(Bruce Wilds) Unnoticed by most taxpayers and touted as good news was the fact we the taxpayers of America have stepped up to the plate and bailed out hundreds of failing pensions. Much of this took place without the average citizen even knowing it occurred.

Tag Archives: Retirement

185 Union Pensions Got Their $86 Billion Piece Of The COVID-19 Rescue “Pie”

(Birch Gold) Both private and public pensions have been having major funding issues and struggling to get a good ROI for a number of years.

So it’s no surprise that any sort of economic relief package presented to Congress would include funds for pensions. Especially since a “bailout” culture seems to have taken root in America.

Where pension debt is a looming danger to taxpayers, via Texas Public Policy Foundation

‘Too Big To Sell’ – Boomers Trapped In McMansions As Retirement Looms

More wealthy baby boomers are finding themselves trapped in homes that are too big to sell. They want to downsize but can’t get what they paid.

This was guaranteed to happen, and did. Baby boomers and retirees built large, elaborate dream homes only to find that few people want to buy them.

Please consider a Growing Problem in Real Estate: Too Many Too Big Houses.

Large, high-end homes across the Sunbelt are sitting on the market, enduring deep price cuts to sell.

That is a far different picture than 15 years ago, when retirees were rushing to build elaborate, five or six-bedroom houses in warm climates, fueled in part by the easy credit of the real estate boom. Many baby boomers poured millions into these spacious homes, planning to live out their golden years in houses with all the bells and whistles.

Now, many boomers are discovering that these large, high-maintenance houses no longer fit their needs as they grow older, but younger people aren’t buying them.

Tastes—and access to credit—have shifted dramatically since the early 2000s. These days, buyers of all ages eschew the large, ornate houses built in those years in favor of smaller, more-modern looking alternatives, and prefer walkable areas to living miles from retail.

The problem is especially acute in areas with large clusters of retirees. In North Carolina’s Buncombe County, which draws retirees with its mild climate and Blue Ridge Mountain scenery, there are 34 homes priced over $2 million on the market, but only 16 sold in that price range in the past year, said Marilyn Wright, an agent at Premier Sotheby’s International Realty in Asheville.

The area around Scottsdale, Ariz., also popular with wealthy retirees, had 349 homes on the market at or above $3 million as of February 1—an all-time high, according to a Walt Danley Realty report. Homes built before 2012 are selling at steep discounts—sometimes almost 50%, and many owners end up selling for less than they paid to build their homes, said Walt Danley’s Dub Dellis.

Kiawah Island, a South Carolina beach community, currently has around 225 houses for sale, which amounts to a three- or four-year supply. Of those, the larger and more expensive homes are the hardest to sell, especially if they haven’t been renovated recently, according to local real-estate agent Pam Harrington.

The problem is expected to worsen in the 2020s, as more baby boomers across the country advance into their 70s and 80s, the age group where people typically exit homeownership due to poor health or death, said Dowell Myers, co-author of a 2018 Fannie Mae report, “The Coming Exodus of Older Homeowners.” Boomers currently own 32 million homes and account for two out of five homeowners in the country.

Not Just the South

It’s not just big houses across the Sunbelt. It’s big houses everywhere. If anything, I suspect it’s worse in the north. There is an exodus of people in high tax states like Illinois who want the hell out.

Already big homes were hard to sell. Now these progressive states are raising taxes.

Triple Whammy

- Millennials trapped in debt and cannot afford them

- Millennials wouldn’t buy them anyway because tastes have changed.

- Taxes are driving people away from states like Illinois

Good luck with that.

For the plight of Illinoisans, please consider Illinois’ Demographic Collapse: Get Out As Soon As You Can.

California Faces Pension Showdown

Governor Jerry Brown, as he leaves office is warning that California and its public agencies are on the road to “fiscal oblivion” if pension benefits can’t be adjusted down.

The media have been celebrating Governor Brown’s management skills at reversing the $27-billion state deficit he inherited from in 2010 from his predecessor, Arnold Schwarzenegger, to leave office in January with an alleged $13.8-billion surplus and a $14.5-billion rainy-day fund balance.

But Brown recently told reporters that California will be financially distressed again if the California Supreme Court rules in a case titled Cal Fire Local 2881 v. California Public Employees’ Retirement System against Brown’s 2012 California’s Public Employees’ Pension Reform Act that stopped the state and local selling of “airtime” that allowed public employees to spike their pension benefits by purchasing up to five years of un-worked service credit seniority.

California drastically increased public employee pension benefits in the fall of 2003, when the state allowed employees to purchase “airtime.” Prior to the pension spike, a 50-year-old fireman making $89,000 a year could retire at age 50 after 30 years of service and collect an $80,100-a-year pension with life expectancy of 76.3 years.

But under “airtime,” the fireman could purchase extra years of seniority at a cost per of $0.18022 per year for every $1 of salary. For $80,197.90, the fireman could increase his pension by $13,350 to $93,450. Such an investment in “airtime” would return a spectacular income stream of $351,105 over the next 26.3 years of life expectancy.

With many California public employees purchasing “airtime” to retire at 50 and make more than when employed, Democrat Brown ended the practice in 2013 for new hires after criticism that the practice amounted to a “gift of public funds” to his union allies.

Stanford University’s Institute for Economic Policy Research found that despite the state terminating “airtime” for new employees in 2013, the annual cost of funding the California Public Employee Retirement System (CalPERS) rose by 400 percent from 2003 to 2018 and would be up by 704 percent by 2030.

With an estimated unfunded pension liability of $464.4 billion in 2015, Stanford researchers estimated that the average unfunded liability per California household jumped from $9,127 in 2008; jumped to $21,491 in 2015; and would be over $40,000 in 2030.

The California Supreme Court heard testimony in Cal Fire v. CalPERS on December 5 over claims by the union that a 1955 decision set a precedent, referred to as the “California Rule,” that bars state and local government from reducing any promised retirement benefits without equivalent new compensation.

Lawyers for the state argued that the California Constitution is not a “straitjacket” and that making pension benefit changes should not be illegal under the California Constitution:

If the impairment is limited and does not meaningfully alter an employee’s right to a substantial or reasonable pension or if it is reasonable and necessary to serve an important public purpose, it may be permissible under the contract clause.

The biggest challenge for Brown’s effort to eliminate the California Rule is that he successfully lobbied the state legislature to pass collective bargaining for public employees in 1982, just as he was retiring from his second four-year term as governor.

The Bureau of Labor Statistics reported that average cost for the average private sector employee contribution for retirement and savings was 3.9 percent, and the average public-sector cost was 11.6 percent.

But even if the California’s Public Employees’ Pension Reform Act survives it Supreme Court appeal, CalPERS’ 2018 average cost for pensions as a percentage of worker compensation was 20.4 percent for State Industrial; 21.5 percent for State Safety; 43.5 percent for State Peace Officer/Fireman; and 55.2 percent for Highway Patrol.

The California Supreme Court is expected to release a decision regarding the California Rule in early 2019, just after Brown leaves office on January 7.

Even A $1 Million Retirement Nest Egg Isn’t Enough Anymore

- With more retirees responsible for their own financial security, even a $1 million nest egg isn’t nearly enough.

- Considering the looming retirement savings shortfall, experts say there are only two ways out: Earn more or spend less.

A cool $1 million has long been considered the gold standard of retirement savings. These days, it’s only a fraction of what you will really need.

For instance, a 67-year-old baby boomer retiring now with $1 million in the bank will generate $40,000 a year to live on adjusted for inflation and assuming a sustainable withdrawal rate of 4 percent, said Mark Avallone, president of Potomac Wealth Advisors and author of “Countdown to Financial Freedom.”

It’s worse for a 42-year-old Gen Xer, whose $1 million at retirement will only generate an inflation-adjusted $19,000 a year when all is said and done. And a 32-year-old millennial planning to retire at 67 with $1 million would live below the poverty line.

That’s called “million-dollar poverty.

For most Americans, there’s been a serious lack of proper investment income and planning, Avallone said. That, coupled with inflation, a looming pension crisis and longer life expectancy, is “a toxic formula for successful retirement,” he said — one that will result in a dramatic drop-off in lifestyle for retirees.

“Today’s generation of working people grew up in an era where their parents went to a mailbox, and a check appeared. But pensions are almost extinct,” Avallone said. “People have to self-fund their retirement, and the enormity of that challenge is underestimated.”

WalletHub conducted a study this year to determine how long a nest egg of $1 million would really last. The personal finance site compared average expenses for people age 65 and older, including groceries, housing, utilities, transportation and health care.

Naturally, depending on where in the U.S. you live, the longevity of a $1 million nest egg varies. Those dollars stretched furthest in states like Mississippi, Arkansas and Tennessee, where retirees could live a life of leisure for at least a quarter of a century.

However, in Hawaii, where residents pay roughly 30 percent more for household items across the board, that same amount will only get you just shy of a dozen years — largely because of that higher cost of living and pricey real estate.

Considering that many families spend more than 100 percent of their income after taxes on monthly expenses alone, there are only two ways to overcome million-dollar poverty, Avallone said: Earn more or spend less.

For those nearing retirement, Avallone suggests getting a side gig, or “hobby job,” and then saving 100 percent of that income.

“The key is to automatically deposit that money in a savings or investment account,” he said.

Alternatively, take a hard look at your expenses and differentiate between what’s necessary and what’s discretionary. Then identify expenditures that can be cut back — which involves making some very tough decisions.

“Some are small, like lunches, but they add up,” he said. “Others are big, like private school.”

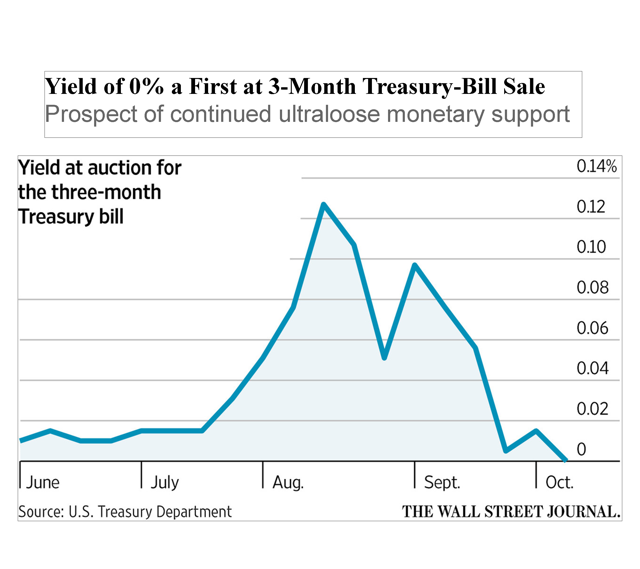

Anything Higher Than 0% Is Now High Yield; Retirees Thrown Under The Bus This Week

From the Seeking Alpha News Team, Oct. 6, 2015:

“Officially joining the 0% bond club, the U.S. Treasury sold a new government security on Monday containing a three-month maturity and a yield of zero for the first time on record. In essence, buyers gave a free short-term loan to the government in exchange for a highly liquid debt instrument for their portfolio. The result adds to the diminishing expectations – stoked by Friday’s disappointing jobs report – that the Fed will keep interest rates at basement levels throughout 2015.”

Record times. Should we break out the bubbly and celebrate, or get out the Valium? Now, after a lifetime of 40-hour weeks, you too can lend your hard-earned money to Uncle Sam and get a negative 2% return for your trouble. (Let’s not forget about that big elephant in the room called inflation.) Figure it into your return calculations and you lose 2% annualized on this “investment”.

The U.S. Treasury has finally joined a rarefied club, along with Germany, Japan and others.

If you are the patriotic type and feel like giving Uncle Sam an interest free loan, be my guest. Do you also pay more tax than required because you think Uncle Sam could use a break dealing with those big deficits? Do you have so much money with no place to go that you’d rather see it locked up, safe and sound for 3 months in Uncle Sam’s vaults than chance it being stolen from underneath your mattress?

Be my guest. I have better ideas for those dollars.

Here’s how the Wall Street Journal reported this astounding event.

By MIN ZENG

Updated Oct. 5, 2015 7:51 p.m.

The U.S. Treasury sold a new government security with a three-month maturity and a yield of zero for the first time on record, reflecting the highest demand since June.

In essence, buyers gave a free short-term loan to the U.S. government in exchange for a highly liquid debt instrument for their portfolio.

The result reflects diminishing expectations in financial markets that the Federal Reserve would raise short-term rates before year-end after Friday’s disappointing jobs report. Yields on these short-term Treasury-debt instruments are highly sensitive to changes in the Fed’s interest-rate policy outlook.

The move occurred on a day that stocks surged, with the Dow Jones Industrial Average adding 304.06 points, or 1.8%, to 16776.43.

The prospect of continued ultra loose monetary support bolstered demand on Monday for riskier assets, including stocks and commodities. That in turn diluted the appeal of relatively safer assets, boosting the yield on the benchmark 10-year Treasury note to 2.058% Monday, from a five-month low of 1.989% Friday. Bond yields rise as prices fall.

The Fed is off the table for 2015 no matter what they say,” said Andrew Brenner, head of international fixed income for broker dealer National Alliance Capital Markets. Investors “will claw their way back” in riskier assets between now and year-end, he said.

Monday’s $21 billion auction of three-month Treasury bills drew $4.14 in bids for each dollar offered, and the resulting bid-to-cover ratio was the highest since June 22. Bills are Treasury debt maturing in a year or less. The Treasury sells bills maturing in one month, three months and six months on a weekly basis.

In terms of demand, concern about Fed hikes in 2015 is evaporating, particularly following the disappointing jobs numbers,” said Andrew Hollenhorst, U.S. short-term interest-rate strategist at Citigroup Global Markets Inc. in New York.

Competition to obtain bills has been intensifying lately. Of the past six one-month bill auctions, five sales were offered at a zero yield.

In the secondary market, some bills have been yielding slightly below zero or around zero for weeks. On Monday, the yield on the one-month bill traded at negative-0.02% and the three-month yield was zero. An investor who holds the one-month bill through maturity will log a moderate capital loss, but that is the price the buyer has been willing to pay to obtain the bills.

It is a bizarre outcome, but that is the world we are living in right now,” said Thomas Simons, money-market economist in the Fixed Income Group at Jefferies LLC. “For many investors investing in short-term markets, bills are the only game in town.”

Bizarre outcome, indeed

Last week, I wrote an article about a bank offering a “high yield” of 1.05% to depositors. I disparaged the misnomer, calling such a product high yield, when clearly, even in ZIRP world, alternatives exist.

Little did I imagine that we’d now be referring to last week’s 3-month Treasury yield of .08% as high yield in comparison to today’s offering of 0%. What have we come to, where anything higher than 0% is now considered high yield?

If there was any doubt in anyone’s mind that we’re stuck at low rates for longer, I think this latest pricing has cleared things up. Which brings us to yet another crossroads:

A. Recognize that this is yet another gift and a tip of the hat to equity markets because cheap money is here to stay, a while longer at least, allowing the equities markets greater running room to extend the six-day rally and re-inflate investors’ wallets. Champagne? Yes, please.

B. Remain downtrodden because we have no place to store our hard-earned money safely and earn any return whatsoever. A little Valium to calm the nerves? Retirees used to being able to comfortably park their money in safe investments like Treasuries and CDs continue to feel the brunt of this zero interest rate policy and perceive that after being thrown under the bus for almost nine years of low rates, now at 0% it feels like that bus keeps crushing them over and over.

I choose alternative A. To accept this proposition from the Treasury is a most certain guarantee that when we are repaid in three months time, we will have lost 2% purchasing power on an annual basis. That strikes me as pure madness.

by George Schneider. Read more in Seeking Alpha

I gotta fever and the only prescription is MORE COWBELL!

Today’s Hottest Trend In Residential Real Estate

The practice of multigenerational housing has been on the rise the past few years, and now experts are saying that it is adding value to properties.

In a recent Wall Street Journal article, several couples across the country are quoted saying that instead of downsizing to a new home, they are choosing to live with their adult children.

This is what many families across the country are doing for both a “peace of mind” and for “higher property values.”

“For both domestic and foreign buyers, the hottest amenity in real estate these days is an in-law unit, an apartment carved out of an existing home or a stand-alone dwelling built on the homeowners’ property,” writes Katy McLaughlin of the WSJ. “While the adult children get the peace of mind of having mom and dad nearby, real-estate agents say the in-law accommodations are adding value to their homes.”

And how much more are these homes worth? In an analysis by Zillow, the homes with this type of living accommodations were priced about 60 percent higher than regular single-family homes.

Local builders are noticing the trend, too. Horsham based Toll Brothers are building more communities that include both large, single-family homes and smaller homes for empty nesters, the company’s chief marketing officer, Kira Sterling, told the WSJ.