by Wolf Richter

by Wolf Richter

February 4th, 2015: Crude oil had rallied 20% in three days, with West Texas Intermediate jumping $9 a barrel since Friday morning, from $44.51 a barrel to $53.56 at its peak on Tuesday. “Bull market” was what we read Tuesday night. The trigger had been the Baker Hughes report of active rigs drilling for oil in the US, which had plummeted by the most ever during the latest week. It caused a bout of short covering that accelerated the gains. It was a truly phenomenal rally!

But the weekly rig count hasn’t dropped nearly enough to make a dent into production. It’s down 24% from its peak in October. During the last oil bust, it had dropped 60%. It’s way too soon to tell what impact it will have because for now, production of oil is still rising.

And that phenomenal three-day 20% rally imploded today when it came in contact with another reality: rising production, slack demand, and soaring crude oil inventories in the US.

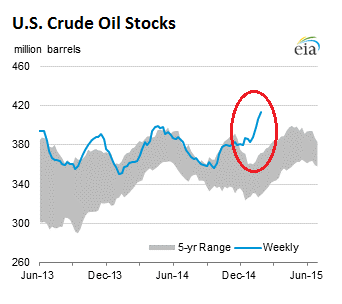

The Energy Information Administration reported that these inventories (excluding the Strategic Petroleum Reserve) rose by another 6.3 million barrels last week to 413.1 million barrels – the highest level in the weekly data going back to 1982. Note the increasingly scary upward trajectory that is making a mockery of the 5-year range and seasonal fluctuations:

And there is still no respite in sight.

Oil production in the US is still increasing and now runs at a multi-decade high of 9.2 million barrels a day. But demand for petroleum products, such as gasoline, dropped last week, according to the EIA, and so gasoline inventories jumped by 2.3 million barrels. Disappointed analysts, who’d hoped for a drop of 300,000 barrels, blamed the winter weather in the East that had kept people from driving (though in California, the weather has been gorgeous). And inventories of distillate, such as heating oil and diesel, rose by 1.8 million barrels. Analysts had hoped for a drop of 2.2 million barrels.

In response to this ugly data, WTI plunged $4.50 per barrel, or 8.5%, to $48.54 as I’m writing this. It gave up half of the phenomenal three-day rally in a single day.

Macquarie Research explained it this way:

In our experience, oil markets rarely exhibit V-shaped recoveries and we would be surprised if an oversupply situation as severe as the current one was resolved this soon. In fact, our balances indicate the absolute oversupply is set to become more severe heading into 2Q15.

Those hoping for a quick end to the oil glut in the US, and elsewhere in the world, may be disappointed because there is another principle at work – and that principle has already kicked in.

As the price has crashed, oil companies aren’t going to just exit the industry. Producing oil is what they do, and they’re not going to switch to selling diapers online. They’re going to continue to produce oil, and in order to survive in this brutal pricing environment, they have to adjust in a myriad ways.

“Efficiency and innovation, when price falls, it accelerates, because necessity is the mother of invention,” Michael Masters, CEO of Masters Capital Management, explained to FT Alphaville on Monday, in the middle of the three-day rally. “Even if the investment only spits out quarters, or even nickels, you don’t turn it off.”

Crude has been overvalued for over five years, he said. “Whenever the return on capital is in the high double digits, that’s not sustainable in nature.” And the industry has gotten fat during those years.

Now, the fat is getting trimmed off. To survive, companies are cutting operating costs and capital expenditures, and they’re shifting the remaining funds to the most productive plays, and they’re pushing 20% or even 30% price concessions on their suppliers, and the damage spreads in all directions, but they’ll keep producing oil, maybe more of it than before, but more efficiently.

This is where American firms excel: using ingenuity to survive. The exploration and production sector has been through this before. And those whose debts overwhelm them – and there will be a slew of them – will default and restructure, wiping out stockholders and perhaps junior debt holders, and those who hold the senior debt will own the company, minus much of the debt. The groundwork is already being done, as private equity firms and hedge funds offer credit to teetering oil companies at exorbitant rates, with an eye on the assets in case of default.

And these restructured companies will continue to produce oil, even if the price drops further.

So Masters said that, “in our view, production will not decrease but increase,” and that increased production “will be around a lot longer than people are forecasting right now.”

After the industry goes through its adjustment process, focused on running highly efficient operations, it can still scrape by with oil at $45 a barrel, he estimated, which would keep production flowing and the glut intact. And the market has to appreciate that possibility.

Rigs Down By 21% Since Start Of 2015

Permian Basin loses 37 rigs first week in February

by Trevor Hawes

The number of rigs exploring for oil and natural gas in the Permian Basin fell 37 this week to 417, according to the weekly rotary rig count released Friday by Houston-based oilfield service company Baker Hughes.

This week’s count marked the ninth-consecutive decrease for the Permian Basin. The last time Baker Hughes reported a positive rig-count change was Dec. 5, when 568 rigs were reported. Since then, the Permian Basin has shed 151 rigs, a decrease of 26.58 percent.

For the year, the Permian Basin has shed 113 rigs, or 21.32 percent.

In District 8, which includes Midland and Ector counties, the rig count fell 19 this week to 256. District 8 has shed 58 rigs, 18.47 percent, this year.

Texas lost 41 rigs this week for a statewide total of 654. The Lone Star State has 186 fewer rigs since the beginning of the year, a decrease of 22.14 percent.

In other major Texas basins, there were 168 rigs in the Eagle Ford, down 10; 43 in the Haynesville, unchanged; 39 in the Granite Wash, down one; and 19 in the Barnett, unchanged.

The Haynesville shale is the only major play in Texas to have added rigs this year. The East Texas play started 2015 with 40 rigs.

At this time last year, there were 483 rigs in the Permian Basin and 845 in Texas.

In the U.S., there were 1,456 rigs this week, a decrease of 87. There were 1,140 oil rigs, down 83; 314 natural gas rigs, down five; and two rigs listed as miscellaneous, up one.

By trajectory, there were 233 vertical drilling rigs, down two; 1,088 horizontal drilling rigs, down 80; and 135 directional drilling rigs, down five.

The top five states by rig count this week were Texas; Oklahoma with 176, down seven; North Dakota with 132, down 11; Louisiana with 107, down one; and New Mexico with 78, down nine.

The top five basins were the Permian; the Eagle Ford; the Williston with 137, down 11; the Marcellus with 71, down four; and the Mississippian with 53, down one.

In the U.S., there were 1,397 rigs on land, down 85; nine in inland waters, down three; and 50 offshore, up one. There were 48 rigs in the Gulf of Mexico, up one.

Canada’s rig count fell 13 this week to 381. There were 184 oil rigs, down 16; 197 natural gas rigs, up three; and zero rigs listed as miscellaneous, unchanged. Canada had 621 rigs a year ago this week, a difference of 240 rigs compared to this week’s count.

The number of rigs exploring for oil and natural gas in the North America region, which includes the U.S. and Canada, fell 100 this week to 1,837. There were 2,392 rigs in North America last year.

Rigs worldwide

On Friday, Baker Hughes released its monthly international rig count for January. The worldwide total was 3,309 rigs. The U.S. ended January with 1,683 rigs, just more than half of all rigs worldwide.

The following are January’s rig counts by region, with the top three nations in each region in parentheses:

— Africa: 132 (Algeria: 97; Nigeria: 19; Angola: 14)

— Asia-Pacific: 232 (India: 108; Indonesia: 36; China offshore: 33)

— Europe: 128 (Turkey: 37; United Kingdom offshore: 15; Norway: 13)

— Latin America: 351 (Argentina: 106; Mexico: 69; Venezuela: 64)

— Middle East: 415 (Saudi Arabia: 119; Oman: 61; Iraq: 60)

Migrant oil worker and wife near Odessa, Texas 1937

Photographer: Dorothea Lange Created: May 1937 Location: Odessa, Texas

Call Number: LC-USF34-016932 Source: MRT.com

You must be logged in to post a comment.