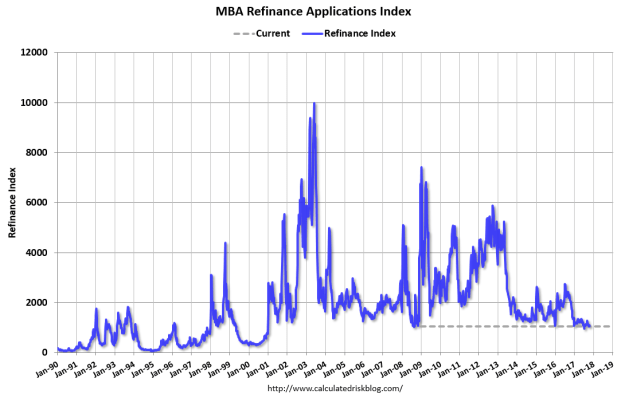

The Mortgage Bankers Association released their weekly survey of members (I don’t know if Quicken Loans is a member or not) and it revealed that mortgage REFINANCING applications remain in Death Valley since mortgage rates started increasing back in mid-2016.

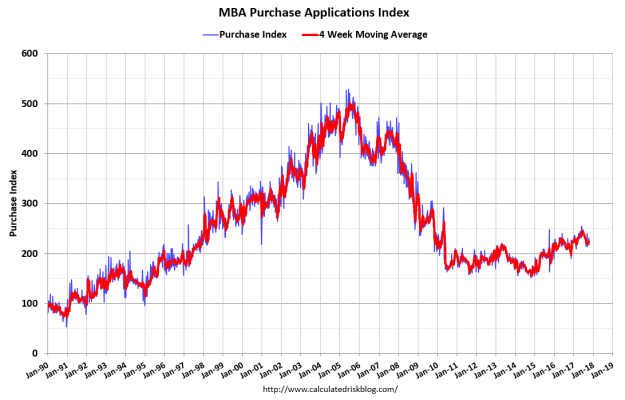

Both purchase and refinancing applications were down from the previous week.

Of course, subprime borrower originations have declined since the finacial crisis and the housing bubble burst. But home prices continue to soar despite the malaise in mortgage purchase applications.

Of course, higher capital requirements for commercial banks and the Consumer Financial Protection Bureau helped chill the mortgage market. But with the Federal Reserve encouraging banks NOT to lend by paying interest on bank excess reserves, are we surprised at the malaise in mortgage purchase applications or originations?

Hence, it is not surprising to see a slowdown in the growth of bank credit YoY.

Yes, it is Death Valley Days … at least for mortgage refinancing.

***

Rescuing the Banks Instead of the Economy

“You can’t bail out the banks, leave the debts in place, and rescue the economy. It’s a zero-sum game. Somebody has to lose. That’s what happened in 2009 when President Obama came in. He invited the bankers to the White House and he said, “I’m the only guy standing between you and the mob with pitchforks,” by which he meant the voters that he was bamboozling. He reassured the bankers. He said, “Look, my loyalty is to my campaign donors not to the voters. Don’t worry; my loyalty is with you.”