Despite efforts by state legislators at creating a socialist utopia, California still has the highest poverty rate in the nation at 19%, despite a 1.4% decrease from last year according to the Census Bureau.

Poverty and income figures released Wednesday reveal that over 7 million Californians are struggling to get by in the second most expensive state to live in, according to the Council for Community and Economic Research‘s 2017 Annual Cost of Living Index.

And while California has a “vigorous economy and a number of safety net programs to aid needy residents,” according to the Sacramento Bee, one out of every five residents is suffering economic hardship – which is fueled in large part by sky-high housing costs, according to Caroline Danielson, policy director at the Public Policy Institute of California.

“We do have a housing crisis in many parts of the state and our poverty rate is highest in Los Angeles County,” she said, adding that cost of living and poverty is often highest in the state’s coastal counties. “When you factor that in we struggle.”

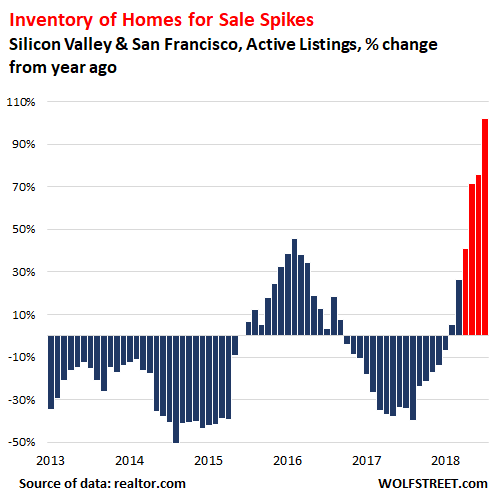

Silicon Valley residents in particular are leaving in droves – more so than any other part of the state. Nearby San Mateo County which is home to Facebook came in Second, while Los Angeles County came in third.

“They’re looking for affordability and not finding it in Santa Clara County,” said Danielle Hale, chief economist for realtor.com.

It’s not just housing prices driving the exodus, of course. Punitive taxes – more than twice as much as some other states, are eating away at disposable income. Nearby Arizona’s income tax rate is 4.54% vs. California’s 9.3%, while the new tax bill may accelerate the exodus.

As Michael Snyder of the Economic Collapse Blog pointed out in May…

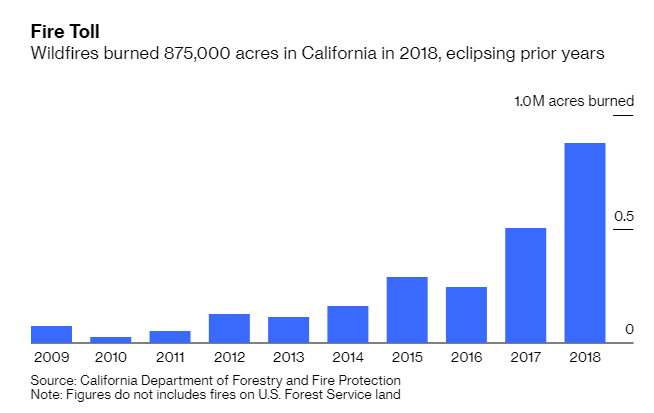

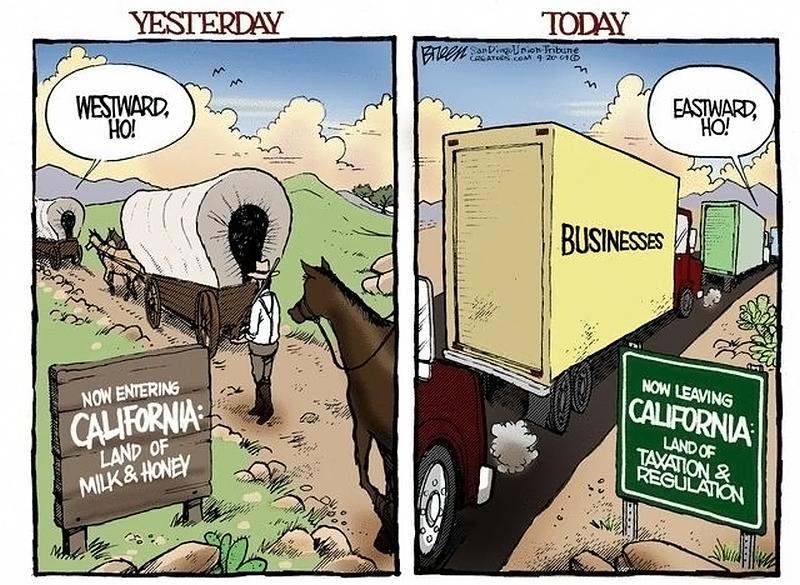

Reasons for the mass exodus include rising crime, the worst traffic in the western world, a growing homelessness epidemic, wildfires, earthquakes and crazy politicians that do some of the stupidest things imaginable. But for most families, the decision to leave California comes down to one basic factor…

Money.

Mass Exodus

As you may or may not be aware, we’ve mentioned the flood of various types of Californians fleeing the state for various reasons; be it wealthy families who want to keep more of their income safe from the tax man, or poor residents leaving the Golden State because they are being crushed by the high cost of living.

To that end, the Orange County Register notes a significant out migration of people in their child-raising years – as the largest group leaving the state, some 28%, are those aged 35 to 44.

According to IRS data from 2015-2016, the latest available, roughly half of those leaving the state make less than $50,000 per year, while roughly 25% of those leaving make over $100,000.

What did the OC register conclude?

Thanks to unaffordable housing, California’s moderate wage earners are going to have to leave the state, while only the wealthy and the impoverished residents will remain.

But the big enchilada in California — by far the largest source of distortion in living costs — is housing. Over 90 percent of the difference in costs between California’s coastal metropolises and the country derives from housing. Coastal California is affordable for roughly 15 percent of residents, down from 30 percent in 2000 and 30 percent in the interior, from nearly 60 percent in 2000. In the country as a whole, affordability hovers at roughly 60 percent.

***

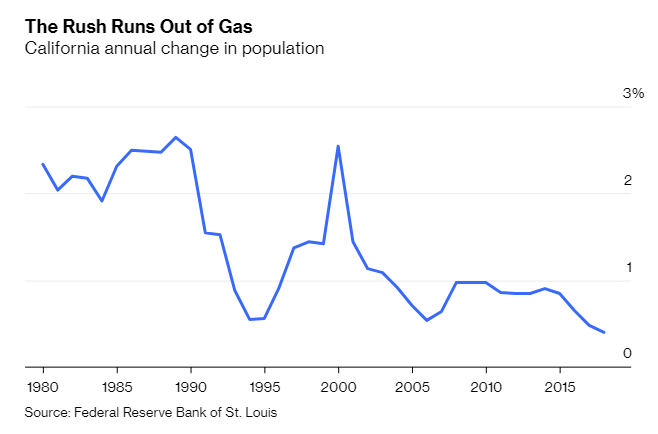

Over time these factors — along with prospects of reduced immigration — will impact severely the state’s future. California is already seeing its population aged 6 to 17 decline. This reflects a continued drop in fertility in comparison to less regulated, and less costly, states such as Utah, Texas and Tennessee. These areas are generally those experiencing the biggest surge in millennial populations. –OC Register

And according to ULI, 74% of California millennials are considering an exodus.

Where to?

As we noted in June, these are the top 10 California counties that people are leaving, and where they’re headed (via the Mercury News):

1. Santa Clara County

Out of state destinations: Arizona, Nevada, Texas and Idaho

In state destinations: Alameda, Sacramento, San Joaquin, Santa Cruz and Placer counties

2. San Mateo County

Out of state destinations: Arizona, Nevada, Texas and Washington

In state destinations: Alameda, Contra Costa, Santa Clara, Sacramento, and San Francisco counties

3. Los Angeles County

Out of state destinations: Nevada, Arizona, and Idaho

In state destinations: San Bernardino, Riverside, Ventura and Kern counties

4. Napa County

Out of state destinations: Arizona, Idaho, Nevada, Florida and Oregon

In state destinations: Solano, Sonoma, Sacramento, Lake and El Dorado counties

5. Monterey County

Out of state destinations: Arizona, Nevada, and Idaho

In state destinations: San Luis Obispo, Fresno, Santa Cruz, Sacramento and San Diego counties

6. Alameda County

Out of state destinations: Arizona, Nevada, Idaho, and Hawaii.

In state destinations: Contra Costa, San Joaquin, Sacramento, Placer, and El Dorado counties

7. Marin County

Out of state destinations: Nevada, Arizona, Oregon and Idaho.

In state destinations: Sonoma, Contra Costa, Solano and San Francisco counties

8. Orange County

Out of state destinations: Arizona, Nevada and Idaho

In state destinations: Riverside, Los Angeles, San Bernardino, San Diego and San Luis Obispo

9. Santa Barbara County

Out of state destinations: Arizona, Nevada and Idaho.

In state destinations: San Luis Obispo, Ventura, Los Angeles, Riverside and Kern counties

10. San Diego County

Out of state destinations: Arizona and Nevada

In state destinations: Riverside, San Bernardino, Imperial, Orange County and Los Angeles

Source: ZeroHedge

You must be logged in to post a comment.