Photographer: Andrew Harrer/Bloomberg

David Stevens, president and chief executive officer of the Mortgage Bankers Association, stands with his daughter Sara Stevens in the Senate Russell Building in Washington, D.C., on June 5, 2014.

David Stevens, chief executive officer of the Mortgage Bankers Association, has spent his career lauding the merits of home ownership. One person still isn’t buying it: his daughter.

Sara Stevens, 27, knows interest rates are low, rents are high and owning a home can build wealth. She also had a front-row seat to the worst real-estate slump since the Great Depression.

“The world has changed,” she said.

Six years since the collapse of Lehman Brothers triggered a financial meltdown, some young adults are more risk averse and view the potential upsides of status and wealth more skeptically than before the crisis, altering the home ownership calculation. It’s more than the weight of student loans, an iffy job market and tight credit — even those who can buy are hesitant.

The doubt is so pervasive that it’s eroded entry-level sales and hampered the recovery. In May, the share of first-time buyers fell for the third month, to 27 percent, according to the National Association of Realtors. Historically, it’s been closer to 40 percent of all buyers.

“We have a younger generation that has sat on the front lines of this housing recession,” said Stevens, 57. “They’re clearly being more thoughtful about it and they’re clearly deferring that decision.”

Dad’s sales pitches started when Sara was 4 years old, big sister to a fussy newborn. To calm the baby, he would load both girls into the family’s Ford Taurus.

Early Indoctrination

“We would drive around neighborhoods and he would point out houses,” chattering about curb appeal and prices, Sara said. “I’ve heard about this my whole life. In my head, I always figured at the age of 27 or 28 I’d buy.”

She can, but hasn’t. She’s a legislative aide to Senator Michael Bennet, a Colorado Democrat. Her fiancé, Dan Nee, is a software developer. Their jobs are steady and their combined income is $107,500. The car is paid for and dad is ready to help with a down payment.

They surf listings on Zillow Inc. from their 765-square-foot one-bedroom in Arlington, Virginia, which costs $2,195 a month, not including parking, utilities and a $35 fee for Max the cockapoo. They have about $25,000 in student debt.

The couple’s rent-or-own conundrum is complicated by the quality of their apartment, which is in the thick of urban nightlife and steps from a subway line to Sara’s job on Capitol Hill. More-affordable neighborhoods have higher crime and fewer amenities, or they’re farther from downtown and require a second car. A fixer-upper, while cheaper, means headaches.

Financially Insecure

“A house is a five- to 10-year commitment,” Sara said. “I’m hesitant about diving in and feeling like I’m not financially ready.”

She and other millennials — the generation born beginning in the early 1980s — started coming of age just as housing collapsed. Sara was just out of college in 2009 when President Barack Obama put her dad in charge of the Federal Housing Administration. Part of his job was to lobby Congress not to dismantle the financial architecture that had made it possible for generations of Americans — including himself — to buy homes. He also was juggling pleas from family and friends who couldn’t pay their adjustable-rate mortgages or sell their devalued houses.

“I watched cousins and other family members go through pretty tough situations in 2008 and 2009,” Sara said. “I can’t tell you how many of them he tried to help get out of bad mortgages.”

Generational Impact

As FHA commissioner, her dad would wonder aloud how the recession might affect Sara and her generation.

Most still aspire to own, though just 52 percent consider homeownership an “excellent long-term investment,” according to an April survey from the Chicago-based John D. and Catherine T. MacArthur Foundation. And almost three-fourths of adults 18 to 34 years old say the U.S. still is in the throes of a housing crisis, a bigger share than any other age group.

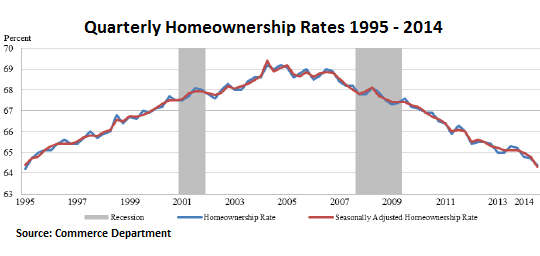

Without first-time buyers, current owners have a harder time selling and trading up, depressing the market and dragging down the economy. U.S. homeownership fell for the ninth straight year in 2013, to 65.1 percent, according to the Commerce Department. The MBA is projecting sales will decline for the first time in four years.

“We need more warm bodies buying homes and first-time buyers are the way to get it,” said Mark Fleming, the Vienna, Virginia-based chief economist of property-data firm CoreLogic Inc.

Taking Plunge

David Stevens took the plunge in 1984, when he was 27 and engaged, like Sara is now. The rate on a 30-year fixed mortgage averaged 13.9 percent as Paul Volcker, then chairman of the Federal Reserve, tried to tame inflation. Home prices were picking up again after back-to-back recessions had reined in double-digit increases seen during the late 1970s.

Stevens paid $73,400 for a three-bedroom, one-bath rambler near Denver. He assumed a 12.5 percent FHA mortgage, putting no money down. Colorado had been hammered by a plunge in oil prices and the seller owed more on the house than it was worth.

“It was similar to the environment we’re in now,” Stevens said, calling the house “an incredible deal.”

On paper, young adults are better positioned to buy now than they were 30 years ago. Affordability for entry-level buyers is more than twice as good, according to the National Association of Realtors. Mortgage payments as a share of income, at 14.2 percent, are half what they were, according to the Realtors. Unemployment among 25- to 34-year-olds, 6.9 percent in the first quarter of this year, was 7.9 percent at the start of 1984.

Greater Urgency

Back then, there was an urgency to get into the market, said John Buckley, managing director of the Harbour Group, a Washington public relations firm and consultant on the MacArthur Foundation’s report. It’s different now, said Buckley, who was a spokesman for President Ronald Reagan’s re-election bid in 1984.

“There was a sense that the window was closing to get a good deal and be able to participate in the American dream,” Buckley said. Today, there’s “tremendous uncertainty about whether the value of that investment is going to be worth the commitment and risk.”

Of course it’s more than negative psychology at work. Student loan debt has more than tripled in the past decade, to more than $1.1 trillion. And it’s harder to get a mortgage. While Fannie- and Freddie-backed borrowers have an average score of 740, most young adults have credit scores below 700, according to FICO, a credit-reporting company.

Channeling Grandma

“We’ve weathered the storm of the crash and Lehman going under better than they have,” said Fleming, 42, calling millennials jaded. “Like their grandparents who went through the depression, they’re apprehensive about overextending themselves.”

At the Stevens household, it’s not lost on Sara that a cheerleader-in-chief for housing can’t get a rah-rah out of his daughter, especially when she’s done everything right. She has an education, a job and dad’s support, financially and otherwise.

“I am incredibly lucky,” she said. “My parents have positioned me well and they’ve given me resources to take on a house if I really wanted to. I think that’s part of his worry. If we’re still having this conversation, what’s it like for a whole generation of other kids?”

You must be logged in to post a comment.