Rents are growing at half the pace they were in the summer and are expected to keep cooling, which should help bring down overall inflation

Tag Archives: Rent

Largest Private U.S. Landlord Jacking Rents As Purchasing Power Of Blown USD Evaporates

Demand for single-family rental homes is off the charts and shows no signs of abating anytime soon, and that is pushing rents sky-high. This has allowed the largest owner of houses in the U.S. to raise rents.

Another Month, Another Record Surge in U.S. Rents To a New All Time High

And Now Prices Are Really Soaring: June Rent Jump Is Biggest On Record

According to the report, so far in 2021, average rental prices have grown a staggering 9.2%.

And Now Prices Are Really Soaring: May Rent Jump Is Biggest On Record

With BofA predicting that the US is facing a period of “transitory hyperinflation” as a result of soaring commodity prices in everything from metals to food…

National Apartment Rents Rise After Pandemic Plunge

As the virus pandemic upended life last year, pricey cities across the US experienced rapid declines in rent prices and widespread concessions. The COVID-19 vaccine rollout, reopening the economy, and higher employment have brought some people back to cities searching for rentals.

Now, US rents are beginning to move higher. Median US asking rent rose 1.1% on an annual basis in March to $1,463 a month across 50 of the largest metro areas, according to WSJ, citing a Realtor.com report.

Rep. Omar Reintroduces Bill To Cancel Rent, Mortgage Payments

(Arnie Aurellano) Rep. Ilhan Omar, D-Minnesota, has introduced the Rent and Mortgage Cancellation Act, a bill that would cancel rents and mortgage payments nationwide through the duration of the COVID-19 pandemic.

MICHAEL BROCHSTEIN/ECHOES WIRE/BARCROFT MEDIA/GETTY IMAGES

The legislation would constitute full payment forgiveness, with no accumulation of debt for renters or homeowners and no negative impact on their credit rating or rental history. Just as significantly, it would also establish relief funds for mortgage holders and landlords to cover the losses incurred from such payment cancellations.

Fight Over Commercial Rent Gets Ugly With Default Wave Looming

(Bloomberg) — Tension is rising in the messy fight over commercial rent payments.

With stores shuttered, struggling retailers are skipping rent and asking for concessions, while landlords are demanding payment and having their own tricky conversations with lenders.

There are no easy answers as officials ponder how to safely get the economy back open. So far this month, some mall owners and other retail landlords collected as little as 15% of what they were owed, according to one estimate. And it’s expected to get worse, with more than $20 billion in rent payments coming due in May.

“It’s all over the map what’s happening out there,” said Tom Mullaney, a managing director in restructuring at Jones Lang LaSalle Inc. “More and more defaults are coming in every single day.”

Companies across the U.S. — from small mom-and-pop operations to giant corporations — have missed April payments or sent out relief requests citing store closures because of the pandemic.

Pushing Back

Landlords have been pitching rent deferment, saying tenants can make reduced payments now as long as they pay the balance at some point. Some businesses are pushing back on that option and asking for rent cuts even after stores are open again.

U.S. retail landlords typically collect more than $20 billion in rent each month, according to data from CoStar Group Inc. So far, April rent collection has ranged from 15% to 30% for landlords with higher concentrations of shuttered businesses, according to an estimate from brokerage firm Marcus & Millichap.

Landlords, who are facing their own debt defaults, are getting frustrated. Some are complaining that large corporations are using the crisis to skip out on rent. Others say they’re not responsible for bailing out tenants and that the federal government or insurance companies should cover the costs instead.

“The landlords are triaging the battlefield,” said Gene Spiegelman, vice chairman at Ripco Real Estate Corp. “The super powerful and strong are not going to get any help and the ones that’ll die anyways, landlords will say why would I help them?”

Some Pay

To be sure, some landlords and tenants are working out deals on a case-by-case basis. And some companies are paying rent for their stores. That includes AT&T Inc. and T-Mobile USA Inc. according to people familiar with the matter. J.C. Penney also said it paid for April.

Ross Stores Inc. and fitness chain Solidcore, meanwhile, are among those standing firm on requests for rent abatements and asking for additional concessions. Williams-Sonoma Inc. is another chain that has stopped paying rent, according to people familiar.

Ross has told landlords that after the shutdown ends their rent on some stores should be cut until sales rebound. Solidcore hasn’t agreed to rent deferral and said it likely won’t be able to pay the same rent as it was before pandemic.

“We’re not going to be bullied by the landlords during this time,” said Anne Mahlum, the fitness company’s founder and chief executive officer said. “We have some leverage here. What are they going to do, say get out and then have vacancy for months on end?”

Backfire

Tenants’ refusal to pay will likely backfire, according to Jackson Hsieh, CEO of retail landlord Spirit Realty Capital Inc.

The firm, which owns more than 1,700 properties, has seen requests for rent relief since the crisis started. But several of those tenants ended up paying, according to Hsieh.

One agreed to pay after getting loans from the government’s relief package, while another did so after being asked to provide financial information. A discount retailer and a company in the auto industry paid after Spirit refused to consider their rent deferral requests.

“If a tenant just says I’m not going to pay, fine, I’ll default you, I’m going to go to the courts, and you have 30 days to pay or quit,” Hsieh said. “I don’t want to be negative, but we own the building.”

Pending Loans

Many landlords are rushing to work out deals with lenders to stave off their own defaults. Banks and insurance companies are negotiating deals on a case-by-case basis, but borrowers in commercial mortgage-backed securities have fewer options.

About 11% of U.S. CMBS retail property loan borrowers have been late on April payments so far, according to preliminary analysis by data firm Trepp. If that number holds up, $13 billion worth of CMBS loans could miss payments for the month.

“The banks are a little more fluid and often there’s recourse,” said Camille Renshaw, CEO brokerage firm B+E. “But many large properties have CMBS debt and when there’s a crisis, no one is there to pick up the phone to negotiate.”

It’s just not retail stores that are suffering. Office space is a ghost town thanks to the Wuhan (bat) virus outbreak. But with tools like Zoom, Webex, Microsoft Teams, GotoMeeting, Skype, etc., one wonders if the days of massive office building demand is over. Other than for socializing and monitoring employees (as Bill Lumbergh did in “Office Space.”)

Of course, administrators can always contact you at home during virtual classes.

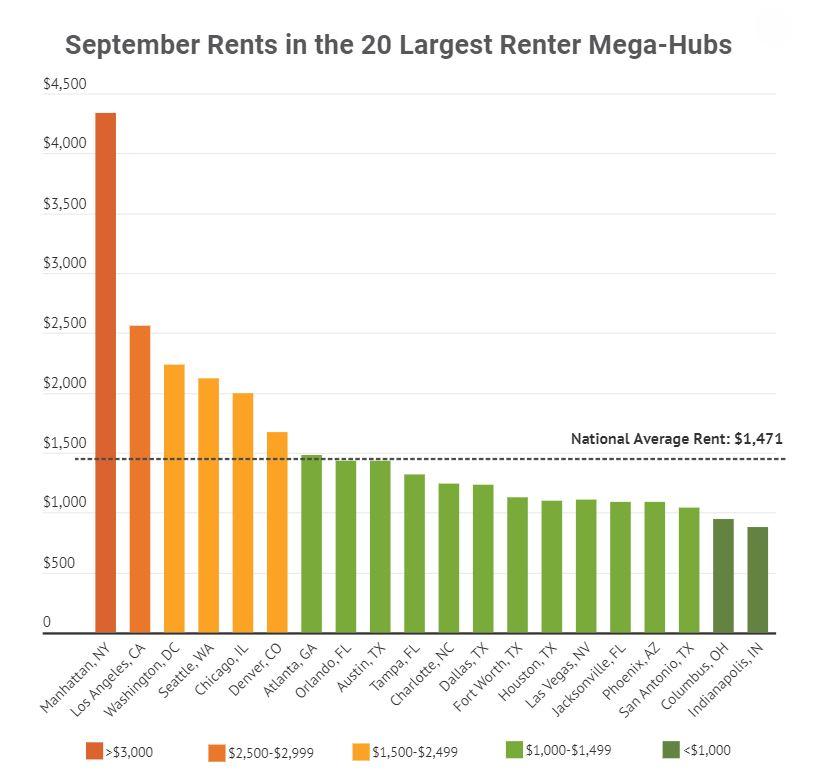

National Average Rent Drops For First Time In 2 Years As US Property Market Sags

Here’s the latest sign that the US housing market is in the early phases of a nation-wide retreat: For the first time in two years, average national monthly rents declined on a QoQ basis – even as the national average rent continued to climb (up 3.2%) on a YoY basis.

Corresponding with the summer slowdown (a period when the rental market is at its slowest), the national average rent decreased for the first time since February 2017, declining by 0.1% – or $1 – from last month to $1,471, according to Rent Cafe’s quarterly report on the American market for rental housing.

The decrease might seem insignificant, but combined with the slowest year-over-year hike in the past 13 months – 3.2% ($45) – it suggests a slight wind-down in rent prices against the backdrop of a more volatile financial climate, according to Yardi Matrix.

Apartment rents have seen minor declines since last month in more than half of the cities analyzed by RentCafe, with small and large cities leading the trend (prices dropped 59% in small cities, and 56% in large cities), while 42% of mid-sized cities saw rental rates decline in September.

These cities recorded the biggest declines:

- Provo (-2.2%)

- North Charleston(-1.5%)

- Santa Clara (-1.3%)

- Portland (-1.2%)

- Midland (-1.5%)

These cities saw the biggest upticks:

- Syracuse (2.2%)

- Moreno Valley (2.1%)

- Manhattan (1.5%)

- Torrance (1.4%)

- Los Angeles (1.2%)

Interestingly enough, changing the time frame slightly presents an entirely different picture. Rents for apartments in more than half of the largest rental hubs in the country have declined between August and September. This includes 65% of the country’s mega hubs (like Manhattan).

Meanwhile, rents decreased in three of the five most expensive large cities in the country since August, during which time only NY hubs recorded an increase. Rents in the Bay Area retreated by -0.1% in San Francisco ($3,703) and -1.1% in San Jose ($2,762) while average rent in Manhattan and Brooklyn ($2,956 for both now) increased by 1.5% and 0.5% on an MoM basis, respectively.

Across the ‘small cities’ category, cities and areas that were already among the cheapest to live in saw their average rents decline, as did the most expensive small cities, like San Mateo, Calif. which saw its average rent decline slightly by 0.5% between August and September. Cambridge, Mass., another one of the most expensive small cities, also saw its average rent decline by 0.6% during the same period..

Meanwhile, after a 0.8% drop, the average rental price in Brownsville, TX, known to Rent Cafe as the cheapest town to rent in, reached $721.

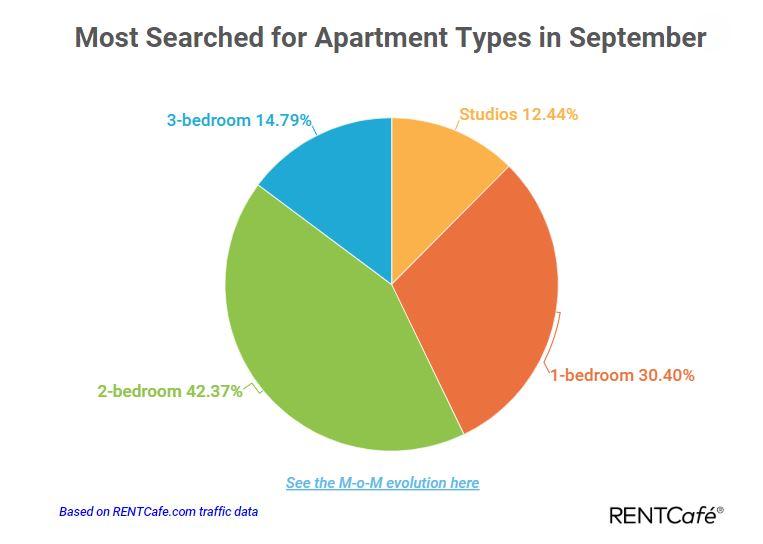

On another tip, Rent Cafe’s data revealed that two-bedroom apartments are the most popular among renters.

As for the survey’s methodology, the company’s researchers analyze data collected across 260 of the largest cities and greater metropolitan areas in the US, while the data on average rents comes directly from competitively-rented (market-rate) large-scale multifamily properties (mostly apartment buildings with at least 50 units). Though it’s different from federal data on the housing market, the study offers some insight into the behavior of people who rent apartments, who are typically younger and without families. All of these data are collected, compiled and analyzed via the Yardi Matrix, a data analysis tool.

Coastal Cities Lead In Apartment Rents

Not surprisingly, apartment rents in the US are the highest in land-use restricted coastal cities like San Francisco, New York city, San Jose CA, Boston and Washington DC. Other west coast cities and Miami round out the remaining top ten most expensive apartment rents.

According to Zumper, North Carolina (Raleigh and Charlotte) and Arizona (Glendale and Scottsdale) along with Fort Worth TX saw the biggest increases in apartment rents.

–Raleigh, NC saw one bedroom rent climb 5.1%, which was the largest monthly rental growth rate in the nation, to $1,040. This large bump moved the city up 2 positions to become 49th most expensive rental market.

–Charlotte, NC took a 5 ranking bump up to 26th with one bedroom rent climbing 5% to $1,260 and two bedrooms increasing 2.2% to $1,370.

–Glendale, AZ jumped up 7 spots to rank as the 67th most expensive city. One bedroom rent grew 5% to $840, while two bedrooms were up 1.9% to $1,070.

–Scottsdale, AZ saw one bedroom rent climb 4.5%, settling at $1,380, and up 3 positions to become the 21st priciest city.

–Fort Worth, TX moved up 3 spots to rank as 40th with one bedroom rent jumping 4.5% to $1,150 and two bedrooms increasing 2.3% to $1,340.

On the downward side, tax- and pension-crazy Chicago has fastest declining rents. And it is Always Sunny In Philadelphia for rents!

–Chicago, IL fell 2 spots to rank as the 17th priciest city with one bedroom rent dropping 5.1%, which is tied with Bakersfield’s growth rate as the largest dip in the nation, to $1,490.

–Bakersfield, CA saw one bedroom rent drop 5.1%, settling at $740, and down 7 positions to become 86th.

–Anchorage, AK moved down 3 spots to 62nd with one bedroom rent falling 4.2% to $910. Two bedrooms, on the other hand, were flat at $1,150.

–Atlanta, GA took a 4 ranking dip to 22nd with one bedroom rent decreasing 4.2% to $1,370 and two bedrooms down 3.3% to $1,740.

–Philadelphia, PA one bedroom rent dropped 3%, settling at $1,310, and down 2 spots to rank as the 24th priciest city. Two bedrooms stayed stable at $1,700.

Of the top 100 cities, LeBron James’s home town of Akron has the lowest apartment rents in the nation. Followed closely by other non-coastal cities like Wichita, Detroit, Lubbock TX and Tucson AZ. And if you are taken back to Tulsa, you will find relatively inexpensive apartment rents.

Rent Unaffordability Continues To Grow For Americans

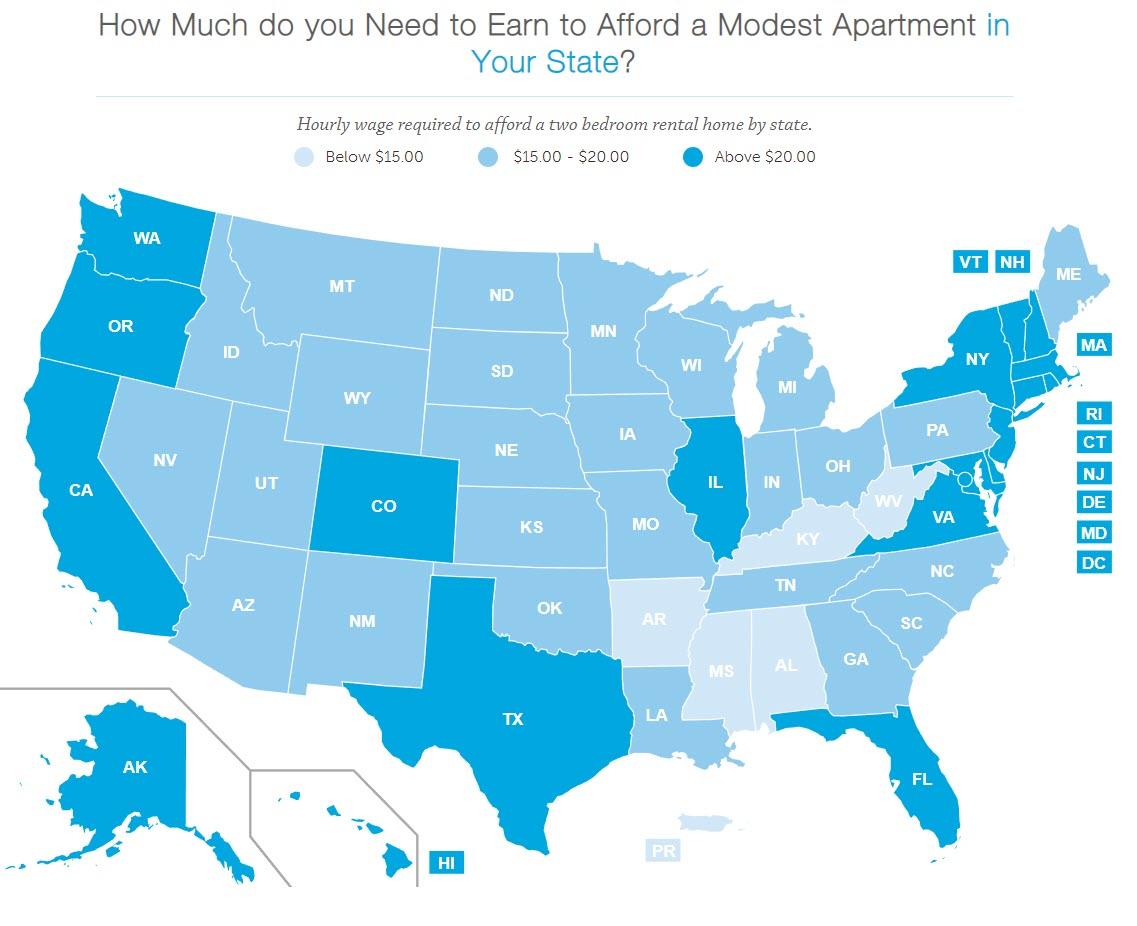

The National Low Income Housing Coalition has published its latest “Out of Reach” report which shows that renting is becoming increasingly unaffordable for countless Americans.

Its central statistic is the Housing Wage which is an estimate of the hourly wage a full-time worker must earn to rent a home without spending more than 30 percent of his or her income on housing costs. As Statista’s Niall McCarthy notes, for 2019, the Housing Wage is $22.96 and $18.65 for a modest two and one-bedroom flat respectively based on the “fair market rent”.

A worker earning the federal wage would have to put in 127 hours every week – equivalent to more than two full-time jobs – to afford a two-bedroom apartment. It isn’t just a regional issue – there isn’t a single state, metro area or county in the U.S. where a full-time worker earning the minimum wage can afford to rent a two-bedroom property.

It isn’t just workers on the minimum wage who are effected.

The report also states that the average renter’s hourly wage is $1.08 less than the Housing Wage for a one-bedroom rental and $5.39 less than a two-bedroom rental. That means that an average renter in the U.S. has to work a 52 hour week, something that becomes increasingly difficult if that renter is a single parent of someone struggling with a disability. When it comes to the situation in different occupations, a median-wage worker in eight of the country’s largest ten occupations does not earn enough to afford a one-bedroom apartment.

(source)

(source)

Software developers, general managers and nurses are able to meet both Housing Wages but for many other occupations and accomodations, renting is becoming increasingly difficult. Medical assistants, laborers and janitors are among those falling short while the gap back to minimum wage workers is even greater still. Worryingly, these are the ten jobs that are expected to see the biggest growth over the coming decade and that is likely to result in an even greater disparity between wages and housing costs by 2026.

US Rents Climb To Fresh Record Highs Despite Slowest Price Increase In 11 Months

US existing home sales slumped for the 13th straight month in March, but the pressures on the national housing market have yet to translate into cheaper rents: To wit, average national rent climbed 3% YoY in April, and 0.3% from the prior month, according to Yardi Matrix data cited by RentCafe.

The national average rent hit $1,436 in April, climbing about $42 from the prior year to $1,436 – which, though still positive, marked the slowest pace of growth in 11 months.

Across major US housing markets, rent in Wichita is the most affordable, averaging $646, followed by Tulsa, at $688. On the other end of the spectrum is the average rent in Manhattan, the world’s most expensive rental market, climbed to $4,130 in April. Behind Manhattan is – of course – San Francisco, with an average rent of $3,647, then Boston ($3,357) then Brooklyn ($2,878), then San Jose ($2,720) and Los Angeles ($2,471), in sixth place. Of the largest metropolitan rental hubs, Indianapolis had the lowest average rent ($861), followed by Columbus, Ohio ($924).

While rents tended to be highest in urban enclaves along the coasts, some large rental markets in the Sun Belt boasted surprisingly affordable prices, including Las Vegas ($1,061) or Phoenix ($1,046).

But in another sign of just how skewed rents are across the US, of the 253 cities examined as part of the study, only 64% have average rents below the $1,436 national average, while the other 36% have average rents above.

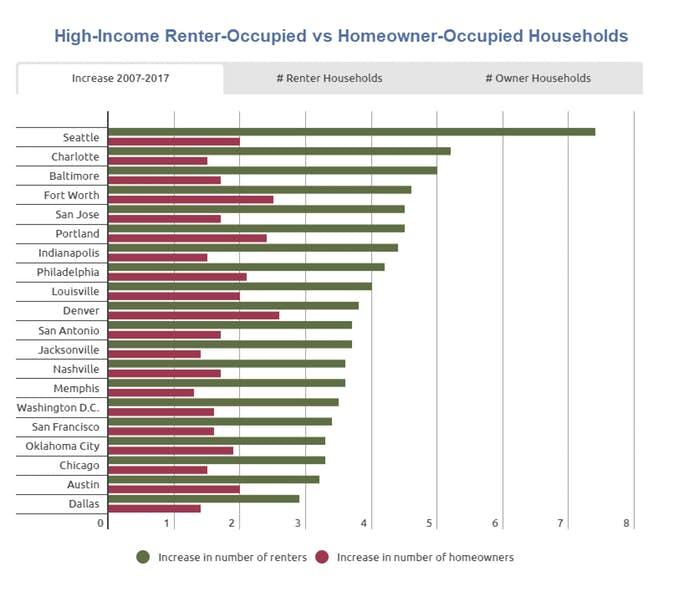

Why Are An Increasing Number Of High-Income Americans Choosing To Rent?

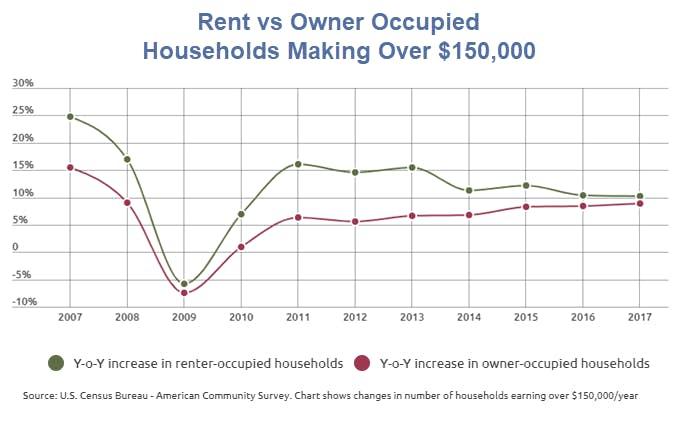

(MishTalk) The percentage of high-income households choosing to rent is on the rise. High-income is defined as $150,000 and up.

The Rent Cafe reports High-Income Americans Are the Fastest Growing Renter Segment — Up by 1.35 Million in a Decade.

The most recent U.S. Census data tells us that the annual increase in the number of high-income renter-occupied households – defined here as those earning $150,000 or more – has been consistently faster than owner-occupied households. As a matter of fact, from 2007 to 2017, the numbers of those rich enough to own, yet who still prefer to rent grew by 175%. That’s compared to a decade-long increase of 67% in homeowners within the same income bracket.

Top-Earning Renters Are Growing Faster than Any Other Renter Income Bracket

Of the 43.3 million renters nationwide, 2.1 million are top earners. High-income renters represent the demographic that experienced the largest boom across the U.S. given that, back in 2007, there were only 774,000.

Breakdown

- Over $150K — ↑175%

- $100K – $150K — ↑111%

- $75K – $100K — ↑66%

- $50K – $75K — ↑32%

- Under $50K —↓0.2%

High-Income Renter-Occupied vs Homeowner-Occupied Households 2007-2017

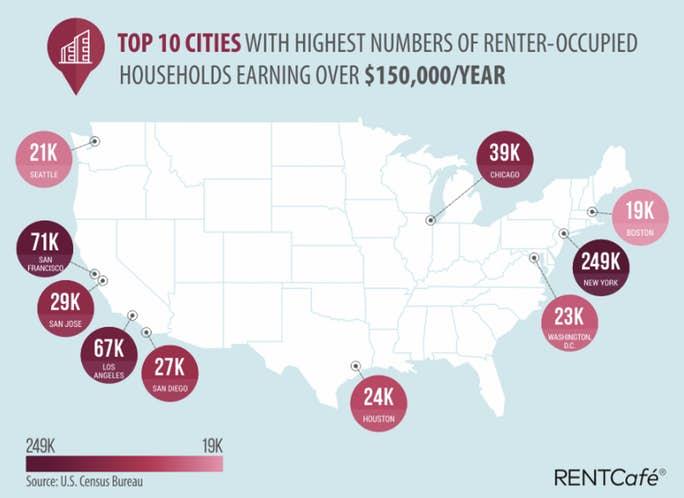

Debate Over High-Income Definition

Arguably, $150K may not be enough to qualify as high-income in places like San Francisco or New York City, which is probably why the two cities have the largest numbers of renter-occupied households inside this bracket.

NYC’s upper-bracket renters outpace owners not only in net numbers but also in the rate of increase. Wealthy renter-occupied households in New York doubled in the course of a decade, going from 125,000 in 2007 to the largest number of wealthy renters in the U.S. today — 249,000. As for people earning $150K or more who own a home in the Big Apple, their numbers have increased by a lesser 63% over the course of a decade (189,000 in 2007 to 306,000 ten years later).

Top 10 Cities With High-Income Renters

American Dream

The Rent Cafe concluded. “The attitude toward renting at any income level is changing. With renters becoming the majority population in many U.S. cities, the spike in the national population of wealthy renter households could mean a change in attitude toward an American Dream that no longer belongs to this generation of renters.”

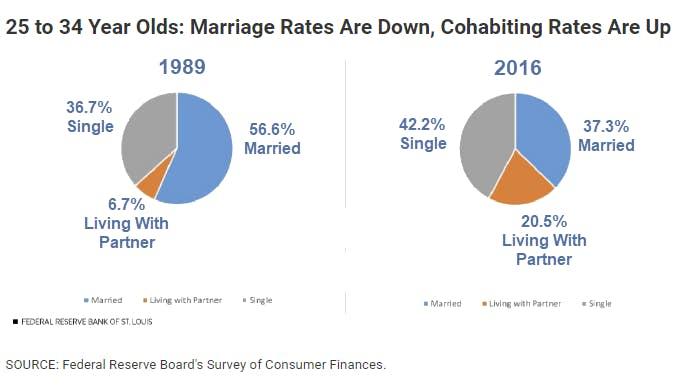

Marriage Rates Down, Cohabitation Up

Not Just Student Debt

The Rent Cafe article ties in nicely with my previous report: Marriage Rates Down, Cohabitating Rates Up: It’s Not Just Student Debt to Blame

Attitudes, Attitudes, Attitudes

A Fed study on Consumers and Communities released last month had an interesting comment on homeownership.

“We estimate that roughly 20 percent of the decline in homeownership among young adults can be attributed to their increased student loan debts since 2005. Our estimates suggest that increases in student loan debt are an important factor in explaining their lowered homeownership rates, but not the central cause of the decline.”

The rest is explained by changing attitudes and affordability.

Attitudes about marriage, having kids, mobility, and debt have all changed.

This is not 1960 or 1971.

To top it off, houses simply are not affordable. That’s what the cohabitation rate shows. Wages have not kept up with home prices even without the burden of student debt.

American Dream

Even when high-income households can afford a house, many choose to rent instead. Why?

- Changing attitudes about the “American Dream”.

- The Marriage Tax Penalty

- The Remarriage Penalty

Reader “Cecilia” thoughtfully added “Liquidity and Walk Away Arbitrage”, which also ties into the remarriage issue.

Remarrying can greatly complicate divorce financial arrangements. It’s easier to live with someone. No one wants a second divorce, especially if the first one was messy.

Oregon Defies Logic With Statewide Rent Control

It is often said by cynical economists and political commentators, usually of the right or libertarian persuasion, that the road to hell is paved with good intentions. There is no more odious and damaging economic policy that comes from the heart than rent control. For years, limiting the cost of living spaces was done at the local level, but one West Coast state aims to be the first to implement statewide rent controls.

Oregon’s Proposed Rent Controls

Oregon is set to pass SB 608, legislation that prohibits landlords from raising rents in the first year of a resident’s tenancy. The bill would also cap future rent hikes at 7% annually, plus inflation. This will target all rental properties 15 years or older but exempt units that are a part of a government housing project.

It should be noted that SB 608 does not have vacancy controls, which means buildings can jack up the rent by any amount once the tenant gives his or her notice. Because of this, the legislation bans no-cause evictions, so any landlord must offer a government-approved excuse for evicting a tenant.

With Democratic supermajorities in both chambers of the legislature, SB 608 is likely to pass, making Oregon the first state with statewide rent control.

Gov. Kate Brown (D-OR) is proud of the move, saying in her inaugural address:

“We also need to help Oregonians who have homes but are struggling with the high cost of rent. We can help landlords and tenants navigate this tight housing market. Speaker [Tina] Kotek and Sen. [Ginny] Burdick have innovative proposals that will give renters some peace of mind.”

Lawmakers are jubilant over the bill, but economic experts call the Beaver State’s policy proposal risky, including Mike Wilkerson of ECONorthwest, an economics consulting firm, telling Reason: “You’d be hard-pressed to find any economist who comes out in favor of rent control as a means to help improve whatever failure you are experiencing.”

Rent Control Hurts the Poor

First, it is important to examine the justification for rent controls. Advocates contend that it is immoral for someone who has lived in a neighborhood his entire life to be suddenly priced out of it. It is also wrong, they assert, that landlords are just sitting on their rear ends, enjoying higher rents, because there is a greater demand to reside in New York, San Francisco, or Boston than in Jerome, AZ, or Bonanza, CO.

Proponents will ignore the unintended consequences of rent control. New properties are not erected, vacancy rates plunge, existing landlords exit the market, and the small supply of housing diminishes. Landlords will try to evade regulations by transforming their units into condominiums, luxury apartments, furnished suites, or offices.

Advocates also overlook two other important facts: Real estate can be utilized for a diverse array of purposes (commercial, housing, or industrial), and these laws distort pricing signals.

Ultimately, the state plays a game of cat-and-mouse, coming up with intrusive ways to rein in the evaders. Regulation begets regulation.

New York City

When World War II ended and peacetime reigned supreme in America again, things were not what they used to be, at least for the thousands of troops returning home. After being engaged in battles overseas, soldiers had a new front to fight at home: life – and everything it had to offer.

Despite the inflation rate either contracting or rising in single digits between 1947 and 1952, the cost of living ballooned for the returning heroes of the Armed Forces. One area of the country that increasingly priced these men out of the market was New York City, where real estate values were skyrocketing – and still are!

Officials had an idea to help everyone affected by rising housing costs: rent controls. While the goal was to make units more affordable, the city made the situation worse by introducing temporary relief.

Like economist Milton Friedman once quipped, “There is nothing more permanent than a temporary government program.” This relic of 1947 is still around today, exacerbating the housing affordability crisis. It is estimated that approximately 50,000 apartments and one million rent-stabilized units are controlled by a 70-year-old law.

To understand how egregious this policy is, look no further than former Rep. Charles Rangel (D-NY). The Wall Street Journal reported in September 2008 that he occupied “four rent-stabilized apartments in a posh New York City building,” living in three and using another as an office. By holding four properties, he took advantage of valuable resources at below-market prices at the expense of others.

Controls

Is there a difference between bombs and rent control? Economists often pose this question when debating the efficacy of government controls. The Mises Institute’s Joseph Salerno delivered a lecture a few years ago, showing pictures of urban areas and asking his audience if these dilapidated units were the victims of a bombing campaign or rent controls.

When you even pose the question, you know it’s necessary to second-guess the prescription.

Any time officials use “controls,” you know the policy is going to be a failure. Whether it is preceded by “price” or “rent,” this economically defiant measure produces destitution, deterioration, and destruction. It’s too bad politicians and bureaucrats never learn their lesson.

The “Rental Affordability Crisis” Explained In Three Charts

Four years ago, the United States Department of Housing and Urban Development (HUD) warned of “the worst rental affordability crisis ever,” citing data that:

“About half of renters spend more than 30% of their income on rent, up from 18% a decade ago, according to newly released research by Harvard’s Joint Center for Housing Studies. Twenty-seven percent of renters are paying more than half of their income on rent.”

This is a significant problem for US consumers, and especially millennials, because as we have noted repeatedly over the past year, and a new report confirms, “rent increases continue to outpace workers’ wage growth, meaning the situation is getting worse.”

In the second quarter of 2017, median asking rents jumped 5% from $864 to $910. In the first half of 2018, they have remained at levels crushing the American worker.

While the surge in median asking rents has triggered an affordability crisis, new data now shows just how much a person must make per month to afford rent.

According to HowMuch.Net, an American should budget 25% to 30% of monthly income for rent, but as shown by the New Deal Democrat, workers are budgeting about 50% more of their salaries than a decade earlier. The report specifically looked at the nation’s capital, where a person must make approximately $8,500 per month to afford rent.

In California, the state with the largest housing bubble, the monthly income to afford rent is roughly $8,300, followed by Hawaii at $7,800 and New York at $7,220.

In contrast, the Rust Belt and the Southeastern region of the United States, one needs to make only $3,500 per month to afford rent.

“Based on the rule of applying no more than one-third of income to housing, people living in the Northeast must earn at least twice as much as those living in the South just to afford rent for what each market considers an average home,” HowMuch.net’s Raul Amoros told MarketWatch.

Which, however, is not to say that owning a house is a viable alternative to renting. In fact, as Goldman notes in its latest Housing and Mortgage Monitor, “buying is looking increasingly less affordable vs. renting with home prices growing faster than rents.”

In short: the situation is not likely to improve in the short-term.

A sign of relief could be coming in the second half of 2019 or entering into 2020 when the US economy is expected to enter a slowdown, if not outright recession. This would reverse the real estate market, thus providing a turning point in rents that would give renters relief after a near decade of overinflated prices.

New York Millennials Paying $1800 Per Month To Cram Into 98-Square-Foot Rooms

Millennials in New York are known for living in a state of perpetual brokeness – between student loans, $20 nightclub drinks and $15 avocado toast, it’s easy to understand why 70% of millennials have less than $1,000 in savings.

Now we can add expensive, glorified closets to the mix, as the Wall Street Journal reports.

30-year-old marketing manager Scott Levine lives in an $1,800 per month, 98-square-foot room in a postage-stamp of an apartment – “basically, a kitchen” – with two roomates. Every week, someone from Ollie – his property manager, stops by to drop off towels and toiletries.

A “community-engagement team” at Ollie helps plan Mr. Levine’s social calendar. A live-in “community manager”—sort of like a residential adviser for a college dorm—gets to know Mr. Levine and everyone else living on the 14 Ollie-managed floors of the Alta LIC building, known as Alta+, and finds creative ways to get them engaged in shared activities, like behind-the-scenes tours of Broadway shows or trips to organic farms. –WSJ

“Life in general can be a bit of a headache,” says Mr. Levine. Thanks to Ollie, he adds, “Everything is done for you, which is convenient.”

Ollie’s business model is all about convenience and roommates – usually single people in their 20s and 30s who have all amenities provided for them, while sharing a kitchen and common area.

For city-dwellers accustomed to living cheek-by-jowl with people whose names they’ll never bother to learn, this might seem strange. But for young people still forming their postcollege friend groups—in an era when participation in civic life is down and going to a bar can mean huddling in a corner swiping on Tinder—it makes sense. So much sense that people put up with apartments so small they’re called “micro.” But hey, free shampoo. –WSJ

Meanwhile, startups such as Ollie and Common are competing with big-city real-estate developers. Common manages 20 co-living properties in six cities where roommate situations are more common, such as New York, Los Angeles and Washington DC. They have approximately 650 renters according to CEO Brad Hargreaves.

“Our audience is people who make $40,000 to $80,000 a year, who we believe are underserved in most markets today,” Mr. Hargreaves says.

Other startups are managing existing homes and apartments, “Airbnb-style” as the WSJ puts it.

Bungalow, which just announced $64 million in funding, wants property owners to offer space to “early-career professionals” looking for a low-maintenance place to stay. It charges rent that’s “slightly higher” than what it pays those owners, a company spokeswoman says. It currently maintains over 200 properties—housing nearly 800 residents—across seven big cities, says co-founder and CEO Andrew Collins.

As with Common and Ollie, Bungalow advertises that it furnishes the common areas in its homes, installs fast free Wi-Fi, and cleans them regularly. The company also organizes events and outings to help you “build a community with… your new friends.” –WSJ

One of the underlying aspects of the co-living startup models is a technology platform that both advertises to prospective tenants and takes care of their needs once they’re living on-site. Ollie’s “Bedvetter” system, for example, shows apartments to potential tenants – and shows who’s already signed up to live there with links to their personal profiles in order to match roommates. Bedvetter also matches people into “pods” of “potential roommates” before they begin an apartment hunt.

“It’s like online dating,” says Levine – while his roommate, Joseph Watson, 29, compares it to eHarmony or Match.com vs. Tinder, as it’s designed for long term pairings.

“Micro Economics”

While millennials in New York and other urban areas scramble to make ends meet, developers are making hand over fist on the co-living movement – even though the renters themselves are paying less than they would for a private studio.

The Alta LIC building also has conventional apartments, but the co-living units are filling up faster, says Matthew Baron, one of the Alta LIC building’s developers. What’s more, he adds, he can get more than $80 a square foot for Ollie units compared with around $60 a square foot for the others, even though the Ollie ones are on the lower, less-desirable floors. –WSJ

Another complication with co-living arrangements is tricky community management. L.A.’s PodShare, for example, vets potential tenants beforehand – however issues with problem tenants are unavoidable. “We’ve hosted 25,000 people at this point, so there’s bound to be some problems,” says founder Elvina Beck.

Common building tenant Teiko Yakobson said that the “community vibe broke down after Common eliminated the paid “house leader,” complaining that “We all just became strangers, and it was no better than living in any other apartment.” Common instead replaced the program with “centralized” community managers at the corporate level – which Hargreaves says is “more coherent” for them.

It’s not all bad, however…

When it does work, co-living can re-create the kind of communities tenants seek online—ones grounded in common interests and shared socioeconomic status.

Mr. Levine, who not only lives in a co-living building but also works in a co-working space—and in whose social circle most people do either one of those or the other—is aware that, while this isn’t for everyone, he is hardly a standout. “One thing I’ve heard before is that I’m a stereotype of a New York millennial,” he says.

Just make sure you have earplugs in case your roommate is able to get laid in their respectively expensive, tiny room.

Average US Rent Hits All Time High Of $1,412

With core CPI printing at a frothy 2.4%, and the Fed’s preferred inflation metric, core PCE finally hitting the Fed’s 2.0% bogey for the first time since 2012, inflation watchers are confused why Jerome Powell’s recent Jackson Hole speech was surprisingly dovish even as inflation threatens to ramp higher in a time of protectionism and tariffs threatening to push prices even higher.

But the biggest concern from an inflation “basket” standpoint has little to do with Trump’s trade war, and everything to do with shelter costs, and especially rent, the single biggest contributor to the Fed’s inflation calculation. It’s a concern because according to the latest report from RentCafe and Yardi Matrix, which compiles data from actual rents charged in the 252 largest US cities, fewer than expected apartment deliveries this year increased competition among existing units, pushing up the national average rent by another 3.1% – the highest monthly increase in 18 months – to $1,412 in August, an all time high.

The national average monthly rent swelled by $42 since last August and $2 since last month. Above-average numbers of renters renewing leases at the end of the summer and heightened demand from college-age renters also contributed to the rise in rents this time of year.

The rental market is so hot right now – perhaps a continue sign that most Americans remain priced out of purchasing a home – that rents increased in 89% of the nation’s biggest 252 cities in August, stayed flat in 10% of cities, and dropped in only 1% of cities compared to August 2017. Queens (NYC), Las Vegas, and Phoenix rents increased the most in one year, while Baltimore, San Antonio, and Washington, DC rents have changed the least among the nation’s largest cities.

Here are the main highlights for large, mid-size and small markets:

- Renter Mega-Hubs: The largest increases were in Orlando (7.7%) and Phoenix (6.8%), while Manhattan (1.9%) and Washington, D.C. (2.1%) saw some of the slowest growing rents in this category. The biggest net changes were felt by renters in Los Angeles, which pay $102 more per month this August compared to last year.

- Large cities: Rents in Queens and Charlotte surge by 8.4% and 5.2% respectively, but barely move in Baltimore (0.2%) and San Antonio (1.5%).

- Mid-size cities: Mesa (6.9%), Tampa (6.4%), and Sacramento (5.5%) rents increase at the fastest pace. At the other end of the spectrum, rents only ticked up in Virginia Beach (1.4%) and Albuquerque (1.7%).

- Small cities: Due to limited stock and high demand, Lancaster and Reno rents soared by 9.7% and 11.3% respectively. Apartment prices in Midland (31.9%) and Odessa (30%) are over $300 per month more expensive than in August 2017. Brownsville (-2%) and Baton Rouge (-0.7%) saw rents decrease over the past year.

Orlando’s fast-growing rents outpaced the nation’s largest renter hubs

Of the top 20 largest renter hubs in the U.S., Orlando apartments are seeing the highest increase in rent over the past year, 7.7%, reaching $1,393 in August, while San Antonio apartments saw the weakest rent growth of the 20 cities, 1.5% in one year, posting an average rent of $996 per month in August. The biggest net changes in rent compared to August 2017 were felt by renters in Los Angeles, who are paying on average $102 per month more this August compared to the same month last year. Orlando rents increased by no less than $99 per month, and Tampa, Chicago, and Manhattan (New York City) rents are $77 above last year’s average. At the opposite end, rents in San Antonio saw the smallest uptick, only $15 more per month than they were one year ago.

NATIONAL LEVEL: Rents in Nevada and Arizona feel the heat from increased demand

Housing in the Permian Basin continues to see the steepest price increases in the country. Apartments for rent in Midland, TX now cost $1,595 per month, a 31.9% leap from one year prior. Likewise, rentals in neighboring Odessa, TX cost $1,365 on average, having jumped 30% in one year.

- Reno, NV‘s housing crunch is worsening due to limited land development and high demand for rentals. Rents in Reno are the third fastest rising in the country, behind only Midland and Odessa. The average rent in Reno is $1,253 per month, a massive 11.3% increase year over year, or $127 more per month compared to the same time last year. The average rent in Reno was around $900 just three years ago but has jumped by more than $300 in 36 months, making it increasingly unaffordable for renters. Nevada’s growing popularity as a destination for those moving out of California is reflected in rapidly-growing real estate prices. Besides Reno, apartments in Las Vegas are also getting expensive, with the third fastest growing rents in the U.S. compared to other large cities.

- Peoria, AZ is facing a similar situation. What used to be an affordable town in the Phoenix area, with an average rent of about $900 per month no more than three years ago, now has apartments that go for $1,114 per month on average, over $200 more expensive, a big leap and a heavy burden for the area’s renters. Compared to August 2017, the average rent in Peoria is 10.1% or $102/month more expensive, the fourth fastest growing this August out of 252 cities surveyed. Likewise, rents in other parts of the Phoenix metro are also rising faster than most other parts of the country, as a consequence of strong demand boosted by big increases in population.

- Lancaster, CA is fifth in the U.S. in terms of fastest-growing rents. The average rent in Lancaster shot up 9.7% year over year, reaching $1,274 per month. The likely reason? Not enough apartments are being built to keep up with the surge in renter population in this town located on the northern fringes of Los Angeles County.

On the other end of the national spectrum, rent prices have decreased in August in border town Brownsville, TX (-2% y-o-y), Orange County’s Irvine, CA (-0.9% y-o-y), Norman, OK (-0.9% y-o-y), Baton Rouge, LA (-0.7%) and Dallas suburb Richardson, TX (-0.6%). Amarillo, TX, New Haven, CT, Baltimore, MD, Frisco, TX and Stamford, CT round up the 10 slowest growing rent prices in the U.S. in August.

LARGE CITIES: Rents rise the fastest in Queens, NY, Phoenix, AZ and Las Vegas, NV

- Step aside Brooklyn: rent prices are now racing in the NYC borough of Queens, up 8.4% compared to last year, with an average rent of $2,342, behind Manhattan’s average rent of $4,119 and Brooklyn’s $2,801. Rents in Manhattan are among the slowest growing in the U.S., 1.9%, while in Brooklyn rents were up 3.9%.

- The second fastest growing rents among the nation’s largest cities are in Phoenix, AZ, up 6.8% over the year. The area has seen a surge in population in search of affordable housing and job opportunities. Even with prices of apartments growing at annual rates of 6-7%, the average rent is still affordable at $996 per month, especially when compared to most other major cities in the country.

- Las Vegas is an increasingly popular place to move to, as Census population estimates show, but the local real estate market is slow to respond. New apartment construction is low, causing rents to go up significantly. An apartment in Las Vegas costs on average $1,011, up 6.2% since August 2017.

At the same time, rents decreased in August in border town Brownsville, TX (-2% y-o-y), Orange County’s Irvine, CA (-0.9% y-o-y), Norman, OK (-0.9% y-o-y), Baton Rouge, LA (-0.7%) and Dallas suburb Richardson, TX (-0.6%). Amarillo, TX, New Haven, CT, Baltimore, MD, Frisco, TX and Stamford, CT round up the 10 slowest growing rent prices in the U.S. in August.

MID-SIZE CITIES: Mesa and Tampa apartments see steepest rises in rents

Apartments in Mesa, AZ and Tampa, FL are seeing price increases above 6% in August. Rents in Mesa reached $965 per month, and in Tampa the average rent is $1,287. Sacramento, Pittsburgh, and Fresno wrap up the top 5, with annual price increases of above 5%.

- Pittsburgh, PA is emerging as a hot rental market, as the city’s job market is gaining traction in tech-related fields. The average rent in Steel City is $1,216, but it is expected to keep growing as apartment construction is not yet in line with the sudden increase in demand.

At the other end of the chart are Wichita, KS, with rents decreasing by 0.8%, Lexington, KY, where prices for apartments moved by 1.1% in one year, Tulsa, OK, where rents changed by 1.3%, Virginia Beach, with prices up by only 1.4% and Albuquerque, NM, where rents saw a 1.7% uptick. The average rent in Lexington sits at $889 per month, in Virginia Beach it is slightly higher, at $1,169 per month, and in Albuquerque, it averages $852 per month.

SMALL CITIES: Rents in Midland and Odessa are over $300 per month more expensive than last year

The most fluctuating prices are in small cities at both ends of the list. The top 20 list of highest annual rent increases is dominated by small cities (17 out of 20). Midland and Odessa, however, stand out from the rest of them, with annual percentage increases of over 30%, which translate into an additional $300 or more per month to the average rent check. The region is economically centered around the shale/oil industry and it’s booming, and real estate prices are taking off as well.

Small cities make up most of the bottom of the list, as well, in terms of slowest growing rents: Brownsville, TX, Irvine, CA, Norman, OK, Baton Rouge, LA, and Richardson, TX saw rents stagnate over the past year. Akron, OH, Thousand Oaks, CA, and McKinney, TX are in the same boat.

In terms of absolute prices, the top cities with the 10 highest rents in the country remains unchanged. Manhattan is still the most expensive, with apartment rents at $4,119, San Francisco is second, with an average rent of $3,579, and Boston is third, with an average rent of $3,388. San Mateo, CA and Cambridge, MA also have an average rent above $3,000 per month. The cheapest rents of the 252 cities surveyed are in Wichita, Brownsville, and Tulsa, all below $700 per month.

According to RentCafe, much of the change in rent prices we see this year is driven by how much demand there is in a specific area and what that area does to deal with it. However, the underlying factors are more complex. The housing market continues to change as a result of the 2007 subprime crisis, according to Doug Ressler, Director of Business Intelligence at Yardi Matrix. Furthermore, markets are undergoing a significant change driven by dramatically different demographic trends. Trends vary by market and will be impacted by population aging, population growth, immigration and home ownership trends, says Ressler.

Naturally, they will also be impacted by the state of the economy, the Fed’s monetary policy and the level of the capital markets.

However, should the current rental surge continue, the Fed will have no choice but to hike rates far higher than the general market consensus expects, especially following Powell’s “dovish” Jackson Hole speech.

Homeownership Losing Edge To Renting

Owning a home is generally viewed as a better deal than renting, but in cities with exploding home prices and relatively flat rents, that may not be the case anymore.

According to Trulia, it now makes more financial sense to rent than buy in the nation’s two most expensive markets — San Jose and San Francisco. The balance is also shifting in favor of renting in a few other high-cost cities, such as Honolulu, Seattle and Portland, Oregon, according to a recent study by the San Francisco-based company.

Trulia said the overall U.S. market still solidly provides buyers with a financial benefit. But in the five years since Trulia began estimating the financial advantages of buying versus renting, this is the first time renters have come out ahead in any of the major metros it tracks.

In San Jose and San Francisco, renting was 12 percent and 6 percent cheaper, respectively, for the consumer than buying a home, Trulia said. San Francisco and San Jose are outliers, though. The National Association of Realtors, for example, has estimated that for a person earning $100,000, just 2.5 percent of the June listings in San Jose and 9 percent in San Francisco were affordable. Trulia reported that buyers still have a significant advantage over renters in places like Detroit.

Trulia estimated that on a nationwide basis, buying a home was 26 percent cheaper for a consumer than renting as of last month. This is the narrowest gap in five years, and has come down from 41 percent in 2016, according to Trulia. The key factor in closing the gap is that house prices have increased steeply along with mortgage rates, while rents are remaining relatively stable. In San Jose, for example, home prices have jumped up 29 percent in a year, while rents were unchanged. Home values rose 14 percent in San Francisco, and rents fell by 3 percent.

“There are a lot of factors,” Trulia’s Senior Economist Cheryl Young said during an interview on Thursday. “Obviously, mortgage rates are going up. That is going to tip the scales a little bit toward renting, but also home value appreciation is far outpacing rent growth right now. So, rents are pretty much cooling out. As they cool down and home prices track up, that margin between buying and renting starts closing.”

Young said the balance could tip in favor of renters in other cities as well.

“There are markets that are always close to that margin, and things that could tip it,” she said. “If mortgage rates were to rise and we still see rents flattening and even decreasing as they have been in some places relative to rising home prices, we may see some markets tip.”

Trulia’s calculations include forecasts on future rent and price appreciation, and also estimates on how much a renter can potentially earn by investing in other vehicles. Trulia assumes that the buyer will stay in the home for seven years, put 20 percent down on a 30-year fixed mortgage.

Other housing analysts told Scotsman Guide News that gauging the advantages of buying versus renting can be a tricky exercise.

“The housing market doesn’t necessarily favor either one right now, as the choice of whether to be an owner or the renter is not a purely economic decision, but often includes the lifestyle decisions of an individual,” said Mark Fleming, chief economist for First American Corp.

Fleming also noted that in some of these high-cost cities, renters are in better position now to buy than when home prices were near their low point seven years ago.

“While housing prices are on the rise across the country, by historical standards they are still within reach in many markets,” Fleming said. “In fact, when you account for the historically low interest rate environment and rising incomes, consumer house-buying power is up nearly 24 percent since 2011,” he added.

Len Kiefer, deputy chief economist for Freddie Mac, said that rising home values tend to give the buyer a financial edge over the renter, who is gaining no equity.

“Certainly if we look back historically, homeowners have done pretty well relative to renters,” Kiefer said. “It doesn’t mean that it is going to be true in the future, but if you look at where our forecast is for the overall economy, we are still forecasting home prices to continue to rise at a pretty healthy pace over the next couple of years.”

Kiefer said in a few high-cost cities with high property taxes, homeowners will be hurt by new tax changes that eliminated or reduced homeownership perks in the federal tax code. This may give renters some advantage. He said the tax changes so far don’t seem to have reduced homebuyer demand significantly, though.

“Certainly in the high-cost, high-tax markets, places like parts of California, New Jersey, Illinois, the cost of homeownership is going to be a little bit negative,” Kiefer said. “But if we look at actual data on what has happened in those markets, it is hard to see a discernible impact in terms of slower overall activity that you could attribute to the tax law,” he said. Kiefer said rising prices and higher rates were likely making homebuying less appealing, however.

Renters have been less sold on the financial benefits of owning a home, according to recent Fannie Mae surveys. In January 2010, for example, 76 percent of surveyed renters saw an advantage in buying. That number has fallen to 68 percent as of the end of June.

“Renters’ view of the financial benefit of owning has come down a little bit,” said Mark Palim, deputy chief economist for Fannie Mae. “That probably reflects that home prices are up substantially.”

Palim said that renters are still expressing a strong desire in buying homes for non-financial, quality-of-life factors. He said the improved economy and a surge in household formation has kept the buyer demand up in spite of rising home prices and rates.

“Millennials have really moved into the market in a big way, and they are closing the gap relative to other generations,” Palim said. “People have far more financial means to afford a home and go out and buy a home, and that has translated into pretty brisk demand.”

New York Rents Plunge 12% In Queens

66-22 to 66-44 Forest Avenue

66-22 to 66-44 Forest Avenue

Today in “free-market capitalism actually benefits consumers” news, rents are being slashed across the board in Queens as landlords make concessions to deal with a supply glut and keep tenants renting. This lowering of rents taking place in Queens – to the tune of 12% YOY – was reported on by Bloomberg on Thursday morning:

For New York City apartment hunters, April was another good month to find a deal on rents. But no one fared better than those in northwest Queens.

Rents there dropped 12 percent from a year earlier, to a median of $2,646 a month after landlord giveaways were subtracted, according to a report Thursday by appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate. Those giveaways were offered on 65 percent of all new leases signed in the area, excluding renewals, a record share in data going back to the beginning of 2016.

The result from the price deflation that our Fed pins as the devil incarnate? More renters, more business and higher quality tenants:

The enticements brought in more renters. New leases in northwest Queens — Long Island City, Astoria, Sunnyside and Woodside — jumped 11 percent to 272, the firms said.

“More customers who were originally looking in Manhattan and Brooklyn are considering Queens,” said Hal Gavzie, Douglas Elliman’s executive manager of leasing. “It used to be just 100 percent a different consumer.”

New York City tenants are crossing borders to compare deals in a market groaning under the weight of new supply. Landlords, who’ve accepted they need to compete to keep their units filled, are working to attract new tenants and offering sweeter renewal terms to keep the ones they have, Gavzie said.

Who knew this could happen to industries and sectors where the government is not subsidizing or interfering with the pricing – and where free market capitalism is actually, in some facet, allowed to run its course?

The consumer now has the control because the concessions landlords are making are benefiting the them. Bloomberg continued:

In Manhattan, 44 percent of all new leases came with a landlord concession, such as a free month of rent or payment of broker fees. In Brooklyn, the share was 51 percent, a record for the borough.

Still, the number of new leases in Manhattan and Brooklyn fell 3.5 percent and 1.6 percent, respectively, a sign that renters there found good reason to stay in their current apartments, Gavzie said.

“Tenants negotiating a renewal, they’ve looked around to see what deals they can get,” he said. “So their landlord gives them a sweet offer to stay.”

Manhattan rents in April, after subtracting concessions, fell 2.2 percent, to a median of $3,236, the fifth consecutive month of year-over-year declines. In Brooklyn, where rents have also fallen for five months, the decline was 2.9 percent, to a median of $2,686.

This comes just about one month after we reported about downtown Manhattan basically turning into a ghost town due to just the opposite – prices rising and government overreach. Pricing out of tenants in some main downtown areas and shopping districts have caused vacancies in areas that have been occupied for decades.

The Fed loves to repeat how necessary and vital inflation is for economic prosperity, but in the case of midtown Manhattan’s “prime” retail real estate, it is doing nothing but helping cause once extremely prominent shopping areas become the very same “ghost towns” they turned into during the 2008 housing crisis.

Mayor DeBlasio’s asinine solution to this issue created in part by faulty government policy: more government and more regulation.

So much for the recovery.

As if brick and mortar retail didn’t have enough problems to deal with being methodically decimated by the ever growing behemoth that is Amazon, store owners are now facing rent that is simply so high it makes it impossible for most to open retail stores and do business in once prominent areas of downtown Manhattan.

Last month, the New York Post wrote an article confirming our writeup from late March suggesting that high prices are driving businesses out of town:

If you want to see the future of storefront retailing, walk nine blocks along Broadway from 57th to 48th Street and count the stores.

The total number comes to precisely one — a tiny shop to buy drones.

That’s right: On a nine-block stretch of what’s arguably the world’s most famous avenue, steps south of the bustling Time Warner Center and the planned new Nordstrom department store, lies a shopping wasteland.

To be sure, none of this comes as a surprise to us – or our regular readers – because in late March we recalled our own 2009 tour of Madison Avenue to discover that it also had turned into a ghost town. Just a week ago we told our readers that the ghost town that was New York’s “Golden Mile” was not surprising: after all the US economy had just been hit with the worst recession since the Great Depression, and only an emergency liquidity injection of trillions of dollars prevented a global financial collapse.

What is more surprising is why nearly 9 years later, at a time of what is supposed to be a coordinated global recovery, a walk along Madison Avenue reveals the exact same picture.

We would love for these two sets of facts to bludgeon the government and regulators over the head and make them realize that inflation isn’t the solution. Rather, they should realize from this that deflation can actually be a reward for capitalism, causing prices to fall, increased competition between sellers, and benefits for buyers.

Rent: Santa Monica Tops New York & Silicon Valley

Now referred to as “Silicon Beach,” Santa Monica’s rent rates for a one-bedroom apartment are approaching $5,000 per month.

According to the Apartment Guide, the average monthly rent for a one-bedroom in Santa Monica is the most expensive in the nation, at $4,799.20. Comparable rents in the local area are $3,922.67 in Venice; $3,780 in Playa Vista; and $3,320.67 in Marina del Rey.

New York is now the second-most expensive market, with an average one-bedroom apartment costing $4,562.72 per month. San Francisco, once the highest cost market, has fallen to an average $3,880.44 per month. New tech companies, including Snap, Inc., are drawing wealthy young professionals to the area.

Breitbart News has chronicled how apartment rental prices in New York City and Silicon Valley have fallenn about 8 percent, due to a glut of luxury unit construction. But the effective rent rates are down substantially more, because developers are giving multiple month rent concessions “to get heads in beds as quickly as possible,” according to Alexander Goldfarb, a San Francisco analyst with Sandler O’Neill + Partners.

In San Francisco’s trendy South of Market neighborhood, referred to as SoMa, four new high-rise apartment buildings are also offering super high-end amenities that include rooftop decks, state-of-the-art gyms and bike rooms. But despite free rent and nicer digs, none of the four buildings that opened in the last 18 months has achieved the 90 percent occupancy rate that developers need to flip their short-term high-interest rate development loans into low-rate long-term “take-out” financing.

Rent.com and the Apartmentguide.com websites predict that high rental prices should stay strong due to L.A.s’ median home price rising 348.1 percent in the last 30 years, from $116,061 to $520,000. The price jump was an even higher 349.3 percent in Orange County, where the price jumped from $143,210 to $643,483.

But according to mortgage banker Bruce Lawrence, the “term” period for construction loans is usually limited to 36 months, and the cost of that type of financing is at least twice the interest rate of 30-year “take-out financing.” Although the default rate for long-term apartment loans has been a tiny .01 percent, he believes that has been due to a “chronic lack of apartment supply,” which supply is beginning to overwhelm.

In the quarter ending December 31, 2016, Lawrence observed that a record 50,000 new apartment units in the U.S. were rented by tenants, or about six times the number in the year-earlier period. But new apartments completed and renting during the quarter hit 88,000, the highest number since the 1980s.

Looking forward, Lawrence believes that at least 378,000 new apartment units will be completed and start renting in 2017. With construction financing in place, he expects there will be no slowdown in building. Lawrence projects that by mid-year 2017, the U.S. will have a national glut of 100,000 new apartments, and in two years that number could be over 300,000. At that point, Lawrence sees rent “getting whacked.”

Bruce Lawrence comments that Santa Monica is a special case for high rents, because the city adopted rent control three decades ago. But with no limit on the rents for new units, California’s state bird is now the “construction crane.”

Rents Set To Keep Rising After Latest Multi-family Starts & Permits Report

Unlike recent months when the Census Bureau reported some fireworks in the New Housing Starts and Permits data, the April update was relatively tame, and saw Starts rise from an upward revised 1,099K to 1,172K, beating expectations of a 1,125K print, mostly as a result of a 36K increase in multi-family units which however remain depressed below recent peaks from early 2015, which will likely stoke even higher asking rents, already at record highs across the nation.

Unlike recent months when the Census Bureau reported some fireworks in the New Housing Starts and Permits data, the April update was relatively tame, and saw Starts rise from an upward revised 1,099K to 1,172K, beating expectations of a 1,125K print, mostly as a result of a 36K increase in multi-family units which however remain depressed below recent peaks from early 2015, which will likely stoke even higher asking rents, already at record highs across the nation.

But if starts were better than expected, then the future pipeline in the form of Housing Permits disappointed, with 1,116K units permitted for the month of April, below the 1,135K expected, if a rebound from last month’s downward revised 1,077K.

The issue, as with the starts data, is the multi-family, aka rental units, barely rebounded and remained at severely depressed levels last seen in 2013: at 348K rental units permitted in April, this is a far cry from the recent highs of 598K in June.

One wonders if this is intentional, because based on soaring asking rents, as shown in the chart below, with Americans increasingly unable or unwilling to buy single-family units, rental prices have exploded to 8% Y/Y based on Census data.

Should multi-family permits and starts remain as depressed as it has been in recent months, we expect that this chart of soaring median asking rents will only accelerate in the near future, and will require a whole host of seasonal adjustments from making its way into the already bubbly CPI data.

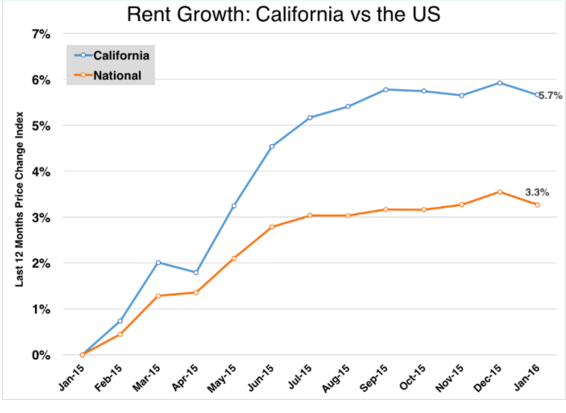

California Renter Apocalypse

The rise in rents and home prices is adding additional pressure to the bottom line of most California families. Home prices have been rising steadily for a few years largely driven by low inventory, little construction thanks to NIMBYism, and foreign money flowing into certain markets. But even areas that don’t have foreign demand are seeing prices jump all the while household incomes are stagnant. Yet that growth has hit a wall in 2016, largely because of financial turmoil. We’ve seen a big jump in the financial markets from 2009. Those big investor bets on real estate are paying off as rents continue to move up. For a place like California where net home ownership has fallen in the last decade, a growing list of new renter households is a good thing so long as you own a rental.

The rise in rents and home prices is adding additional pressure to the bottom line of most California families. Home prices have been rising steadily for a few years largely driven by low inventory, little construction thanks to NIMBYism, and foreign money flowing into certain markets. But even areas that don’t have foreign demand are seeing prices jump all the while household incomes are stagnant. Yet that growth has hit a wall in 2016, largely because of financial turmoil. We’ve seen a big jump in the financial markets from 2009. Those big investor bets on real estate are paying off as rents continue to move up. For a place like California where net home ownership has fallen in the last decade, a growing list of new renter households is a good thing so long as you own a rental.

The problem of course is that household incomes are not moving up and more money is being siphoned off into an unproductive asset class, a house. Let us look at the changing dynamics in California households.

More renters

Many people would like to buy but simply cannot because their wages do not justify current prices for glorious crap shacks. In San Francisco even high paid tech workers can’t afford to pay $1.2 million for your typical Barbie house in a rundown neighborhood. So with little inventory investors and foreign money shift the price momentum. With the stock market moving up nonstop from 2009 there was plenty of wealth injected back into real estate. The last few months are showing cracks in that foundation.

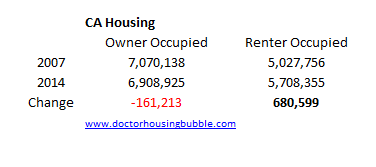

It is still easy to get a mortgage if you have the income to back it up. You now see the resurrection of no money down mortgages. In the end however the number of renter households is up in a big way in California and home ownership is down:

Source: Census

So what we see is that since 2007 we’ve added more than 680,000 renter households but have lost 161,000 owner occupied households. At the same time the population is increasing. When it comes to raw numbers, people are opting to rent for whatever reason. Also, just because the population increases doesn’t mean people are adding new renter households. You have 2.3 million grown adults living at home with mom and dad enjoying Taco Tuesdays in their old room filled with Nirvana and Dr. Dre posters.

And yes, with little construction and unable to buy, many are renting and rents have jumped up in a big way in 2015:

Source: Apartmentlist.com

This has slowed down dramatically in 2016. It is hard to envision this pace going on if a reversal in the economy hits (which it always does as the business cycle does its usual thing).

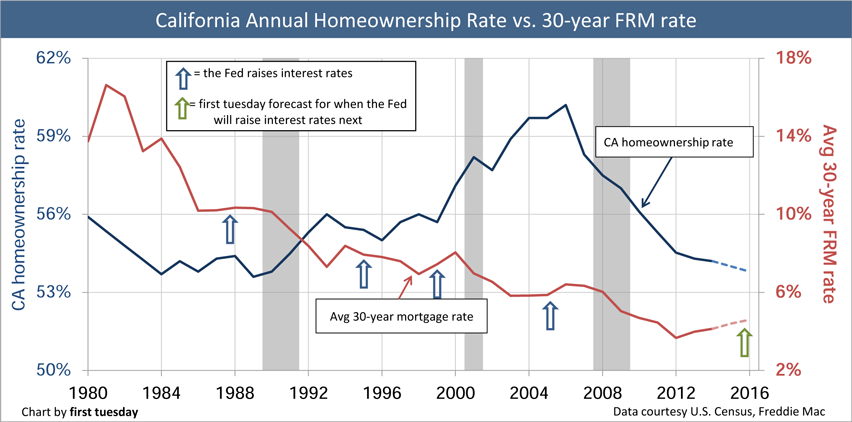

Home ownership rate in a steep decline

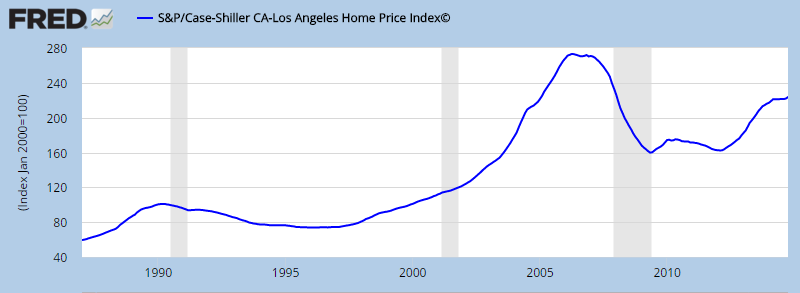

In the LA/OC area home prices are up 37 percent in the last three years:

Of course there are no accompanying income gains. If you look at the stock market, the unemployment rate, and real estate values you would expect the public to be happy this 2016 election year. To the contrary, outlier momentum is massive because people realize the system is rigged and are trying to fight back. Watch the Big Short for a trip down memory lane and you’ll realize nothing has really changed since then. The house humping pundits think they found some new secret here. It is timing like buying Apple or Amazon stock at the right time. What I’ve seen is that many that bought no longer can afford their property in a matter of 3 years! Some shop at the dollar store while the new buyers are either foreign money or dual income DINKs (which will take a big hit to their income once those kids start popping out). $2,000 a month per kid daycare in the Bay Area is common.

If this was such a simple decision then the home ownership rate would be soaring. Yet the home ownership rate is doing this:

In the end a $700,000 crap shack is still a crap shack. That $1.2 million piece of junk in San Francisco is still junk. And you better make sure you can carry that housing nut for 30 years. For tech workers, mobility is key so renting serves more as an option on housing versus renting the place from the bank for 30 years. Make no mistake, in most of the US buying a home makes total sense. In California, the massive drop in the home ownership rate shows a different story. And that story is the middle class is disappearing.

Hooray! Huge Rent Hikes Coming

In news that is bound to make the inflationists at the Fed as well as property owners happy, Landlords Will Hike Rents by 8% this Year.

Some 88% of property managers raised their rent in the last 12 months and 68% predict that rental rates will continue to rise in the next year by an average of 8%, according to a survey of more than 500 of Rent.com’s property management customers, which the site says represents thousands of rental properties and hundreds of thousands of rental units. That’s nearly three times the wage increase that most employees can expect this year.

What’s more, 55% of property managers said that they are less likely to offer concessions or lower rents in order to fill vacancies. One reason why they’re getting even tougher: They are in a stronger position than they were this time last year.

More than 46% of property managers surveyed reported a decrease in rental vacancies in Rent.com’s survey and, in the second quarter of 2015, vacancy rates in the U.S. for rental housing was 6.8%, the lowest it has been in almost 20 years, according to data from the U.S. Census Bureau.

Despite this, many renters are spending more than 30% of their income on rent (the amount generally recommended) and need help qualifying for the lease.

Yardi Survey

Mish reader “BJ” is retired but works part-time a number of hours each week, surveying apartments for rent. He reports …

I am retired but work part-time for Yardi from my home, surveying apartments for rents. Yardi runs a full survey 3 times a year, Jan, May and Sept. These generally run about 6 weeks.

Yardi has the country divided into 24 sectors and we normally work 6-7 sectors once a month for a week on a rotating basis. Toward the end of the survey, we can work any market and I’ve been keeping track of a few select places. From what I see, rents are up and up a lot. Some of the places I watch are up 7% or more than last year for the same apartments.

The absolute worst places to be looking for a rental unit are San Fran and North LA. If anyone does answer the phone in those areas, it’s either a new building just opening, or they don’t have anything. You can’t even get on a waiting list. I’ve seen apartments in tight areas where they want you to make 3X net before they will talk to you.

Portland, Seattle, Washington DC, northern NJ, Miami and Boston are also difficult. I talked to a complex in Portland last week that had 3500 apartments under management with a total of 7 open apartments.

I am amazed by the amount of apartments that are either tax credit or subsidized in some manner. All of them have long waiting lists.

Measuring Housing Inflation

The Fed wants inflation. But how do they measure it?

Rents Have Been Skyrocketing In These 13 US Cities

Seven years ago, the American home ownership “dream” was shattered when a housing bubble built on a decisively shaky foundation burst in spectacular fashion, bringing Wall Street and Main Street to their knees.

In the blink of an eye, the seemingly inexorable rise in the American home ownership rate abruptly reversed course, and by 2014, two decades of gains had disappeared and the ashes of Bill Clinton’s National Home ownership Strategy lay smoldering in the aftermath of the greatest financial collapse since the Great Depression.

In short, decades of speculative excess driven by imprudence, greed, and financial engineering and financed by the world’s demand for GSE debt had come crashing down and in relatively short order, a nation of homeowners was transformed into a nation of renters.

It wasn’t difficult to predict what would happen next.

As demand for rentals increased and PE snapped up foreclosures, rents rose, just as a subpar jobs market, a meteoric rise in student debt, tougher lending standards, and critically important demographic shifts put further pressure on home ownership rates. Now, America faces a rather dire housing predicament: buying and renting are both unaffordable. Or, as WSJ put it last month, “households are stuck between homes they can’t qualify for and rents they can’t afford.”

We’ve seen evidence of this across the country with perhaps the most telling statistic coming courtesy of The National Low Income Housing Coalition who recently noted that in no state can a minimum wage worker afford a one bedroom apartment.

In this context, Bloomberg is out with a list of 13 cities where single-family rents have risen by double-digits in just the last 12 months. Note that in Iowa, rents have risen more than 20% over the past year alone.

More color from Bloomberg:

More color from Bloomberg:

Landlords have been preparing to raise rents on single-family homes this year, Bloomberg reported in April. It looks like those plans are already being put into action.

The median rent for a three-bedroom single-family house increased 3.3 percent, to $1,320, during the second quarter, according to data compiled by RentRange and provided to Bloomberg by franchiser Real Property Management. Median rents are up 6.1 percent over the past 12 months. Even that kind of increase would have been welcome in 13 U.S. cities where single-family rents increased by double digits.

It’s more evidence that rising rents have affected a broad scope of Americans. Sixty percent of low-income renters spend more than 50 percent of their income on rent, according to a report in May from New York University’s Furman Center. High rents have also stretched the budgets of middle-class workers and made it harder for young professionals to launch careers and start families.

“You’re finding that people who wouldn’t have shared accommodations in the past are moving in with friends,”says Don Lawby, president of Real Property Management. “Kids are staying in their parents’ homes for longer and delaying the formation of families.”

And for those with short memories, we thought this would be an opportune time to remind you of who became America’s landlord in the wake of the crisis…

You must be logged in to post a comment.