That criticism takes two forms — one, Fed officials say evidence doesn’t show much effectiveness where they have been tried, and two, negative interest rates might throw markets, such as those for money markets, into turmoil.

But don’t get your hopes up for negative mortgage rates. At best, 30-year mortgage rates will shadow the already low 10-year Treasury yield. It really depends on how the 10-year Treasury yield responds.

To put the -0.5% rate in simple terms: If you bought a house for $1 million and paid off your mortgage in full in 10 years, you would pay the bank back only $995,000.

It should be noted that even with a negative interest rate, banks often charge fees linked to the borrowing, which means homeowners could still pay back more.

“It’s another chapter in the history of the mortgage,” the Jyske Bank housing economist Mikkel Høegh told Danish TV,according to the news website Copenhagen Post. “A few months ago, we would have said that this would not be possible, but we have been surprised time and time again, and this opens up a new opportunity for homeowners.”

Jyske Bank’s negative rate is the latest in a series of extremely low interest offers from banks to Danish homeowners.

According to The Local,Nordea Bank, Scandinavia’s biggest lender, said it would offer a 20-year fixed-rate mortgage with 0% interest.Bloomberg reportedthat some Danish lenders were offering 30-year mortgages at a 0.5% rate.

It should also be noted that negative rates have been available on short-term mortgage bonds in Denmark since May,according to Bloomberg; they have only just been made directly available to consumers.

“It’s never been cheaper to borrow,” Lise Nytoft Bergmann, the chief analyst at Nordea’s home finance unit in Denmark, told Bloomberg.

It may seem counterintuitive for banks to lend out their money at such low rates — but there is a rationale behind it.

Financial markets are in a volatile, uncertain spot right now. Factors includethe US-China trade war, Brexit, and a generalized economic slowdown across the world — and particularly in Europe.

Many investors fear a substantial crash in the near future. As such, some banks are willing to lend money at negative rates, accepting a small loss rather than risking a bigger loss by lending money at higher rates that customers cannot meet.

“It’s an uncomfortable thought that there are investors who are willing to lend money for 30 years and get just 0.5% in return,” Bergmann said.

“It shows how scared investors are of the current situation in the financial markets, and that they expect it to take a very long time before things improve.”

This doesn’t mean borrowers are being paid to take mortgages.

Jyske Bank appears to describe in the attached press release that they add a 1% “variable contribution rate” + fees to a -0.5 negative “bond rate”, resulting in borrowers qualifying to pay a positive amortized rate over a maximum 10 year period, plus taxes and insurance, to 80% loan to value at closing.

Most home buyers are unable to qualify for a ten year mortgage with 20% down. This means the program is being targeted to existing equity rich homeowners interested in cash out mortgages.

Negative interest rates are little understood in the U.S., and this may lead to very expensive mistakes by many investors.

The move to negative interest rates can be extremely profitable – but investors have to be prepared before it happens or the opportunities will be gone.

Detailed analysis of how the Fed using trillions in quantitative easing to force negative interest rates can directly create hundreds of billions of dollars in profits for sophisticated insiders.

When we “follow the money”, quantitative easing in a new recession would use monetary creation to force artificially high prices and vastly overpay knowledgeable investors.

(Daniel Amerman) “Following the money” can be a good way of unraveling complexity. Sometimes what the technical jargon is covering up can be as simple as Insider A handing money over to Insider B in massive quantities – and when we understand that, our whole perspective can change.

In this analysis, we will explore how a potential future of negative interest rates in combination with quantitative easing could become one of the largest re-distributions of wealth in U.S. history, with hundreds of billions of dollars in profits going disproportionately to insiders – at the expense of the general public. As illustrated with a step by step example when we follow the money – $279 billion out of every $1 trillion in newly created money could end up going straight into the hands of organizations and individuals who make up a relatively small percentage of the nation.

If there is another recession, then the Federal Reserve intends to engage in what could become the largest round of monetary creation in U.S. history. Those dollars will be quite real, and the reason for their creation is to spend them. A big chunk of that spending will become profits going straight into the pockets of investors. This won’t actually be a closed game – anyone can try for a share of those new Federal Reserve dollars, but first, they have to understand that the game exists, and then they need to learn how it is played.

On Tuesday, Federal Reserve Chairman Jerome Powell, in his opening remarks at a monetary policy conference in Chicago, raised concerns about the rising trade tensions in the U.S.

The extremely negative environment that existed, particularly in the asset markets, provided a fertile starting point for monetary interventions.

Given rates are already negative in many parts of the world, which will likely be even more negative during a global recessionary environment, zero yields will still remain more attractive to foreign investors.

This idea was discussed in more depth with members of my private investing community,Real Investment Advice PRO.

(Lance Roberts) On Tuesday, Federal Reserve Chairman Jerome Powell, in his opening remarks at a monetary policy conference in Chicago, raised concerns about the rising trade tensions in the U.S.,

“We do not know how or when these issues will be resolved. As always, we will act as appropriate to sustain the expansion, with a strong labor market and inflation near our symmetric 2 percent objective.”

However, while there was nothing “new” in that comment, it was his following statement that sent “shorts” scrambling to cover.

“In short, the proximity of interest rates to the ELB has become the preeminent monetary policy challenge of our time, tainting all manner of issues with ELB risk and imbuing many old challenges with greater significance.

“Perhaps it is time to retire the term ‘unconventional’ when referring to tools that were used in the crisis. We know that tools like these are likely to be needed in some form in future ELB spells, which we hope will be rare.”

“To translate that statement, not only is the Fed ready to cut rates, but it may take ‘unconventional’ tools during the next recession, i.e., NIRP and even more QE.”

This is a very interesting statement considering that these tools, which were indeed unconventional“emergency” measures at the time, have now become standard operating procedure for the Fed.

Yet, these “policy tools” are still untested.

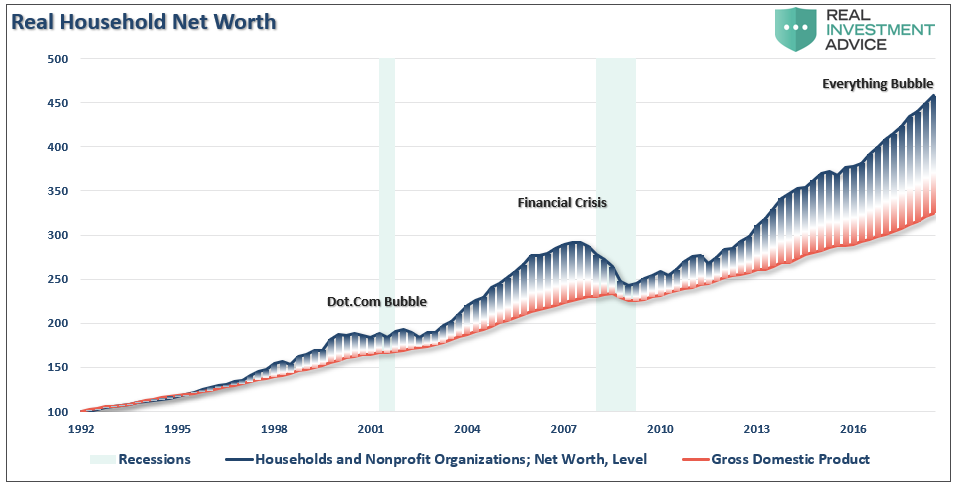

Clearly, QE worked well in lifting asset prices, but not so much for the economy. In other words, QE was ultimately a massive “wealth transfer” from the middle class to the rich which has created one of the greatest wealth gaps in the history of the U.S., not to mention an asset bubble of historic proportions.

However, they have yet to operate within the confines of an economic recession or a mean-reverting event in the financial markets. In simpler terms, no one knows for certain whether the bubbles created by monetary policies are infinitely sustainable? Or, what the consequences will be if they aren’t.

The other concern with restarting monetary policy at this stage of the financial cycle is the backdrop is not conducive for “emergency measures” to be effective. As we wrote in“QE, Then, Now, & Why It May Not Work:”

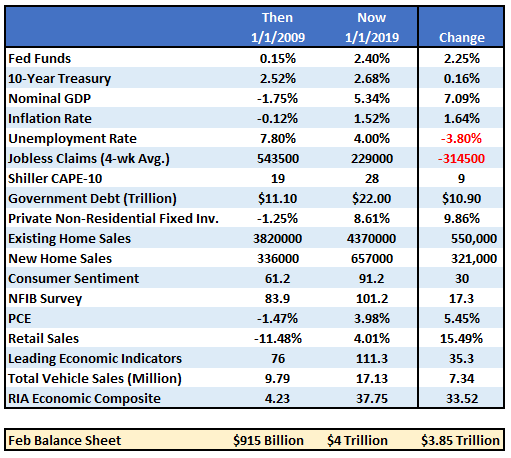

“If the market fell into a recession tomorrow, the Fed would be starting with roughly a $4 Trillion balance sheet with interest rates 2% lower than they were in 2009. In other words, the ability of the Fed to ‘bail out’ the markets today, is much more limited than it was in 2008.

But there is more to the story than just the Fed’s balance sheet and funds rate. The entire backdrop is completely reversed. The table below compares a variety of financial and economic factors from 2009 to present.

“The critical point here is that QE and rate reductions have the MOST effect when the economy, markets, and investors have been ‘blown out,’ deviations from the ‘norm’ are negatively extended, confidence is hugely negative.

In other words, there is nowhere to go but up.”

The extremely negative environment that existed, particularly in the asset markets, provided a fertile starting point for monetary interventions. Today, as shown in the table above, the economic and fundamental backdrop could not be more diametrically opposed.

This suggests that the Fed’s ability to stem the decline of the next recession, or offset a financial shock to the economy from falling asset prices, may be much more limited than the Fed, and most investors, currently believe.

While Powell is hinting at QE4, it likely will only be employed when rate reductions aren’t enough. Such was noted in 2016 by David Reifschneider, deputy director of the division of research and statistics for the Federal Reserve Board in Washington, D.C., released a staff working paper entitled“Gauging The Ability Of The FOMC To Respond To Future Recessions.”

The conclusion was simply this:

“Simulations of the FRB/US model of a severe recession suggest that large-scale asset purchases and forward guidance about the future path of the federal funds rate should be able to provide enough additional accommodation to fully compensate for a more limited [ability] to cut short-term interest rates in most, but probably not all, circumstances.”

In effect, Powell has become aware he has become caught in a liquidity trap. Without continued “emergency measures” the markets, and subsequently economic growth, cannot be sustained. This is where David compared three policy approaches to offset the next recession:

Fed funds goes into negative territory, but there is no breakdown in the structure of economic relationships.

Fed funds returns to zero and keeps it there long enough for unemployment to return to baseline.

Fed funds returns to zero and the FOMC augments it with additional $2-4 Trillion of QE and forward guidance.

This is exactly the prescription that Jerome Powell laid out on Tuesday, suggesting the Fed is already factoring in a scenario in which a shock to the economy leads to additional QE of either $2 trillion, or in a worst-case scenario, $4 trillion, effectively doubling the current size of the Fed’s balance sheet.

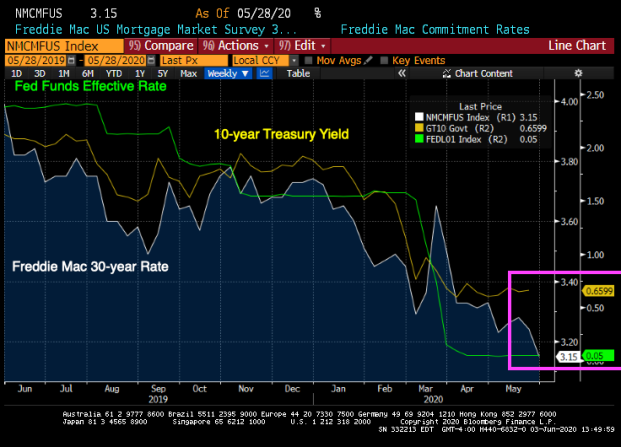

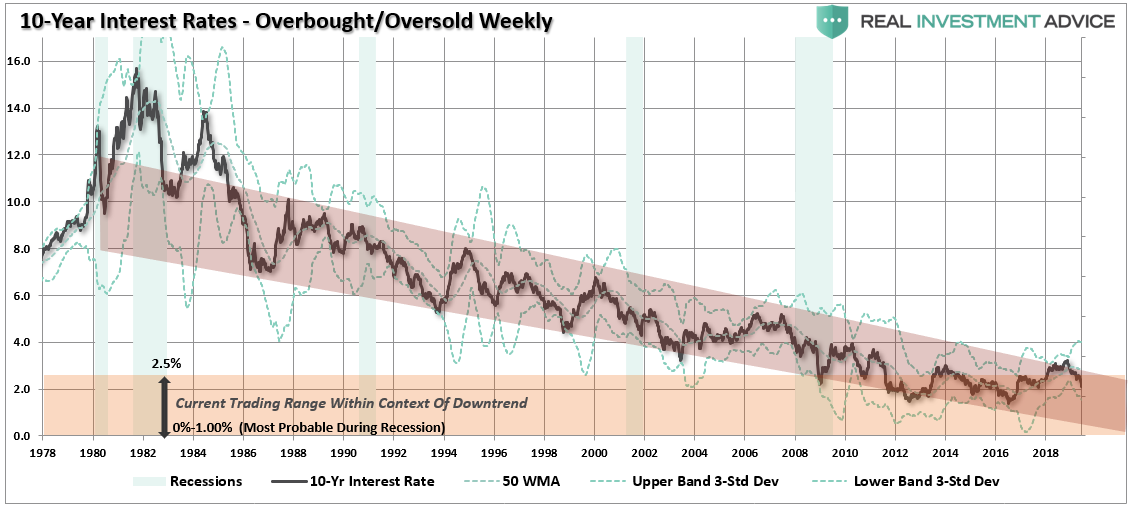

This is also why 10-year Treasury rates are going to ZERO.

“There is an assumption that because interest rates are low, that the bond bull market has come to its inevitable conclusion. The problem with this assumption is three-fold:

All interest rates are relative. With more than $10-Trillion in debt globally sporting negative interest rates, the assumption that rates in the U.S. are about to spike higher is likely wrong. Higher yields in U.S. debt attracts flows of capital from countries with negative yields which push rates lower in the U.S. Given the current push by Central Banks globally to suppress interest rates to keep nascent economic growth going, an eventual zero-yield on U.S. debt is not unrealistic.

The coming budget deficit balloon. Given the lack of fiscal policy controls in Washington, and promises of continued largesse in the future, the budget deficit is set to swell back to $1 Trillion or more in the coming years. This will require more government bond issuance to fund future expenditures which will be magnified during the next recessionary spat as tax revenue falls.

Central Banks will continue to be a buyer of bonds to maintain the current status quo, but will become more aggressive buyers during the next recession. The next QE program by the Fed to offset the next economic recession will likely be $2-4 Trillion which will push the 10-year yield towards zero.”

It’s item #3 that is most important.

In “Debt & Deficits: A Slow Motion Train Wreck”, I laid out the data constructs behind the points above.

However, it was in April 2016, when I stated that with more government spending, a budget deficit heading towards $1 Trillion, and real economic growth running well below expectations, the demand for bonds would continue to grow. Even from a purely technical perspective, the trend of interest rates suggested at that time a rate below one percent was likely during the next economic recession.

Outside of other events such as the S&L Crisis, Asian Contagion, Long-Term Capital Management, etc. which all drove money out of stocks and into bonds pushing rates lower, recessionary environments are especially prone at suppressing rates further. But, given the inflation of multiple asset bubbles, a credit-driven event that impacts the corporate bond market will drive rates to zero.

Furthermore, given rates are already negative in many parts of the world, which will likely be even more negative during a global recessionary environment, zero yields will still remain more attractive to foreign investors. This will be from both a potential capital appreciation perspective (expectations of negative rates in the U.S.) and the perceived safety and liquidity of the U.S. Treasury market.

Rates are ultimately directly impacted by the strength of economic growth and the demand for credit. While short-term dynamics may move rates, ultimately, the fundamentals, combined with the demand for safety and liquidity, will be the ultimate arbiter.

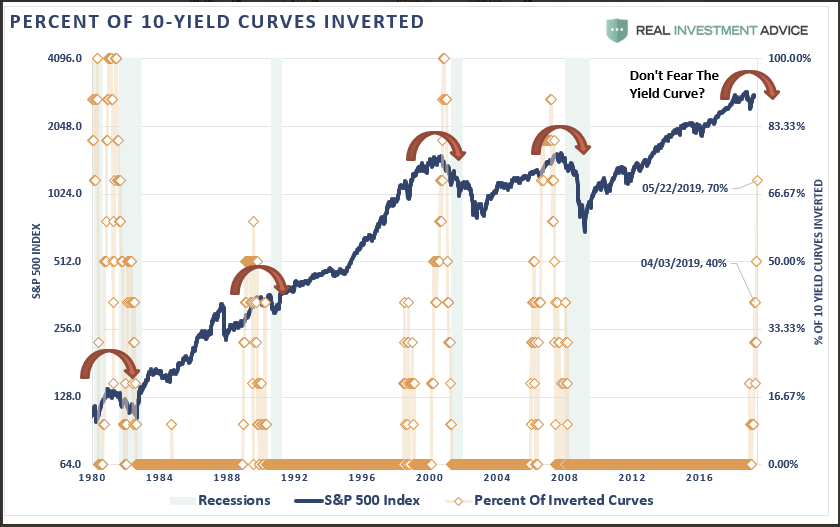

With the majority of yield curves that we track now inverted, many economic indicators flashing red, and financial markets dependent on “Fed action” rather than strong fundamentals, it is likely the bond market already knows a problem in brewing.

However, while I am fairly certain the “facts” will play out as they have historically, rest assured that if the “facts” do indeed change, I will gladly change my view.

Currently, there is NO evidence that a change of facts has occurred.

Of course, we aren’t the only ones expecting rates to go to zero.As Bloomberg noted:

“Billionaire Stan Druckenmiller said he could see the Fed funds rate going to zero in the next 18 months if the economy softens and that he recently piled into Treasuries as the U.S. trade war with China escalated.

‘When the Trump tweet went out, I went from 93% invested to net flat, and bought a bunch of Treasuries,’ Druckenmiller said Monday evening, referring to the May 5 tweet from President Donald Trump threatening an increase in tariffs on China. ‘Not because I’m trying to make money, I just don’t want to play in this environment.'”

It has taken a massive amount of interventions by Central Banks to keep economies afloat globally over the last decade, and there is rising evidence that growth is beginning to decelerate.

While another $2-4 Trillion in QE might indeed be successful in further inflating the third bubble in asset prices since the turn of the century, there is a finite ability to continue to pull forward future consumption to stimulate economic activity. In other words, there are only so many autos, houses, etc., which can be purchased within a given cycle.

There is evidence the cycle peak has been reached.

If I am correct, and the effectiveness of rate reductions and QE are diminished due to the reasons detailed herein, the subsequent destruction to the “wealth effect” will be far larger than currently imagined. There is a limit to just how many bonds the Federal Reserve can buy and a deep recession will likely find the Fed powerless to offset much of the negative effects.

If more “QE” works, great.

But, as investors, with our retirement savings at risk, what if it doesn’t?

In a moment of rare insight, two weeks ago in response to a question “Why is establishment media romanticizing communism? Authoritarianism, poverty, starvation, secret police, murder, mass incarceration? WTF?”, we said that this was simply a “prelude to central bank funded universal income”, or in other words, Fed-funded and guaranteed cash for everyone.

On Thursday afternoon, in a stark warning of what’s to come, San Francisco Fed President John Williams confirmed our suspicions when he said that to fight the next recession, global central bankers will be forced to come up with a whole new toolkit of “solutions”, as simply cutting interest rates won’t well, cut it anymore, and in addition to more QE and forward guidance – both of which were used widely in the last recession – the Fed may have to use negative interest rates, as well as untried tools including so-called price-level targeting or nominal-income targeting.

This is a bold, tactical admission that as a result of the aging workforce and the dramatic slack which still remains in the labor force that the US central bank will have to take drastic steps to preserve social order and cohesion.

According to Williams’,Reuters reports, central bankers should take this moment of “relative economic calm” to rethink their approach to monetary policy. Others have echoed Williams’ implicit admission that as a result of 9 years of Fed attempts to stimulate the economy – yet merely ending up with the biggest asset bubble in history – the US finds itself in a dead economic end, such as Chicago Fed Bank President Charles Evans, who recently urged a strategy review at the Fed, but Williams’ call for a worldwide review is considerably more ambitious.

Among Williams’ other suggestions include not only negative interest rates but also raising the inflation target – to 3%, 4% or more, in an attempt to crush debt by making life unbearable for the majority of the population – as it considers new monetary policy frameworks. Still, even the most dovish Fed lunatic has to admit that such strategies would have costs, including those that diverge greatly from the Fed’s current approach. Or maybe not: “price-level targeting, he said, is advantageous because it fits “relatively easily” into the current framework.”

Considering that for the better part of a decade the Fed prescribed lower rates and ZIRP as the cure to the moribund US economy, only to flip and then propose higher rates as the solution to all problems. It is not surprising that even the most insane proposals are currently being contemplated because they fit “relatively easily” into the current framework.

Additionally, confirming that the Fed has learned nothing at all, during a Q&A in San Francisco, Williams said that “negative interest rates need to be on the list” of potential tools the Fed could use in a severe recession. He also said that QE remains more effective in terms of cost-benefit, but “would not exclude that as an option if the circumstances warranted it.”

“If all of us get stuck at the lower bound” then “policy spillovers are far more negative,” Williams said of global economic interconnectedness. “I’m not pushing for” some “United Nations of policy.”

And, touching on our post from mid-September, in which we pointed out that the BOC was preparing to revising its mandate, Williams also said that “the Fed and all central banks should have Canada-like practice of revisiting inflation target every 5 years.”

Meanwhile, the idea of Fed targeting, or funding, “income” is hardly new: back in July,Deutsche Bank was the first institutionto admit that the Fed has created “universal basic income for the rich”:

The accommodation and QE have acted as a free insurance policy for the owners of risk, which, given the demographics of stock market participation, in effect has functioned as universal basic income for the rich. It is not difficult to see how disruptive unwind of stimulus could become. Clearly, in this context risk has become a binding constraint.

It is only “symmetric” that everyone else should also benefit from the Fed’s monetary generosity during the next recession.

* * *

Finally, for those curious what will really happen after the next “great liquidity crisis”, JPM’s Marko Kolanovic laid out a comprehensive checklist one month ago. It predicted not only price targeting (i.e., stocks), but also negative income taxes, progressive corporate taxes, new taxes on tech companies, and, of course, hyperinflation. Here is the excerpt.

What will governments and central banks do in the scenario of a great liquidity crisis? If the standard rate cutting and bond purchases don’t suffice, central banks may more explicitly target asset prices (e.g., equities). This may be controversial in light of the potential impact of central bank actions in driving inequality between asset owners and labor. Other ‘out of the box’ solutions could include a negative income tax (one can call this ‘QE for labor’), progressive corporate tax, universal income and others. To address growing pressure on labor from AI, new taxes or settlements may be levied on Technology companies (for instance, they may be required to pick up the social tab for labor destruction brought by artificial intelligence, in an analogy to industrial companies addressing environmental impacts). While we think unlikely, a tail risk could be a backlash against central banks that prompts significant changes in the monetary system. In many possible outcomes, inflation is likely to pick up.

The next crisis is also likely to result in social tensions similar to those witnessed 50 years ago in 1968. In 1968, TV and investigative journalism provided a generation of baby boomers access to unfiltered information on social developments such as Vietnam and other proxy wars, Civil rights movements, income inequality, etc. Similar to 1968, the internet today (social media, leaked documents, etc.) provides millennials with unrestricted access to information on a surprisingly similar range of issues. In addition to information, the internet provides a platform for various social groups to become more self-aware, united and organized. Groups span various social dimensions based on differences in income/wealth, race, generation, political party affiliations, and independent stripes ranging from alt-left to alt-right movements. In fact, many recent developments such as the US presidential election, Brexit, independence movements in Europe, etc., already illustrate social tensions that are likely to be amplified in the next financial crisis. How did markets evolve in the aftermath of 1968? Monetary systems were completely revamped (Bretton Woods), inflation rapidly increased, and equities produced zero returns for a decade. The decade ended with a famously wrong Businessweek article ‘the death of equities’ in 1979.

Kolanovic’s warning may have sounded whimsical one month ago. Now, in light of Williams’ words, it appears that it may serve as a blueprint for what comes next.

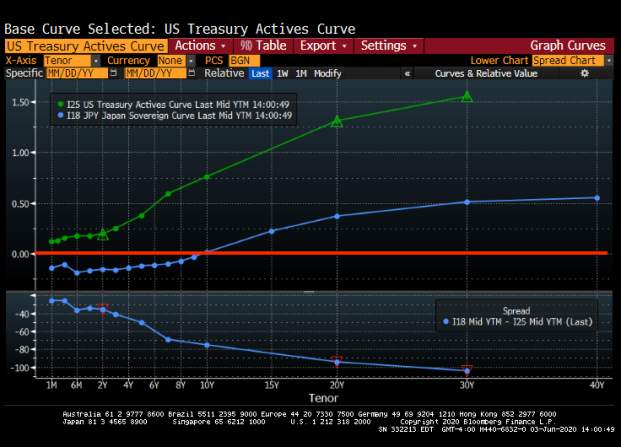

Negative interest rate policies elsewhere hit US Treasury yields

The side effects of Negative Interest Rate Policies in Europe and Japan — what we’ve come to call the NIRP absurdity — are becoming numerous and legendary, and they’re fanning out across the globe, far beyond the NIRP countries.

No one knows what the consequences will be down the line. No one has ever gone through this before. It’s all a huge experiment in market manipulation. We have seen crazy experiments before, like creating a credit bubble and a housing bubble in order to stimulate the economy following the 2001 recession in the US, which culminated with spectacular fireworks.

Not too long ago, economists believed that nominal negative interest rates couldn’t actually exist beyond very brief periods. They figured that you’d have to increase inflation and keep interest rates low but positive to get negative “real” interest rates, which might have a similar effect, that of “financial repression”: perverting the behavior of creditors and borrowers alike, and triggering a massive wealth transfer.

But the NIRP absurdity has proven to be possible. It can exist. It does exist. That fact is so confidence-inspiring to central banks that more and more have inflicted it on their bailiwick. The Bank of Japan was the latest, and the one with the most debt to push into the negative yield absurdity — and therefore the most consequential.

But markets are globalized, money flows in all directions. The hot money, often borrowed money, washes ashore tsunami like, but then it can recede and dry up, leaving behind the debris. These money flows trigger chain reactions in markets around the globe.

NIRP is causing fixed income investors, and possibly even equity investors, to flee that bailiwick. They sell their bonds to the QE-obsessed central banks, which play the role of the incessant dumb bid in order to whip up bond prices and drive down yields, their stated policy. Investors take their money and run.

And then they invest it elsewhere — wherever yields are not negative, particularly in US Treasuries. This no-questions-asked demand from investors overseas has done a job on Treasury yields. That’s why the 10-year yield in the US has plunged even though the Fed got serious about flip-flopping on rate increases and then actually raised its policy rate, with threats of more to come.

So here are some of the numbers and dynamics — among the many consequences of the NIRP absurdity — by Christine Hughes, Chief Investment Strategist at OtterWood Capital:

Negative interest rate policies implemented by central banks in Europe and Japan have driven yields on many sovereign debt issues into negative territory.

If you look at the BAML Sovereign Bond index, just 6% of the bonds had negative yields at the beginning of 2015. Since then the share of negative yielding bonds has increased to almost 30% of the index, see below.

With negative yielding bonds becoming the norm, investors are instead reaching for the remaining assets with positive yields (i.e. US Treasuries). Private Japanese investors have purchased nearly $70 billion in foreign bonds this year with the sharpest increase coming after the BoJ adopted negative rates. Additionally, inflows into US Treasuries from European funds have increased since 2014:

“According to an analysis by Bank of America Merrill Lynch, for every $100 currently managed in global sovereign benchmarks, avoiding negative yields would result in roughly $20 being pushed into overweight US Treasuries assets,” wrote Christine Hughes of OtterWood Capital.

That’s a lot of money in markets where movements are measured in trillions of dollars. As long as NIRP rules in the Eurozone and Japan, US Treasury yields will become even more appealing every time they halfheartedly try to inch up just one tiny bit.

So China, Russia, and Saudi Arabia might be dumping their holdings of US Treasuries, for reasons of their own, but that won’t matter, and folks that expected this to turn into a disaster for the US will need some more patience: these Treasuries will be instantly mopped up by ever more desperate NIRP refugees.

QUESTION: Mr. Armstrong, I think I am starting to see the light you have been shining. Negative interest rates really are “completely insane”. I also now see that months after you wrote about central banks were trapped, others are now just starting to entertain the idea. Is this distinct difference in your views that eventually become adopted with time because you were a hedge fund manager?

ANSWER: I believe the answer is rather simple. How can anyone pretend to be analysts if they have never traded? It would be like a man writing a book explaining how it feels to give birth. You cannot analyze what you have never done. It is just impossible. Those who cannot teach and those who can just do. Negative interest rates are fueling deflation. People have less income to spend so how is this beneficial? The Fed always needed 2% inflation. The father of negative interest rates is Larry Summers. He teaches or has been in government. He is not a trader and is clueless about how markets function. I warned that this idea of negative interest rates was very dangerous.

Yes, I have warned that the central banks are trapped. Their QE policies have totally failed. There were numerous “analysts” without experience calling for hyperinflation, collapse of the dollar, yelling the Fed is increasing the money supply so buy gold. The inflation never appeared and gold declined. Their reasoning was so far off the mark exactly as people like Larry Summers. These people become trapped in their own logic it becomes irrational gibberish. They only see one side of the coin and ignore the rest.

Central banks have lost all ability to manage the economy even in theory thanks to this failed reasoning. They have bought-in the bonds and are unable to ever resell them again. If they reverse their policy of QE and negative interest rates, government debt explodes with insufficient buyers. If the central banks refuse to reverse this crazy policy of QE and negative interest rates they will see a massive capital flight from government to the private sector once the MAJORITY realize the central banks are incapable of any control.

The central banks have played a very dangerous game and lost. It appears we are facing the collapse of Social Security which began August 14th, 1935 (1935.619) because they stuffed with government debt and robbed the money for other things. Anyone else would go to prison for what politicians have done and prosecutors would never defend the people because they want to become famous politicians. We will probably see the end of this Social Security program by 2021.772 (October 9th, 2021), or about 89 weeks into the next business cycle. These people are completely incompetent to manage the economy and we are delusional to think people with no experience as a trader can run things. If you have never traded, you have no busy trying to “manipulate” society with you half-baked theories. So yes. The central banks are trapped. They have lost ALL power. It becomes just a matter of time as the clock ticks and everyone wakes up and say: OMG!

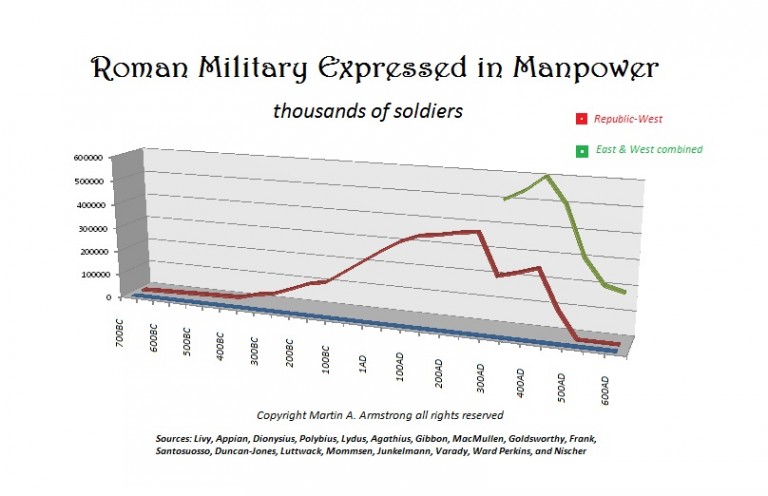

We have government addicted to borrowing and if rates rise, then everything will explode in their face. Western Civilization is finished as we know it just as Communism collapsed because we too subscribe to the theory of Marx that government is capable of managing the economy. Just listen to the candidates running for President. They are all preaching Marx. Vote for me and I will force the economy to do this. IMPOSSIBLE! We have debt which is unsustainable the further you move away from the United States which is the core economy such as emerging markets. Unfunded pensions destroyed the Roman Empire. We are collapsing in the very same manner and for the very same reason. We are finishing a very very very important report on the whole pension crisis issue worldwide.

If you’re a fan of dovish policymakers who are committed to Keynesian insanity, you can always count on Minneapolis Fed chief Narayana Kocherlakota who, as we’ve detailed extensively, is keen on the idea that if the US wants to help itself out, it will simply issue more monetizable debt, because that way, the Fed will have more room to ease in the event its current easing efforts continue to prove entirely ineffective (and yes, the irony inherent in that assessment is completely intentional).

On Thursday, Kocherlakota is out with some fresh nonsense he’d like you to blindly consider and what you’ll no doubt notice from the following Bloomberg bullet summary is that, as the latest dot plot made abundantly clear, NIRP is in now definitively in the playbook.

KOCHERLAKOTA SAYS FED SHOULD CONSIDER NEGATIVE RATES

KOCHERLAKOTA: TAPERING ASSET PURCHASES LED TO SLOWER JOB GAINS

KOCHERLAKOTA SAYS JOBS SLOWDOWN ‘NOT SURPRISING’ GIVEN POLICY

KOCHERLAKOTA: TAPERING ASSET PURCHASES LED TO SLOWER JOB GAINS

So not only should the Fed take rates into the Keynesian NIRP twilight zone, but in fact, the subpar September NFP print was the direct result of not printing enough money which is particularly amusing because Citi just got done telling the market that the Fed should hike (i.e. tighten policy) because jobs data at this time of the year is prone to being biased to the downside.

“Can’t Princeton turn out a half decent person these days instead of the constant stream of “pinky and the brain” economists they have created lately?!”

You must be logged in to post a comment.