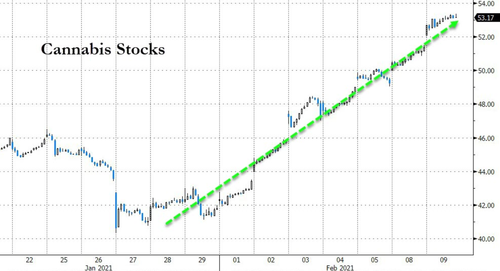

With Gamestop stock in freefall, down a further 5% Wednesday morning to the low 47-handle, r/WallStreetBets has gravitated to cannabis stocks in recent days, squeezing the living daylights out of any hedge fund that is short pot stocks.

With Gamestop stock in freefall, down a further 5% Wednesday morning to the low 47-handle, r/WallStreetBets has gravitated to cannabis stocks in recent days, squeezing the living daylights out of any hedge fund that is short pot stocks.

While all eyes have been focused on GameStop and a handful of other heavily-shorted stocks as they exploded higher under continuous fire from WallStreetBets traders igniting a short-squeeze coinciding with a gamma-squeeze, the last few days saw another asset suddenly get in the crosshairs of the ‘Reddit-Raiders’ – Silver.

Brokerages/Markets A CRIME IN PROGRESS FOR RETAIL INVESTORS

This is unacceptable.

We now need to know more about @RobinhoodApp’s decision to block retail investors from purchasing stock while hedge funds are freely able to trade the stock as they see fit.

As a member of the Financial Services Cmte, I’d support a hearing if necessary. https://t.co/4Qyrolgzyt

— Alexandria Ocasio-Cortez (@AOC) January 28, 2021

A week after New Jersey Governor Phil Murphy signaled his virtue to the ‘social justice’ agenda-watchers by proposing a tax on high frequency trading, no lesser establishment organization than The New York Stock Exchange has passive-aggressively signaled its displeasure by saying in a statement that it will test its ability to operate outside of New Jersey.

The major exchange operators previously have gone to court over proposals that they said would harm markets. NYSE, Nasdaq Inc. and CBOE Global Markets even took the extreme step of suing their main regulator, the U.S. Securities and Exchange Commission, over a transaction-fee pilot program last year. They won.

“A financial transaction tax is a recycled idea with a lousy track record — all over the world,” said the Equity Markets Association, a trade group that represents the three companies.

The move by New Jersey would “cause unintended and irreparable harm to the U.S. capital markets,” CBOE said in a separate statement. “A transaction tax is a direct cost shouldered by investors, who will also end up paying for the price of diminished liquidity and wider spreads in our markets.”

And as we noted previously, the NYSE has already threatened to depart the moment a tax was enacted:

“We have data centers in various states and the ability to move trading outside of New Jersey in a business day,” said Hope Jarkowski, co-head of government affairs for New York Stock Exchange parent Intercontinental Exchange.

And today, the exchange, in coordination with Nasdaq, CBOE Global Markets, and other industry participants, ramped up the rhetoric, saying that it will conduct a test of all its exchanges operating from their secondary locations on Sept. 26 to “confirm the industry’s ability to seamlessly move live trading out of New Jersey,” according to a statement.

* * *

Audience: NYSE, NYSE AmericanEquities, NYSE American Options, NYSE Arca Equities, NYSE Arca Options, NYSE Chicago, NYSE National, FINRA/NYSE TRF, and Global OTC Traders

Subject: NYSE exchanges to prepare for potential move from New Jersey data center, including temporary relocation of NYSE Chicago on September 28

Numerous NYSE member firms have recently reached out to the Exchange to understand our plans should New Jersey institute its proposed tax on financial transactions processed through electronic infrastructure located in the state. They are concerned, as are we, that any tax imposed will be passed through to NYSE members, and ultimately their clients, who are often the very same Main Street investors who reside in states like New Jersey and elsewhere.

NYSE has the ability to operate all of its markets out of either its primary data center in Mahwah, New Jersey or an alternate data center. Designed for various disaster recovery scenarios, a change in location can be performed in a matter of minutes, if necessary.

If our members express a strong preference to permanently relocate our trading infrastructure out of New Jersey, the process to do this is well-documented, regularly tested and would not cause any disruption to NYSE operations.

To help test and prepare our members for any such action, NYSE will implement two immediate measures:

1. Relocation of production trading for NYSE Chicago the week of September 28: The NYSE will operate one of its equity exchanges, NYSE Chicago, from its secondary data center from September 28th to October 2nd. This will confirm the industry’s ability to seamlessly move live trading out of New Jersey.

2. Weekend test of all markets: The NYSE, in coordination with Nasdaq, CBOE, SIFMA and other industry participants, will conduct a test of all its exchanges operating from their secondary locations on Saturday, September 26, 2020. This controlled test will exercise the industry’s preparedness for a potential wholesale transition out of New Jersey. Details for the weekend test will follow in a separate announcement.

* * *

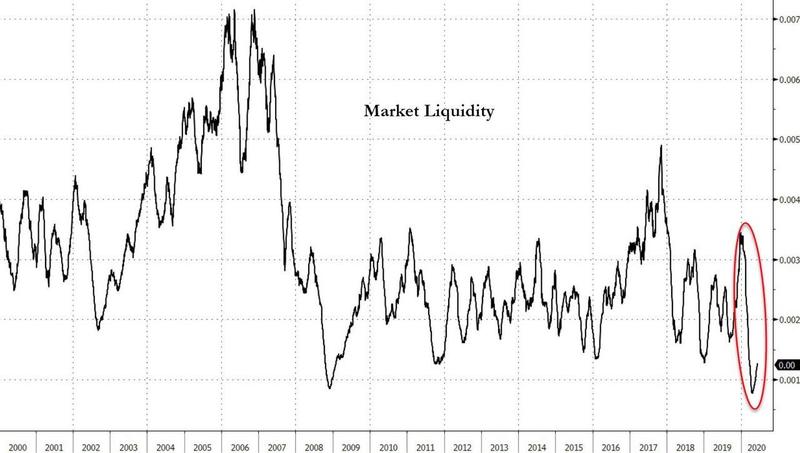

Of course, the big question, as we previously noted, what happens when all the states in which NYSE have data centers follow NJ in establishing a paywall for ultra fast trades which do nothing to make the market more efficient unless one counts surging flash crashes “efficiency”?

Market liquidity is already at record lows!

A city boy, Kenny, moved to the country and bought a donkey from an old farmer for $100. The farmer agreed to deliver the donkey the next day.

The next day the farmer drove up and said: “Sorry son, but I have some bad news. The donkey died.”

Kenny replied, “Well then, just give me my money back.”

The farmer said, “Can’t do that. I went and spent it already.”

Kenny said, “OK, then just unload the donkey.”

The farmer asked, “What ya gonna do with him?”

Kenny: “I’m going to raffle him off.”

Farmer: “You can’t raffle off a dead donkey!”

Kenny: “Sure I can. Watch me. I just won’t tell anybody he is dead.”

A month later the farmer met up with Kenny and asked, “What happened with that dead donkey?”

Kenny: “I raffled him off. I sold 500 tickets at $2 a piece and made a profit of $998.00.”

Farmer: “Didn’t anyone complain?”

Kenny: “Just the guy who won. So I gave him his $2 back.”

Kenny grew up and eventually became the chairman of *****

(USA.watchdog) Bo Polny: “In the last interview, I gave you a time point, and I am going to give it to you again. This time point is incredible, and it is a Biblical calculation.

I am waiting to see what happens at this time point because it is supposed to be a truly epic time point, and that time point is April 21, 2020.

It’s a time point where the world changes, one system comes to an end or something really obvious happens. So, coming into the month of May, we have this new time point or this new era.”

Polny says all his work is based on Biblical cycles. He goes through the last 7,000 years with a powerful PowerPoint presentation that culminates with the Second Coming of Jesus Christ and predicts a time window for his return in the not-so-distant future. Polny also says his charts say the bottom is going to be ugly for the so-called long term investors. Polny says, “What it points to is a market drop that keeps falling. The potential target is 5,000 to 5,050 range for the DOW, and the time point for this comes at the end of the year 2022.”

Polny also says the U.S. dollar has topped and is going lower. Bo says, “I looked at a chart recently, and the dollar has a double top. It has not made new highs in a long time. It has just been sitting there. A lot of times with market events, you see the dollar move down with the stock market. (The dollar was down big time on Friday 3/27/2020. It lost more the 1% on a day the DOW lost more than 900 points.) So, that is unusual. The dollar moved with the stock market, and gold did not go anywhere. Gold was steady.”

Bo says, “The people in control of this system will try to stop the fall, and they will fail. For that reason, point E (15,000 on the DOW) is coming. . . . They will try to stop it, and they will fail. Look what’s happening. What we have seen in March was a crash. . . . We have not seen is a plunge. The plunge comes in April.”

There is lots more in this hour long interview, including a free 30 page PowerPoint presentation on the 7,000 year cycle that started in the days of Adam and Eve. Join Greg Hunter of USAWatchdog.com as he goes One-on-One with analyst Bo Polny of Gold 2020Forecast.com.

PowerPoint associated with the video presentation:

https://drive.google.com/file/d/1ylA48rUgsObrFrI_IhiWFh3pIDTF8Ilm/view

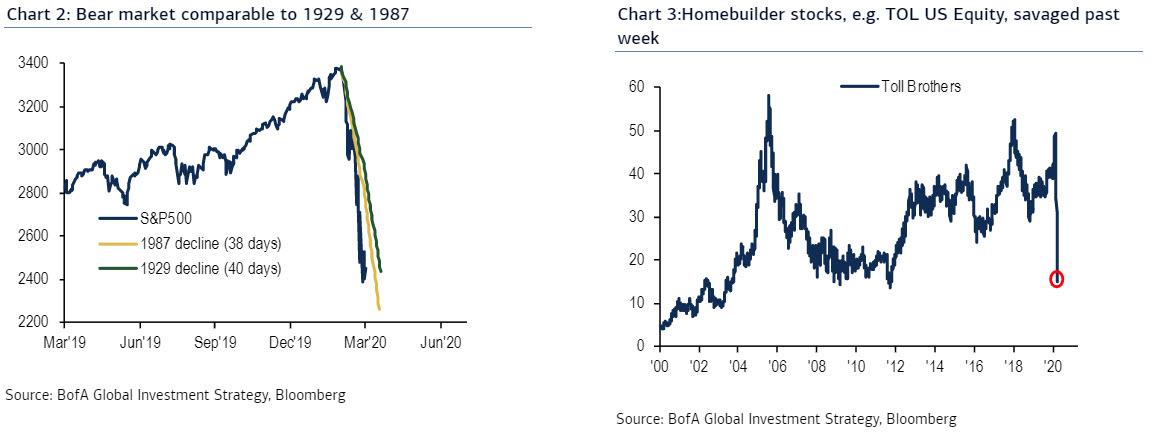

Back in December, someone in China made bat soup (at least according to the officially accepted narrative that doesn’t get you banned on Facebook, Twitter, etc), and the rest is history: in the next three months, the global equity market has lost $24 trillion in value, more than the $22 trillion in US GDP. And here is a staggering chart from BofA putting the crash of 2020 in its historic context: in the past month, the US stock market has crashed faster than both the Great Depression and Black Monday, and in terms of the total draw down, the crash of 2020 is now worse than 1929 and is fast approaching 1987.

Below, courtesy of BofA CIO Michael Hartnett, are several other stunning observations on the Crash of 2020:

Good luck to everyone.

It was definitely a ‘deer’ day…

Stocks down, Bonds down, credit down, gold down, oil down, copper down, crypto down, global systemically important banks down, and liquidity down…

Today was the worst day for a combined equity/bond portfolio… ever…

We just witnessed a global collapse in asset prices the likes we haven’t seen before. Not even in 2008 or 2000. All these prior beginnings of bear markets happened over time, relatively slowly at first, then accelerating to the downside.

This collapse here has come from some of the historically most stretched valuations ever setting the stage for the biggest bull trap ever. The coronavirus that no one could have predicted is brutally punishing investors that complacently bought into the multiple expansion story that was sold to them by Wall Street. Technical signals that outlined trouble way in advance were ignored while the Big Short 2 was already calling for a massive explosion in $VIX way before anybody ever heard of corona virus.

Worse, there is zero visibility going forward as nobody knows how to price in collapsing revenues and earnings amid entire countries shutting down virtually all public gatherings and activities. Denmark just shut down all of its borders on Friday, flight cancellations everywhere, the planet is literally shutting down in unprecedented fashion.

Last week was a central bank induced bear trap.

Look forward to huge trading opportunities, long and short, in the weeks and months ahead, while markets sort out what happened.

… and then there’s that virus

It’s absolutely stunning how the Fed/ECB/BoJ injected upwards of $1.1 trillion into global markets in the last quarter and cut rates 80 times in the past 12 months, which allowed money-losing companies to survive another day.

The leader of all this insanity is Telsa, the biggest money-losing company on Wall Street, has soared 120% since the Fed launched ‘Not QE.’

Tesla investors are convinced that fundamentals are driving the stock higher, but that might not be the case, as central bank liquidity has been pouring into anything with a CUSIP.

The company has lost money over the last 12 months, and to be fair, Elon Musk reported one quarter that turned a profit, but overall – Tesla is a black hole. Its market capitalization is larger than Ford and General Motors put together. When you listen to Tesla investors, near-term profitability isn’t important because if it were, the stock would be much lower.

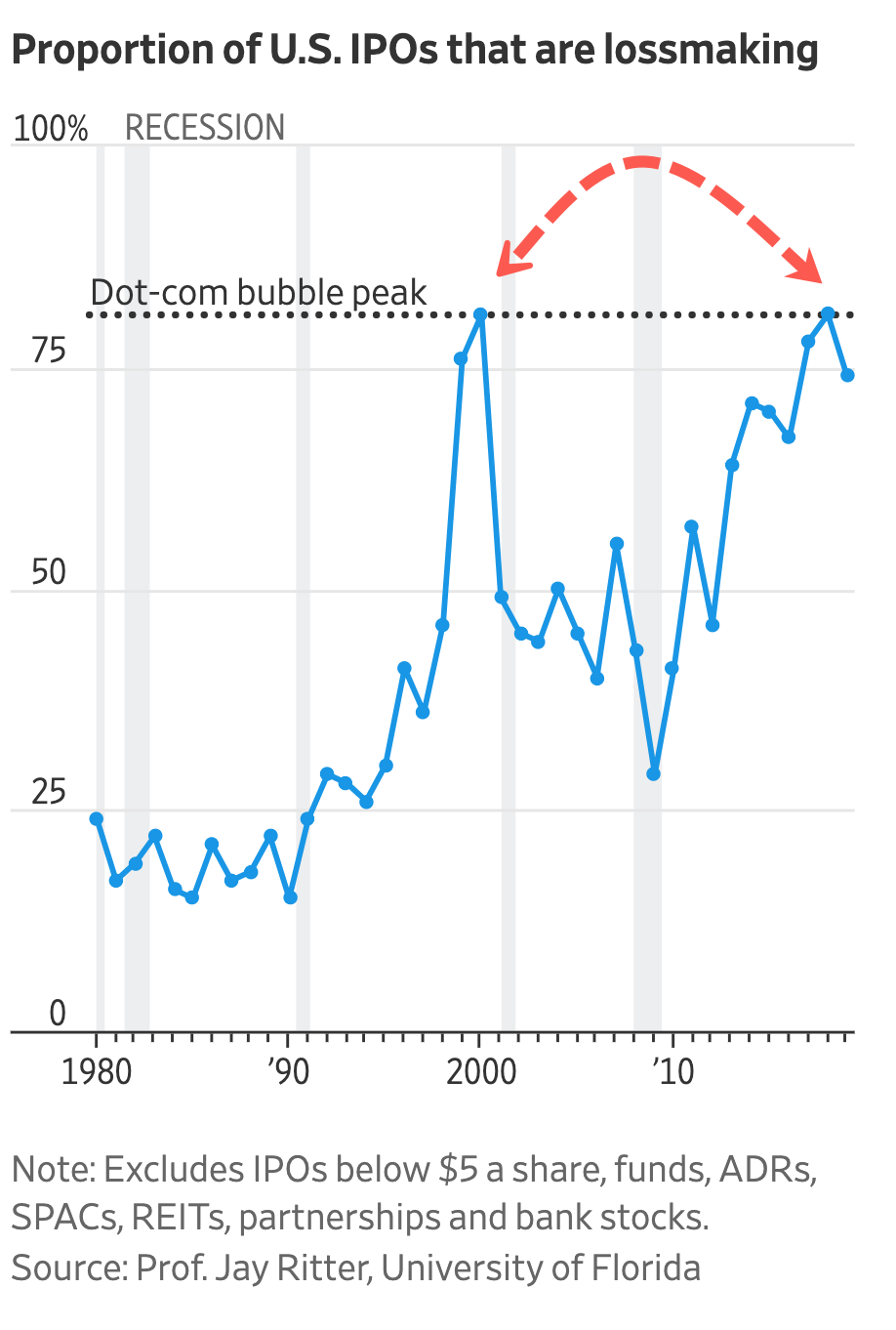

The Wall Street Journal notes that in the past 12 months, 40% of all US-listed companies were losing money, the highest level since the late 1990s – or a period also referred to as the Dot Com bubble.

Jay Ritter, a finance professor at the University of Florida, provided The Journal with a chart that shows the percentage of money-losing IPOs hit 81% in 2018, the same level that was also seen in 2000.

The Journal notes that 42% of health-care companies lost money, mostly because of speculative biotech. About 17% of technology companies also fail to turn a profit.

A more traditional company that has been losing money is GE. Its shares have plunged 60% in the last 42 months as a slowing economy, and insurmountable debts have forced a balance sheet recession that has doomed the company.

Data from S&P Global Market Intelligence shows for small companies, losing money is part of the job. About 33% of the 100 biggest companies reported losses over the last 12 months.

Among the smallest 80% of companies, there has been a notable rise in money-losing operations in the last three years.

“The proportion of these loss-making companies rose after each of the last two recessions and didn’t come down again afterward. The story should be familiar by now: Many small companies are being dominated by the biggest corporates, squeezing them out of markets and crushing their ability to invest for growth,” The Journal noted.

And while central bank liquidity has zombified companies, investors are already starting to make a mad dash out of trash into companies that turn a profit ahead of the next recession.

There was a period of about two months when some of the more confused, Fed sycophantic elements, would parrot everything Powell would say regarding the recently launched $60 billion in monthly purchases of T-Bills, and which according to this rather vocal, if always wrong, sub-segment of financial experts, did not constitute QE. Perhaps one can’t really blame them: after all, unable to think for themselves, they merely repeated what Powell said, namely that

“growth of our balance sheet for reserve management purposes should in no way be confused with the large-scale asset purchase programs that we deployed after the financial crisis. Neither the recent technical issues nor the purchases of Treasury bills we are contemplating to resolve them should materially affect the stance of monetary policy. In no sense, is this QE.“

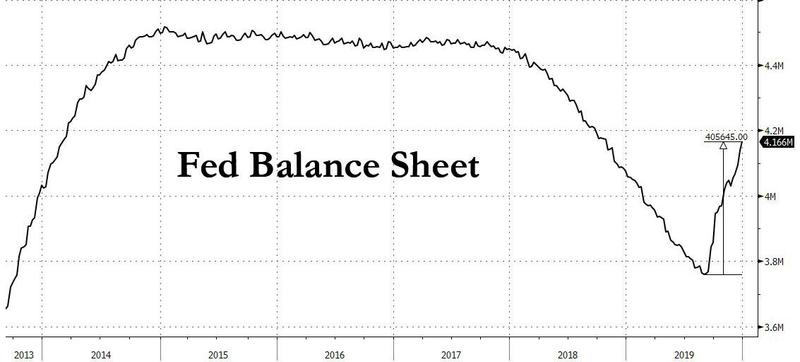

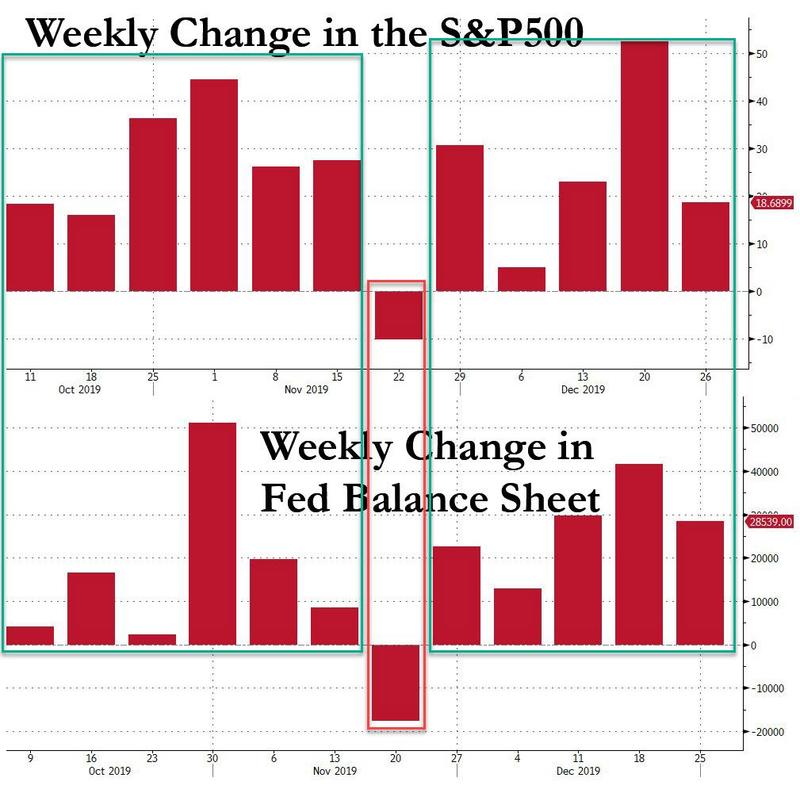

As it turned out, it was QE from the perspective of the market, which saw the Fed boosting its balance sheet by $60BN per month, and together with another $20BN or so in TSY and MBS maturity reinvestments, as well as tens of billions in overnight and term repos, and soared roughly around the time the Fed announced “not QE.”

And so, as the Fed’s balance sheet exploded by over $400 billion in under four months, a rate of balance sheet expansion that surpassed QE1, QE2 and Qe3…

… stocks blasted off higher roughly at the same time as the Fed’s QE returned, and are now up every single week since the start of the Fed’s QE4 announcement when the Fed’s balance sheet rose, and are down just one week since then: the week when the Fed’s balance sheet shrank.

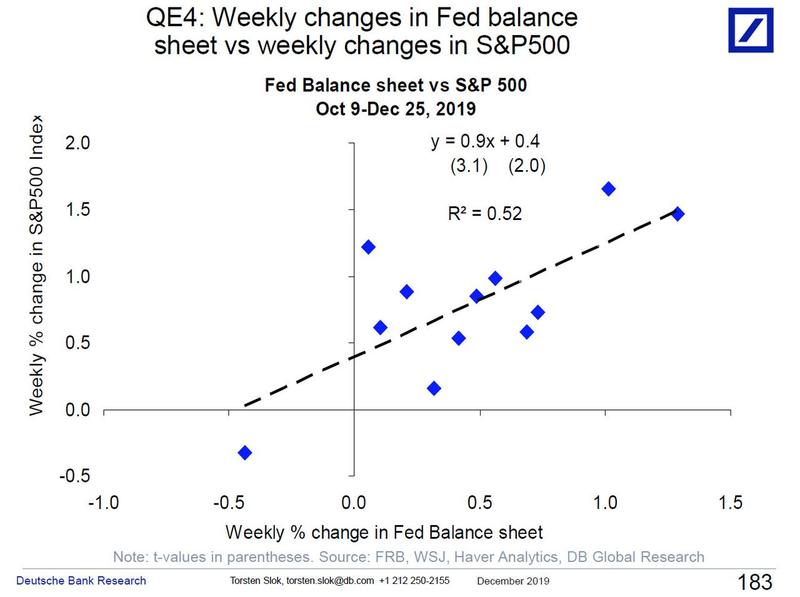

The result of this unprecedented correlation between the market’s response to the Fed’s actions – and the Fed’s growing balance sheet – has meant that it gradually became impossible to deny that what the Fed is doing is no longer QE. It started with Bank of America in mid-November (as described in “One Bank Finally Admits The Fed’s “NOT QE” Is Indeed QE… And Could Lead To Financial Collapse“), and then after several other banks also joined in, and even Fed fanboy David Zervos admitted on CNBC that the Fed is indeed doing QE, the tipping point finally arrived, and it was no longer blasphemy (or tinfoil hat conspiracy theory) to call out the naked emperor, and overnight none other than Deutsche Bank joined the “truther” chorus, when in a report by the bank’s chief economist Torsten Slok, he writes what we pointed out several weeks back, namely that

“since QE4 started in October, a 1% increase in the Fed balance sheet has been associated with a 1% increase in the S&P500, see chart below.”

Not that DB has absolutely no qualms about calling what the Fed is doing QE4 for the simple reason that… it is QE4.

The chart in question, which is effectively the same as the one we created above, shows the weekly change in the Fed’s balance sheet and the S&P500 as a scatterplot, and concludes that all it takes to push the S&P higher by 1% is to grow the Fed’s balance sheet by 1%.

And just to underscore this point, the strategist points out that such a finding is “consistent with this new working paper, which finds that QE boosts stock markets even when controlling for improving macro fundamentals.” Which, of course, is hardly rocket science – after all when you inject hundreds of billions into the market in months, and this money can’t enter the economy, it will enter the market. The result: the S&P trading at an all time high in a year in which corporate profits actually decreased and the entire rise in the stock market was due to multiple expansion.

In short: the Kool Aid is flowing, the party is in full force and everyone has to dance, because the Fed will continue to perform QE4 at least until Q2 2020. Which reminds us of what we wrote last week, namely that another big bank, Morgan Stanley, has already seen through the current melt up phase, and predicts the “Melt-Up Lasting Until April, After Which Markets Will “Confront A World With No Fed Support“.”

The Fed, reportedly, took action in 2019 – with its massive flip-flop, cutting rates drastically and expanding its balance sheet at the fastest pace since the financial crisis – in order to ‘fix’ the yield curve which had dropped into the media-terrifying inverted state… but what investors (and The Fed) appear to have forgotten (or choose to ignore) is that it is now much more concerning.

The last few months have seen the yield curve steepen dramatically, up 35bps from August’s -5bps spread in 2s10s to over 30bps today – the steepest since October 2018…

Source: Bloomberg

That is great news, right? No more recession risk, right?

Wrong!

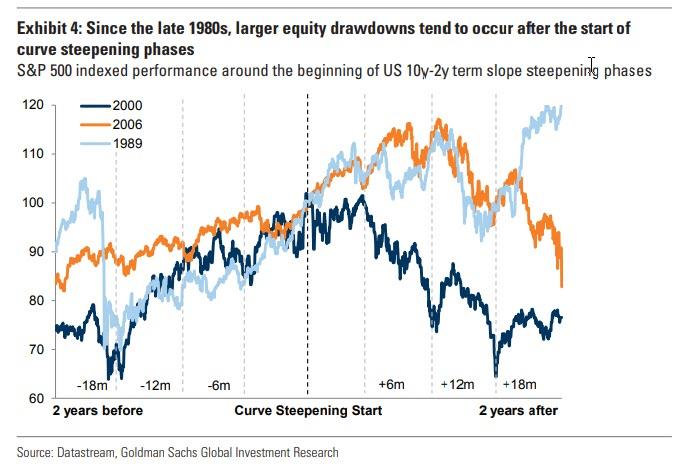

While investors buy stocks with both hands and feet, we take a look at how risk assets perform after the curve flattens and/or inverts. According to back tests from Goldman, while risky assets in general can have positive performance with a flat yield curve, risky asset performances tend to be lower. This is consistent with Goldman’s base case forecast combining low (but positive) returns from here given the lack of profit growth and a less favorable macro backdrop.

What is far more notable, as ZeroHedge showed most recently last July, is that since the mid-1980s, significant stock draw downs (i.e. market crashes) began only when term slope started steepening after being inverted.

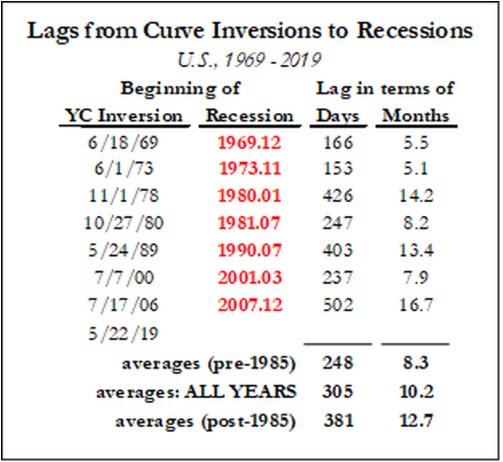

And remember, the yield curve’s forecasting record since 1968 has been perfect: not only has each inversion been followed by a recession, but no recession has occurred in the absence of a prior yield-curve inversion. There’s even a strong correlation between the initial duration and depth of the curve inversion and the subsequent length and depth of the recession.

So, be careful what you wish for… and celebrate; because as history has shown, the un-inverting of the yield curve is when the recessions start and when the markets begin to reflect reality.

Authored by Kevin Ludolph via Crescat Capital,

Dear Investors:

The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions.

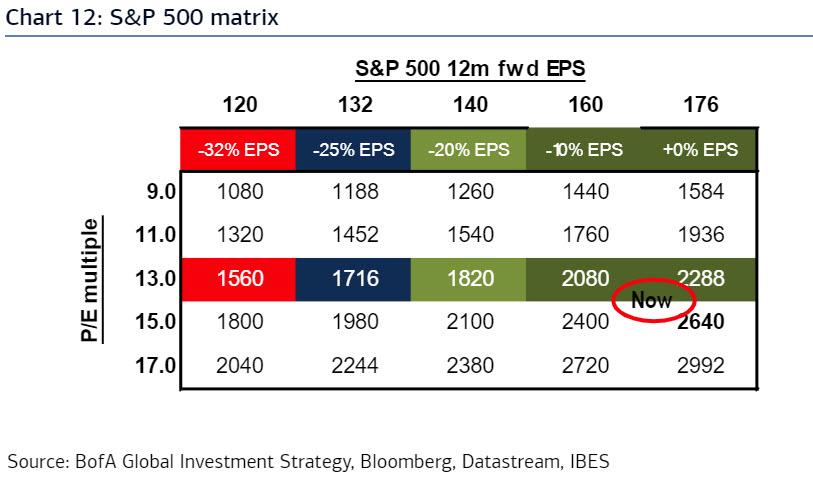

US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart below between the S&P 500 and its underlying expected earnings for 2019. Expected earnings for 2019 already trended down sharply in the first quarter and have started trending down again after the May trade war escalation.

Things are getting increasingly more crazy in bond land, where moments ago the 2Y Treasury dipped below 2.40%, trading at 2.3947% to be exact, and joining its 3Y and 5Y peers, which were already trading with a sub-2.4% handle. Why is that notable? Because 2.40% is where the Effective Fed Funds rate is, by definition the safest of safe yields in the market, that backstopped by the Fed itself. In other words, for the first time since 2008, the 2Y (and 3Y and 5Y) are all trading below the effective Fed Funds rate.

That the curve is now inverted from the Fed Funds rate all the way to the 5Y Treasury position suggests that whatever is coming, will be very ugly as increasingly more traders bet that one or more central banks may have no choice but to backstop risk assets and they will do it – how else – by buying bonds, sending yields to levels last seen during QE… i.e., much, much lower.

While the Fed has been engaging in quantitative tightening for over a year now in an attempt to shrink its asset holdings, it still has over $4.1 trillion in bonds on its balance sheet, and as a result of the spike in yields since last summer, their massive portfolio has suffered substantial paper losses which according to the Fed’s latest quarterly financial report, hit a record $66.453 billion in the third quarter, raising questions about their strategy at a politically charged moment for the central bank, whose “independence” has been put increasingly into question as a result of relentless badgering by Donald Trump.

What immediately caught the attention of financial analysts is that the gaping Q3 loss of over $66 billion, dwarfed the Fed’s $39.1 billion in capital, leaving the US central bank with a negative net worth…

… which would suggest insolvency for any ordinary company, but since the Fed gets to print its own money, it is of course anything but an ordinary company as Bloomberg quips.

It’s not just the fact that the US central bank prints the world’s reserve currency, but that it also does not mark its holdings to market. As a result, Fed officials usually play down the significance of the theoretical losses and say they won’t affect the ability of what they call “a unique non-profit entity’’ to carry out monetary policy or remit profits to the Treasury Department. Indeed, confirming this the Fed handed over $51.6 billion to the Treasury in the first nine months of the year.

The risk, however, is that should the Fed’s finances continue to deteriorate if only on paper, it could impair its standing with Congress and the public when it is already under attack from President Donald Trump as being a bigger problem than trade foe China.

Commenting on the Fed’s paper losses, former Fed Governor Kevin Warsh told Bloomberg that “a central bank with a negative net worth matters not in theory. But in practice, it runs the risk of chipping away at Fed credibility, its most powerful asset.’’

Additionally, the growing unrealized losses provide fuel to critics of the Fed’s QE and the monetary operating framework underpinning them, just as central bankers begin discussing the future of its balance sheet. And, as Bloomberg cautions, the metaphoric red ink also could make it politically more difficult for the Fed to resume QE if the economy turns down.

“We’re seeing the downside risk of unconventional monetary policy,’’ said Andy Barr, the outgoing chairman of the monetary policy and trade subcommittee of the House Financial Services panel. “The burden should be on them to tell us why this does not compromise their credibility and why the public and Congress should not be concerned about their solvency.’’

Of course, the culprit for the record loss is not so much the holdings, as the impact on bond prices as a result of rising rates which spiked in the summer as a result of the Fed’s own overoptimism on the economy, and which closed the third quarter at 3.10% on the 10Y Treasury. Indeed, with rates rising slower in the second quarter, the loss for Q3 was a more modest $19.6 billion.

And with yields tumbling in the fourth quarter as a result of the current growth and markets scare, it is likely that the Fed could book a major “profit” for the fourth quarter as the 10Y yield is now trading just barely above the 2.86% where it was on June 30.

Meanwhile, the Fed continues to shrink its bond holdings by a maximum of $50 billion per month, an amount that was hit on October 1, not by selling them, which could force it to recognize but by opting not to reinvest some of the proceeds of securities as they mature.

The Fed is expected to continue shrinking its balance sheet at rate of $50BN / month until the end of 2020 (as shown below) unless of course market stress forces the Fed to halt QT well in advance of its tentative conclusion.

In any case, the Fed will certainly never return to its far leaner balance sheet from before the crisis, which means that it will continue to indefinitely pay banks interest on the excess reserves they park at the Fed, with many of the recipient banks being foreign entities.

Barr, a Kentucky Republican, has accurately criticized that as a subsidy for the banks, one which will amount to tens of billions in annual “earnings” from the Fed, the higher the IOER rate goes up. He is not alone: so too has California Democrat Maxine Waters, who will take over as chair of the House Financial Services Committee in January following her party’s victory in the November congressional elections.

* * *

Going back to the Fed’s unique treatment of losses on its income statement and its under capitalization, in an Aug. 13 note, Fed officials Brian Bonis, Lauren Fiesthumel and Jamie Noonan defended the central bank’s decision not to follow GAAP in valuing its portfolio. Not only is the central bank a unique creation of Congress, it intends to hold its bonds to maturity, they wrote.

Under GAAP, an institution is required to report trading securities and those available for sale at fair or market value, rather than at face value. The Fed reports its balance-sheet holdings at face value.

The Fed is far less cautious with the treatment of its “profits”, which it regularly hands over to the Treasury: the interest income on its bonds was $80.2 billion in 2017. The central bank turns a profit on its portfolio because it doesn’t pay interest on one of its biggest liabilities – $1.7 trillion in currency outstanding.

The Fed’s unique financial treatments also extends to Congress, which while limiting to $6.8 billion the amount of profits that the Fed can retain to boost its capital has also repeatedly “raided” the Fed’s capital to pay for various government programs, including $19 billion in 2015 for spending on highways.

Still, a negative net worth is sure to raise eyebrows especially after Janet Yellen said in December 2015 that “capital is something that I believe enhances the credibility and confidence in the central bank.”

* * *

Furthermore, as Bloomberg adds, if it had to the Fed could easily operate with negative net worth – as it is doing now – like other central banks in Chile, the Czech Republic and elsewhere have done, according to Nathan Sheets, chief economist at PGIM Fixed Income. That said, questionable Fed finances pose communications and mostly political problems for Fed policymakers.

As for long-time Fed critic and former Fed governor, Kevin Warsh, he zeroed in on the potential impact on quantitative easing.

“QE works predominantly through its signaling to financial markets,’’ he said. “If Fed credibility is diminished for any reason — by misunderstanding the state of the economy, under-estimating the power of QE’s unwind or carrying a persistent negative net worth — QE efficacy is diminished.’’

The biggest irony, of course, is that the more “successful” the Fed is in raising rates – and pushing bond prices lower – the greater the un-booked losses on its bond holdings will become; should they become great enough to invite constant Congressional oversight, the casualty may be none other than the equity market, which owes all of its gains since 2009 to the Federal Reserve.

While a central bank can operate with negative net worth, such a condition could have political consequences, Tobias Adrian, financial markets chief at the IMF said. “An institution with negative equity is not confidence-instilling,’’ he told a Washington conference on Nov. 15. “The perception might be quite destabilizing at some point.”

That point will likely come some time during the next two years as the acrimonious relationship between Trump and Fed Chair Jerome Powell devolves further, at which point the culprit by design, for what would be the biggest market crash in history will be not the Fed – which in the past decade blew the biggest asset bubble in history – but President Trump himself.

One week after even the IMF joined the chorus of warnings sounding the alarm over the unconstrained, unregulated growth of leveraged loans, and which as of November included the Fed, BIS, JPMorgan, Guggenheim, Jeff Gundlach, Howard Marks and countless others, we reported that investors had finally also joined the bandwagon and are now fleeing an ETF tracking an index of low-grade debt as credit spreads blow out and cracks appeared across virtually all credit products.

Specifically, we noted that not only had the $6.4 billion Invesco BKLN Senior Loan ETF seen seven straight days of outflows to close out November, with investors pulling $129 million in one day alone and reducing the fund’s assets by 2% to the lowest level in more than two years, but over 800 million has been pulled in last current month, the biggest monthly outflow ever as investors are packing it in.

Fast forward to today, when another major loan ETF, the Blackstone $2.9BN leverage-loan ETF, SRLN, just suffered its largest ever one-day outflow since its 2013 inception.

Year to date, the shares of this ETF backed by the risky debt have dropped 2.6%, hitting their lowest level since February 2016; the ETF’s underlying benchmark, the S&P/LSTA Leveraged Loan Index, has also been hit recently and is down 2.3% YTD, effectively wiping out all the cash interest carry generated YTD and then some.

BLKN and SRLN aren’t alone: investors have pulled over $4 billion from leveraged loan funds in the three weeks ended Dec. 5, the largest cash bleed in almost four years for such a period, according to Lipper data.

“The price action in the ETF hasn’t warranted investors to justify keeping it on to collect the monthly coupon it pays,” said Mohit Bajaj, director of exchange-traded funds at WallachBeth Capital. “The risk/reward hasn’t been there compared to short-term treasury products like JPST,” he added, referring to the $4.2 billion JPMorgan Ultra-Short Income ETF, which hasn’t seen a daily outflow since April 9.

Analysts have pointed to widening credit spreads and the fact that loan ETFs have floating-rate underlying instruments, assets that become less attractive than fixed-rate ones should the Fed skip its March rate hike, which after Powell’s latest dovish turn and today’s weak payrolls may – or may not – happen.

The ongoing loan ETF puke comes at a time when both US investment grade and junk bond spreads have blown out, while yields spiked to a 30-month high this month. In November, investment grade bonds suffered their worst year in terms of total returns since 2008 and December isn’t looking much better. Meanwhile in high yield, junk bonds yields just had their biggest one-day jump since April.

According to a note from Citi strategists Michael Anderson and Philip Dobrinov, leveraged loans in the U.S. may no longer be the “star performer” amid a potential pause in rate hikes by the Fed, while the recent redemption scramble has caused ETFs to offload better quality loans to raise cash, according to the Citi duo. That’s despite leveraged loan issuance being at its highest since 2008 largely as a result of insatiable CLO demand.

If investors are, indeed, unloading to raise cash, Anderson and Dobrinov write “this is a bearish sign, particularly if outflows persist and managers eventually turn to deep discount paper for cash. Furthermore, as we get closer to the end of the Fed’s hiking cycle, we expect further outflows as traditional fixed-rate credit products become more in vogue.”

Incidentally the behavior described by Citi’s strategists, in which ETF administrators first sell high quality paper then shift to deep discount holdings, was one of the catalysts that hedge fund manager Adam Schwartz listed three weeks ago as a necessary condition for credit ETFs to enter a “death spiral.” And with virtually everyone – including the Fed, BIS and IMF – all warning that the next crisis will begin in the leverage loan sector, the question to ask is “has it begun“?

One answer comes from the primary market, and it hardly reassuring.

As we discussed last week, while the leveraged-loan party isn’t quite over, jitters around the world have made lenders and investors less willing to give loans to heavily indebted companies, with numerous loan offerings getting pulled and lenders are demanding – and getting – sweeter terms.

As Bloomberg reports, on Tuesday JPMorgan had to slash the price on a $210 million loan to 93 cents on the dollar from par to sweeten investor demand and help finance a private jet takeover. Specifically, JPMorgan offloaded loans financing the takeover of XOJET at 93 cents on the dollar, one of the steepest discounts seen in the leveraged loan market this year. And with the market on the verge of freezing, the size of the deal was cut by $70 million from the originally targeted amount.

In Europe, the market appears to have already locked up, as three loans were scrapped over the last two weeks, victims of the Brexit tensions gripping the UK. To wit, movie theater chain Vue International withdrew a 833 million pound-equivalent ($1.07 billion) loan sale. While the deal was meant to mostly refinance existing debt, around 100 million pounds was underwritten to finance the company’s acquisition of German group CineStar.

Last week more deals were pulled when diversified manufacturer Jason Inc. became at least the fourth issuer to scrap a U.S. leveraged loan. Additionally, Perimeter Solutions also pulled its repricing attempt, Ta Chen International scrapped a $250MM term loan set to finance the company’s purchase of a rolling mill, and Algoma Steel withdrew its $300m exit financing. Global University System in November also dropped its dollar repricing.

Fears of a slowing global economic growth even as rates continue to rise, combined with anxiety over trade talks between the U.S. and China, reluctance to take risk before year end and the recent rout in credit products, have all led to a widespread fear across markets; investors are also concerned about higher interest rates weighing on corporate profits. These fears are spreading across credit markets, from investment-grade debt to junk bonds.

“No one thinks this is the big one,” said Richard Farley, chair of the leveraged finance group at Kramer Levin told Bloomberg. “But on the fear to greed continuum we have definitely moved closer to fear.”

The fear has resulted in the S&P/LSTA leverage loan price index tumbling to a two year low.

The sharp shift in sentiment has been remarkable: for most of 2018, investors couldn’t get enough of floating-rate products like leveraged loans based on the assumption that they will fare better in a rising-rate environment. As a result of blistering demand, companies were able to sell new debt with virtually no covenant protections and higher leverage, triggering warnings about deteriorating standards from regulators and bond graders in recent months (see above).

And, in the aftermath of Chair Powell infamous Oct 3 speech which sent risk assets tumbling and tightened financial conditions, leveraged loan price indexes in Europe and the U.S. have dropped to their lowest level in over two years, while nearly all of the loans outstanding are now trading below their face value. According to JPM, the percentage of loans trading above face value has dropped to just 3.9%, a 29-month low, down from 65.4% in early October. This suggests that virtually all leverage loan investors are now underwater on a total return basis.

* * *

With the leveraged loan market freezing up – and potentially entering a death spiral – the recent weakness has raised concerns that other debt sales currently in the works may be sold at discounts that are so deep underwriters may have to book a loss, if they can be sold at all. This is precisely what happened in late 2007 and early 2008 when underwriters found themselves with pipelines of debt sales that sudden got blocked, and were forced to take massive haircuts to keep the credit flowing.

Still, optimists remain: “The downdraft in loans has been very orderly thus far,” said Chris Mawn, head of the corporate loan business at investment manager CarVal Investors. “We anticipate most managers will keep buying in this market trying to be opportunistic and those who don’t have to sell will just hold.”

Of course, speaking of flashbacks to 2007/2008 it was just this kind of investor optimism that died last…

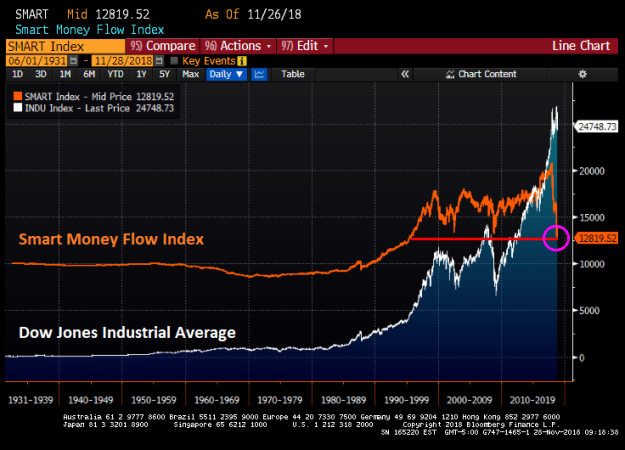

The Smart Money Flow Index, measuring the movement of the Dow in two time periods: the first 30 minutes and the last hour, has just declined AGAIN.

The Smart Money Flow Index, like the DJIA, has been around for decades. But it has just fallen to the lowest level since 1995.

Is the asset bubble starting to burst? Or is it just one lone indicator getting sick?

New Home Sales (SAAR) in September plunged to their lowest since Dec 2016, crashing 5.5% MoM (and revised dramatically lower in August)… Maybe Trump has a point on Fed rate hikes?

Remember this is the first month that takes the impact of the latest big spike in rates – not good!

This is a disastrous print:

August’s 629k SAAR was revised drastically lower to 585k and September printed 553k (SAAR) massively missing expectations of 625k (SAAR) – plunging to the weakest since Dec 2016…

That is a 13.2% collapse YoY – the biggest drop since May 2011

The median sales price decreased 3.5% YoY to $320,000…

New homes sales were down across all regions … except the midwest.

As the supply of homes at current sales rate rose to 7.1 months, the highest since March 2011, from 6.5 months.

The decline in purchases was led by a 40.6 percent plunge in the Northeast to the lowest level since April 2015 and 12 percent drop in the West.

Spooked by fears about peak profits, the slowing Chinese economy, Trump’s tariffs, ongoing political turmoil in the UK and Italy, and ongoing jitters among systematic, vol-targeting funds, on Tuesday the S&P tumbled as much as 2.34% in early trade – a drop which almost wiped out all gains for the year – before paring losses and closing only -0.55% lower. The drop pushed the S&P’s decline from its September highs to 6.5%, two-thirds on the way to a technical correction.

However the relatively stability at the index level has masked turmoil among individual names where some 1,256 stocks hit 52-week lows, while only 21 establishing new highs.

More concerning, and a testament to the tech-heavy leadership of the market concentrated amid just a handful of stocks, is that while the broader S&P 500 index has yet to enter a correction, more than three quarters of all S&P stocks – or 353 – have already fallen more than 10% from their highs. Worse, of those, more than half 179 have already fallen by 20% or more from their highs, entering a bear market.

The reason why the broader index has so far avoided a similar fate is because Apple, whose $1 trillion market value makes it by far the most heavily weighted stock within the S&P 500, has fallen only 4.6% from its October 3 record high. That has helped the S&P 500 itself stay out of correction territory.

Broken down by sector, the S&P 500 materials index – the closest proxy of Chinese economic growth – has fared the worst in October, leaving it down 19% from its 52-week highs, with the utilities index is the outperformer, down just 5 percent.

At the individual level, among the bottom 10 S&P 500 performers, are names likes Wynn Resorts and Western Digital, both highly exposed to China. Nektar Therapeutics and Newell Brands are also among the S&P 500’s worst performers.

Taking a step back, despite its relative resilience, the S&P 500 is still on track for its worst month since August 2015, while most global equities are down for the year. North America is still the best performing region with 67% of the six countries having benchmark equities trading higher on the year in US dollar terms, according to Deutsche Bank. In EMEA, only 23% of countries are up, and only 6% of countries in the European Union (in USD). In South American (6 countries) and Asia (18), not a single country has a positive return in USD terms this year.

One day later, and despite widespread call for an imminent market bounce, traders remain completely ambivalent as today’s market cash open action shows:

Meanwhile, the Nasdaq has a more negative tone with decliners outpacing advancers. In other words, as Bloomberg’s Andrew Cinko writes, “there’s no follow through on either the upside or the downside after yesterday’s epic rebound. At this moment, he who hesitates isn’t lost, in fact, he’s got a lot of company as stock market pundits engage in verbal duel over where we go from here.”

For those looking for key market inflection points, BMO’s Brad Wishak highlights a divergence that was a key tell for recent market action, and may portend even more pain in the coming weeks.

According to Wishak, one place that telegraphed the recent market turmoil was the venerable New York Stock Exchange: the NYSE is the worlds largest stock exchange by market cap (21 trillion) yet “seems to get very little main stream attention for reasons I’ll never understand.”

And, Wishak adds, “when the largest stock exchange in the world throws up a few negative divergences, I want to listen” for the following three reasons:

Emerging markets sold off anew Tuesday as South Africa entered a recession and Indonesia’s rupiah joined currencies from Turkey to Argentina in tumbling toward record lows, reinforcing concern that contagion risks are too big to ignore.

MSCI Inc.’s index of currencies dropped for a fifth time in six days, set for the lowest close in more than a year. The rand led global declines as data showed the economy fell into a recession last quarter. Turkey’s lira slid on worry the central bank will disappoint investors at its rate meeting next week, while the Argentine peso slumped to a record and Indonesian rupiah sank to the lowest in two decades even after the central bank intensified its fight to protect it.

The dollar extended its advance to a fourth day as Donald Trump threatened to ramp up a trade dispute with China with an announcement of tariffs on as much as $200 billion in additional Chinese products as soon as Thursday. As U.S. rates rise, investor fears over idiosyncratic risks in emerging markets have climbed, including Argentina’s fiscal woes, Turkey’s twin deficits, Brazil’s contentious elections and South Africa’s land-reform bill.

Meantime, the dollar is winning by default, according to Kit Juckes, a global strategist at Societe Generale SA.

“There’s not much to make me think the dollar should be going up, but there’s plenty to make me nervous about other currencies,” Juckes said. “The dollar is very strong and lacking rate support, but other currencies are worse.”

| HIGHLIGHTS: |

|---|

|

|

|

|

|

|

|

READ: JPMorgan Survey Shows How Quickly Emerging Markets Can Unravel

Here’s what other analysts are saying about the latest in emerging markets:

Tsutomu Soma, general manager for fixed-income trading at SBI Securities Co. in Tokyo:

Michael Every, head of Asia financial markets research at Rabobank in Hong Kong:

Lukman Otunuga, research analyst at FXTM:

Stephen Innes, head of Asia Pacific trading at Oanda Corp. in Singapore:

Masakatsu Fukaya, an emerging-market currency trader at Mizuho Bank Ltd.:

— With assistance by Tomoko Yamazaki, Yumi Teso, Lilian Karunungan, and Ben Bartenstein

Emerging market chaos is now front page news.

American corporations are simply raking in profits. Some are so bloated and cash-rich they literally can’t figure out what to do with it all. Apple, for instance, is sitting on nearly a quarter of a trillion dollars — and that’s down a bit from earlier this year. Microsoft and Google, meanwhile, were sitting on “only” $132 billion and $63 billion respectively (as of March this year).

However, American corporations in general are taking those profits and kicking them out to shareholders, mainly in the form of share buybacks. These are when a corporation uses profits, cash, or borrowed money to buy its own stock, thus increasing its price and the wealth of its shareholders. (Big Tech is doing this as well, just not fast enough to draw down their dragon hoards.) As a new joint report from the Roosevelt Institute and the National Employment Law Project by Katy Milani and Irene Tung shows, from 2015 to 2017 corporations spent nearly 60 percent of their net profits on buybacks.

This practice should be banned immediately, as it was before the Reagan administration.

The most immediately objectionable consequence of share buybacks is they come at the expense of wages. Milani and Tung calculate that if buybacks spending had been funneled into wage increases, McDonald’s employees could get a raise of $4,000; those at Starbucks could get $8,000; and those at Lowes, Home Depot, and CVS could get an eye-popping $18,000.

Some economists are skeptical of this reasoning, arguing that wages are set according to labor market conditions. But if you set aside free market dogmatism, it is beyond obvious that this sort of behavior is coming at workers’ expense. Wall Street bloodsuckers are not at all subtle about it, screaming bloody murder and tanking stocks every time a public company proposes paying workers instead of shareholders. Indeed, it provides a highly convincing explanation for something that has been puzzling analysts for months: the situation of wages continuing to stagnate or decline while unemployment is at 4 percent. The answer is that wages are low in large part because the American corporate structure has been rigged in favor of shareholders and executives.

This raises an objection: What about dividends? (These are payments made directly to shareholders, as opposed to buying stock to increase their price.) Wouldn’t banning buybacks just lead to increased dividends?

It might. But buybacks are worse, for three reasons. First, selling shares is generally counted as capital gains, which are usually (though not always) taxed at a much lower rate than dividend payments. Secondly, where dividends are regular occurrences, buybacks happen at erratic intervals, making it easier for huge payments to slip by unnoticed.

More importantly, share buybacks incentivize corporate short-termism and Wall Street predation. Making a quick buck at the expense of the underlying corporate enterprise is easy: simply pressure the company into spending all its money on buybacks — or more than all; Milani and Tung find the restaurant industry spent 136 percent of profits on buybacks from 2015-17, through cash and borrowing — then sell the stock once the price pops up. Money that might have gone into badly-needed investment or debt repayment is now in your pocket, and if the enterprise collapses later, who cares? Not your problem — you’re already on to the next victim.

Dividends, by contrast, are a lot more amenable to the value investor who wants the company to succeed over the long term. In general, banning buybacks will make it somewhat harder for corporations to be turned into a wealth funnel for the top 1 percent.

That said, dividends payments are also out of control — enabled by low top marginal tax rates and special loopholes, plus a powerless working class — and should be wrenched down as well. Banning buybacks should be considered the first step in reining in the outrageous abuse of the American corporate form, not a panacea.

Before about 2005, postwar corporate profits had never reached 9 percent of GDP (save for a couple quarters in the early 1950s). Immediately after the financial crisis, they bounced back up to that level, where they remain to this day.

This is a social crisis for the United States. Having an economy rigged to suck the wealth out of society and place it in the pockets of a tiny, already ultra-wealthy minority is an extremely risky situation for a democratic state. We need big, aggressive moves to club down corporate profits, and start directing that money back into the country as a whole. Banning buybacks is a simple and straightforward way to get started.

Two weeks ago, Goldman made a surprising finding: as of July 1, just one stock alone was responsible for more than a third of the market’s YTD performance: Amazon, whose 45% YTD return has contributed to 36% of the S&P 3% total return this year, including dividends. Goldman also calculated that the rest of the Top 10 S&P 500 stocks of 2018 are the who’s who of the tech world, and collectively their total return amounted to 122% of the S&P total return in the first half of the year.

And another striking fact: just the Top 4 stocks, Amazon, Microsoft, Apple and Netflix have been responsible for 84% of the S&P upside in 2018 (and yes, these are more or less the stocks David Einhorn is short in his bubble basket, which explains his -19% YTD return).

Now, in a review of first half performance, Bank of America has performed a similar analysis and found that excluding just the five FAANG stocks, the S&P 500 return in H1 would have been -0.7%; Staples (-8.6%) and Telco (-8.4%) were the worst.

FAANGs aside, here are the other notable sector observations about a market whose leadership has rarely been this narrow:

Looking at the entire first half performance, tech predictably was the biggest contributor to the S&P 500’s 1H gain, contributing 2.6ppt or 98% of the S&P 500’s 2.6% total return.

The broader market did ok: trade tensions, negative headlines, and the slow withdrawal of Fed liquidity contributed to volatility’s return in June and earlier in February, but the S&P 500 still ended 2Q +3.4% and the 1H +2.6%, outperforming bonds and gold.

The Russell 2000 led the Russell 1000 by 4.9ppt in the 1H as small caps may have benefitted from expectations of a stronger US economy, a strong USD and the sense that smaller more domestic companies are shielded from trade tensions (where we take issue with this notion). However, mega-caps also did well: the “Nifty 50” largest companies within the S&P 500 beat the “Not-so-nifty 450” in the 2Q and the 1H. Non-US performed worst.

Some additional return details by asset class:

Performance by quant groups:

The Russell 1000 Growth Index beat the Russell 1000 Value Index by 9ppt in the 1H, on track to exceed last year’s 17ppt spread. Growth factors were the best-performing group in the 1H (+6.7% on avg.), followed by Momentum factors. But Momentum broke down in June, and June saw the 56th worst month out of 60, -1.4 standard deviations from average returns.

What About Alpha?

Unfortunately for active managers, BofA notes that while pair-wise correlations remain lows, alpha remained scarce. The average pairwise correlation of S&P 500 stocks rose sharply in 1Q with the increased volatility which typically hurts stock pickers, but quickly came down below its long-term average of 26% in 2Q. However, performance dispersion (long-short alpha) continues to trail its long-term average.

What does this mean for active managers? According to BofA, never has the herding been this profound: since the bank began to track large cap fund holdings in 2008, managers have been increasing their tilts towards expensive, large, low dividend yield and low quality stocks. And today, their respective factor exposure relative to the S&P 500 is near its record level.

This is a risk because as we discussed recently, the threat is that as a result of an adverse surprise, “everyone” would be forced to sell at the same time. As BofA notes, “positioning matters more than fundamentals in the short-term, and this has been especially true around the quarter-end rebalancing. Since 2012, a long-short strategy of selling the 10 most overweight stocks and buying the 10 most underweight stocks by managers over the 15 days post-quarter-end would have yielded an average annualized spread of 90ppt, 15x higher than the average annualized spread of 6ppt over the full 90 days.”

Keep an eye on the first FAANG today when Netflix reports after the close.

Is Tesla The New Theranos?

I originally started following Tesla as I felt it was a structurally unprofitable business nearing a cash crunch as hundreds of competing products were about to enter the market.

As I’ve studied Tesla more closely, I’ve come to realize that Elon Musk appears to be running a Ponzi Scheme disguised as an auto-manufacturer; where he has to keep unveiling new products, many of which will never come to market, in order to raise new capital (equity/debt/customer deposits) to keep the scheme alive. The question has always been; when will Tesla collapse?

Tesla’s Bullshit Conversion Cycle is the key financial metric underlying this scheme (from @ProphetTesla)

Tesla’s Bullshit Conversion Cycle is the key financial metric underlying this scheme (from @ProphetTesla)

As part of my research on Tesla, I decided to read Bad Blood by John Carreyrou, the journalist who first uncovered the Theranos fraud. It is the story of how Elizabeth Holmes created Theranos and then lurched between publicity events in order to raise additional capital and keep the fraud going, despite the fact that the technology did not work. The key lesson from Theranos for determining when a fraud will implode is that there are always idiots willing to put fresh money into a well marketed fraud – so you need a catalyst for when the funding dries up.

The other salient fact was that most senior employees actually knew that something wasn’t quite right, but feared losing their jobs or getting sued if they did anything about it. Therefore, employee turnover was off the charts but no one was willing to risk their career by saying anything publicly. However, when Theranos started risking customers’ lives, the secret got out pretty fast. This is because most people are inherently ethical – especially when they know that their employer is doing something immoral, like releasing flawed lab results to sick patients. Eventually, some employees felt compelled to become whistle-blowers and started to reach out to journalists and regulators. This started a cascading event.

First, one intrepid journalist took the career risk to write about the Theranos fraud. Then other whistle-blowers felt emboldened to step forward and contact this first journalist, as they also wanted their story told – especially as they had already reached out to government regulators who were too scared to investigate a politically powerful company.

Once a few good articles had been written about Theranos, the dam broke open and the feeding frenzy began. Other journalists, smelling page-clicks rapidly descend on Theranos; more workers spoke out, more incriminating evidence came to light and then there was a sense of voter outrage. Finally, the regulators who were first contacted by the whistle-blowers many months previously, felt compelled to act – at which point the fraud collapsed and the money spigot shut off.

Executives Fleeing Tesla Is A True Bull Market “Up And To The Right”

Executives Fleeing Tesla Is A True Bull Market “Up And To The Right”

We’ve already seen the mass exodus of senior Tesla executives. When they say they “want to spend time with their family,” it really means they “want to spend less time in prison.” Next, we have the first whistle-blowers—there will be MANY more. Currently there are at least 3 different ones feeding information to journalists. Using past frauds as a guide, once we get to this point of the media cycle, the fraud usually unravels pretty fast. Given the perilous state of Tesla’s finances, they are in urgent need of new capital. The question is; who would want to invest new capital when Tesla is now admitting to knowingly selling cars without testing the brakes in order to hit some arbitrary one week production target? When a company admits that it will sacrifice vehicle quality and even risk killing its customers to win a twitter feud and start a short squeeze, regulators must step in. The question is; what else has Tesla done illegally to hit its targets? We know that Tesla long ago passed over the ethical threshold of selling faulty products that have killed people—what other allegations will soon come to light? Elon Musk demanded that Tesla stop testing brakes on June 26. Doug Field, chief engineer, resigned on June 27. Is this a coincidence? Of course not—Doug Field doesn’t want to be responsible for killing people. I think Tuesday’s article will speed up the pace of Tesla’s bankruptcy quite dramatically and I purchased some shorter dated puts after reading it.

Tesla is the fluke stock-promote that found a way to address society’s fascination with ‘green technology’ and the ‘next Steve Jobs.’ Elon Musk eagerly stepped into the role of mad scientist and investors gave him a free pass. It now increasingly seems that everything he’s done for the past few years was simply designed to keep the share price up, keep the dream alive and raise more capital – as opposed to creating shareholder value. Along the way, customer safety has been ignored in order to hit production targets and appease the stock market. In addition to not testing brakes, a recent whistle-blower has accused Tesla of installing over 700 dangerously defective batteries into Model 3 vehicles.

I suspect there will be many more allegations as whistle-blowers come out of the woodwork. It really is the Theranos of auto makers. I suspect it will all end soon. Theranos and Enron both collapsed within 90 days of the journalists getting up to speed. The reporters now know the right questions to ask and Tesla will be out of cash by the time they are all answered.

Stock Promotion In Overdrive Lately. What’s Elon Trying To Distract People From?

Stock Promotion In Overdrive Lately. What’s Elon Trying To Distract People From?

Besides, Elon Musk isn’t even all that innovative. Hitler already tried this same automotive customer deposit scam 80 years ago (From Wages of Destruction)

Source: ZeroHedge | Submitted by Kuppy Via AdventuresInCapitalism.com

The conditions at Tesla’s production facility leading up to meeting its Model 3 production goal have been reported as nothing short of hellish as Elon Musk “barked” at employees working 12 hour shifts, bottlenecking other parts of the company’s production and reportedly causing concern by employees that the long hours and strenuous environment would cause even more workplace injuries and accidents.

SocGen’s permabear skeptic Albert Edwards is best known for one thing: predicting that the financial world will end in a deflationary singularity, one which will send yields in the US deep in the negative, and which he first dubbed two decades ago as the “Ice Age.” He is also known for casually and periodically forecasting – as he did a few weeks ago in an interview with Barrons – that the S&P will suffer a historic crash, one which will send it back under the March 2009 low of 666.

In this context, a couple of recent events caught Edwards’ attention.

First, speaking of the above mentioned Barron’s interview, Edwards was taken aback by one commentator who took the SocGen strategist to task for his relentless bearishness. Indirectly responding to the reader, in his latest letter to clients Edwards writes that “its good to have a little humility in this business because its so darn humiliating when forecasts are proved wrong. And the bolder the forecast, the more humiliating it is!” He continues:

That is one reason why most commentators on the sell-side never stray too far from consensus. When I was an avid consumer of sell-side research some 30 years ago, there was one thing about the macro sell-side that I truly marvelled at namely the analysts ability to totally reverse a view and pretend that had been their view all along! In the days before the internet and email, I had to rifle through our storage cupboards to find the evidence of what were often 180 degree handbrake turns. In the internet age, there is no hiding any more.

One of the most leveling experiences at the end of an article or interview about my thoughts is to scroll down and read some of the readers comments. In my case, they often marvel that I am still in any sort of employment at all! Some are witty and make me smile - like the one below in response to a recent interview I did with Barrons.

Edwards refers to the comment titled “Prescient as a Broken Clock?” authored by one Gordon Gould from Boulder, Colorado who writes:

“Barron’s notes that Société Générale’s Albert Edwards is a permabear (“S&P 500 Could Still Test 2009 Lows,” Interview, April 7). However, your readers would surely like to know how some of his previous calls have turned out. A quick Google search revealed that nearly five years ago, Edwards called for the Standard & Poor’s 500 index to hit 450 and gold to exceed $10,000. While even a broken clock is correct twice a day, perhaps in Edwards’ case, we’re talking about a broken calendar on Saturn, which takes about 29 years to orbit the sun.”

Albert summarizes his response to this comment eloquently, using just one word: “ouch.” Hit to his pride aside, Albert asks rhetorically “Where did it all go so wrong?” and explains that in the Barrons interview, “I explain why in my Ice Age thesis I still expect US equity prices to fall to new lows in the next recession.” To be sure, this is familiar to ZH readers, as we highlight every incremental piece from Edwards, because no matter if one agrees or disagrees, he always provides the factual backing to justify his outlook, gloomy as it may be.

He explains as much:

I always expected the equity markets day of reckoning to come in a recession with equity valuations falling to lower lows than in the two previous cyclical bear market bottoms in 2001 and 2009. If I am right, the next recession will see a lower level than the forward PE of 10.5x in March 2009. A forward PE of 7x and a 30% decline in forward earnings would take the market to new lows as part of a long-term secular valuation bear market (which began in 2001). Then the stratospheric rise in the market over the past few years will be seen as just a temporary aberration fuelled by QE.

The moment of truth for my strategic Ice Age view will come when we know how far the equity bear market will fall in the next recession, or conversely whether the bond bull market will continue with 10y US yields, for example, falling into negative territory.

And yet, here we are a decade into central planning, and global stocks are just shy of all time highs. How come?

If I were to identify the major error that led me to be too bearish on equities, it would not be the inflationary impact of QE on asset prices. What I got wrong is that after the end of the Great Moderation, which saw an extended period of economic expansion from Dec 2001 to Dec 2007 as well as low financial volatility, triggering rampant credit growth I expected economic volatility to return to normal. The lesson from Japan I told clients was that once their Great Moderation died in 1990, the economic cycle returned to normal amplitude as private credit growth could no longer be induced to keep it going. Thus I expected that after the 2008 economic debacle the US economic cycle would return to normality and for recessions to become much more frequent events as they were in Japan after 1990. And as in Japan, I expected each rapidly arriving recession would take equity valuations down to new lower lows. After 2008, I expected the US economic recovery to quickly fall back into recession and the cyclical bull run in equities to be surprisingly short-lived. How wrong I was!

Indeed, because as Bank of America observed recently, every time the stock market threatened to tumble, central banks would step in: that, if anything, is what Edwards failed to anticipate. The rest is merely noise:

Despite the economy flirting with outright recession on a couple of occasions, this current recovery has endured to the point where we now have enjoyed the second longest economic cycle in US history. We have not returned to normal economic cycles as I had expected. QE has helped this, one of the most feeble economic recoveries in history, to also hobble into the record books for its length!

To be sure, Edwards will eventually get the last laugh as the constant, artificial interventions assure that the (final) crash will be unlike anything ever experienced: “a recession delayed is ultimately a recession deepened as more and more credit excesses have built up, Minsky-like, in the system.”

Then again, will it be worth having a final laugh if the S&P is hovering near zero, the fiat system has been crushed, modern economics discredited, and life as we know it overturned? We’ll cross that bridge when we come to it, for now however, Edwards has to bear the cross of his own forecasting indignities:

… having stepped away from the crazed run-up in equity prices, my reputation for calling the equity market correctly has been severely dented, if it is not actually in tatters. I know that.

Still, it’s not just Edwards. As the strategist notes, increasingly wiser heads than I, who did not leave the equity party early, are suggesting a top might be close. He then goes on to quote Mark Mobious who we first referenced earlier this week:

The renowned investor Mark Mobius is also getting nervous. The Financial Express reports that “After Jim Rogers recently warned of the ‘biggest crash in our lifetimes,’ veteran investor and emerging markets champion Mark Mobius warns of a severe stock market correction. “I can see a 30% drop. The market looks to me to be waiting for a trigger to tumble.” He then goes on in the article to cite some possible triggers.

To be fair, there are plenty of others who have recently and not so recently joined Edwards in the increasingly bearish camp (among them not only billionaire traders but economists and pundits like David Rosenberg and John Authers), although one thing missing so far has been the catalyst that will push the world out of its centrally-planned hypnosis and into outright chaos. Now, Edwards believes that this all important trigger has finally emerged:

Perhaps the greatest near-term threat to the stability of the equity markets is seen as the recent surge in bond yields, which are now testing the critical 3% technical level.

As this is so important, I want to repeat verbatim what our own Stephanie Aymes says on this point. She says, referring to the front page chart, the 10Y UST is marching towards the major support (price) of 3.00%/3.05% consisting of the multi-decade channel, 2013-2014 lows, and the 61.8% retracement of the 2009-2016 uptrend. Moreover, this is also the confirmation level of the multi-year Double Top, which if confirmed, would act as a catapult towards the 2-year channel limit at 3.33%/3.43%, and perhaps even towards 2009-2011 levels of 3.77%/4.00%, also the 50% retracement of the 2007-2016 up-cycle. The Monthly Stochastic indicator continues to withstand a pivotal decadal floor (blue line in chart) which emphasizes the relevance of the 3.00%/3.05% support.

So with everyone chiming in on the significance of the 3% breach in the 10Y, here is Edwards:

“Let me translate: 3% resistance is very strong but if broken, there is big trouble afoot!“

The irony, of course, is that yields blowing out is precisely the opposite of an Ice Age, although to Edwards the implication is simple: once stocks tumble, it will force the Fed to return to active management of markets and risk, and launch the next Fed debt monetization program which will culminate with the end of the current economic paradigm, and Edwards’ long anticipated collapse in risk assets coupled with the long-overdue arrival of the Ice Age.

Or maybe not, as Edwards’ parting words suggest:

I think, like Mark Mobius, that equities are looking for an excuse to sell off and the current rally may abruptly end for any number of reasons. Although I personally do not think it likely that US bonds can break much above 3%, if at all, I discount nothing given the clear end of cycle cyclical pressures that have built up. But if I am wrong on bonds and we have seen the end of the bond bull market, after having been wrong on equities, maybe it is time to think hard on what the Barrons correspondent said and take a sabbatical – maybe on Saturn.

And while we commiserate with Albert’s lament, it could certainly be worse: have you heard of Dennis Gartman?

Over the weekend, ZH looked at the notional amount of non-financial Libor-linked debt (so excluding the roughly $200 trillion in floating-rate derivatives which have little practical impact on the real world until there is a Lehman-like collateral chain break, of course at which point everyone is on the hook), to see what the real-world impact of the recent blow out in 3M USD Libor is on the business and household sector.

To this end, JPM calculated that based on Fed data, there is a little under $8 trillion in pure Libor-related debt…

… and that a 35bps widening in the LIBOR-OIS spread could raise the business sector interest burden by $21 billion. As we wondered previously, “whether or not that modest amount in monetary tightening is enough to “break” the market remains to be seen.”

In other words, unless the Fed – and JPMorgan – have massively miscalculated how much floating-rate debt is outstanding, and how much more interest expense the rising LIBOR will prompt, the ongoing surge in Libor and Libor-OIS, should not have a systemic impact on the financial system, or economy.

What about at the corporate borrower level?

In an analysis released on Monday afternoon, Goldman’s Ben Snider writes that while for equities in aggregate, rising borrowing costs pose only a modest headwind, “stocks with high variable rate debt have recently lagged in response to the move in borrowing costs.”

Goldman cautions that these stocks should struggle if borrowing costs continue to climb – which they will unless the Fed completely reverses course on its tightening strategy – amid a backdrop of elevated corporate leverage and tightening financial conditions.

Indeed, while various macro Polyannas have said to ignore the blowout in both Libor and Libor-OIS because, drum roll, they are based on “technicals” and thus not a system risk to the banking sector (former Fed Chair Alan Greenspan once called the Libor-OIS “a barometer of fears of bank insolvency”), what they forget, and what Goldman demonstrates is what many traders already know well: the share prices of companies with high floating rate debt has mirrored the sharp fluctuation in short-term borrowing costs. This is shown below in the chart of 50 S&P 500 companies with floating rate bond debt (i.e. linked to Libor) amounting to more than 5% of total.

Here are some details on how Goldman constructed the screen:

We exclude Financials and Real Estate, and the screen captures stocks from every remaining sector except for Telecommunication Services. So far in 2018, as short-term rates have climbed, these stocks have lagged the S&P 500 by 320 bp (-4% vs. -1%). The group now trades at a 10% P/E multiple discount to the median S&P 500 stock (16.0x vs. 17.6x). These stocks should struggle if borrowing costs continue to climb, but may present a tactical value opportunity for investors who expect a reversion in spreads. The tightening in late March of the forward-looking FRA/OIS spread has been accompanied by a rebound of floating rate debt stocks and suggests investors expect some mean-reversion in borrowing costs.

Goldman also notes that small-caps generally carry a larger share of floating rate debt than do large-caps, which may lead to a higher beta for the data set due to size considerations.

In any event, the inverse correlation between tighter funding conditions (higher Libor spreads) and the stock under performance of floating debt-heavy companies is unmistakable.

Finally, traders who wish to hedge rising Libor by shorting those companies whose interest expense will keep rising alongside 3M USD Libor, in the process impairing their equity value, here is a list of the most vulnerable names.

Money manager Michael Pento says the biggest unreported story is the skyrocketing interest rate of LIBOR. What’s that? Pento explains, “LIBOR, and people don’t understand or talk about it, is the London Inter-Bank Offered Rate. This rate has gone from 0.3% at the end of 2015 to 2.3% today. The London Inter-Bank Offered Rate is the rate that is applied to $370 trillion of loans and derivatives and loans, from credit cards, to student loans, to auto loans are priced off of LIBOR. . . That is the biggest reason why the stock market is rolling over because the cost of borrowing money. . . is going up very, very sharply. . . All of this is going to hit a crescendo in October of 2018.” Pento Says gold prices are going way up because the Fed will no be able to raise interest rates.

Only one thing matters in bubble markets: sentiment

Yesterday saw Jerome Powell sworn into office as the new Chairman of the Federal Reserve, replacing Janet Yellen. Looking at the sea of red across Monday’s financial markets, Mr. Powell is very likely *not* having the sort of first day on the job he was hoping for…

Jerome H. Powell, new Chairman of the Federal Reserve.

Jerome H. Powell, new Chairman of the Federal Reserve.Also having a rough start to the week is anyone with a long stock position or a cryptocurrency portfolio.

The Dow Jones closed down over 1,200 points today, building off of Friday’s plunge of 666 points. The relentless ascension of stock prices has suddenly jolted into reverse, delivering the biggest 2-day drop stocks have seen in years.

But that’s nothing compared to the bloodletting we’re seeing in the cryptocurrency space. The price of Bitcoin just broke below $7,000 moments ago, now nearly two-thirds lower from its $19,500 high reached in mid-December. Other coins, like Ripple, are seeing losses of closer to 80% over the same time period. That’s a tremendous amount of carnage in such a short window of time.

And while stocks and cryptos are very different asset classes, the underlying force driving their price corrections is the same — a change in sentiment.

Both markets had entered bubble territory (stocks much longer ago than the cryptos), and once they did, their continued price action became dependent on sentiment much more so than any underlying fundamentals.

History is quite clear on how bubble markets behave.

On the way up, a virtuous cycle is created where quick, out sized gains become the rationale that attracts more capital into the market, driving prices up further and even faster. A mania ensues where everyone who missed out on the earlier gains jumps in to buy regardless of the price, desperate not to be left behind (this is called fear of missing out, or “FOMO”).

This mania produces a last, magnificent spike in price — called a “blow-off” top — which is then immediately followed by an equally sharp reversal. The reversal occurs because there are simply no remaining new desperate investors left to sell to. The marginal buyer has suddenly switched from the “greater fool” to the increasingly cautious investor.

Those sitting on early gains and looking to cash out near the top start selling. They don’t mind dropping the price a bit to get out. So the price continues downwards, spooking more and more folks to start selling what they have. Suddenly, the virtuous cycle that drove prices to their zenith has now metastasized into a vicious cycle of selling, driving prices lower and lower as panicking investors give up on their dreams of easy riches and increasingly scramble to limit their mounting losses.

In the end, the market price retraces nearly all of the gains made, leaving a small cadre of now-rich early investors who managed to get out near the top, and a large despondent pool of ‘everyone else’.

We’ve seen this same compressed bell-curve shape in every major asset bubble in financial history:

And we’re seeing it play out in real-time now in both stocks and cryptos.

It’s amazing how fast asset price bubbles can pop.

Just a month ago, the Internet was replete with articles proclaiming the new age of cryptocurrencies. Every day, fresh stories were circulated of individuals and companies making overnight fortunes on their crypto bets, shaking their heads at all the rubes who simply “didn’t get” why It’s different this time.

Here at PeakProsperity.com the demand for educational content on cryptocurrencies from our audience rose to a loud crescendo.

We did our best to provide answers as factually as we could through articles and webinars, though we tried very hard not to be seen as encouraging folks to pile in wantonly. A big reason for this is we’re more experienced than most in identifying what asset bubbles look like.

After all, we *are* the ones who produced Chapter 17 of the The Crash Course: Understanding Asset Bubbles: