(Autumn Spreademann) Attempting to further sequester Russia’s economy U.S. President Joe Biden announced on March 8 the ban of all Russian oil imports as part of a multi-faceted response to the eastern nation’s military invasion of Ukraine.

While strict sanctions on Russian exports remain a cornerstone of Western efforts to stop President Vladimir Putin’s attack, it comes with a hefty price tag already felt by global consumers.

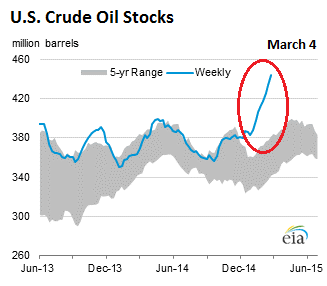

Traders say that Cushing stockpiles might fall to critical levels within weeks; the last time that happened was in 2014.

(Devika Krishna Kumar) Stockpiles at the biggest U.S. crude depot are quickly approaching critically low levels. The last time that happened, crude cost more than $100 a barrel.

Now that the global energy crisis has slammed China’s economy, leading to the first contractionary PMI since March 2020 as a result of widespread shutdowns of factory and manufacturing, not to mention hundreds of millions of Chinese residents suffering from periodic blackouts, Bloomberg reports that China’s central government officials “ordered the country’s top state-owned energy companies to secure supplies for this winter at all costs.”

(John Hayward) Prince Abdulaziz bin Salman, Saudi Arabia’s energy minister, crowed at Thursday’s OPEC meeting that the American energy revolution is over, OPEC would soon regain control over oil markets, and “Drill, baby, drill is gone forever.”

“Drill, baby, drill” began as a Republican campaign slogan in 2008, popularized by vice-presidential candidate Sarah Palin, although it was coined by then-Lt. Governor of Maryland Michael Steele. The basic idea was that aggressively developing America’s energy resources would bring economic prosperity and make the United States less dependent on foreign oil.

Back in the late fall of 2014, when Saudi Arabia broke up OPEC for the first time and unleashed a torrent of crude oil on the world despite the protests of its fellow cartel members, oil prices crashed as a result of what then seemed to be a “calculated” move by Riyadh which hoped to put US shale out of business amid a flawed gamble betting that shale breakeven prices were around $60-80. They, however, turned out to be much lower, which coupled with Saudi misreading of the willingness of junk bond investors to keep funding US shale producers, meant that despite a 3 years stretch of low oil prices, US shale emerged stronger than ever before, with the US eventually eclipsing both Saudi Arabia and Russia as the world’s biggest crude oil producer.

Fast forward to March 2020, when Saudi Arabia doubled down in its attempt to crush shale, only to avoid angering long-time ally Donald Trump, the Crown Prince pretended that the latest flood of oil was an oil price war aimed at Moscow not Midland. And this time, unlike 2014, with the benefit of the global economic shutdown resulting from the coronavirus pandemic, the Saudis may have finally lucked out in the ongoing crusade against US oil, because as Bloomberg writes with “negative oil prices, ships dawdling at sea with unwanted cargoes, and traders getting creative about where to stash oil”, the next chapter in the oil crisis is now inevitable: “great swathes of the petroleum industry are about to start shutting down.”

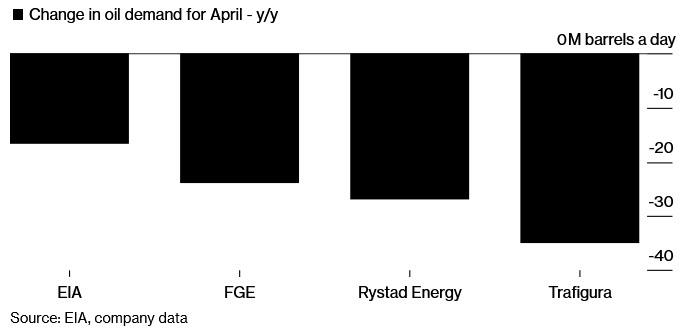

As the recent OPEC summit so vividly demonstrated, the marginal price of oil is no longer determined by supply or cuts thereof (such as the recently announced agreement by OPEC+ for a 9.7mmb/d output cut), but rather by demand, or the lack thereof, which according to some estimate is as much as 36mmb/d lower, or roughly a third of the global oil market every day, as billions of people are stuck at home instead of driving, while major corporations mothball production in a world where major economies have ground to a halt.

The economic impact of the coronavirus has ripped through the oil industry in dramatic phases, Bloomberg’s Javier Blas writes. First it destroyed demand as lock downs shut factories and kept drivers at home. Then storage started filling up and traders resorted to ocean-going tankers to store crude in the hope of better prices ahead.

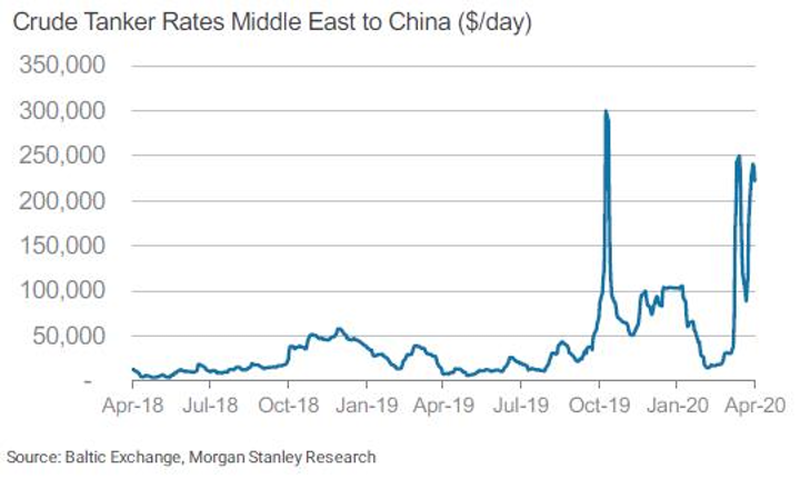

Now shipping prices are surging to stratospheric levels as the industry runs out of tankers, a sign of just how distorted the market has become.

Ironically, in its latest attempt to kill off shale, Saudi Arabia may have gone a step too far, as “the specter of production shut-downs – and the impact they will have on jobs, companies, their banks, and local economies – was one of the reasons that spurred world leaders to join forces to cut production in an orderly way. But as the scale of the crisis dwarfed their efforts, failing to stop prices diving below zero last week, shut-downs are now a reality. It’s the worst-case scenario for producers and refiners.“

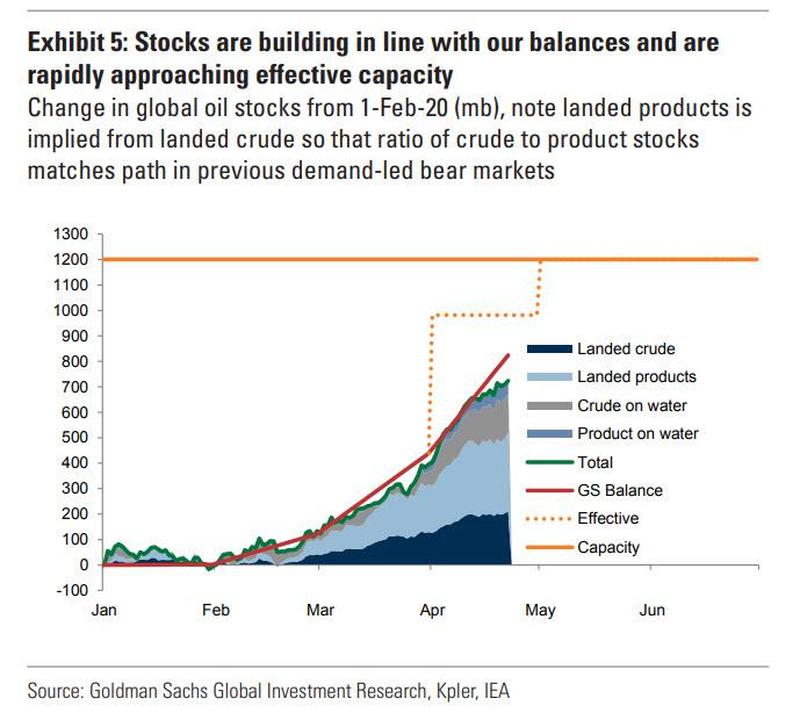

In short, the entire oil production industry is shutting down, not because it wants to – of course – but because it has no choice. According to Goldman, in as little as three weeks there will be literally no place left on earth to store oil, and unless oil producers want to pay “buyers” to hold the oil as happened on that historic date of April 20, they have no choice but to shut in output.

Which brings us back to why in 2020 Riyadh has succeeded where it failed in 2014: as Bloomberg writes “in theory, the first oil output cuts should have come from the OPEC+ alliance, which earlier this month agreed to reduce production from May 1. Yet after the catastrophic price plunge on Monday, when West Texas Intermediate fell to -$40 a barrel, it’s the U.S. shale patch that is leading”

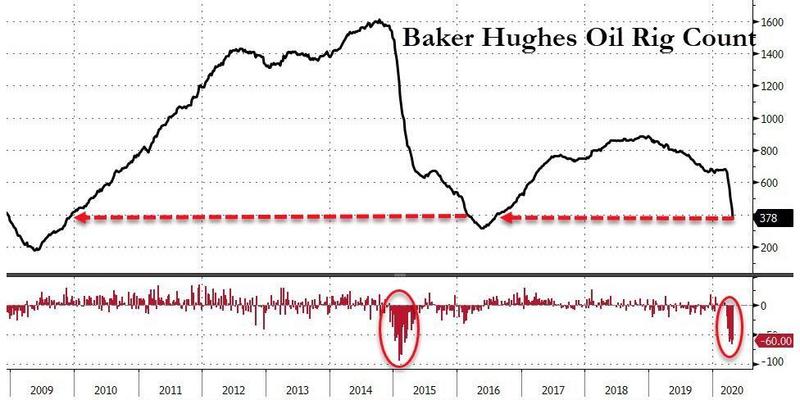

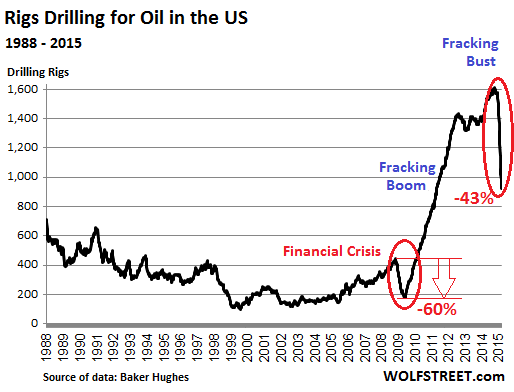

The best indicator of how the shale industry is reacting is the sudden collapse in the number of oil rigs in operation, which last week fell to a four-year low: “Before the coronavirus crisis hit, oil companies ran about 650 rigs in the US. By Friday, more than 40% of them had stopped working, with only 378 left.”

And while there is a delay between total US oil production and the rig count, it is now obvious that US production is set to collapse next:

“Monday really focused people’s minds that production needs to slow down,” said the co-head of oil trading at commodity merchant Trafigura. “It’s the smack in the face the market needed to realize this is serious.” Incidentally, Trafigura, one of the largest exporters of US crude from the U.S. Gulf of Mexico, believes that output in Texas, New Mexico, North Dakota and other states will now fall much faster than expected as companies react to negative prices…

Until prices collapsed on Monday, the consensus was that output would drop by about 1.5MM barrels a day by December. Now market watchers see that loss by late June. “The severity of the price pressure is likely to act as a catalyst for the immediate turn down in activity and shut-ins,” said Roger Diwan, oil analyst at consultant IHS Markit Ltd.

As detailed last week, this price shock has been especially acute in the physical market where producers of crude streams such as South Texas Sour and Eastern Kansas Common had to pay more than $50 a barrel to offload their output last week.

And so the US industry is finally shutting down as ConocoPhillips and shale producer Continental Resources have all announced plans to shut in output. Regulators in Oklahoma voted to allow oil drillers to shut wells without losing leases; New Mexico made a similar decision. Even North Dakota, which for years was synonymous with the U.S. shale revolution, is witnessing a rapid retrenchment, as Bloomberg notes that “oil producers have already closed more than 6,000 wells, curtailing about 405,000 barrels a day in production, or about 30% of the state’s total.”

However, it won’t be just the US: output cuts can be seen from Chad, a poor and landlocked country in Africa, to Vietnam and Brazil, producers are now either reducing output or making plans to do so. “I wouldn’t want to get sensational about it but yes, clearly there must be a risk of shut-ins,” Mitch Flegg, the head of North Sea oil company Serica Energy, said in an interview. “In certain parts of the world it is a real and present risk.”

In emergency board meetings last week, oil companies small and large discussed an outlook that’s the most somber any oil executive has ever witnessed. For the small firms, the next few weeks will be all about staying afloat. But even for the bigger ones, like Exxon Mobil Corp. and BP Plc, it’s a challenge. Big Oil will offer an insight into the crisis when companies report earnings this week.

Then on Friday, May 1, Saudi Arabia, Russia and the rest of OPEC+ will join the output cuts, slashing their output by 23%, or 9.7 million barrels a day. Saudi Aramco, the state-owned company has already cut production, and Russian oil companies have announced exports of their flagship Urals crude would drop in May to a 10-year low.

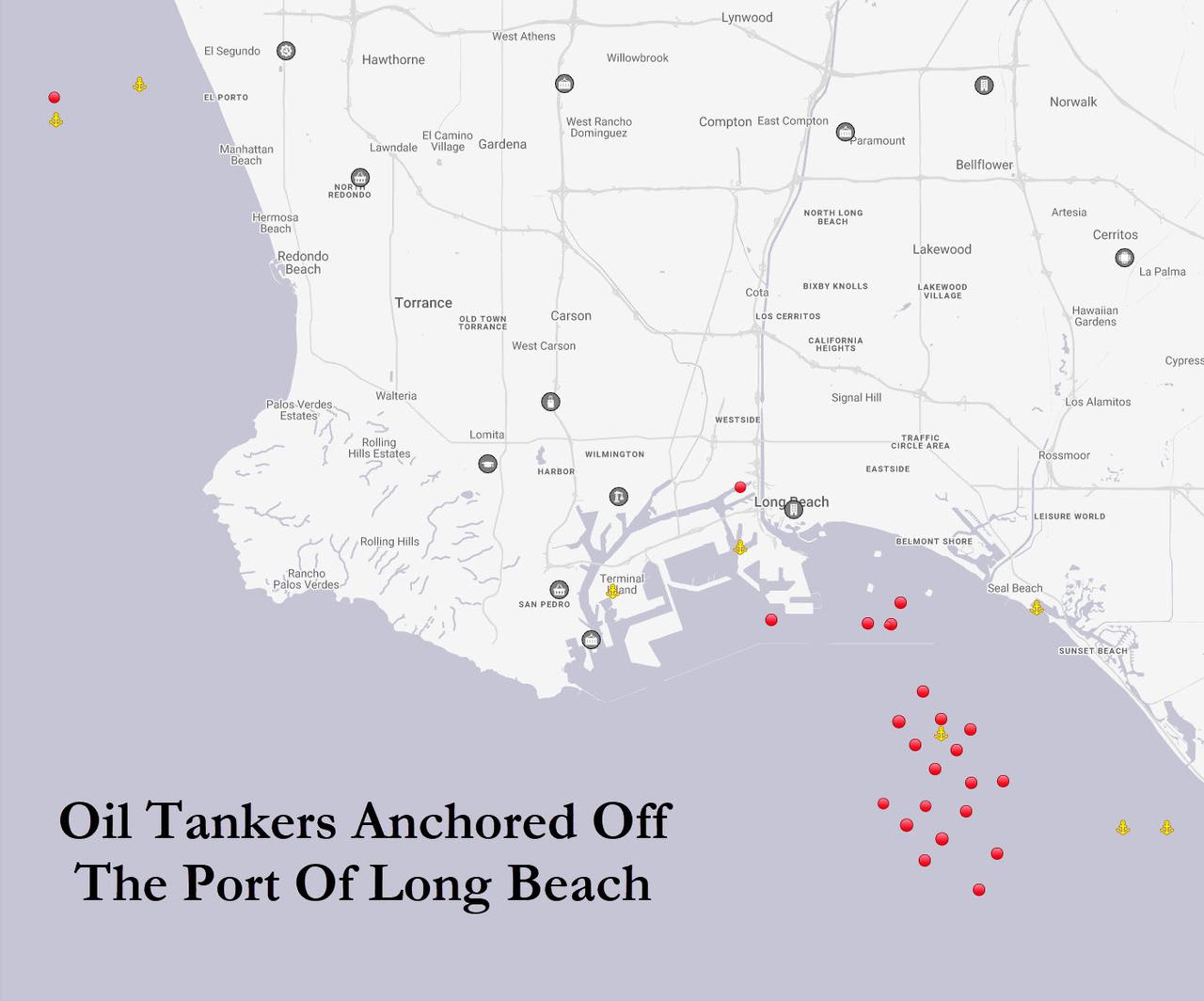

And yet, as warned here repeatedly, it may still not be enough, as every week, another 50 million barrels of crude are going into storage, enough to fuel Germany, France, Italy, Spain, and the U.K. combined, with estimates that the world will run out of land-based storage some time in late May or early June. Meanwhile, what’s not stored onshore, is stashed in tankers. As Bloomberg’s Blas points out, the U.S. Coast Guard on Friday said there were so many tankers at anchor off California that it was keeping an eye on the situation.

VIDEO: US Coast Guard says it’s keeping an eye on 27 oil tankers anchored off the coast of Southern California. Another great example of floating storage build-up as demand for oil and refined products plunge | #OOTT#Contango video via @USCGLosAngeles pic.twitter.com/B7pjWIsdnp

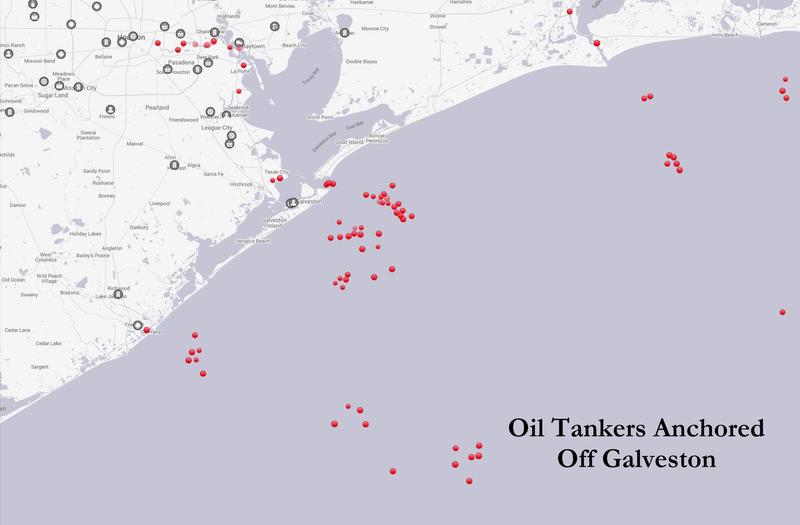

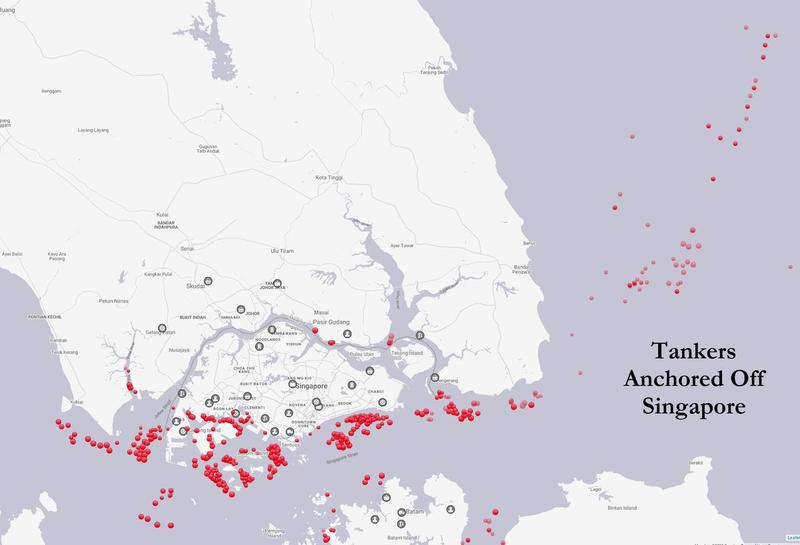

But if the two dozen or so tankers piled up off the coast of California is bad…

… and those next to Galveston, TX is worse…

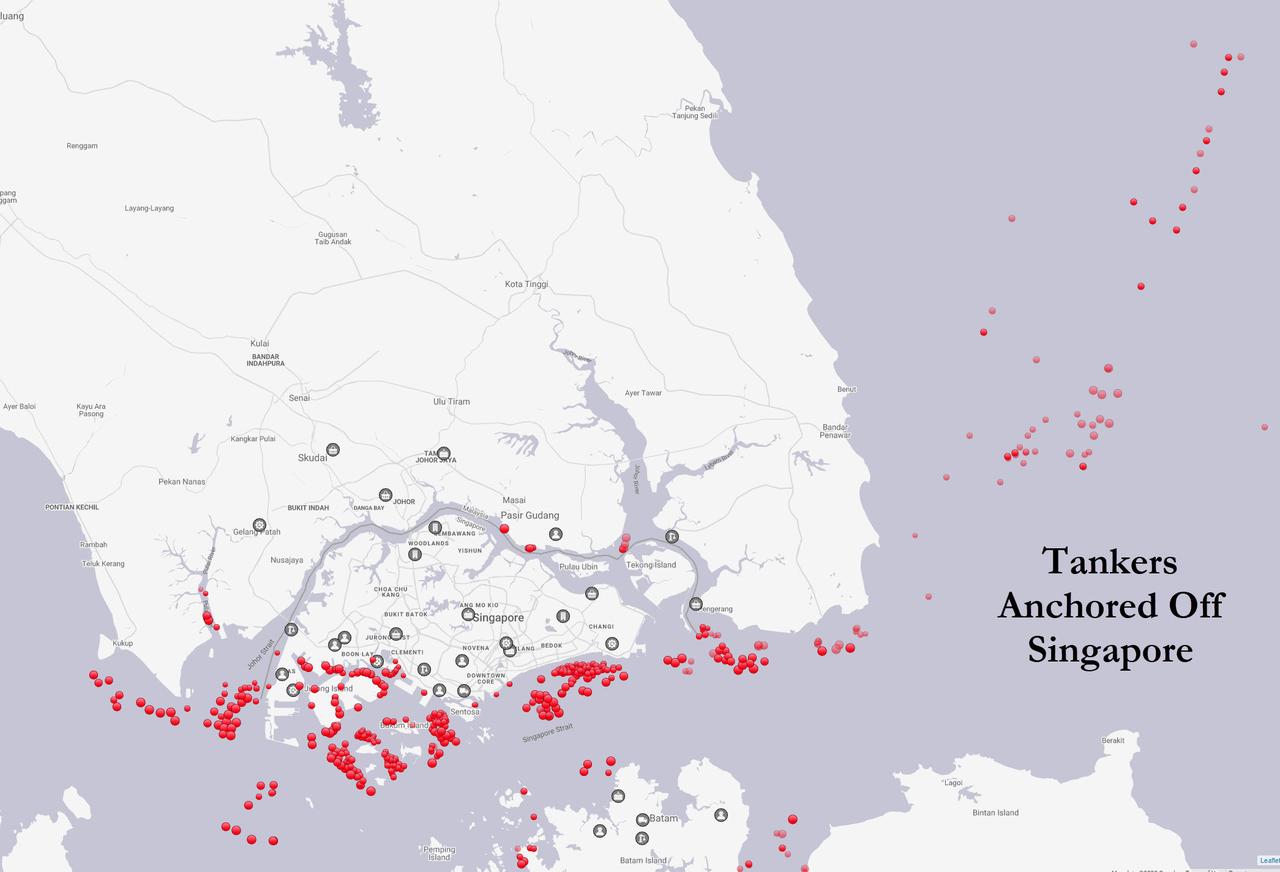

… what is going on in that tanker parking lot off of Singapore is absolutely insane.

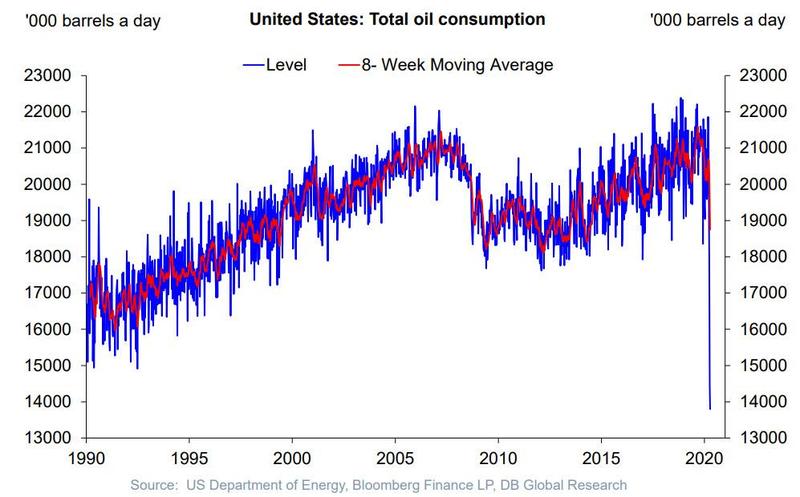

There is some good news: oil traders say after plunging by a third, US oil consumption has probably hit a bottom, and will start a very gentle recovery, although that also depends on how fast the US economy can reopen from the coronavirus coma.

But before even a modest recovery takes hold, the great shutdown will spread through oil refining too. Over the past week, Marathon Petroleum, one of the biggest U.S. refiners, announced it would stop production at a plant near San Francisco. Royal Dutch Shell has idled several units in three U.S. refineries in Alabama and Louisiana. And across Europe and Asia, many refineries are running at half rate. U.S. oil refiners processed just 12.45 million barrels a day on the week to April 17, the lowest amount in at least 30 years, except for hurricane-related closures.

The closures have already sent thousands packing: the oil and gas industry shed nearly 51,000 drilling and refining jobs in March, a 9% reduction that will only get worse in April. March’s job losses rise by 15,000 when ancillary jobs such as construction, manufacturing of drilling equipment and shipping are included, according to BW Research Partnership, a research consultancy, which analyzed Department of Labor data combined with the firm’s own survey data of about 30,000 energy companies.

“We’re looking at anywhere between five and seven years of job growth wiped out in a month,” Philip Jordan, the company’s vice president said in an interview. “What makes it sort of scary is this really is just the beginning. April is not looking good for oil and gas.”

And so, as the oil industry shuts down – at least for a few weeks (or perhaps months) – more refinery shutdowns are coming, oil traders and consultants said, particularly in the U.S. where lockdowns started later than in Europe and demand is still contracting. Steve Sawyer, director of refining at Facts Global Energy, said that global refineries could halt as much as 25% of total capacity in May.

“No one is going to be able to dodge this bullet.”

A historic crash in crude prices is driving U.S. shale into full-on retreat with operators halting new drilling and shutting in old wells, moves that could cut output by 20% for the world’s biggest producer of oil and leave thousands of workers unemployed.

For shale companies, the price of West Texas Intermediate crude went from hunker-down-and-ride-it-out mode to crisis mode in just a few days, with many now unsure whether there will even be a market for their oil. Some 1.75 million barrels a day is at immediate risk of shutting down while the number of new wells being brought online is forecast to plunge almost 90% by the end of the year, according to IHS Markit Ltd.

In short, it’s a swift and brutal end to the shale revolution, which only last year had President Donald Trump proclaiming “American Energy Dominance.”

West Texas Intermediate crude prices turned negative for the first time in history on Monday, meaning at one point sellers had to pay buyers to take it away. Then, the financial squeeze on the May contract spilled over to June and into the wider market, with prices now trading around $14 a barrel, well below the daily pumping cost in large swaths of America’s oil industry.

Even at $15, “everything back in the field, except the newest and most productive wells, is losing money on a cash-cost basis,” said Raoul LeBlanc, a Houston-based analyst at IHS Markit. “At this price you’ll start shutting in large amounts of production.”

It’s a bloodbath whichever way you look.

Operators are switching off wells, retiring one in three drill rigs, abandoning fracking, laying off 51,000 workers, slashing salaries and even going bankrupt just six weeks after the latest price plunge began. Now, with the coronavirus pandemic destroying demand, storage is just weeks away from filling up, a further factor choking back output.

Publicly-traded companies have axed more than $31 billion from drilling budgets, while distressed debt in the U.S. energy sector has jumped to $190 billion, up more than $11 billion in less than a week. Oil companies made up five of the top 10 issuers with the most distressed debt as of Tuesday. Evercore ISI reckons 5 million barrels a day, or around 40% of U.S. production, could be temporarily shut in by the end of June to help balance the market.

The potential for next to no revenue in the second and third quarters this year may mean that large U.S. oil explorers burn through $7 billion in cash, according Evercore. By the end of it all, as many as 30% of publicly traded shale explorers could be forced to exit the market one way or another, the Evercore analysts said.

For Gene Ames, an 85-year-old, fourth-generation oilman who was born in the East Texas oil rush during the Great Depression, when crude traded for 5 cents a barrel, it’s the worst crash he’s ever seen. “I’ve been through about six major busts and so far this is going to be the worst,” he said by telephone. “It’s the most intense, quickest and deepest collapse.”

The Saudi-Russia price war, which accelerated the price drop due to Covid-19, “has succeeded in hammering the last nail in the coffin of U.S. shale production and posed a major threat to the national security of the United States,” he said. He’s pushing the Texas Railroad Commission to impose mandatory production cuts. The commission deferred a decision on whether to do so on Tuesday.

Houston Economy

In Houston, America’s oil capital, the pain is set to reverberate across the broader economy.

The industry is far and away the “best paid” in the city, said Patrick Jankowski, an economist at the Greater Houston Partnership. “Someone who works on the blue-collar side can make $100,000 a year, so when those jobs go away it has a disproportionate impact on the economy.”

Now, the region needs to find its next growth engine. “Energy will still be important, but it’s going to be less important than before,” Jankowski said.

There’s little chance of relief any time soon. Oil traders are on a desperate questto find somewhere — anywhere, really — to store their crude as tanks from Texas to Siberia fill to capacity. Virtually all commercial onshore storage in the U.S. has been booked since the end of February, according to people with knowledge of the matter.

It will likely take months to clear the oversupply, with no clear end in sight for the pandemic’s effects.

“We’re all having to anticipate revenues that are significantly cut or just completely cut for an unforeseen period of time,” said Kyle Armstrong, president of Armstrong Energy Inc., a closely held producer on the New Mexico side of the Permian Basin. “Whether it’s negative $37 or $5, to me it doesn’t matter,” he added. “It’s effectively zero because I can’t operate wells productively at those prices.”

The first taps to be turned off will likely be the 1.75 million barrels a day from older, conventional U.S. wells that produce just a few dozen barrels a day each, according to IHS Markit’s LeBlanc. Producers will seek to ride out the storm with more productive wells providing some cash flow, even if made at a loss, in part due to the costs associated with shut-ins.

“The U.S. oil market actually gets worse fundamentally over the next month,” said Paul Sankey, a veteran oil analyst, in a note to clients. Producers have “nowhere to go with the inexorable production that takes weeks and months to reduce to zero.”

But the bigger problem for the shale industry is the lack of new wells being drilled. Shale wells decline by more than 60% in the first year, meaning new ones are needed to replaced production from old ones.

With few new wells coming online, IHS sees U.S. oil production declining to 10.1 million barrels a day by the end of the year, from 12.8 million barrels a day at the start. That will likely drop further to somewhere around 8.5 million barrels a day in 2021 to 2022, according to Noah Barrett, a Denver-based energy analyst at Janus Henderson.

“A good portion of production, particularly areas of the Bakken and Oklahoma, will go away completely,” said Barrett, whose employer manages $356 billion. “Fresh capital will be needed to grow off that lower base. But there’s zero appetite for that in the foreseeable future.”

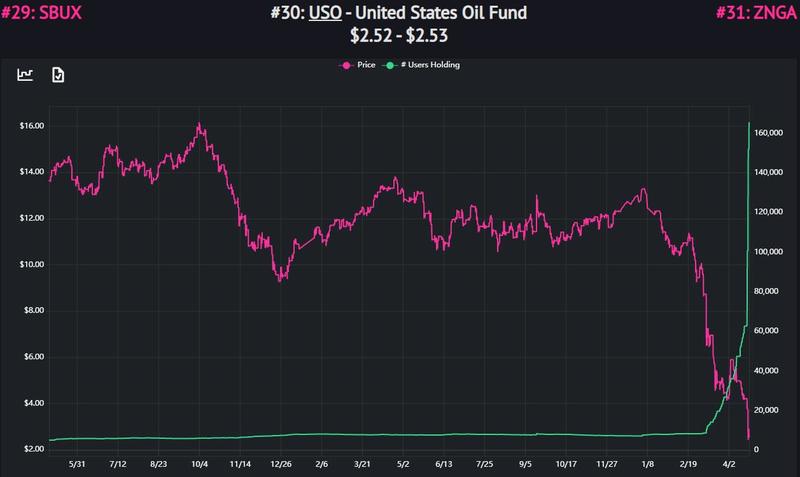

By now even the 165,727 “professional investors” who are long the USO ETF on the free, glitch-prone platform Robin Hood, are aware that the problem facing global oil production is that there is simply no storage where to put all the physical oil (as ZeroHedge warned in late March).

And if even the army of Robinhood-ers now know how impossible it is to find space for physical oil on the continental US, then Saudi Arabia – which sparked the current crude crisis and which will not stop until shale is completely crushed – is certainly aware.

Which is why with the US unable to store its own output, some 50 million barrels of Saudi oil are on their way to the United States and due to arrive in the coming weeks, piling even more pressure on markets already struggling to absorb a glut of stocks, Reuters and Marine Traffic reported.

Source: Marine Traffic

Shipping data showed the more than 20 supertankers – each capable of carrying 2 million barrels of oil – were sailing to key U.S. terminals, especially in the U.S. Gulf. Three separate tankers, also chartered by Saudi Arabia, were currently anchored outside U.S. Gulf ports.

According to Reuters sources, the kingdom had tried to seek storage options for the cargoes from tanker owners when the ships were chartered last month, but many pushed back given booming rates and not wanting tied up vessels.

The result was an outpouring of anger from the increasingly political hedge fund manager, Kyle Bass, who tweeted earlier that “the Saudis and Russians have declared war against US shale energy companies. It seems they weren’t happy with American energy independence. Storage full..largest glut in history..Saudis are sending us a 50 million barrel oil bomb. How negative will June crude go?”

The Saudis and Russians have declared war against US shale energy companies. It seems they weren't happy with American energy independence. Storage full..largest glut in history..Saudis are sending us a 50 million barrel oil bomb. How negative will June crude go? #Oil#USOILhttps://t.co/oiNfkI2pfM

The anger at the incoming Saudi “bomb” has spread all the way to Washington, and U.S. officials said in recent days that Washington is considering blocking Saudi shipments of crude oil, or putting tariffs on those shipments, adding to difficulties for the cargoes now on the water.

U.S. senator Ted Cruz said on Twitter on Tuesday: “My message to the Saudis: TURN THE TANKERS THE HELL AROUND.”

20 tankers—filled w/ 40mm barrels of Saudi oil—are headed to the US. This is SEVEN TIMES the typical monthly flow. At the same time, oil futures are plummeting & millions of US jobs in jeopardy. My message to the Saudis: TURN THE TANKERS THE HELL AROUND. https://t.co/gYoQzvHAEQ

In response, two sources said Saudi Arabia was looking into whether it could re-route the cargoes elsewhere if the United States halted imports.

Oil traders active in European and Asian markets said there was expectation that the Saudis would look to divert the cargoes to other markets if a ban was imposed… which in turn would put huge pressure on storage tanks in those two regions, and depress local oil benchmarks.

“Europe looks full, but surely if the Saudis offer it at really cheap levels, buyers would take it,” a source with an international trading firm told Reuters. “Some still have storage spaces or may agree to float it for some time.” A source at a separate oil trading firm active in Asia said they expected many of the barrels that were bound for the United States to flow to the region if exports were blocked.

* * *

“This could prove to be a very expensive exercise for Saudi Arabia as whatever happens with the cargoes and the tanker owners will need to be paid demurrage (for the ships) and those costs would have been locked in when the market was higher to secure the charters,” a shipping source said. “While this is an expensive gamble for the Saudis, shutting off production would have been proved even more costly.”

Additional costs – or demurrage – were estimated at $250,000 a day based on rates last month when a lot of vessels were booked. Daily tanker rates soared to nearly $300,000 in the past month and though they have retreated to $150,000 a day this week, they are still significant and would be in addition to other costs including insurance if the ships are held up.

Even if the Saudi tankers make it to the US, it is not clear who would want their cargo. With the economy shut down, driving virtually non-existent and gasoline demand falling off a cliff, refiners have been absent from oil markets in the United States in recent days as they slash processing rates and as demand dries up, physical oil market sources said. “There is more reluctance now with fresh shipments as refiners in the U.S. have no homes for the oil,” another shipping source said.

Marathon Petroleum, Exxon Mobil, Chevron and Phillips 66, which traditionally among the biggest U.S. buyers of Saudi crude, have gone radio silent.

As Reuters adds, most of the large buyers of Saudi oil are along the West Coast. The region accounts for about half of all Saudi crude imports to the United States, according to the EIA. Storage there was already 65% full as of April 10; two weeks later and that number is approaching100%. The Gulf Coast – which is the second biggest US destination for Saudi oil – was about 55% full.

The imminent arrival of the Saudi tankers comes at a time when the main U.S. storage hub in Cushing, OK, is expected to be full within weeks.

The question reached the very top on Monday, when President Trump said he would “look at” possibly stopping Saudi shipments to the United States. While it wasn’t clear what Trump had in mind, last week, Frank Fannon, the U.S. assistant secretary of state for energy resources, said tariffs were a possibility.

After the bloodbath caused by Saudi Arabia’s decision to ramp up output, European oil companies at first blush look enticingly cheap.

The Johan Sverdrup oil field in the North Sea, west of Stavanger, Norway, Getty Images

The dividend yield in BP, for example, is a mouth-watering 9.35%, according to FactSet Research. For perspective, the yield on a British 10-year gilt is 0.27%.

But with oil prices so low, how could BP possibly afford to pay such a dividend?

In a note to clients with little in the way of commentary, Morgan Stanley ran the numbers on what European major oil companies would look like with Brent crude at $35 a barrel.

Probably the most jarring numbers are the dividend cover at that level.

Equinor this year could cover just 1% of its dividend versus its previous estimate of 93%, according to the Morgan Stanley calculation of life at $35 a barrel.

The best positioned is OMV, which can still cover 107% of its dividend at $35, down from an estimated 198%.

BP’s dividend cover falls to 54% from 107%; Shell’s drops to 72% from 115%; Total’s goes to 62% from 125%; Eni’s drops to 57% from 87%; Repsol’s falls to 79% from 123%; and Galp’s drops to 52% from 115%.

Stock buybacks for the European major oil companies would drop by two-thirds on the Morgan Stanley numbers.

This comes as demand has been slashed due to the coronavirus outbreak

Prince Abdulaziz, energy minister of Saudi Arabia

Saudi Arabia will increase its oil output next month to more than 10 million barrels per day, following talks between OPEC and its allies which failed to come to an agreement.

KSA has cut its oil prices drastically, more than it has in 20 years, with discounts to buyers in Europe, the Far East, and the US meant to draw more refiners to Saudi crude rather than other crude oil suppliers.

Bloomberg reported that Saudi Arabia has privately said it could raise production to 12 million barrels per day, citing anonymous sources.

This comes as demand is slashed due to the ongoing coronavirus outbreak.

The Russian central bank opened its first overseas office in Beijing on March 14, marking a step forward in forging a Beijing-Moscow alliance to bypass the US dollar in the global monetary system, and to phase-in a gold-backed standard of trade.

According to theSouth China Morning Postthe new office was part of agreements made between the two neighbours “to seek stronger economic ties” since the West brought in sanctions against Russia over the Ukraine crisis and the oil-price slump hit the Russian economy.

According to Dmitry Skobelkin, the deputy governor of the Central Bank of Russia, the opening of a Beijing representative office by the Central Bank of Russia was a “very timely” move to aid specific cooperation, including bond issuance, anti-money laundering and anti-terrorism measures between China and Russia.

The new central bank office was opened at a time when Russia is preparing to issue its first federal loan bonds denominated in Chinese yuan. Officials from China’s central bank and financial regulatory commissions attended the ceremony at the Russian embassy in Beijing, which was set up in October 1959 in the heyday of Sino-Soviet relations. Financial regulators from the two countries agreed last May to issue home currency-denominated bonds in each other’s markets, a move that was widely viewed as intended to eventually test the global reserve status of the US dollar.

Speaking on future ties with Russia, Chinese Premier Li Keqiang said in mid-March that Sino-Russian trade ties were affected by falling oil prices, but he added that he saw great potential in cooperation. Vladimir Shapovalov, a senior official at the Russian central bank, said the two central banks were drafting a memorandum of understanding to solve technical issues around China’s gold imports from Russia, and that details would be released soon.

If Russia – the world’s fourth largest gold producer after China, Japan and the US – is indeed set to become a major supplier of gold to China, the probability of a scenario hinted by many over the years, namely that Beijing is preparing to eventually unroll a gold-backed currency, increases by orders of magnitude.

* * *

Meanwhile, as the Russian central bank was getting closer to China, China was responding in kind with the establishment of a clearing bank in Moscow for handling transactions in Chinese yuan. The Industrial and Commercial Bank of China (ICBC) officially started operating as a Chinese renminbi clearing bank in Russia on Wednesday this past Wednesday.

“The financial regulatory authorities of China and Russia have signed a series of major agreements, which marks a new level of financial cooperation,” Dmitry Skobelkin, the abovementioned deputy head of the Russian Central Bank, said.

“The launching of renminbi clearing services in Russia will further expand local settlement business and promote financial cooperation between the two countries,” he added according to.

Irina Rogova, a Russian financial analysttold the Russian magazine Expertthat the clearing center could become a large financial hub for countries in the Eurasian Economic Union.

* * *

Bypassing the US dollar appears to be paying off: according to the Chinese State Administration of Taxation, trade turnover between China and Russia increased by 34% in January, in annual terms. Bilateral trade in January 2017 amounted to $6.55 billion. China’s exports to Russia grew 29.5% reaching $3.41 billion, while imports from Russia increased by 39.3%, to $3.14 billion. Just as many suspected, with Russian sanctions forcing Moscow to find other trading partners, chief among which China, this is precisely what has happened.

The creation of the clearing center enables the two countries to further increase bilateral trade and investment while decreasing their dependence on the US dollar. It will create a pool of yuan liquidity in Russia that enables transactions for trade and financial operations to run smoothly.

In expanding the use of national currencies for transactions, it could also potentially reduce the volatility of yuan and ruble exchange rates. The clearing center is one of a range of measures the People’s Bank of China and the Russian Central Bank have been looking at to deepen their co-operation,Sputnik reported.

One of the most significant measures under consideration is the previouslyreported push for joint organization of trade in gold. In recent years, China and Russia have been the world’s most active buyers of the precious metal. On a visit to China last year, the deputy head of the Russian Central Bank Sergey Shvetsov said that the two countries want to facilitate more transactions in gold between the two countries.

“We discussed the question of trade in gold. BRICS countries are large economies with large reserves of gold and an impressive volume of production and consumption of this precious metal. In China, the gold trade is conducted in Shanghai, in Russia it is in Moscow. Our idea is to create a link between the two cities in order to increase trade between the two markets,” First Deputy Governor of the Russian Central Bank Sergey Shvetsov toldRussia’s TASS news agency.

In other words, China and Russia are shifting away from dollar-based trade, to commerce which will eventually be backstopped by gold, or what is gradually emerging as an Eastern gold standard, one shared between Russia and China, and which may day backstop their respective currencies.

Meanwhile, the price of gold continues to reflect none of these potentially tectonic strategic shifts, just as China – which has been the biggest accumulator of gold in recent years – likes it.

The Russian central bank sees several catalysts that could stop the oil rally in its tracks.

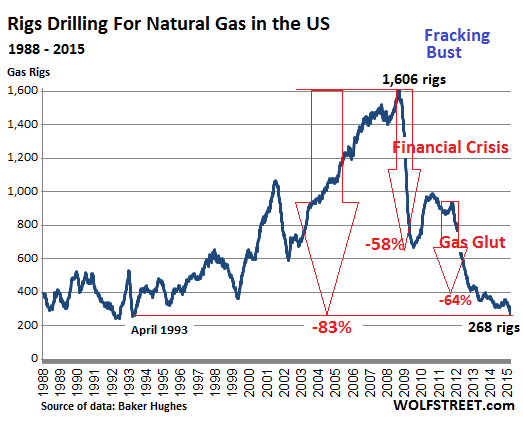

Bearish rig count report from Baker Hughes could signal a reverse in direction.

Supply will continue to increase rather than slow down in 2016 – even if there is a decline in shale production.

Battle for market share is one of the major catalysts not being considered.

I believe it’s very clear this oil rally is running on fumes and was never the result of an improvement in fundamentals. That means to me this rally is going to quickly run out of steam if it isn’t able to run up quicker on existing momentum. I don’t see that happening, and it could pull back dramatically, catching a lot of investors by surprise. The Russian central bank agrees, saying it doesn’t believe the price of oil is sustainable under existing market conditions.

Cited by CNBC, the Russian central bank said, “the current oil market still features a continued oversupply, on the backdrop of a slowdown in the Chinese economy, more supplies originating from Iran and tighter competition for market share.”

In other words, most things in the market that should be improving to support the price of oil aren’t. That can only mean one thing: a violent pullback that could easily push the price of oil back down to the $30 to $32 range. If the price starts to fall quickly, we could see panic selling driving the price down even further.

I think most investors understand this is not a legitimate rally when looking at the lack of change in fundamentals. I’ll be glad when the production freeze hoax is seen for what it is: a manipulation of the price of oil by staggered press releases meant to pull investors along for the ride. The purpose is to buy some time to give the market more time to rebalance. Once this is seen for what it really is, oil will plummet. It could happen at any time in my opinion.

Rig count increases for first time in three months

For the first time in three months, the U.S. rig count was up, increasing by one to 387. By itself this isn’t that important, but when combined with the probability that more shale supply may be coming to the market in 2016, it definitely could be an early sign of the process beginning.

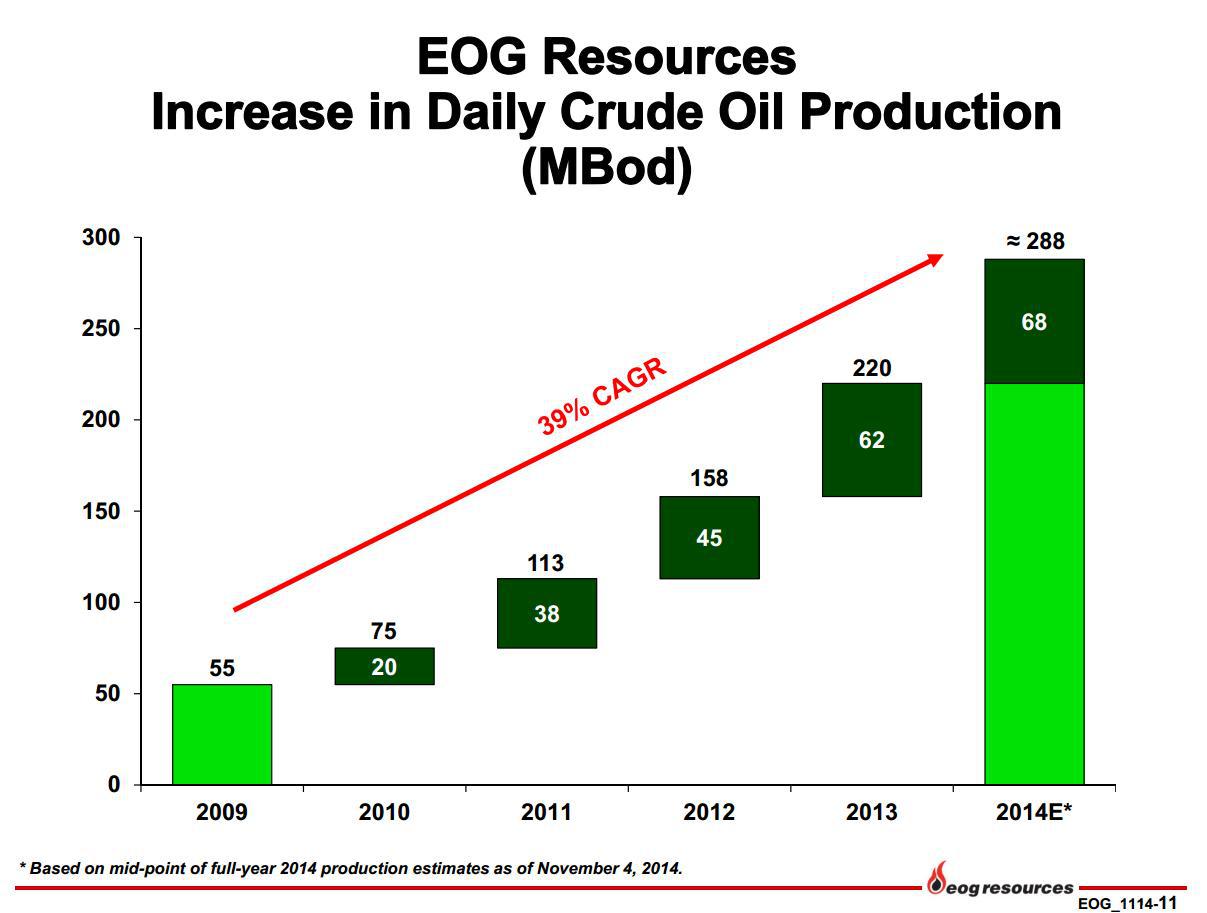

EOG Resources (NYSE:EOG) has stated it plans on starting up to 270 wells in 2016. We don’t know yet how much additional supply it represents, but it’s going to offset some of the decline from other companies that can’t continue to produce at these price levels. There are other low-cost shale producers that may be doing the same, although I think the price of oil will have to climb further to make it profitable for them, probably around $45 per barrel.

It’s impossible to know at this time if the increase in the price of oil was a catalyst, or we’ve seen the bottom of the drop in rig counts. The next round of earnings reports will give a glimpse into that.

Fundamentals remain weak

Most of the recent strength of the price of oil has been the continual reporting on the proposed production freeze from OPEC and Russia. This is light of the fact there really won’t be a freeze, even if a piece of paper is signed saying there is.

We know Iran isn’t going to agree to a freeze, and with Russia producing at post-Soviet highs and Iraq producing at record levels, what would a freeze mean anyway? It would simply lock in output levels the countries were going to operate at with or without an agreement.

The idea is the freeze is having an effect on the market and this will lead to a production cut. That simply isn’t going to happen. There is zero chance of that being the outcome of a freeze, if that ever comes about.

And a freeze without Iran isn’t a freeze. To even call it that defies reality. How can there be a freeze when the one country that would make a difference isn’t part of it? If Iran doesn’t freeze production, it means more supply will be added to the market until it reaches pre-sanction levels. At that time, all Iran has promised is it may consider the idea.

What does that have to do with fundamentals? Absolutely nothing. That’s the point.

Analysis and decisions need to be based on supply and demand. Right now that doesn’t look good. The other major catalyst pushing up oil prices has been the belief that U.S. shale production will decline significantly in 2016, which would help support oil. The truth is we have no idea to what level production will drop. It seems every time a report comes out it’s revised in a way that points to shale production remaining more resilient than believed.

I have no doubt there will be some production loss in the U.S., but to what degree there will be a decline, when considering new supply from low-cost shale companies, has yet to be determined. I believe it’s not going to be near to what was originally estimated, and that will be another element weakening support over the next year.

Competing for market share

One part of the oil market that has been largely ignored has been the competition for market share itself. When U.S. shale supply flooded the market, the response from Saudi Arabia was to not cede market share in any way. That is the primary reason for the plunge in oil prices.

There has been no declaration by the Saudis that they are going to change their strategy in relationship to market share and have said numerous times they are going to let the market sort it out, as far as finding a balance between supply and demand. So the idea they are now heading in a different direction is a fiction created by those trying to find anything to push up the price of oil.

It is apparent some of the reason for increased U.S. imports comes from Saudi Arabia in particular lowering its prices to nudge out domestic supply. It’s also why the idea of inventory being reduced in conjunction with lower U.S. production can’t be counted on. It looks like imports will continue to climb while shale production declines.

More competition means lower prices, although in this case, Saudi Arabia is selling its oil at different price points to different markets. It’s the average that matters there, and we simply don’t have the data available to know what that is.

In the midst of all of this, Russia is battling the Saudis for share in China, while the two also battle it out in parts of Europe, with Saudi Arabia looking to take share away from Russia. Some of Europe has opened up to competitors because it doesn’t want to rely too much on Russia as its major energy source.

For this and other competitive reasons, I could never trust a production freeze agreement if it ever came to fruition. They haven’t been adhered to in the past, and they won’t be if it happens again. Saudi Arabia has stated several times that it feels the same way.

Conclusion

To me the Russian central bank is spot on in saying the chance of a sustainable oil rally is slim. It also accurately pointed out the reasons for that: it’s about the lack of the fundamentals changing.

With U.S. inventory increasing, rig counts probably at or near a bottom, no end in sight to oversupply continuing, and competition for a low-demand market heating up, there is nothing I see that can justify an ongoing upward price move. I don’t even see it being able to hold.

A weaker U.S. dollar has legitimately helped some, but it can’t support the price of oil on its own. When all the other factors come together in the minds of investors, and the price of oil starts to reverse direction, there is a very strong chance a lot of bullish investors are going to get crushed hard. It is probably time to take some profits and run for the exit if you’re in the oil market for the short term.

Irrational Oil Optimists About To Experience Some Panic Selling Pain

Summary

Short-term positions in oil getting more risky.

U.S. production will outperform estimates as shale producers add supply to the market.

Inventory will come under more strain as key U.S. storage facilities approach full capacity.

Dollar weakness isn’t enough to maintain oil price momentum.

The longer the price of oil has upward momentum, and the higher it goes, the more risky it becomes for investors because there is nothing outside of a weakening U.S. dollar to justify any kind of move we’ve seen the price of oil make recently.

The falling dollar isn’t enough to keep the oil price from falling to where it belongs, and that means when the selloff begins, it’s likely to gravitate into full-panic mode, with sellers running for the exits before they get burned.

This is especially risky for those looking to make a quick windfall from the upward movement of oil. I’m not concerned about those taking long-term positions in quality energy companies with significant oil exposure, since they’ve probably enjoyed some great entry points. There is, of course, dividend risk, along with the strong probability of further share erosion before there is a real recovery that has legs to stand on because it’s based on fundamentals.

For that reason, investors should seriously consider taking profits off the table and wait for better conditions to re-enter.

Oil has become a fear play. Not the fear of losing money, but the fear of not getting in on the fast-moving action associated with the quick-rising price of oil. Whenever there is a fear play, it is ruled by emotion, and no amount of data will convince investors to abandon their giddy profits until they lose much, if not all, of what they gained. Don’t be one of them.

Having been a financial adviser in the past, I know what a lot of people are thinking at this time in response to what I just said. I’ve heard it many times before. It usually goes something like this: “What if the price of oil continues to rise and I lose a lot of money because of leaving the market too soon?” That’s a question arising from a fear mentality. The better question is this: “What if the oil price plunges and panic selling sets in?”

Oil is quickly becoming a casino play on the upside, and the longer investors stay in, the higher the probability they’ll lose the gains they’ve enjoyed. Worse, too much optimism could result in losses if preventative action isn’t taken quickly enough.

What needs to be considered is why one should stay in this market. What is so convincing it warrants this type of increasing risk, which offers much less in the way of reward than even a week ago? What fundamentals are in place that suggest a sustainable upward movement in the price of oil? The answer to those questions will determine how oil investors fare in the near future.

U.S. shale production

The more I think on the estimates associated with U.S. shale production in 2016, measured against the statements made by stronger producers that they’re going to boost supply from premium wells this year, the more I’m convinced it isn’t going to fall as much as expected. New supply will offset a lot of the less productive and higher cost wells being shuttered. I do believe there will be some loss of production from that, but not as much as is being suggested.

There are various predictions on how much production is going to be lost, but the general consensus is from 300,000 bpd to 600,000 bpd. It could come in on the lower side of that estimate, but I don’t think it’ll be close to the upper end of the estimate.

What is unknown because we don’t have an historical guideline to go by is, the amount of oil these premium wells will add to supply. We also don’t know if the stated goals will be followed up on. I think they will, but we won’t know for certain until the next couple of earnings reports give a clearer picture.

When combined with the added supply coming from Iran, and the ongoing high levels of production from Saudi Arabia, Russia and Iraq, I don’t see how the current support for the price of oil can continue on for any length of time.

There is no way of knowing exactly when the price of oil will once again collapse, but the longer it stays high without a change in the fundamentals, the higher the risk becomes, and the more chance it could swing the other way on momentum, even if it isn’t warranted. It could easily test the $30 mark again under those conditions.

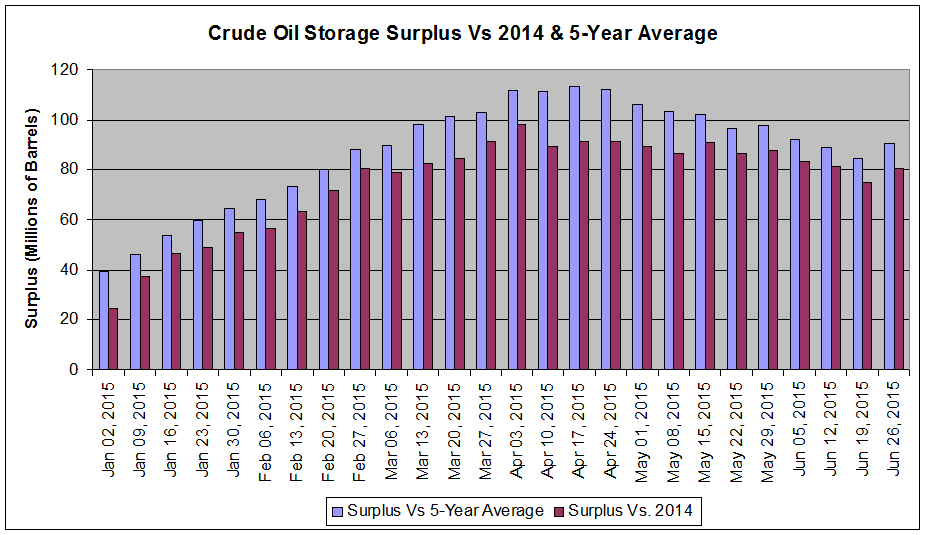

Inventory challenges

What many investors don’t understand about storage and inventory is it definitely matters where the challenges are located. That’s why Cushing being over 90 percent capacity and Gulf storage only a little under 90 percent capacity means more than if other facilities were under similar pressure. Together, they account for over 60 percent of U.S. storage.

With the imbalance of supply and demand driving storage capacity levels, the idea of oil staying above $40 per barrel for any period of time is highly unlikely. A lower U.S. dollar and the highly irrelevant proposed production freeze talks can’t balance it off.

Once the market digests this, which could happen at any time, we’ll quickly enter bear mode again. The problem is the price of oil is straining against its upper limits, and if momentum starts to deflate, the race to sell positions will become a sprint and not a marathon.

Uncertainty about shale is the wild card

As already mentioned, U.S. shale production continues to be the major catalyst to watch. The problem is we have no way of knowing what has already been unfolding in the first quarter. If investors start to abandon their positions, and we find shale supply is stronger than projected, it’ll put further downward pressure on oil after it has already corrected.

What I mean by that is we should experience some fleeing from oil before the next earnings reports from shale producers are released. If the industry continues to surprise on the upside of supply, it’ll cause the price of oil to further deteriorate, making the outlook over the next couple of months potentially ominous.

This isn’t just something that has a small chance of happening; it’s something that has a very strong probability of happening. Agencies like IEA have already upwardly revised their outlook for shale supply in 2016, and if that’s how it plays out, the entire expected performance for the year will have to be adjusted.

Conclusion

Taking into account the more important variables surrounding what will move the price of oil, shale production remains the most important information to follow. Not much else will matter if supply continues to exceed expectations. It will obliterate all the models and force analysts to admit this has little to do with prior supply cycles and everything to do with a complete market disruption. Many are still in denial of this. They’ll learn the reality soon enough.

That doesn’t mean there won’t eventually be a time when demand finally catches up with supply, but within the parameters of this weak global economy and oil supply that continues to grow, it’s going to take a lot longer to realize than many thought.

For several months, it has been understood that the market underestimated the expertise and efficiency of U.S. shale producers, and to this day they continue to do so. We will find out if that remains in play in the first half of 2016, and by then, whether it’ll extend further into 2017.

As for how it will impact the price of oil now, if we start to have some panic selling before the earnings reports, and the earnings reports of the important shale producers exceed expectations on the supply side, with it being reflected in an increase in the overall output estimates for the year, it will put more downward pressure on oil.

The other scenario is oil lingers around $40 per barrel until the earnings reports come out. There will still be a decline in the price of oil, the level of which would depend on how much more supply shale producers brought to the market in the first quarter than expected.

My thought is we’re going to experience a drop in the price of oil before earnings reports, which then could trigger a secondary exodus from investors in it for short-term gains.

For those having already generated some decent returns, it may be time to take it off the table. I don’t see how the shrinking reward can justify the growing risk.

The Mosul Dam in Iraq could collapse at any time, causing massive flooding across the country.

Iraq produces over four million barrels of oil per day, a number which will drop immediately when this event occurs.

The destruction of oil production in Iraq will immediately decrease world supply, lifting oil prices.

The Oil Situation: Since 2014, the oil market has been in a tailspin due to a multitude of global factors. As of March 2016, prices seem to have stabilized, although the persistence of crude oversupply continues to hang over the market. For months, declining US production and a potential output freeze by OPEC have been putting a potential floor in place. However, I believe an event is on the horizon which will change the equilibrium of oil prices immediately… the collapse of the Mosul Dam.

The Mosul Dam:The Mosul Dam is the largest dam in Iraq. It is located on the Tigris River in the western governance of Ninawa, upstream of the city of Mosul. Constructed in 1981, the dam has had a history of structural issues, requiring perpetual maintenance in order to maintain its integrity. Since 1984, this consisted of 300 man crews, working 24 hours a day across three shifts, filling holes in the bedrock through a process called grouting. For 30 years, this process worked, although it was always considered to be a ticking time bomb, dubbed “the most dangerous dam in the world” by the US Army Corps of Engineers.

In August 2014, the Islamic State of Iraq and the Levant took control of the dam, halting the maintenance process until it was retaken by Iraqi, Kurdish and US Forces two weeks later. Unfortunately, the damage was already done… since then, the maintenance crews have been limited to 30 personnel or less, and the equipment is inadequate to continue patching holes. Per the dam’s former chief engineer, Nasrat Adamo, “The machines for grouting have been looted. There is no cement supply. They can do nothing. It is going from bad to worse, and it is urgent. All we can do is hold our hearts.” As winter snows melt, the water levels will rise to unsustainable levels, and while it has two pressure release gates to avoid this scenario, one has been non-functioning for years, and using the second one alone risks the stability of the structure.

The Event: When the Mosul Dam collapses (and without reconstruction measures being implemented quickly, this is considered a ‘when’, not an ‘if’), a wave 45-65 feet high is expected to flood the country, drowning Mosul in four hours and reaching Baghdad within two to four days.

Estimates range from 500,000 to 1,500,000 lives lost. In addition to flooding, there will be secondary and tertiary effects… as demonstrated in America during Hurricane Katrina, panic and lawlessness can be equally as dangerous as the flooding itself, but even worse, diseases such as malaria and West Nile fever will follow. A catastrophic event of this magnitude will immediately push the entire country into chaos, and Iraq does not have the capability to respond without global support. The closest comparison to make is Haiti, which with billions in global assistance has not returned to normalcy in five years. Overall, I anticipate this catastrophe will take years to overcome… in the meantime, it will have a significant effect on the world’s supply of oil today.

The Effects:As of winter 2015, Iraq was producing 4.3M barrels per day, with the southern fields producing 3.3M barrels and the remaining 1M coming from the north. The graphic below (left) is from 2014, but gives a picture of the oil field placements. To the right is a topographical map, which gives us an idea of how the floodwaters will progress. Based on the elevation of where the flood would initiate, everything between Mosul and Baghdad will be completely covered, and while the wave will dissipate over time, the fields between Baghdad and Basra will see enough water (and everything that comes with it, to include bodies, disease and unexploded ordinance) to temporarily disable operations. Additionally, the pipeline between Kirkuk and Ramadi will be underwater, and there is a potential for damage to the Iraq Strategic Pipeline, which runs parallel to the direction of the water’s progression.

The world’s oversupply of oil is estimated around one million barrels per day. Assume that the above happens, and in a best-case scenario, only northern production is affected. What would occur immediately is the elimination of one quarter of Iraq’s oil output, rapidly pushing supply and demand into equilibrium. In a worst-case scenario, where all of Iraq’s oil is temporarily eliminated, it will move the supply deficit to three million barrels per day, leading to large ramifications on the world’s crude oil surplus within weeks.

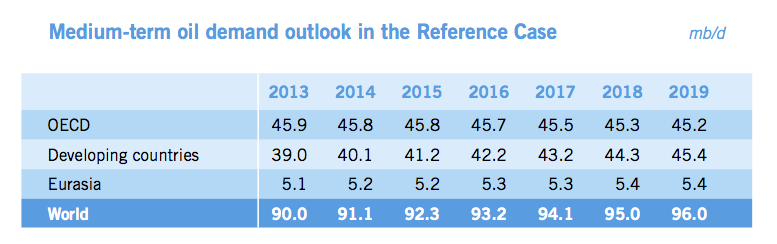

While the true answer lies somewhere between these possibilities, what is undeniable is that a catastrophe of this magnitude will immediately move the price of crude oil up, and depending on the timeline to return to today’s production levels, that move could be enormous. In late 2015, the world produced 97M barrels per day, causing the price to collapse to $26.00 per barrel. In 2014, while producing 93M barrels per day, the price averaged near $110.00 prior to its fall. Although the above is simple extrapolation, demand continues to grow, so I think we can all agree that the price shift north will be significant.

Conclusion: The subject of this article is admittedly morbid. The true fallout of this event is the loss of hundreds of thousands of Iraqi lives, and damage that would take years to erase. However, as informed investors, it would be irresponsible to not consider global events, and this has the potential to re-balance the oil market in a matter of days. When this occurs, over four million barrels per day can disappear from production, immediately shifting the direction of oil prices. Based on the above information, I believe a production cut decision by OPEC is irrelevant, as natural forces are preparing to address the oil oversupply on their own.

Last week, during the peak of the commodity short squeeze, we pointed out how this default cycle is shaping up to be vastly different from previous one: recovery rates for both secured and unsecured debts are at record low levels. More importantly, we noted how this notable variance is impacting lender behavior, explaining that banks – aware that the next leg lower in commodities is imminent – are not only forcing the squeeze in the most trashed stocks (by pulling borrow) but are doing everything in their power to “assist” energy companies to sell equity, and use the proceeds to take out as much of the banks’ balance sheet exposure as possible, so that when the default tsunami finally arrives, banks will be as far away as possible from the carnage. All of this was predicated on prior lender conversations with the Dallas Fed and the OCC, discussions which the Dallas Fed vocally denied accusing us of lying, yet which the WSJ confirmed, confirming the Dallas Fed was openly lying.

This was the punchline:

[Record low] recovery rate explain what we discussed earlier, namely the desire of banks to force an equity short squeeze in energy stocks, so these distressed names are able to issue equity with which to repay secured loans to banks who are scrambling to get out of the capital structure of distressed E&P names. Or as MatlinPatterson’s Michael Lipsky put it: “we always assume that secured lenders would roll into the bankruptcy become the DIP (debtor in possession) lenders, emerge from bankruptcy as the new secured debt of the company. But they don’t want to be there, so you are buying the debt behind them and you could find yourself in a situation where you could lose 100% of your money.“

And so, one by one the pieces of the puzzle fall into place: banks, well aware that they are facing paltry recoveries in bankruptcy on their secured exposure (and unsecured creditors looking at 10 cents on the dollar), have engineered an oil short squeeze via oil ETFs…

… to take advantage of panicked investors some of whom are desperate to cover their shorts, and others who are just as desperate to buy the new equity issued. Those proceeds, however, will not go to organic growth or even to shore liquidity but straight to the bank to refi loan facilities and let banks, currently on the hook, leave silently by the back door. Meanwhile, the new investors have no security claims and zero liens, are at the very bottom of the capital structure, and face near certain wipe outs.

In short, once the current short squeeze is over, expect everyone to start paying far more attention to recovery rates and the true value of “fundamentals.”

Going back to what Lipsky said, “the banks do not want to be there.” So where do they want to be? As far away as possible from the shale carnage when it does hit.

Today, courtesy of The New York Shock Exchange, we present just the case study demonstrating how this takes place in the real world. Here the story of troubled energy company “Lower oil prices for longer” Weatherford, its secured lender JPM, the incestuous relationship between the two, and how the latter can’t wait to get as far from the former as possible, in…

I am on record saying that Weatherford International is so highly-leveraged that it needs equity to stay afloat. With debt/EBITDA at 8x and $1 billion in principal payments coming due over the next year, the oilfield services giant is in dire straits. Weatherford has been in talks with JP Morgan Chase to re-negotiate its revolving credit facility — the only thing keeping the company afloat. However, in a move that shocked the financial markets, JP Morgan led an equity offering that raised $565 million for Weatherford. Based on liquidation value Weatherford is insolvent. The question remains, why would JP Morgan risk its reputation by selling shares in an insolvent company?

According to the prospectus, at Q4 2015 Weatherford had cash of $467 million debt of $7.5 billion. It debt was broken down as follows: [i] revolving credit facility ($967 million), [ii] other short-term loans ($214 million), [iii] current portion of long-term debt of $401 million and [iv] long-term debt of $5.9 billion. JP Morgan is head of a banking syndicate that has the revolving credit facility.

Even in an optimistic scenario I estimate Weatherford’s liquidation value is about $6.7 billion less than its stated book value. The lion’s share of the mark-downs are related to inventory ($1.1B), PP&E ($1.9B), intangibles and non-current assets ($3.5B). The write-offs would reduce Weatherford’s stated book value of $4.4 billion to – $2.2 billion. After the equity offering the liquidation value would rise to -$1.6 billion.

JP Morgan and Morgan Stanley also happen to be lead underwriters on the equity offering. The proceeds from the offering are expected to be used to repay the revolving credit facility.

In effect, JP Morgan is raising equity in a company with questionable prospects and using the funds to repay debt the company owes JP Morgan. The arrangement allows JP Morgan to get its money out prior to lenders subordinated to it get their $401 million payment. That’s smart in a way. What’s the point of having a priority position if you can’t use that leverage to get cashed out first before the ship sinks? The rub is that [i] it might represent a conflict of interest and [ii] would JP Morgan think it would be a good idea to hawk shares in an insolvent company if said insolvent company didn’t owe JP Morgan money?

The answer? JP Morgan doesn’t care how it looks; JP Morgan wants out and is happy to do it while algos and momentum chasing day traders are bidding up the stock because this time oil has finally bottomed… we promise.

So here’s the good news: as a result of this coordinated lender collusion to prop up the energy sector long enough for the affected companies to sell equity and repay secured debt, the squeeze may last a while; as for the bad news: the only reason the squeeze is taking place is because banks are looking to get as far from the shale patch and the companies on it, as possible.

We leave it up to readers to decide which “news” is more relevant to their investing strategy.

We grow up being taught a very specific set of principles.

One plus one equals two. I before E, except after C.

As we grow older, the principles become more complex.

Take economics for example.

The law of supply states that the quantity of a good supplied rises as the market price rises, and falls as the price falls. Conversely, the law of demand states that the quantity of a good demanded falls as the price rises, and vice versa.

These basic laws of supply and demand are the fundamental building blocks of how we arrive at a given price for a given product.

At least, that’s how it’s supposed to work.

But what if I told you that the principles you grew up learning is wrong?

With today’s “creative” financial instruments, much of what you learned no longer applies in the real world.

Especially when it comes to oil.

The Law of Oil

Long time readers of this Letter will have read many of my blogs regarding commodities manipulation.

With oil, price manipulation couldn’t be more obvious.

“…While agencies have found innovative ways to explain declining oil demand, the world has never consumed more oil.

In 2010, the world consumed a record 87.4 million barrels per day. This year (2014), the world is expected to consume a new record of 92.7 million barrels per day.

Global oil demand is still expected to climb to new highs.

If the price of oil is a true reflection of supply and demand, as the headlines tell us, it should reflect the discrepancy between supply and demand.

Since we know that demand is actually growing, that can’t be the reason for oil’s dramatic drop.

So does that mean it’s a supply issue? Did the world all of a sudden gain 40% more oil? Obviously not.

So no, the reason behind oil’s fall is not the causality of supply and demand.

The reason is manipulation. The question is why.

I go on to talk about the geopolitical reasons of why the price of oil is manipulated.

“On September 11, Saudi Arabia finally inked a deal with the U.S. to drop bombs on Syria.

But why?

Saudi Arabia possesses 18 per cent of the world’s proven petroleum reserves and ranks as the largest exporter of petroleum.

Syria is home to a pipeline route that can bring gas from the great Qatar natural gas fields into Europe, making billions of dollars for Saudi Arabia as the gas moves through while removing Russia’s energy stronghold on Europe.

Could the U.S. have persuaded Saudi Arabia, during their September 11 meeting, to lower the price of oil in order to hurt Russia, while stimulating the American economy?

… On October 1, 2014, shortly after the U.S. dropped bombs on Syria on September 26 as part of the September 11 agreement, Saudi Arabia announced it would be slashing prices to Asian nations in order to “compete” for crude market share. It also slashed prices to Europe and the United States.”

Following Saudi Arabia’s announcement, oil prices have plunged to a level not seen in more than five years.

Is it a “coincidence” that shortly after the Saudi Arabia-U.S. meeting on the coincidental date of 9-11, the two nations inked a deal to drop billions of dollars worth of bombs on Syria? Then just a few days later, Saudi Arabia announces a massive price cut to its oil.

Coincidence?

There are many other factors – and conspiracies – in oil price manipulation, such as geopolitical attacks on Russia and Iran, whose economies rely heavily on oil. Saudi Arabia is also flooding the market with oil – and I would suggest that it’s because they are rushing to trade their oil for weapons to lead an attack or beef up their defense against the next major power in the Middle East, Iran.

However, all of the reasons, strategies or theories of oil price manipulation could only make sense if they were allowed by these two major players: the regulators and the Big Banks.

How Oil is Priced

On any given day, if you were to look at the spot price of oil, you’d likely be looking at a quote from the NYMEX in New York or the ICE Futures in London. Together, these two institutions trade most of the oil that creates the global benchmark for oil prices via oil futures contracts on West Texas Intermediate (WTI) and North Sea Brent (Brent).

What you may not see, however, is who is trading this oil, and how it is being traded.

Up until 2006, the price of oil traded within reason. But all of a sudden, we saw these major price movements. Why?

“Until recently, U.S. energy futures were traded exclusively on regulated exchanges within the United States, like the NYMEX, which are subject to extensive oversight by the CFTC, including ongoing monitoring to detect and prevent price manipulation or fraud.

In recent years, however, there has been a tremendous growth in the trading of contracts that look and are structured just like futures contracts, but which are traded on unregulated OTC electronic markets. Because of their similarity to futures contracts they are often called ”futures look-a likes.”

The only practical difference between futures look-alike contracts and futures contracts is that the look-a likes are traded in unregulated markets whereas futures are traded on regulated exchanges.

The trading of energy commodities by large firms on OTC electronic exchanges was exempted from CFTC oversight by a provision inserted at the behest of Enron and other large energy traders into the Commodity Futures Modernization Act of 2000 in the waning hours of the 106th Congress.

The impact on market oversight has been substantial.

NYMEX traders, for example, are required to keep records of all trades and report large trades to the CFTC. These Large Trader Reports (LTR), together with daily trading data providing price and volume information, are the CFTC’s primary tools to gauge the extent of speculation in the markets and to detect, prevent, and prosecute price manipulation.

…In contrast to trades conducted on the NYMEX, traders on unregulated OTC electronic exchanges are not required to keep records or file Large Trader Reports with the CFTC, and these trades are exempt from routine CFTC oversight.

In contrast to trades conducted on regulated futures exchanges, there is no limit on the number of contracts a speculator may hold on an unregulated OTC electronic exchange, no monitoring of trading by the exchange itself, and no reporting of the amount of outstanding contracts (”open interest”) at the end of each day.

The CFTC’s ability to monitor the U.S. energy commodity markets was further eroded when, in January of this year (2006), the CFTC permitted the Intercontinental Exchange (ICE), the leading operator of electronic energy exchanges, to use its trading terminals in the United States for the trading of U.S. crude oil futures on the ICE futures exchange in London-called ”ICE Futures.”

Previously, the ICE Futures exchange in London had traded only in European energy commodities-Brent crude oil and United Kingdom natural gas. As a United Kingdom futures market, the ICE Futures exchange is regulated solely by the United Kingdom Financial Services rooority. In 1999, the London exchange obtained the CFTC’s permission to install computer terminals in the United States to permit traders here to trade European energy commodities through that exchange.

Then, in January of this year, ICE Futures in London began trading a futures contract for West Texas Intermediate (WTI) crude oil, a type of crude oil that is produced and delivered in the United States. ICE Futures also notified the CFTC that it would be permitting traders in the United States to use ICE terminals in the United States to trade its new WTI contract on the ICE Futures London exchange.

Beginning in April, ICE Futures similarly allowed traders in the United States to trade U.S. gasoline and heating oil futures on the ICE Futures exchange in London. Despite the use by U.S. traders of trading terminals within the United States to trade U.S. oil, gasoline, and heating oil futures contracts, the CFTC has not asserted any jurisdiction over the trading of these contracts.

Persons within the United States seeking to trade key U.S. energy commodities-U.S. crude oil, gasoline, and heating oil futures-now can avoid all U.S. market oversight or reporting requirements by routing their trades through the ICE Futures exchange in London instead of the NYMEX in New York.

As an increasing number of U.S. energy trades occurs on unregulated, OTC electronic exchanges or through foreign exchanges, the CFTC’s large trading reporting system becomes less and less accurate, the trading data becomes less and less useful, and its market oversight program becomes less comprehensive.

The absence of large trader information from the electronic exchanges makes it more difficult for the CFTC to monitor speculative activity and to detect and prevent price manipulation. The absence of this information not only obscures the CFTC’s view of that portion of the energy commodity markets, but it also degrades the quality of information that is reported.

A trader may take a position on an unregulated electronic exchange or on a foreign exchange that is either in addition to or opposite from the positions the trader has taken on the NYMEX, and thereby avoid and distort the large trader reporting system.

Not only can the CFTC be misled by these trading practices, but these trading practices could render the CFTC weekly publication of energy market trading data, intended to be used by the public, as incomplete and misleading.”

Simply put, any one can now speculate and avoid being tagged with illegal price. The more speculative trading that occurs, the less “real” price discovery via true supply and demand become.

With that in mind, you can now see how the big banks have gained control and cornered the oil market.

Continued from the Report:

“…Over the past few years, large financial institutions, hedge funds, pension funds, and other investment funds have been pouring billions of dollars into the energy commodities markets…to try to take advantage of price changes or to hedge against them.

Because much of this additional investment has come from financial institutions and investment funds that do not use the commodity as part of their business, it is defined as ”speculation” by the Commodity Futures Trading Commission (CFTC).

…Reports indicate that, in the past couple of years, some speculators have made tens and perhaps hundreds of millions of dollars in profits trading in energy commodities.

This speculative trading has occurred both on the regulated New York Mercantile Exchange (NYMEX) and on the over-the-counter (OTC) markets.

The large purchases of crude oil futures contracts by speculators have, in effect, created an additional demand for oil, driving up the price of oil to be delivered in the future in the same manner that additional demand for the immediate delivery of a physical barrel of oil drives up the price on the spot market.

As far as the market is concerned, the demand for a barrel of oil that results from the purchase of a futures contract by a speculator is just as real as the demand for a barrel that results from the purchase of a futures contract by a refiner or other user of petroleum.

Although it is difficult to quantify the effect of speculation on prices, there is substantial evidence that the large amount of speculation in the current market has significantly increased prices.

Several analysts have estimated that speculative purchases of oil futures have added as much as $20-$25 per barrel to the current price of crude oil, thereby pushing up the price of oil from $50 to approximately $70 per barrel.”

The biggest banks in the world, such as Goldman Sachs, Morgan Stanley, Citigroup, JP Morgan, are now also the biggest energy traders; together, they not only participate in oil trades, but also fund numerous hedge funds that trade in oil.

Knowing how easy it is to force the price of oil upwards, the same strategies can be done in reverse to force the price of oil down.

All it takes is for some media-conjured “report” to tell us that Saudi Arabia is flooding the market with oil, OPEC is lowering prices, or that China is slowing, for oil to collapse.

Traders would then go short oil, kicking algo-traders into high gear, and immediately sending oil down further. The fact that oil consumption is actually growing really doesn’t matter anymore.

In reality, oil price isn’t dictated by supply and demand – or OPEC, or Russia, or China – it is dictated by the Western financial institutions that trade it.

“For years, I have been talking about how the banks have taken control of our civilization.

…With oil prices are falling, economies around the world are beginning to feel the pain causing a huge wave of panic throughout the financial industry. That’s because the last time oil dropped like this – more than US$40 in less than six months – was during the financial crisis of 2008.

…Let’s look at the energy market to gain a better perspective.

The energy sector represents around 17-18 percent of the high-yield bond market valued at around $2 trillion.

Over the last few years, energy producers have raised more than a whopping half a trillion dollars in new bonds and loans with next to zero borrowing costs – courtesy of the Fed.

This low-borrowing cost environment, along with deregulation, has been the goose that laid the golden egg for every single energy producer. Because of this easy money, however, energy producers have become more leveraged than ever; leveraging themselves at much higher oil prices.

But with oil suddenly dropping so sharply, many of these energy producers are now at serious risk of going under.

In a recent report by Goldman Sachs, nearly $1 trillion of investments in future oil projects are at risk.

…It’s no wonder the costs of borrowing for energy producers have skyrocketed over the last six months.

…many of the companies are already on the brink of default, and unable to make even the interest payments on their loans.

…If oil continues in this low price environment, many producers will have a hard time meeting their debt obligations – meaning many of them could default on their loans. This alone will cause a wave of financial and corporate destruction. Not to mention the loss of hundreds of thousands of jobs across North America.”

You may be thinking, “if oil’s fall is causing a wave of financial disaster, why would the banks push the price of oil down? Wouldn’t they also suffer from the loss?”

Great question. But the banks never lose. Continued from my letter:

“If you control the world’s reserve currency, but slowly losing that status as a result of devaluation and competition from other nations (see When Nations Unite Against the West: The BRICS Development Bank), what would you do to protect yourself?

You buy assets. Because real hard assets protect you from monetary inflation.

With the banks now holding record amounts of highly leveraged paper from the Fed, why would they not use that paper to buy hard assets?

Bankers may be greedy, but they’re not stupid.

The price of hard physical assets is the true representation of inflation.

Therefore, if you control these hard assets in large quantities, you could also control their price.

This, in turn, means you can maintain control of your currency against monetary inflation.

And that is exactly what the banks have done.

The True World Power

Last month, the U.S. Senate’s Permanent Subcommittee on Investigations published a 403-page report on how Wall Street’s biggest banks, such as Goldman Sachs, Morgan Stanley, and JP Morgan, have gained ownership of a massive amount of commodities, food, and energy resources.

The report stated that “the current level of bank involvement with critical raw materials, power generation, and the food supply appears to be unprecedented in U.S. history.”

For example:

“…Until recently, Morgan Stanley controlled over 55 million barrels of oil storage capacity, 100 oil tankers, and 6,000 miles of pipeline. JPMorgan built a copper inventory that peaked at $2.7 billion, and, at one point, included at least 213,000 metric tons of copper, comprising nearly 60% of the available physical copper on the world’s premier copper trading exchange, the LME.

In 2012, Goldman owned 1.5 million metric tons of aluminum worth $3 billion, about 25% of the entire U.S. annual consumption. Goldman also owned warehouses which, in 2014, controlled 85% of the LME aluminum storage business in the United States.” – Wall Street Bank Involvement with Physical Commodities, United States Senate Permanent Subcommittee on Investigations

From pipelines to power plants, from agriculture to jet fuel, these too-big-to-fail banks have amassed – and may have manipulated the prices – of some of the world’s most important resources.

The above examples clearly show just how much influence the Big Banks have over our commodities through a “wide range of risky physical commodity activities which included, at times, producing, transporting, storing, processing, supplying, or trading energy, industrial metals, or agricultural commodities.”

With practically an unlimited supply of cheap capital from the Federal Reserve, the Big Banks have turned into much more than lenders and facilitators. They have become direct commerce competitors with an unfair monetary advantage: free money from the Fed.

Of course, that’s not their only advantage.

According to the report, the Big Banks are engaging in risky activities (such as ownership in power plants and coal mining), mixing banking and commerce, affecting prices, and gaining significant trading advantages.

Just think about how easily it would be for JP Morgan to manipulate the price of copper when they – at one point – controlled 60% of the available physical copper on the world’s premier copper trading exchange, the LME.

How easy would it be for Goldman to control the price of aluminum when they owned warehouses – at one point – that controlled 85% of the LME aluminum storage business in the United States?

And if they could so easily control such vast quantities of hard assets, how easy would it be for them to profit from going either short or long on these commodities?

Always a Winner

But if, for some reason, the bankers’ bets didn’t work out, they still wouldn’t lose.