While speaking through his face mask, China Joe was seen waving his hands around, one of them moving behind one of the microphones apparently being held by a reporter. Even though Biden’s image was clearly standing several feet away, his hand mysteriously moved to the reporter’s side of the mic, suggesting that some kind of green screen or superimposed imagery was used to create the fake footage.

Radicalized Christian President Donald Trump’s supporters storming the US Capitol. Samuel Corum/Getty Images

(Sophia Ankel) On the morning of the Capitol riot, Vern Swieringa told his wife during a walk with their dogs: “Something is going to happen today. I don’t know what, but something’s going to happen today.”

The Christian Reformed Church pastor from Michigan had been watching for months as some members of his congregation grew captivated by videos about the QAnon conspiracy theory on social media, openly discussing sex trafficking and Satan-worshipping pedophiles.

He had watched as other spiritual advisors, including the self-proclaimed “Trump Prophet” Mark Taylor, incorporated wild and dangerous QAnon beliefs into their sermons on YouTube and as organizers of the Christian Jericho March gathered in Washington, DC, days before the insurrection, urging followers to “pray, march, fast, and rally for election integrity.”

So when hundreds of President Donald Trump’s supporters stormed the Capitol hours after his premonition, Swieringa was shocked, but not surprised.

“I think some of the signs had been there all along, and it just all came to a perfect storm,” Swieringa told Insider.

(Chris Menahan) The Biden regime has signed off on new plans to conduct COVID-19 vaccine trials on infants and newborns — even though the CDC’s own data shows they face virtually zero risk of death from the virus.

The CDC’s data shows young people aged 0-19 have a 99.997% survival rate.

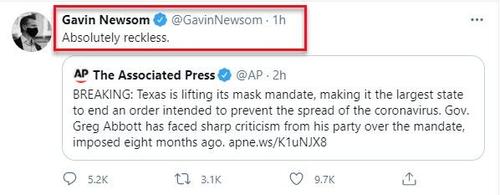

Shortly after Gov. Abbott’s decision to follow the science and allow the people of his state to be ‘free’ to judge their own risks once again, none other than California Gov. Newsom – desperate to virtue-signal as he fights for political survival amid an imminent recall vote – had a two word response: “Absolutely reckless”

During the debate last week over the Equality Act, a measure that would create a right to kill babies in abortions and force Americans to fund abortions, Republicans accused Democrats of ignoring Biblical values. And a surprising comment from pro-abortion Democrat Congressman Jerry Nadler confirmed that to be true.

(Sundance) It appears the bloom is off the ruse, at least with Sky News. In one of the first admissions to what is transparently obvious, an Australian news pundit finally points out that Joe Biden has cognitive issues. The vast majority of Americans already know this, but the U.S. media have been pretending not to know for well over a year. WATCH:

He may not have lost all his marbles, but there’s definitely a hole in the bag…

The false gospel of collectivism and the True Gospel of Jesus Christ cannot coexist.

Let’s skip the whole bloody Civil War thing and instead jump to the Reconstruction Era. The Cultural and Spiritual Civil War has been going on for decades. We are standing in the ashes of it now. Time to reconstruct, reform, and rebuild for the Glory of God.

(by Dave Hodges) This is a time of unprecedented evil on planet earth. Many Americans are looking for refuge and direction with regard to dealing with unprecedented tyranny in our present lifetimes. Historically, Americans look to their church for salvation and direction. However, most of today’s churches have been taken over from within by the very evil we fear. Many of your religious leaders have become the newest version of Benedict Arnold with regard to their faith. In short, most 501(c)(3) churches do NOT represent God. Judas sold out the savior of humanity, Jesus Christ, for a mere thirty pieces of silver. Today, many religious leaders are selling out their congregations for even less. This is not meant to imply that there are not religious leaders who hold steadfastly to the word of God and stand as a beacon of spiritual and moral courage before their congregations. However, an increasing number of clergy are more interested in serving the dictates of Homeland Security than they are in accurately espousing and exemplifying the word of God. This betrayal by the “earthly” pastors towards the word of God, is precisely what is keeping the church from launching a massive Christian revival that would turn back the evil that has taken over our country.

The Beehive State joins 16 other states that have adopted permitless constitutional concealed carry

(Frank Salvato) As the nation’s gun sales soar, the State of Utah has is set to adopt a permitless concealed carry system in which anyone legally permitted to own a firearm – from any state in the Union – can carry a firearm under his or her clothing while in the state.

(Tom Pappert) A 24-year-old man who says he graduated from college just before COVID-19 provoked massive lockdowns and a stagnant economy, now says that the cost of his insulin and other diabetic supplies have skyrocketed to $2,000. This comes after Joe Biden rescinded an executive order, signed by President Donald Trump, that lowered the cost of life sustaining insulin for low income Americans.

(Pam Key) Washington D.C. Mayor Muriel Bowser told “Just the News” on Friday that the Democratic-led Senate and House will vote in favor of statehood for the District of Columbia and send the bill to President Joe Biden’s desk, who has expressed support for D.C. statehood in the past.

Bowser said, “The nation’s capital, the federal enclave, continues to exist as the nation’s capital and everything outside of those new boundaries becomes the 51st state. Our congresswoman – we had our first successful vote on statehood in the House of Representatives last year. She reintroduced the bill. She has a record number of sponsors.”

She continued, “It is going to be reintroduced in the Senate in a couple of weeks, and we expect to have a favorable vote in the Senate as well, and then it goes to the president of the United States. We have made a big focus to President Biden to support D.C. statehood and make it part of his 100-day agenda.”

She added, “Just like you, we pay the same federal taxes as every citizen of the fifty states of the U.S. expect we do not have two senators. We literally have no one to speak for us in the Senate. We have to have full representation.”

(Tanay Warerkar) Yesterday, we reported that with in parallel with Andrew Cuomo’s decision to once again shut down indoor dining in New York starting Monday, more than half of the city’s restaurants are in danger of closing. Yet as Eater New York reports, many in the New York hospitality industry were dismayed by Cuomo’s decision as it followed close on the heels of new state data which showed that restaurants and bars in the state accounted for just 1.4% of cases over the last three months. While most were prepared for the ban to be announced this week, many felt the decision seemed to contradict the data.

If you are making less than $3,000 a month, you have plenty of company, because about half of the country is in the exact same boat. The Social Security Administration just released new wage statistics for 2019, and they are pretty startling. To me, the most alarming thing in the entire report is the fact that the median yearly wage was just $34,248.45 last year. In other words, half of all American workers made less than $34,248.45 in 2019, and half of all American workers made more than $34,248.45. That isn’t a whole lot of money. In fact, when you divide $34,248.45 by 12 you get just $2,854.05.

(Stewart Jones) As the Federal Reserve’s quantitative easing practices generate the biggest debt bubble in history, gold futures are trading at record highs, a phenomenon some have called “a bit of a mystery.” However, this “mystery” was solved long ago by the laws of economics. The only “mystery” here is why—contrary to centuries of economic wisdom—we allowed centralized paper money to become the dominant form of currency in the first place.

As recent waves of civil unrest and economic turmoil have prompted some to look back in time and reflect on the observations of the Founding Fathers, it seems most have opted to reject them entirely. Yet among the founders’ many warnings against the institutions that would eventually dominate the modern world are the timeless—and astonishingly accurate—warnings against central banking.

On August 1, 1787, George Washington wrote in a letter to Thomas Jefferson that “paper currency [can] ruin commerce, oppress the honest, and open the door to every species of fraud and injustice.” Jefferson also opposed the concept, warning that “banking establishments are more dangerous than standing armies.” James Madison called paper money “unjust,” recognizing that it allowed the government to confiscate and redistribute property through inflation: “It affects the rights of property as much as taking away equal value in land.”

In other words, inflation is a hidden form of taxation. Washington understood this. Jefferson understood this. Madison understood this. And generations of preeminent economists since then—from Ludwig von Mises to F.A. Hayek, to Murray Rothbard—have understood this quite clearly.

And there’s nothing controversial or mysterious about sound money, that is, currency backed by some form of secure, fixed weight commodity like gold or silver. Both have been valued in some fashion for six thousand years and have been used as currency for around twenty-six hundred years. As confidence in the dollar continues to nosedive, the market is not only putting more confidence in gold and silver, but in some crypto currencies sharing many of the characteristics of gold.

The presidencies of Woodrow Wilson and Franklin D. Roosevelt are rightfully regarded as some of the darkest years for freedom in America. Often overlooked, however, are the deeply repressive monetary policies introduced by both presidents. In 1838, Senator John C. Calhoun foreshadowed the economic evils that would eventually emerge at the peak of the Progressive Era, explaining,

“It is the nature of stimulus…to excite first, and then depress afterwards….Nothing is more stimulating than an expanding and depreciating currency. It creates a delusive appearance of prosperity, which puts everything in motion. Everyone feels as if he was growing richer as prices rise.”

Seventy-five years later, the autocrats running the Wilson administration dealt two devastating blows to liberty with the Federal Reserve Act and the Revenue Act, forever marking 1913 as a tragic year for liberty. Both laws struck at the heart of property rights by establishing the Federal Reserve System and the income tax, respectively. Then, in 1933, Roosevelt issued Executive Order No. 6102, requiring Americans to surrender much of their gold to the US government. Shortly after, Congress passed the Gold Reserve Act of 1934, artificially raising the price of gold and guaranteeing the government a profit of $14.33 for each ounce of gold it had seized from the people.

Finally, in 1971, President Richard Nixon—like any self-respecting twentieth-century Keynesian—committed himself to finishing the work of Wilson and Roosevelt by closing the gold window, forever divorcing the gold standard from the dollar. Rather than usher in a new era of economic stability, this unnatural union between the Fed and the federal government produced a vicious loop of boom-bust cycles and depressions. The consequences have not only been inflation and devaluation (both of which have stripped the people of their purchasing power and savings); now, every time a depression hits, the government is allowed to do two things: grow its power and tax and spend at will without fear of accountability.

In other words, with every inflation of currency comes an inflation of government power.

With government shutdowns of local economies, the second economic quarter of this year was among the worst in history, with the total debt-to-GDP reaching a staggering 136 percent. As the national debt approaches $27 trillion (with even bigger spending bills in the works), we can expect the days of such flagrant government spending to come to a screeching halt. If we continue on this path, that correction will result in an unprecedented collapse of the dollar and the monetary system. The ultimate danger in this scenario: the government eventually confiscates the vast majority or even all private property in order to pay off the national debt. As German American economist Hans Sennholz once said, “Government debt is a government claim against personal income and private property—an unpaid tax bill.”

This is why a dramatic downsizing of government is key to bringing the US out of this manic, outmoded cycle of depressions and upswings. For the government to fulfill its core function as a safeguard of liberty, we must prevent it from meddling in affairs beyond the boundaries prescribed by the Founding Fathers. This includes a swift withdrawal from the use of paper fiat currency and spending cuts across the board.

Such a sweeping transformation could begin with the state governments, the legislatures of which could override the federal government by passing legislation allowing individuals to use gold and silver currency.

Regardless, if meaningful legislative action is not taken somewhere, we have little choice other than to acquiesce to the gloom and terror of socialism—a system that would devour all in its path and make slaves of once free people for generations to come. Freedom is the natural ability of people to control their own destiny. Sound money has the ability to help keep people free.

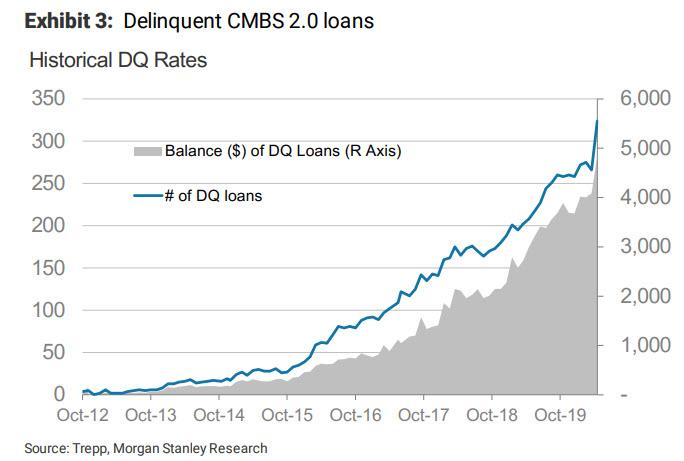

Even before the coronavirus pandemic, US malls were in a crisis, with vacancies in January hitting a record high.

However, in the post-corona world, commercial real estate has emerged as one of the most adversely impacted sectors (perhaps because the Fed has so far refused to bail it out), with the number of new delinquencies soaring to a record high in recent weeks.

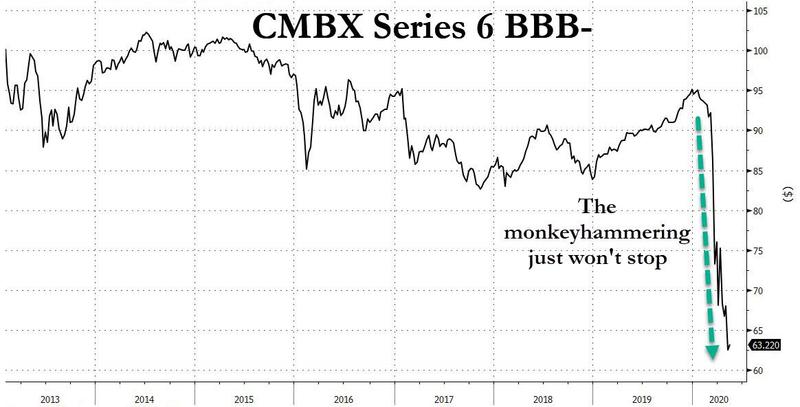

The gloom facing malls has also helped push the Big Short trade, which was the CMBX Series 6 BBB- tranche (the one with the most exposure to malls), to a fresh all time low last week.

And now, the implosion of the US retail sector has reached the very top, because according to Bloomberg The Mall of America, the largest US shopping center, has missed two months of payments for a $1.4 billion commercial mortgage-backed security, in confirmation that no business is immune to the devastating consequences of the coronavirus.

“The loan is currently due for the April and May payments,” according to a report filed by the trustee of the debt, Wells Fargo & Co., which is also the master servicer for the loan. “Borrower has notified master servicer of Covid-19 related hardships.”

Mall owners reported rock-bottom April rent collections, including about 12% for Tanger Factory Outlet Centers Inc., roughly 20% for Brookfield Property Partners LP and 26% for Macerich. Retailers and their landlords, hurt by competition from online stores before coronavirus-spurred shutdowns made things worse, are struggling to make rent and mortgage payments.

The 5.6 million-square-foot (520,000-square-meter) mall was ordered closed on March 17, and has announced plans to begin reopening on June 1, starting with retailers, followed later by food services and attractions, such as the mega-mall’s aquarium, cinema, miniature golf course and indoor theme park.

“Reopening a building the size of Mall of America is no small task, but we are confident taking the necessary time to reopen will help us create the safest environment possible,” the mall said in a statement on its website.

The Mall of America is owned by members of the Ghermezian family, whose holdings also include the West Edmonton Mall, a 5.3 million-square-foot complex in their Canadian hometown, and American Dream, a 3 million-square-foot mall in East Rutherford, New Jersey.

Once the government’s ability to sustain its enforcement with money created out of thin air vanishes, the entire order vanishes along with it.

The era of waste, greed, fraud and living on borrowed money is dying, and those who’ve known no other way of living are mourning its passing. Its passing was inevitable, for any society that squanders its resources is unsustainable. Any society that makes private greed the primary motivator and priority is unsustainable. Any society that rewards fraud above all else is unsustainable. Any society which lives on money borrowed from the future and other forms of phantom capital is unsustainable.

We know this in our bones, but we fear the future because we know no other arrangement other than the unsustainable present. And so we hear the faint echo of the cries of alarm filling the streets of ancient Rome when the Bread and Circuses stopped: what do we do now?

When the free bread and entertainments disappeared, people found new arrangements. They left Rome.

The greatest private fortunes in history vanished as Rome unraveled. All the land, the palaces, the gold and all the other treasures were no protection against the collapse of the system that institutionalized corruption as the ultimate protector of concentrated wealth.

The most zealously guarded power of government is the creation of money, for without money the government cannot pay the soldiers, police, courts and administrators needed to enforce its rule. Western Rome created money by controlling silver mines; in the current era, governments create money (currency) out of thin air.

Once the government’s money loses purchasing power, the system collapses. And so in the final stages of Rome’s decline, Imperial orders still flowed to distant legions, but the legions no longer existed; they were only phantom entries on Imperial ledgers.

Our “money” is also nothing but phantom entries on digital ledgers, and so its complete loss of purchasing power is inevitable.

Without “money,” the government can no longer enforce the will of its self-serving elites: orders will still flow in a furious flood to every corner of the land, but the legions to enforce the institutional corruption will be nothing but phantom entries on Imperial ledgers.

Once the government’s ability to sustain its enforcement with money created out of thin air vanishes, the entire order vanishes along with it. The destruction of the value of central bank-created “money” is already ordained, for there is no limit on human greed and the desire to maintain control, and so governments will create their “money” in ever-increasing amounts until the value has been completely leached from the phantom digital entries.

The outlines of a better world are emerging, an arrangement that prioritizes something more than maximizing private gain and institutionalizing the corruption needed to protect those gains. We will relearn to live within our means, and relearn how to institutionalize opportunity rather than corruption designed to protect elites.

We will come to a new understanding of the teleology of centralized power, that centralized power only knows how to extend its power and so the only possible outcome is collapse.

We will come to understand technology need not serve only monopolies, cartels and the state, that it could serve a sustainable, decentralized economy that does more with less, i.e. a DeGrowth economy.

The Federal Reserve will fail, just as the Roman gods failed to sustain the corrupt and bankrupt Roman elites. A host of decentralized, transparently priced non-state currencies will compete on the open market, just like goods, services and commodities. The Fed’s essential role– serving the few at the expense of the many, under the cover of creating currency out of thin air–will be repudiated by the implosion of the economy as all the Fed’s phantom “wealth” evaporates.

The outlines of a better world are emerging. Do you discern them through the smoke as the last frantic phantoms of an unsustainable system issue orders to reverse the tides of history as they dissipate into thin air?

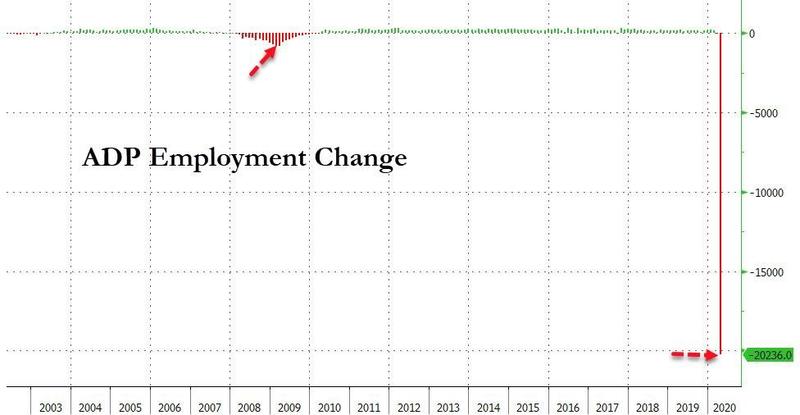

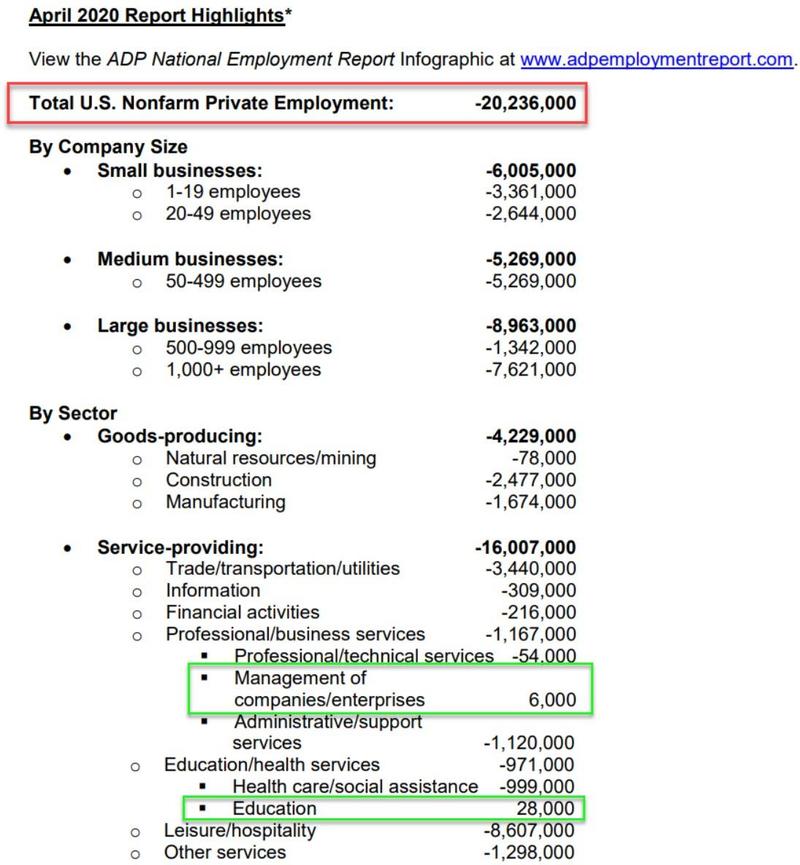

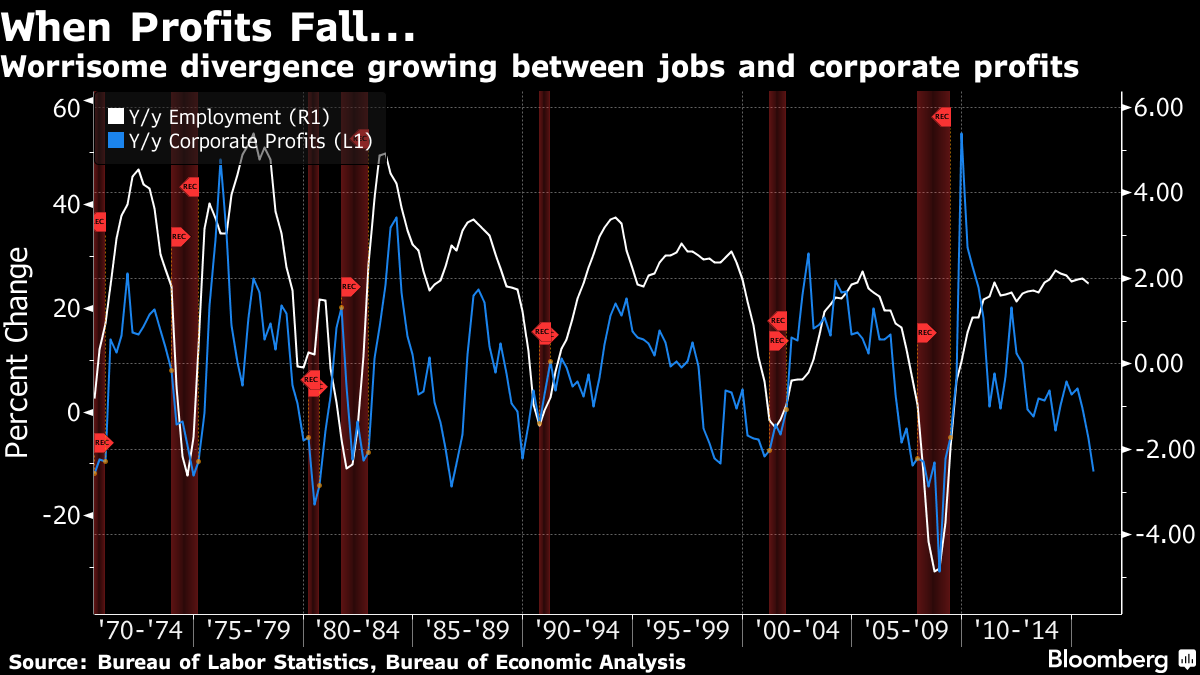

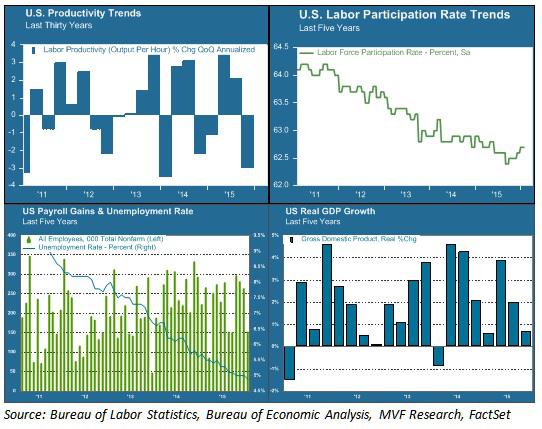

Given the fact that over 30 million Americans have filed for initial jobless claims in the last six weeks, it is perhaps no surprise that economists expected a 20.5 million ADP job loss in April. In fact, silver lining, the number ‘beat’ with 20.236 million.

For context, the largest monthly job loss during the great financial crisis was just 834,700!

Large- and mid-sized companies saw the biggest job-losses…

And the service sector saw the biggest job losses…

If you’re an educator or in “management”, it would appear times remain good…

“Job losses of this scale are unprecedented. The total number of job losses for the month of April alone was more than double the total jobs lost during the Great Recession,” said Ahu Yildirmaz, co-head of the ADP Research Institute.

“Additionally, it is important to note that the report is based on the total number of payroll records for employees who were active on a company’s payroll through the 12th of the month. This is the same time period the Bureau of Labor and Statistics uses for their survey.”

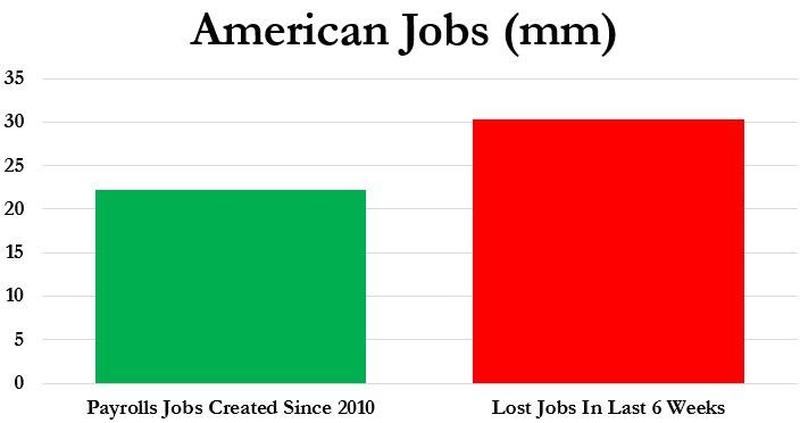

And as we noted previously, far more Americans have lost their jobs in the last month than jobs gained during the last decade since the end of the Great Recession… (22.13 million gained in a decade, 30.3 million lost in 6 weeks)

Worse still, the final numbers will likely be worsened due to the bailout itself: as a reminder, the Coronavirus Aid, Relief, and Economic Security (CARES) Act, passed on March 27, could contribute to new records being reached in coming weeks as it increases eligibility for jobless claims to self-employed and gig workers, extends the maximum number of weeks that one can receive benefits, and provides an additional $600 per week until July 31. A recent WSJ article noted that this has created incentives for some businesses to temporarily furlough their employees, knowing that they will be covered financially as the economy is shutdown. Meanwhile, those making below $50k will generally be made whole and possibly be better off on unemployment benefits.

As Mises’ Robert Aro noted earlier in the week, the stimulus packages being handed out across this world provide us with an opportunity to document the anti-capitalist process as it unfolds in real time, keeping in mind that when these inflation schemes fail, it will likely be blamed on capitalism.

The combination of increasing the money supply in order to pay people not to produce goods or services has consequences that not a lot of people are talking about.

It flies in the face of the free market and is as nonsensical as a negative interest rate. A loan that is forgivable is unconventional to say the least, because a loan is normally defined as an amount borrowed that is expected to be paid back with interest. When a loan is given on a first-come-first-served basis for the purpose of paying people not to work and is forgivable because it’s guaranteed by the United States government, we shouldn’t call it a loan.

It may be called socialism, maybe interventionism, and some may still prefer the term statism; but one thing is certain when it comes to the Paycheck Protection Program: it’s not capitalism!

Welfare cliffs are of course not the only reason so many capable Americans languish in partial dependency on government assistance. Dreadful government schools in poor areas and systematic obstacles to getting a job, such as minimum wage laws and occupational licensing laws, are also to blame. But the perverse incentives of America’s welfare system really hurt, and the CARES Act may have been a serious tipping point.

But, hey, there’s good news… well optimistic headlines as Treasury Secretary Steven Mnuchin said he anticipates most of the economy will restart by the end of August.

Finally, it is notable, we have lost 434 jobs for every confirmed US death from COVID-19 (60,999).

Was it worth it?

You will have only two choices now: do hard things, or submit to Globohomo. What are you doing today to prepare yourself and your people for Hard Tasks?

President Trump’s trade war is back. It’s an election year, and the efforts by the administration to ‘turbocharge’ an initiative to deglobalize that world by removing critical supply chains from China could be seen with new rounds of tariffs to strike Beijing for its handling of the COVID-19 outbreak, US officials told Reuters.

It’s clear that coronavirus lock downs have resulted in a crashed economy with more than 30 million people unemployed have derailed President Trump’s normal campaigning process and the promises of a vibrant economy. This could suggest President Trump is about to unleash tariff hell on Beijing as it would do two things: First, it would pressure US companies with supply chains in China to exit, and second, the president can say the tariffs are a punishment for the more than 68,000 Americans that have died from the virus.

“We’ve been working on [reducing the reliance of our supply chains in China] over the last few years but we are now turbocharging that initiative,” Keith Krach, undersecretary for Economic Growth, Energy and the Environment at the U.S. State Department told Reuters.

“I think it is essential to understand where the critical areas are and where critical bottlenecks exist,” Krach said, adding that the matter was key to U.S. security and one the government could announce new action on soon.

Current and former officials said the Commerce Department and other federal agencies are investigating ways to push US companies away from sourcing and manufacturing in China. “Tax incentives and potential re-shoring subsidies are among measures being considered to spur changes,” they said.

“There is a whole of government push on this,” said one. Agencies are probing which manufacturing should be deemed “essential” and how to produce these goods outside of China.

Another official said, “this moment is a perfect storm; the pandemic has crystallized all the worries that people have had about doing business with China.”

“All the money that people think they made by making deals with China before, now they’ve been eclipsed many-fold by the economic damage” from the coronavirus, the official said.

Amid a pandemic and recession, it appears the comments from US officials suggest geopolitics could soon become major headaches for global markets. President Trump’s latest comments have stirred new concerns that an economic war with China is about to restart. This could be potentially dangerous for investors who are looking for V-shaped recoveries.

Last week, President Trump said China “will do anything they can” to make him lose his re-election bid in November. He said Beijing faced a “lot” of possible consequences for the virus outbreak.

He told Reuters: “There are many things I can do. We’re looking for what happened.”

President Trump recently said he could slap new tariffs of up to 25% tax on $370 billion in Chinese goods currently in place. Officials said the president could introduce new sanctions on officials or companies or project closer relations with Taiwan, all moves that would infuriate Beijing.

Secretary of State Mike Pompeo recently said the administration is working with allies, including Australia, India, Japan, New Zealand, South Korea, and Vietnam, to “move the global economy forward.”

Conversations among US officials have so far been about “how we restructure … supply chains to prevent something like this from ever happening again,” Pompeo said.

And it appears Beijing is preparing for President Trump to strike. We noted on Monday that Chinese President Xi Jinping is preparing for a worst-case scenario of armed conflict with the US.

For years, we have documented the possibility of Thucydides Trap playing out between the US and China. That is when a dominant regional power (the US) feels threatened by the rise of a competing power (China). Read:

“For a successful technology, reality must take precedence over public relations, for Nature cannot be fooled.” – Richard Feynman – Rogers Commission

“It appears that there are enormous differences of opinion as to the probability of a failure with loss of vehicle and of human life. The estimates range from roughly 1 in 100 to 1 in 100,000. The higher figures come from the working engineers, and the very low figures from management. What are the causes and consequences of this lack of agreement? Since 1 part in 100,000 would imply that one could put a Shuttle up each day for 300 years expecting to lose only one, we could properly ask “What is the cause of management’s fantastic faith in the machinery? … It would appear that, for whatever purpose, be it for internal or external consumption, the management of NASA exaggerates the reliability of its product, to the point of fantasy.” –Richard Feynman – Rogers Commission

(Jim Quinn) The phrase “Throttle Up” jumped into my consciousness in the last week when Trump and his coronavirus task force of government hacks and bureaucrat lackeys announced the guidelines for re-opening America, as if a formerly $22 trillion economy, tied to a $90 trillion global economy, could be turned off and on like a light switch. Clap off, clap on. It just doesn’t work that way. The arrogance and hubris of people who think they can declare a global shut down for a virus and think they can easily deal with the intended and unintended consequences of doing so, is breathtaking in its outrageous recklessness and egotistical belief in their own infallibility.

This contemptible belief in their own superiority has permeated every fiber of those who rule over us, particularly among captured central bankers, corrupt politicians, bought off scientists, and billionaire oligarchs. It is the same groupthink, purposeful failure to address risks, and willfully ignoring those in the trenches that murdered seven astronauts on January 28, 1986 and has created the 2nd Great Depression of today. “Throttle Up” is going to result in the same outcome as it did in 1986.

Thirty-four years ago, on a cold January morning, Space Shuttle Challenger thundered into a crystal-clear blue Florida sky on its 10th voyage into space. The seven astronauts, including civilian Christa McAuliffe, put their trust in the “experts” from NASA, Thiokol, and Rockwell that the shuttle was safe and launching when the temperature was 30 degrees would not pose any added risks. When Richard Covey in Mission Control informed the crew to “go at throttle up”, they expected what their training told them would happen.

Instead, Space Shuttle Challenger exploded in a horrific display witnessed live on TV by 17% of the American population. School children all over the country were watching in their classrooms because McAuliffe was a school teacher chosen from thousands to go into space. It was a tragedy that shook the nation and led to one of Reagan’s better speeches that night, where he addressed the nation’s school children.

“I want to say something to the schoolchildren of America who were watching the live coverage of the shuttle’s takeoff. I know it is hard to understand, but sometimes painful things like this happen. It’s all part of the process of exploration and discovery. It’s all part of taking a chance and expanding man’s horizons. The future doesn’t belong to the fainthearted; it belongs to the brave. The Challenger crew was pulling us into the future, and we’ll continue to follow them.”

And he ended with this line from the poem ‘High Flight’:

“We will never forget them, nor the last time we saw them, this morning, as they prepared for their journey and waved goodbye and ‘slipped the surly bonds of Earth’ to ‘touch the face of God.’”

Thus, began the politician’s use of death to create heroes when human error, hubris, and recklessness is the true cause of avoidable tragedy and despair. Those seven astronauts were not heroes, they were victims. Just as we are all victims of the incompetency, arrogance, corruption and greed of those who lead our government, financial system, and corporate fascist oligarchy passing for capitalism in this globalist-controlled fraud of a former republic.

Using victims to create false heroes has now been elevated to an art form by politicians, the corporate media and mega-corporations to push whatever agenda supports their narrative. The propaganda machine is their most useful tool, as decades of dumbing down the public through government school indoctrination has created millions of pliable useful idiots who will believe anything presented by “experts” on the boob tube. The fear and panic created by politicians and the media about a virus only marginally more dangerous than the common flu is the perfect representation of this power over reality.

The Space Shuttle Challenger disaster is a perfect analogy for the current debacle being perpetrated on the American people by fecklessly corrupt authoritarian politicians, IYI medical “experts”, and fear mongering fake news media pushing the narrative in whatever direction benefits their bottom line. There is the simple technical reason why the Challenger blew up and then there is the real reason – the truthful explanation. What we must understand from history and experience is, if we don’t accept the narratives pushed by “experts” and think critically based upon facts, the truth will eventually be revealed.

The immediate cause of the explosion was a failure in the O-rings sealing the aft field joint on the right solid rocket booster, causing pressurized hot gases and eventually flame to “blow by” the O-ring and contact the adjacent external tank, causing structural failure. The truth is, decisions made and not made over years sealed the fate of those victims, just as we are facing today with this man-made global catastrophe.

After the shuttle disaster, politicians do what they do best, create a commission to cover-up the true cause and protect the establishment from blame. It was led by William Rogers, a government bureaucrat for decades, along with numerous other people with a vested interest in protecting NASA, the massive defense corporations sucking off the government teat, and the crooked politicians supporting NASA.

There were a couple of members from the trenches, like Sally Ride and Chuck Yeager, but the thorn in the side of the establishment was theoretical physicist and Nobel Prize winner Richard Feynman. Despite being racked by cancer, Feynman reluctantly agreed to join the commission, knowing he was going to be out of his element in the swamp of Washington D.C. The nation’s capital, he told his wife, was “a great big world of mystery to me, with tremendous forces.”

Feynman immediately created problems by thinking outside the box and having the gall to ignore the excuses and lies of high-level managers at NASA, Thiokol and Rockwell, while seeking the opinions of the actual engineers who did the real work. His unwillingness to toe the company line irritated the old guard looking to cover up the truth. During a break in one hearing, Rogers told commission member Neil Armstrong, “Feynman is becoming a pain in the ass.”

The establishment always thinks anyone who questions their authority or expertise is a pain in the ass, at best. Often, they treat anyone with an opposing viewpoint as the enemy, and will undertake any means to shut them up and destroy them. Witness how YouTube and Google are currently memory holing anything questioning the establishment narrative about this virus or Joe Biden’s sexual assault on a young woman as a Senator. Feynman embarrassed the “experts” on national TV when he conducted a simple demonstration of why the shuttle blew up.

“I took this stuff I got out of your [O-ring] seal and I put it in ice water, and I discovered that when you put some pressure on it for a while and then undo it, it doesn’t stretch back. It stays the same dimension. In other words, for a few seconds at least, and more seconds than that, there is no resilience in this particular material when it is at a temperature of 32 degrees. I believe that has some significance for our problem.” – Richard Feynman

The truth is top management at NASA knew the O-rings were defective in 1977 and contained a potentially catastrophic flaw. NASA managers also disregarded warnings from engineers about the dangers of launching posed by the low temperatures of that morning, and failed to adequately report these technical concerns to their superiors. Thiokol engineer Bob Ebeling in October 1985 wrote a memo—titled “Help!” so others would read it—of concerns regarding low temperatures and O-rings.

There were numerous teleconferences on the 27th of January where Ebeling and other engineers argued against the launch due to the freezing temperatures. According to Ebeling, a second conference call was scheduled with only NASA and Thiokol management, excluding the engineers. Thiokol management disregarded its own engineers’ warnings and now recommended the launch proceed as scheduled. Ebeling told his wife that night Challenger would blow up. He was right.

The Commission attempted to let NASA’s culture off the hook with no recommended sanctions against the deeply flawed organization. Feynman could not in good conscience recommend NASA should continue without a suspension of operations and a major overhaul. His fellow commission members were alarmed by Feynman’s dissent. Feynman was so critical of flaws in NASA’s “safety culture” that he threatened to remove his name from the report unless it included his personal observations on the reliability of the shuttle, which appeared as Appendix F.

The quote at the beginning of this article about upper management believing there was only a 1 in 100,000 chance of disaster, when the odds were really 1 in 100 or less, came from Feynman’s dissent in Appendix F. The fools at NASA and on the Commission didn’t understand or willfully ignored Feynman’s first principle:

“The first principle is that you must not fool yourself — and you are the easiest person to fool.” – Richard Feynman

The truth stands on its own and is self-evident. Feynman is an example of an actual hero, not an MSM touted hero like Bernanke, Paulson, Geithner, Powell and the dozens of other psychopaths in suits who have been portrayed in the press as brilliant financial minds that saved the world. Real heroes take a singular stand for the truth, when everyone else goes along with mistruths, half-truths, and false narratives of those with a subversive self-serving agenda. The world is inundated in a blizzard of lies, designed to further the plans of those who control the levers of power and wealth.

Lies, backed by an unceasing stream of propaganda and fear, are being used to panic the masses into willingly abandon their freedoms, liberties and rights for the chains of false safety, security, and state control over every aspect of their lives. It is astonishing to watch in real time as a vast swath of America cowers in their homes, as demanded by their authoritarian elected leaders, while their livelihoods and net worth are purposely destroyed to benefit the .1% ruling class.

I see multiple analogies today with the shuttle disaster and the lessons learned and not learned. The leadership of NASA did not learn, as the same disregard for facts and data led to the Space Shuttle Columbia disaster seventeen years later.

Just as the mid-level engineers at Thiokol warned of imminent disaster for years before the tragedy, there have been voices in the wilderness (scorned and ridiculed as conspiracy theorists) warning about the reckless arrogance of the Federal Reserve and their Wall Street owners, as they pumped up the largest financial bubble in world history as their solution for the catastrophe created by their previous monetary disaster in 2008. Just as the hubristic out of touch leadership of NASA murdered fourteen innocent astronauts, the Fed has now twice destroyed millions of lives in the last twelve years.

These self-proclaimed experts have known the financial system was going to explode since the middle of 2019 when they began a series of desperate ruses, behind the curtain of the debt saturated Ponzi scheme, to keep the Wall Street cabal and hedge fund billionaires from facing the consequences of their fraudulent monetary machinations.

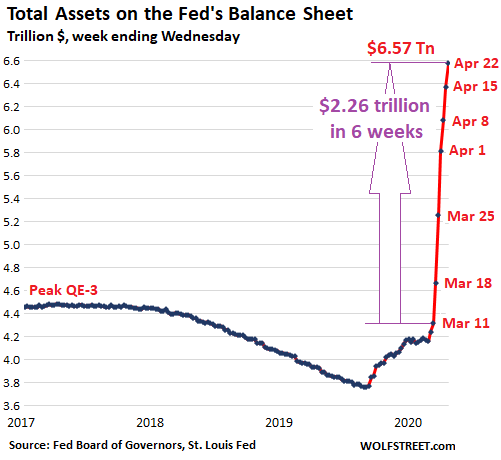

The surprise cutting of interest rates and emergency repo operations every night as we entered 2020 covered up the imminent disaster, as the mindless Harvard and Wharton MBAs programmed their high frequency trading computers to buy, buy, buy. Best economy ever. Greatest in the history of the world. Stock market at all-time highs. Then the China flu arrived, just in time. A quick 30% plunge in the stock market was all the Fed needed to rescue their true constituents – Wall Street and billionaire hedge funds – with $6 trillion, under the guise of saving the financial system for the little people.

If you want to figure out who benefits from a man-made crisis, just follow the money. The Federal government has committed at least $3 trillion of your grandchildren’s money to the crisis thus far, with the Federal Reserve announcing another $6 trillion of monetary support. That’s $9 trillion, or $70,000 per household. The average household size is 2.5. If we assume each household got their $1,200 Covid-19 rebate (actually just giving them back the taxes they already pay), that’s $3,000 per household.

A critical thinking individual might wonder who got the other $67,000 of stimulus, or 95.7% of the money allocated to “save America”. It certainly hasn’t made its way to small business owners who are going out of business faster than burning gas through a defective O-ring. If only $400 billion is making its way into the pockets of formerly working Americans, where did the other $8.6 trillion go?

It went directly into the pockets of Wall Street bankers, hedge fund managers, and the biggest corporations on the planet. The Fed has used this faux crisis to further enrich and bailout the richest men on the planet, while again dropping interest rates to zero and throwing grandma under the bus again. Let her eat cat food, declares Jerome Powell, champion and hero of downtrodden bankers. He’ll be “earning” $25 million a year from Wall Street as his payoff, the minute he saunters out of the Eccles Building in a couple years.

As unemployment approaches 20%, GDP plunges by 30%, food banks are running out of food, citizens remain locked in their homes under threat of arrest, and human misery approaches 1930 Great Depression levels, the Fed has managed to buy enough toxic debt and artificially rig the stock market, to engineer a 27% surge from its March lows. We should all applaud the brilliance of Powell and his fellow sycophants, as they have saved the asses of the .1%, for now.

The fate of this country was sealed well before this overblown hyped coronavirus appeared, to accelerate our demise. The warnings about too much debt, rigged financial markets, unrestrained politicians running trillion dollar deficits, silicon valley giants conspiring with the Deep State to turn the country into a surveillance state, a military industrial complex creating conflict around the globe, and a state media propaganda machine providing false information to the masses, were dismissed by those who could have acted.

The deficit is now expected to hit $3.7 trillion in 2020, pushing the national debt to $27 trillion. This country is 231 years old and 85% of our debt has been taken on in the last 23 years. The Fed’s balance sheet was $800 billion in 2008. It will shortly surpass $10 trillion, just a mere 1,250% increase in 12 years. Do you understand the analogy with the Space Shuttle Challenger yet?

We’ve left the launchpad at the same rate and angle as the Fed balance sheet. Those in charge assure us they have everything under control, but the coronavirus will prove to be our frozen O-ring. It has been decades of mismanagement, corruption, bad decisions, horrible leadership, delusional thinking, herd mentality, and an inability to summon the courage to deal with critical problems before they blew our country into a million smoking pieces of debris.

Average Americans are trapped in the crew cabin relying on Trump, Powell, Mnuchin, and a myriad of other “experts” to safely launch the American economy back into space. Trump has convened a re-opening task force consisting of dozens of CEOs from the biggest mega-corporations on earth. I know because I watched him read their names for fifteen minutes during one of his daily mind-numbing press conferences. If you had any doubt about who your leaders work for, that list tells you all you need to know. No one from your local steak shop, butcher or candlestick maker are represented on this task force. It reminded me of the list of prominent people chosen for the Rogers Commission.

The belief by those in charge that things can just go on as if nothing has happened are as delusional as the NASA administrators who were willfully blind to the truth of an impending disaster. The actions taken by the political and financial arms of the Deep State have guaranteed this malfunction will prove fatal for our country. The only question is how many seconds we have before our throttle up moment. I tend to be a pessimist, so I am leaning towards an explosion before the November election. The forthcoming financial catastrophic detonation will set off a chain of events considered impossible just a few short months ago.

The core elements of this Fourth Turning (debt, civic decay, global disorder) are going to juxtapose and connect, accelerating into a chain reaction of chaos, civil uprising, global war, mass casualties, the fall of empires, and ultimately the destruction of the existing social order (aka Deep State). Hopefully, heroes of Feynman’s stature will arise to help rebuild our country based upon common sense, truthfulness, factual assessment of our situation, and honoring the essential principles of our Constitution. Reality must take precedence over delusions, propaganda, and lies for us to regain our nation. Are we capable of learning the lessons from this major malfunction?

“Flight controllers here looking very carefully at the situation. Obviously, a major malfunction.” – Steve Nesbitt – NASA Mission Control

(Pepe Escobar) You don’t need to read Michel Foucault’s work on biopolitics to understand that neoliberalism – in deep crisis since at least 2008 – is a control/governing technique in which surveillance capitalism is deeply embedded.

But now, with the world-system collapsing at breathtaking speed, neoliberalism is at a loss to deal with the next stage of dystopia, ever present in our hyper-connected angst: global mass unemployment.

Henry Kissinger, anointed oracle/gatekeeper of the ruling class, is predictably scared. He claims that, “sustaining the public trust is crucial to social solidarity.” He’s convinced the Hegemon should “safeguard the principles of the liberal world order.” Otherwise, “failure could set the world on fire.”

That’s so quaint. Public trust is dead across the spectrum. The liberal world “order” is now social Darwinist chaos. Just wait for the fire to rage.

The numbers are staggering. The Japan-based Asian Development Bank (ADB), in its annual economic report, may not have been exactly original. But it did note that the impact of the “worst pandemic in a century” will be as high as $4.1 trillion, or 4.8 percent of global GDP.

This an underestimation, as “supply disruptions, interrupted remittances, possible social and financial crises, and long-term effects on health care and education are excluded from the analysis.”

We cannot even start to imagine the cataclysmic social consequences of the crash. Entire sub-sectors of the global economy may not be recomposed at all.

The International Labor Organization (ILO) forecasts global unemployment at a conservative, additonal 24.7 million people – especially in aviation, tourism and hospitality.

According to the ILO, income losses for workers may range from $860 billion to an astonishing $3.4 trillion. “Working poverty” will be the new normal – especially across the Global South.

“Working poor,” in ILO terminology, means employed people living in households with a per capita income below the poverty line of $2 a day. As many as an additional 35 million people worldwide will become working poor in 2020.

Switching to feasible perspectives for global trade, it’s enlightening to examine that this report about how the economy may rebound is centered on the notorious hyperactive merchants and traders of Yiwu in eastern China – the world’s busiest small-commodity, business hub.

Their experience spells out a long and difficult recovery. As the rest of the world is in a coma, Lu Ting, chief China economist at Nomura in Hong Kong stresses that China faces a 30 percent decline in external demand at least until next Fall.

Neoliberalism in Reverse?

In the next stage, the strategic competition between the U.S. and China will be no-holds-barred, as emerging narratives of China’s new, multifaceted global role – on trade, technology, cyberspace, climate change – will set in, even more far-reaching than the New Silk Roads. That will also be the case in global public health policies. Get ready for an accelerated Hybrid War between the “Chinese virus” narrative and theHealth Silk Road.

The latest report by the China Institute of International Studies would be quite helpful for the West — hubris permitting — to understand how Beijing adopted key measures putting the health and safety of the general population first.

Now, as the Chinese economy slowly picks up, hordes of fund managers from across Asia are tracking everything from trips on the metro to noodle consumption to preview what kind of economy may emerge post-lock down.

In contrast, across the West, the prevailing doom and gloom elicited a priceless editorial from TheFinancial Times. Like James Brown in the 1980s Blues Brothers pop epic, the City of London seems to have seen the light, or at least giving the impression it really means it. Neoliberalism in reverse. New social contract. “Secure” labor markets. Redistribution.

Cynics won’t be fooled. The cryogenic state of the global economy spells out a vicious Great Depression 2.0 and an unemployment tsunami. The plebs eventually reaching for the pitchforks and the AR-15s en masse is now a distinct possibility. Might as well start throwing a few breadcrumbs to the beggars’ banquet.

That may apply to European latitudes. But the American story is in a class by itself.

Mural, Seattle, February 2017. (Mitchell Haindfield, Flickr)

For decades, we were led to believe that the world-system put in place after WWII provided the U.S. with unrivaled structural power. Now, all that’s left is structural fragility, grotesque inequalities, unplayable Himalayas of debt, and a rolling crisis.

No one is fooled anymore by the Fed’s magic quantitative easing powers, or the acronym salad – TALF, ESF, SPV – built into the Fed/U.S. Treasury exclusive obsession with big banks, corporations and the Goddess of the Market, to the detriment of the average American.

It was only a few months ago that a serious discussion evolved around the $2.5 quadrillion derivatives market imploding and collapsing the global economy, based on the price of oil skyrocketing, in case the Strait of Hormuz – for whatever reason – was shut down.

Now it’s about Great Depression 2.0: the whole system crashing as a result of the shutdown of the global economy. The questions are absolutely legitimate: is the political and social cataclysm of the global economic crisis arguably a larger catastrophe than Covid-19 itself? And will it provide an opportunity to end neoliberalism and usher in a more equitable system, or something even worse?

‘Transparent’ Black Rock

Wall Street, of course, lives in an alternative universe. In a nutshell, Wall Street turned the Fed into a hedge fund. The Fed is going to own at least two thirds of all U.S. Treasury bills in the market before the end of 2020.

The U.S. Treasury will be buying every security and loan in sight while the Fed will be the banker – financing the whole scheme.

So essentially this is a Fed/Treasury merger. A behemoth dispensing loads of helicopter money.

And the winner is Black Rock—the biggest money manager on the planet, with tentacles everywhere, managing the assets of over 170 pension funds, banks, foundations, insurance companies, in fact a great deal of the money in private equity and hedge funds. Black Rock — promising to be fully “transparent” — will buy these securities and manage those dodgy SPVs on behalf of the Treasury.

Black Rock, founded in 1988 by Larry Fink, may not be as big as Vanguard, but it’s the top investor in Goldman Sachs, along with Vanguard and State Street, and with $6.5 trillion in assets, bigger than Goldman Sachs, JP Morgan and Deutsche Bank combined.

Now, Black Rock is the new operating system (OS) of the Fed and the Treasury. The world’s biggest shadow bank – and no, it’s not Chinese.

Compared to this high-stakes game, mini-scandals such as the one around Georgia Senator Kelly Loffler are peanuts. Loffler allegedly profited from inside information on Covid-19 by the CDC to make a stock market killing. Loffler is married to Jeffrey Sprecher – who happens to be the chairman of the NYSE, installed by Goldman Sachs.

While corporate media followed this story like headless chickens, post-Covid-19 plans, in Pentagon parlance, “move forward” by stealth.

The price? A meager $1,200 check per person for a month. Anyone knows that, based on median salary income, a typical American family would need $12,000 to survive for two months. Treasury Secretary Steven Mnuchin, in an act of supreme effrontry, allows them a mere 10 percent of that. So American taxpayers will be left with a tsunami of debt while selected Wall Street players grab the whole loot, part of an unparalleled transfer of wealth upwards, complete with bankruptcies en masse of small and medium businesses.

Fink’s letter to his shareholdersalmost gives the game away: “I believe we are on the edge of a fundamental reshaping of finance.”

And right on cue, he forecasted that, “in the near future – and sooner than most anticipate – there will be a significant reallocation of capital.”

He was referring, then, to climate change. Now that refers to Covid-19.

Implant Our Nano chip, Or Else?

The game ahead for the elites, taking advantage of the crisis, might well contain these four elements:

a social credit system,

mandatory vaccination,

a digital currency,

and a Universal Basic Income (UBI).

This is what used to be called, according to the decades-old, time-tested CIA playbook, a “conspiracy theory.” Well, it might actually happen.

West Virginia National Guard members reporting to a Charleston nursing home to assist with Covid-19 testing. April 6, 2020. (U.S. Army National Guard, Edwin L. Wriston)

A social credit system is something that China set up already in 2014. Before the end of 2020, every Chinese citizen will be assigned his/her own credit score – a de facto “dynamic profile”, elaborated with extensive use of AI and the internet of things (IoT), including ubiquitous facial recognition technology. This implies, of course, 24/7 surveillance, complete with Blade Runner-style roving robotic birds.

The U.S., the U.K., France, Germany, Canada, Russia and India may not be far behind. Germany, for instance, is tweaking its universal credit rating system, SCHUFA. France has an ID app very similar to the Chinese model, verified by facial recognition.

Mandatory vaccination is Bill Gates’s dream, working in conjunction with the WHO, the World Economic Forum (WEF) and Big Pharma. He wants “billions of doses” to be enforced over the Global South. And it could be a cover to everyone getting a digital implant.

“Eventually what we’ll have to have is certificates of who’s a recovered person, who’s a vaccinated person…Because you don’t want people moving around the world where you’ll have some countries that won’t have it under control, sadly. You don’t want to completely block off the ability for people to go there and come back and move around.”

Then comes the last sentence which was erased from the official TED video. This was noted by Rosemary Frei, who has a master on molecular biology and is an independent investigative journalist in Canada. Gates says: “So eventually there will be this digital immunity proof that will help facilitate the global reopening up.”

This “digital immunity proof” is crucial to keep in mind, something that could be misused by the state for nefarious purposes.

The three top candidates to produce a coronavirus vaccine are American biotech firm Moderna, as well as Germans CureVac and BioNTech.

Digital cash might then become an offspring of blockchain. Not only the U.S., but China and Russia are also interested in a national crypto-currency. A global currency – of course controlled by central bankers – may soon be adopted in the form of a basket of currencies, and would circulate virtually. Endless permutations of the toxic cocktail of IoT, blockchain technology and the social credit system could loom ahead.

Already Spain has announced that it is introducing UBI, and wants it to be permanent. It’s a form insurance for the elite against social uprisings, especially if millions of jobs never come back.

So the key working hypothesis is that Covid-19 could be used as cover for the usual suspects to bring in a new digital financial system and a mandatory vaccine with a “digital identity” nano chip with dissent not tolerated: what Slavoj Zizek calls the “erotic dream” of every totalitarian government.

Yet underneath it all, amid so much anxiety, a pent-up rage seems to be gathering strength, to eventually explode in unforeseeable ways. As much as the system may be changing at breakneck speed, there’s no guarantee even the 0.1 percent will be safe.

WAR WITH THE INTERNATIONAL BANKING CARTEL? OR NESARA?

***Neither, just another hopium psyop***

Tucked in the $2 trillion coronavirus stimulus bill passed by Congress is a curious provision that essentially outlines how the Treasury and the Federal Reserve will merge into one organization. Is this President Trump’s way of taking back America’s monetary sovereignty, or is it a smokescreen that expands the Fed’s power?

No one alive has experienced an economic plunge this sudden…

We can’t say we’re in a recession yet, at least not formally. A committee decides these things—no, really. The government generally adopts the view that a contraction is not a recession unless economic activity has declined over two quarters. But we’re in a recession and everyone knows it. And what we’re experiencing is so much more than that: a black swan, a financial war, a plague.

Maybe things feel normal where you are. Maybe things do not feel normal.

Things are not normal. For weeks or months, we won’t know how much GDP has slowed down and how many people have been forced out of work. Government statistics take a while to generate. They look backwards, the latest numbers still depicting a hot economy near full employment. To quantify the present reality, we have to rely on anecdotes from businesses, surveys of workers, shreds of private data, and a few state numbers. They show an economy not in a downturn or a contraction or a soft patch, not experiencing losses or selling off or correcting. They show evaporation, disappearance on what feels like a biblical scale.

What is happening is a shock to the American economy more sudden and severe than anyone alive has ever experienced. The unemployment rate climbed to its apex of 9.9 percent 23 months after the formal start of the Great Recession. Just a few weeks into the domestic coronavirus pandemic, and just days into the imposition of emergency measures to arrest it, nearly 20 percent of workers report that they have lost hours or lost their job. One payroll and scheduling processor suggests that 22 percent of work hours have evaporated for hourly employees, with three in 10 people who would normally show up for work not going as of Tuesday. Absent a strong governmental response, the unemployment rate seems certain to reach heights not seen since the Great Depression or even the miserable late 1800s. A 20 percent rate is not impossible.

State jobless filings are growing geometrically, a signal of how the national numbers will change when we have them. Last Monday, Colorado had 400 people apply for unemployment insurance. This Tuesday: 6,800. California has seen its daily filings jump from 2,000 to 80,000. Oregon went from 800 to 18,000. In Connecticut, nearly 2 percent of the state’s workers declared that they were newly jobless on a single day. Many other states are reporting the same kinds of figures.

These numbers are subject to sharp changes; things like large plant closures lead them to jump and fall and jump and fall. But for them to rise so precipitously, across all of the states? To stay high? That is new. The economy is not tipping into a jobs crisis. It is exploding into one. Given the trajectory of state reports, it is certain that the country will set a record for new jobless claims next week, not only in raw numbers but also in the share of workers laid off. The total is expected to be in the range of 1.5 million to 2.5 million, and to climb from there.

None of that is surprising.

The economy needs to halt to protect lives and sustain the medical system. Planes have been grounded, conferences canceled, millions of Americans told not to leave their homes except to get groceries and other necessities. Because of the emergency measures now in place, businesses have had no choice but to let workers go. The list of employers laying off workers en masse includes cruise lines, airlines, hotels, restaurants, bars, cabinetmakers, linen companies, newspapers, bookstores, caterers, and festivals. I started adding up numbers in news reports, and quit when I hit 100,000.

The economy had been plodding along in its late expansion, growing at a 2 or 3 percent annual pace. Now, private forecasters expect it will contract at something like a 15 percent pace, though nobody really knows. A viral quarantine is impossible to model, because modeling would mean knowing how long the necessary emergency measures will last and how well the government will respond with some degree of accuracy. Still, real-time measures show a consumer-economy apocalypse. One credit-card processor said that payments to businesses were down 30 percent in Seattle, 26 percent in Portland, and 12 percent in San Francisco. Nearly every state is seeing dramatic declines, with hotels and restaurants hit particularly hard.

The markets are not normal, either. The stock market lost 20 percent of its value in just 21 days – the fastest and sharpest bear market on record, faster than 1929, faster than 1987, 10 times faster than 2007.

The financial system has required no less than seven emergency interventions by the Federal Reserve in the past week.The country’s central bank has wrenched interest rates to zero, started buying more than half a trillion dollars of financial assets, and opened up special facilities to inject liquidity into the financial system.

Yet in the real economy, everything has halted, frozen in place. This is not a recession. It is an ice age.

After falling for 3 of the last 4 months, and following Germany’s disastrous January print, US Industrial Production was expected to drop by 0.2% but yet again it disappointed, falling 0.3% MoM.

This means US Industrial Production has contracted year-over-year for 5 straight months.

Utilities fell 4% in Jan. after falling 6.2% in Dec. (warm weather-related?)

Mining rose 1.2% in Jan. after rising 1.5% in Dec.

In the manufacturing segment, production slipped 0.1% MoM, matching expectations, but is down year-over-year for the seventh straight month…

Finally, we note that Capacity Utilization slumped to 76.8%.

And this is before the impact of the virus had fully hit global supply chains.

George Washington’s crossing of the Delaware River

The U.S. Constitution states:

Article 1, Section 8

1. The Congress shall have Power …

5. To coin Money, regulate the value thereof, and of foreign coin….

6. To provide for the punishment of counterfeiting … current coin of the United States.

Article 1, Section 10

No state shall … emit Bills of Credit and make any Thing but gold and silver Coin a Tender in Payment of Debts.

The intent of the Framers could not have been clearer. The Constitution clearly and unequivocally brought into existence a monetary system based on gold coins and silver coins being the official money of the United States.

Sound Money

Notice that the states are prohibited from issuing “bills of credit.” What are “bills of credit.” That was the term used during that time for paper money. The Constitution expressly prohibited the states from publishing paper money and making anything but gold and silver coins official legal money.

What about the federal government? The Constitution didn’t expressly prohibit it from emitting “bills of credit” like it did with the states. Does that mean that the federal government was empowered to make paper money the official money of the United States?

No, it does not mean that. In the case of the federal government, its powers are limited to those enumerated in the Constitution. If a power isn’t enumerated, then the federal government is automatically prohibited from exercising it.

Therefore, it was unnecessary for the Framers to provide for an express prohibition on the federal government to make paper money the official legal tender of the nation. All that was necessary was to ensure that the Constitution did not empower the federal government to issue paper money.

The powers relating to money that are delegated to the federal government, which are stated above, expressly make it clear that gold coins and silver coins, not paper, were to be the official money of the country. That is reflected by the power given the federal government to “coin money.” At the risk of belaboring the obvious, one does not “coin” paper. Paper is published or “emitted.” It is not coined. Coins are coined.

The provision on counterfeiting also expressly confirms that the official money of the United States was to be gold coins and silver coins. The Framers didn’t provide for punishment for counterfeiting paper money because there was no paper money. They provided for punishment for counterfeiting “current coin of the United States.”

Add up all of these provision and there is but one conclusion that anyone can logically and reasonably draw: The Constitution established a monetary system in which gold and silver coins were to be the official money of the United States.

The power to borrow

That’s not to say, of course, that federal officials could not borrow money. The Constitution did give them that power:

Article1, Section 8

1. The Congress shall have Power …

2. To borrow money on the credit of the United States.

When the federal government borrows money, it issues debt instruments to lenders, consisting of bills, notes, or bonds. But everyone understood that federal debt instruments were not money but instead simply promises to pay money. The money that they promised to pay was the gold and silver coins, which were the official money of the country.

And in fact, that was the monetary system of the United States for more than a century, one in which gold coins and silver coins were the official money of the American people.

It is often said that the “gold standard” was a system in which paper money was “backed by gold.” Nothing could be further from the truth. There was no paper money. The “gold standard” was a system where gold coins, along with silver coins, were the official money of the country.

Monetary debauchery and destruction

It all came to an end in the 1930s, when the (D) Franklin Roosevelt regime ordered all Americans to deliver their gold coins to the federal government. Anyone who failed to do so would be prosecuted for a federal felony offense and severely punished through incarceration and fine if convicted.

In exchange, people were handed federal debt instruments, ones that promised to pay money. But since the money was now illegal, the debt instruments were promises to pay nothing. That’s reflected by the Federal Reserve Notes that people now use to pay for things.

Roosevelt’s actions were among the most abhorrent in the history of the United States. In one fell swoop, he and his regime destroyed what had been the finest and soundest monetary system in the history of the world, one that contributed mightily to the tremendous increase in prosperity and standards of living in the 19th century.

What is also amazing is that Roosevelt did it without even the semblance of a constitutional amendment. To change a system that the Constitution established requires a constitutional amendment. That is an arduous and difficult process, which is what the Framers wanted. Roosevelt circumvented that process by simply getting Congress to nationalize people’s gold.

The result of Roosevelt’s illegal and immoral actions regarding money and the Constitution? Moral, economic, and monetary debauchery, which has entailed almost 90 years of plundering and looting people through monetary debasement and devaluation to finance the ever-burgeoning expenses of America’s welfare-warfare state way of life.

The solution

The solution to all this monetary mayhem is doing what the Framers did: Separate private banking from the state entirely, in the same way that they separated church and state. This means terminate all government involvement in banking, including by ending the private Federal Reserve Bank. And while we’re at it, nationalize the sovereign city, District Of Columbia which would end London and Vatican maritime law control over America. No doubt they won’t go down without a fight however, this is the jump start necessary towards restoring any chance for freedom, peace, and prosperity to our land.

Georgetown University Medical Center reveals brutal dynamic governing long-term care in America

The results of a six-year study by Georgetown University Medical Center revealed just how fast U.S. nursing home prices have been increasing all across America. And the future looks just as grim.

Dr. Sean Huang, the study’s lead author, said the brutal dynamic governing long-term care in America — where many nursing home residents must spend down the bulk of their life savings before qualifying for federal assistance — is intensifying. California, Florida, New York and Texas all saw increases that far outstripped the 11.6% rise in inflation between 2005 and 2010, the period reviewed by Georgetown’s analysis of eight states. Additional data show the upward trend has continued in the years since.

And it’s not just baby boomers who need to worry — Generation X, millennials and Generation Z might face an even darker old age. Rising wage pressure on a sector in need of workers is driving up costs, and unless Washington comes up with a fix, be it a version of Medicare-for-All or something less ambitious, the funding for some programs is projected to start running out in the next decade.

“We’re talking about long stays — people who have disabilities, dementia, Parkinson’s disease,” Mr. Huang explained about the growing nursing home population. “Medicare does not cover that. They will pay out-of-pocket until they use all of their wealth.”

Many Americans have no idea how Medicare works, including those approaching retirement. A sort-of government health insurance policy largely for older Americans, eligibility generally begins at age 65, covering some of the costs of routine and emergency medical care. What it doesn’t cover is most aspects of long-term “custodial” care — as in nursing homes, where a large portion of Americans can expect to spend the last years of their lives.

That’s where Medicaid — state-administered coverage for Americans whose assets fall below a certain level — comes in. For those who qualify for nursing home admission, Medicaid generally requires they exhaust most of their assets first before qualifying for coverage. Without expensive long-term care insurance, which most people don’t have, an increasing number of older Americans are falling into this financial trap, Mr. Huang said.

And their nest eggs are being depleted more quickly than ever. Mr. Huang’s study found nursing home price rises over the period measured generally outpaced increases in overall medical care (20.2%) and consumer prices (11.7%). For example, in California between 2002 and 2011, the median out-of-pocket cost for nursing home care increased by 56.7%.

Mr. Huang and three co-authors began looking into the matter in 2013. With no central database, they had to collect information from each state and individual nursing homes. Some states only had data through 2010, he said. In the end, they managed to crunch data from an average of 3,900 nursing homes for each of the years measured, representing approximately 27% of freestanding U.S. facilities.

Nursing homes in New York during the period reviewed had the highest average daily price of $302, while Texas had the lowest average daily price of $121. Additional information has shown that nursing home costs have continued to increase at a much higher rate than inflation, albeit slightly slower than the study period.

In 2010, the average price per day for nursing home care in California was $217, up more than 30% (with Florida close behind) from 2005. In a more recent analysis, Mr. Huang calculated that, from 2010 to 2015, nursing home prices in California rose more slowly, by roughly 19.6% to $258 per day. However, inflation from 2010 to 2015 only increased by 8.7%, he noted. Mr. Huang said his research doesn’t point to any improvement going forward.

“I don’t see there’s any major changes that suggest the trend will be different,” Mr. Huang said.

Indeed, the median daily price for a private room in a California nursing home just last year was $323, while the national median was $275 per day, according to life insurance company Genworth. Looking at the issue from an annual perspective, the median cost in the U.S. for a private room in a nursing home was $100,375. Oklahoma provided the cheapest annual median cost at $63,510, while Alaska was the most expensive at $330,873, Genworth data showed.

Nursing homes have long been a financial drain on most who need them, constituting one of the greatest risks retirees face when it comes to managing retirement funds, a report from the U.S. Department of Health and Human Services showed. Unfortunately, the annual costs for nursing home care will continue to grow at a rate much faster than inflation, according to Urban Institute Senior Fellow Richard W. Johnson.

“It’s that labor market pressure,” Mr. Johnson said. More elderly Americans mean more demand for nursing home care, and more demand for nursing home employees. Wages go up, and the cost is passed along to consumers who, under the current system by which America looks after its elderly, coverage is limited.

In an industry that requires significant hands-on attention, technology can’t eliminate many jobs, Mr. Johnson said. And just when the labor market for nursing homes is already tight, uncertainty over U.S. immigration policies may further reduce available workers, he said. In 2017, immigrants made up 23.5% of formal and non-formal long-term care sector workers, according to Health Affairs.

“It’s unlikely that you’re going to see any improvement in these trends, and if anything, things will probably get worse because nursing homes are probably going to face something of a worker shortage,” Mr. Johnson said. Home health aides and personal care aides are ranked as the third and fourth fastest growing occupations and are expected to increase 47% and 39% respectively from 2016 to 2026, according to the Bureau of Labor Statistics.

“The baby boom generation is so large,” Mr. Johnson said. “They’re approaching their 80s, and that means that many more of them are going to need nursing home care or other types of long term care.”

“If there would be a higher reimbursement rate, either by Medicaid or Medicare, nursing home quality would be likely to improve.”

Another trend emerging in the industry that may be driving up costs is Wall Street. Four out of the 10 largest for-profit nursing home chains were purchased by private equity firms from 2003-2008, according to a case study analyzing private equity takeover.

Research on the impact of private equity has shown mixed results, though one study showed how a nursing home chain that was taken over by a private equity firm showed a general reinforcement of profit-seeking strategies that were already in place, while adding some strategies aimed at improving efficiency. Other reports have detailed darker results.

During the Obama administration, the Community Living Assistance Services and Supports Act (CLASS Act) was signed into law to help ease the burden as part of the Affordable Care Act (ACA), but it was later rescinded by Congress over concerns voluntary enrollment wasn’t viable — premiums would be too high and the system would eventually collapse, Mr. Johnson said. This left the ACA with little to no assistance for long-term care costs.

Some states have started taking matters into their own hands. Washington State passed a bill in April that would implement a 0.58% payroll tax that would give residents up to $36,500 to pay for long-term care services. Payroll tax will begin collecting in 2022, while residents can start withdrawing in 2025. But that’s just one state, and the problem, Huang and Johnson note, is national in scope.

“If there would be a higher reimbursement rate, either by Medicaid or Medicare, nursing home quality would be likely to improve,” Mr. Huang said. “But I don’t see that happening in the near future.