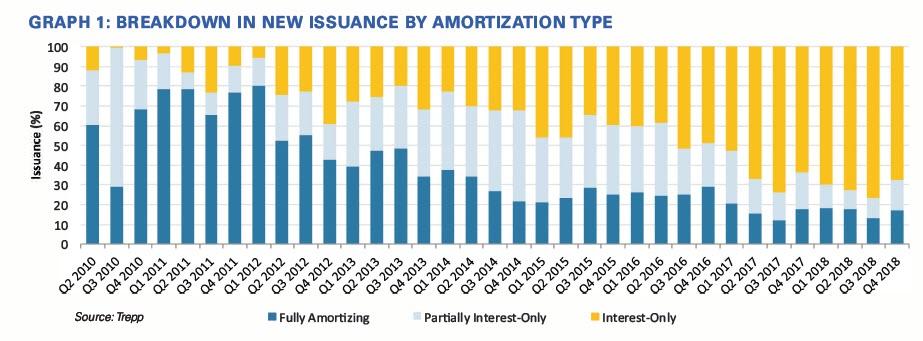

A larger volume of CMBS loans are being issued with interest-only (IO) structures, but this rise may put the CMBS market in a dicey position when the economy reaches its next downturn. To put things in perspective, interest-only loan issuance reached $19.5 billion in Q3 2018, six times greater than fully amortizing loan issuance. In comparison, nearly 80% of all CMBS issued in the FY 2006 and FY 2007 was either interest-only or partially interest-only loans.

In theory, the popularity of interest-only loans makes sense, because they provide lower debt service payments and free up cash flow for borrowers. But these benefits are partially offset by some additional risks in the interest-only structure, with the borrower’s inability to deleverage during the loan’s life perhaps being the biggest concern. Additionally, borrowers who opt for a partial interest-only structure incur a built-in “payment shock” when the payments switch from interest-only to principal and interest.

Why are we seeing a spike in interest-only issuance if the loans are inherently riskier than fully amortizing loans? Commercial real estate values are at all-time highs; interest rates are still historically low; expectations for future economic and rent growth are fundamentally sound, and competition for loans on stabilized, income-producing properties is higher than ever. Furthermore, the refinancing pipeline is miniscule compared to the 2015-2017Wall of Maturities, so more capital is chasing fewer deals. This causes lenders to augment loan proceeds and loosen underwriting parameters, including offering more interest-only deals.

Then and Now: Why the Rise in 10 Debt Has Raised Concerns

Between Q1 2010 and Q1 2012, fully amortizing loans dominated new issuance, with its market share amassing as much as 80.4% (Q1 2012). Interest-only issuance was nearly equal to the fully amortizing tally by Q3 2012, as interest-only debt totaled $5.10 billion, only $510 million less than fully amortized loans. Interest-only issuance would soon overtake fully amortizing loan issuance by Q2 2017, as its volume skyrocketed from $5.3 billion in Q1 2017 to $19.5 billion in Q3 2018.

Prior to the 2008 recession, the CMBS market experienced a similar upward trend in interest-only issuance. By 02 2006, interest-only loans represented 57.6% of new issuance, outpacing fully amortizing notes by 38.86%. The difference in issuance between interest-only and fully amortizing loans continued to widen as the market approached the recession, eventually reaching a point where interest-only debt represented 78.8% of new issuance in 01 2007. Even though the prevalence of interest-only debt is mounting, why would this be a concern in today’s market?

IO Loans Are More Likely to Become Delinquent

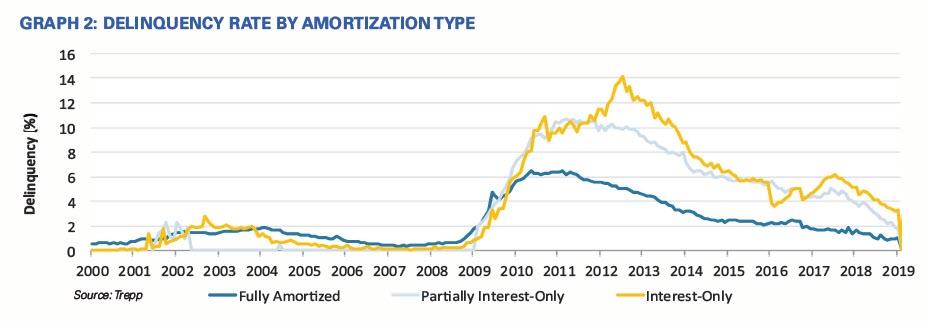

Interest-only loans have historically been more susceptible to delinquency when the economy falters. Immediately following the recession, delinquency rates across all CMBS loans moved upward. Once the economy began to show signs of recovery, the delinquency rate for fully amortized loans began to decline, while interest-only and partially interest-only delinquencies continued to rise. In July 2012, the delinquency rate for fully amortizing loans was sitting at 5.07% while the interest-only reading reached 14.15%. The outsized delinquency rate for interest-only loans during this time period is not surprising, since many of the five-year and seven-year loans originated in the years prior to the recession were maturing. Many of the borrowers were unable to meet their payments due to significant declines in property prices paired with loan balances that had never amortized.

Over time, the stabilization of the CMBS market led to subsequent declines in the delinquency rates for both the interest-only and partial interest-only sectors. The delinquency rate for interest-only loans clocked in at 3.17% in December 2018, which is down nearly 11 % from its peak. Delinquency rates across all amortization types have failed to return to pre-crisis levels.

Just because a large chunk of interest-only debt became delinquent during the previous recession does not mean the same is destined to happen in the next downturn.

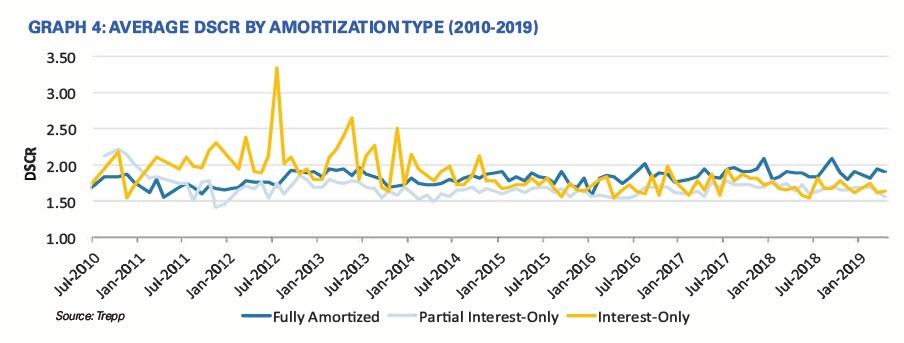

Measuring the likelihood of a loan turning delinquent is typically done by calculating its debt-service coverage ratio (DSCR). Between 2010 and 2015, the average DSCR across all interest-only loans was a relatively high 1.94x. Since 2016, the average DSCR for interest-only debt has fallen slightly. If the average DSCR for interest-only loans continues to decline, the inherent risk those loans pose to the CMBS market will become more concerning.

The average DSCR for newly issued interest-only loans in March 2019 registered at 1.61 x, which is about 0.35x higher than the minimum DSCR recommended by the Commercial Real Estate Finance Council (CREFC). In 2015, CREFC released a study analyzing the impact of prudential and securities regulation across the CRE finance sector. In the study, CREFC cited a 1.25x-DSCR as the cutoff point between relatively healthy and unhealthy loans. The value was chosen through loan-level analysis and anecdotal information from conversations with members.

The figure below maps the DSCR for both fully amortizing and interest-only loans issued between 2004 and 2008. Notice that toward the end of 2006, the average DSCR hugged the 1.25x cutoff level recommended by CREFC. Beyond 2006, the average DSCR for interest-only loans oscillated between healthy and concerning levels.

The second figure focuses on CMBS 2.0 loans, where a similar trend can be spotted. After roughly converting interes-tonly loan DSCRs to amortizing DSCRs using underwritten NOI levels and assuming 30-year amortization, the average DSCR for interest-only loans issued between 2010 and mid- 2014 (2.04x) is much greater than that for fully amortizing issuance (1.78x). While part of this trend can be attributed to looser underwriting standards and/or growing competition, the other driver of the trend is due to selection bias. Lenders will typically give interest-only loans to stronger properties and require amortization from weaker properties, so it makes sense that they would also require less P&I coverage for those interest-only loans on lower-risk properties.

What Lies Ahead for the IO Sector?

Rising interest-only loan issuance paired with a drop in average DSCR may spell for a messy future for the CMBS industry if the US economy encounters another recession. At this point, CMBS market participants can breath a little easier since interest-only performance has remained above the market standard. However, this trend is worth monitoring as the larger volume could portend a loosening in underwriting standards.