Last Wednesday, ZeroHedge reported that based on recent earnings calls, “Companies Are Freaking Out About Soaring Costs“ and today they received more confirmation of this in a Bank of America report which warns that Inflation is:

“arguably the biggest topic during this earnings season, with a broad array of sectors (Consumer/Industrials/Materials) citing inflation pressures.”

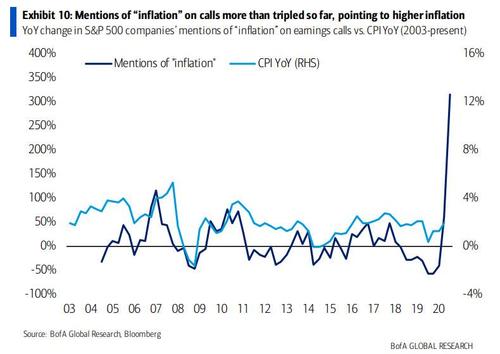

Exhibit A: the chart below showing the number of mentions of “inflation” during earnings calls which exploded, more than tripling YoY per company so far, the and the biggest jump in history since BofA started keeping records in 2004.

Why is this a problem? Because the number of mentions has historically led CPI by a quarter with 52% correlation and points to explosive higher inflation ahead.

Similar to what we did, BofA has also picked up key inflation commentaries from earnings calls, which noted that raw materials, transportation, labor, etc. were cited as sources of inflation and many plan to (or have already) raise prices to pass through higher costs.

- FAST (Industrials): “we are experiencing significant material cost inflation, particularly for steel, fuel and transportation costs.”

- GIS (Staples): “Looking ahead, as we experienced higher inflationary environment, our first line of defense will continue to be our strong holistic margin management cost savings program. In addition, we are taking actions now and in the coming months […] to drive net price realization that will benefit our FY2022. “

- CAG (Staples): “we’re seeing input cost inflation accelerate in many of our categories and across the industry.”

- LW (Staples): “while the pandemic-related effects on our supply chain were the primary drivers of our cost increases, we also realized higher costs due to input cost inflation in the low single-digits. We expect that rate will begin to tick up in the coming quarters as edible oil and transportation costs continue to increase.”

- STZ (Staples): “similar to previous years, we’re expecting substantial inflation headwinds in the low to mid-single-digit increase range, largely related to glass and other packaging materials, raw materials, transportation and labor costs in Mexico. “

- PPG (Materials): “we experienced a significant acceleration of raw material and logistics cost inflation during the quarter. Coming into the year, we were expecting an inflationary environment and had prioritized selling price increases across all of our businesses. This has helped us achieve solid price increases year-to-date. With a higher inflation backdrop, we have already secured further selling price increases and are in the process of executing additional ones during the second quarter. “

- DOV (Industrials): “What we are going to fight against between now and the end of the year […] is inflationary input costs between raw materials, labor, and price/cost. […] the way it’s looking we may have to intervene on price again in certain of the businesses over the balance of the year.”

- TEL (Tech): “I would expect our margins to modestly improve as we work our way forward here into the third and fourth quarter based on some of the actions that are underway and our ability to combat some of the inflationary pressures out there. […] Certainly, we’re feeling the biggest inflation right now is on the freight side. The freight inflation has been significant. And as we battled through there and there’s a variety of reasons for that including higher air freight and so forth in terms of that. And that’s not unique to TE. Certainly, I think that’s been as well publicized across the overall supply chain. […] labor cost is not a major issue on the inflation side, but labor availability in certain places that are still being more impacted by COVID continues to drive some inefficiencies.”

- CMG (Consumer Discretionary): “So, all of that is very, very manageable and we feel like if there is going to be significant increased inflation because of market-driven or because of federal minimum wage, we think everybody in the restaurant industry is going to have to pass those costs along to the customer.”

- ALLE (Industrials): “This guide incorporates pricing actions to offset direct material inflation, as well as reflecting our supply chain capability to mitigate industry challenges on supply and electronic component shortages. We anticipate that these challenges will persist for the balance of the year, and we will continue to monitor and adapt to changing market conditions.”

- WHR (Consumer Discretionary): “The global material cost inflation in particular in steel and resins will negatively impact our business by about $1 billion. We expect cost increases to peak in the third quarter.”

- PNR (Industrials): “All inflation remains high. We have instituted a number of selling price increases across the portfolio that we expect to help mitigate inflation in the second half of the year.”

- TSCO (Consumer Discretionary): “Compared to our initial outlook for the year, our forecast does reflect higher transportation costs and product inflation. We experienced increasing pressures from these factors during the first quarter and expect them to continue to be a headwind throughout 2021.”

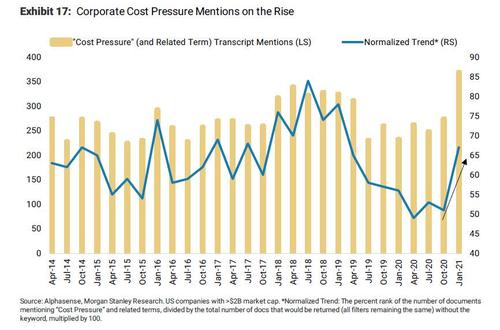

So between BofA’s latest observations, and our post from last week which have created a self-fulfilling prophecy of inflation becoming the primary topic of discussion, it’s no surprise that companies have been discussing rising costs on 1Q earnings calls. In the chart below, Morgan Stanley does a similar exercise as BofA, and shows the number of “cost pressure” mentions from US corporates over time. It’s interesting to note that the series shown are inflecting higher in the current period—a trend worth watching as earnings season progresses.

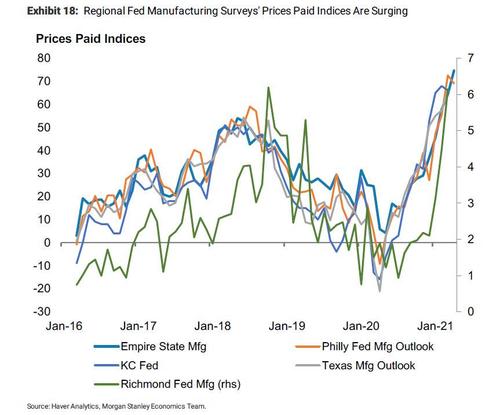

Along the same lines, the next chart shows that prices paid indices from regional Fed manufacturing surveys are surging higher.

Confirming this point, below are several comments from the recent release of the Kansas City Fed’s April Manufacturing Survey which illustrate the breadth of cost increases that companies are currently facing. Labor shortages stand out prominently among this list of quotes.

- “It is very difficult to handle the increased business with supply chain issues across all materials and finding anyone who wants to work. The federal government has incentivized people to stay home and not be productive.”

- “Stimulus and increased unemployment money are wrecking the labor pool. Lower level employees are quitting to make just as much not working.”

- “Unemployed workers have no incentive to return to work given the COVID bonus payments.”

- “Entry level pay will need to be increased. This will create pressure on all other positions.”

- “We believe the shortage of workers is not an impact from the 2nd stimulus as much as a systematic problem of the gig economy and simply not enough workers for unskilled and critical skill positions. We are focused on retention.”

- “We are facing significant supply chain problems due to COVID-19 issues, tariff issues, and the weather problems in Texas earlier this year.”

- “Steel market needs to become stable. Steel producers recording record profits, while downstream suffers margin erosion.”

- “Largest raw material provider is refusing to deliver previously accepted purchased orders at accepted prices – demanding 18% price increase to fill previously accepted orders of flat rolled USA stainless steel.”

- “We could greatly grow our business if it were not for steel and labor issues. We could get more orders and employ more people. Supply chains are a mess and we cannot get people to apply. We pay upwards of $20 or more per hour with full benefits.”

- “Liquidity is the BIGGEST issue. Ramp up of production is stressing cash more than usual since we depleted cash during the downturn more than what would have been typical.”

- “The labor shortage is driving up the price of most proteins in food manufacturing.”