Mortgage Lending Just Broke, Fannie & Freddie Freaking Out!

Something is seriously wrong in the mortgage lending business with all the major players now on the defensive as once again it appears that widespread fraud is causing a major disruption to the flow of credit in real estate. Chaos has erupted in the mortgage business this week that the mainstream press is ignoring.

If you find yourself in an awkward situation and somebody else is there to witness it, you hope they aren’t too quick to judge. Ameriquest Mortgage Company thankfully went out of business but they left us with a series of funny ads to enjoy. If you find yourself in an awkward situation always try to find the humor.

A clear bifurcation of risk emerged between mortgaged homes purchased relatively recently versus those bought early in or prior to the pandemic: Black Knight

(Connie Kim) Home price corrections exposed a growing pocket of equity risk concentrated among purchase mortgages originated in 2022, Black Knight said in its latest mortgage monitor report. Of all homes purchased with a mortgage in 2022, 8% are now at least marginally underwater.

Of the 450,000 underwater borrowers at the end of the third quarter, nearly 60% of the mortgages originated in the first nine months of 2022, according to Black Knight. In total, 5% of all mortgages originated so far this year are now marginally underwater, with another 20% in low equity positions.

The U.S. along with most other countries are moving towards implementation of central bank digital currencies. With this comes concerns related to privacy, political overreach, and discrimination.

This means your new next door neighbor and their extended family from, pick any third world country, might have gotten in with a zero down, zero interest, 100 year mortgage from the Fed to provide much needed diversification to your neighborhood and community.

(Arnie Aurellano) Rep. Ilhan Omar, D-Minnesota, has introduced the Rent and Mortgage Cancellation Act, a bill that would cancel rents and mortgage payments nationwide through the duration of the COVID-19 pandemic.

MICHAEL BROCHSTEIN/ECHOES WIRE/BARCROFT MEDIA/GETTY IMAGES

The legislation would constitute full payment forgiveness, with no accumulation of debt for renters or homeowners and no negative impact on their credit rating or rental history. Just as significantly, it would also establish relief funds for mortgage holders and landlords to cover the losses incurred from such payment cancellations.

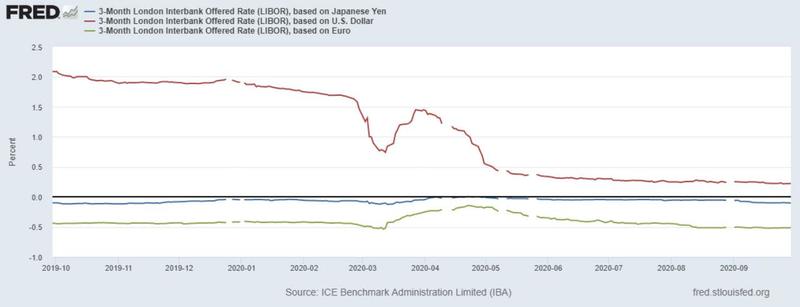

(Christopher Whalen) Watching the talking heads pondering the next move in US interest rates, we are often amazed at the domestic perspective that dominates these discussions. Just as the Federal Open Market Committee never speaks about foreign anything when discussing interest rate policy, so too most observers largely ignore the offshore markets. Yen, dollar and euro LIBOR spreads are shown below.

Zoltan Pozsar, the influential money-market strategist at Credit Suisse (NYSE:CS), warns that the short-end of the US money markets are likely to be awash in cash over the end-of-year liquidity hump. Unlike the unpleasantness in 2018, for example, we may see instead a surfeit of lending as banks scramble for yield in a wasteland bereft of duration. Would that it were so.

The Pozsar view does not exactly fit well with the rising rate, end of the world scenario popular in some corners of the financial media ghetto. The 10-year note is certainly rising and with it the 30-year mortgage rate. Indeed, Pozsar reminds CS clients that yen/$ swaps are now yielding well-above Treasury yields for seven years. Hmm.

We believe short-term rates will remain low in the US, even as offshore demand for dollars soars. If the 10-year Treasury backs up much further, then we’d look for the FOMC to act on some calls by governors to buy longer duration securities. That is, a very direct and large scale increase in QE and particularly on the long end of the curve.

We expect that Chairman Powell knows that underneath the comfortable blanket of low interest rates lie some truly appalling credit problems ahead for the global economy, the US banking sector and also for private debt and equity investors. We expect the low interest rate environment to drive volumes in corporate debt and residential mortgages, even as other sectors like ABS languish and commercial real estate gets well and truly crushed.

“The pandemic is putting unprecedented stress on CMBS markets that even the Fed is having difficulty offsetting,” writes Ralph Delguidice at Pavilion Global Markets.

“Limited reserves are being exhausted even as rent collection and occupancy levels remain serious issues… Bondholders expecting cash are getting keys instead, and in our view, ratings downgrades and significant losses are now only a formality.”

We noted several months ago that the resolution of the credit collapse in commercial mortgage backed securities or CMBS will be very different from when a bank owns the mortgage. As we discussed with one banker this week over breakfast in Midtown Manhattan, holding the mortgage and even some equity in a prime property allows for time to recover value.

With CMBS, the “AAA” tranche is first in line, thus the seniors have no incentive to make nice with the subordinate investors. The deals will liquidate, the property will be sold and the junior bond investors will take 100% losses. But as Delguidice and others note with increasing frequency, this time around the “AAA” investors are getting hit too. More to come.

Manhattan

Meanwhile, over in the relative calm of the agency collateral markets, large, yield hungry money center banks led by Wells Fargo & Co are deploying liquidity to buy billions of dollars in delinquent government loans out of MBS pools.

The bank buys the asset and gives the investor par, with a smidgen of interest. Market now has more cash, but less cash than it had before buying the mortgage bond in the first place. Why? Because it likely took a loss on the transaction. Buy at 109. Prepayment at par six months later. You get the idea.

In fact, if you look at the Treasury yield curve, rates are basically lying flat along the bottom of the chart out to 48 months. Why? Because this nice fellow named Fed Chairman Jerome Powell, along with many other buyers, are gobbling up the available supply of risk free assets inside of five years.

Spreads on everything from junk bonds to agency mortgage passthroughs are contracting, suggesting that the private bid for paper remains strong. When you look at the fact that implied valuations for new production MBS and mortgage servicing rights (MSR) have been rising since July, this even though prepayment rates are astronomical, certainly implies that there is a great deal of cash sitting on the sidelines.

Remember that the price of an MSR is not just about cash flows and prepayments, but it’s also about default rates and the relationship with the consumer. We described in our last missive for The IRA Premium Service (“The Bear Case for Mortgage Lenders”), that a rising rate environment could generate catastrophic losses for residential lenders, particularly in the government loan market. We write:

“For both investors and risk professionals operating in the secondary mortgage market, the next several years contain both great opportunities and considerable risks.We look for the top lenders and servicers to survive the coming winter of default resolution that must inevitably follow a period of low interest rates by the FOMC.The result of the inevitable consolidation will be fewer, larger IMBs.”

Don’t get distracted by the rising rate song from the Street. We don’t look for short or medium term interest rates to rise in the near term or frankly for years. Agency 1.5% coupons “did not find a place in the latest Fed’s purchase schedule. It is possible (they) are included in the next update,” writes Nomura this week. This seems a pretty direct prediction of lower yields. But as one veteran mortgage operator cautions The IRA: “Not just yet.”

We don’t think that the Fed is going to take its foot off the short end of the curve anytime soon, in part because the system simply cannot withstand a sustained period of rising rates. In fact, we note that our friends at SitusAMC are adding 1.5% MBS coupons to forward rate models this month. But that does not necessarily mean that mortgage rates will fall any time soon.

We hear that the Fed of New York has bought a few 1.5s in recent days, but supply is sorely lacking. You see, the mortgage industry is not quite ready to print many new 1.5% MBS coupons and will not do so anytime soon. As the chart above suggests, mortgage rates are in fact rising. Why? Is not the FOMC in charge of the U.S mortgage market?

No, the market rules. Today you can make more money selling a new 1-4 family residential mortgage into a 2.5% coupon from Fannie, Freddie or Ginnie Mae at 105. You book a five point gain on sale and are therefore a hero. And a year from now, after the liquidity does in fact migrate down to 1.5s c/o the beneficence of the FOMC, you can again be a hero.

Specifically, you call up that same borrower and refinance the mortgage into a brand new 1.5% Fannie, Freddie or Ginnie Mae at 105. You take another five point gain on sale. Right? And who paid for this blessed optionality? The Bank of Japan, Peoples Bank of China, and PIMCO, among many other fortunate global investors.

These multinational holders of US mortgage bonds may not like negative returns on risk free American assets, but that’s life in the big city. And thankfully for Chairman Powell, it’s not his problem. Many years ago, a friend in the mortgage market said of loan repurchase demands from Fannie Mae: “What do you want from me?”

(Bloomberg) — Tension is rising in the messy fight over commercial rent payments.

With stores shuttered, struggling retailers are skipping rent and asking for concessions, while landlords are demanding payment and having their own tricky conversations with lenders.

There are no easy answers as officials ponder how to safely get the economy back open. So far this month, some mall owners and other retail landlords collected as little as 15% of what they were owed, according to one estimate. And it’s expected to get worse, with more than $20 billion in rent payments coming due in May.

“It’s all over the map what’s happening out there,” said Tom Mullaney, a managing director in restructuring at Jones Lang LaSalle Inc. “More and more defaults are coming in every single day.”

Companies across the U.S. — from small mom-and-pop operations to giant corporations — have missed April payments or sent out relief requests citing store closures because of the pandemic.

Pushing Back

Landlords have been pitching rent deferment, saying tenants can make reduced payments now as long as they pay the balance at some point. Some businesses are pushing back on that option and asking for rent cuts even after stores are open again.

U.S. retail landlords typically collect more than $20 billion in rent each month, according to data from CoStar Group Inc.So far, April rent collection has ranged from 15% to 30% for landlords with higher concentrations of shuttered businesses, according to an estimate from brokerage firm Marcus & Millichap.

Landlords, who are facing their own debt defaults, are getting frustrated. Some are complaining that large corporations are using the crisis to skip out on rent. Others say they’re not responsible for bailing out tenants and that the federal government or insurance companies should cover the costs instead.

“The landlords are triaging the battlefield,” said Gene Spiegelman, vice chairman at Ripco Real Estate Corp. “The super powerful and strong are not going to get any help and the ones that’ll die anyways, landlords will say why would I help them?”

Some Pay

To be sure, some landlords and tenants are working out deals on a case-by-case basis. And some companies are paying rent for their stores. That includes AT&T Inc. and T-Mobile USA Inc.according to people familiar with the matter. J.C. Penney also said it paid for April.

Ross Stores Inc. and fitness chain Solidcore, meanwhile, are among those standing firm on requests for rent abatements and asking for additional concessions. Williams-Sonoma Inc. is another chain that has stopped paying rent, according to people familiar.

Ross has told landlords that after the shutdown ends their rent on some stores should be cut until sales rebound. Solidcore hasn’t agreed to rent deferral and said it likely won’t be able to pay the same rent as it was before pandemic.

“We’re not going to be bullied by the landlords during this time,” said Anne Mahlum, the fitness company’s founder and chief executive officer said. “We have some leverage here. What are they going to do, say get out and then have vacancy for months on end?”

Backfire

Tenants’ refusal to pay will likely backfire, according to Jackson Hsieh, CEO of retail landlord Spirit Realty Capital Inc.

The firm, which owns more than 1,700 properties, has seen requests for rent relief since the crisis started. But several of those tenants ended up paying, according to Hsieh.

One agreed to pay after getting loans from the government’s relief package, while another did so after being asked to provide financial information. A discount retailer and a company in the auto industry paid after Spirit refused to consider their rent deferral requests.

“If a tenant just says I’m not going to pay, fine, I’ll default you, I’m going to go to the courts, and you have 30 days to pay or quit,” Hsieh said. “I don’t want to be negative, but we own the building.”

Pending Loans

Many landlords are rushing to work out deals with lenders to stave off their own defaults. Banks and insurance companies are negotiating deals on a case-by-case basis, but borrowers in commercial mortgage-backed securities have fewer options.

About 11% of U.S. CMBS retail property loan borrowers have been late on April payments so far, according to preliminary analysis by data firm Trepp. If that number holds up, $13 billion worth of CMBS loans could miss payments for the month.

“The banks are a little more fluid and often there’s recourse,” said Camille Renshaw, CEO brokerage firm B+E. “But many large properties have CMBS debt and when there’s a crisis, no one is there to pick up the phone to negotiate.”

It’s just not retail stores that are suffering. Office space is a ghost town thanks to the Wuhan (bat) virus outbreak. But with tools like Zoom, Webex, Microsoft Teams, GotoMeeting, Skype, etc., one wonders if the days of massive office building demand is over. Other than for socializing and monitoring employees (as Bill Lumbergh did in “Office Space.”)

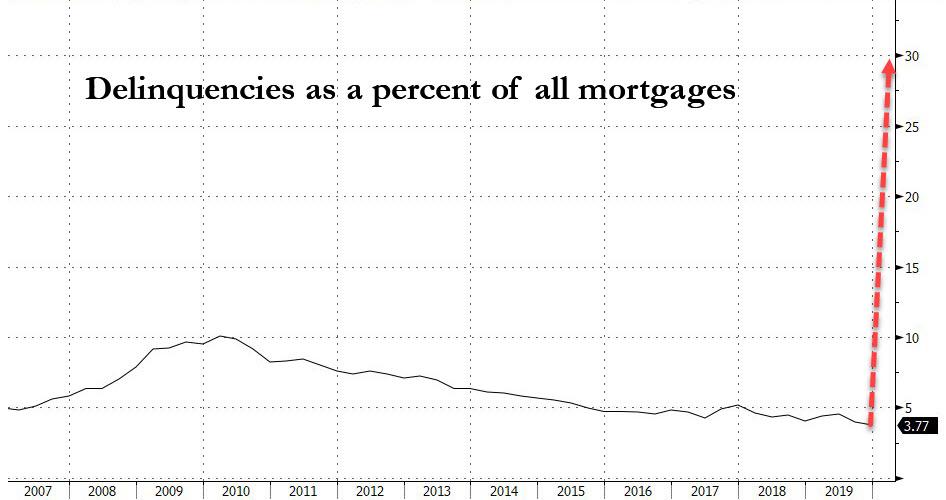

The cascading failures that have been set into motion by this “coronavirus shutdown” are going to make the financial crisis of 2008 look like a Sunday picnic. As you will see below, it is being estimated that unemployment in the U.S. is already higher than it was at any point during the last recession. That means that millions of American workers no longer have paychecks coming in and won’t be able to pay their mortgages. On top of that, the CARES Act actually requires all financial institutions to allow borrowers with government-backed mortgages to defer payments for an extended period of time. Of course this is a recipe for disaster for mortgage lenders, and industry insiders are warning that we are literally on the verge of a “collapse” of the mortgage market.

Never before in our history have we seen a jump in unemployment like we just witnessed. If you doubt this, just check out this incredible chart.

Millions upon millions of American workers are now facing a future with virtually no job prospects for the foreseeable future, and former Fed Chair Janet Yellen believes that the unemployment rate in the U.S. is already up to about 13 percent…

Former Federal Reserve Chair Janet Yellen told CNBC on Monday the economy is in the throes of an “absolutely shocking” downturn that is not reflected yet in the current data.

If it were, she said, the unemployment rate probably would be as high as 13% while the overall economic contraction would be about 30%.

If Yellen’s estimate is accurate, that means that unemployment in this country is already significantly worse than it was at any point during the last recession.

And young adults are being hit particularly hard during this downturn…

As measures to slow the pandemic decimate jobs and threaten to plunge the economy into a deep recession, young adults such as Romero are disproportionately affected. An Axios-Harris survey conducted through March 30 showed that 31 percent of respondents ages 18 to 34 had either been laid off or put on temporary leave because of the outbreak, compared with 22 percent of those 35 to 49 and 15 percent of those 50 to 64.

As I have documented repeatedly over the past several years, most Americans were living paycheck to paycheck even during “the good times”, and so now that disaster has struck there will be millions upon millions of people that will not be able to pay their mortgages.

A broad coalition of mortgage and finance industry leaders on Saturday sent a plea to federal regulators, asking for desperately needed cash to keep the mortgage system running, as requests from borrowers for the federal mortgage forbearance program are pouring in at an alarming rate.

The Cares Act mandates that all borrowers with government-backed mortgages—about 62% of all first lien mortgages according to Urban Institute—be allowed to delay at least 90 days of monthly payments and possibly up to a year’s worth.

Needless to say, many in the mortgage industry are absolutely furious with the federal government for putting them into such a precarious position, and one industry insider is warning that we could soon see the “collapse” of the mortgage market…

“Throwing this out there without showing evidence of hardship was an outrageous move, outrageous,” said David Stevens, who headed the Federal Housing Administration during the subprime mortgage crisis and is a former CEO of the Mortgage Bankers Association.

“The administration made a huge mistake bringing moral hazard in and thrust extraordinary risk into the private sector that could collapse the mortgage market.”

Of course a lot of other industries are heading for immense pain as well.

At this point, even JPMorgan Chase CEO Jamie Dimon is admitting that the U.S. economy as a whole is plunging into a “bad recession”…

Jamie Dimon said the U.S. economy is headed for a “bad recession” in the wake of the coronavirus pandemic, but this time around his company is not going to need a bailout. Instead, JPMorgan Chase is ready to lend a hand to struggling consumers and small businesses.

“At a minimum, we assume that it will include a bad recession combined with some kind of financial stress similar to the global financial crisis of 2008,” Dimon, the CEO of JPMorgan Chase, said Monday in his annual letter to shareholders.

And the longer this coronavirus shutdown persists, the worse things will get for our economy.

Sunday on New York AM 970 radio’s “The Cats Round Table,” economist Stephen Moore weighed in on the potential impact of the coronavirus to the United States economy.

Moore warned the nation could be “facing a potential Great Depression scenario” if the United States stays on lock down much past the beginning of May, as well as an additional amount of deaths caused by the raised unemployment rate.

The good news is that the “shelter-in-place” orders all over the globe appear to be “flattening the curve” at least to a certain extent.

The bad news is that we could see another huge explosion of cases and deaths once all of the restrictions are lifted.

Of course that is only happening because most people are staying home, but having people stay home is absolutely killing the economy.

And if people stay home long enough, a lot of them will no longer be able to pay the mortgages on those homes.

Our leaders are being forced to make choices between saving lives and saving the economy, and those choices are only going to become more painful the longer this crisis persists.

Let us pray that they will have wisdom to make the correct choices, because the stakes are exceedingly high.

Unlike in the 2008 financial crisis when a glut of subprime debt, layered with trillions in CDOs and CDO squareds, sent home prices to stratospheric levels before everything crashed scarring an entire generation of home buyers, this time the housing sector is facing a far more conventional problem: the sudden and unpredictable inability of mortgage borrowers to make their scheduled monthly payments as the entire economy grinds to a halt due to the coronavirus pandemic.

And unfortunately this time the crisis will be far worse, because as Bloomberg reports mortgage lenders are preparing for the biggest wave of delinquencies in history. And unless the plan to buy time works – and as we reported earlier there is a distinct possibility the Treasury’s plan to provide much needed liquidity to America’s small businesses may be on the verge of collapse – an even worse crisis may be coming: mass foreclosures and mortgage market mayhem.

Borrowers who lost income from the coronavirus, which is already a skyrocketing number as the 10 million new jobless claims in the past two weeks attests, can ask to skip payments for as many as 180 days at a time on federally backed mortgages, and avoid penalties and a hit to their credit scores. But as Bloomberg notes, it’s not a payment holiday and eventually homeowners they’ll have to make it all up.

According to estimates by Moody’s Analytics chief economist Mark Zandi, as many as 30% of Americans with home loans – about 15 million households – could stop paying if the U.S. economy remains closed through the summer or beyond.

“This is an unprecedented event,” said Susan Wachter, professor of real estate and finance at the Wharton School of the University of Pennsylvania. She also points out another way the current crisis is different from the 2008 GFC: “The great financial crisis happened over a number of years. This is happening in a matter of months – a matter of weeks.”

Meanwhile lenders – like everyone else – are operating in the dark, with no way of predicting the scope or duration of the pandemic or the damage it will wreak on the economy. If the virus recedes soon and the economy roars back to life, then the plan will help borrowers get back on track quickly. But the greater the fallout, the harder and more expensive it will be to stave off repossessions.

“Nobody has any sense of how long this might last,” said Andrew Jakabovics, a former Department of Housing and Urban Development senior policy adviser who is now at Enterprise Community Partners, a nonprofit affordable housing group. “The forbearance program allows everybody to press pause on their current circumstances and take a deep breath. Then we can look at what the world might look like in six or 12 months from now and plan for that.”

But if the economic turmoil is long-lasting, the government will have to find a way to prevent foreclosures – which could mean forgiving some debt, said Tendayi Kapfidze, Chief Economist at LendingTree. And with the government now stuck in “bailout everyone mode”, the risk of allowing foreclosures to spiral is just too great because it would damage financial markets and that could reinfect the economy, he explained.

“I expect policy makers to do whatever they can to hold the line on a financial crisis,” Kapfidze said hinting at just a trace of a conflict of interest as his firm may well be next to fold if its borrowers declare a payment moratorium. “And that means preventing foreclosures by any means necessary.”

“I don’t know how I’m going to pay my mortgage and my condo dues and still be able to feed myself,” Habberstad said. “I just hope that, once things open up again, we who are impacted by Covid-19 are given consideration and sufficient time to bring all payments current without penalty and in a manner that does not bring us even more financial hardship.”

Borrowers must contact their lenders to get help and avoid black marks on their credit reports, according to provisions in the stimulus package passed by Congress last week. Bank of America said it has so far allowed 50,000 mortgage customers to defer payments. That includes loans that are not federally backed, so they aren’t covered by the government’s program.

Meanwhile, Treasury Secretary Steven Mnuchin has convened a task force to deal with the potential liquidity shortfall faced by mortgage servicers, which collect payments and are required to compensate bondholders even if homeowners miss them. The group was supposed to make recommendations by March 30.

“If a large percentage of the servicing book – let’s say 20-30% of clients you take care of – don’t have the ability to make a payment for six months, most servicers will not have the capital needed to cover those payments,” QuickenChief Executive Officer Jay Farner said in an interview. But not Quicken, of course.

Quicken, which serves 1.8 million borrowers, and in 2018 surpassed Wells Fargo as the #1 mortgage lender in the US, has a strong enough balance sheet to serve its borrowers while paying holders of bonds backed by its mortgages, Farner said, although something tells us that in 6-8 weeks his view will change dramatically. Until then, the company plans to almost triple its call center workers by May to field the expected onslaught of borrowers seeking support, he said.

Ironically, as Bloomberg concludes, “if the pandemic has taught us anything, it’s how quickly everything can change. Just weeks ago, mortgage lenders were predicting the biggest spring in years for home sales and mortgage refinances.”

Habberstad, the bar manager, was staffing up for big crowds at the beer garden, which is across from National Park, home of the World Series champions. Then came coronavirus. Now, she’s dependent on her unemployment check of $440 a week.

“Everybody wants to work but we’re being asked not to for the sake of the greater good,” she said.

Update (1500ET): A top U.S. regulator is exploring whether to throw a lifeline to mortgage servicers stressed by the coronavirus pandemic by tapping a program meant to address natural disasters.

Bloomberg reports that, in order to prepare for an expected wave of missed payments as borrowers deal with the economic fallout from the virus, officials at Ginnie Mae are considering using relief programs most often activated in the wake of hurricanes, floods and other calamities, according to people familiar with the matter.

Mortgage-industry lobbyists unsuccessfully tried to get Congress to include some sort of liquidity facility for servicers in the stimulus bill. Still, many servicers expect the Treasury Department and the Federal Reserve to create a lifeline for servicers out of other money in the $2 trillion package.

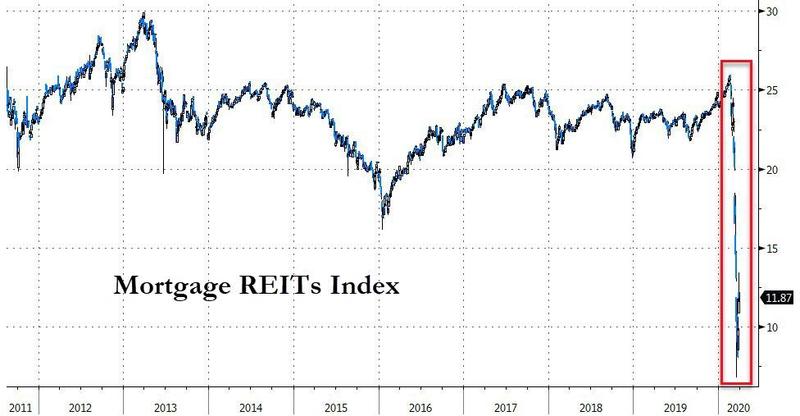

Earlier this week,ZeroHedge highlighted the fact that numerous mortgage-related companies were facing considerable – and in some cases existential – crises in their day-to-day operations amid margin calls, illiquidity, and a drying up of demand for non-agency products thanks to The Fed’s intervention.

First, its was AG Mortgage Investment Trust which last Friday said it failed to meet some margin calls and doesn’t expect to be able to meet future margin calls with its current financing. Then it was TPG RE Finance Trust which also hit a liquidity wall and could not repay its lenders. Then, on Monday it was first Invesco, then ED&F Man Capital, and then the mortgage mayhem took down MFA Financial, which stated “due to the turmoil in the financial markets resulting from the global pandemic of the COVID-19 virus, the Company and its subsidiaries have received an unusually high number of margin calls from financing counterparties, and have also experienced higher funding costs in respect of its repurchase agreements.”

And now that mortgage-mayhem has impacted one of the largest U.S. mortgage firms catering to riskier borrowers.

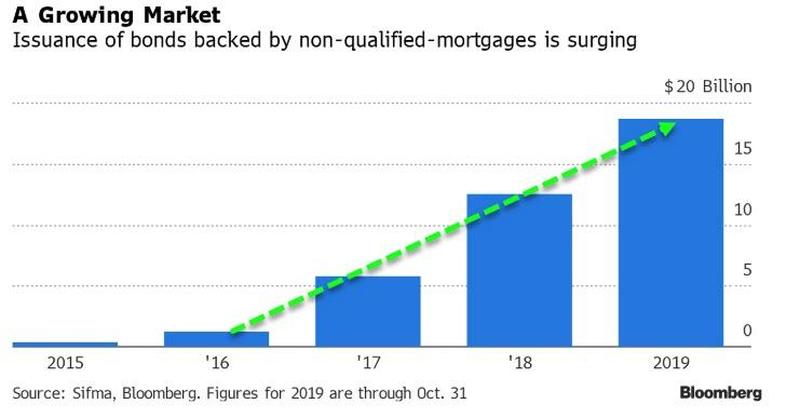

Earlier in the week, we mentioned Angel Oak Mortgage Solutions – which specializes in so-called non-qualified mortgages that can’t be sold to Fannie Mae or Freddie Mac – pointing out that the company would pause all originations of loans for two weeks “due to the constant shifts and the inability to appropriately evaluate credit risk.”

And now Sreeni Prabhu, co-chief executive officer of the firm’s parent, Angel Oak Cos., is slashing 70% of the comany’s workforce (almost 200 of its 275 employees).

“The world has dramatically changed,” Prabhu said.

“We have to slow down and re-underwrite in the new world that we’re in. That’s going to take some time.”

Bloomberg reports that Angel Oak is primarily known for its riskier lending arm, which is one of the leaders in funding non-qualified mortgages. Such loans include those made to borrowers who verify their incomes with bank statements instead of tax returns and others who may have recently filed for bankruptcy or had a previous foreclosure that hurt their credit scores.

Angel Oak Mortgage Solutions funded some $3.3 billion of non-QM loans in 2019, making it one of the biggest lenders in the space. In January, Angel Oak’s mortgage units said they planned to fund more than $8 billion of home loans in 2020, but the total is now likely to be perhaps a quarter of that, Prabhu said.

The coronavirus pandemic has brought non-QM lending to a virtual standstill industrywide. Many non-QM borrowers are self-employed, making them among the hardest hit by a broad slowdown in business activity.

Add this halting of originations to the margin calls of the fund side, and it all sounds ominously similar to July 2007, when two Bear Stearns hedge funds (Bear Stearns High-Grade Structured Credit Fund and the Bear Stearns High-Grade Structured Credit Enhanced Leveraged Fund) – exposed to mortgage-backed securities and various other leveraged derivatives on same – crashed and burned and started the dominoes falling…

(ZeroHedge) We warned last week that, despite The Fed’s unlimited largesse, there is trouble brewing in the mortgage markets that has an ugly similarity to what sparked the last crisis in 2007. For a sense of the decoupling, here is the spread between Agency MBS (FNMA) and 10Y TSY yields…

At that time, WSJ’s Greg Zuckerman reported that the AG Mortgage Investment Trust, a real-estate investment trust operated by New York hedge fund Angelo, Gordon & Co., is among those feeling pressure, the company said, and, in the latest sign of turmoil in crucial areas of the credit markets, is examining a possible asset sale.

“In recent weeks, due to the turmoil in the financial markets resulting from the global pandemic of the Covid-19 virus, the company and its subsidiaries have received an unusually high number of margin calls from financing counterparties,” AG Mortgage said Monday morning.

Well, they are not alone.

As Bloomberg reports, the $16 trillion U.S. mortgage market – epicenter of the last global financial crisis – is suddenly experiencing its worst turmoil in more than a decade, setting off alarms across the financial industry and prompting the Fed to intervene. But, as we previously noted, it is too late and too limited (the central bank is focusing on securities consisting of so-called agency home loans and commercial mortgages that were created with help from the federal government).

And the aftershocks of a chaotic rush to offload mortgage bonds are spilling over to regional broker-dealers facing mounting margin calls.

Flagstar Bancorp,one of the nation’s biggest lenders to mortgage providers, said Friday it stopped funding most new home loans without government backing. Other so-called warehouse lenders are tightening terms of financing to mortgage providers, either raising costs or refusing to support certain types of home loans.

One prominent mortgage funder, Angel Oak Mortgage Solutions, said Monday it’s even pausing all loan activity for two weeks. It blamed an “inability to appropriately evaluate credit risk.”

Things escalated over the weekend, according to Bloomberg, when some firms rushed to raise cash by requesting offers for their bonds backed by home loans.

“I ran dealer desks for over 20 years,” said Eric Rosen, who oversaw credit trading at JPMorgan Chase & Co., ticking off the collapse of Long-Term Capital Management, the bursting of the dot-com bubble some 20 years ago, and the 2008 global financial crisis. “And I never recall a BWIC on a weekend.”

And now, commodity-broker ED&F Man Capital Markets has been hit with growing demands to post more capital to cover souring hedges in its mortgage division, according to people with knowledge of the matter.

The requests are coming from central clearinghouses and exchanges, forcing the firm to put up almost $100 million on Friday alone, the people said, asking not to be identified because the information isn’t public.

ED&F, whose hedges exceed $5 billion in net notional value, has been in discussions with the clearinghouses and has met all the margin calls, one of the people said.

As a reminder, ED&F Man Capital is the financial-services division of ED&F Man Group, the 240-year-old agricultural commodities-trading house.

It has about $14 billion in assets and more than $940 million in shareholder equity, according to the firm’s website.

Concern about losses in mortgage bonds could feed turmoil in the overall mortgage market that ultimately drives up borrowing costs for consumers looking to buy homes and refinance. Mortgage rates have risen in recent weeks, despite a fall in benchmark rates.

“The Fed is going to do whatever it takes to restore normal functioning in the market,” said Karen Dynan, a Harvard University economics professor who formerly worked as a Fed economist and senior official at the Treasury Department.

“But we need to remember that the root of the problem is that financial institutions and investors are desperately seeking cash, so in that sense the Fed’s announcement is not everything that needs to be done.”

All of which sounds ominously similar to July 2007, when two Bear Stearns hedge funds (Bear Stearns High-Grade Structured Credit Fund and the Bear Stearns High-Grade Structured Credit Enhanced Leveraged Fund) – exposed to mortgage-backed securities and various other leveraged derivatives on same – crashed and burned and started the dominoes falling…

(John Rubino) There are trillions of dollars of bonds in the world with negative yields – a fact with which future historians will find baffling.

Copenhagen Mint Images/Getty Images

Until now those negative yields have been limited to the safest types of bonds issued by governments and major corporations. But this week a new category of negative-yielding paper joined the party: mortgage-backed bonds.

(Investing.com) – At the biggest mortgage bank in the world’s largest covered-bond market, a banker took a few steps away from his desk this week to make sure his eyes weren’t deceiving him.

As mortgage-bond refinancing auctions came to a close in Denmark, it was clear that homeowners in the country were about to get negative interest rates on their loans for all maturities through to five years, representing multiple all-time lows for borrowing costs.

“During this week’s auctions, there were three times when I had to stand back a little from the screen and raise my eyebrows somewhat,” said Jeppe Borre, who analyzes the mortgage-bond market from a unit of the Nykredit group that dominates Denmark’s $450 billion home-loan industry.

For one-year adjustable-rate mortgage bonds, Nykredit’s refinancing auctions resulted in a negative rate of 0.23%. The three-year rate was minus 0.28%, while the five-year rate was minus 0.04%.

The record-low mortgage rates, which don’t take into account the fees that homeowners pay their banks, are the latest reflection of the global shift in the monetary environment as central banks delay plans to remove stimulus amid concerns about economic growth.

Denmark has had negative rates longer than any other country. The central bank in Copenhagen first pushed its main rate below zero in the middle of 2012, in an effort to defend the krone’s peg to the euro. The ultra-low rate environment has dragged down the entire Danish yield curve, with households in the country paying as little as 1% to borrow for 30 years. That’s considerably less than the U.S. government.

The spread of negative yields to mortgage-backed bonds is both inevitable and ominous. Inevitable because the current amount of negative-yielding debt has not ignited the kind of rip-roaring boom that overindebted countries think they need, which, since interest rates are just about their only remaining stimulus tool, requires them to find other kinds of debt to push into negative territory. Ominous because, as the world discovered in the 2000s, mortgages are a cyclical instrument, doing well in good times and defaulting spectacularly in bad. Giving bonds based on this kind of paper a negative yield appears to guarantee massive losses in the next housing bust.

Meanwhile, this is year ten of an expansion – which means the next recession is coming fairly soon. During recessions, the US Fed, for instance, tends to cut short-term rates by about 5 percentage points to counter the slowdown in growth.

… this imminent slide in interest rates will turn the rest of the global financial system Danish, giving us bank accounts and bond funds that charge rather than pay, and very possibly mortgages that pay rather than charge.

Anyone who claims to know how this turns out is delusional.

“A Crack in The Foundation?” Part 2: Three Decades of Red Flags — Mortgage Policy & Praxis, 1970-1999

Welcome to “A Crack in the Foundation?”, a four-part series in which Maxwell Digital Mortgage Solutions will examine the evolution of the mortgage industry and homeownership in America, with an eye on government policies and how GSEs can promote (or prohibit) periods of economic growth.

Part 2 begins at the start of the 1970s and follows the uneasy path of government policy and economic turmoil as we creep towards the end of the century. (Missed Part 1?Read it here). This section will follow the astronomical growth in the secondary market, the mounting government pressure put on Fannie and Freddie to increase their offerings to lower- and moderate-income borrowers, as well as a widespread shift towards deregulation in the market that (spoiler alert) will prove to have disastrous consequences as the new millennium begins.

“A Crack in The Foundation?” Part 1: Fannie & Friends — The Evolution of Mortgage Policy from 1930-1960

Welcome to “A Crack in the Foundation?”, a four-part series in which Maxwell Digital Mortgage Solutions will examine the evolution of the mortgage industry and homeownership in America, with an eye on government policies and how GSEs can promote (or prohibit) periods of economic growth.

Part I starts at the turn of the 20th century and traces the establishment of the Federal Housing Administration (FHA), as well as the birth of Fannie and Ginnie, to look at the inception of the modern mortgage and its impact on home ownership.

Ah, the problems of trying to model residential mortgage purchase and refinancing applications. When mortgage rates fall, models predict a rise in both purchase and refinancing applications.This has left mortgage modelers dazed and confused.

Mortgage rates have been dropping since November, yet mortgage purchase applications dropped in for the latest week. Very likely this was the displacement of purchase applications was simply the “start of the year” effect after a sleepy holiday season.

Ditto for mortgage refinancing applications. Despite mortgage rates declining. there was “start of the year” surge. But continued rate decreases have resulted in generally declining purchase applications after the surge.

On a long term view, purchase applications have remained sedate following the financial crisis and new regulations.

Mortgage refinancing applications remain in Death Valley.

Fannie Mae and Freddie Mac are bankrolling significantly fewer loans this year, reflecting the general slowdown in the residential U.S. mortgage market.

In the nine months through the third quarter, the government-sponsored enterprises (GSEs) purchased a combined 2.47 million home loans, down 9 percent for the same nine months in 2017, the companies reported last week in quarterly reports.

The GSEs bankroll around 45 percent of all residential mortgages, according to the Urban Institute, by purchasing loans from lenders, wrapping them with a government guarantee and securitizing most of them for sale in the secondary market.

The combined balance of these loans through the third quarter was $577 billion, down 7 percent from the 2017 level for the same nine months.

GSE funding activity has dropped for the second consecutive year.

The 2018 year-to-date counts and volume balances were down 16 percent and 15 percent, respectively, compared to same nine months in 2016.

During a conference call last week, Fannie Mae Chief Financial Officer Celeste Brown alluded to tough conditions for lenders.

“At a high level, what I see is that our customers are facing a lot of headwinds in the market,” she said. “Rates are up, volumes are down, and margins are tight, so lender profitability is challenged. New housing supply is up but not all the supply has been created where it’s needed. While we do see income growth nationally, in many markets home-price growth has outstripped income growth so affordability for home buyers remains a challenge,” Brown said.

The numbers have waned as a result of the big drop in refinancing activity. The combined GSE refinance counts totaled 909,000, down 26 percent from the 1.23 million refinance loans acquired by the GSEs through the first nine months of 2017. The GSE reports indicate that cash-out refinancing levels have remained fairly stable, whereas rate-reduction and term refinances are falling steeply.

Meanwhile, the home-purchase market hasn’t grown at anywhere near the pace that refinance activity has been falling.The combined GSE home-purchase loan counts through the third quarter totaled 1.56 million, up 5 percent over the 2017 level.

U.S. home sales are expected to be flat this year or even decline marginally due to rising prices; a lack of affordable, entry-level homes for sale; and rising rates.

“Our expectations for housing have become more pessimistic,” Fannie Mae Chief Economist Doug Duncan said in October. “Rising interest rates and declining housing sentiment from both consumers and lenders led us to lower our home sales forecast over the duration of 2018 and through 2019. Meanwhile, affordability, especially for first-time home buyers, remains atop the list of challenges facing the housing market.”

Fannie Mae’s most recent forecast calls for the origination volume for the entire market to fall 10.5 percent year over year in 2018, to $1.63 trillion. Refinance volume is predicted to decline by 30 percent over the 2017 level to $454 billion. Purchase volume in 2018 will remain essentially flat with the 2017 level at $1.18 trillion, Fannie forecasts.

With purchase applications tumbling alongside the collapse in refinancings, the headline mortgage application data slumped to its lowest level since September 2000 last week.

This should not be a total surprise asWells Fargo’s latest resultsshows the pipeline is collapsing – a forward-looking indicator on the state of the broader housing market and how it is impacted by rising rates, that was even more dire, slumping from $67BN in Q2 to $57BN in Q3, down 22% Y/Y and the the lowest since the financial crisis.

But in the month since those results, mortgage rates have gone higher still… (this is now the biggest 2Y rise in mortgage rates since 2000)…

Sparking further weakness in the housing market…

And absent Christmas weeks in 2000 and 2014, this is the weakest level of mortgage applications since September 2000…

What these numbers reveal, is that the average US consumer can barely afford to take out a new mortgage at a time when rates continued to rise – if not that much higher from recent all time lows. It also means that if the Fed is truly intent in engineering a parallel shift in the curve of 2-3%, the US can kiss its domestic housing market goodbye.

The economist, who predicted the 2007-2008 crisis,told Yahoo Financethat current data shows “a sign of weakness.”

“This is a sign of weakness that we’re starting to see. And it reminds me of 2006 … Or 2005 maybe,”

Housing pivots take more time than those in the stock market, Shiller said, adding that:

“the housing market does have a momentum component and we’re seeing a clipping of momentum at this time.”

The Nobel Laureate explained:

“If the markets go down, it could bring on another recession. The housing market has been an important element of economic activity. If people start to get pessimistic about housing and pull back and don’t want to buy, there will be a drop in construction jobs and that could be a seed for another recession.”

When reminded that 2006 predated the greatest financial crisis in a lifetime,RT notesthat Shiller acknowledged that any correction would likely be far less severe.

“The drop in home prices in the financial crisis was the most severe drop in the US market since my data begin in 1890,” the Yale economist said.

“It could be that we’re primed to repeat it because it’s in our memory and we’re thinking about it but still I wouldn’t expect something as severe as the Great Financial Crisis coming on right now. There could be a significant correction or bear market, but I’m waiting and seeing now.”

(ZeroHedge) When we reported Wells Fargo’s Q1 earningsback in April, we drew readers’ attention to one specific line of business, the one we dubbed the bank’s “bread and butter“, namely mortgage lending, and which as we then reported was “the biggest alarm” because “as a result of rising rates, Wells’ residential mortgage applications and pipelines both tumbled, sliding just shy of the post-crisis lows recorded in late 2013.”

Then, a quarter ago a glimmer of hope emerged for the America’s largest traditional mortgage lender (which has since lost the top spot to alternative mortgage originators), as both mortgage applications and the pipeline posted a surprising, if modest, rebound.

However, it was not meant to last, because buried deep in its presentation accompanyingotherwise unremarkable Q3 results(modest EPS miss; revenues in line), Wells just reported that its ‘bread and butter’ is once again missing, and in Q3 2018 the amount in the all-important Wells Fargo Mortgage Application pipeline shrank again, dropping to $22 billion, the lowest level since the financial crisis.

Yet while the mortgage pipeline has not been worse in a decade despite the so-called recovery, at least it has bottomed. What was more troubling is that it was Wells’ actual mortgage applications, a forward-looking indicator on the state of the broader housing market and how it is impacted by rising rates, that was even more dire, slumping from $67BN in Q2 to $57BN in Q3, down 22% Y/Y and the the lowest since the financial crisis (incidentally, a topic we covered recently in “Mortgage Refis Tumble To Lowest Since The Financial Crisis, Leaving Banks Scrambling“).

Meanwhile, Wells’ mortgage originations number, which usually trails the pipeline by 3-4 quarters, was nearly as bad, dropping $4BN sequentially from $50 billion to just $46 billion. And since this number lags the mortgage applications, we expect it to continue posting fresh post-crisis lows in the coming quarter especially if rates continue to rise.

That said, it wasn’t all bad news for Wells, whose Net Interest Margin managed to post a modest increase for the second consecutive quarter, rising to $12.572 billion. This is what Wells said: “NIM of 2.94% was up 1 bp LQ driven by a reduction in the proportion of lower yielding assets, and a modest benefit from hedge ineffectiveness accounting.” On the other hand, if one reads the fine print, one finds that the number was higher by $80 million thanks to “one additional day in the quarter” (and $54 million from hedge ineffectiveness accounting), in other words, Wells’ NIM posted another decline in the quarter.

There was another problem facing Buffett’s favorite bank: while true NIM failed to increase, deposits costs are rising fast, and in Q3, the bank was charged an average deposit cost of 0.47% on $907MM in interest-bearing deposits, nearly double what its deposit costs were a year ago.

Just as concerning was the ongoing slide in the scandal-plagued bank’s deposits, which declined 3% or $40.1BN in Q3 Y/Y (down $2.3BN Q/Q) to $1.27 trillion. This was driven by consumer and small business banking deposits of $740.6 billion, down $13.7 billion, or 2%.

But even more concerning was the ongoing shrinkage in the company’s balance sheet, as average loans declined from $944.3BN to $939.5BN, the lowest in years, and down $12.8 billion YoY driven by “driven by lower commercial real estate loans reflecting continued credit discipline” while period-end loans slipped by $9.6BN to $942.3BN, as a result of “declines in auto loans, legacy consumer real estate portfolios including Pick-a-Pay and junior lien mortgages, as well as lower commercial real estate loans.” This is a problem as most other banks are growing their loan book, Wells Fargo’s keeps on shrinking.

And finally, there was the chart showing the bank’s overall consumer loan trends: these reveal that the troubling broad decline in credit demand continues, as consumer loans were down a total of $11.3BN Y/Y across most product groups.

What these numbers reveal, is that the average US consumer can barely afford to take out a new mortgage at a time when rates continued to rise – if not that much higher from recent all time lows. It also means that if the Fed is truly intent in engineering a parallel shift in the curve of 2-3%, the US can kiss its domestic housing market goodbye.

Chase, one of the biggest home lenders, announces cutting employees in Florida, Ohio, Arizona.

J.P. Morgan Chase CEO Jamie Dimon, Getty Images

JPMorgan Chase & Co. is laying off about 400 employees in its consumer mortgage banking division as parts of the market slow down, people familiar with the matter said.

The bankJPM, -0.56%one of the largest mortgage lenders with about 34,000 mortgage-banking employees, is in the midst of laying off employees in cities including Jacksonville, Fla.; Columbus, Ohio; Phoenix and Cleveland particularly as mortgage servicing has fallen, the people said.

Home sales have slowed as the rise in mortgage rates has been compounded by a lack of homes for sale, increasing prices and a tax bill that reduced some incentives for home ownership. Rising interest rates have also discouraged homeowners from either refinancing their current mortgage or moving and having to get a new mortgage.

JPMorgan isn’t the only bank to lay off mortgage employees. Wells Fargo & Co.WFC, -0.60%the largest U.S. mortgage lender, said in August it is laying off about 650 mortgage employees who mainly work in retail fulfillment and mortgage servicing “to better align with current volumes.”

You’d think the previous decade’s housing bust would still be fresh in the minds of mortgage lenders, if no one else. But apparently not.

One of the drivers of that bubble was the emergence of private label mortgage “originators” who, as the name implies, simply created mortgages and then sold them off to securitizers, who bundled them into the toxic bonds that nearly brought down the global financial system.

The originators weren’t banks in the commonly understood sense. That is, they didn’t build long-term relationships with customers and so didn’t need to care whether a borrower could actually pay back a loan. With zero skin in the game, they were willing to write mortgages for anyone with a paycheck and a heartbeat. And frequently the paycheck was optional.

In retrospect, that was both stupid and reckless. But here we are a scant decade later, and the industry is headed back towards those same practices. Today’s Wall Street Journal, for instance, profiles a formerly-miniscule private label mortgage originator that now has a bigger market share than Bank of America or Citigroup:

Its rise points to a bigger shift in the home-lending business to specialized mortgage lenders that fall outside the banking sector. Such non-banks, critically wounded in the housing crisis, have re-emerged to become the market’s dominant players, with 52% of U.S. mortgage originations, up from 9% in 2009. Six of the 10 biggest U.S. mortgage lenders today are non-banks, according to the research group.

They symbolize both the healthy reinvention of a mortgage market brought to its knees a decade ago—and how the growth in that market almost exclusively has been in its less-regulated corner.

Post crisis regulations curb bank and non-bank lenders alike from making the “liar loans” that wiped out many lenders and forced a wave of foreclosures during the crisis. What worries some industry participants is that little has changed about non-bank lenders’ structure.

Their capital levels aren’t as heavily regulated as banks, and they don’t have deposits or other substantive business lines. Instead they usually take short-term loans from banks to fund their lending. If the housing market sours, banks could cut off their funding—which doomed some non-banks in the last crisis. In that scenario, first-time buyers or borrowers with little savings would be the first to get locked out of the mortgage market.

“As long as the good times roll on, it’s fine,” said Ed Pinto, co-director of the Center on Housing Markets and Finance at the American Enterprise Institute. “But all I can say is, we’re in a boom, and you cannot keep going up like this forever.”

Freedom was just a small lender in the last crisis. When it became hard to borrow money, Freedom Chief Executive Stan Middleman embraced government-backed loans on the theory they would offer more stability.

As Quicken Loans Inc., the biggest and best-known non-bank, grew with the help of flashy technology and advertising campaigns, Freedom stayed under the radar, buying smaller lenders and scooping up other companies’ huge portfolios of loans, often made to relatively risky borrowers.

Mr. Middleman is fond of saying that one man’s trash is another man’s treasure. “I always believed that, if somebody is applying for a loan, we should try to make it for them,” says Mr. Middleman.

One afternoon this spring, a dozen or so employees lined up in front of Freedom Mortgage’s office in Mount Laurel, N.J., to get their picture taken. Clutching helium balloons shaped like dollar signs, they were being honored for the number of mortgages they had sold.

Freedom is nowhere near the size of behemoths like Citigroup or Bank of America; yet last year it originated more mortgages than either of them, some $51.1 billion, according to industry research group Inside Mortgage Finance. It is now the 11th-largest mortgage lender in the U.S., up from No. 78 in 2012.

What does this mean? Several things, depending on the resolution of the lens you’re using.

In the mortgage market it means that emerging private sector lenders are taking market share – presumably by being more aggressive – which puts pressure on the relatively stodgy brand-name banks to lower their own standards to keep up. To grasp the truth of this, just re-read the last sentence in the above article: “I always believed that, if somebody is applying for a loan, we should try to make it for them.” That is fundamentally not how banks work. Their job is to write profitable loans by weeding out the applicants who probably won’t make their payments.

Now, faced with competitors from the “No Credit, No Problem!” part of the business spectrum, the big guys will once again have to choose between adopting that attitude or leaving the business. SeeBad Bankers Drive Out Good Bankers: Wells Fargo, Wall Street, And Gresham’s Law.Since the biggest mortgage lender is currently Wells Fargo, for which cutting corners is standard practice, it presumably won’t be long before variants of liar loans and interest only mortgages will be back on the menu.

From a broader societal perspective, this is par for the late-cycle course. After a long expansion, most banks have already lent money to their high-quality customers. But Wall Street continues to demand that those banks maintain double-digit earnings growth, and will punish their market caps if they fall short.

This leaves formerly-good banks with no choice but to loosen standards to keep the fee income flowing. So they start working their way towards the bottom of the customer barrel, while instructing their prop trading desks and/or investment bankers to explore riskier bets. Miss allocation of capital becomes ever-more-common until the system blows up.

The signs that we’re back there (2007in some cases,2008in others) are spreading, which means the reckoning is moving from “inevitable” to “imminent”.

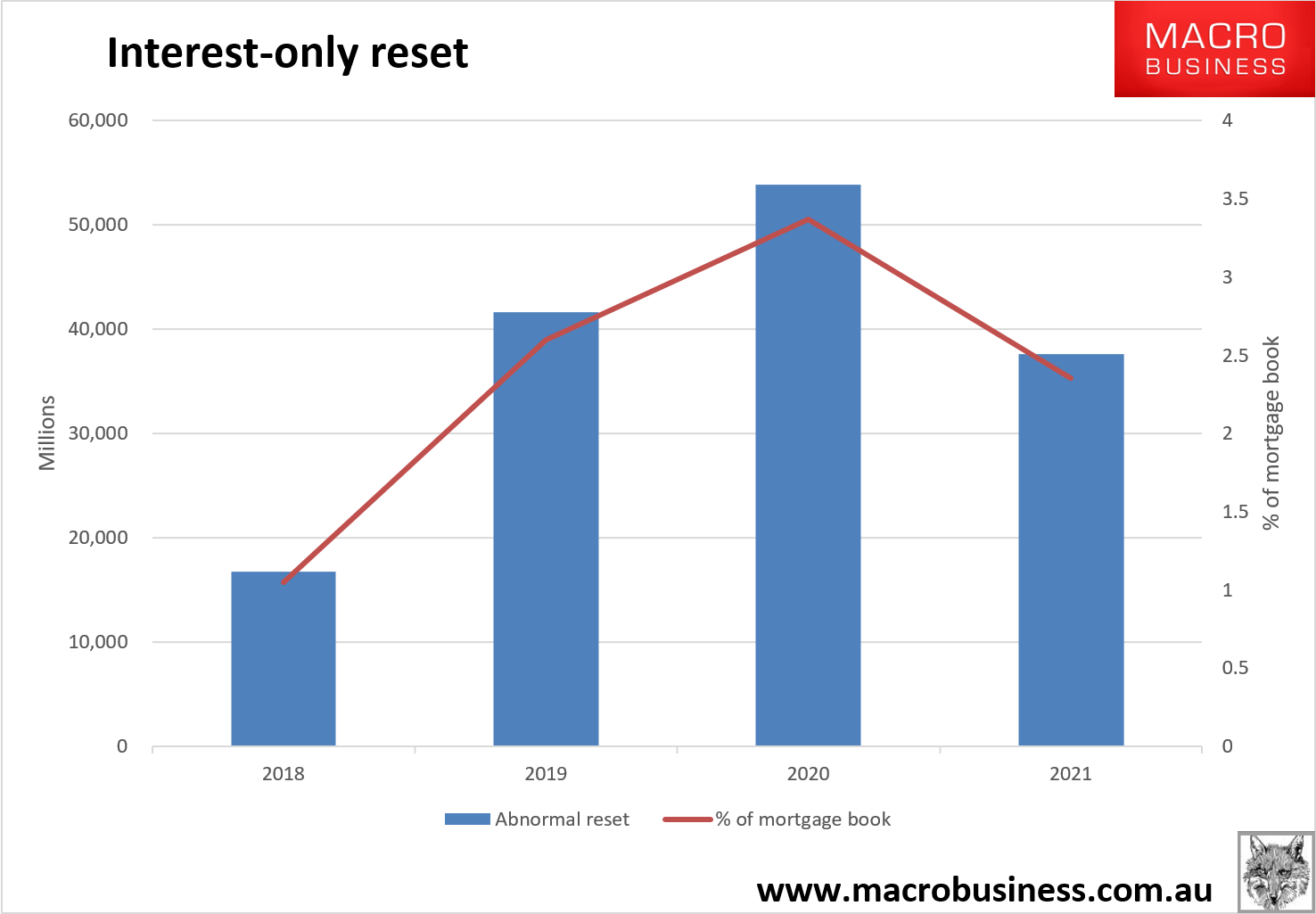

Day of Reckoning: Hundreds of thousands of interest-only loan terms expire each year for the next few years.

The Reserve Bank of Australia (RBA), Australia’s central bank, warns of a$7000 Spike in Loan Repaymentsas interest-only term periods expire.

Every year for the next three years, up to an estimated 200,000 home loans will be moved from low repayments to higher repayments as their interest-only loans expire. The median increase in payments is around $7000 a year, according to the RBA.

What happens if people can’t afford the big hike in loan repayments? They may have to sell up, which could see a wave of houses being sold into a falling market. The RBA has been paying careful attention to this because the scale of the issue is potentially enough to send shockwaves through the whole economy.

Interest Only Period

In 2017, the government cracked down hard on interest-only loans. Those loans generally have an interest-only period lasting five years. When it expires, some borrowers would simply roll it over for another five years. Now, however, many will not all be able to, and will instead have to start paying back the loan itself.

That extra repayment is a big increase. Even though the interest rate falls slightly when you start paying off the principal, the extra payment required is substantial.

Loan Payments

RBA Unconcerned

For now, the RBA is unconcerned: “This upper-bound estimate of the effect is relatively modest,” the RBA said.

Australian Government Rolls Out Universal Reverse Mortgage Plan

The Australian government has proposed a wide-ranging reverse mortgage plan that would make an equity release program available to every senior over the age of 65.

Previously restricted to those who partially participate in the country’s social pension program, the government-sponsored plan will extend to any homeowner above the age cutoff, according to areportfrom Australian housing publication Domain.

Under the terms of the government-sponsored plan, homeowners can receive up to $11,799 each year for the remainder of their lives, essentially taken out of the equity already built up in their homes. Domain gives the example of a 66-year-old who can receive a total of $295,000 during a lifetime that ends at age 91.

As in the United States, older Australians have a significant amount of wealth tied up in their homes; the publication cited research showing that homeowners aged 65 to 74 would likely have to sell their homes in order to realize the $480,000 increase in personal wealth the cohort enjoyed over the previous 12-year span.

In fact, the Australian government last year attempted to encourage aging baby boomers to sell their empty nests to free up the properties for younger families. Under that plan, homeowners 65 and older could get a $300,000 benefit from the government, a powerful incentive in a tough housing market for downsizers — and in a government structure that counts income against seniors when calculating pension amounts.

“Typically, older homeowners have been reluctant to sell for both sentimental and financial reasons,” Domainreportedlast year. “Often selling property is costly, and funds left over after buying a smaller home could then be considered in the means test.”

But the baked-in reverse mortgage benefit represents a shift toward helping seniors age in place instead of downsizing. The Australian government’s “More Choices for a Longer Life” plan also expands in-home care access by 14,000 seniors,accordingto the Financial Review, while boosting funding for elder physical-fitness initiatives and other efforts to reduce isolation among aging Australians.

The reverse mortgage plan will offer interest rates of 5.25%, which Domain noted is less than most banks, and will cost taxpayers about $11 million through 2022. Loan-to-value ratios are calculated to ensure that the loan balance can never exceed the eventual sale price of the home.

Greens leader Richard Di Natale has proposed a radical overhaul of Australia’s welfare system through the introduction of a universal basic income scheme, but critics believe this would only increase inequality.

Di Natale gave a speech at the National Press Club on Wednesday, outlining why he thought Australia’s current social security system was inadequate.

“With the radical way that the nature of work is changing, along with increasing inequality, our current social security system is outdated,” Di Natale said.

“It can’t properly support those experiencing underemployment, insecure work and uncertain hours.

“A modern, flexible and responsive safety net would increase their resilience and enable them to make a greater contribution to our community and economy.”

— National Press Club (@PressClubAust) April 4, 2018

To address this, Di Natale called for the introduction of a universal basic income scheme, which he labelled a “bold move towards equality”.

“We need a universal basic income. We need a UBI that ensures everyone has access to an adequate level of income, as well as access to universal social services, health, education and housing,” he said.

“A UBI is a bold move towards equality. It epitomises a government which looks after its citizens, in contrast to the old parties, who say ‘look out for yourselves’. It’s about an increased role for government in our rapidly changing world.

“The Greens are the only party proudly arguing for a much stronger role for government. Today’s problems require government to be more active and more interventionist, not less.”

However Labor’s shadow assistant treasurer Andrew Leigh, responded on Twitter that Australia had the most targeted social safety net in the world and that Di Natale’s plan would increase inequality.

Aust has the most targeted social safety net in the world. Replacing it with a universal basic income, as @RichardDiNatale suggests, would increase inequality. Why give the same amount to billionaires as battlers? #auspolpic.twitter.com/aHefpfWJpn

Leigh was unavailable for comment when contacted by Pro Bono News, but in aspeechgiven at the Crawford School of Public Policy in April last year, he explained why he opposed a UBI.

“As it happens, using social policy to reduce inequality is almost precisely the opposite of the suggestion that Australia adopt a ‘universal basic income’,” Leigh said.

“Some argue that a universal basic income should be paid for by increasing taxes, rather than by destroying our targeted welfare system. But I’m not sure they’ve considered how big the increase would need to be.

“Suppose we wanted the universal basic income to be the same amount as the single age pension (currently $23,000, including supplements). That would require an increase in taxes of $17,000 per person, or around 23 percent of GDP. This would make Australia’s tax to GDP ratio among the highest in the world.”

Liberal Senator Eric Abetz described Di Natale’s plan as “economic lunacy”.

“Its catastrophic impact would see the biggest taxpayers in Australia, the banking sector, become unprofitable and shut down and his plan for universal taxpayer handouts would see our nation bankrupted in a matter of years,” Abetz said.

“This regressive and ultra-socialist approach of less work, higher welfare and killing profitable businesses has been tried and failed around the world and you need only look at the levels of poverty and riots in Venezuela.

“Senator Di Natale must explain… who will pay for this regressive agenda when he runs out of other people’s money.”

Despite this criticism, welfare groups said they welcomed a conversation on a “decent income for all”.

Dr Cassandra Goldie, the CEO of the Australian Council of Social Service, indicated that a UBI would be discussed among their member organisations.

“We are very glad a decent income for all is being discussed. Too many people lack the income they need to cover even the very basic essentials such as housing, food and the costs of children,” Goldie told Pro Bono News.

“We will be discussing basic income options with our member organisations.

“Our social security system has a job to protect people from poverty and help with essential costs and life transitions such as the costs of children and decent housing. It is failing at this. The basic minimum allowance for unemployed people is just $278 per week.

“Budget cuts – including the freezing of family payments – have made matters worse.”

Goldie said that working out if a basic income proposal would increase or reduce inequality depended on the detail.

“We don’t oppose universal payments on principle, but reform of social security should begin with those who have the least. This must be the first priority,” she said.

“The principle that everyone should have access to at least a decent basic income is a good starting point for reform. Let’s have that debate.”

The convenor of the Anti-Poverty Network SA, Pas Forgione, told Pro Bono News that a UBI would only address inequality if payments were set to an adequate level.

“If universal basic income means that everyone gets the same income that people on Newstart gets, roughly $260 a week, then I don’t think that’s going to do much to alleviate poverty,” Forgione said.

“It needs to be set at an adequate level. And I think that involves looking at what it takes to have a reasonable standard of living and a reasonable quality of life in a country like Australia. So it depends on the details.

“If it is set at an adequate level, than it would be a terrific thing for the quality of life for a number of very low income people. I’m not saying that it’s a panacea… but I think you could make a very strong case for looking at a UBI.”

Di Natale’s speech also called for the creation of a nationalised “People’s Bank”, to give more people access to affordable banking services and to add “real competition” to the banking sector.

“A people’s bank, along with more support for co-operatives and mutuals, would inject some real competition into the banking sector,” he said.

“We have a housing crisis that has been created by governments.

“So now is the time for government to step in: through a People’s Bank, by ending policies skewed in favour of investors like negative gearing and the capital gains tax discount, and through a massive injection of funds for social and public housing.”

The Mortgage Bankers Association returned from its holiday hiatus today, issuing its first update on mortgage applications’ activity since that for the week ended December 16. The results thus include data for the last two weeks and an adjustment to account for the Christmas holiday.

The Market Composite Index, a measure of application volume, for the week ended December 30 was down 12 percent on a seasonally adjusted basis compared to the December 9 summary. Before the adjustment, the drop in application activity was 48 percent.

The Refinance Index decreased 22 percent from two weeks earlier and the seasonally adjusted Purchase Index declined by 2 percent. The unadjusted Purchase Index was 41 percent lower than the two-week old reading and lost 1 percent when compared to the same week in 2015.

Purchase Applications vs. 30-Year Rates:

Its difficult to say at what point consumers thrown in the towel on new home purchases as a number of factors are in play.

Refinance Window Closing Fast:

Refis show a clear pattern. Only those whose interest rate is above the red dotted line is likely to refi. Given closing costs, it’s only profitable to refi when rates are substantially above the red line.

Bear in mind this data is for a slow holiday period. Nonetheless, refi applications behave as expected.

Mortgage Application Activity Wraps Up 2016 on a Down Note

Residential loan application activity continued its post-election slump, declining for the sixth time in the eight weeks, according to the Mortgage Bankers Association’s survey for the week ending Dec. 30. The results included adjustments to account for the Christmas holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 12% on a seasonally adjusted basis from two weeks earlier, the last time the MBA conducted its Weekly Application Survey. On an unadjusted basis, the index decreased 48% compared with two weeks ago. The refinance index decreased 22% from two weeks ago.

The seasonally adjusted purchase index decreased 2% from two weeks earlier, while the unadjusted purchase index decreased 41% compared with two weeks ago and was 1% lower than the same week one year ago.

The refinance share of mortgage activity increased to 52.2% of total applications from 51.8% over the previous seven-day period.

Interest rate comparisons are made with the period ended Dec. 23. The adjustable-rate mortgage share of activity decreased to 5.4%, while the Federal Housing Administration share increased to 11.6% from 10.7% the week prior.

The VA share decreased to 12.3% from 12.4% and the USDA share increased to 1.1% from 1% the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) decreased to 4.39% from 4.45%. For 30-year fixed-rate mortgages with jumbo loan balances (greater than $417,000), the average contract rate decreased to 4.37% from 4.41%.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA remained unchanged at 4.22%, while for 15-year fixed-rate mortgages backed by the FHA, the average decreased to 3.64% from 3.7%.

The average contract interest rate for 5/1 ARMs decreased to 3.28% from 3.41%.

Big banks have drastically reduced their share of the Federal Housing Administration market, a massive shift that has big implications, according to new analysis by the American Enterprise Institute.

Large banks — which had a 60% share of FHA refinancings in late 2013 — had a 6% share as of May 31, according to Stephen Oliner, a resident scholar at AEI. Nonbank lenders currently originate 90% of FHA-insured refinancings, according to new data released by the group.

Large banks also had a 65% share of the FHA purchase market in 2012, which is now down to 20%, according to AEI.

“The shift away from large banks to non-banks and mortgage brokers has been truly massive,” Oliner said.

The recent drop in interest rates is expected to spur another surge in refinancings due to Britain’s unexpected decision to leave the European Union.

But the large banks have decided that refinancing FHA loans is “not a good business” due to the regulatory environment and litigation risk, Oliner said.

“They are getting out,” he said, noting that many FHA lenders have been sued under the False Claims Act and had to pay huge fines to the Justice Department.

Banks also don’t get Community Reinvestment Act credit for refinancings. “So this is pretty much a lose-lose business for them,” Oliner said.

Apparently the biggest banks in the US didn’t learn their lesson the first time around…

Because a few days ago, Wells Fargo, Bank of America, and many of the usual suspects made a stunning announcement that they would start making crappy subprime loans once again!

I’m sure you remember how this all blew up back in 2008.

Banks spent years making the most insane loans imaginable, giving no-money-down mortgages to people with bad credit, and intentionally doing almost zero due diligence on their borrowers.

With the infamous “stated income” loans, a borrower could qualify for a loan by simply writing down his/her income on the loan application, without having to show any proof whatsoever.

Fraud was rampant. If you wanted to qualify for a $500,000 mortgage, all you had to do was tell your banker that you made $1 million per year. Simple. They didn’t ask, and you didn’t have to prove it.

Fast forward eight years and the banks are dusting off the old playbook once again.

Here’s the skinny: through these special new loan programs, borrowers are able to obtain a mortgage with just 3% down.

Now, 3% isn’t as magical as 0% down, but just wait ‘til you hear the rest.

At Wells Fargo, borrowers who have almost no savings for a down payment can actually qualify for a LOWER interest rate as long as you go to some silly government-sponsored personal finance class.

I looked at the interest rates: today, Wells Fargo is offering the exact same interest rate of 3.75% on a 30-year fixed rate, whether you have bad credit and put down 3%, or have great credit and put down 30%.

But if you put down 3% and take the government’s personal finance class, they’ll shave an eighth of a percent off the interest rate.

In other words, if you are a creditworthy borrower with ample savings and a hefty down payment, you will actually end up getting penalized with a HIGHER interest rate.

The banks have also drastically lowered their credit guidelines as well… so if you have bad credit, or difficulty demonstrating any credit at all, they’re now willing to accept documentation from “nontraditional sources”.

In its heroic effort to lead this gaggle of madness, Bank of America’s subprime loan program actually requires you to prove that your income is below-average in order to qualify.

Think about that again: this bank is making home loans with just 3% down (because, of course, housing prices always go up) to borrowers with bad credit who MUST PROVE that their income is below average.

[As an aside, it’s amazing to see banks actively competing for consumers with bad credit and minimal savings… apparently this market of subprime borrowers is extremely large, another depressing sign of how rapidly the American Middle Class is vanishing.]

Now, here’s the craziest part: the US government is in on the scam.

The federal housing agencies, specifically Fannie Mae, are all set up to buy these subprime loans from the banks.

Wells Fargo even puts this on its website: “Wells Fargo will service the loans, but Fannie Mae will buy them.” Hilarious.

They might as well say, “Wells Fargo will make the profit, but the taxpayer will assume the risk.”

Because that’s precisely what happens.

The banks rake in fees when they close the loan, then book another small profit when they flip the loan to the government.

This essentially takes the risk off the shoulders of the banks and puts it right onto the shoulders of where it always ends up: you. The consumer. The depositor. The TAXPAYER.

You would be forgiven for mistaking these loan programs as a sign of dementia… because ALL the parties involved are wading right back into the same gigantic, shark-infested ocean of risk that nearly brought down the financial system in 2008.

Except last time around the US government ‘only’ had a debt level of $9 trillion. Today it’s more than double that amount at $19.2 trillion, well over 100% of GDP.

In 2008 the Federal Reserve actually had the capacity to rapidly expand its balance sheet and slash interest rates.

Today interest rates are barely above zero, and the Fed is technically insolvent.

Back in 2008 they were at least able to -just barely- prevent an all-out collapse.

This time around the government, central bank, and FDIC are all out of ammunition to fight another crisis. The math is pretty simple.

Look, this isn’t any cause for alarm or panic. No one makes good decisions when they’re emotional.

But it is important to look at objective data and recognize that the colossal stupidity in the banking system never ends.

So ask yourself, rationally, is it worth tying up 100% of your savings in a banking system that routinely gambles away your deposits with such wanton irresponsibility…

… especially when they’re only paying you 0.1% interest anyhow. What’s the point?

There are so many other options available to store your wealth. Physical cash. Precious metals. Conservative foreign banks located in solvent jurisdictions with minimal debt.

You can generate safe returns through peer-to-peer arrangements, earning up as much as 12% on secured loans.

(In comparison, your savings account is nothing more than an unsecured loan you make to your banker, for which you are paid 0.1%…)

There are even a number of cryptocurrency options.

Bottom line, it’s 2016. Banks no longer have a monopoly on your savings. You have options. You have the power to fix this.

The purpose of the Federal Housing Administration is “to help creditworthy low-income and first-time home buyers“, individuals and families often denied traditional credit, to obtain a mortgage and purchase a home.” This system has been successful, and has aided in promoting home ownership. However, the FHA loan program and its related benefits are under threat as the Department of Justice continues to bring investigations and actions against lenders under the False Claims Act.