / renminbi was added to the IMF basket of currencies accounting for the SDR global trade note. Then fourteen months later decided to jump back in and have been adding to their horde ever since.

Last year, central banks bought 651.5 tons, 74% up on the previous year, theWorld Gold Councilsaid in January. Official sector purchases could reach 700 tons this year, assuming the China trend continues and Russia at least matches 2018 volumes of about 275 tons,Citigroup Inc.said in April. Buying from central banks in the first five months of this year is 73% higher than a year earlier, with Turkey and Kazakhstan joining China and Russia as the four biggest buyers, according to data released on Monday by the WGC.Source

If 2018 saw national / central banks acquiring more than they have since 1968 and this they are outpacing last year by 73% will this be the biggest year for gold national / central bank acquisitions in history? If not history it would have to be much earlier than 1968 since that record has already been breached.

With the global economic changes that are occurring we have been calling for some type of gold trade settlement for a number of years. We believe that Russia and China are on the cusp on making this change. We have no proof this going to happen this year or next, but all the signs are pointing in that direction. We believe, especially if China continues acquiring more “official” gold on the open market, there will be a gold trade settlement note announced before 2025. Possibly much sooner if the warmongers in Washington DC continue with the war drums over Iran. If President Trump listens to the war-pigs in the Pentagon this will not fare well for the U.S. economy and gold will be much in demand at all levels – from retail to government and everything in between.

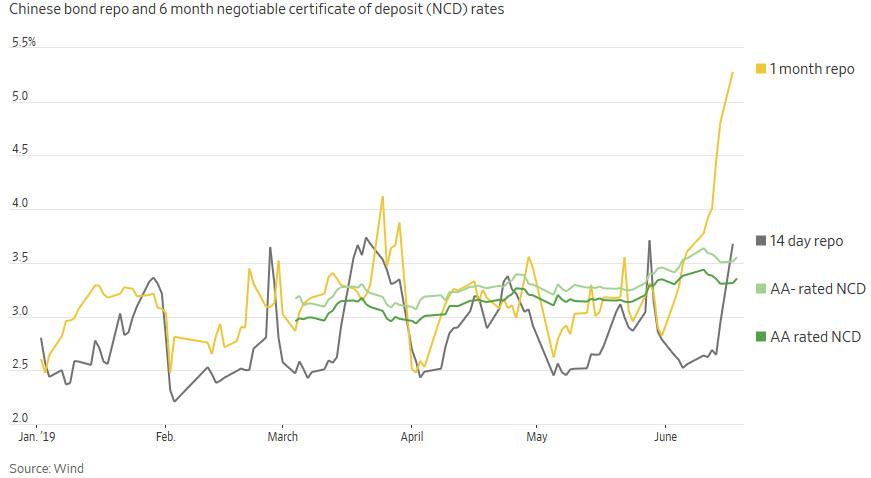

… China’s banking stress has taken a turn for the worse, and on Monday, China’s overnight repurchase rate dropped to its lowest level in nearly 10 years, after the central bank’s repeated liquidity injections to ease credit concerns in small-to-medium banks: The rate fell as much as 11 basis points to 0.9861% on Monday, before being fixed at exactly 1.000%.

Seeking to ease funding strains after the Baoshang collapse and to unfreeze the financial channels in the banking sector, the PBOC has been injecting cash into the financial system to soothe credit risk concerns in smaller banks following the seizure of Baoshang Bank, which sent shockwaves through China’s markets.

Also helping drive the rate lower is China’s move to allow brokerages to issue more debt, said ANZ Bank’s Zhaopeng Xing, quoted by Bloomberg. As a result, at least five brokerages had their short-term debt quotas increased by the People’s Bank of China in recent days, according to filings.

The improved access to shorter-term debt will cut costs for brokerages compared with alternative funding sources such as bond issuance. The flipside, of course, is that the lower overnight funding rates drop, the greater the investor skepticism that China’s massive, $40 trillion financial system is doing ok, especially since the last time overnight funding rates were this low, the near-collapse of the global financial system was still fresh and the S&P was trading in the triple-digits.

Commenting on the ongoing collapse in SHIBOR, Commodore Research wrote overnight that “low SHIBOR lending rates are supposed to be supportive and accommodative in nature — but rates are now at the lowest level seen this decade and are very likely an indication that China is facing significant banking stress at the moment. It is extremely rare for the overnight SHIBOR lending rate to be set as low as 1.00%. This previously had not all been seen this decade, and the last time it occurred was during the financial crisis in 2008 – 2009.”

Meanwhile, as the world’s biggest financial time bomb ticks ever louder, traders and analysts are blissfully oblivious, focusing instead on central banks admitting that the recession is imminent and trying to spin how a world war with Iran would be bullish for stocks.

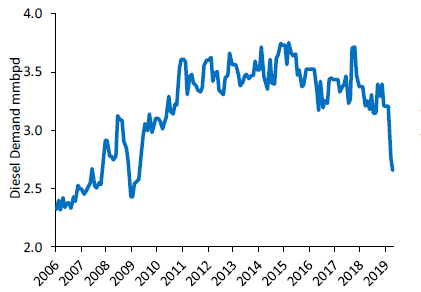

Diesel demand in China fell 14% and 19% in March and April respectively, reaching levels not seen in a decade, according to data compiled by Wells Fargo.

“We believe the accelerating decline is most likely tied to economic factors and the effects of the tariff ‘war’ with the U.S.,” Wells Fargo energy analyst Roger Read said in a note Monday. “If one wants to worry, that is where to focus most closely in our view.”

China said in April its economy grew by 6.4% in the first quarter of 2019. However, global investors and economists have been skeptical of China’s official economic figures for years as they believe they overstate how much China’s economy is growing.

China’s true pace of economic growth is always hard to decipher, but the country’s lagging diesel demand could be a sign that the world’s second-largest economy is in a much more dire state than official numbers indicate.

Diesel demand in China fell 14% and 19% in March and April, respectively, reaching levels not seen in a decade, according to data compiled by Wells Fargo. Monthly demand has also been falling every month since December 2017, the data shows.

Source: Wells Fargo Securities, Bloomberg

“We believe the accelerating decline is most likely tied to economic factors and the effects of the tariff ‘war’ with the U.S. (lifted demand earlier in 2019 to ‘beat’ the tariffs, but now falling),” Wells Fargo energy analyst Roger Read said in a note Monday. “If one wants to worry, that is where to focus most closely in our view.”

China said in April itseconomy grew by 6.4%in the first quarter of 2019. However, global investors and economists have been skeptical of China’s official economic figures for years as they believe they are overstated.

This skepticism has led analysts to use other ways to measure economic growth in China, including demand for diesel fuel and electricity. Diesel is largely used to fuel trucks that transport goods. Declining diesel demand is seen as signal of slowing economic growth as it could indicate fewer trucks are being used, hence fewer goods are being bought and sold.

China’s massive drop in diesel demand comes as it wages a trade war against the U.S.

Both countries have slapped tariffs on billions of dollars worth of their goods. Earlier this month, both countries hiked tariffs across their goods, leading to a ripple effect throughout financial markets.

Crude prices, for example, posted their worst weekly performance of 2019 last week and are down more than 7% this month. The S&P 500 is down more than 4% in May while the Shanghai Composite has lost 5.5%.

Neither side is showing signs of backing down, either. President Donald Trump said Monday the U.S. was not ready to make a deal with China. Meanwhile, a commentary in Chinese state-run newspaper Xinhua indicated China would not give into U.S. demands to change its state-run economy.

These tensions could shave off between 0.3% and 0.4% from China’s economic growth, according to UBS analyst Anna Ho. The analyst also said in a note: “Open economies, like Singapore, Korea and Malaysia are more sensitive to global trade and higher export exposure, and could see a reduced chance of growth recovery in 2H19.”

In another sign of tension between the two countries and perhaps declining economic activity, Chinese tourism to the U.S. fell for the first time in 15 years last year, according to the National Travel and Tourism Office.

The deepening trade war between the US and China has roiled complex global supply chains and America’s Heartland. The latest breakdown in negotiations comes at a time when soybean exports to China have crashed, and huge stockpiles are building, have resulted in many farmers teetering on the verge of bankruptcy. Mounting financial stress in the Midwest has allowed a public health crisis, where suicide rates among farmers have hit record highs, according to one trade organization’s interview with theSouth China Morning Post.

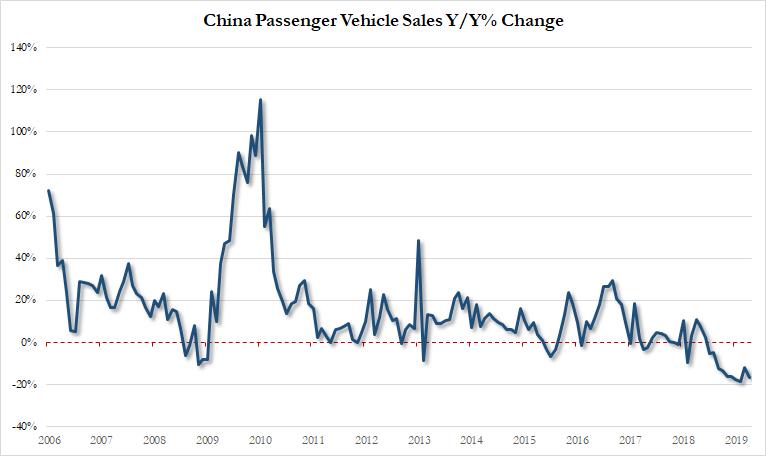

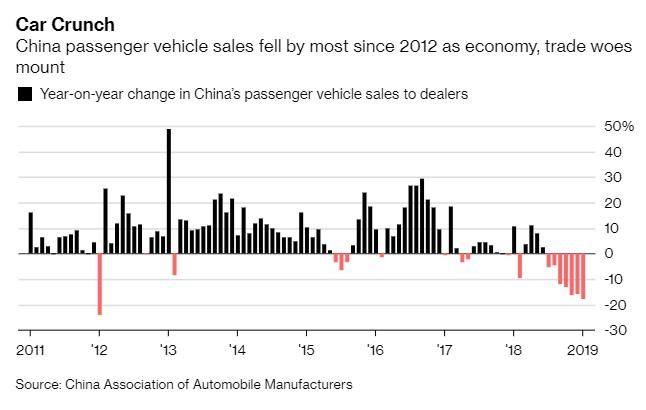

No country has better exemplified the global automobile recession than China. Sales for the world’s largest auto market continue to deteriorate, with the latest report confirming that passenger vehicle sales in China tanked yet again – this time dropping 16.6% year-over-year to 1.54 million units, following a 12% decline in March and an 18.5% slide in February. In addition, April SUV sales fell 14.7% to 642,220 units.

Those curious who is more impacted by the sudden re-escalation in trade hostilities between the US and China can get a quick answer by looking at the market reaction to Sunday’s unexpected news: while the S&P is down barely 1%, overnight Chinese stocks plunged nearly 6%, their biggest drop in over three years, indicating just how much more sensitive to every twist and turn in trade relations Chinese stocks are.

Of course, one can counter just how smaller – and far less relevant – the Chinese stock market is in comparison to the S&P500, which is also the basis for the vast majority of household net worth for Americans, and global investors (whereas in China, it is the local housing that is far more critical and accounts for roughly 70% of household net worth).

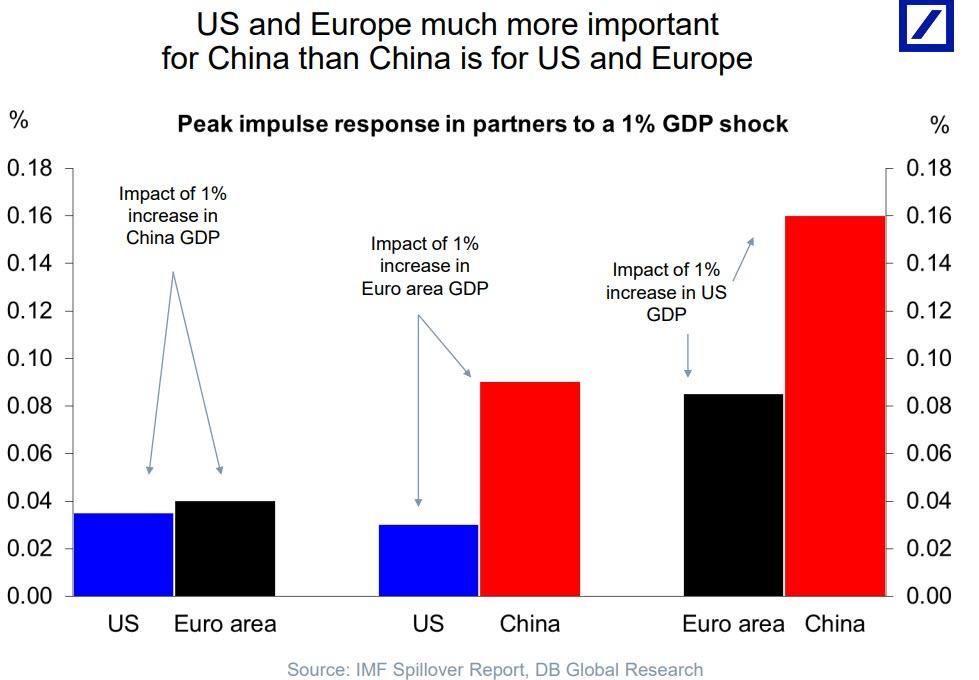

But it’s not just the stock market that shows why China should tread very lightly in its ongoing negotiations with Trump, or why the US president has decided suddenly to re-escalate. Below we lay out [ ] charts showing just why the US indeed continues to have the upper hand in negotiations with China, starting with the relative importance of the US and European economies to China rather than vice versa.

As the first chart below from Deutsche Bank shows, the US and Europe are “much more important for China than China is for US and Europe” as China remains the nation with the highest beta, or the highest relative impact, from a 1% move in either direction for either the US or the Euro area.

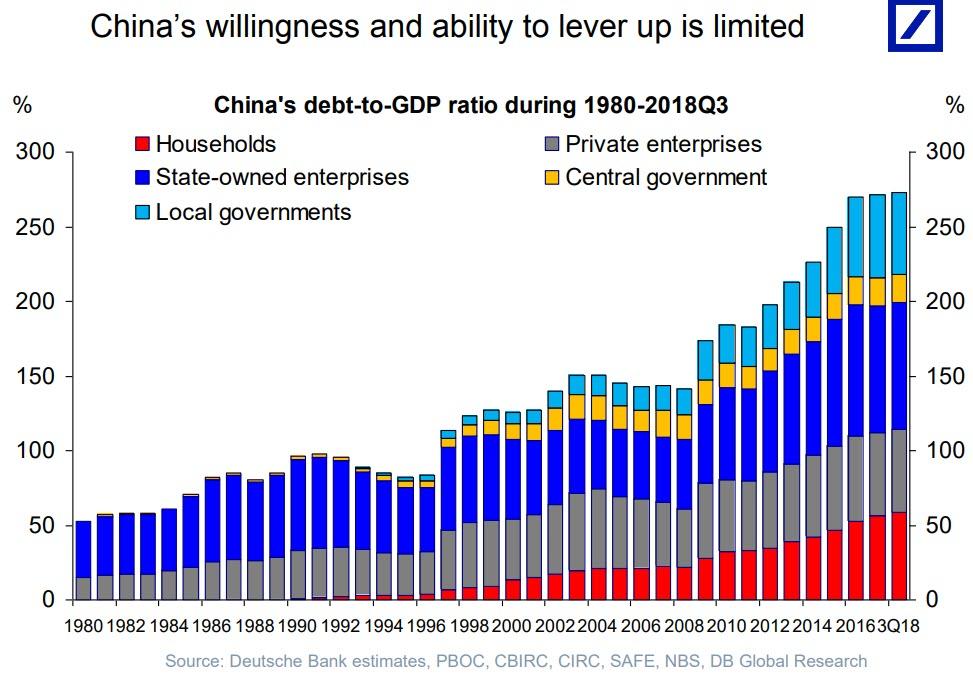

Second, whereas the US is now actively contemplating the launch of MMT, and exploding the US twin deficit by issuing virtually unlimited amounts of debt – which it ostensibly can do as long as the US Dollar is the world’s reserve currency – China is already near its leverage peak. In fact, as shown in the chart below, both China’s willingness and ability to lever up is now quite limited according to Deutsche Bank’s Torsten Slok.

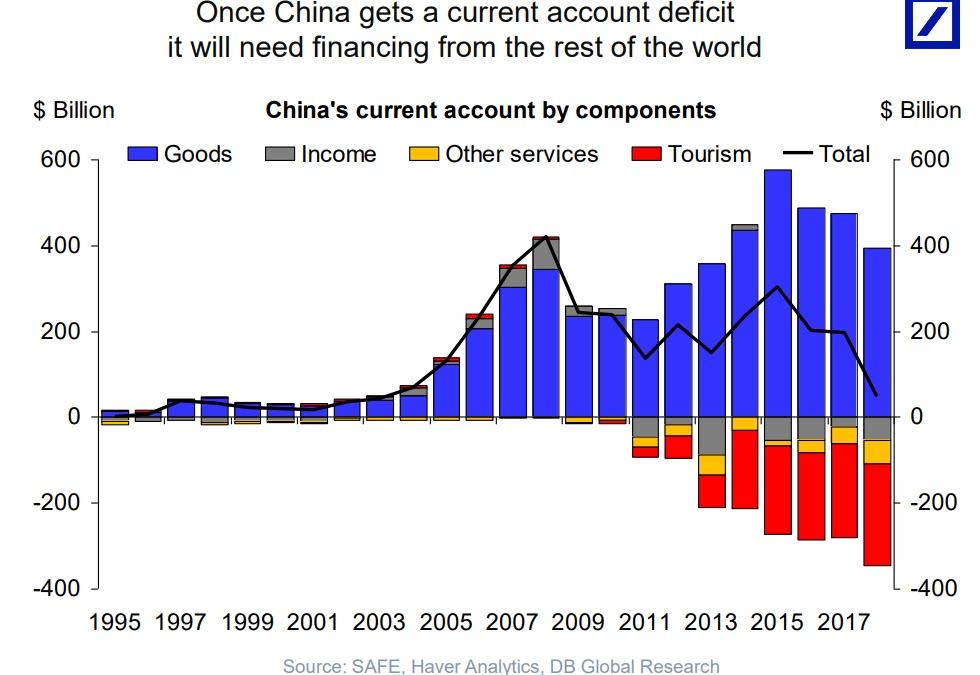

Last, and certainly not least, is what we saidback in January representeda “tectonic shift” in China’s economy, when we observed that this year, for the first time in history, China’s current account deficit will turn negative meaning that China will henceforth need financing from the rest of the world, and specifically the US. Which is why, as we said five months ago, it is not Beijing that has leverage over the US, but rather the US whose ability – and desire – to allocate capital to China could mean all the difference for China’s economic growth, or lack thereof.

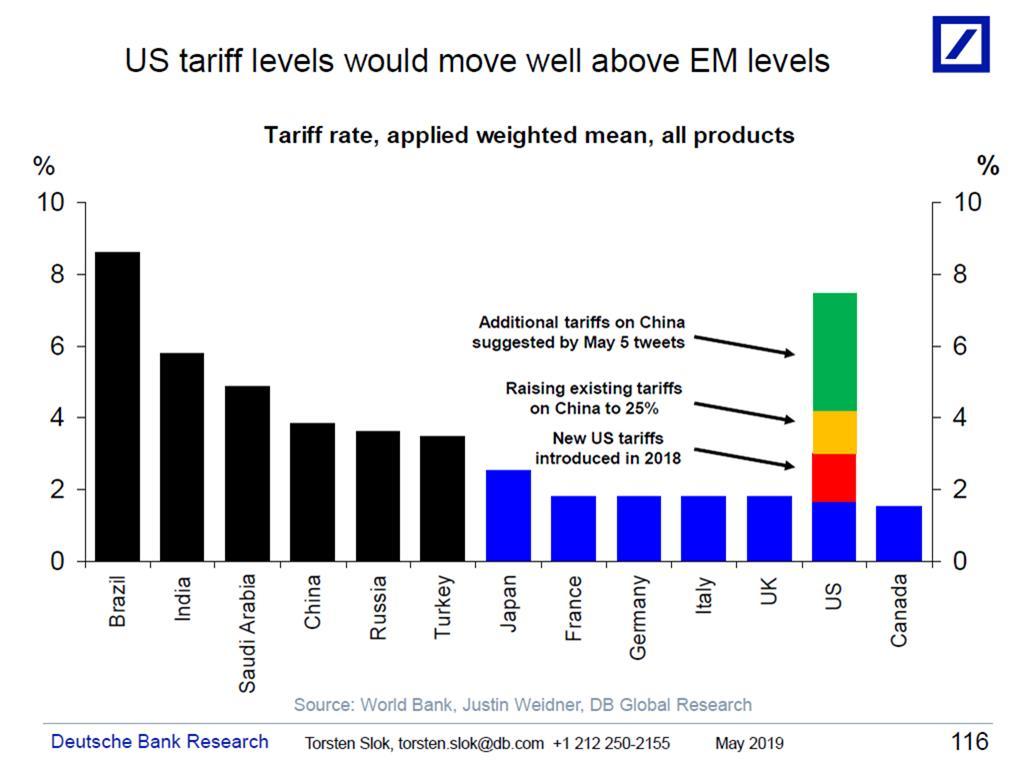

Finally, and tangentially, assuming trade talks collapse and Trump follows through on his threat of hiking taxes on Chinese imports, it would, as Torsten Slok shows in his latest chart, push US tariffs – which are already higher than most advanced economies – higher than many emerging market countries making the US one of the leading protectionist countries in the work.

That alone would cripple China’s economy, and is perhaps the main reason why Trump decided to once again flex his muscles, if so far only on twitter.

Back in 2017, ZeroHedge explained why the “fate of the world economy is in the hands of China’s housing bubble.” The answer was simple: for the Chinese population, and growing middle class to keep spending vibrant and borrowing elevated, it had to feel comfortable and confident that its wealth would keep rising. However, unlike the US where the stock market is the ultimate barometer of the confidence boosting “wealth effect”, in China it has always been about housing asthree quarters of Chinese household assetsare parked in real estate, compared to only 28% in the US, with the remainder invested in financial assets.

Beijing knows this, of course, which is why China periodically and consistently reflates its housing bubble any time it feels the broader economy is slowing, hoping that any subsequent popping of the bubble, which happened in late 2011 and again in 2014, will be a controlled, “smooth landing” process. For now, Beijing has been successful in maintaining price stability at least according to official data, allowing the air out of the “Tier 1” home price bubble which peaked in early 2016, while preserving modest home price appreciation in secondary markets.

How long China will be able to avoid a sharp price decline remains to be seen, but in the meantime another problem faces China’s housing market: in addition to being the primary source of household net worth – and therefore stable and growing consumption – it has also been a key driver behind China’s economic growth, with infrastructure spending and capital investment long among the biggest components of the country’s goalseeked GDP. One result has been China’s infamous ghost cities, built only for the sake of Keynesian spending to hit a predetermined GDP number that would make Beijing happy.

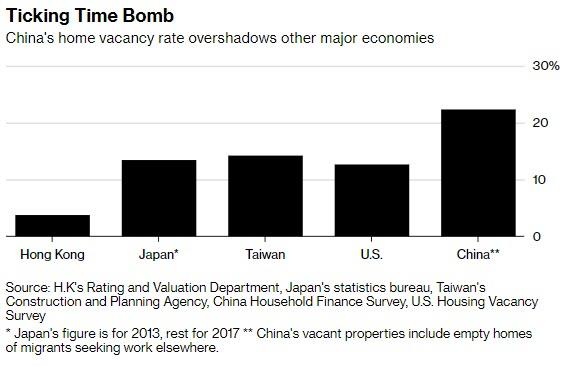

Meanwhile, in the process of reflating the latest housing bubble, another dangerous byproduct of this artificial housing “market” has emerged: tens of millions of apartments and houses standing empty across the country. As wereported recently, according to recent research, roughly 22% of China’s urban housing stock is unoccupied, according to Professor Gan Li, who runs the main nationwide study. That amounts to more than 50 million empty homes.

The reason for the massive empty inventory glut: to keep supply low and prices artificially elevated by taking out as much inventory off the market as possible. This, however, works both ways, and while it helps boost prices on the way up as the economy grow and speculators flood the housing market with easy money, the moment the trend flips the spike in supply as empty units are offloaded will lead to a panic liquidation of homes, resulting in what may be the biggest housing market crash ever observed, and putting the US home bubble of 2006 to shame.

Indeed, as Bloomberg noted, the “nightmare scenario” for Chinese authorities is that owners of unoccupied dwellings rush to sell when cracks start appearing in the property market, causing a self-reinforcing downward price spiral.

Which is why preserving the narrative (or rather myth) of constantly rising prices is so critical for China: any cracks in the facade of the price appreciation story could have a dire consequence first for the housing market, and then, the broader economy whose growth is already the slowest in modern Chinese history, as any scramble to liquidate inventory could promptly result in a bidless market as the tens of millions of empty units are suddenly exposed for both buyers and sellers to see.

* * *

While the key role of China’s housing market in the country’s economy, and thus the world’s, has long been known, a recent troubling development is that despite what Beijing deems stable home prices, the foundations behind the housing market are starting to crack. As theWSJ recently reported, in early December, a group of homeowners stormed the sales office of their Shanghai complex, “Central Washington”, whose developer, Shanghai Zhaoping Real Estate Development, was advertising new apartments at a fraction of the prices of the ones sold earlier in the year. One apartment owner said the new prices suggested the value of the apartment she bought from the developer in March had dropped by about 17.5%.

“There are people who bought multiple homes who are now trying to sell one to pay off the mortgage on another,” said Ran Yunjie, a property agent. One of his clients bought an apartment last year for about $230,000. To find a buyer now, the client would have to drop the price by 60%, according to Ran.

Meanwhile, in a truly concerning demonstration of what will happen when the bubble finally bursts, in October we reported that angry homeowners who paid full price for units at the Xinzhou Mansion residential project in Shangrao attacked the Country Garden sales office in eastern Jiangxi province last week, after finding out it had offered discounts to new buyers of up to 30%.

Country Garden cut the selling price at one of its residential developments by 1/3. Those who paid full price smashed the sales office. Similar incidents had happened before, and will again. It’s impossible to remove “the guarantee of principal”(刚性兑付)in China. pic.twitter.com/UxHFODYxmc

“Property accounts for roughly 70 per cent of urban Chinese families’ total assets – a home is both wealth and status. People don’t want prices to increase too fast, but they don’t want them to fall too quickly either,” said Shao Yu, chief economist at Oriental Securities. “People are so used to rising prices that it never occurred to them that they can fall too. We shouldn’t add to this illusion,”Shao added, echoing Ben Bernankecirca 2005.

The bottom line is that just like true price discovery for US capital markets is prohibited (and sees Fed intervention any time there is an even modest, 10-20% drop in asset prices) or else the risk of an all out panic is all too real, in China true price discovery is also not permitted, however when it comes to the country’s all important, and wealth effect boosting, real estate.

Which is a problem, because whereas China suddenly appears to be suffering from all the conventional signs of deflation in the auto retail sector, where as wenoted previously, neither lower prices nor easier loans have managed to put a dent the ongoing demand plunge…

… the same ominous price cuts – which are clearly meant to boost flagging demand – are starting to emerge in China’s housing sector.

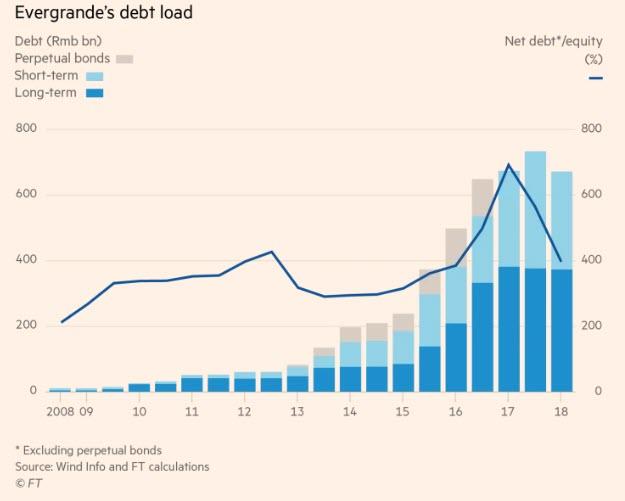

Case in point, according toChina’s Paper, Hui Ka Yan, the Chairman of Evergrande, China’s biggest property developer, and China’s second richest person announced it must ramp up home sales and to do that it would sell all its properties at a 10% discount after its home sales tumbled in January amid a cooling market.

Evergrande Chairman Hui Ka Yam

The fact that Evergrande has had financial difficulties for the past year is not new. In November, Evergrande, which carries the industry’s largest debt pile of any Chinese housing developer, was caught in a vicious funding squeeze and raised eyebrows with a $1.8BN, 5-year bond deal, which it had to pay a whopping 13.75% coupon, prompting analysts to say the move “carried a whiff of desperation.” The fact that chairman Hui Ka Yan, China’s second-richest person, bought $1bn of it himself, added to a sense that outside investors were shunning the company.

In many ways, Evergrande had no choice: after the property market boomed for the past three years, helping to power the economy through Xi Jinping’s crucial political transition year of 2017, in 2018 the market slowed sharply, after local governments shifted focus to controlling frothy prices and China Development Bank, the policy lender, phased out a $1 trillion subsidy program for homebuyers in smaller cities, where Evergrande’s projects are concentrated, theFT reported.

Even the official China News Service, usually a cheerleader for the economy, acknowledged recently that the property market “was a bit chilly”. Nomura chief China economist Ting Lu put it more starkly, forecasting a “frigid winter”.

The bigger problem for Evergrande, which had $208 billion in total liabilities at the end of June 2018 — the most of any Chinese developer — including $43bn maturing in 2019, is that should China’s housing market suffer a steep downturn, it will likely be the company to suffer the most, if for no other reason than its massive leverage which stood at a net debt to equity ratio of 400%.

Commenting on the bond sale, a high-yield debt underwriter at a western bank in Hong Kongtold the FTthat “Evergrande is very levered, so, yes, they do need cash,” said “That said, they are not a name we see as having a near-term liquidity crisis. That cannot be said about other smaller players.”

That was in November; and while there are no signs that the funding situation at Evergrande has deteriorated sharply since then – especially since the company is widely seen as systematically important and Beijing would never let it fail (although the same was said about Kaisa, another Chinese property developer that did default not too long ago), it now appears that the company has decided to start liquidating properties in an unexpected scramble to either gain market share, or to obtain much needed funding.

In any case, the fact that China’ largest property developer is now slashing prices across the board by as much as 10%, means that a deflationary hurricane is about to blow across what most see as the most important sector in China’s economy, and worse, should other property developers follow in slashing prices launching a race to the bottom, nobody knows how far prices could truly fall should a liquidation domino effect ensue.

What is most troubling however, is that as recently as November, the property slowdown was seen to be in large part due to efforts by city governments to restrain runaway price increases, which has included draconian interventions such as price controls and sales bans.

However, now that Evergrande is rushing to slash prices, it appears that runaway home prices are no longer a concern for Beijing, and in fact, a far greater concern is how Beijing may intervene to prevent what could soon be a price plunge spiral; many have already speculated that Beijing will have no choice but to bar Evergrande’s sales. If it doesn’t, or if homeowners have already figured out that their home prices are floating in the sky on a bubbly foundation that has now burst, the knock on effect could be devastating as instead of an asset, China’s most popular and aspirational “wealth effect” product could turn into a liability overnight.

If that happens, no amount of intervention by Beijing could stop the avalanche of selling that would ensue, not to mention the deflationary shock wave that a hard landing – i.e. crash – in China’s housing market would launch across the entire world…

Shock video shows staffers suffering cruel punishment

Workers from a Chinese beauty products company have been forced to crawl on the street after failing to reach their annual targets.

The staff were on all fours as they made their way through busy traffic in the Chinese city of Tengzhou, according to local reports.

Pedestrians of the city in eastern China were shocked by the scene as they stopped to watch as the employees moving forward on their hands and knees, videos show.

Warren Buffett has famously told Berkshire Hathaway investors: “You only find out who is swimming naked when the tide goes out.”

Buffett’s market wisdom can be applied to the Chinese property market.

Now, the tide is going out and the boom days are over, the industry israpidly slowing as credit growthis the slowest on record – pointing to a weakening in the economy in coming months.

As for “swimming naked when the tide goes out,” well, it seems like one real estate firm, in southwest China used topless models covered in body paint as a last-ditch effort to unload a new property development before the market implodes.

Nanning Weirun Investment Company, a real estate developer in Nanning, capital of the southwestern Guangxi Zhuang, hired a bunch of models to advertise its condominiums by using their bare skin as a canvas, saidAsia Times.

Floor plans of the condos were painted on the back of each model, and their breasts were painted with logos and other advertising slogans.

While it is unclear if the topless models helped to spur sales, Asia Times indicated that the stunt attracted many people to the showroom last Friday.

Hundreds of Sina Weibo users, China’s Twitter, criticized the promotion and called it disgusting, as others thought it was an interesting method, in the attempt to generate sales in a slowing market.

An employee at Nanning Weirun told the website Btime.com that the bodypainting promotion was a one-off event to drive sales.

The strategy is one of the more unconventional approaches being taken by desperate developers to attract new buyers as GDP growth, and the housing market are expected to fall in the first half of 2019.

Was the marketing stunt worth it for the developer?

Probably not, as the city planning authority suspended the firm’s marketing permit on Monday.

Video: Revealing the naked truth of China’s real estate slowdown

Back in 2017, we explained why the “fate of the world economy is in the hands of China’s housing bubble.” The answer was simple: for the Chinese population, and growing middle class, to keep spending vibrant and borrowing elevated, it had to feel comfortable and confident that its wealth would keep rising. However, unlike the US where the stock market is the ultimate barometer of the confidence boosting “wealth effect”, in China it has always been about housing asthree quarters of Chinese household assetsare parked in real estate, compared to only 28% in the US, with the remainder invested financial assets.

Beijing knows this, of course, which is why China periodically and consistently reflates its housing bubble, hoping that the popping of the bubble, which happened in late 2011 and again in 2014, will be a controlled, “smooth landing” process. For now, Beijing has been successful in maintaining price stability at least according to official data, allowing the air out of the “Tier 1” home price bubble which peaked in early 2016, while preserving modest home price appreciation in secondary markets.

How long China will be able to avoid a sharp price decline remains to be seen, but in the meantime another problem faces China’s housing market: in addition to being the primary source of household net worth – and therefore stable and growing consumption – it has also been a key driver behind China’s economic growth, with infrastructure spending and capital investment long among the biggest components of the country’s goal seeked GDP. One result has been China’s infamous ghost cities, built only for the sake of Keynesian spending to hit a predetermined GDP number that would make Beijing happy.

Meanwhile, in the process of reflating the latest housing bubble, another dire byproduct of this artificial housing “market” has emerged: tens of millions of apartments and houses standing empty across the country.

According toBloomberg, soon-to-be-published research will show that roughly 22% of China’s urban housing stock is unoccupied, according to Professor Gan Li, who runs the main nationwide study. That amounts to more than 50 million empty homes.

The reason for the massive empty inventory glut: to keep supply low and prices artificially elevated by taking out as much inventory off the market as possible. This, however, works both ways, and while it helps boost prices on the way up as the economy grow and speculators flood the housing market with easy money, the moment the trend flips the spike in supply as empty units are offloaded will lead to a panic liquidation of homes, resulting in what may be the biggest housing market crash ever observed, and putting the US home bubble of 2006 to shame.

Indeed, as Bloomberg notes, the “nightmare scenario” for Chinese authorities is that owners of unoccupied dwellings rush to sell when cracks start appearing in the property market, causing a self-reinforcing downward price spiral.

Worse, the latest data, from a survey in 2017, also suggests Beijing’s efforts to curb property speculation – which alongside shadow banking and the persistent threat of sudden bank runs (like theone discussed last week) is considered by Beijing a key threat to financial and social stability – have failed.

“There’s no other single country with such a high vacancy rate,” said Gan, of Chengdu’s Southwestern University of Finance and Economics. “Should any crack emerge in the property market, the homes to be offloaded will hit China like a flood.”

How did the Chinese researcher obtain this troubling number? To find the percentage of vacant housing, thousands of researchers spread out across 363 Chinese counties last year as part of the China Household Finance Survey, which Gan runs at the university.

Gan said that the vacancy rate, which excludes homes yet to be sold by developers, was little changed from a 2013 reading of 22.4%. And while that study showed 49 million vacant homes, Gan puts the number now at “definitely more than 50 million units.“

Meanwhile, Beijing – which is fully aware of these stats, and is also aware that even a modest price decline could be magnified instantly as millions of “for sale” units hit the market at the same time – is worried. That’s why Chinese authorities have imposed buying restrictions and limited credit availability, only to see money flooding into other areas. Rampant price gains also mean millions of people are shut out from the market, exacerbating inequality.

In fact, China’s president Xi famously said in October last year that “houses are built to be inhabited, not for speculation”, and yet a quarter of China’s housing is just that: empty, and only serves to amplify speculation.

While holiday homes and the empty dwellings of migrants seeking work elsewhere account for some of the deserted properties, Gan found that investment purchases have been the biggest factor keeping the vacancy rate high. That’s despite curbs across the country meant to discourage buying of multiple dwellings.

There is another economic cost to this speculative frenzy: the drop in supply puts upward pressure on prices and crowds young buyers out of the market, according to Kaiji Chen, who co-authored a Fed paper called “The Great Housing Boom of China.”

And, as Americans so fondly recall, the result of chasing unaffordable homes for the purpose of price speculation has resulted in yet another unprecedented debt bubble: according to Caixin, outstanding personal home mortgages in China have exploded seven fold from 3 trillion yuan ($430 billion) in 2008 to 22.9 trillion yuan in 2017, according to PBOC data

By the end of September, the value of outstanding home mortgages had surged another 18% Y/Y to a record 24.9 trillion yuan, resulting in a trend that as Caixin notes, has turned many people into what are called “mortgage slaves.”

It has also resulted in yet another housing bubble: home mortgage debt now makes up more than half of total household debt in China. As of the third quarter, it accounted for 53% of the 46.2 trillion yuan in outstanding household debt.

For now, few are losing sleep over what will be the next massive housing bubble to burst. An example of a vacant home is a villa on the outskirts of Shanghai that 27-year-old Natalie Feng’s parents bought for her. The two-story residence was meant to be a weekend escape for the family of three. In reality, it’s empty most of the time, and Feng says it’s too much trouble to rent it out.

“For every weekend we spend there, we need to drive for an hour first, and clean up for half a day,” Feng said. She joked that she sometimes wishes her parents hadn’t bought it for her in the first place. That’s because any apartment she buys now would count as a second home, which means she’d have to make a bigger down payment.

* * *

What is troubling is that despite relatively stable home prices, the foundations behind the housing market are cracking. As the WSJ recently reported, in early December, a group of homeowners stormed the sales office of their Shanghai complex, “Central Washington”, whose developer, Shanghai Zhaoping Real Estate Development, was advertising new apartments at a fraction of the prices of the ones sold earlier in the year. One apartment owner said the new prices suggested the value of the apartment she bought from the developer in March had dropped by about 17.5%.

“There are people who bought multiple homes who are now trying to sell one to pay off the mortgage on another,” said Ran Yunjie, a property agent. One of his clients bought an apartment last year for about $230,000. To find a buyer now, the client would have to drop the price by 60%, according to Ran.

Meanwhile, in a truly concerning demonstration of what will happen when the bubble finally bursts, last month we reported that angry homeowners who paid full price for units at the Xinzhou Mansion residential project in Shangrao attacked the Country Garden sales office in eastern Jiangxi province last week, after finding out it had offered discounts to new buyers of up to 30%.

Country Garden cut the selling price at one of its residential developments by 1/3. Those who paid full price smashed the sales office. Similar incidents had happened before, and will again. It’s impossible to remove “the guarantee of principal”(刚性兑付)in China. pic.twitter.com/UxHFODYxmc

“Property accounts for roughly 70 per cent of urban Chinese families’ total assets – a home is both wealth and status. People don’t want prices to increase too fast, but they don’t want them to fall too quickly either,” said Shao Yu, chief economist at Oriental Securities. “People are so used to rising prices that it never occurred to them that they can fall too. We shouldn’t add to this illusion,”Shao added, echoing Ben Bernankecirca 2005.

But the biggest surprise once the music finally stops may be that – as a fascinatingWSJ reportrevealed one year ago – China’s housing downturn is likely far, far worse than meets the eye, as under Beijing’s direction more than 200 cities across China for the last three years have been buying surplus apartments from property developers and moving in families from condemned city blocks and nearby villages. China’s Housing Ministry, which is behind the purchases, said it plans to continue the program through 2020. The strategy, supported by central-government bank lending, has rescued housing developers and lifted the property market.

In other words, while China already has a record 50 million empty apartments, the real number – when excluding the government’s own stealthy purchases of excess inventory – is likely significantly higher. It is this, and not China’s stock market, that has long been the biggest time bomb for Beijing, and if Trump and Peter Navarro truly want to crush China in their ongoing trade war, they should focus on destabilizing the housing market: the Chinese stock market was, and remains just a distraction.

To summarize:

China has more than 50 million vacant apartments

Mortgage loans have grown 8-fold in the past decade

Prices are kept steady thanks to constant government purchases of surplus inventory

Home prices are already cracking, with some homebuilders forced to cut prices by 30%.

Homebuyers revolt, forming angry militias and storm homesellers’ offices when prices dip

For now, China has been able to maintain the illusion of stability to preserve social order. However, should the housing slowdown accelerate significantly and tens of millions in empty units suddenly hit the market, then the “working class insurrection” that China has been preparing for since 2014…

… will become an overnight reality, with dire consequences for the entire world.

…When you plant your trees in another man’s orchard, don’t be surprised when you pay for your own apples…

President Trump has instructed U.S. Trade Representative Robert Lighthizer to execute Round Two of tariffs on Chinese imports. The first round applied to $50 billion in products. The current round applies a 10% tariff to $200 billion (effective Sept. 24, 2018), until January 1st, 2019, when the tariff increases to 25%.

Thelist of productsis particularly focused, and happily we note it includes almost all Chinese processed food imports.

Chinese food processing is sketchy, and China has refused to comply with most international food safety programs. However, President Trump spared smart watches from Apple and Fitbit and other consumer products such as bicycle helmets and baby car seats.

In a statement announcing the Round-Two tariffs, President Trump warned China if they take retaliatory action against U.S. farmers or industries, “we will immediately pursue phase three, which is tariffs on approximately $267 billion of additional imports.” That would hit Apple and all consumer good imports. Here’s the announcement and the list of products:

Washington, DC– As part of the United States’ continuing response to China’s theft of American intellectual property and forced transfer of American technology, the Office of the United States Trade Representative (USTR) today released a list of approximately $200 billion worth of Chinese imports that will be subject to additional tariffs.

In accordance with the direction of President Trump, the additional tariffs will be effective starting September 24, 2018, and initially will be in the amount of 10 percent. Starting January 1, 2019, the level of the additional tariffs will increase to 25 percent.

The list contains 5,745 full or partial lines of the original 6,031 tariff lines that were on a proposed list of Chinese imports announced on July 10, 2018.

[…] In March 2018, USTR released the findings of its exhaustiveSection 301 investigationthat found China’s acts, policies and practices related to technology transfer, intellectual property and innovation are unreasonable and discriminatory and burden or restrict U.S. commerce.

Specifically, the Section 301 investigation revealed:

China uses joint venture requirements, foreign investment restrictions, and administrative review and licensing processes to require or pressure technology transfer from U.S. companies.

China deprives U.S. companies of the ability to set market-based terms in licensing and other technology-related negotiations.

China directs and unfairly facilitates the systematic investment in, and acquisition of, U.S. companies and assets to generate large-scale technology transfer.

China conducts and supports cyber intrusions into U.S. commercial computer networks to gain unauthorized access to commercially valuable business information.

After separate notice and comment proceedings, in June and August USTR released two lists of Chinese imports, with a combined annual trade value of approximately $50 billion, with the goal of obtaining the elimination of China’s harmful acts, policies and practices.

Unfortunately, China has been unwilling to change its policies involving the unfair acquisition of U.S. technology and intellectual property. Instead, China responded to the United States’ tariff action by taking further steps to harm U.S. workers and businesses. In these circumstances, the President has directed the U.S. Trade Representative to increase the level of trade covered by the additional duties in order to obtain elimination of China’s unfair policies. The Administration will continue to encourage China to allow for fair trade with the United States.

A formal notice of the $200 billion tariff action will be published shortly in the Federal Register. (read more)

A PDF list of the Round #2 impacted products isAvailable HERE.

As expected, Beijing did not waste much time responding to Trump’s latest tariffs, and moments ago China issued a statement disclosing what its planned retaliation would look like.

Chinese leaders know that their country suffers from massive over-investment in construction and manufacturing, that its real-estate market is a bubble that makes the Dutch tulip frenzy look restrained, that both conventional debt and debt in the shadow-banking system are too large and growing too rapidly.

But even as the Communist Party centralizes power and clamps down on dissent, it dithers when it comes to the costly and difficult work of shifting China’s economic development onto a sustainable track.

Chinese authorities have tried to tackle some of these problems, but often retreat when reforms start to bite and powerful interests push back.

China is the 800-pound gorilla of global infrastructure. Its building prowess has permeated popular culture, as in the disaster movie “2012” where China constructs giant ships to help humankind escape rising seas.

Recently, however, China’s infrastructure build has all but ground to a halt.

Here’s why…

The central government last year started to crack down on unregulated, opaque – so-called ‘shadow-bank’ borrowing – alarmed at its vast scale, and potential for corruption.

For five straight months, the shadow banking system has contracted under this pressure, sucking the malinvestment lifeblood out of economic growth and construction booms as Chinese local governments, which account for the bulk of such investment, set up as so-called local-government financing vehicles (off balance sheet), or LGFVs, and have seen an unprecedented net $19 billion outflow in recent months.

As WSJ’s Talpin notes,these days Beijing prefers that local governments borrow on-the-books, through the now legal municipal bond market. The problem is that lower-rated and smaller cities are mostly shut out, even though they do most actual capital spending. As a result, investment has kept slowing even though China’s net muni bond issuance in July was three times higher than it was in March. Infrastructure investment excluding power and heat was up just 5.7% in the first seven months of 2018 compared with a year earlier, down from 19% growth in 2017.

Eventually, all the cash big cities and provinces are raising through muni bonds will start filtering down. Meanwhile, the investment drought will likely worsen, raising pressure on Beijing to ease credit conditions further – making the incipient rally in the yuan hard to sustain.

That also means China’s debt-to-GDP ratio, which fell marginally in 2017, could start rising again next year.

Simply put, as with water and wine, China’s leaders haven’t figured out how to crack down on local governments’ dubious infrastructure spending during good times without severely damaging growth – or how to loosen the reins during bad times without creating lots more bad debt.

Unless they can square that circle, it bodes ill for the nation’s long-term prospects.

When you plant your tree in another man’s orchard, you might end up paying for your own apples; it’s a risk you take…

….and President Trump knows how to use that leverage better than anyone could possibly fathom; because in this metaphor Beijing relies upon the U.S. for both the seeds and the harvest. President Trump drops the $200b M.O.A.T (Mother of All Tariffs):

White House – On Friday, I announced plans for tariffs on $50 billion worth of imports from China. These tariffs are being imposed to encourage China to change the unfair practices identified in the Section 301 action with respect to technology and innovation. They also serve as an initial step toward bringing balance to our trade relationship with China.