(Peter St Onge, Ph.D) The Federal Reserve has been gas lighting the American people for two years now on inflation in the economy. At this point the happy talk is hitting reality with the latest Empire State manufacturing survey, a bellwether for conditions across the country showing its biggest plunge ever, second only to the month they literally shut down the economy for COVID-19. Economists had expected a minus five on the survey. A minus means the economy is contracting. The actual number was minus 31.

(E.J. Antonio) Following the 2008 global financial crisis, the Federal Reserve created trillions of dollars to ease financial conditions and keep banks afloat. Many economists predicted record inflation would result. Continue reading →

Target down 25% TODAY. Walmart down 14% between YESTERDAY and TODAY, represents the single largest drops for these companies since the market crash of 1987.

Working class Americans have never been hammered this hard by government fiscal policy.

“2nd CIVIL WAR… The Republicrats, the globalists are raging an ALL OUT WAR against us…Continue reading →

(Bryan Jung) Commodities prices could rise by 40 percent and will likely continue to go higher, according to a note from JPMorgan Chase from April 7, as raw materials hit a record high last month following Western sanctions on Russia due to its invasion of Ukraine.

Russia is a main supplier for up to 10 percent of global energy production and about 20 percent of global wheat production.

Just days after Germany reported the highest inflation in generation (with February headline CPI soaring at a 7.6% annual pace and blowing away all expectations), giving locals a distinctly unpleasant deja vu feeling even before the Russian invasion of Ukraine broke what few supply chains remained and sent prices even higher into the stratosphere…

Over the past few months we have repeated a statement which – because it is controversial and because it is true – sparked feigned outrage among the financially illiterate macrotourists (which these days is the vast majority of the financial commentariat): we said that in light of the galloping inflation which has crushed BIden’s approval ratings and has ensured a landslide loss for Democrats in the midterms, the Fed desperately wants to create a recession (and, at this rate, it will get it).

Fed wants recession. It will get it in a few months.

Credit Suisse short-term rate strategist Zoltan Pozsar also said the new order would weaken the US dollar and create higher inflation in the western world.

(Jocelyn Fernandez) Credit Suisse short-term rate strategist Zoltan Pozsar, a former United States Federal Reserve and US Treasury Department official, in a report said the US is in a commodity crisis and this will give rise to a new world order that will weaken the US dollar and create higher inflation in the western world.

(Sundance) The Bureau of Labor and Statistics (BLS) released the August review [DATA HERE] of producer prices for last month. August rose 0.7% with cumulative results now showing an 8.3% increase in prices; the largest year-over-year jump in prices for final demand products in the history of tracking. The prior record was July with 7.8%.

Surging construction costs to build a new home is not sustainable and is becoming a pain in the arse for home builders and prospective home buyers. From concrete to lumber to copper pipes to paint and even appliances, costs have surged over the past year.

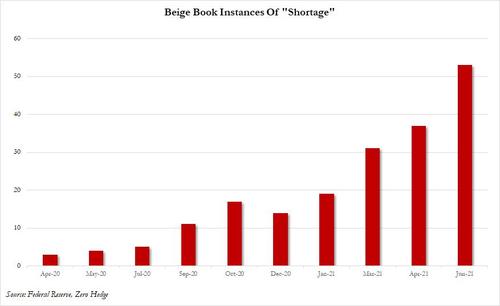

With the economy overheating, it will hardly come as a surprise that the latest Fed Beige Book – which found that the economy expanded at what the Fed absurdly called a “moderate pace” from early April to late May, at least clarifying that this was a “somewhat faster” rate than the prior reporting period – one of the top concerns was soaring costs, but nothing spooked the various Fed districts quite as much as what appears to be a shortage of everything, with district after district complaining about broken supply chains, a lack of workers, and critical commodities that just can’t be procured, all resulting in sharply higher prices, slower delivery times and all around chaos.

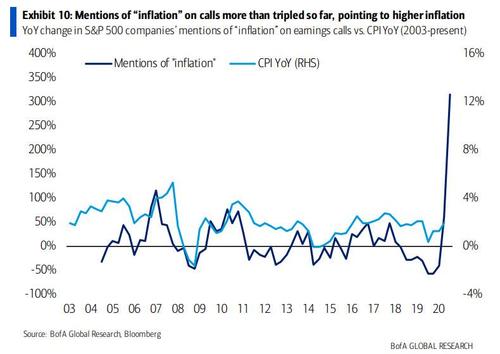

Last Wednesday, ZeroHedge reported that based on recent earnings calls, “Companies Are Freaking Out About Soaring Costs“ and today they received more confirmation of this in a Bank of America report which warns that Inflation is:

“arguably the biggest topic during this earnings season, with a broad array of sectors (Consumer/Industrials/Materials) citing inflation pressures.”

Exhibit A: the chart below showing the number of mentions of “inflation” during earnings calls which exploded, more than tripling YoY per company so far, the and the biggest jump in history since BofA started keeping records in 2004.

Following the explosive surge in producer prices, analysts expected a similar jump in consumer prices and were not disappointed as headline CPI jumped 0.6% MoM (+0.5% exp) and 2.6% YoY (+2.5% exp).

This is the biggest MoM jump since June 2009 and biggest YoY jump since Aug 2018, as CPI follows PPI higher.

The numbers: The producer price index rose 1% in March, the U.S. Labor Department said Friday. Economists polled by the Wall Street Journal had forecast a 0.5% rise.

The rate of wholesale inflation over the past 12 months climbed to 4.2% in March. That’s the highest level since September 2011. Because PPI was so weak last spring, increases this year are going to push the annual readings higher for at least a few months.

After China’s factory inflation surprised to the upside with the hottest print since July 2018, this morning’s US producer price data was highly anticipated and expected to surge to multi-year highs.

And when it hit it was dramatically hotter than expected, printing up 1.0% MoM (vs +0.5% exp) and a stunning 4.2% rise YoY (+3.8% exp) – the highest since 2011…

(Peter Schiff) Since the beginning of the pandemic, government debt and money printing are off the chart. This is creating inflationary pressure. Prices are on the rise. And this is by design. In fact, the Fed has been promising more inflation for years. As Peter Schiff explains, it looks like this is one promise the Fed is going to keep.

In Wednesday’s press conference, Jay Powell confirmed that the Fed is setting off on a historic experiment: welcoming a conflagration of red-hot inflation for an indefinite period of time in an overheating economy, with the underlying assumption that it’s all “transitory” and that inflation will return to normal in a few years, and certainly before 2023 when the Fed’s rates will still be at zero.

There is a big problem with that assumption: while FOMC members, most of whom are independently wealthy and can just charge their Fed card for any day to day purchases of “non-core” CPI basket items, the vast majority of the population does not have the luxury of having someone else pay for their purchases or looking beyond the current period of runaway inflation, which will certainly crush the purchasing power of the American consumer, especially once producers of intermediate goods start hiking prices even more and passing through inflation.

(Neils Christensen) The debate between goldand bitcoin, as to which is the ultimate safe-haven and inflation hedge, continued to rage this past week. However, I feel that the longer this debate goes on, the more investors are missing the bigger picture.

The stark reality is that there is more than $16 trillion worth of negative-yielding debt floating around the world right now. The U.S. government continues to move forward with its proposed $1.9 trillion stimulus package to support the U.S. economy. The Federal Reserve’s balance sheeting grows from record high to record high, pushing above $7.4 trillion.

The U.S. also isn’t in this boat alone; central banks around the world are maintaining extremely accommodative monetary policies and growing their balance sheets to record levels.

And here it is. THIS is how The Fed is going to finish it, via an EPIC binge of money creation unlike ANYTHING that has been seen before. The effect of this will be much higher prices of Gold, Silver, Crypto, Crude, AND Stocks…

The Fed Is Expected To Make A Major Commitment To Ramping Up Inflation Soon

(Jeff Cox) In the next few months, the Federal Reserve will be solidifying a policy outline that would commit it to low rates for years as it pursues an agenda of higher inflation and a return to the full employment picture that vanished as the coronavirus pandemic hit.

Recent statements from Fed officials and analysis from market veterans and economists point to a move to “average inflation” targeting in which inflation above the central bank’s usual 2% target would be tolerated and even desired.

To achieve that goal, officials would pledge not to raise interest rates until both the inflation and employment targets are hit. With inflation now closer to 1% and the jobless rate higher than it’s been since the Great Depression, the likelihood is that the Fed could need years to hit its targets.

The policy initiatives could be announced as soon as September. Addressing the issue last week, Fed Chairman Jerome Powell said only that a yearlong examination of policy communication and implementation would be wrapped “in the near future.” The culmination of that process, which included public meetings and extensive discussions among central bank officials, is expected to be announced at or around the Federal Open Market Committee’s meeting.

Markets are anticipating a Fed that would adopt an even more accommodative approach than it did during the Great Recession.

“We remain firmly of the view that this is a deeply consequential shift, even if it is one that has been seeping into Fed decision-making for some time, that will shape a different Fed reaction function in this cycle than in the last,” said Krishna Guha, head of global policy and central bank strategy at Evercore ISI.

Indeed, Powell said the policy statement will be “really codifying the way we’re already acting with our policies. To a large extent, we’re already doing the things that are in there.”

Guha, though, said the approach “would be sharply more dovish even than the strategy followed by the [Janet] Yellen Fed” when the central bank held rates near zero for six years even after the end of the Great Recession.

All in on inflation

One implication is that the Fed would be slower to tighten policy when it sees inflation rising.

Powell and his colleagues came under fire in 2018 when they enacted a series of rate increases that eventually had to be rolled back. The Fed’s benchmark overnight lending rate is now targeted near zero, where it moved in the early days of the pandemic.

The Fed and other global central banks have been trying to gin up inflation for years under the reasoning that a low level of price appreciation is healthy for a growing economy. They also worry that low inflation is a problem that feeds on itself, keeping interest rates low and giving policymakers little wiggle room to ease policy during downturns.

In the latest shot at getting inflation going, the Fed would commit to enhanced “forward guidance,” or a commitment not to raise rates until its benchmarks are hit and, in the case of inflation, perhaps exceeded.

In recent days, Fed regional Presidents Robert Kaplan of Dallas and Charles Evans of Chicago have expressed varying levels of support for enhanced guidance. Evans in particular said he would like to keep rates where they are until inflation gets up around 2.5%, which it has not been for most of the past decade.

“We believe that the Fed publicly would welcome inflation in a range of 2% up to 4% as a long overdue offset to inflation running below 2% for so long in the past,” said Ed Yardeni, head of Yardeni Research.

The market weighs in

The investing implications are substantial.

Yardeni said the approach would be “wildly bullish” for alternative asset classes and in particular growth stocks and precious metals like gold and silver. Guha said the Fed’s moves would see “real yields persistently lower, the dollar lower, volatility lower, credit spreads lower and equities higher.”

Investors have been making heavy bets that would be consistent with inflation: record highs in gold, sharp declines in the U.S. dollar and a rush into TIPS, or Treasury Inflation Protected Securities. TIPS funds have seen six consecutive weeks of net inflows of investor cash, including $1.9 billion and $1.5 billion respectively during the weeks of June 24 and July 1 and $271 million for the week ended July 29, according to Refinitiv.

Still, the Fed’s poor record in reaching its inflation target is raising doubts.

“If there’s any lesson that should have been learned by all the world’s central banks it’s that picking an inflation target is easy. Trying to actually get there is extraordinarily difficult,” said Peter Boockvar, chief investment officer at Bleakley Advisory Group. “Just manipulating interest rates doesn’t mean you get to some finger-in-the-air inflation rate that you choose.”

“It doesn’t make any economic sense whatsoever,” he said. “The consumer is very fragile right now. The last thing we should be shooting for is a higher cost of living.”

“You have enormous buyers of debt meeting massive coordinated fiscal stimulus by governments across the globe. For bond investors, you’re caught between a rock and a hard place.”

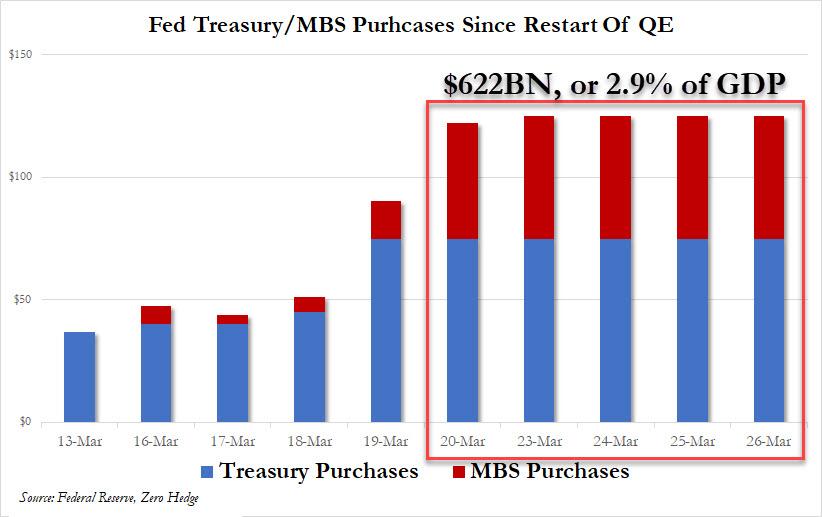

With the Fed buying $622 billion in Treasury and MBS, a staggering 2.9% of US GDP, in just the past five days…

… any debate what to call the current phase of the Fed’s asset monetization – “NOT NOT-QE”, QE4, QE5, or just QEternity – can be laid to rest: because what the Fed is doing is simply Helicopter money, as it unleashes an unprecedented debt – and deficit – monetization program, one which is there to ensure that the trillions in new debt the US Treasury has to issue in the coming year to pay for the $2 (or is that $6) trillion stimulus package find a buyer, which with foreign central banks suddenly dumping US Treasuries…

… would otherwise be quite problematic, even if it means the Fed’s balance sheet is going to hit $6 trillion in a few days.

The problem, at least for traders, is that this new regime is something they have never encountered before, because during prior instances of QE, Treasuries were a safe asset. Now, however, with fears that helicopter money will unleash a tsunami of so much debt not even the Fed will be able to contain it resulting in hyperinflation, everything is in flux, especially when it comes to triangulating pricing on the all important 10Y and 30Y Treasury.

Indeed, as Bloomberg writes today, core investor tenets such as what constitutes a safe asset, the value of bonds as a portfolio hedge, and expectations for returns over the next decade are all being thrown out as governments and central banks strive to avert a global depression.

And as the now infamous “Money Printer go Brrr” meme captures so well, underlying the uncertainty is the risk that trillions of dollars in monetary and fiscal stimulus, and even more trillions in debt, “could create an eventual inflation shock that will trigger losses for bondholders.”

Needless to say, traders are shocked as for the first time in over a decade, they actually have to think:

“You have enormous buyers of debt meeting massive coordinated fiscal stimulus by governments across the globe. For bond investors, you’re caught between a rock and a hard place.”

And while equity investors may be confident that in the long run, hyperinflation results in positive real returns if one sticks with stocks, the Weimar case showed that that is not the case. But that is a topic for another day. For now we will focus on bond traders, who are finding the current money tsunami unlike anything they have seen before.

Indeed, while past quantitative easing programs have led to similar concerns, this emergency response is different because it’s playing out in weeks rather than months and limits on QE bond purchases have quickly been scrapped.

Any hope that the Fed will ease back on the Brrring printer was dashed when Fed Chairman Jerome Powell said Thursday the central bank will maintain its efforts “aggressively and forthrightly” saying in an interview on NBC’s “Today” show that the Fed will not “run out of ammunition” after promising unlimited bond purchases. His comments came hours after the European Central Bank scrapped most of the bond-buying limits in its own program.

The problem is that while this type of policy dominates markets, fundamental analysis scrambling to calculate discount rates and/or debt in the system fails, and “strategic thinking is stymied and some prized investment tools appear to be defunct”, said Ronald van Steenweghen of Degroof Petercam Asset Management.

“Valuation models, correlation, mean reversion and other things we rely on fail in these circumstances,” said the Brussels-based money manager. Oh and as an added bonus, “Liquidity is also very poor so it is difficult to be super-agile.”

The irony: the more securities the Fed soaks up, be they Treasuries, MBS, Corporate bonds, ETFs or stocks, the worse the liquidity will get, as the BOJ is finding out the hard way, as virtually nobody wants to sell their bonds to the central bank.

Another irony: normally the prospect of a multi-trillion-dollar government spending surge globally ought to send borrowing costs soaring. But central bank purchases are now reshaping rates markets – emulating the Bank of Japan’s yield-curve control policy starting in 2016 – and quashing these latest volatility spikes.

In effect, the Fed’s takeover of bond markets (and soon all capital markets), means that any signaling function fixed income securities have historically conveyed, is now gone, probably for ever.

“Investors shouldn’t expect to see much more than moderately steep yield curves, since the Fed and its peers don’t want higher benchmark borrowing costs to undermine their stimulus,” said Blackrock strategist Scott Thiel. “That would be detrimental to financial conditions and to the ability for the stimulus to feed through to the economy. So the short answer is, it’s yield-curve control.”

Said otherwise, pretty soon the entire yield curve will be completely meaningless when evaluating such critical for the economy conditions as the price of money or projected inflation. They will be, simply said, whatever the Fed decides.

And with the yield curve no longer telegraphing any inflationary risk, it is precisely the inflationary imbalances that will build up at an unprecedented pace.

Additionally, when looking further out, Bloomberg notes that money managers need to reassess another assumption that’s become widely held in recent years: that inflation is dead. Van Steenweghen says he’s interested in inflation-linked bonds, though timing a foray into that market is “tricky.”

Naeimi also said he expects that the coordination by central banks and governments will spike inflation at some stage. “It all adds to the volatility of holding bonds,” he said. But for the time being, he’s range-trading Australian bonds — buying when 10-year yields hit 1.5%, and selling at 0.6%.

That’s right: government bonds have become a daytrader’s darling. Whatever can possibly go wrong.

But the biggest fear – one we have warned about since 2009 – is that helicopter money, which was always the inevitable outcome of QE, will lead to hyperinflation, and the collapse of both the US Dollar, and the fiat system, of which it is the reserve currency. Bloomberg agrees:

Many market veterans agree that faster inflation may return in a recovery awash with stimulus that central banks and governments may find tough to withdraw. A reassessment of consumer-price expectations would be a major setback for expensive risk-free bonds, especially those with the longest maturities, which are most vulnerable to inflation eroding their value over time.

Of course, at the moment that’s hard to envisage, with market-implied inflation barely at 1% over the next decade, but as noted above, at a certain point the bond market no longer produces any signal, just central bank noise, especially when, as Bloomberg puts it, “central bank balance sheets are set to explode further into unchartered territory.” Quick note to the Bloomberg editors: it is “uncharted”, although you will have plenty of opportunity to learn this in the coming months.

Alas, none of this provides any comfort to bond traders who no longer have any idea how to trade in this new “helicopter normal“, and thus another core conviction is being revised: the efficacy of U.S. Treasuries as a safe haven and portfolio hedge.

Mark Holman, chief executive and founding partner of TwentyFour Asset Management in London, started questioning that when the 10-year benchmark hit its historic low early this month.

“Will government bonds play the same role in your portfolio going forward as they have in the past?” he said. “To me the answer is no they don’t — I’d rather own cash.”

For now, Mark is turning to high-quality corporate credit for low-risk income, particularly in the longer maturity bonds gradually rallying back from a plunge, especially since they are now also purchased by the Fed. He sees no chance of central banks escaping the zero-bound’s gravitational pull in the foreseeable future. “What we do know is we’re going to have zero rates around the world for another decade, and we’re going to have the need for income for another decade,” he said.

Other investors agree that cash is the only solution, which is why T-Bills – widely seen as cash equivalents – are now trading with negative yields for 3 months and over.

Yet others rush into the safety of gold… if they can find it. At least check, physical gold was trading with a 10% premium to paper gold and rising fast.

Ultimately, as Bloomberg concludes, investors will have to find their bearings “in a crisis without recent historical parallel.”

“It’s very hard to look at this in a historical context and then apply an investment framework around it,” said BlackRock’s Thiel. “The most applicable period is right before America entered WW2, when you had gigantic stimulus to spur the war effort. I mean, Ford made bombers in WW2 and now they’re making ventilators in 2020.”

On Wednesday, the Fed cut rates for the third time this year, which was widely expected by the market.

What was not expected was the following statement.

“I think we would need to see a really significant move up in inflation that’s persistent before we even consider raising rates to address inflation concerns.”

– Jerome Powell 10/30/2019

The statement did not receive a lot of notoriety from the press, but this was the single most important statement from Federal Reserve Chairman Jerome Powell so far. In fact, we cannot remember a time in the last 30 years when a Fed Chairman has so clearly articulated such a strong desire for more inflation.

Why do we say that? Let’s dissect the bolded words in the quote for further clarification.

“really significant”– Powell is not only saying that they will allow a significant move up in inflation but going one better by adding the word significant.

“persistent”– Unlike the prior few Fed Chairman who claimed to be vigilant towards inflation, Powell is clearly telling us that he will not react to inflation that is not only well beyond a “really significant” leap from current levels, but a rate that lasts for a period of time.

“even consider”– If inflation is not only a really significant increase from current levels and stays at such levels for a while, they will only consider raising rates to fight inflation.

We are stunned by the choice of words Powell used to describe the Fed’s view on inflation. We are even more shocked that the markets or media are not making more of it.

Maybe, they are failing to focus on the three bolded sections. In fact, what they probably think they heard was: I think we would need to see a move up in inflation before we consider raising rates to address inflation concerns. Such a statement would have been more in line with traditional “Fed-speak.”

There is an other far more insidious message in Chairman Powell’s statement which should not be dismissed.

The Fed just acknowledged they are caught in a “liquidity trap.”

When an economy turns from expansion to contraction there is an order of events. The first signs are an unexpected increase in inventories of unsold goods, both accompanied with and followed by business surveys indicating a general softening in demand. For monetarists, this is often confirmed by an inverting yield curve, which tells them that at the margin the short-term rates set by the central bank are becoming too high for business conditions.

That was the position for the US 10-year bond less the 2-year bond very briefly at the end of August, since when this measure, which is often taken to predict recessions, has turned mildly positive again. A generally negative sentiment, fueled mainly by the escalating tariff war between America and China, had earlier alerted investors to an international trade slowdown, expected to undermine the American economy in due course along with all the others. It stands to reason that backward-looking statistics have yet to reflect the global slowdown on the US economy, which is still buoyed up by consumer credit. The German economy, which is driven by production rather than consumption is perhaps a better guide and is already in recession.

So reliant have markets become on monetary expansion that the default assumption is that an economy will always be rescued from recession by an easing of monetary policy, and furthermore that monetary inflation will prevent it from being any more than mild and short. We see this in the performance of stock market indices, which reflect perpetual optimism.

There is a further problem. Other than a rise in bankruptcies, unemployment and negative indications from business surveys, there may be no statistical evidence of a slump. The reason this is almost certainly the case is we are dealing with a combination of funny money and statistics which are simply not fit for measuring anything. The money and credit are backed by nothing, and when expanded by the banking system simply dilutes the quantity of existing money, which if continued is bound to end up impoverishing everyone with cash balances and whose wages and profits do not increase at least as fast as the surge in the quantity of money.

Indeed, the official purpose of the expansion of money and credit is to somehow persuade economic actors that things are better than they really are, and to stimulate those animal spirits. You’d think that with this policy now being continually in operation that people would have become aware of the dilution fraud. But as Keynes, the architect of it all said, not one man in a million understands money, and in this he has been proved right.

For five years, the ECB has applied negative interest rates on commercial bank reserves, and commercial banks have paid €21.4bn to it in deposit interest. Since it introduced negative interest rates, it has injected some €2.7 trillion of base money into the Eurozone economy, increasing M1, the narrower measure of the money quantity, by 61%. Almost all of it has supported the finances of Eurozone governments.

The effect on broader money, which includes bank credit, has been to increase M3 by 30%. Far from stimulation, this is daylight robbery perpetrated on everyone’s liquidity and cash deposits. It is a tax on the purchasing power of their wages.

The ECB is not alone. Since Lehman went under, the major central banks have collectively increased their balance sheets from $7 trillion to $19.4 trillion, an increase of 177%. Most of this monetary expansion has been to buy government bonds, providing a money-fountain for profligate governments. The purpose of money-printing is always to finance government spending, not to stimulate or ease conditions for the private sector: while some trusting souls in the system believe it is for the latter, that amounts to just a myth.

Due to the flood of new money the yields on government debt have been depressed, giving holders of this debt, principally the banks, a nice fat capital profit. But that is not the purpose of all this monetary largess: it is to make it ultra-cheap for governments to borrow yet more and to encourage banks to expand credit in their governments’ favor. Just listen to the central bankers now encouraging governments to take the opportunity to ease fiscal policy, extend their debts and borrow even more.

Central banks pretend all these benefits come at no cost to anyone. Unfortunately, there is no such thing as a perpetual motion of money creation, and someone ultimately pays the price. But who pays for it all? Why, it is the wage-earner and saver and anyone else with deposits at the bank. They are also robbed of the compounding interest their pension funds would otherwise receive. These are the very people who, in a bizarre twist of macroeconomic logic, we are told benefit from having the prices of their everyday purchases continually increased.

Attempts to measure the supposed benefits of inflation on the general public are in turn dishonest, with the true rise in prices concealed in official calculations of price inflation. Suppressed evidence of rising prices is then applied to estimates of GDP to make them “real”. For the purpose of measuring the true condition of an economy these official statistics are taken as gospel by both the commentariat and investors.

We cannot know the accumulating economic cost of cycles of progressively greater monetary inflation, because all government statistics are based on the lie that money is a constant, when in fact it has become the greatest variable in everyone’s life. The transfer of wealth from all consumers through monetary debasement is an act of impoverishment, and to the extent it is not offset in other ways the economy as a whole suffers.

“It’s pretty eye-popping if you’ve been doing this for 20-plus years, to see how much more leverage a number of these companies can incur with the same credit rating.”

Inflation? Deflation? Stagflation? Consecutively? Concurrently?… or from a great height.

We’ve reached a pivotal moment where all of the narratives of what is actually happening have come together. And it feels confusing. But it really isn’t.

How can we stuff fake money onto more fake balance sheets to maintain the illusion of price stability?

The consequences of this coordinated policy to save the banking system from itself has resulted in massive populist uprisings around the world thanks to a hollowing out of the middle class to pay for it all.

The central banks’ only move here is to inflate to the high heavens, because the civil unrest from a massive deflation would sweep them from power quicker.

For all of their faults leaders like Donald Trump, Matteo Salvini and even Boris Johnson understand that to regain the confidence of the people they will have to wrest control of their governments from the central banks and the technocratic institutions that back them.

That fear will keep the central banks from deflating the global money supply because politicians like Trump and Salvini understand that their central banks are enemies of the people. As populists this would feed their domestic reform agendas.

So, the central banks will do what they’ve always done — protect the banks and that means inflation, bailouts and the rest.

At the same time the powers that be, whom I like to call The Davos Crowd, are dead set on completing their journey to the Dark Side and create their transnational superstructure of treaties and corporate informational hegemony which they ironically call The Open Society.

This means continuing to use whatever powers are at their disposal to marginalize, silence and outright kill anyone who gets in their way, c.f. Jeffrey Epstein.

But all of this is a consequence of the faulty foundation of the global financial system built on fraud, Ponzi schemes and debt leverage… but I repeat myself.

And once the Ponzi scheme reaches its terminal state, once there are no more containers to stuff more fake money into the virtual mattresses nominally known as banks, confidence in the entire system collapses.

It’s staring us in the face every day. The markets keep telling us this. Oil can’t rally on war threats. Equity markets tread water violently as currencies break down technically. Gold is in a bull market. Billions flow through Bitcoin to avoid insane capital controls.

Any existential threat to the current order is to be squashed. It’s reflexive behavior at this point. But, as the Epstein murder spotlights so brilliantly, this reflexive behavior is now a Hobson’s Choice.

They either kill Epstein or he cuts a deal or stands trial and hundreds of very powerful people are exposed along with the honeypot programs that are the source of so much of the bad policy we all live with every day.

These operations are the lifeblood of the power structure, without it glitches in the Matrix occur. People get elected to power who can’t be easily controlled.

The central banks are faced with the same problem. To deflate is worse than inflating therefore there is no real choice. So, inflation it is. Inflation extends their control another day, another week.

Whenever I analyze situations like this I think of a man falling out of a building. In that state he will do anything to find a solution to his problem, grasp onto any hope and use that as a means to prolong his life and avoid hitting the ground for as long as possible.

Desperate people do desperate and stupid things. So as the mother of all Battles of the ‘Flations unfolds over the next two years, remember it’s not your job to take sides because they will take you with them.

This is not a battle you win, but rather survive. Like Godzilla and Mothra destroying the city. If Epstein’s murder tells you anything, there’s a war going on for control of what’s left of the crumbling power structure.

And since inflation is the only choice that choice will undermine what little faith there is in the current crop of institutions we’ve charged with maintaining societal order.

As those crumble that feeds the inflation to be unleashed.

For the smart investor, the best choice is not to play. Wealth preservation is the key to survival. That means holding assets whose value may fluctuate but which cannot be taken from you during a crisis.

It means having productive assets and being efficient with your time.

It means minimizing your counter-party risk. Getting out of debt. Buying gold and cryptos on program or on pullbacks. Most importantly, it means keeping your skills up to date and your value to your employer(s) high.

And if you’re really smart, diversifying your income streams to keep your options open.

Deflation and inflation are two sides of the same coin (or the same side of two coins). Both are just as destructive.

While the Fed may be surprised that low income workers aren’t as enthused about inflation as they are, we are not. A recentBloomberg reportlooked at the stark disconnect between Fed policy and well, everybody else but banks and the 1%.

While the Fed sees low inflation as “one of the major challenges of our time,” Shawn Smith, who trains some of the nation’s most vulnerable, low-income workers stated the obvious: people don’t want higher prices. Smith is the director of workforce development at Goodwill of Central and Coastal Virginia.

In fact, he said that “even slight increases make a huge difference to someone who is living on a limited income. Whether it is a 50 cents here or 10 cents there, they are managing their dollars day to day and trying to figure out how to make it all work.’’ Indeed, as wediscussed yesterday, it is the low-income workers – not the “1%”ers, who are most impacted by rising prices, as such all attempts by the Fed to “help” just make life even more unaffordable for millions of Americans.

Fears, and risks, associated higher prices comprise much of the feedback that the Fed has getting as part of its “Fed Listens” 2019 strategy tour, labeled as a multi-city “outreach tour”. So much for objectivity. Fed Governor Lael Brainard faced additional feedback from community leaders earlier this week in Chicago when she chaired a panel on full employment.

Patrick Dujakovich, president of the Greater Kansas City AFL-CIO, told the audience in Chicago: “I have heard a lot about price stability and fiscal sustainability from the Fed for a very, very long time. Maybe I wasn’t listening, but today is the first time I’ve heard about employment sustainability and employment security.”

The problem that the Fed continues to face is that it has backed itself into a corner. With the economy supposedly “booming” and the stock market at all time highs, rates remain low and any tick higher would likely begin to cause massive shocks to a debt-laden and spending-addicted economy that has been swelling into dangerously uncharted waters over the last 10 years.

As one potential answer, the Fed is now looking at “inflation targeting” (whose disastrous policies wediscussed here yesterday), which amounts to simply pursuing higher inflation for a while to “make up” for “undershoots” of the Fed’s 2% target since 2009. But the reality is that this idea cripples consumers, especially those at the lower end of the income spectrum.

Stuart Comstock-Gay, president of Delaware Community Foundation, told an audience at the Philadelphia Fed: “The sometimes positive impacts of inflation for certain of us have no good benefits for people at the lower end of the spectrum.”

And even former Fed economists agree. Andrew Levin, who’s now a Dartmouth College professor said: “The Fed and other central banks need to make sure they can foster the recovery from a severe adverse shock. But the answer is not to push inflation higher. Elevated inflation would be particularly burdensome for lower-income families.’’

Other economists have similar takes:

University of Chicago economist Greg Kaplan found that the cumulative inflation rate was 8-to-9 percentage points lower for households with incomes above $100,000 versus those with incomes below $20,000 over the 2004-2012 period. During that time, inflation averaged 2.2% which would be in the range of what Fed officials are now discussing as a possible strategy.

While unsuspecting U.S. consumers continue to expect low, sub-2% inflation according to the latest YTD low breakeven rate, little do they know they are about to be blindsided by a coming inflationary shock, according to a new WSJreportwhich notes that many U.S. consumer staple and industry-leading companies are either already in the process of raising prices, or have set concrete plans to do so in the very near future.

Once these price increases are passed through to consumers, it will likely mark the end to a long period of “low inflation” that the Fed has constantly leaned on as an excuse to keep rates low for nearly a decade.

Take Clorox for example, which is raising prices on everyday products like cat litter. Coca-Cola also reported higher prices for the past quarter. Mondelez International also plans to raise prices in North America next year according to an interview with its CEO on Monday. The food giant said that it is passing along rising costs, including ingredient and transportation costs, to consumers.

Airlines are also passing on costs as they are paying about 40% more for jet fuel than they were a year ago. Delta, JetBlue and American have all raised fees, fares, or both. Trucking costs were up 7% annually in September and private sector wages and salaries in the September quarter rose 3.1%.

Arconic was able to widen its operating margins this past quarter on its aluminum products by using tariffs to justify price hikes. Manufacturers are paying about 8% more for aluminum and 38% more for steel than they were a year ago. Looming potential tariffs with China to the tune of $200 billion also continue to weigh on input costs.

Even such supposedly immune to day-to-day price fluctuation companies as Apple,recently raised priceson its new MacBook Air and iPad Pro products by between 20% and 25%.

The list goes on: Steve Madden said it would be raising prices on handbags and other products that it imports from China. It’s looking to shift production to other countries to avoid tariffs and said that products made in China could rise as much as 10% in price.

An interior designer working for Whiski Kitchen in Royal Oak, Michigan was cited by the Journal as stating that she was paying 15% more for quartz countertops made in China also as a result of U.S. tariffs. She’s also paying about 10% more for imported cabinets.

Sherwin-Williams and PPG, both in the paint manufacturing business, stated in recent weeks that they would continue to raise prices to cover rising costs for input materials like titanium dioxide. Sherwin-Williams raised prices by as much as 6% this month.

Sherwin-Williams Chief Executive John Morikis said last week that “Raw material inflation has been unrelenting and accelerating.”

Food companies are also hiking prices. McDonalds’ 2.4% SSS comps in Q3 were a result of higher burger prices. Chili’s Restaurants raised the price of its two entree and an appetizer deal from $22 to $25 in the quarter. Habit Restaurants saw its prices rise by 3.9% in May of this year, even while traffic declined 3.4%. Hershey also has plans to sell candy in packaging next year that will raise its price per ounce.

“Retailers understand that when costs go up, something has to give,” said Michele Buck, chief executive of Hershey, last week.

“Tariffs are causing inflation: increased costs of imports, increased cost of freight and increased domestic costs from suppliers who import.”

While inflation still technically remains near the Fed’s 2% target, if you believe the CPI number, which as we have discussed previously woefully under counts true inflation which is as much asthree times higherthan the Fed’s hedonically adjusted, politically motivated number, prices are set to move higher as a result of labor shortages, while headwinds for prices include the recent strength of the dollar, making imports cheaper. And then there are tariffs.

It’s obvious that higher prices will “work” alongside the Fed’s rate hikes to help dampen the United States economy further. Not only that, but higher prices could cause even more damage if the Fed sees raising rates as the main solution to inflation exceeding its expectations.

Diane Swonk, Grant Thornton’s chief economist, previewed what will happen next best: “We might see a pop of inflation in the first quarter.”

Once that happens in what is already a rising rate environment in which the president has made it clear he is solidly against any more Fed tightening, we wonder just what Powell’s next move will be when even higher prices force his bluff?

If you were contemplating an investment at the beginning of 2014, which of the two assets graphed below would you prefer to own?

Data Courtesy: Bloomberg

In the traditional and logical way of thinking about investing, the asset that appreciates more is usually the preferred choice.

However, the chart above depicts the same asset expressed in two different currencies. The orange line is gold priced in U.S. dollars and the teal line is gold priced in Turkish lira. The y-axis is the price of gold divided by 100.

Had you owned gold priced in U.S. dollar terms, your investment return since 2014 has been relatively flat. Conversely, had you bought gold using Turkish Lira in 2014, your investment has risen from 2,805 to 7,226 or 2.58x. The gain occurred as the value of the Turkish lira deteriorated from 2.33 to 6.04 relative to the U.S. dollar.

Although the optics suggest that the value of gold in Turkish Lira has risen sharply, the value of the Turkish Lira relative to the U.S. dollar has fallen by an equal amount. A position in gold acquired using lira yielded no more than an investment in gold using U.S. dollars.

Data Courtesy: Bloomberg

This real-world example is elusive but important. It helps quantify the effects of the recent economic chaos in

This real-world example is elusive but important. It helps quantify the effects of the recent economic chaos in Turkey. Turkey’s economic future remains uncertain, but the reality is that their currency has devalued as a result of large fiscal deficits and heavy borrowing used to make up the revenue shortfall. Inflation is not the cause of the problem; it is a symptom. The cause is the dramatic increase in the supply of lira designed to solve the poor fiscal condition.

A Turkish citizen who held savings in lira is much worse off today than even two months ago as the lira has fallen in value. She still has the same amount of savings, but the savings will buy far less today than only a few weeks ago. Her neighbor, who held gold instead of lira, has retained spending power and therefore wealth. This illustration highlights the ability of gold to convey clear comparisons of various countries’ circumstances. It also illustrates the damage that imprudent monetary policy can inflict and the importance of gold as insurance against those policies.

Penalty

Using Turkey as an example also helps illustrate why we say that inflationary regimes impose a penalty on savers. Inflation encourages and even forces people to spend, invest or speculate to offset the effects of inflation. Investing and speculating entail risk, however, so in an inflationary regime one must assume risk or accept a decline in purchasing power.

Most people think of inflation as rising prices. Although that is the way most economists represent inflation, the truth is that inflation is actually your money losing value. Inflation is not caused by rising prices; rising prices are a symptom of inflation. The value of money declines as a result of increasing money supply provided by the stewards of monetary discipline, the Federal Reserve or some other global central bank.

This is difficult to conceptualize, so let’s bring it home in a simple example. If you live in a country where the annual inflation rate is a steady 2%, the value of the currency will decline every year by 2% on a compounded basis. At this rate, the purchasing power of the currency will be cut in half in less than 35 years.

Now consider a country, like Turkey, that has been running chronic deficits, printing money rapidly to make up a revenue shortfall, and begins to experience accelerating inflation. The annual inflation rate in Turkey is now estimated to be over 100% or 8.30% per month, a difficult number to comprehend. The value of their currency is currently falling at an accelerating pace so that what might have been purchased with 500 lira 9 months ago now requires 1,000 lira.

Put another way, for the prudent retiree who had 10,000 lira in cash stashed away nine months ago, the inflation-adjusted value of that money has now fallen to less than 5,000 lira. If inflation persists at that rate, the 10,000 will become less than 1,000 in 29 months.

Believe it or not, Turkey is, so far, a relatively mild example compared to hyperinflationary episodes previously seen in Germany, Czechoslovakia, Venezuela, and Zimbabwe. These instances devastated the currencies and the wealth of the affected citizens. Fiscal imprudence is a real phenomenon and one that eventually destroys the financial infrastructure of a country. For more on the insidious role that even low levels of inflation have on purchasing power, please read our article:The Fed’s Definition of Price Stability is Likely Different than Yours.

Summary

There are over 3,800 historical examples of paper currencies that no longer exist. Although some of these currencies, like the French franc or the Greek drachma disappeared as a result of being replaced by an alternative (euro), many disappeared as a result of government imprudence, debauching the currency and hyperinflation. In all of those cases, persistent budget deficits and printed money were common factors. This should sound worryingly familiar.

Modern day central banks function by employing a steady dose of propaganda arguing against the risks of deflation and in favor of the benefits of a “modest” level of inflation. The Fed’s Congressional mandate is to “foster economic conditions that promote stable prices and maximum sustainable employment” but promoting stable prices evolved into a 2% inflation target. The math is not complex but it is difficult to grasp. Any number, no matter how small, compounded over a long enough time frame eventually takes on a parabolic, hockey stick, shape. The purpose of the inflation target is clearly intended to encourage borrowing, spending and speculating as the value of the currency gradually erodes but at an ever-accelerating pace. Those not participating in such acts will get left behind.

In the same way that rising prices are a symptom of inflation attributable to too much printed money in the system, deflation is falling prices due to unfinanceable inventories and merchandise pushed on to the market caused by too much debt. Contrary to popular economic opinion, deflation is not falling prices caused by a technology-enhanced decline in the costs of production – that is more properly labeled as “progress.” The Fed is either knowingly or unknowingly conflating these two separate and very different issues under the deflation label as support for their “inflation target”. In doing so, they are creating the conditions for deflation as debt burdens mount.

Gold, for all its imperfections, offers a time-tested, stable base against which to measure the value of fiat currencies. Accountability cannot be denied. Despite the unwillingness of most central bankers to acknowledge gold’s relevance, the currencies of nations will remain beholden to the “barbarous relic”, especially as governments continue to prove feckless in their application of fiscal and monetary discipline.

The only way to pay all these future obligations is by creating new money.

I’ve been focusing on inflation, which is more properly understood as the loss of purchasing power of a currency, which when taken to extremes destroys the currency and the wealth/income of everyone forced to use that currency.

The funny thing about the loss of a currency’s purchasing power is that it wipes out every holder of that currency, rich and not-so-rich alike. There are a few basics we need to cover first to understand how soaring future obligations–pensions, healthcare, entitlements, interest on debt, etc.–lead to a feedback loop which will hasten the loss of purchasing power of our currency, the US dollar.

1. As I have explained many times, the only possible output of the way we create and distribute “money” (credit and currency) is soaring wealth/income inequality, as all the new money flows to the wealthy, who use the “cheap” money from central and private banks to lend at high rates of interest to debt-serfs, buy back corporate shares or buy up income-producing assets.

The net result is whatever actual “growth” has occurred (removing the illusory growth that accounts for much of the GDP “growth” this decade) has flowed almost exclusively to the top of the wealth-power pyramid (see chart below).

The mainstream financial media swallows the bogus “growth” story without question because that story is the linchpin of the entire status quo: if it’s revealed as inaccurate, i.e. statistical sleight of hand, the whole idea that “growth” can effortlessly fund all future obligations goes up in flames.

Combine that “growth” has been grossly over-estimated with an increasing concentration of wealth and income in the top .1% of 1%, and the only possible conclusion is there’s less available to pay fast-rising obligations out of what’s left to the bottom 99.9%.

3. We’ve been paying our obligations with debt for the past decade. Look at the chart below of the debt to GDP ratio–it has skyrocketed as GDP has inched higher while debt has exploded. (Remove the fictitious “growth” in GDP and the picture worsens significantly.)

Look at the chart of federal debt and explain how the steepening trajectory of debt is sustainable in a stagnating real economy with stagnating wages for the bottom 95% of the populace.

4. Recall that the federal, state and local governments pay interest on all the money they borrow to fund deficit spending, i.e. every dollar spent above and beyond tax revenues. All that interest is an increasing obligation that must be paid in the future. Borrowing more to pay interest increases the interest payments due in the future–a classic self-reinforcing runaway feedback loop.

5. Politicians get re-elected by increasing entitlements and obligations without regard to how they will be funded. “Growth” will effortlessly take care of everything–that’s the centerpiece assumption of all conventional economics, free-market, Keynesian and socialist alike.

6. The core constituencies of politicians are government employees and contractors, as these interest groups are funded by the government, which is nominally managed by elected officials and their appointees. Nobody’s more generous (or demanding) than those feeding directly at the government trough. (By “contractors” I mean the vast array of Corporate America cartels that feed off government spending: defense, Big Pharma, Higher Education, etc.)

7. The obligations that have been promised are expanding at a nearly exponential rate, as healthcare costs continue to soar and the number of government pensioners is rising rapidly. This chart illustrates the basic dynamic: the tax revenues required to fund these obligations are far outstripping the income and wealth of the bottom 95% of the populace.

Consider this chart of real GDP per capita. Real GDP is adjusted to remove inflation from the picture, so this is supposed to be “real growth.” How many people are demonstrably 19% better off than they were in 2000?

Not many, judging by the decline in family financial wealth since 2001:

Income increases flow disproportionately to the top .1%. Adjusted for real-world inflation, the bottom 95% have actually lost ground:

Here’s the uncomfortable reality: the means to pay all these future obligations— the real-world economy, and the wealth and income of the vast majority of the populace– are far too modest to fund the fast-expanding obligations,which include interest due on the ever-increasing mountain of public and private debt.

The current “everything” asset bubbles have temporarily boosted the wealth and income of corporations and the wealthy, but all bubbles eventually pop as the marginal elements that are propping up the expansion weaken and implode.

Once the asset bubbles pop, the illusion that “taxing the rich” will pay for all the obligations pops along with the bubble. And as I’ve noted many times, those at the top of the wealth-power pyramid wield political power, so they have the means and the motive to limit their tax burden to roughly 20% or less–(sometimes much less, as in zero.)

That 20% is an interesting threshold, as once federal tax burdens rise above 20%, the higher taxes trigger a recession which then crushes tax revenues.This makes sense– if I pay an extra $2,000 annually in higher junk fees and taxes, that’s $2,000 less I have to invest or spend.

Put these dynamics together and you get one outcome: the federal government cannot possibly pay all its obligations out of tax revenues nor can it raise taxes high enough to do so without gutting tax revenues via a recession.

The only way to pay all these future obligation is by creating new money, which in a stagnant, dysfunctional economy can only reduce the purchasing power of the currency, in effect robbing every holder of the currency of wealth and income.

Here’s the end-game, folks: Venezuela. The nostrum has it that “the government can’t go broke because it can always print more money.” True, but as the wretched populace of Venezuela has discovered, there is a consequence of that money-creation to meet obligations: the destruction of the currency, and thus the wealth and income of everyone forced to use that currency.

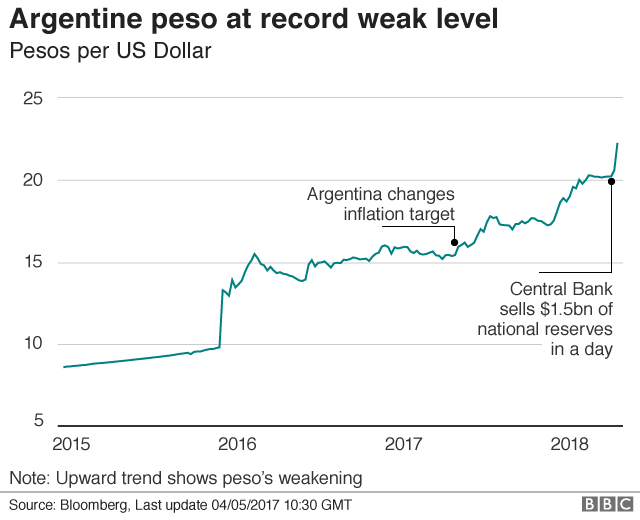

Argentina’s central bank has raised interest rates for the third time in eight days as the country’s currency, the peso, continues to fall sharply.

On Friday, the bank hiked rates to 40% from 33.25%, a day after they were raised from 30.25%. A week ago, they were raised from 27.25%. The rises are aimed at supporting the peso, which has lost a quarter of its value over the past year.

Analysts say the crisis is escalating and looks set to continue.

Argentina is in the middle of a pro-market economic reform programme under President Mauricio Macri, who is seeking to reverse years of protectionism and high government spending under his predecessor, Cristina Fernandez de Kirchner. Inflation, a perennial problem in Argentina, was at 25% in 2017, the highest rate in Latin America except for Venezuela. This year, the central bank has set an inflation target of 15% and has said it will continue to act to enforce it.

‘Aggressive steps’

Despite the twin rate rises, the peso, which was fixed by law at parity with the US dollar before Argentina’s economic meltdown in 2001-02, is now trading at about 22 to the dollar.

“This crisis looks set to continue unless the government steps in to reassure investors that it will take more aggressive steps to fix Argentina’s economic vulnerabilities,” said Edward Glossop, Latin America economist at Capital Economics. “Risks to the peso have been brewing for a while – large twin budget and current account deficits, a heavy dollar debt burden, entrenched high inflation and an overvalued currency.

“The real surprise is how quickly and suddenly things seem to be escalating.”

Mr Glossop said “a sizeable fiscal tightening” was planned for 2018, but it might now need to be larger and prompter. “Unless or until that happens, the peso is likely to remain under pressure, and there remains a real risk of a messy economic adjustment.” Argentina’s president Mauricio Macri is a controversial figure in a country that is still strongly divided ideologically. But among international investors he is unanimously praised. Since coming to office, he moved swiftly to end capital controls and re-establish trust in economic data coming from Argentina. However, he is not winning a crucial battle in the country – the one against inflation. Markets are taking notice and there has been a sell-off of the peso. The opposition wants to stop Macri from removing subsidies in controlled prices, such as energy and utility tariffs, which may bring more inflation in the short term but could help bring it down from above 20% now to about 5% by 2020.

Friday was a day for emergency measures – a massive hike to 40% in interest rates and another promise to bring down government spending.

Investors still believe Macri has a sound plan to recover Argentina, but they are not convinced he can see it through.

Argentina Raises Interest Rates To 40% To Support Their Currency

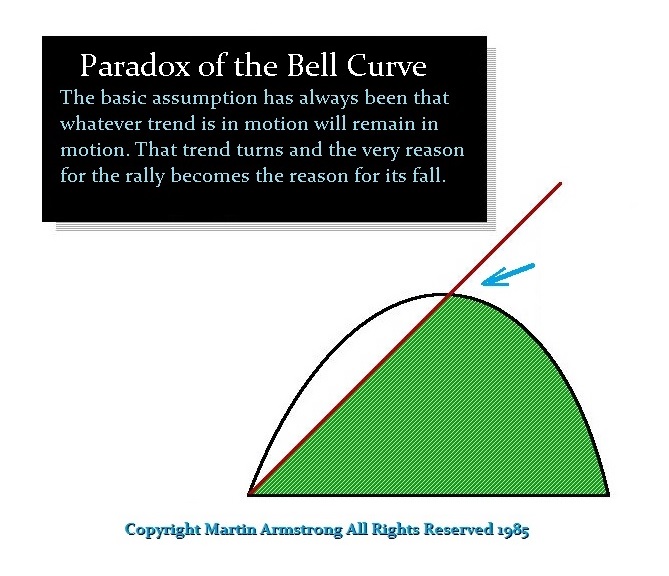

Argentina has just raised interest rates to40% trying to support the currency. I have explained many times that interest rates follow a BELL-CURVE and by no means are they linear. This is one of the huge problems behind attempts by central banks to manipulate the economy by impacting demand-side economics. Raising interest rates to stem inflation will work only up to a point and even that is debatable. The entire interrelationship between markets and interest rates has three main phase transitions and each depends upon the interaction with CONFIDENCE of the people in the survivability of the state.

PHASE TWO: Raising interest rates will flip the economy as Volcker did in 1981 ONLY when they exceed the expectation of profits in asset inflation provided there is CONFIDENCE that the government will survive as in the USA back in 1981 compared to Zimbabwe, Venezuela, Russia during 1917 or China back in 1949. In other words, if the nation is going into civil war, then tangible assets will collapse and the solution becomes assets flee the country.

In the case of the USA back in 1981, the high interest rates worked because we were only in Phase Two where there was no civil war or revolution so the survivability of the government did not come into question. Hence, Volcker created DELATION as capital then ran away from assets and into bonds to capture the higher interest rates. Then and only then did rates begin to decline between 1981 into 1986 reflecting the high demand for US government bonds, which in turn drove the US dollar to record highs and the British pound to $1.03 in 1985 resulting in the Plaza Accord and the creation of the G5 (now G20).

So many people want to take issue with me over how the stock market will rise with higher interest rates. It is a BELL-CURVE and you better begin to understand this. If not, just hand-over all your assets to the New York bankers now, go on welfare and just end your misery.

Here are charts of the Argentine share market the currency in terms of US dollars. You can see that the stock market offers TANGIBLE assets that rise in local currency terms because assets have an international value. Here we can see the dollar has soared against the currency and the stock market has risen in proportion the decline in the currency. I do not think there is any other way that is better to demonstrate the BELL-CURVE effect of interest rates than these two charts.

To those who doubt that the stock market can rise with rising interest rates, I really do not know what to say. Keep listening to the talking heads of TV and all the pundits who claim only gold will rise and everything else will fall to dust. Then we have the sublime blind idiots who never look outside the USA and proclaim the dollar will crash and burn not the rest of the world so buy gold and cryptocurrency you cannot spend and certainly with no power grid.

PHASE THREE

Is when no level of interest rate will save the day. Capital simply flees the political state for the risk of revolution or civil war means that tangible assets which are immovable will not hold their value such as companies and real estate. This is the period that Goldbugs envision. At that point, the value of everything will even move into the extreme PHASE FOUR where even gold will decline and the only thing to survive is food. There, the political state completely collapses and a new political government comes into being.

Meanwhile, the following is an analysis update on the pending 2021 LIBOR reset that will affect trillions in debt and derivative instruments across the globe…

I am going to break from regular market commentary to step back and think about the big picture as it relates to debt and inflation. Let’s call it philosophical Friday. But don’t worry, there will be no bearded left-wing rants. This will definitely be a market-based exploration of the bigger forces that affect our economy.

One of the greatest debates within the financial community centers around debt and its effect on inflation and economic prosperity. The common narrative is that government deficits (and the ensuing debt) are bad. It steals from future generations and merely brings forward future consumption. In the long run, it creates distortions, and the quicker we return to balancing our books, the better off we will all be.

I will not bother arguing about this logic. Chances are you have your own views about how important it is to balance the books, and no matter my argument, you won’t change your opinion. I will say this though. I am no disciple of the Krugman “any stimulus is good stimulus” logic.

Thebroken window fallacyis real and digging ditches to fill them back in is a net drain on the economy. Full stop. You won’t hear any complaints from me there.

Yet, the obsession with balancing the government’s budget is equally damaging. In a balance sheet challenged economy the government is often the last resort for creating demand. Trying to balance a government deficit in this environment (like the Troika imposed on Greece during the recent Euro-crisis) is a disaster waiting to happen.

Have a look at these charts from the NY Times outlining the similarity of the Greece depression to the American Great Depression of the 1930s.

Now you might look at these charts and say, “Greece spent too much and suffered the consequences. Ultimately they will be better off taking the hit and reorganizing in a more productive economic fashion.” If so, you probably also still have this poster hanging in your room at your parent’s house where you grew up.

Personally, I don’t want to even bother discussing the possibility of this sort of Austrian-style-rebalancing coming to Western democracies. Yeah, it might be your dream, but it’s just a dream. I have Salma Hayek on myfreebie list, but what do I think of my chances? About as close to zero without actually ticking at the perfect zero level. It’s not a “can’t happen,” but it’s certainly a “it’s not going to happen in a million years.”

Governments were faced with a choice during the 2008 Great Financial Crisis. Credit was naturally contracting, and the economy wanted to go through a cleansing economic rebalancing where debt would be destroyed through a severe recession. Yet, governments had practically zero appetite to allow this sort of cathartic cleansing to happen. Instead, they stepped up and stopped the credit contraction through government spending and quantitative easing.

I believe that government spending is not all bad, and at times, it plays an important role in our economy. I am a huge fan ofRichard Koo’swork. When economies’ interest-rate policies become zero bound, governments are crucial in engaging in anti-cyclical spending. All debt is not bad. Take debt your company might issue for instance. Borrowing a million dollars to invest in capital equipment to make your firm more productive is a much different prospect than taking out a loan to engage in a Krugman-inspired-all-you-can-drink-party-headlined-by-the-Killers. Sure, the party sounds like fun, but it’s not going to benefit your firm past one night of excitement. Governments shouldn’t perpetuate unproductive pension grabs by workers, but instead actually spend money on infrastructure that will make the economy more productive. During the 1950s Eisenhower invested in the American highway system, helping America secure its place as the world’s most economically dominant country. Today that sort of infrastructure spending would be shouted down as irresponsible. Well, not continuing to invest in your country’s productive capacity is the irresponsible part.

The point is that not all spending is bad, but nor is all spending good. And even more importantly, government spending should be anti-cyclical. No sense spending more when your economy is rocking. Better to save the bullets to ebb the natural flow of the business cycle.

But I digress. Let’s get back to debt.

Creating debt is inflationary, while paying down debt is deflationary. That’s pretty basic.

The easiest way for me to demonstrate this fact is to look at an area where debt has been created for spending in a specific area. No better example than student loans.

Over the past fifteen years, inflation in college tuition has exploded. It’s been absolutely bonkers. Here is the chart of regular CPI versus tuition CPI.

But it should really be no surprise. If we add the student loan debt versus Federal debt series, it becomes clear that a tremendous amount of credit has been extended to students.

So let’s agree that credit creation is inflationary, and by definition, credit destruction should be deflationary.

Therefore when the market pundits that I like to affectionately call deflationistas argue that this next chart is ultimately deflationary, I understand where they are coming from.

If you assume that this debt needs to be paid back, then it’s easy to understand their argument. When debt starts to contract and this chart heads lower, this will be deflationary. And if you assume that governments start to balance their books, then there is every reason to expect that future deflation is the worry, not inflation. After all, the money has already been spent. The inflation from that spending is already in the system.

I can already hear the deflationistas argument – over 100% of GDP is unsustainable therefore credit growth will at worst go sideways, but most likely actually contract in coming years.

Really? How about Japan?

The same argument was made at the turn of the century when Japan was running a debt that was over 150% of GDP, yet they somehow managed to push that up another 80% to 230% without causing some sort of apocalyptic collapse.

Now before you send me an angry email about the moral irresponsibility of suggesting debt can go higher, save your clicks. I understand your argument. I am not interested in debating what should be done, but rather I am trying to determine what will be done. You might believe governments and Central Banks will gain religion and start conducting prudent and responsible policies. So be it. If you believe that, then by all means – load up on long-dated sovereign bonds as they will continue to be the trade of the century.

I, on the other hand, believe that Central Banks will continue printing until, as my favourite West Coast skeptic Bill Fleckenstein says, “the bond market takes away the keys.” And even when Central Banks are mildly responsible, politicians are sitting in the wings waiting to spend at any chance they get. Take Trump’s recent stimulus program. We are now more than eight years into an economic recovery, and he just pushed through one of the most stimulative fiscal policies of the past couple of decades. Regardless of where you stand politically regarding these tax cuts, there can be no denying they were much more needed in 2008 than today.

This is a long-winded way of saying that although I agree that the creation of debt is inflationary, and that the destruction of debt is deflationary, I don’t buy the argument that any sort of absolute amount of debt means the trend has to change. I don’t look at the 100% debt-to-GDP figure and worry that the US government will somehow institute deflationary policies to pay that back. Nope, I don’t see anything but a sea of growing deficits and debts. And in fact, the larger debts grow, the less likely they are to be paid back.

How will Japan pay back their debt that is 230% of GDP? The answer is that they can’t. It will be inflated away.

It’s foolish to believe that the end-game is anything but inflation. And even though increasing debt seems scary, if there is one thing that I am sure of, it’s that they will figure out a way to make even more of it.

Rant over. And no more big picture philosophy for a while – I promise.

Over the span of 2000-2016, the amount of money spent on food by the average American household increased from $5,158 to $7,203, which is a 39.6% increase in spending.

Despite this,as Visual Capitalist’s Jeff Desjardins notes, for most of the U.S. population, food actually makes up a decreasing portion of their household spending mix because of rising incomes over time. Just 13.1% of income was spent on food by the average household in 2016, making it a less important cost than both housing and transportation.

That said, fluctuations in food prices can still make a major impact on the population. For lower income households, food makes up a much higher percentage of incomes at 32.6% – and how individual foods change in price can make a big difference at the dinner table.

FLUCTUATING GROCERY PRICES

Today’s infographic comes from TitleMax, and it uses data from the Bureau of Labor Statistics to show the prices for 30 common grocery staples over the last decade.

In 1791, the first Secretary of the Treasury of the US, Alexander Hamilton, convinced then-new president George Washington to create a central bank for the country.

Secretary of State Thomas Jefferson opposed the idea, as he felt that it would lead to speculation, financial manipulation, and corruption. He was correct, and in 1811, its charter was not renewed by Congress.

Then, the US got itself into economic trouble over the War of 1812 and needed money. In 1816, a Second Bank of the United States was created. Andrew Jackson took the same view as Mister Jefferson before him and, in 1836, succeeded in getting the bank dissolved.

Then, in 1913, the leading bankers of the US succeeded in pushing through a third central bank, the Federal Reserve. At that time, critics echoed the sentiments of Messrs. Jefferson and Jackson, but their warnings were not heeded. For over 100 years, the US has been saddled by a central bank, which has been manifestly guilty of speculation, financial manipulation, and corruption, just as predicted by Mister Jefferson.

From its inception, one of the goals of the bank was to create inflation. And, here, it’s important to emphasize the term “goals.” Inflation was not an accidental by-product of the Fed – it was a goal.

Over the last century, the Fed has often stated that inflation is both normal and necessary. And yet, historically, it has often been the case that an individual could go through his entire lifetime without inflation, without detriment to his economic life.

Yet, whenever the American people suffer as a result of inflation, the Fed is quick to advise them that, without it, the country could not function correctly.

In order to illustrate this, the Fed has even come up with its own illustration “explaining” inflation. Here it is, for your edification:

If the reader is of an age that he can remember the inventions of Rube Goldberg, who designed absurdly complicated machinery that accomplished little or nothing, he might see the resemblance of a Rube Goldberg design in the above illustration.

And yet, the Fed’s illustration can be regarded as effective. After spending several minutes taking in the above complex relationships, an individual would be unlikely to ask, “What did they leave out of the illustration?”

Well, what’s missing is the Fed itself.

As stated above, back in 1913, one of the goals in the creation of the Fed was to have an entity that had the power to create currency, which would mean the power to create inflation.

It’s a given that all governments tax their people. Governments are, by their very nature, parasitical entities that produce nothing but live off the production of others. And, so, it can be expected that any government will increase taxes as much and as often as it can get away with it. The problem is that, at some point, those being taxed rebel, and the government is either overthrown or the tax must be diminished. This dynamic has existed for thousands of years.

However, inflation is a bit of a magic trick. Now, remember, a magician does no magic. What he does is create an illusion, often through the employment of a distraction, which fools the audience into failing to understand what he’s really doing.

And, for a central bank, inflation is the ideal magic trick. The public do not see inflation as a tax; the magician has presented it as a normal and even necessary condition of a healthy economy.

However, what inflation (which has traditionally been defined as the increase in the amount of currency in circulation) really accomplishes is to devalue the currency through oversupply. And, of course, anyone who keeps his wealth (however large or small) in currency units loses a portion of their wealth with each devaluation.

In the 100-plus years since the creation of the Federal Reserve, the Fed has steadily inflated the US dollar. Over time, this has resulted in the dollar being devalued by over 97%.

The dollar is now virtually played out in value and is due for disposal. In order to continue to “tax” the American people through inflation, a reset is needed, with a new currency, which can then also be steadily devalued through inflation.

Once the above process is understood, it’s understandable if the individual feels that his government, along with the Fed, has been robbing him all his life. He’s right—it has.

And it’s done so without ever needing to point a gun to his head.

The magic trick has been an eminently successful one, and there’s no reason to assume that the average person will ever unmask and denounce the magician. However, the individual who understands the trick can choose to mitigate his losses. He or she can take measures to remove their wealth from any state that steadily imposes inflation upon their subjects and store it in physically possessed gold, silver and private cryptocurrency keys.

We present some somber reading on this holiday season from Macquarie Capital’s Viktor Shvets, who in this exclusive to ZH readers excerpt from his year-ahead preview, explains why central banks can no longer exit the “doomsday highway” as a result of a “dilemma from hell” which no longer has a practical, real-world resolution, entirely as a result of previous actions by the same central bankers who are now left with no way out from a trap they themselves have created.

* * *

“It has been said that something as small as the flutter of a butterfly’s wing can ultimately cause a typhoon halfway around the world” – Chaos Theory.

There is a good chance that 2018 might fully deserve shrill voices and predictions of dislocations that have filled almost every annual preview since the Great Financial Crisis.