Personal Income Decreased 13.1% in April, Spending increased 2.4%

“Given that the economy is now totally and completely dependent on inflating asset bubbles, it makes no sense to invest for the long-term” – Charles Hugh Smith

Beneath the endlessly hyped expansion in gross domestic product (GDP) of the past two decades, the economy has changed dramatically. The American Dream boils down to social and economic mobility, a.k.a. getting ahead through hard work, merit and wise investments in oneself and one’s family.

The opportunities for this mobility in the post World War 2 era broadened as civil rights and equal rights expanded. The 1970s saw a disruption of working-class mobility as high-paying factory jobs disappeared, leaving services jobs that paid less or required more training, i.e. a college degree.

The U.S. economy took off in the 1980s for a number of reasons, including computer technologies, federal stimulus (deficit spending) and financialization (a topic I’ve covered many times). With millions more college graduates entering the workforce and the Internet creating entire new industries, the opportunities to “get ahead” increased across the social and economic spectrum.

But something changed in the aftermath of the dot-com bubble bursting. The fruits of financialization–highly leveraged debt gambled for short-term gains in markets–were extended to everyone with a job (or a willingness to lie) via liar loans, no-document loans and subprime mortgages.

Just like bigshot financiers on Wall Street, J.Q. Citizen could leverage a couple thousand dollars in cash (or even better, borrow the closing costs via a 105% of value mortgage and put nothing down) and buy a McMansion worth $250,000 or even $500,000.

The only difference between bigshot financiers and J.Q. Citizen was the scale of the leverage and gamble: J.Q. Citizen could leverage a few grand into hundreds of thousands, while the financier could leverage a bit of collateral into mega-millions.

The goal wasn’t homeownership, the purported “official” goal of subprime mortgages: it was short-term speculative gains via “flipping” the house in a few months. Just like the bigshot financiers, the subprime mortgage market enabled marginal borrowers to take control of assets far in excess of their actual capital and sell them to a greater fool for a quick profit far in excess of their earnings.

Wall Street loved this distribution of financialization to the masses because Wall Street made a fortune packaging (securitizing) this toxic debt and selling it to unwary, credulous investors as “low risk” (heh) assets.

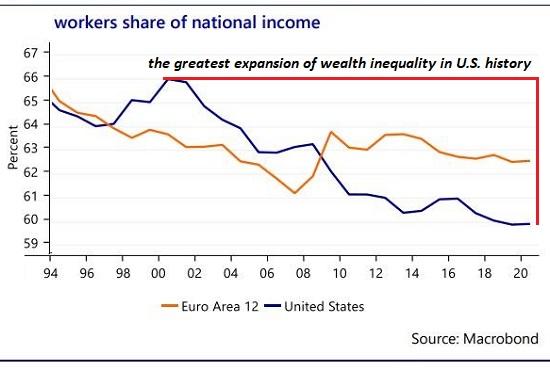

After the mortgage-securitization-fraud-housing bubble popped, a secular trend– wages for the bottom 95% of wage earners stagnating–accelerated. “Getting ahead” via earning a college diploma, working hard and counting on merit no longer worked; families with privileges and capital got wealthier, and everyone else found the purchasing power of their earnings declined even as stocks and housing soared.

The only way to “get ahead” in a globalized, financialized economy is either 1) earn at least $200,000 a year from one’s labor or 2) gamble in the inflating bubbles of stocks and housing. In high-cost regions, even $200,000 isn’t enough to get ahead (i.e. buy a crumbling bungalow on a tiny lot for $800,000) if the wage-earner has student loans and/or children; the household needs two earners making top 5% salaries.

The more money the central banks throw at stock-housing asset bubbles, the higher they loft, a process that has pushed housing in high-cost regions out of reach of all those with average jobs and incomes. So much for “getting ahead.”

The economy has changed dramatically for the worse: getting a graduate degree no longer guarantees getting ahead (millions of other workers globally have the same credentials); working hard is equally iffy, and traditional investments in one’s family either no longer yields gains (higher education) or they are gambles in the guise of “investments” (housing).

Given that the economy is now totally and completely dependent on inflating asset bubbles, it makes no sense to invest for the long-term: a short-term gambling mentality is required to avoid getting destroyed when the bubble-du-jour pops.

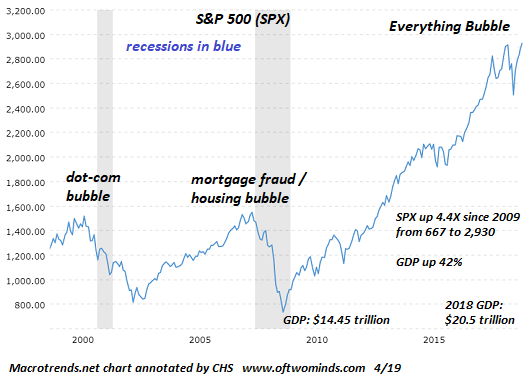

Everyone who believes bubbles never pop, they only expand forever and ever, has never looked at a chart of the S&P 500 (SPX), which illustrates that bubbles always pop, destroying the capital of all who neglected to sell at the top.

If “getting ahead” depends on playing asset bubbles, it’s not getting ahead, it’s gambling.

Source: by Charles Hugh Smith via OfTwoMinds blog,

For the 29th month in a row, Americans annual spending grew faster than their incomes as the ‘no consequences’ new normal rolls on, leaving the savings rate languishing near record lows – even if it did very modestly uptick in May.

Year-over-Year income growth reached 4.0% – the highest since Nov 2015; while YoY spending growth stalled at 4.4%.

Income growth was dominated by private workers seeing another uptick…

On the month, personal incomes grew 0.4% (as expected) – the fastest rate since Dec 2017.

However, for the second straight month, month-over-month spending growth disappointed – rising just 0.2% MoM vs +0.4% expectations.

But the growth in both continues.

The PCE Inflation data came in a little hotter than expected – rising at the fastest since March 2012…

As a reminder, the vast gap between extreme high confidence and extreme low savings rate – a borrow-my-way-to-happiness narrative – has never ended well in the past…

Remember, nothing lasts forever – ask the German soccer team.

For the 26th month in a row, US spending growth outpaced income growth with the latter rising just 3.7% YoY (the lowest since Oct 2017) and former rising 4.6% YoY (slightly faster than in Feb).

Which prompted a drop in the savings rate and a notable downward revision to the last two months (of notable conservatism) with Jan revised down from 3.2% to 3.0% and Feb down from 3.4% to 3.3% and now March at just 3.1%.

However, while income growth did disappoint (rising just 0.3% MoM vs 0.4% MoM expectations), wage growth was up a notable 4.4% YoY with private wages dominating government worker gains (+4.8% YoY vs +2.5% YoY).

Finally we note that Real Personal Spending rose a disappointing 0.4% MoM (versus 0.5% expectations) as The FT notes that the Fed’s favored inflation measure picked up to its strongest level in 17 months in March, further boosting the case for US policy makers to increase rates two or three more times this year after a lift last month.

The so-called core personal consumption expenditures price index, which excludes the volatile food and energy components, jumped 1.9 per cent on the year last month, according to a report from the Bureau of Economic Analysis.

The rise in consumer spending, which accounts for 70% of the economy, gives the economy some momentum at the end of an otherwise weak quarter, and provide some support for forecasts that consumption will accelerate this quarter as tax cuts and a gradual pickup in wages filter into Americans’ bank accounts and sentiment. However, as Bloomberg notes, at the same time, the income figures were slightly below forecasts, reflecting the weakest gain in wages and salaries since October.