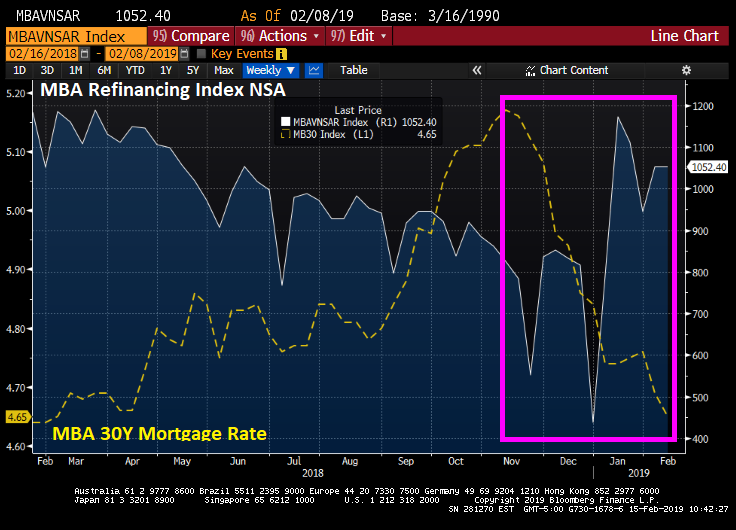

The rigging of interest rates by hapless central banks continues to do its job in distorting the market. In addition to boosting both bonds and stocks, it also has homeowners drawing on cash out refinancings at the quickest clip since the last global financial crisis.

Category Archives: Mortgage

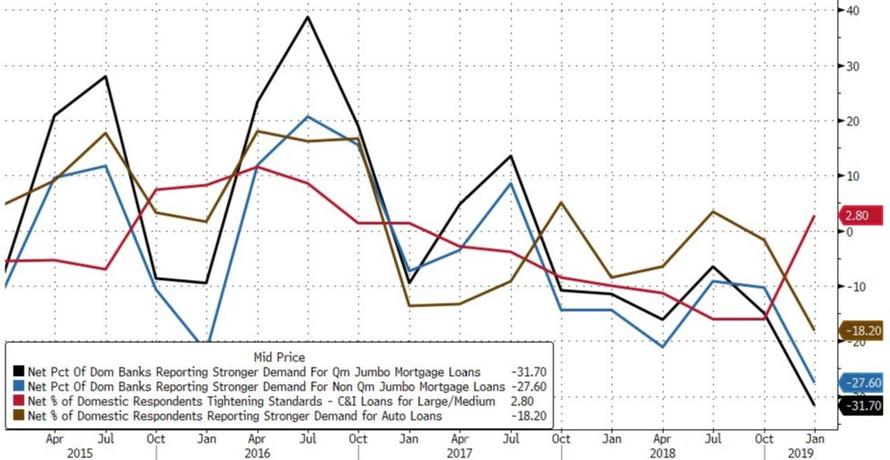

Commercial Loan Demand Plunges To New Post-Lehman Low Even As Lending Standards Ease

Mortgage Rates Hit Record Low For 10th Time This Year

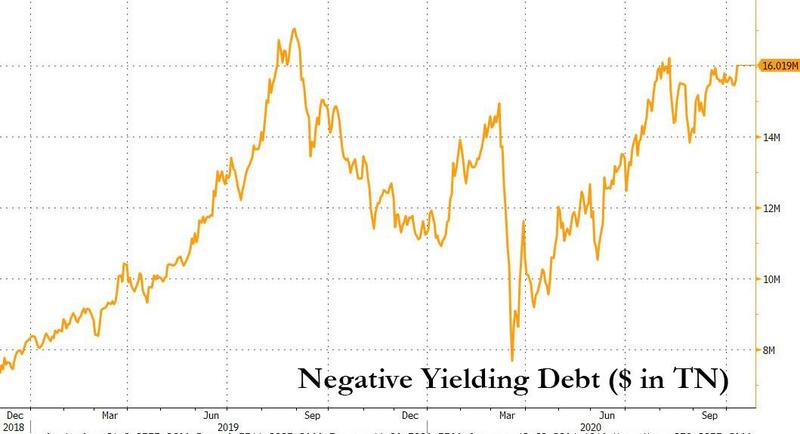

In a world where over $16 trillion in debt now trades with negative yields…

… the US remains one of the outliers where nominal yields are still positive (if not for too long). Still, with rates in the US remaining caught in a tight range, and as bank funding conditions increasingly normalize, it means that yields on mortgages continue to shrink, and sure enough according to the latest Freddie Mac data, the average yield for a 30-year, fixed loan dropped to 2.81%, down from 2.87% last week, which was not only the lowest in almost 50 years of data-keeping, but also the 10th record low this year. The previous all time low – 2.86% – held for about a month.

The availability of record cheap loans – which is unlikely to change with the Fed signaling it will hold its benchmark rate near zero through at least 2023 – has fueled a home buying spree which while bolstering the pandemic economy, has resulted in yet another bubble (for more details see Visualizing The U.S. Housing Frenzy In 34 Charts)

Meanwhile, the surging demand for the scarce supply of properties on the market is pushing up prices, putting home ownership out of reach for many Americans, and leading to even greater wealth inequality which, as a reminder, is how we got here in the first place. Adding insult to injury, lenders have tightened credit standards to near record levels, presenting another potential obstacle for would-be buyers.

“It’s important to remember that not all people are able to take advantage of low rates, given the effects of the pandemic,” Sam Khater, Freddie Mac’s chief economist, said in the statement.

Mortgage Rates Crashing With Crashing Money Velocity

Best ‘K’ shaped economic recovery ever…

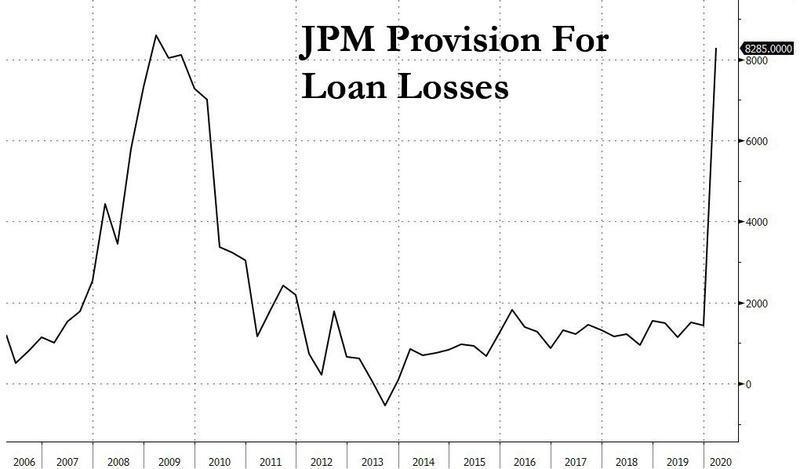

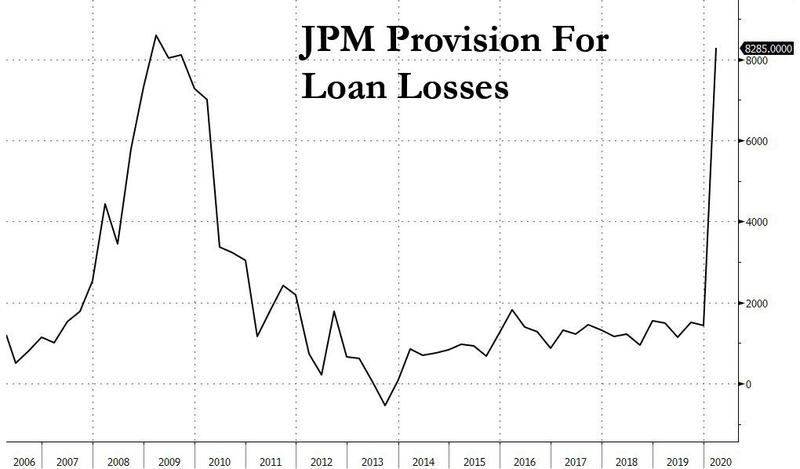

Dimon Signals The All Clear: JPMorgan Earnings Smash Expectations As Loss Provisions Plummet 94%

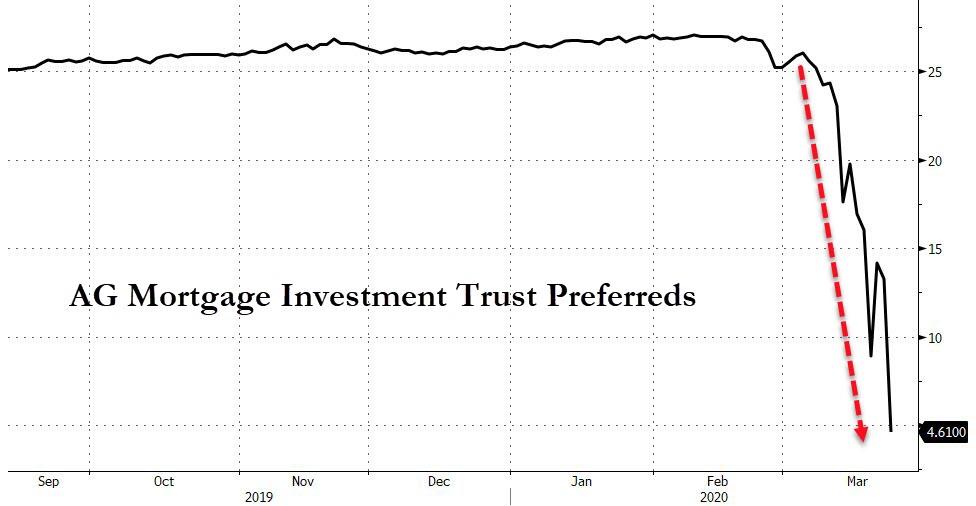

Negative Returns Are Now In US Mortgages

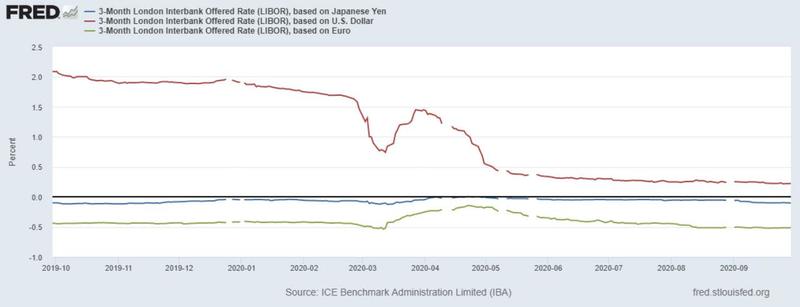

(Christopher Whalen) Watching the talking heads pondering the next move in US interest rates, we are often amazed at the domestic perspective that dominates these discussions. Just as the Federal Open Market Committee never speaks about foreign anything when discussing interest rate policy, so too most observers largely ignore the offshore markets. Yen, dollar and euro LIBOR spreads are shown below.

Zoltan Pozsar, the influential money-market strategist at Credit Suisse (NYSE:CS), warns that the short-end of the US money markets are likely to be awash in cash over the end-of-year liquidity hump. Unlike the unpleasantness in 2018, for example, we may see instead a surfeit of lending as banks scramble for yield in a wasteland bereft of duration. Would that it were so.

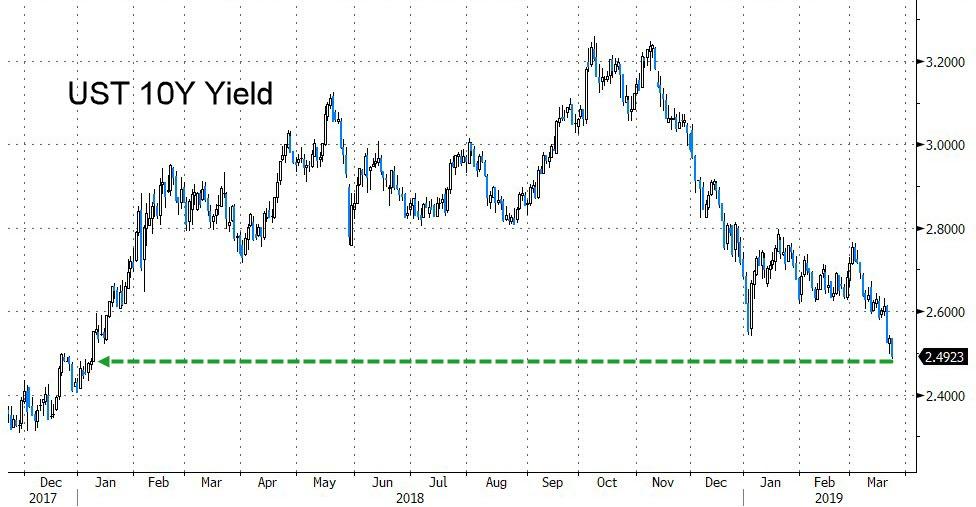

The Pozsar view does not exactly fit well with the rising rate, end of the world scenario popular in some corners of the financial media ghetto. The 10-year note is certainly rising and with it the 30-year mortgage rate. Indeed, Pozsar reminds CS clients that yen/$ swaps are now yielding well-above Treasury yields for seven years. Hmm.

We believe short-term rates will remain low in the US, even as offshore demand for dollars soars. If the 10-year Treasury backs up much further, then we’d look for the FOMC to act on some calls by governors to buy longer duration securities. That is, a very direct and large scale increase in QE and particularly on the long end of the curve.

We expect that Chairman Powell knows that underneath the comfortable blanket of low interest rates lie some truly appalling credit problems ahead for the global economy, the US banking sector and also for private debt and equity investors. We expect the low interest rate environment to drive volumes in corporate debt and residential mortgages, even as other sectors like ABS languish and commercial real estate gets well and truly crushed.

“The pandemic is putting unprecedented stress on CMBS markets that even the Fed is having difficulty offsetting,” writes Ralph Delguidice at Pavilion Global Markets.

“Limited reserves are being exhausted even as rent collection and occupancy levels remain serious issues… Bondholders expecting cash are getting keys instead, and in our view, ratings downgrades and significant losses are now only a formality.”

We noted several months ago that the resolution of the credit collapse in commercial mortgage backed securities or CMBS will be very different from when a bank owns the mortgage. As we discussed with one banker this week over breakfast in Midtown Manhattan, holding the mortgage and even some equity in a prime property allows for time to recover value.

With CMBS, the “AAA” tranche is first in line, thus the seniors have no incentive to make nice with the subordinate investors. The deals will liquidate, the property will be sold and the junior bond investors will take 100% losses. But as Delguidice and others note with increasing frequency, this time around the “AAA” investors are getting hit too. More to come.

Manhattan

Meanwhile, over in the relative calm of the agency collateral markets, large, yield hungry money center banks led by Wells Fargo & Co are deploying liquidity to buy billions of dollars in delinquent government loans out of MBS pools.

The bank buys the asset and gives the investor par, with a smidgen of interest. Market now has more cash, but less cash than it had before buying the mortgage bond in the first place. Why? Because it likely took a loss on the transaction. Buy at 109. Prepayment at par six months later. You get the idea.

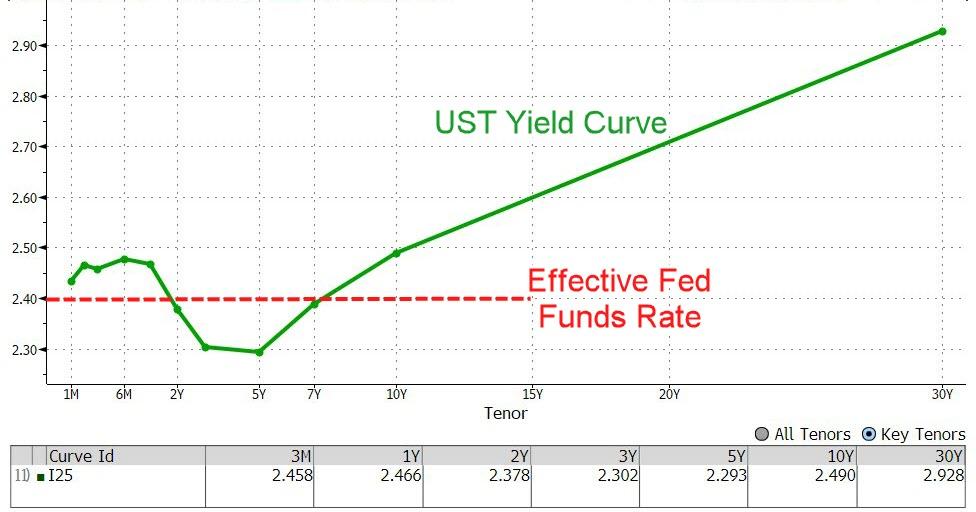

In fact, if you look at the Treasury yield curve, rates are basically lying flat along the bottom of the chart out to 48 months. Why? Because this nice fellow named Fed Chairman Jerome Powell, along with many other buyers, are gobbling up the available supply of risk free assets inside of five years.

Spreads on everything from junk bonds to agency mortgage passthroughs are contracting, suggesting that the private bid for paper remains strong. When you look at the fact that implied valuations for new production MBS and mortgage servicing rights (MSR) have been rising since July, this even though prepayment rates are astronomical, certainly implies that there is a great deal of cash sitting on the sidelines.

Remember that the price of an MSR is not just about cash flows and prepayments, but it’s also about default rates and the relationship with the consumer. We described in our last missive for The IRA Premium Service (“The Bear Case for Mortgage Lenders”), that a rising rate environment could generate catastrophic losses for residential lenders, particularly in the government loan market. We write:

“For both investors and risk professionals operating in the secondary mortgage market, the next several years contain both great opportunities and considerable risks. We look for the top lenders and servicers to survive the coming winter of default resolution that must inevitably follow a period of low interest rates by the FOMC. The result of the inevitable consolidation will be fewer, larger IMBs.”

Don’t get distracted by the rising rate song from the Street. We don’t look for short or medium term interest rates to rise in the near term or frankly for years. Agency 1.5% coupons “did not find a place in the latest Fed’s purchase schedule. It is possible (they) are included in the next update,” writes Nomura this week. This seems a pretty direct prediction of lower yields. But as one veteran mortgage operator cautions The IRA: “Not just yet.”

We don’t think that the Fed is going to take its foot off the short end of the curve anytime soon, in part because the system simply cannot withstand a sustained period of rising rates. In fact, we note that our friends at SitusAMC are adding 1.5% MBS coupons to forward rate models this month. But that does not necessarily mean that mortgage rates will fall any time soon.

We hear that the Fed of New York has bought a few 1.5s in recent days, but supply is sorely lacking. You see, the mortgage industry is not quite ready to print many new 1.5% MBS coupons and will not do so anytime soon. As the chart above suggests, mortgage rates are in fact rising. Why? Is not the FOMC in charge of the U.S mortgage market?

No, the market rules. Today you can make more money selling a new 1-4 family residential mortgage into a 2.5% coupon from Fannie, Freddie or Ginnie Mae at 105. You book a five point gain on sale and are therefore a hero. And a year from now, after the liquidity does in fact migrate down to 1.5s c/o the beneficence of the FOMC, you can again be a hero.

Specifically, you call up that same borrower and refinance the mortgage into a brand new 1.5% Fannie, Freddie or Ginnie Mae at 105. You take another five point gain on sale. Right? And who paid for this blessed optionality? The Bank of Japan, Peoples Bank of China, and PIMCO, among many other fortunate global investors.

These multinational holders of US mortgage bonds may not like negative returns on risk free American assets, but that’s life in the big city. And thankfully for Chairman Powell, it’s not his problem. Many years ago, a friend in the mortgage market said of loan repurchase demands from Fannie Mae: “What do you want from me?”

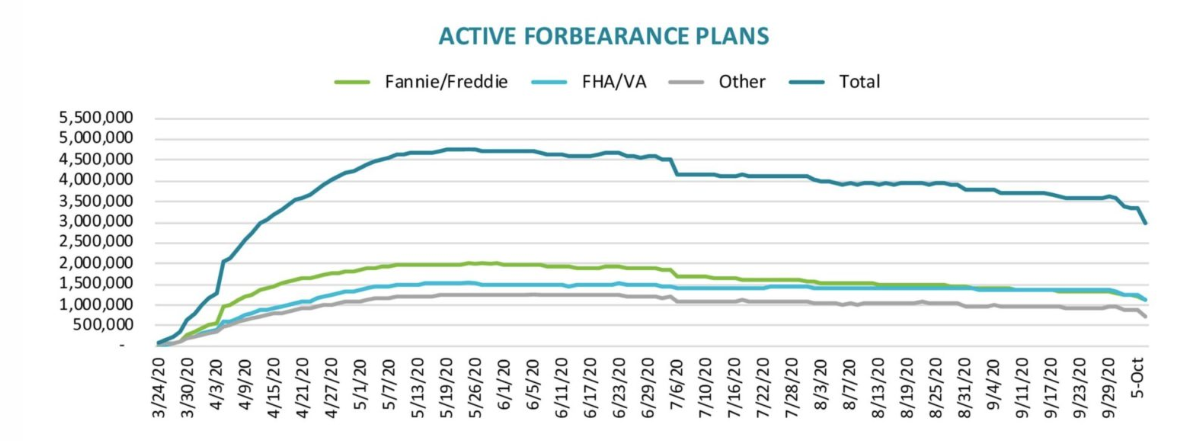

Number of Homeowners in COVID-19-Related Forbearance Plans Declined Sharply

(Calculated Risk) Note: Both Black Knight and the MBA (Mortgage Bankers Association) are putting out weekly estimates of mortgages in forbearance.

This data is as of October 6th.

From Forbearances See: Largest Single Week Decline Yet

After a slight uptick last week, active forbearance volumes plummeted over the past seven days, falling by 649K from the week prior. An 18% reduction in the number of active forbearances, this represents the largest single-week decline since the beginning of the pandemic and its related fallout in the U.S. housing market.

New data from Black Knight’s McDash Flash Forbearance Tracker shows that as the first wave of forbearances from April are hitting the end of their initial six-month term, the national forbearance rate has decreased to 5.6%. This figure is down from 6.8% last week, with active forbearances falling below 3 million for the first time since mid-April.

This decline noticeably outpaced the 435K weekly reduction we saw when the first wave of cases hit the three-month point back in July.

As of October 6, 2.97 million homeowners remain in COVID-19-related forbearance plans, representing $614 billion in unpaid principal.

… Though the market continues to adjust to historic and unprecedented conditions, these are clear signs of long-term improvement. We hope to see a continuation of the promising trend of forbearance reduction in the coming weeks, as an additional 800K forbearance plans are slated to reach the end of their initial six-month term in the next 30 days.

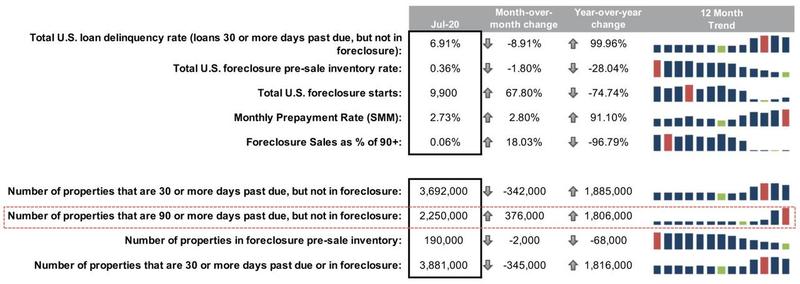

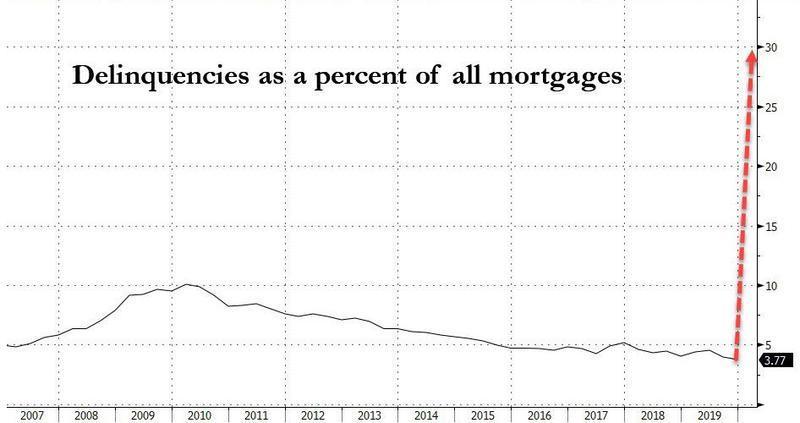

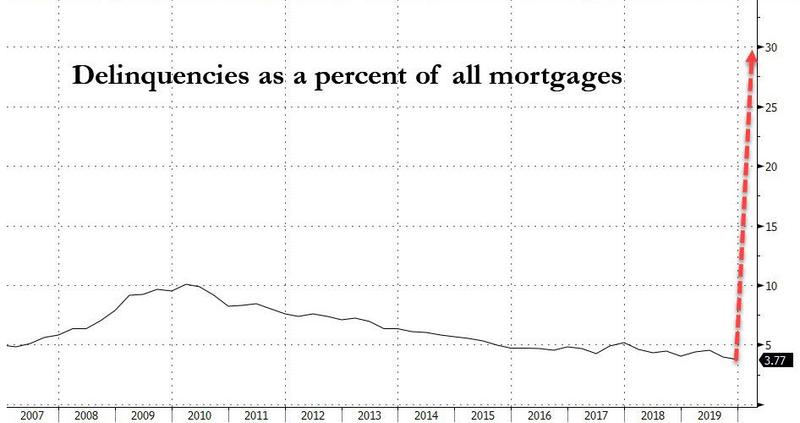

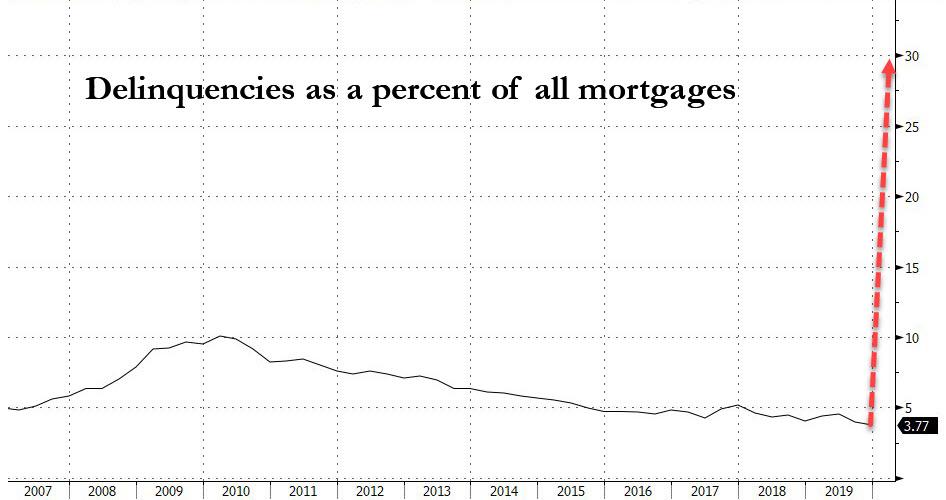

Mortgage Delinquencies Soar To Decade High

Readers may recall last week ZeroHedge outlined the dam of pent up mortgage delinquencies continued to crack, with the share of delinquent Federal Housing Administration’s loans hitting a record high in the second quarter.

With millions of Americans out of work due to the virus-induced recession, their personal income has become overly reliant on Trump stimulus checks, as we’ve outlined, a quarter of all personal income now comes from the government.

![]()

A fiscal cliff hit the economy on August 01, when the program to distribute stimulus checks to tens of millions of broke Americans ran out of funds. Even though President Trump signed an executive order to fund additional rounds of checks, only one state, as of August 21, has paid out new jobless benefits and paused evictions as stimulus talks in Washington have failed to materialize into a deal.

The number of homes with mortgage payments past due by 90 days or more rose by 376,000 in July to a total of 2.25 million. Serious mortgage delinquencies have jumped by 1.8 million since July 2019, a decade high, not seen since the last financial crisis.

Black Knight’s July 2020 Month-End Mortgage Performance Statistics:

Black Knight said, “foreclosure activity continues to remain muted due to widespread moratoriums; though starts rose for the month, overall activity remains near record lows.”

Cracks in the dam of pent up mortgage delinquencies are becoming larger as the presidential election nears. Still, millions of folks are unable to service mortgages, remain protected from foreclosure by the federal forbearance program, in which borrowers with pandemic-related hardships can delay payments for as much as a year without penalty. What happens when the program finally ends, and all the payments that were deferred come due could result in housing market weakness.

The prospect of a tidal wave of foreclosures could be ahead as the mortgage industry and government’s policies were merely short-term measures to push a housing crisis off until after the election.

If homeowners still can’t find jobs as the labor market recovery falters, then their ability to service future mortgage becomes impossible. At the same time, deep economic scarring is being realized, resulting in the shape of the economic recovery transforming from a “V” to a “Nike Swoosh.”

Even with part of the housing market booming, that is primarily due to folks ditching metro areas for suburbia and ultra-low mortgage rates pulling demand forward in such a massive way that today’s boom will lead to much lower activity in the future.

Think about it, millions of folks still can’t pay their mortgage, and many of them still can’t find jobs. But, of course, none of that matters as President Trump distracts the sheep and points to how well the Nasdaq is doing.

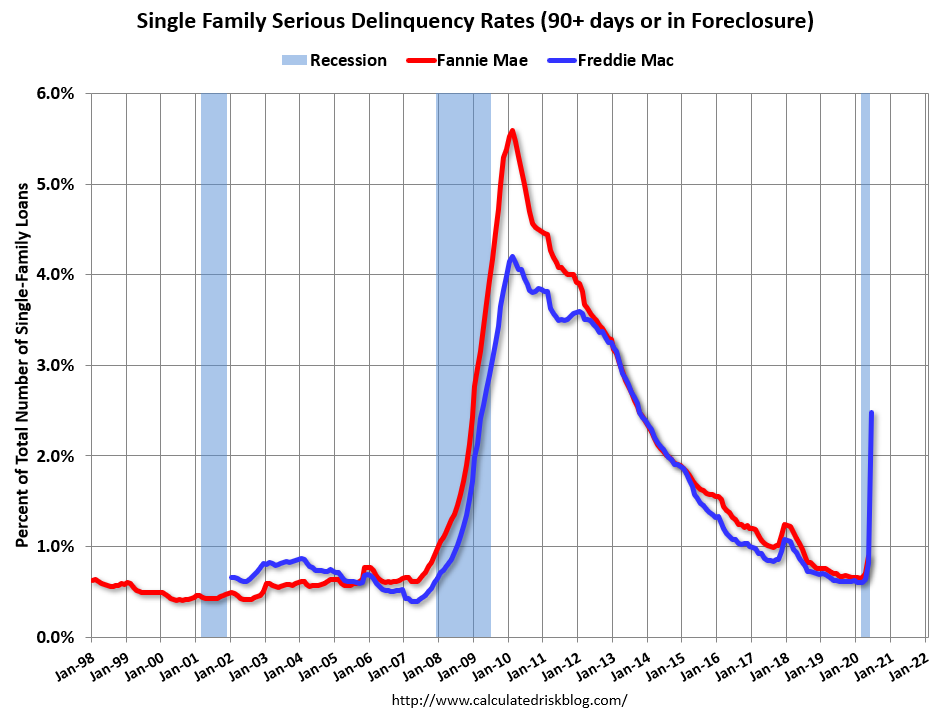

Freddie Mac: Mortgage Serious Delinquency Rate Increased Sharply In June, Highest In 7 Years

Freddie Mac reported that the Single-Family serious delinquency rate in June was 2.48%, up from 0.81% in May. Freddie’s rate is up from 0.63% in June 2019.

This is the highest serious delinquency rate since October 2013.

Freddie’s serious delinquency rate peaked in February 2010 at 4.20%.

These are mortgage loans that are “three monthly payments or more past due or in foreclosure”.

With COVID-19, this rate will increase significantly again in July (it takes time since these are mortgages three months or more past due).

Mortgages in forbearance are being counted as delinquent in this monthly report, but they will not be reported to the credit bureaus.

This is very different from the increase in delinquencies following the housing bubble. Lending standards have been fairly solid over the last decade, and most of these homeowners have equity in their homes – and they will be able to restructure their loans once they are employed.

Note: Fannie Mae will report for June soon.

Wells Fargo Names New Head Of Mortgage

(Reuters) – Wells Fargo & Co (WFC.N) said on Thursday it has hired Flagstar Bank’s Kristy Fercho to run its mortgage division following the retirement of 23-year veteran Michael DeVito from the company.

Fercho will oversee home lending operations of the largest mortgage lender in the United States during a time of uncertainty in the industry. She had run Flagstar’s mortgage business for the past three years.

Wells Fargo has pared back some mortgage offerings and raised requirements for certain kinds of loans during the coronavirus-fueled economic downturn. As of last month, the bank had received forbearance requests for roughly 13% of its mortgage balances, it has said.

Since taking over as chief executive late last year, Charles Scharf has shaken up leadership at the bank and installed a slew of former colleagues in top positions. In the wake of racial tensions across the United States, Scharf has also pledged to diversify the bank’s leadership team.

“She has been an inspiring and vocal leader across the mortgage industry while driving transformational growth at Flagstar,” said Mike Weinbach, new CEO of Consumer Lending at Wells Fargo, referring to Fercho, who is Black.

DeVito, who ran the mortgage division for two years, will retire later this summer.

Power Woman with Class Interview – Kristy Fercho

Mortgage Forbearance Surge Following A Three Week Decline

- The number of active mortgage forbearance plans rose by 79,000 in the past week, erasing roughly half of the improvement seen since the peak of May 22.

- Increases happened every day for the past five business days.

- As of Tuesday, 4.68 million homeowners were in forbearance plans, allowing them to delay their mortgage payments for at least three months.

- This represents 8.8% of all active mortgages, up from 8.7% last week.

After declining for three weeks, the number of borrowers delaying their monthly mortgage payments due to the coronavirus rose sharply once again.

The number of active forbearance plans rose by 79,000 in the past week, erasing roughly half of the improvement seen since the peak of May 22, according to Black Knight, a mortgage data and technology firm. By comparison, the number of borrowers in forbearance plans fell by 57,000 the previous week. Increases happened every day for the past five business days.

As of Tuesday, 4.68 million homeowners were in forbearance plans, allowing them to delay their mortgage payments for at least three months. This represents 8.8% of all active mortgages, up from 8.7% last week. Together, they represent just over $1 trillion in unpaid principal.

The mortgage bailout program, part of the CARES Act, which President Donald Trump signed into law in March, allows borrowers to miss monthly payments for at least three months and potentially up to a year. Those payments can be remitted either in repayment plans, loan modifications, or when the home is sold or the mortgage refinanced.

While some borrowers who initially asked for the mortgage bailouts in March and April ended up making their monthly payments, the vast majority now are not. There were expectations that the mortgage bailout numbers would improve as the economy reopened and job losses slowed. But this surge is a red flag to the market that homeowners are still struggling as coronavirus cases continue to increase in several states.

By loan type, 6.9% of all Fannie Mae and Freddie Mac-backed mortgages and 12.5% of all FHA/VA loans are currently in forbearance plans. Another 9.6% of loans in private label securities or banks’ portfolios are also in forbearance.

The volumes rose across all types of loans but were sharpest for FHA/VA loans. FHA offers low down payment loans to borrowers with lower credit scores. Such loans are popular among first-time home buyers. The number of FHA/VA borrowers in forbearance plans increased by 42,000 last week, while government-sponsored enterprise and non-agency loan forbearances increased by 25,000 and 12,000, respectively.

At today’s level, mortgage servicers may need to advance up to $3.5 billion per month to holders of government-backed mortgage securities on Covid-19-related forbearances. That is in addition to up to $1.4 billion in tax and insurance payments they must make on behalf of borrowers.

Why it’s impossible to stop SARS-CoV-2 and what can be done about it …

Weekly Mortgage Applications Point To A Remarkable Recovery In Home Buying

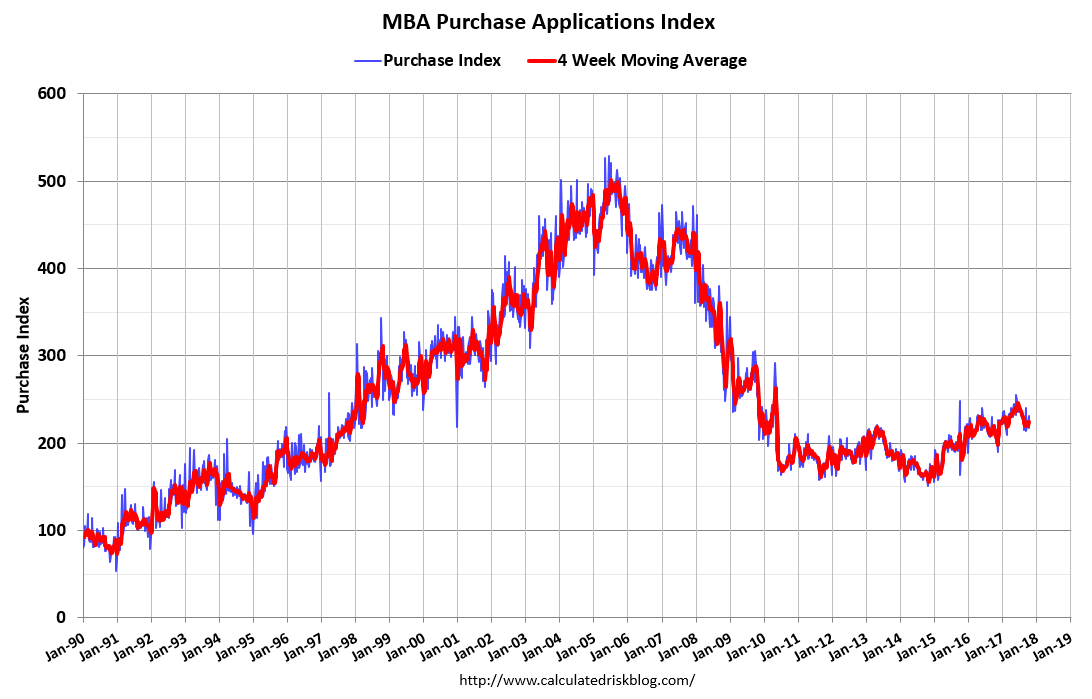

If mortgage demand is an indicator, buyers are coming back to the housing market far faster than anticipated, despite coronavirus shutdowns and job losses.

(CNBC) Mortgage applications to purchase a home rose 6% last week from the previous week, according to the Mortgage Bankers Association’s seasonally adjusted index. Purchase volume was just 1.5% lower than a year ago, a rather stunning recovery from just six weeks ago, when purchase volume was down 35% annually.

“Applications for home purchases continue to recover from April’s sizable drop and have now increased for five consecutive weeks,” said Joel Kan, an MBA economist. “Government purchase applications, which include FHA, VA, and USDA loans, are now 5 percent higher than a year ago, which is an encouraging turnaround after the weakness seen over the past two months.”

As states reopen, so are open houses, and buyers have been coming out in force, if masked. Record low mortgage rates, combined with strong pent-up demand from before the pandemic and a new desire to leave urban down towns due to the pandemic, are driving buyers back to the single-family home market. It remains to be seen if this is simply the pent-up demand or a long-term trend.

Buoying buyers, the average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances of up to $510,400 decreased to 3.41% from 3.43%. Points including the origination fee increased to 0.33 from 0.29 for 80 percent loan-to-value ratio loans.

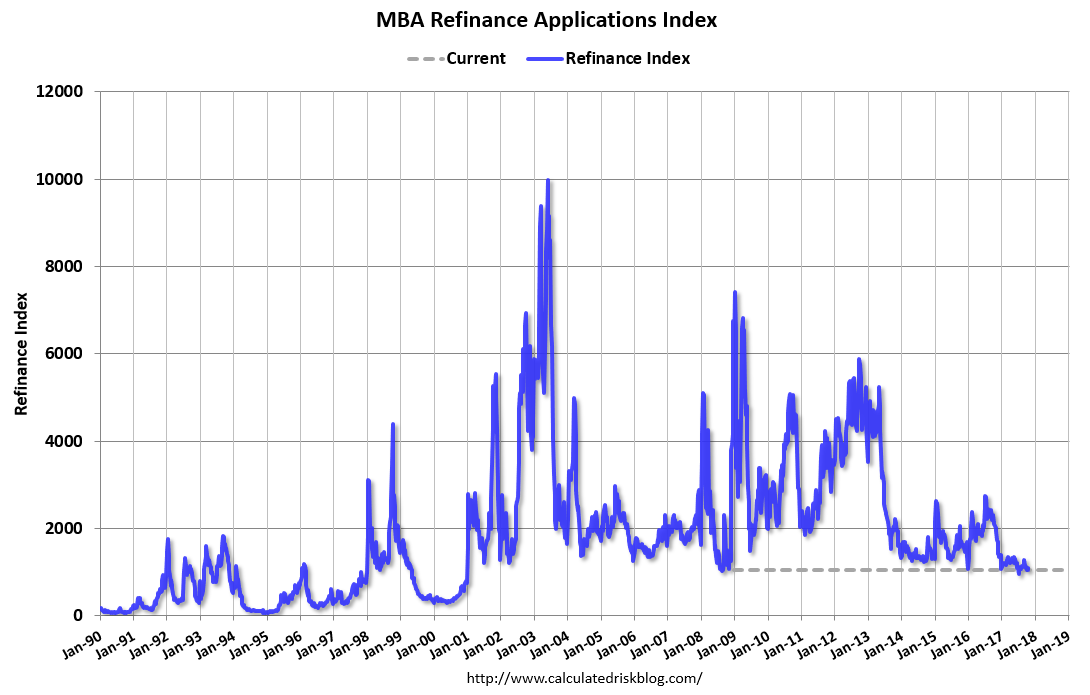

Low rates are not, however, giving current homeowners much incentive to refinance. Those applications fell 6% for the week but were still 160% higher than one year ago, when interest rates were 92 basis points higher. That is the lowest level of refinance activity in over a month.

“The average loan amount for refinances fell to its lowest level since January — potentially a sign that part of the drop was attributable to a retreat in cash-out refinance lending as credit conditions tighten,” said Kan. “We still expect a strong pace of refinancing for the remainder of the year because of low mortgage rates.”

Federal regulators this week changed lending guidelines for Fannie Mae and Freddie Mac, allowing refinances on loans that were or still are in the government’s mortgage bailout, part of the coronavirus relief package. Those loans can be refinanced once borrowers have made at least three regular monthly payments. Given tough economic conditions and rising unemployment, more borrowers may be looking to save money on their monthly payments.

Weaker refinance demand pushed total mortgage application volume down 2.6% for the week.

The refinance share of mortgage activity decreased to 64.3% of total applications from 67% the previous week. The share of adjustable-rate mortgage activity increased to 3.2% of total applications.

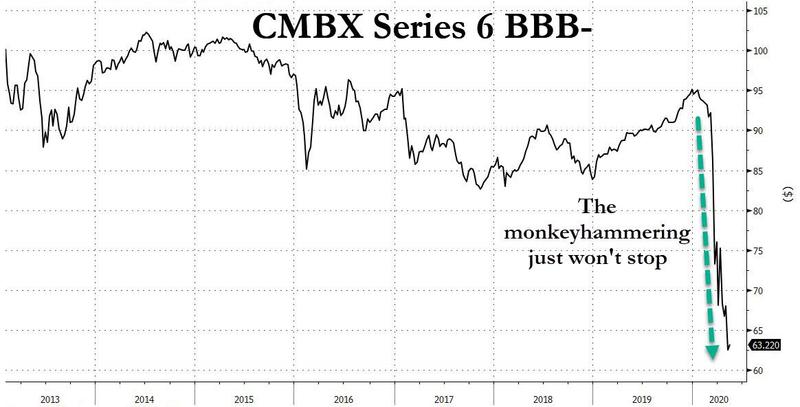

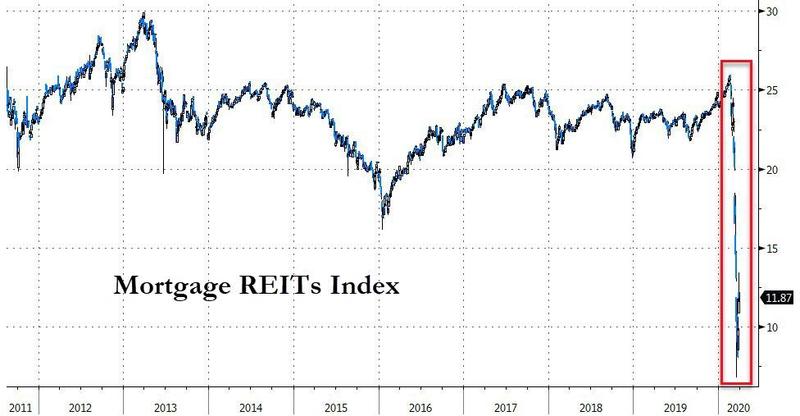

The “Big Short 2” Hits An All Time Low As Commercial Real Estate Implodes

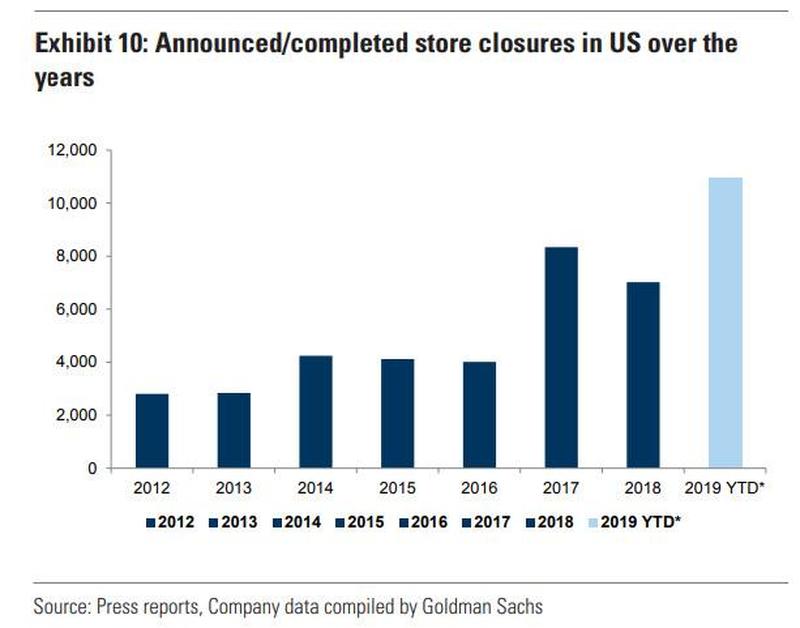

(ZeroHedge) Back in March 2017, a bearish trade emerged which quickly gained popularity on Wall Street, and promptly received the moniker “The Next Big Short.”

As we reported at the time, similar to the run-up to the housing debacle, a small number of bearish funds were positioning to profit from a “retail apocalypse” that could spur a wave of defaults. Their target: securities backed not by subprime mortgages, but by loans taken out by beleaguered mall and shopping center operators which had fallen victim to the Amazon juggernaut. And as bad news piled up for anchor chains like Macy’s and J.C. Penney, bearish bets against commercial mortgage-backed securities kept rising.

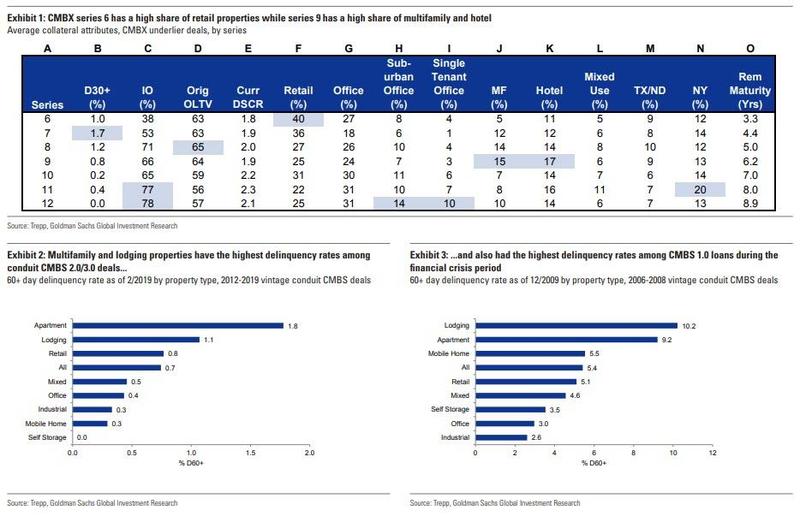

The trade was simple: shorting malls by going long default risk via CMBX 6 (BBB- or BB) or otherwise shorting the CMBS complex. For those who have not read our previous reports (here, here, here, here, here, here and here) on the second Big Short, here is a brief rundown via the Journal:

each side of the trade is speculating on the direction of an index, called CMBX 6, which tracks the value of 25 commercial-mortgage-backed securities, or CMBS. The index has grabbed investor attention because it has significant exposure to loans made in 2012 to malls that lately have been running into difficulties. Bulls profit when the index rises and shorts make money when it falls.

The various CMBX series are shown in the chart below, with the notorious CMBX 6 most notable for its substantial, 40% exposure to retail properties.

One of the firms that had put on the “Big Short 2” trade back in late 2016 was hedge fund Alder Hill Management – an outfit started by protégés of hedge-fund billionaire David Tepper – which ramped up wagers against the mall bonds. Alder Hill joined other traders which in early 2017 bought a net $985 million contracts that targeted the two riskiest types of CMBS.

“These malls are dying, and we see very limited prospect of a turnaround in performance,” said a January 2017 report from Alder Hill, which began shorting the securities. “We expect 2017 to be a tipping point.”

Alas, Alder Hill was wrong, because while the deluge of retail bankruptcies…

… and mall vacancies accelerated since then, hitting an all time high in 2019…

… not only was 2017 not a tipping point, but the trade failed to generate the kinds of desired mass defaults that the shorters were betting on, while the negative carry associated with the short hurt many of those who were hoping for quick riches.

One of them was investing legend Carl Icahn who as we reported last November, emerged as one of the big fans of the “Big Short 2“, although as even he found out, CMBX was a very painful short as it was not reflecting fundamentals, but merely the overall euphoria sweeping the market and record Fed bubble (very much like most other shorts in the past decade). The resulting loss, as we reported last November, was “tens if not hundreds of millions in losses so far” for the storied corporate raider.

That said, while Carl Icahn was far from shutting down his family office because one particular trade has gone against him, this trade put him on a collision course with two of the largest money managers, including Putnam Investments and AllianceBernstein, which for the past few years had a bullish view on malls and had taken the other side of the Big Short/CMBX trade, the WSJ reports. This face-off, in the words of Dan McNamara a principal at the NY-based MP Securitized Credit Partners, was “the biggest battle in the mortgage bond market today” adding that the showdown is the talk of this corner of the bond market, where more than $10 billion of potential profits are at stake on an obscure index.

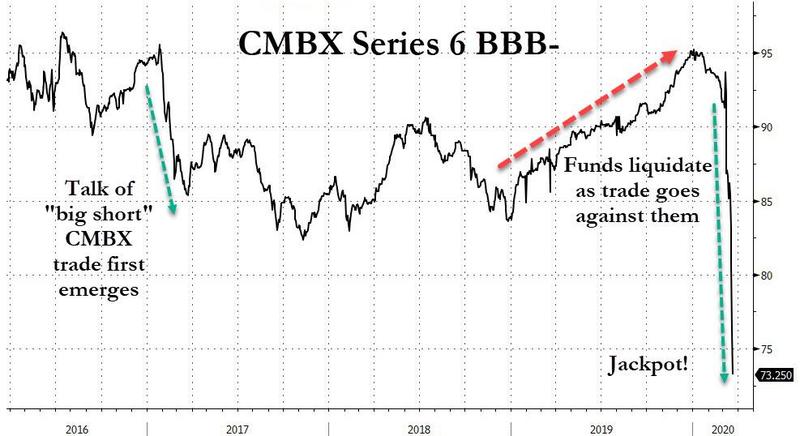

However, as they say, good things come to those who wait, and are willing to shoulder big losses as they wait for a massive payoffs, and for the likes of Carl Icahn, McNamara and others who were short the CMBX, payday arrived in mid-March, just as the market collapsed, hammering the CMBX Series BBB-.

And while the broader market has rebounded since then by a whopping 30%, the trade also known as the “Big Short 2” has continued to collapse and today CMBX 6 hit a new lifetime low of just $62.83, down $10 since our last update on this storied trade several weeks ago.

That, in the parlance of our times, is what traders call a “jackpot.”

Why the continued selling? Because it is no longer just retail outlets and malls: as a result of the Covid lock down, and America’s transition to “Work From Home” and “stay away from all crowded places”, the entire commercial real estate sector is on the verge of collapse, as we reported last week in “A Quarter Of All Outstanding CMBS Debt Is On Verge Of Default“

Sure enough, according to a Bloomberg update, a record 167 CMBS 2.0 loans turned newly delinquent in May even though only 25% of loans have reported remits so far, Morgan Stanley analysts said in a research note Wednesday, triple the April total when 68 loans became delinquent. This suggests delinquencies may rise to 5% in May, and those that are late but still within grace period track at 10% for the second month.

Looking at the carnage in the latest remittance data, and explaining the sharp leg lower in the “Big Short 2” index, Morgan Stanley said that several troubled malls that are a part of CMBX 6 are among the loans that were newly delinquent or transferred to special servicers. Among these:

- Crystal Mall in Waterford, Connecticut, is currently due for the April and May 2020 payments. There has been a marked decline in both occupancy and revenue. This loan accounts for nearly 10% of a CMBS deal called UBSBB 2012-C2

- Louis Joliet Mall in Joliet, Illinois, is also referenced in CMBX 6. The mall was originally anchored by Sears, JC Penney, Carson’s, and Macy’s. The loan is also a part of the CMBS deal UBSBB 2012-C2

- A loan for the Poughkeepsie Galleria in upstate New York was recently transferred to special servicing for imminent monetary default at the borrower’s request. The loan has exposure in two 2012 CMBS deals that are referenced by CMBX 6

- Other troubled mall-chain tenants include GNC, Claire’s, Body Works and Footlocker, according to Datex Property Solutions. These all have significant exposure in CMBX 6.

Of course, the record crash in the CMBX 6 BBB has meant that all those shorts who for years suffered the slings and stones of outrageous margin calls but held on to this “big short”, have not only gotten very rich, but are now getting even richer – this is one case where everyone will admit that Carl Icahn adding another zero to his net worth was fully deserved as he did it using his brain and not some crony central bank pumping the rich with newly printed money – it has also means the pain is just starting for all those “superstar” funds on the other side of the trade who were long CMBX over the past few years, collecting pennies and clipping coupons in front of a P&L mauling steamroller.

One of them is mutual fund giant AllianceBernstein, which has suffered massive paper losses on the trade, amid soaring fears that the coronavirus pandemic is the straw on the camel’s back that will finally cripple US shopping malls whose debt is now expected to default en masse, something which the latest remittance data is confirming with every passing week!

According to the FT, more than two dozen funds managed by AllianceBernstein have sold over $4 billion worth of CMBX protection to the likes of Icahn. One among them is AllianceBernstein’s $29 billion American Income Portfolio, which crashed after written $1.9bn of protection on CMBX 6, while some of the group’s smaller funds have even higher concentrations.

The trade reflected AB’s conviction that American malls are “evolving, not dying,” as the firm put it last October, in a paper entitled “The Real Story Behind the CMBX. 6: Debunking the Next ‘Big Short’” (reader can get some cheap laughs courtesy of Brian Philips, AB’s CRE Credit Research Director, at this link).

Hillariously, that paper quietly “disappeared” from AllianceBernstein’s website, but magically reappeared in late March, shortly after the Financial Times asked about it.

“We definitely still like this,” said Gershon Distenfeld, AllianceBernstein’s co-head of fixed income. “You can expect this will be on the potential list of things we might buy [more of].”

Sure, quadruple down, why not: it appears that there are still greater fools who haven’t redeemed their money.

In addition to AllianceBernstein, another listed property fund, run by Canadian asset management group Brookfield, that is exposed to the wrong side of the CMBX trade recently moved to reassure investors about its financial health. “We continue to enjoy the sponsorship of Brookfield Asset Management,” the group said in a statement, adding that its parent company was “in excellent financial condition should we ever require assistance.”

Alas, if the plunge in CMBX continues, that won’t be the case for long.

Meanwhile, as stunned funds try to make sense of epic portfolio losses, the denials got even louder: execs at AllianceBernstein told FT the paper losses on their CMBX 6 positions reflected outflows of capital from high-yielding assets that investors see as risky. They added that the trade outperformed last year. Well yes, it outperformed last year… but maybe check where it is trading now.

Even if some borrowers ultimately default, CDS owners are not likely to be owed any cash for several years, said Brian Phillips, a senior vice-president at AllianceBernstein.

He believes any liabilities under the insurance will ultimately be smaller than the annual coupon payment the funds receive. “We’re going to continue to get a coupon from Carl Icahn or whoever — I don’t know who’s on the other side,” Phillips added. “And they’re going to keep [paying] that coupon in for many years.”

What can one say here but lol: Brian, buddy, no idea what alternative universe you are living in, but in the world called reality, it’s a second great depression for commercial real estate which due to the coronavirus is facing an outright apocalypse, and not only are malls going to be swept in mass defaults soon, but your fund will likely implode even sooner between unprecedented capital losses and massive redemptions… but you keep “clipping those coupons” we’ll see how far that takes you. As for Uncle Carl who absolutely crushed you – and judging by the ongoing collapse in commercial real estate is crushing you with every passing day – since you will be begging him for a job soon, it’s probably a good idea to go easy on the mocking.

Afterthought: with CMBX 6 now done, keep a close eye on CMBX 9. With its outlier exposure to hotels which have quickly emerged as the most impacted sector from the pandemic, this may well be the next big short.

Worst Commercial Property Debt Crash in Years Looming For Workout Specialists (Fitch Says 26% of CMBS Borrowers Asked About Payment Relief)

First it was on-line shopping spearheaded by Amazon that helped crush physical retail space. Then the knock-out punch was the government shutdown of the the US economy.

(Bloomberg) — Emptied out malls and hotels across the U.S. have triggered an unprecedented surge in requests for payment relief on commercial mortgage-backed securities (CMBS), an early sign of a pandemic-induced real estate crisis.

Borrowers with mortgages representing almost $150 billion in CMBS, accounting for 26% of the outstanding debt, have asked about suspending payments in recent weeks, according to Fitch Ratings. Following the last financial crisis, delinquencies and foreclosures on the debt peaked at 9% in July 2011.

Special servicers — firms assigned to handle vulnerable CMBS loans — are bracing for the worst crash of their careers. They’re staffing up following years of downsizing to handle a wave of defaults, modification requests and other workouts, including potential foreclosures.

“Everything is happening at once,” said James Shevlin, president of CWCapital, a unit of private equity firm Fortress Investment Group and one of the largest special servicers. “It’s kind of exciting times. I mean, this is what you live for.”

No Relief

A surge in residential foreclosures helped ignite the last financial crisis. Now, commercial real estate is getting hit because the economic shutdown has shuttered stores and put travel on ice.

Not all of the borrowers who have requested forbearance will be delinquent or enter foreclosure, but Fitch estimates that the $584 billion industry could near the 2011 peak as soon as the third quarter of this year.

There’s no government relief plan for commercial real estate. Bankers usually have leeway to negotiate payment plans on commercial property, but options for borrowers and lenders are limited for CMBS.

Debt transferred to special servicers from master servicers, mostly banks that handle routine payment collections, is already swelling. Unpaid principal in workouts jumped to $22 billion in April, up 56% from a month earlier, according to the data firm Trepp.

Make Money

Special servicers make money by charging fees based on the unpaid principal on the loans they manage. Most are units of larger finance companies. Midland Financial, named as special servicer on approximately $200 billion of CMBS debt, is a unit of PNC Financial Services Group Inc., a Pittsburgh-based bank.

Rialto Capital, owned by private equity firm Stone Point Capital, was a named special servicer on about $100 billionof CMBS loans. LNR Partners, which finished 2019 with the largest active special-servicer portfolio, is owned by Starwood Property Trust, a real estate firm founded by Barry Sternlicht.

Sternlicht said during a conference call on Monday that special servicers don’t “get paid a ton money” for granting forbearance.

“Where the servicer begins to make a lot of money is when the loans default,” he said. “They have to work them out and they ultimately have to resolve the loan and sell it or take back the asset.”

Hardball

Like debt collectors in any industry, special servicers often play hardball, demanding personal guarantees, coverage of legal costs and complete repayment of deferred installments, according to Ann Hambly, chief executive officer of 1st Service Solutions, which works for about 250 borrowers who’ve sought debt relief in the current crisis.

“They’re at the mercy of this handful of special servicers that are run by hedge funds and, arguably, have an ulterior motive,” said Hambly, who started working for loan servicers in 1985 before switching sides to represent borrowers.

But fears about self-dealing are exaggerated, according to Fitch’s Adam Fox, whose research after the 2008 crisis concluded most special servicers abide by their obligations to protect the interests of bondholders.

“There were some concerns that servicers were pillaging the trust and picking up assets on the cheap,” he said. “We just didn’t find it.”

Troubled Hotels

Hotels, which have closed across the U.S. as travelers stay home, have been the fastest to run into trouble during the pandemic. More than 20% of CMBS lodging loans were as much as 30 days late in April, up from 1.5% in March, according to CRE Finance Council, an industry trade group. Retail debt has also seen a surge of late payments in the last 30 days.

Special servicers are trying to mobilize after years of downsizing. The seven largest firms employed 385 people at the end of 2019, less than half their headcount at the peak of the last crisis, according to Fitch.

Miami-based LNR, where headcount ended last year down 40% from its 2013 level, is calling back veterans from other duties at Starwood and looking at resumes.

CWCapital, which reduced staff by almost 75% from its 2011 peak, is drafting Fortress workers from other duties and recruiting new talent, while relying on technology upgrades to help manage the incoming wave more efficiently.

“It’s going to be a very different crisis,” said Shevlin, who has been in the industry for more than 20 years.

Ya think?

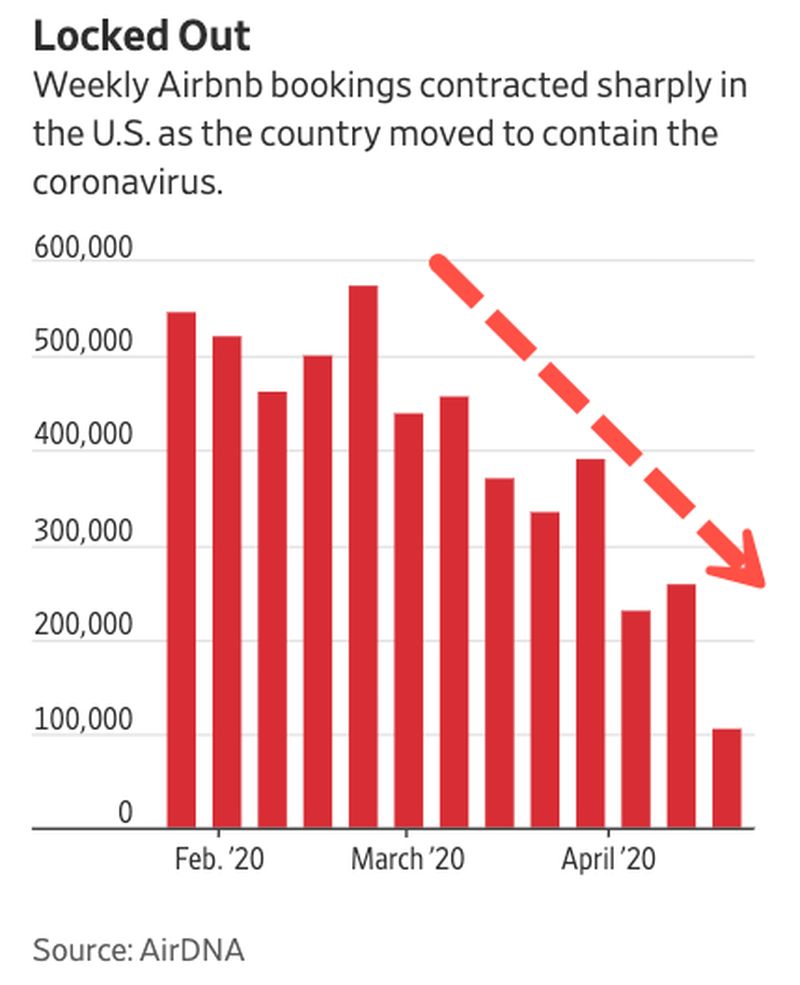

“Holy God. We’re About To Lose Everything” – Pandemic Crushes Over Leveraged Airbnb Superhosts

History doesn’t repeat itself, but it often rhymes,” as Mark Twain is often reputed to have said. Before the 2007-2008 GFC, people built real estate portfolios based around renters. We all know what happened there; once consumers got pinched in the GFC, rent payments couldn’t be made, and it rippled down the chain and resulted in landlords foreclosing on properties. Now a similar event is underway, that is, over leveraged Airbnb Superhosts, who own portfolios of rental properties built on debt, are now starting to blow up after the pandemic has left them incomeless for months and unable to service mortgage debt.

Zerohedge described the financial troubles that were ahead for Superhosts in late March after noticing nationwide lock downs led to a crash not just in the tourism and hospitality industries, but also a plunge in Airbnb bookings. It was to our surprise that Airbnb’s management understood many of their Superhosts were over leveraged and insolvent, which forced the company to quickly erect a bailout fund for Superhosts that would cover part of their mortgage payments in April.

The Wall Street Journal has done the groundwork by interviewing Superhosts that are seeing their mini-empires of short-term rental properties built on debt implode as the “magic money” dries up.

Cheryl Dopp,54, has a small portfolio of Airbnb properties with monthly mortgage payments totaling around $22,000. She said the increasing rental income of adding properties to the portfolio would offset the growing debt. When the pandemic struck, she said $10,000 in rental income evaporated overnight.

“I made a bargain with the devil,” she said while referring to her financial misery of being overleveraged and incomeless.

Dopp said when the pandemic lock downs began, “I thought, ‘Holy God. We’re about to lose everything.'”

Market-research firm AirDNA LLC said $1.5 billion in bookings have vanished since mid-March. Airbnb gave all hosts a refund, along with Superhosts, a bailout (in Airbnb terms they called it a “grant”).

“Hosts should’ve always been prepared for this income to go away,” said Gina Marotta, a principal at Argentia Group Inc., which does credit analysis on real estate loans. “Instead, they built an expensive lifestyle feeding off of it.”

We noted that last month, “Of the four million Airbnb hosts across the world, 10% are considered “Superhosts,” and many have taken out mortgages to accumulate properties to build rental portfolios.”

Airbnb spokesman Nick Papas said the decline in bookings and slump in the tourism and travel industry is “temporary: Travel will bounce back and Airbnb hosts—the vast majority of whom have just one listing—will continue to welcome guests and generate income.”

Papas’ optimism about a V-shaped recovery has certainly not been echoed in the petroleum and aviation industry. Boeing CEO Dave Calhoun warned on Tuesday that air travel growth might not return to pre-corona levels for years. Fewer people traveling is more bad news for Airbnb hosts that a slump could persist for years, leading to the eventual deleveraging of properties.

AirDNA has determined that a third of Airbnb’s US hosts have one property. Another third have two and 24 properties and get ready for this: a third have more than 24.

Startups such as Sonder Corp. and Lyric Hospitality Inc. manage properties for hosts that have 25+ properties. Many of these companies have furloughed or laid off staff in April.

Jennifer Kelleher-Hazlett of Clawson, Michigan, spent $380,000 on two properties in 2018. She and her husband borrowed $100,000 to furnish each. Rental income would net up to $7,000 per month from Airbnb after mortgage payments, which would supplement her income as a part-time pharmacist and husband’s work in academia.

Before the virus struck, both were expecting to buy more homes – now they can’t make the payments on their Airbnb properties because rental income has collapsed. “We’re either borrowing more or defaulting,” she said.

Here’s another Airbnb horror story via The Journal:

“That sum would provide little relief to hosts such as Jennifer and David Landrum of Atlanta. In 2016, they started a company named Local, renting the 18 apartments they leased and 21 apartments they managed to corporate travelers and film-industry workers. They spent more than $14,000 per apartment to outfit them with rugs, throw pillows, art and chandeliers. They grossed about $1.5 million annually, mostly through Airbnb, Ms. Landrum said.

They spend about $50,000 annually with cleaning services, about $25,000 on an inspector and $30,000 a year on maintenance staff and landscapers, Ms. Landrum said, not to mention spending on furnishings.

When Airbnb began refunding guests March 14, the Landrums had nearly $40,000 in cancellations, she said. The couple has been able to pay only a portion of April rent on the 18 apartments they lease and can’t fulfill their obligations to pay three months’ rent unless bookings resume. They have reduced pay to cleaning staff and others. Adding to the stress, Georgia banned short-term rentals through April.

“It’s scary,” said Ms. Landrum, who said she has discounted some units three times since mid-March. The Landrums have negotiated to get some leniency from apartment owners on their leases. If not, Ms. Landrum said, they would have to sell their house.”

To make matters worse, and this is exactly what we warned about last month, Airbnb Superhosts are now panic selling properties:

Greg Hague, who runs a Phoenix real-estate firm, said Airbnb hosts are “desperate to sell properties” in April.

“There’s been a flood of people. You have people coming to us saying, ‘I’m a month or two away from foreclosure. What’s it going to take to get it sold now?'” Hague said.

And here’s what we said in March: “We might have discovered the next big seller that could ruin the real estate market: Airbnb Superhosts that need to get liquid.”

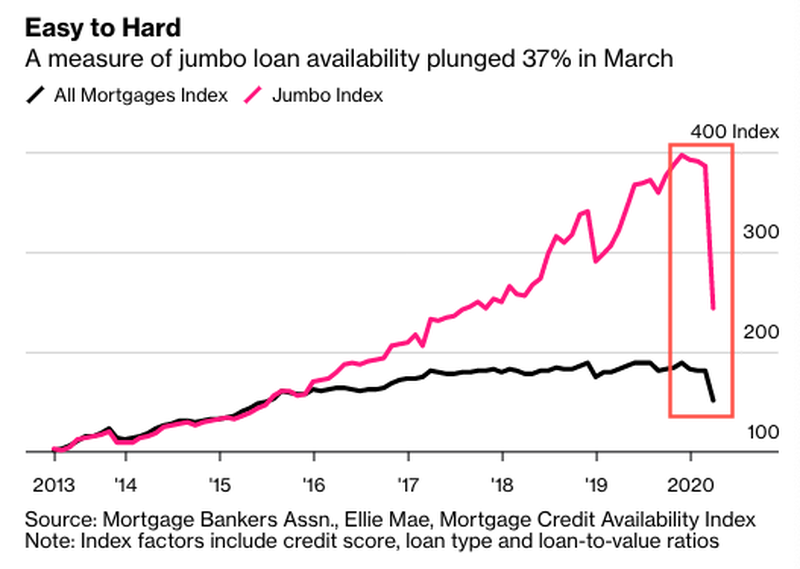

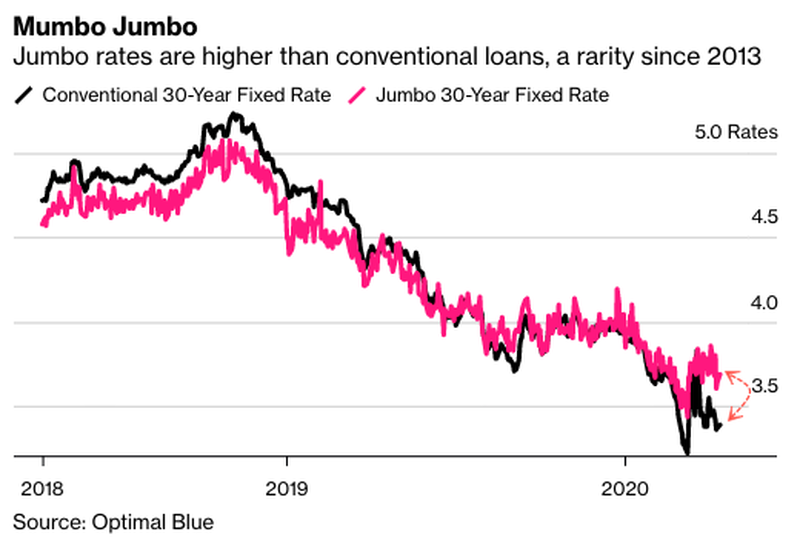

“There’s No Liquidity” – Mortgage Lenders Abandon “No Brainer” Jumbo Mortgages

The jumbo loan market is facing a classic liquidity crunch. A perfect storm is brewing as millions of homeowners are seeking forbearances as the economy crashes into depression from coronavirus lock downs, and firms who usually bundle up jumbo loans have immediately exited the market.

Jumbo loans are mortgages for the best credit risk borrowers who want to purchase mansions. In pre-corona times, lenders were falling over each other to welcome jumbo borrowers, but not anymore.

Greg McBride, the Bankrate chief financial analyst, recently said demand has dried up for jumbo mortgages as investors shift to mortgage bonds for government-backed loans where “they’re assured of receiving payments even if large numbers of borrowers are in forbearance.”

“Most mortgages get made by lenders who then sell it to someone else,” McBride said. “If there is no willing buyer, lenders will stop closing loans so as not to be stuck holding the bag.”

Tendayi Kapfidze, the chief economist at LendingTree Inc., said in normal times, jumbo loans were all the rage. Now because these loans “don’t have the government guarantee, a lot of those loans end up on the bank balance sheet.”

According to Optimal Blue, a Texas-based firm that monitors mortgage rates, lenders are charging more for jumbos than conventional mortgages, and this is the first time in seven years. Lenders have also tightened lending standards for wealthy households.

David Adler, an aerospace executive in Irvine, California, told Bloomberg that he thought it would be easy to get a jumbo loan at a rate of 3.7% on his $700,000 home. Even with excellent credit, he was told the rate would be much higher.

“I told the guy at the bank, ‘I’m trying to use logic here,'” Adler said in an interview. “And he said, ‘That’s your problem.'”

The Mortgage Bankers Association said the availability for jumbo loans has plunged by 37% since March, making it harder for the best credit risk borrowers to get jumbos versus all other mortgages.

Before the pandemic, lenders welcomed jumbo borrowers, but now, since the economy crashed and 22 million people have lost their jobs, with the expectation the economic downturn could extend into 2021, the market for jumbos has dried up, hence why rates are surging.

Lenders are pulling out of the jumbo loan market because a correction in real estate could be nearing, and many of the loans aren’t government guaranteed.

Wells Fargo has suspended the purchase of jumbo loans from other lenders, but not “direct-to-consumer originations through their retail mortgage channel,” said Tom Goyda, senior VP of consumer lending communications at Wells Fargo.

“Due to unprecedented market conditions, Wells Fargo Home Lending is temporarily suspending the purchase of non-conforming mortgage loans from correspondent sellers, effective immediately and until business conditions stabilize,” Goyda said in an email statement to Bloomberg. “This difficult business decision reflects efforts to prioritize how we serve customers and maintain prudent balance sheet discipline.”

Truist Financial Corp. and Flagstar Bancorp Inc. are other banks that have “pulled back by limiting refinancings, suspending their purchases of new loans made by correspondent lenders or pulling short-term credit lines from smaller mortgage companies they fund that make jumbo loans,” said Bloomberg.

Freedom Mortgage Corp. CEO Stanley Middleman said much of the pullback is from investors who would typically buy these loans no longer want them because of the challenging economic conditions.

“Whether the assets are good or not good is irrelevant because there’s no liquidity to buy them,” Middleman said.

Damon Germanides, a broker at Beverly Hills-based Insignia Mortgage, said closing loans is getting much more difficult than ever before. He said a wealthy client that has good credit and owns a business in the area might not be able to qualify for a mortgage.

“A month ago, he was a no-brainer,” Germanides said. “Now he’s 50-50.”

Last week, JPMorgan scrambled to raise borrowing standards on new home loans as the “moves to mitigate lending risk stemming from the novel coronavirus disruption.”

JPM also reported that its loan loss provision surged fivefold to over $8.2 billion for the first quarter, the biggest quarterly increase since the financial crisis.

The bank also said it would stop accepting new home equity lines of credit, or HELOC, applications.

And as a reminder, we noted earlier this month the residential mortgage market is already free falling after borrower requests to delay mortgage payments exploded by 1,896% in the second half of March. Moody’s Analytics predicted as many as 30% of Americans with home loans – about 15 million households – could stop paying if lock downs continued through summer.

Getting Out Of Dodge: After Exiting Loans And Hiking Mortgage Standards, JPMorgan Stops Accepting HELOCs

The largest US bank is quietly shutting down ahead of a historic default shit storm that is about to hit the U.S.

Earlier this week, JPMorgan reported that its loan loss provision surged five fold to over $8.2 billion for the first quarter, the biggest quarterly increase since the financial crisis (even if its total reserve for losses is still a fraction of what it was during the 2008-2009 crash).

And while Jamie Dimon was mum on how much more losses the bank may be forced to take in coming quarters to offset the coming default surge (something we discussed in Houston: The Banks Have A Huge Problem), it hinted that things are about to get much worse when it first halted all non-Paycheck Protection Program based loan issuance for the foreseeable future (i.e., all non-government guaranteed loans) because as we said “the only reason why JPMorgan would “temporarily suspend” all non-government backstopped loans such as PPP, is if the bank expects a default tsunami to hit coupled with a full-blown depression that wipes out the value of any and all assets pledged to collateralize the loans.”

Then, just a few days later, the bank also said it would raise its mortgage standards, stating that customers applying for a new mortgage will need a credit score of at least 700, and will be required to make a down payment equal to 20% of the home’s value, a dramatic tightening since the typical minimum requirement for a conventional mortgage is a 620 FICO score and as little as 5% down. Reuters echoed our gloomy take, stating that “the change highlights how banks are quickly shifting gears to respond to the darkening U.S. economic outlook and stress in the housing market, after measures to contain the virus put 16 million people out of work and plunged the country into recession.”

In short, JPM appears to be quietly exiting the origination of all interest income generating revenue streams over fears of the coming recession, which prompted us to ask“just how bad will the US depression get over the next few months if JPMorgan has just put up a “closed indefinitely” sign on its window.”

That question was especially apt today, when JPM exited yet another loan product, when it announced that it has stopped accepting new home equity line of credit, or HELOC, applications. The bank confirmed that this change was made due to the uncertainty in the economy, and didn’t give an end date to the pause according to the Motley Fool.

Like in the other previous exits, the move doesn’t affect customers who already have HELOCs with the bank. They’ll still be able to withdraw funds on their existing HELOCs as they wish.

With HELOCs generally seen as riskier for banks than purchase or refinance mortgages as they represent a second lien on the home, it was only a matter of time before the bank – which had already exited new first-lien loan issuance would but up a “closed” sign on this particular product.

In short, JPMorgan wants no part of the shit storm that is about to be unleashed on middle America, and especially the housing sector which is about to be hammered like never before.

While the U.S. housing market was on a steady footing earlier this year, all hell broke loose as a result of the economic paralysis and deepening depression resulting from the Coronavirus pandemic. And with would-be home buyers unable to view properties or close purchases due to social distancing measures, the health crisis now threatens to derail the sector, especially as banks are going to make it next to impossible to get a new mortgage.

To be sure, as we reported last week the residential mortgage market is already free falling after borrower requests to delay mortgage payments exploded by 1,896% in the second half of March. And unfortunately, this is just the beginning: last week, Moody’s Analytics predicted that as much as 30% of homeowners – about 15 million households – could stop paying their mortgages if the U.S. economy remains closed through the summer or beyond. Bloomberg called this the “biggest wave of delinquencies in history.”

This would result in a housing market depression and would lead to tens of billions in losses for mortgage servicers and originators such as JPMorgan.

Fight Over Commercial Rent Gets Ugly With Default Wave Looming

(Bloomberg) — Tension is rising in the messy fight over commercial rent payments.

With stores shuttered, struggling retailers are skipping rent and asking for concessions, while landlords are demanding payment and having their own tricky conversations with lenders.

There are no easy answers as officials ponder how to safely get the economy back open. So far this month, some mall owners and other retail landlords collected as little as 15% of what they were owed, according to one estimate. And it’s expected to get worse, with more than $20 billion in rent payments coming due in May.

“It’s all over the map what’s happening out there,” said Tom Mullaney, a managing director in restructuring at Jones Lang LaSalle Inc. “More and more defaults are coming in every single day.”

Companies across the U.S. — from small mom-and-pop operations to giant corporations — have missed April payments or sent out relief requests citing store closures because of the pandemic.

Pushing Back

Landlords have been pitching rent deferment, saying tenants can make reduced payments now as long as they pay the balance at some point. Some businesses are pushing back on that option and asking for rent cuts even after stores are open again.

U.S. retail landlords typically collect more than $20 billion in rent each month, according to data from CoStar Group Inc. So far, April rent collection has ranged from 15% to 30% for landlords with higher concentrations of shuttered businesses, according to an estimate from brokerage firm Marcus & Millichap.

Landlords, who are facing their own debt defaults, are getting frustrated. Some are complaining that large corporations are using the crisis to skip out on rent. Others say they’re not responsible for bailing out tenants and that the federal government or insurance companies should cover the costs instead.

“The landlords are triaging the battlefield,” said Gene Spiegelman, vice chairman at Ripco Real Estate Corp. “The super powerful and strong are not going to get any help and the ones that’ll die anyways, landlords will say why would I help them?”

Some Pay

To be sure, some landlords and tenants are working out deals on a case-by-case basis. And some companies are paying rent for their stores. That includes AT&T Inc. and T-Mobile USA Inc. according to people familiar with the matter. J.C. Penney also said it paid for April.

Ross Stores Inc. and fitness chain Solidcore, meanwhile, are among those standing firm on requests for rent abatements and asking for additional concessions. Williams-Sonoma Inc. is another chain that has stopped paying rent, according to people familiar.

Ross has told landlords that after the shutdown ends their rent on some stores should be cut until sales rebound. Solidcore hasn’t agreed to rent deferral and said it likely won’t be able to pay the same rent as it was before pandemic.

“We’re not going to be bullied by the landlords during this time,” said Anne Mahlum, the fitness company’s founder and chief executive officer said. “We have some leverage here. What are they going to do, say get out and then have vacancy for months on end?”

Backfire

Tenants’ refusal to pay will likely backfire, according to Jackson Hsieh, CEO of retail landlord Spirit Realty Capital Inc.

The firm, which owns more than 1,700 properties, has seen requests for rent relief since the crisis started. But several of those tenants ended up paying, according to Hsieh.

One agreed to pay after getting loans from the government’s relief package, while another did so after being asked to provide financial information. A discount retailer and a company in the auto industry paid after Spirit refused to consider their rent deferral requests.

“If a tenant just says I’m not going to pay, fine, I’ll default you, I’m going to go to the courts, and you have 30 days to pay or quit,” Hsieh said. “I don’t want to be negative, but we own the building.”

Pending Loans

Many landlords are rushing to work out deals with lenders to stave off their own defaults. Banks and insurance companies are negotiating deals on a case-by-case basis, but borrowers in commercial mortgage-backed securities have fewer options.

About 11% of U.S. CMBS retail property loan borrowers have been late on April payments so far, according to preliminary analysis by data firm Trepp. If that number holds up, $13 billion worth of CMBS loans could miss payments for the month.

“The banks are a little more fluid and often there’s recourse,” said Camille Renshaw, CEO brokerage firm B+E. “But many large properties have CMBS debt and when there’s a crisis, no one is there to pick up the phone to negotiate.”

It’s just not retail stores that are suffering. Office space is a ghost town thanks to the Wuhan (bat) virus outbreak. But with tools like Zoom, Webex, Microsoft Teams, GotoMeeting, Skype, etc., one wonders if the days of massive office building demand is over. Other than for socializing and monitoring employees (as Bill Lumbergh did in “Office Space.”)

Of course, administrators can always contact you at home during virtual classes.

PennyMac Warns Mortgage Originators That Forbearance Buybacks Could Be Coming

(HousingWire) With the housing industry at large raising alarms about mortgage servicers’ desperate need for liquidity as more borrowers are requesting forbearance, the nation’s largest mortgage aggregator is now warning originators that it could force them to buy back loans that go into forbearance.

Late last week, PennyMac, which grew last year into the largest mortgage aggregator in the country, told its correspondent originators that it will not buy any loan that is currently in forbearance.

Beyond that, PennyMac also said that it may force originators to buy back a loan that goes into forbearance within 15 days of PennyMac buying it.

“Any loan in forbearance or for which forbearance has been requested is not eligible for purchase by PennyMac,” the company said in a note to originators. “Additionally, any loan that is in forbearance or for which forbearance has been requested up to 15 days post purchase by PennyMac may result in a repurchase.”

The move by PennyMac is a notable one considering its status as the largest mortgage aggregator in the country last year, according to data from Inside Mortgage Finance.

As an aggregator, PennyMac purchases loans from smaller originators, which then allows those smaller lenders to continue originating.

Per the company’s latest 10-K filing with the Securities and Exchange Commission, PennyMac purchased nearly $50 billion in loans through its correspondent channel last year. Of those, PennyMac asked for a repurchase on just over $12 million in loans.

But that could change as more borrowers are requesting forbearance due to loss of income or employment in the wake of the spread of the coronavirus.

The latest data from the Department of Labor shows that nearly 10 million people have filed for unemployment in the last few weeks, and that number is expected to continue to climb.

The massive surge in unemployment in recent weeks will likely lead to a significant number of forbearance requests, as under the CARES Act, homeowners with federally backed mortgages can request forbearance of up to 12 months.

That’s leading companies like PennyMac to take steps to protect themselves because they don’t want to be on the hook for advancing the principal and interest to investors, as they are required to do when a loan goes into forbearance.

And without clarification from the government on what will happen to servicers as loans go into forbearance, odds are that PennyMac won’t be the only aggregator to make such a move.

“The COVID-19 epidemic has caused unprecedented disruption to the lives and incomes of many current and prospective mortgage borrowers throughout the country,” PennyMac said in its announcement. “In this challenging time, it is important that borrowers whose ability to repay a mortgage loan has been compromised be directed to appropriate borrower assistance programs while new loans be made available for those borrowers who maintain the capacity to make payments.”

Worse Than 2008? We’re Being Warned That The Shutdown “Could Collapse The Mortgage Market”

The cascading failures that have been set into motion by this “coronavirus shutdown” are going to make the financial crisis of 2008 look like a Sunday picnic. As you will see below, it is being estimated that unemployment in the U.S. is already higher than it was at any point during the last recession. That means that millions of American workers no longer have paychecks coming in and won’t be able to pay their mortgages. On top of that, the CARES Act actually requires all financial institutions to allow borrowers with government-backed mortgages to defer payments for an extended period of time. Of course this is a recipe for disaster for mortgage lenders, and industry insiders are warning that we are literally on the verge of a “collapse” of the mortgage market.

Never before in our history have we seen a jump in unemployment like we just witnessed. If you doubt this, just check out this incredible chart.

:format(webp):no_upscale()/cdn.vox-cdn.com/uploads/chorus_asset/file/19866745/unemployment_chart_2_UPDATE.jpg)

Millions upon millions of American workers are now facing a future with virtually no job prospects for the foreseeable future, and former Fed Chair Janet Yellen believes that the unemployment rate in the U.S. is already up to about 13 percent…

Former Federal Reserve Chair Janet Yellen told CNBC on Monday the economy is in the throes of an “absolutely shocking” downturn that is not reflected yet in the current data.

If it were, she said, the unemployment rate probably would be as high as 13% while the overall economic contraction would be about 30%.

If Yellen’s estimate is accurate, that means that unemployment in this country is already significantly worse than it was at any point during the last recession.

And young adults are being hit particularly hard during this downturn…

As measures to slow the pandemic decimate jobs and threaten to plunge the economy into a deep recession, young adults such as Romero are disproportionately affected. An Axios-Harris survey conducted through March 30 showed that 31 percent of respondents ages 18 to 34 had either been laid off or put on temporary leave because of the outbreak, compared with 22 percent of those 35 to 49 and 15 percent of those 50 to 64.

As I have documented repeatedly over the past several years, most Americans were living paycheck to paycheck even during “the good times”, and so now that disaster has struck there will be millions upon millions of people that will not be able to pay their mortgages.

A broad coalition of mortgage and finance industry leaders on Saturday sent a plea to federal regulators, asking for desperately needed cash to keep the mortgage system running, as requests from borrowers for the federal mortgage forbearance program are pouring in at an alarming rate.

The Cares Act mandates that all borrowers with government-backed mortgages—about 62% of all first lien mortgages according to Urban Institute—be allowed to delay at least 90 days of monthly payments and possibly up to a year’s worth.

Needless to say, many in the mortgage industry are absolutely furious with the federal government for putting them into such a precarious position, and one industry insider is warning that we could soon see the “collapse” of the mortgage market…

“Throwing this out there without showing evidence of hardship was an outrageous move, outrageous,” said David Stevens, who headed the Federal Housing Administration during the subprime mortgage crisis and is a former CEO of the Mortgage Bankers Association.

“The administration made a huge mistake bringing moral hazard in and thrust extraordinary risk into the private sector that could collapse the mortgage market.”

Of course a lot of other industries are heading for immense pain as well.

At this point, even JPMorgan Chase CEO Jamie Dimon is admitting that the U.S. economy as a whole is plunging into a “bad recession”…

Jamie Dimon said the U.S. economy is headed for a “bad recession” in the wake of the coronavirus pandemic, but this time around his company is not going to need a bailout. Instead, JPMorgan Chase is ready to lend a hand to struggling consumers and small businesses.

“At a minimum, we assume that it will include a bad recession combined with some kind of financial stress similar to the global financial crisis of 2008,” Dimon, the CEO of JPMorgan Chase, said Monday in his annual letter to shareholders.

And the longer this coronavirus shutdown persists, the worse things will get for our economy.

In fact, economist Stephen Moore is actually predicting that we will be “facing a potential Great Depression scenario” if normal economic activity does not resume in a few weeks…

Sunday on New York AM 970 radio’s “The Cats Round Table,” economist Stephen Moore weighed in on the potential impact of the coronavirus to the United States economy.

Moore warned the nation could be “facing a potential Great Depression scenario” if the United States stays on lock down much past the beginning of May, as well as an additional amount of deaths caused by the raised unemployment rate.

The good news is that the “shelter-in-place” orders all over the globe appear to be “flattening the curve” at least to a certain extent.

The bad news is that we could see another huge explosion of cases and deaths once all of the restrictions are lifted.

And the really bad news is that what we have experienced so far is nothing compared to what is coming.

But in the short-term we should be very thankful that the numbers around the world are starting to level off a bit.

Of course that is only happening because most people are staying home, but having people stay home is absolutely killing the economy.

And if people stay home long enough, a lot of them will no longer be able to pay the mortgages on those homes.

Our leaders are being forced to make choices between saving lives and saving the economy, and those choices are only going to become more painful the longer this crisis persists.

Let us pray that they will have wisdom to make the correct choices, because the stakes are exceedingly high.

Trump Organization Seeks Concessions On Loans Backed Personally By President Trump From Deutsche Bank

No business is immune to the country’s coronavirus shutdown, including the President’s. In fact, it was was reported yesterday that the Trump Organization is actively seeking out concessions from Deutsche Bank, one of its lenders, due to the pandemic.

Representatives from the President’s company reached out to Deutsche Bank late in March and talks between the company and the bank are ongoing, according to Bloomberg.

Or, as one person simply put it on social media: “Two broke organizations restructuring debt”.

Deutsche Bank is said to be having similar talks with other commercial real estate companies in the U.S., as well. The pandemic, and ensuing economic shutdown, has squeezed both borrowers and lenders across the world. Central banks have worked on a plan to try and backstop banks and provide relief to companies, even considering lending to some businesses directly. However, it is going to be tough to paper over every single company that is facing a default.

The request from the Trump organization is noteworthy, since President Trump is arguably the most powerful person in the world and Deutsche Bank has been under scrutiny for years, with many speculating the bank could have solvency issues behind the scenes. The loans, which were taken out by Trump between 2012 and 2015, include a personal guarantee from Trump.

That means that in the case of a default, the lenders would have to collect from a sitting President.

The loans that the bank has provided for the Trump Organization include money for a Florida golf resort, a Washington D.C. hotel and a Chicago skyscraper.

Doral, Trump’s golf resort near Miami, has closed all operations. Trump’s hotel in Washington has shut down its restaurant and its bar. Additionally, a sale of the hotel’s lease has been halted while the commercial real estate market goes up in flames.

Deutsche Bank has been under scrutiny since Trump first took office back in 2016. The bank had previously considered the idea of extending Trump’s maturities to his loans to 2025, after the end of a second potential term, but ultimately decided against entering into any new business with a sitting President.

Here Comes The Next Crisis: Up To 30% Of All Mortgages Will Default In “Biggest Wave Of Delinquencies In History”

Unlike in the 2008 financial crisis when a glut of subprime debt, layered with trillions in CDOs and CDO squareds, sent home prices to stratospheric levels before everything crashed scarring an entire generation of home buyers, this time the housing sector is facing a far more conventional problem: the sudden and unpredictable inability of mortgage borrowers to make their scheduled monthly payments as the entire economy grinds to a halt due to the coronavirus pandemic.

And unfortunately this time the crisis will be far worse, because as Bloomberg reports mortgage lenders are preparing for the biggest wave of delinquencies in history. And unless the plan to buy time works – and as we reported earlier there is a distinct possibility the Treasury’s plan to provide much needed liquidity to America’s small businesses may be on the verge of collapse – an even worse crisis may be coming: mass foreclosures and mortgage market mayhem.

Borrowers who lost income from the coronavirus, which is already a skyrocketing number as the 10 million new jobless claims in the past two weeks attests, can ask to skip payments for as many as 180 days at a time on federally backed mortgages, and avoid penalties and a hit to their credit scores. But as Bloomberg notes, it’s not a payment holiday and eventually homeowners they’ll have to make it all up.

According to estimates by Moody’s Analytics chief economist Mark Zandi, as many as 30% of Americans with home loans – about 15 million households – could stop paying if the U.S. economy remains closed through the summer or beyond.

“This is an unprecedented event,” said Susan Wachter, professor of real estate and finance at the Wharton School of the University of Pennsylvania. She also points out another way the current crisis is different from the 2008 GFC: “The great financial crisis happened over a number of years. This is happening in a matter of months – a matter of weeks.”

Meanwhile lenders – like everyone else – are operating in the dark, with no way of predicting the scope or duration of the pandemic or the damage it will wreak on the economy. If the virus recedes soon and the economy roars back to life, then the plan will help borrowers get back on track quickly. But the greater the fallout, the harder and more expensive it will be to stave off repossessions.

“Nobody has any sense of how long this might last,” said Andrew Jakabovics, a former Department of Housing and Urban Development senior policy adviser who is now at Enterprise Community Partners, a nonprofit affordable housing group. “The forbearance program allows everybody to press pause on their current circumstances and take a deep breath. Then we can look at what the world might look like in six or 12 months from now and plan for that.”

But if the economic turmoil is long-lasting, the government will have to find a way to prevent foreclosures – which could mean forgiving some debt, said Tendayi Kapfidze, Chief Economist at LendingTree. And with the government now stuck in “bailout everyone mode”, the risk of allowing foreclosures to spiral is just too great because it would damage financial markets and that could reinfect the economy, he explained.

“I expect policy makers to do whatever they can to hold the line on a financial crisis,” Kapfidze said hinting at just a trace of a conflict of interest as his firm may well be next to fold if its borrowers declare a payment moratorium. “And that means preventing foreclosures by any means necessary.”

“I don’t know how I’m going to pay my mortgage and my condo dues and still be able to feed myself,” Habberstad said. “I just hope that, once things open up again, we who are impacted by Covid-19 are given consideration and sufficient time to bring all payments current without penalty and in a manner that does not bring us even more financial hardship.”

Borrowers must contact their lenders to get help and avoid black marks on their credit reports, according to provisions in the stimulus package passed by Congress last week. Bank of America said it has so far allowed 50,000 mortgage customers to defer payments. That includes loans that are not federally backed, so they aren’t covered by the government’s program.

Meanwhile, Treasury Secretary Steven Mnuchin has convened a task force to deal with the potential liquidity shortfall faced by mortgage servicers, which collect payments and are required to compensate bondholders even if homeowners miss them. The group was supposed to make recommendations by March 30.

“If a large percentage of the servicing book – let’s say 20-30% of clients you take care of – don’t have the ability to make a payment for six months, most servicers will not have the capital needed to cover those payments,” QuickenChief Executive Officer Jay Farner said in an interview. But not Quicken, of course.

Quicken, which serves 1.8 million borrowers, and in 2018 surpassed Wells Fargo as the #1 mortgage lender in the US, has a strong enough balance sheet to serve its borrowers while paying holders of bonds backed by its mortgages, Farner said, although something tells us that in 6-8 weeks his view will change dramatically. Until then, the company plans to almost triple its call center workers by May to field the expected onslaught of borrowers seeking support, he said.

Ironically, as Bloomberg concludes, “if the pandemic has taught us anything, it’s how quickly everything can change. Just weeks ago, mortgage lenders were predicting the biggest spring in years for home sales and mortgage refinances.”

Habberstad, the bar manager, was staffing up for big crowds at the beer garden, which is across from National Park, home of the World Series champions. Then came coronavirus. Now, she’s dependent on her unemployment check of $440 a week.

“Everybody wants to work but we’re being asked not to for the sake of the greater good,” she said.

Landlords Squeezed Between Missed Rent and Overdue Mortgages

(Bloomberg) — Chuck Sheldon, a landlord and property manager in Albuquerque, New Mexico, has owned apartments for more than half a century. These days, he can barely keep up with all the moving pieces.

He’s talking with owners of roughly 1,700 units he manages, who are worried what’s going to happen if rent checks stop coming in. He’s talking with tenants, about half of whom he assumes will be delinquent this month because they lost jobs or choose not to pay. And he’s in discussions with banks, trying to figure out how he’ll make mortgage payments on the properties he owns during a rapidly worsening global health crisis.

“That’s the $100,000 question,” said Sheldon, the president of T&C Management. “I’ve never seen something like this.”

It’s rent day in America, with roughly $22 billion in monthly payments on apartments due, according to CoStar. But just how much of it gets paid in the coming days is anybody’s guess.

Some large property owners have already rolled out payment plans and halted evictions as the coronavirus outbreak roils the economy. But many apartments in the U.S. are essentially small businesses that tend to have less financial flexibility and will need help in the coming months.

Few Choices

There are few good choices for the millions of Americans who lost their jobs and have no clear prospects for when they’ll get them back. Eviction moratoriums, unemployment benefits and cash payments from the federal government could help many keep a roof over their heads.

But nearly half of the nation’s 44 million renter households were already stretched financially. Over the next six months, they could need as much as $96 billion in relief, according to a recent analysis by the Urban Institute.