(Neil Callanian) Almost $1.5 trillion of US commercial real estate debt comes due for repayment before the end of 2025. The big question facing those borrowers is who’s going to lend to them?

Tag Archives: CMBS

Negative Returns Are Now In US Mortgages

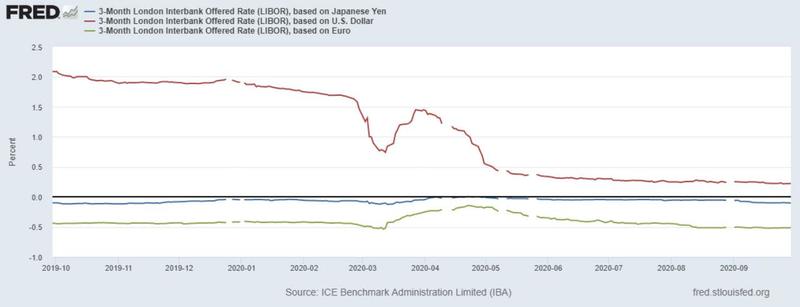

(Christopher Whalen) Watching the talking heads pondering the next move in US interest rates, we are often amazed at the domestic perspective that dominates these discussions. Just as the Federal Open Market Committee never speaks about foreign anything when discussing interest rate policy, so too most observers largely ignore the offshore markets. Yen, dollar and euro LIBOR spreads are shown below.

Zoltan Pozsar, the influential money-market strategist at Credit Suisse (NYSE:CS), warns that the short-end of the US money markets are likely to be awash in cash over the end-of-year liquidity hump. Unlike the unpleasantness in 2018, for example, we may see instead a surfeit of lending as banks scramble for yield in a wasteland bereft of duration. Would that it were so.

The Pozsar view does not exactly fit well with the rising rate, end of the world scenario popular in some corners of the financial media ghetto. The 10-year note is certainly rising and with it the 30-year mortgage rate. Indeed, Pozsar reminds CS clients that yen/$ swaps are now yielding well-above Treasury yields for seven years. Hmm.

We believe short-term rates will remain low in the US, even as offshore demand for dollars soars. If the 10-year Treasury backs up much further, then we’d look for the FOMC to act on some calls by governors to buy longer duration securities. That is, a very direct and large scale increase in QE and particularly on the long end of the curve.

We expect that Chairman Powell knows that underneath the comfortable blanket of low interest rates lie some truly appalling credit problems ahead for the global economy, the US banking sector and also for private debt and equity investors. We expect the low interest rate environment to drive volumes in corporate debt and residential mortgages, even as other sectors like ABS languish and commercial real estate gets well and truly crushed.

“The pandemic is putting unprecedented stress on CMBS markets that even the Fed is having difficulty offsetting,” writes Ralph Delguidice at Pavilion Global Markets.

“Limited reserves are being exhausted even as rent collection and occupancy levels remain serious issues… Bondholders expecting cash are getting keys instead, and in our view, ratings downgrades and significant losses are now only a formality.”

We noted several months ago that the resolution of the credit collapse in commercial mortgage backed securities or CMBS will be very different from when a bank owns the mortgage. As we discussed with one banker this week over breakfast in Midtown Manhattan, holding the mortgage and even some equity in a prime property allows for time to recover value.

With CMBS, the “AAA” tranche is first in line, thus the seniors have no incentive to make nice with the subordinate investors. The deals will liquidate, the property will be sold and the junior bond investors will take 100% losses. But as Delguidice and others note with increasing frequency, this time around the “AAA” investors are getting hit too. More to come.

Manhattan

Meanwhile, over in the relative calm of the agency collateral markets, large, yield hungry money center banks led by Wells Fargo & Co are deploying liquidity to buy billions of dollars in delinquent government loans out of MBS pools.

The bank buys the asset and gives the investor par, with a smidgen of interest. Market now has more cash, but less cash than it had before buying the mortgage bond in the first place. Why? Because it likely took a loss on the transaction. Buy at 109. Prepayment at par six months later. You get the idea.

In fact, if you look at the Treasury yield curve, rates are basically lying flat along the bottom of the chart out to 48 months. Why? Because this nice fellow named Fed Chairman Jerome Powell, along with many other buyers, are gobbling up the available supply of risk free assets inside of five years.

Spreads on everything from junk bonds to agency mortgage passthroughs are contracting, suggesting that the private bid for paper remains strong. When you look at the fact that implied valuations for new production MBS and mortgage servicing rights (MSR) have been rising since July, this even though prepayment rates are astronomical, certainly implies that there is a great deal of cash sitting on the sidelines.

Remember that the price of an MSR is not just about cash flows and prepayments, but it’s also about default rates and the relationship with the consumer. We described in our last missive for The IRA Premium Service (“The Bear Case for Mortgage Lenders”), that a rising rate environment could generate catastrophic losses for residential lenders, particularly in the government loan market. We write:

“For both investors and risk professionals operating in the secondary mortgage market, the next several years contain both great opportunities and considerable risks. We look for the top lenders and servicers to survive the coming winter of default resolution that must inevitably follow a period of low interest rates by the FOMC. The result of the inevitable consolidation will be fewer, larger IMBs.”

Don’t get distracted by the rising rate song from the Street. We don’t look for short or medium term interest rates to rise in the near term or frankly for years. Agency 1.5% coupons “did not find a place in the latest Fed’s purchase schedule. It is possible (they) are included in the next update,” writes Nomura this week. This seems a pretty direct prediction of lower yields. But as one veteran mortgage operator cautions The IRA: “Not just yet.”

We don’t think that the Fed is going to take its foot off the short end of the curve anytime soon, in part because the system simply cannot withstand a sustained period of rising rates. In fact, we note that our friends at SitusAMC are adding 1.5% MBS coupons to forward rate models this month. But that does not necessarily mean that mortgage rates will fall any time soon.

We hear that the Fed of New York has bought a few 1.5s in recent days, but supply is sorely lacking. You see, the mortgage industry is not quite ready to print many new 1.5% MBS coupons and will not do so anytime soon. As the chart above suggests, mortgage rates are in fact rising. Why? Is not the FOMC in charge of the U.S mortgage market?

No, the market rules. Today you can make more money selling a new 1-4 family residential mortgage into a 2.5% coupon from Fannie, Freddie or Ginnie Mae at 105. You book a five point gain on sale and are therefore a hero. And a year from now, after the liquidity does in fact migrate down to 1.5s c/o the beneficence of the FOMC, you can again be a hero.

Specifically, you call up that same borrower and refinance the mortgage into a brand new 1.5% Fannie, Freddie or Ginnie Mae at 105. You take another five point gain on sale. Right? And who paid for this blessed optionality? The Bank of Japan, Peoples Bank of China, and PIMCO, among many other fortunate global investors.

These multinational holders of US mortgage bonds may not like negative returns on risk free American assets, but that’s life in the big city. And thankfully for Chairman Powell, it’s not his problem. Many years ago, a friend in the mortgage market said of loan repurchase demands from Fannie Mae: “What do you want from me?”

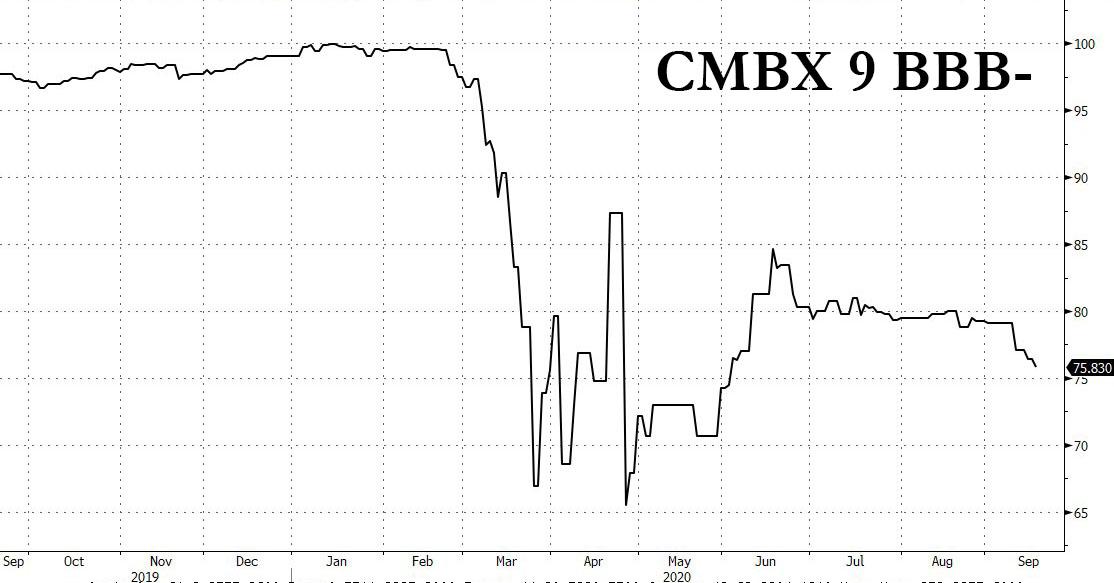

First CMBS Mega-Casualty On Deck: $700MM Starwood Portfolio On Verge Of Default

Over the past 6 months ZeroHedge has repeatedly discussed the plight of commercial real estate which unlike most other financial assets, failed to benefit from a Fed bailout or backstop (but that may soon change). It culminated in June when we wrote that the “Unprecedented Surge In New CMBS Delinquencies Heralds Commercial Real Estate Disaster.” The ongoing crisis in structured debt backed by commercial real estate in general and hotel properties in particular, prompted Wall Street to launch the “Big Short 3.0“ trade: betting against hotel-backed loans, which had the broadest representation in the CMBX 9 index, whose fulcrum BBB- series has continued to slide even as the broader market rebounded.

Commercial Real Estate Paying Lowest Return In Over A Decade

Investors taking on more risk in US commercial real estate are now receiving the lowest return since the housing crisis. The premium spread for buying BBB- tranches of commercial mortgage backed securities versus AAA is the lowest its been since May 2007, according to a new report from analytics company Trepp, the FT reports.

The euphoria associated with the US economy even as the overall global economy is rolling over means that those bearing the brunt of risk for commercial mortgage backed securities are getting paid the least. This also comes as a result of investors chasing yield, which could be another obvious canary in the coal mine that the now record bull market could be reaching an apex.

“As you get toward the latter innings of the credit cycle, people have money they need to put to work and they take on more risk for less return,” said Alan Todd, a CMBS analyst at Bank of America Merrill Lynch.

Commercial mortgage backed securities are made up of a combination of types of mortgages which are then divided up by risk. Traditionally, as with any financial instrument, the more risk that investors bear, the more they get paid. But now, investors are looking more and more like they’re “picking up pennies in front of bulldozers” as demand for AAA tranches of CMBS’ has fallen. Meanwhile BBB- slices of CMBS continue to see an influx of demand. The conclusion?

“You are probably not getting paid for the risk you are taking and that definitely concerns us,” Dushyant Mehra, co-chief investment officer at Hildene, told the Financial Times.

The Federal Reserve’s tightening could be another potential cause for the shift: higher quality fixed rate investments like AAA tranches of CMBS, have fallen in price as a result of Fed policy. This, in turn, has caused investors to seek out riskier products, like floating rate company loans, to juice returns.

Meanwhile, the boom in commercial housing has resulted in a significant amount of CMBS supply. $49 billion in new issuance between January and July of this year eclipses the $45 billion that was sold throughout the same period of time last year.

The credit premium between AAA and BBB-, which is as low as you can go without hitting a junk rating, has fallen to 2.1% in August from 2.2% in July, according to the report. While this is below the 2014 low of 2.3%, it still is nowhere near the pre-financial crisis lows of just 0.67%, which printed in May 2007 when everyone was long, and just before RMBS and CMBS blew up, catalyzing the financial crisis.

“It is something everyone frets over,” Gunter Seeger, a portfolio manager at fund manager PineBridge, said of the evaporating premium investors are demanding. “You are always concerned that the pendulum swings too far but the reach for yield is still there.”

Everyone may be “fretting” but it has yet to stop them from buying.

As is the case during any euphoric period, few are paying attention and taking the data as a warning. Perhaps once the numbers start to move closer to May 2007 levels, it will catch people’s attention, although considering that even the Fed has repeatedly warned about “froth” in commercial real estate with no change in behavior, it is safe to say that no lessons from the financial crisis have been learned.

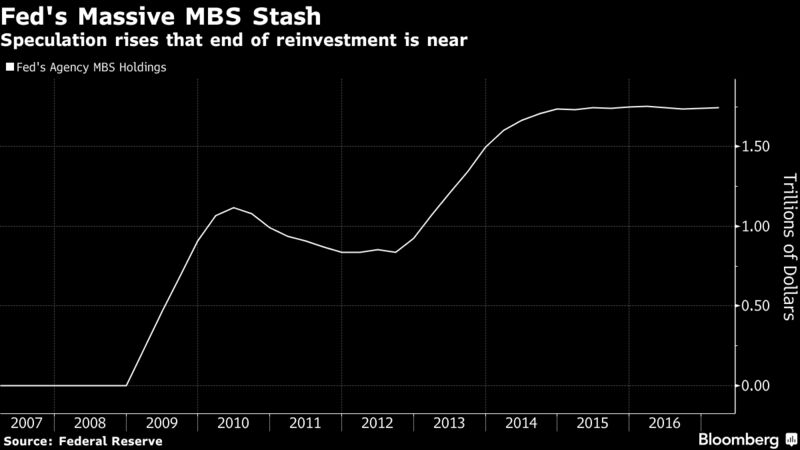

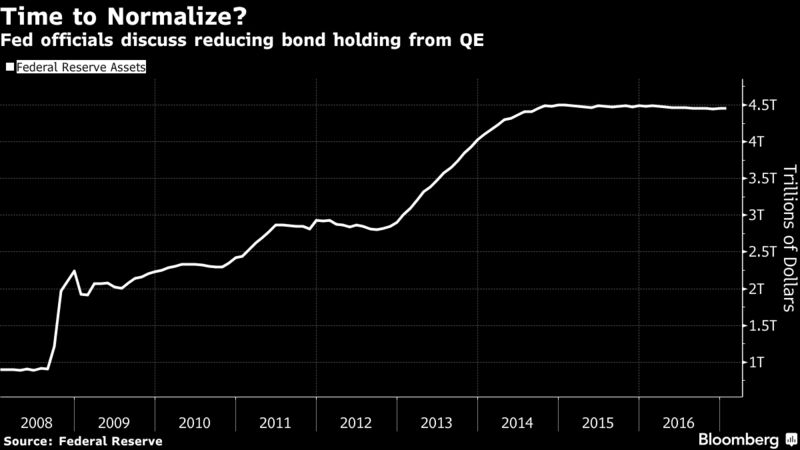

The Mortgage-Bond Whale That Everyone Is Suddenly Worried About

◆ Fed holds $1.75 Trillion of MBS from quantitative easing program ◆

◆ Comments spur talk Fed may start draw down as soon as this year

Almost a decade after it all began, the Federal Reserve is finally talking about unwinding its grand experiment in monetary policy.

And when it happens, the knock-on effects in the bond market could pose a threat to the U.S. housing recovery.

Just how big is hard to quantify. But over the past month, a number of Fed officials have openly discussed the need for the central bank to reduce its bond holdings, which it amassed as part of its unprecedented quantitative easing during and after the financial crisis. The talk has prompted some on Wall Street to suggest the Fed will start its drawdown as soon as this year, which has refocused attention on its $1.75 trillion stash of mortgage-backed securities.

While the Fed also owns Treasuries as part of its $4.45 trillion of assets, its MBS holdings have long been a contentious issue, with some lawmakers criticizing the investments as beyond what’s needed to achieve the central bank’s mandate. Yet because the Fed is now the biggest source of demand for U.S. government-backed mortgage debt and owns a third of the market, any move is likely to boost costs for home buyers.

In the past year alone, the Fed bought $387 billion of mortgage bonds just to maintain its holdings. Getting out of the bond-buying business as the economy strengthens could help lift 30-year mortgage rates past 6 percent within three years, according to Moody’s Analytics Inc.

Unwinding QE “will be a massive and long-lasting hit” for the mortgage market, said Michael Cloherty, the head of U.S. interest-rate strategy at RBC Capital Markets. He expects the Fed to start paring its investments in the fourth quarter and ultimately dispose of all its MBS holdings.

Unprecedented Buying

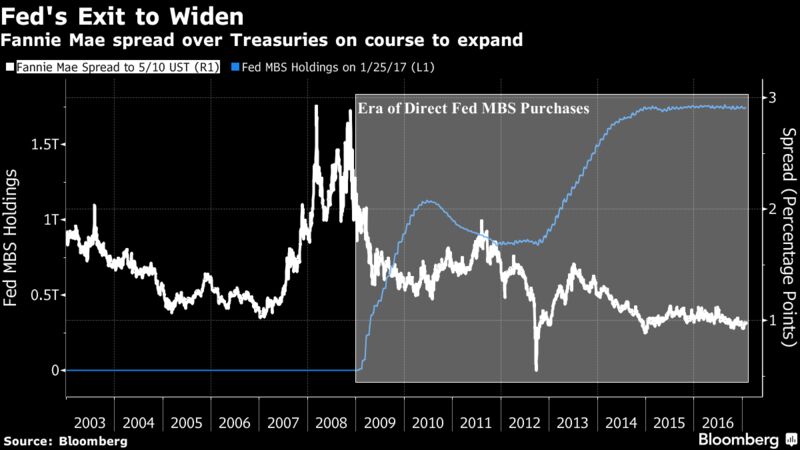

Unlike Treasuries, the Fed rarely owned mortgage-backed securities before the financial crisis. Over the years, its purchases have been key in getting the housing market back on its feet. Along with near-zero interest rates, the demand from the Fed reduced the cost of mortgage debt relative to Treasuries and encouraged banks to extend more loans to consumers.

In a roughly two-year span that ended in 2014, the Fed increased its MBS holdings by about $1 trillion, which it has maintained by reinvesting its maturing debt. Since then, 30-year bonds composed of Fannie Mae-backed mortgages have only been about a percentage point higher than the average yield for five- and 10-year Treasuries, data compiled by Bloomberg show. That’s less than the spread during housing boom in 2005 and 2006.

Talk of the Fed pulling back from the market has bond dealers anticipating that spreads will widen. Goldman Sachs Group Inc. sees the gap increasing 0.1 percentage point this year, while strategists from JPMorgan Chase & Co. say that once the Fed actually starts to slow its MBS reinvestments, the spread would widen at least 0.2 to 0.25 percentage points.

“The biggest buyer is leaving the market, so there will be less demand for MBS,” said Marty Young, fixed-income analyst at Goldman Sachs. The firm forecasts the central bank will start reducing its holdings in 2018. That’s in line with a majority of bond dealers in the New York Fed’s December survey.

The Fed, for its part, has said it will keep reinvesting until its tightening cycle is “well underway,” according to language that has appeared in every policy statement since December 2015. The range for its target rate currently stands at 0.5 percent to 0.75 percent.

Mortgage Rates

Mortgage rates have started to rise as the Fed moves to increase short-term borrowing costs. Rates for 30-year home loans surged to an almost three-year high of 4.32 percent in December. While rates have edged lower since, they’ve jumped more than three-quarters of a percentage point in just four months.

The surge in mortgage rates is already putting a dent in housing demand. Sales of previously owned homes declined more than forecast in December, even as full-year figures were the strongest in a decade, according to data from the National Association of Realtors.

People are starting to ask the question, “Gee, did I miss my opportunity here to get a low-rate mortgage?” said Tim Steffen, a financial planner at Robert W. Baird & Co. in Milwaukee. “I tell them that rates are still pretty low. But are rates going to go up? It certainly seems like they are.”

Part of it, of course, has to do with the Fed simply raising interest rates as inflation perks up. Officials have long wanted to get benchmark borrowing costs off rock-bottom levels (another legacy of crisis-era policies) and back to levels more consist with a healthy economy. This year, the Fed has penciled in three additional quarter-point rate increases.

The move to taper its investments has the potential to cause further tightening. Morgan Stanley estimates that a $325 billion reduction in the Fed’s MBS holdings from April 2018 through end of 2019 may have the same impact as nearly two additional rate increases.

Finding other sources of demand won’t be easy either. Because of the Fed’s outsize role in the MBS market since the crisis, the vast majority of transactions are done by just a handful of dealers. What’s more, it’s not clear whether investors like foreign central banks and commercial banks can absorb all the extra supply — at least without wider spreads.

On the plus side, getting MBS back into the hands of private investors could help make the market more robust by increasing trading. Average daily volume has plunged more than 40 percent since the crisis, Securities Industry and Financial Markets Association data show.

“Ending reinvestment will mean there are more bonds for the private sector to buy,” said Daniel Hyman, the co-head of the agency-mortgage portfolio management team at Pacific Investment Management Co.

What’s more, it may give the central bank more flexibility to tighten policy, especially if President Donald Trump’s spending plans stir more economic growth and inflation. St. Louis Fed President James Bullard said last month that he’d prefer to use the central bank’s holdings to do some of the lifting, echoing remarks by his Boston colleague Eric Rosengren.

Nevertheless, the consequences for the U.S. housing market can’t be ignored.

The “Fed has already hiked twice and the market is expecting” more, said Munish Gupta, a manager at Nara Capital, a new hedge fund being started by star mortgage trader Charles Smart. “Tapering is the next logical step.”

Struggling Shopping Malls Pose Outsized Risk to CMBS

Like used cars and retired pro football players, regional shopping malls do not age well.

Like used cars and retired pro football players, regional shopping malls do not age well.

In a span of no more than a decade, a popular mall with high-end anchor stores and boutique retail tenants can fall into substandard Class B or C property condition, left behind by shifting customer demographics or newer amenities at rival shopping centers. More so today, they also face the reality of more consumers choosing to stay home to shop online.

When these malls become passé, that’s when trouble starts for commercial mortgage bond investors, who can sustain outsized losses on their exposure to these properties, compared with other kinds of collateral such as office buildings, hotels and industrial property.

In a report published Thursday, Moody’s Investors Service warned that loans backed by shopping centers are an increasing cause of concern for mortgage bond investors and provided some criteria for evaluating the long-term viability of regional malls.

“The ability of a mall to adapt to this changing environment and find new ways to attract shoppers is key to its ongoing success,” the report states. “Very few of the top tenants in malls 20 years ago are still strong performers — or even in still in business — today.”

Moody’s looked at the loss severity on loans backed by 30 regional malls that have liquidated since 2008: each averaged 75%, almost twice as severe as the 45% average for all other CMBS loan liquidations in that time period. In the case of 10 of the failed malls, the loss severity was over 100%.

Loans backed by shopping malls are typically structured no differently than other kinds of commercial mortgages: they have 10-year tenors with large balloon payments due at maturity, meaning they amortize very little during their terms. The issue is that malls can have relatively short lives as premier properties, and so may need new capital investments — and thus new financing — within a decade to expand their shelf life.

Individual malls have been under pressure to maintain their appeal and customer interest since the 1980s, but these challenges are now exacerbated by competition from online retailers, which is hitting traditional mall anchor stores like Macy’s and Sears particularly hard. With a business model dependent on traffic driven by magnet department stores, malls could be in significant trouble, and as a result, perform poorly as CMBS collateral.

For example, Macy’s plans to shutter 100 stores this year, a move that Morningstar Credit Ratings estimates could impact $3.64 billion in outstanding securitized commercial mortgages backed by malls with Macy’s as a prime tenant.

So how can CMBS investors assess their risk?

To find out, Moody’s mapped out the capabilities of local and national mall owners to keep their properties viable and profitable during long-term 10- to 20-year leases. Demographics, location and property age were not the only, or the most important, factors. Some properties like The Florida Mall in Orlando having weathered the replacement of four anchor stores over 30 years to remain a competitive shopping mecca in central Florida.

Malls that maintain upscale amenities and ties to national ownership attract high-end, non-anchor stores (or “inline” tenants, with stores under 10,000 square feet), the report noted. The healthiest malls average more than $400 in per-square-feet sales for their non-anchor stores, and have occupancy cost ratios (tenant real estate costs divided by gross sales) above 13% for its inline tenants.

Those gross sales figures for the strongest malls, as measured by Moody’s, exclude the transactions from high-demand boutique retail outlets that skew sales figures, such as Apple Stores. An Apple retail store by itself can boost a mall’s sales per square foot by $100, Moody’s stated.

Weaker malls will usually average inline store sales of no more than $275 per square foot and have locations with limited demographics and fewer national chain tenants. If they do have chain tenants, those stores will likely have lower-than-average sales figures for than sister stores across the country.

Low traffic volume, whether due to mundane store options or too few neighboring entertainment and dining establishments, often gives malls less negotiating power with tenants over rent terms. These property owners might have to accept “gross” leases where the tenant pays a percentage of sales versus a base rent for occupancy.

Net income operating margins could fall below 65%, sometimes 50% for struggling substandard malls, compared to 70%-80% for the stronger malls that can demand excess percentages above base rents. Strong performers can also draw up “triple net” leases that foist some of the real estate expenses onto some tenants.

National sponsorship is considered a key indicator for a strong mall’s performance, with ability to provide more incentives for key anchor tenants to maintain or expand their presence. A sell-off by a national ownership group to a local owner can often trigger a mall’s weakening performance — tenants may ask for rent relief or may exit the mall in the absence of a national ownership backer.

Even if weaker-performing malls demonstrate stability, investors must weigh the cost-effectiveness of when the inevitable, and capital-intensive, rehab of a mall must be undertaken. For “highly productive” malls, Moody’s stated, the high cost of market repositioning or a refresh of the tenant lineup can be justified. For less-productive malls, they are often forced to sell well below par to give new owners the capital space to invest in a revitalization project.

“Depreciation for malls is not just an accounting concept; malls need to stay current and vibrant or risk a reduction in their earnings power,” the report states.