Unlike in the 2008 financial crisis when a glut of subprime debt, layered with trillions in CDOs and CDO squareds, sent home prices to stratospheric levels before everything crashed scarring an entire generation of home buyers, this time the housing sector is facing a far more conventional problem: the sudden and unpredictable inability of mortgage borrowers to make their scheduled monthly payments as the entire economy grinds to a halt due to the coronavirus pandemic.

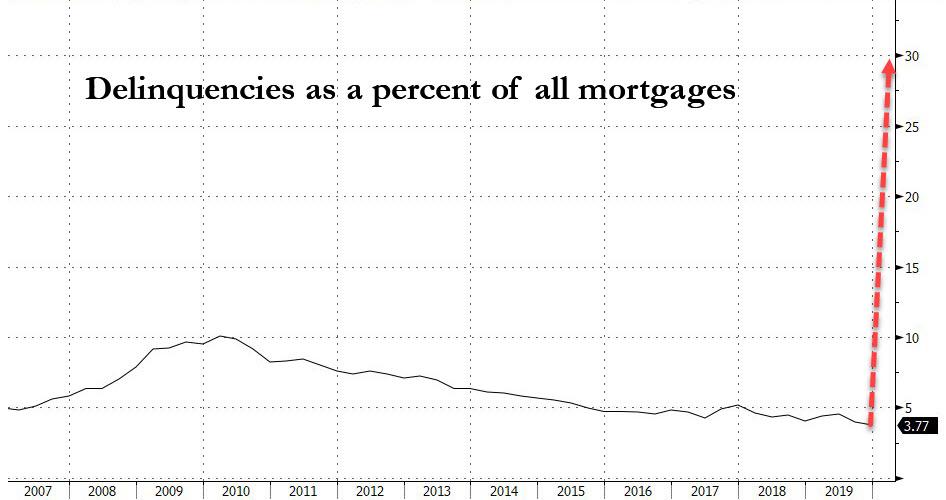

And unfortunately this time the crisis will be far worse, because as Bloomberg reports mortgage lenders are preparing for the biggest wave of delinquencies in history. And unless the plan to buy time works – and as we reported earlier there is a distinct possibility the Treasury’s plan to provide much needed liquidity to America’s small businesses may be on the verge of collapse – an even worse crisis may be coming: mass foreclosures and mortgage market mayhem.

Borrowers who lost income from the coronavirus, which is already a skyrocketing number as the 10 million new jobless claims in the past two weeks attests, can ask to skip payments for as many as 180 days at a time on federally backed mortgages, and avoid penalties and a hit to their credit scores. But as Bloomberg notes, it’s not a payment holiday and eventually homeowners they’ll have to make it all up.

According to estimates by Moody’s Analytics chief economist Mark Zandi, as many as 30% of Americans with home loans – about 15 million households – could stop paying if the U.S. economy remains closed through the summer or beyond.

“This is an unprecedented event,” said Susan Wachter, professor of real estate and finance at the Wharton School of the University of Pennsylvania. She also points out another way the current crisis is different from the 2008 GFC: “The great financial crisis happened over a number of years. This is happening in a matter of months – a matter of weeks.”

Meanwhile lenders – like everyone else – are operating in the dark, with no way of predicting the scope or duration of the pandemic or the damage it will wreak on the economy. If the virus recedes soon and the economy roars back to life, then the plan will help borrowers get back on track quickly. But the greater the fallout, the harder and more expensive it will be to stave off repossessions.

“Nobody has any sense of how long this might last,” said Andrew Jakabovics, a former Department of Housing and Urban Development senior policy adviser who is now at Enterprise Community Partners, a nonprofit affordable housing group. “The forbearance program allows everybody to press pause on their current circumstances and take a deep breath. Then we can look at what the world might look like in six or 12 months from now and plan for that.”

But if the economic turmoil is long-lasting, the government will have to find a way to prevent foreclosures – which could mean forgiving some debt, said Tendayi Kapfidze, Chief Economist at LendingTree. And with the government now stuck in “bailout everyone mode”, the risk of allowing foreclosures to spiral is just too great because it would damage financial markets and that could reinfect the economy, he explained.

“I expect policy makers to do whatever they can to hold the line on a financial crisis,” Kapfidze said hinting at just a trace of a conflict of interest as his firm may well be next to fold if its borrowers declare a payment moratorium. “And that means preventing foreclosures by any means necessary.”

“I don’t know how I’m going to pay my mortgage and my condo dues and still be able to feed myself,” Habberstad said. “I just hope that, once things open up again, we who are impacted by Covid-19 are given consideration and sufficient time to bring all payments current without penalty and in a manner that does not bring us even more financial hardship.”

Borrowers must contact their lenders to get help and avoid black marks on their credit reports, according to provisions in the stimulus package passed by Congress last week. Bank of America said it has so far allowed 50,000 mortgage customers to defer payments. That includes loans that are not federally backed, so they aren’t covered by the government’s program.

Meanwhile, Treasury Secretary Steven Mnuchin has convened a task force to deal with the potential liquidity shortfall faced by mortgage servicers, which collect payments and are required to compensate bondholders even if homeowners miss them. The group was supposed to make recommendations by March 30.

“If a large percentage of the servicing book – let’s say 20-30% of clients you take care of – don’t have the ability to make a payment for six months, most servicers will not have the capital needed to cover those payments,” QuickenChief Executive Officer Jay Farner said in an interview. But not Quicken, of course.

Quicken, which serves 1.8 million borrowers, and in 2018 surpassed Wells Fargo as the #1 mortgage lender in the US, has a strong enough balance sheet to serve its borrowers while paying holders of bonds backed by its mortgages, Farner said, although something tells us that in 6-8 weeks his view will change dramatically. Until then, the company plans to almost triple its call center workers by May to field the expected onslaught of borrowers seeking support, he said.

Ironically, as Bloomberg concludes, “if the pandemic has taught us anything, it’s how quickly everything can change. Just weeks ago, mortgage lenders were predicting the biggest spring in years for home sales and mortgage refinances.”

Habberstad, the bar manager, was staffing up for big crowds at the beer garden, which is across from National Park, home of the World Series champions. Then came coronavirus. Now, she’s dependent on her unemployment check of $440 a week.

“Everybody wants to work but we’re being asked not to for the sake of the greater good,” she said.