Tag Archives: Zillow

Zillow Layoffs Tell More About Real Estate Market Than Most Think

Zillow Fires 25% Of Workforce, Scraps Robo-Flipping Program After Huge Loss

On Monday we reported that Zillow Group had ‘halted‘ it’s AI-powered house-flipping operation after 93% of homes listed in their Phoenix portfolio are underwater, and is scrambling to unload 7,000 homes for $2.8 billion.

Today, the company announced during earnings that it’s going to reduce its workforce by 25% and completely scrap its home-flipping operation which began buying homes in December 2019.

Zillow Caught Holding The Bag As 93% Of Phoenix ‘Flipping’ Portfolio Listed At Loss

Two weeks ago Zerohedge reported that Zillow’s electronic house flipping operation had been underperforming – as the real estate company had been buying houses at inflated prices and flipping them for a loss.

Zillow’s Spencer Rascoff Lists His California Brentwood Park Home for $7M Over Zestimate

Rascoff purchased the house in 2016 for $19.7 million

Spencer Rascoff and the property (Credit: Twitter, Zillow, and Google Maps)

Spencer Rascoff, the co-founder and former CEO of Zillow, has put his Brentwood Park estate on the market for $24 million, according to Redfin. The asking price is $7 million over the “Zestimate,” or Zillow’s appraisal of what the home is worth.

Property records show that Rascoff paid $19.7 million for the property in 2016.

The listing states that the 12,700-square-foot home – remodeled by architects Ken Ungar and Steve Giannetti – is located on a half acre in a gated neighborhood. The Zillow Zestimate for the house suggests it’s worth $16.7 million.

Josh and Matt Altman of Douglas Elliman have the listing.

Rascoff purchased the house from investment banker Michael J. Richter, who reportedly paid $9.3 million for the Parkyns Street manse in 2012.

The home has six bedrooms and nine bathrooms, along with a “spectacular” chef’s kitchen, a state-of-the-art theater with stadium seating, a fitness studio and a large master suite with a large balcony. The estate also features a two-bedroom guest wing, a motor court, and a spa, pool and mudroom.

Rascoff is currently launching dot.LA, a news and events company that will cover the tech scene in Los Angeles.

Last year, Rascoff stepped down from Zillow, which has pivoted to an ibuyer model with Rich Barton at the helm.

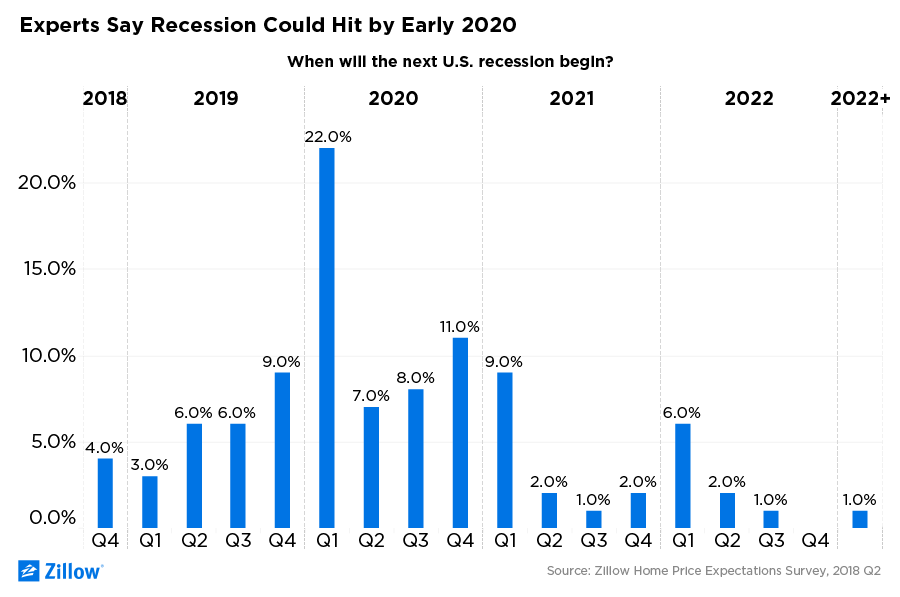

Zillow: The Next Recession is Two Years Away

The next U.S. recession is likely to begin in the first quarter of 2020, according to a poll of 100 economists published Zillow’s Home Price Expectations Survey for the second quarter.

More than half of the survey respondents pointed to monetary policy as the likeliest cause for the next downturn, with only nine of the polled economists predicting that the housing market will be the cause of the next crash. Indeed, most of the economists predicted home values will rise 5.5 percent in 2018 to a median of $220,800. But if the Federal Reserve raises rates too quickly, the economists warned, the economy will start to slow and that could spur a new recession.

“As we close in on the longest economic expansion this country has ever seen, meaningfully higher interest rates should eventually slow the frenetic pace of home value appreciation that we have seen over the past few years, a welcome respite for would-be buyers,” said Zillow Senior Economist Aaron Terrazas. “Housing affordability is a critical issue in nearly every market across the country, and while much remains unknown about the precise path of the U.S. economy in the years ahead, another housing market crisis is unlikely to be a central protagonist in the next nationwide downturn.”

Increasing Rent Costs Present a Challenge to Aspiring Homeowners

by Tory Barringer

by Tory Barringer

Fast-rising rents have made it difficult for many Americans to save up a down payment for a home purchase—and experts say that problem is unlikely to go away any time soon.

Late last year, real estate firm Zillow reported that renters living in the United States paid a cumulative $441 billion in rents throughout 2014, a nearly 5 percent annual increase spurred by rising numbers of renters and climbing prices. Last month, the company said that its own Rent Index increased 3.3 percent year-over-year, accelerating from 2013 even as home price growth slows down.

Results from a more recent survey conducted by Zillow and Pulsenomics suggest that rent prices will continue to be a problem for the aspiring homeowner for years to come.

Out of more than 100 real estate experts surveyed, 51 percent said they expect rental affordability won’t improve for at least another two years, Zillow reported Friday. Another 33 percent were a little more optimistic, calling for a deceleration in rental price increases sometime in the next one to two years.

Only five percent said they expect affordability conditions to improve for renters within the next year.

Despite the challenge that rising rents presents to home ownership throughout the country, more than half—52 percent of respondents—said the market should be allowed to correct the problem on its own, without government intervention.

“Solving the rental affordability crisis in this country will require a lot of innovative thinking and hard work, and that has to start at the local level, not the federal level,” said Zillow’s chief economist, Stan Humphries. “Housing markets in general and rental dynamics in particular are uniquely local and demand local, market-driven policies. Uncle Sam can certainly do a lot, but I worry we’ve become too accustomed to automatically seeking federal assistance for housing issues big and small, instead of trusting markets to correct themselves and without waiting to see the impact of decisions made at a broader local level.”

On the topic of government involvement in housing matters: The survey also asked respondents about last month’s reduction in annual mortgage insurance premiums for loans backed by the Federal Housing Administration (FHA). The Obama administration has projected that the cuts will help as many as 250,000 new homeowners make their first purchase.

The panelists were lukewarm on the change: While two-thirds of those with an opinion said they think the changes could be “somewhat effective in making homeownership more accessible and affordable,” just less than half said the new initiatives are unwise and potentially risky to taxpayers.

Finally, the survey polled panelists on their predictions for U.S. home values this year. As a whole, the group predicted values will rise 4.4 percent in 2015 to a median value of $187,040, with projections ranging from a low of 3.1 percent to a high of 5.5 percent.

“During the past year, expectations for annual home value appreciation over the long run have remained flat, despite lower mortgage rates,” said Terry Loebs, founder of Pulsenomics. “Regarding the near-term outlook, there is a clear consensus among the experts that the positive momentum in U.S. home prices will continue to slow this year.”

On average, panelists said they expect median home values will pass their precession peak ($196,400) by May 2017.

Today’s Hottest Trend In Residential Real Estate

The practice of multigenerational housing has been on the rise the past few years, and now experts are saying that it is adding value to properties.

In a recent Wall Street Journal article, several couples across the country are quoted saying that instead of downsizing to a new home, they are choosing to live with their adult children.

This is what many families across the country are doing for both a “peace of mind” and for “higher property values.”

“For both domestic and foreign buyers, the hottest amenity in real estate these days is an in-law unit, an apartment carved out of an existing home or a stand-alone dwelling built on the homeowners’ property,” writes Katy McLaughlin of the WSJ. “While the adult children get the peace of mind of having mom and dad nearby, real-estate agents say the in-law accommodations are adding value to their homes.”

And how much more are these homes worth? In an analysis by Zillow, the homes with this type of living accommodations were priced about 60 percent higher than regular single-family homes.

Local builders are noticing the trend, too. Horsham based Toll Brothers are building more communities that include both large, single-family homes and smaller homes for empty nesters, the company’s chief marketing officer, Kira Sterling, told the WSJ.

Assisted-Living Complexes for Young People

One of the most surprising developments in the aftermath of the housing crisis is the sharp rise in apartment building construction. Evidently post-recession Americans would rather rent apartments than buy new houses.

When I noticed this trend, I wanted to see what was behind the numbers.

Is it possible Americans are giving up on the idea of home ownership, the very staple of the American dream? Now that would be a good story.

What I found was less extreme but still interesting: The American dream appears merely to be on hold.

Economists told me that many potential home buyers can’t get a down payment together because the recession forced them to chip away at their savings. Others have credit stains from foreclosures that will keep them out of the mortgage market for several years.

More surprisingly, it turns out that the millennial generation is a driving force behind the rental boom. Young adults who would have been prime candidates for first-time home ownership are busy delaying everything that has to do with becoming a grown-up. Many even still live at home, but some data shows they are slowly beginning to branch out and find their own lodgings — in rental apartments.

A quick Internet search for new apartment complexes suggests that developers across the country are seizing on this trend and doing all they can to appeal to millennials. To get a better idea of what was happening, I arranged a tour of a new apartment complex in suburban Washington that is meant to cater to the generation.

What I found made me wish I was 25 again. Scented lobbies crammed with funky antiques that led to roof decks with outdoor theaters and fire pits. The complex I visited offered Zumba classes, wine tastings, virtual golf and celebrity chefs who stop by to offer cooking lessons.

“It’s like an assisted-living facility for young people,” the photographer accompanying me said.

Economists believe that the young people currently filling up high-amenity rental apartments will eventually buy homes, and every young person I spoke with confirmed that this, in fact, was the plan. So what happens to the modern complexes when the 20-somethings start to buy homes? It’s tempting to envision ghost towns of metal and pipe wood structures with tumbleweeds blowing through the lobbies. But I’m sure developers will rehabilitate them for a new demographic looking for a renter’s lifestyle.

Implosion of Housing Bubble 2 Hits Six Cities In The West

Source: Testosterone Pit

“Homes in more than 1,000 cities and towns nationwide either already are, or soon will be, more expensive than ever,” Zillow reported gleefully the other day. “National home values have climbed year-over-year for 21 consecutive months, a steady march upward….”

Glorious recovery. Our phenomenal housing bubble that, when it blew up spectacularly, helped topple our financial system, threw the economy into the Great Recession, caused millions of jobs to evaporate, and made people swear up and down: never-ever again another housing bubble.

Steps in the Fed, and trillions of dollars get printed and handed to Wall Street, and asset prices become airborne, and Wall Street jumps into the housing market and buys up hundreds of thousands of vacant single-family homes, drives up prices, and armed with free money, shoves aside first-time buyers and others who would actually live in these homes, and turned them instead into rental units. Now in over 1,000 cities, prices are, or soon will be, as high as they were at the peak of the last housing bubble.

The difference? Last time, all that craziness was called a “bubble” with hindsight. This time, it’s called a “housing recovery.”

The result of this, as Zillow called it, “remarkable milestone”: real buyers who intend to live in these homes are falling by the wayside. Every week for months, mortgages to purchase homes have been between 10% and 15% below the same week in the prior year. In the latest week, they dropped 21%, the worst week I remember seeing. The number of refis has plunged even more, but that only ate into bank income statements and caused thousands of people to get laid off. Purchase mortgages, when they drop, decimate home sales.

Real Americans, rather than Wall Street, have been priced out of the housing market. Inflation has eaten into their wages. Many people can only find part-time work. Mortgage interest has risen from ridiculously low to just historically low [ Hot Air Hisses Out Of Housing Bubble 2.0: Even Two Middle-Class Incomes Aren’t Enough Anymore To Buy A Median Home].

So the rate of homeownership in the first quarter, after ticking up last year and triggering bouts of false hope, fell to 64.8%. The lowest level since 1995! It had peaked in Q2 2004 at 69.2%, a sign that even as the prior housing bubble was gaining steam, regular folks were already priced out of the market. This ugly trajectory is the face of the “housing recovery” sans Wall Street:

And now history has become a Fed-induced rerun. It started in six until recently white-hot housing markets in Arizona and California – Phoenix, Ventura, Riverside, L.A., Sacramento, and San Diego – where home prices have skyrocketed to the point where few people can afford them. Electronic real-estate broker Redfin, which covers 19 metro areas around the country, explained the impact of “the double whammy” – rising prices and mortgage rates – this way:

Someone who purchased a $350,000 home in Riverside in March 2013 with a 20 percent down payment and a 30-year fixed rate of 3.4% would have a monthly mortgage payment of $1,241. But with prices up 19.6%, the same home would now cost $418,600. At the current mortgage rate of 4.33%, the monthly mortgage payment on that home is now $1,663, a 34% jump from a year ago.

And even a year ago, a family with two median incomes had to stretch to buy that house. Now, in these six markets, sales are plunging and inventories of houses for sale are soaring. A deadly mix.

In Phoenix, inventories were up 42.7% in March from prior year, but sales were down 17.4%. So sellers slashed prices to get rid of these homes. In Phoenix, the hardest hit of the bunch, 45% of the sellers cut their prices. That’s how it starts. Haven’t we been there before? For instance, at the beginning of the prior housing-bubble implosion? This is what that debacle looks like:

It didn’t look quite this terrible in 11 of the other markets that Redfin tracks: Austin, Baltimore, Boston, Chicago, Long Island, Philadelphia, Portland, San Francisco, San Jose, Seattle, and Washington, D.C. (due to “data anomalies,” Denver and Las Vegas were not included). Sales were still down, but so were inventories. When the last housing bubble imploded, it didn’t happen all at once across the country. In some cities, home prices peaked in early 2006; in San Francisco, they peaked in November 2007.

And what happened to the Wall Street investors who whipped the market into frenzy by deploying the Fed’s free money? Soaring prices are “eroding investor profit potential,” Redfin points out, and many have pulled back. As of year-end 2013, the percentage of investor purchases in these six markets dropped to 10.6% from 15.6% a year earlier. And since then, they’ve dropped even more. Easy come, easy go.

“Housing affordability is really taking a bite out of the market,” is how the chief economist for the California Association of Realtors explained the March home sales fiasco. “We haven’t seen this issue since 2007.” And so, the benchmarks established during the terrible implosion of the prior housing bubble are suddenly reappearing.

California Dominates Top 10 Sellers’ Housing Markets

Source: Reverse Mortgage Daily

Five of the nation’s top 10 sellers’ markets are located in California, while all of the top buyers’ markets are located in Midwest and Eastern metros as the housing market increasingly becomes localized.

San Jose, San Francisco, Los Angeles, Riverside, and Sacramento are among the top sellers’ markets according to the February Zillow Real Estate Market Reports, accompanied by San Antonio, Seattle, Denver, D.C., and Dallas-Forth Worth.

It’s more of a buyer’s market on the other side of the country, where there’s less competition and more room for bargaining on prices in metros such as Cleveland, Philadelphia, Tampa, Chicago, and Pittsburgh.

“The real estate data in markets on both coasts are telling markedly different stories. Relatively strong job markets in the West are helping spur robust demand, which is being met with limited supply, causing rapid home value appreciation and giving sellers an edge,” said Zillow Chief Economist Dr. Stan Humphries. ”In the East, housing markets are appreciating a bit more slowly, and homes are staying on the market longer, which helps give buyers the upper hand.”

Buyers in sellers’ markets can expect tight inventory, more competition, and a greater sense of urgency, he continued.

Home values rose to $169,200 in February, Zillow’s Home Value Index indicates, up 5.6% year-over-year, and are expected to rise another 3% through next February. However, national home values stayed almost flat from January to February, while monthly and annual home value appreciation slowed to their lowest paces in months.

“As we put the housing recession further in the rear-view mirror, the broad-based dynamics that applied during those days, when all markets were reacting similarly to nationwide economic conditions, are fading,” Humphries said. “Real estate has always been local, and as the spring market gains momentum, this old adage will only become more pronounced.”