‘US Dollar has lost 98.2% of its value since 1913 which renders the DXY meaningless’

‘US Dollar has lost 98.2% of its value since 1913 which renders the DXY meaningless’

(Ryan McMaken) Earlier this month, Larry Kudlow insisted that it is “it’s incumbent on the U.S. government, no matter who’s in power, to maintain the reserve currency status of the dollar.” Kudlow laments that a toppling of the dollar from that perch “seems to be the direction we’re going in.”

The yuan became the most widely-used currency for cross-border transactions in China in March, overtaking the dollar for the first time, official data showed, reflecting efforts by Beijing to internationalise use of the yuan.

(ZeroHedge) In a time when de-dollarization news are dropping fast and furious and even Elon Musk is now jumping on a bandwagon…

Combined with excess government spending, which forces other countries to absorb a significant part of our inflation

— Elon Musk (@elonmusk) March 29, 2023

… which we first defined a decade ago, not a day goes by without some modest or not so modest shift toward a world in which the US currency – fully weaponized after February 2022 for the entire world to see and fear – is no longer the world’s reserve. And today was no exception.

Following a series of corporate cyberattacks that American intelligence agencies have blamed on Russian actors, Russia’s sovereign wealth fund (officially the National Wellbeing Fund) has decided to dump all of its dollars and dollar-denominated assets in favor of those denominated in euros, yuan – or simply buying precious metals like gold, which Russia’s central bank has increasingly favored for its own reserves.

(Stewart Jones) As the Federal Reserve’s quantitative easing practices generate the biggest debt bubble in history, gold futures are trading at record highs, a phenomenon some have called “a bit of a mystery.” However, this “mystery” was solved long ago by the laws of economics. The only “mystery” here is why—contrary to centuries of economic wisdom—we allowed centralized paper money to become the dominant form of currency in the first place.

As recent waves of civil unrest and economic turmoil have prompted some to look back in time and reflect on the observations of the Founding Fathers, it seems most have opted to reject them entirely. Yet among the founders’ many warnings against the institutions that would eventually dominate the modern world are the timeless—and astonishingly accurate—warnings against central banking.

On August 1, 1787, George Washington wrote in a letter to Thomas Jefferson that “paper currency [can] ruin commerce, oppress the honest, and open the door to every species of fraud and injustice.” Jefferson also opposed the concept, warning that “banking establishments are more dangerous than standing armies.” James Madison called paper money “unjust,” recognizing that it allowed the government to confiscate and redistribute property through inflation: “It affects the rights of property as much as taking away equal value in land.”

In other words, inflation is a hidden form of taxation. Washington understood this. Jefferson understood this. Madison understood this. And generations of preeminent economists since then—from Ludwig von Mises to F.A. Hayek, to Murray Rothbard—have understood this quite clearly.

And there’s nothing controversial or mysterious about sound money, that is, currency backed by some form of secure, fixed weight commodity like gold or silver. Both have been valued in some fashion for six thousand years and have been used as currency for around twenty-six hundred years. As confidence in the dollar continues to nosedive, the market is not only putting more confidence in gold and silver, but in some crypto currencies sharing many of the characteristics of gold.

The presidencies of Woodrow Wilson and Franklin D. Roosevelt are rightfully regarded as some of the darkest years for freedom in America. Often overlooked, however, are the deeply repressive monetary policies introduced by both presidents. In 1838, Senator John C. Calhoun foreshadowed the economic evils that would eventually emerge at the peak of the Progressive Era, explaining,

“It is the nature of stimulus…to excite first, and then depress afterwards….Nothing is more stimulating than an expanding and depreciating currency. It creates a delusive appearance of prosperity, which puts everything in motion. Everyone feels as if he was growing richer as prices rise.”

Seventy-five years later, the autocrats running the Wilson administration dealt two devastating blows to liberty with the Federal Reserve Act and the Revenue Act, forever marking 1913 as a tragic year for liberty. Both laws struck at the heart of property rights by establishing the Federal Reserve System and the income tax, respectively. Then, in 1933, Roosevelt issued Executive Order No. 6102, requiring Americans to surrender much of their gold to the US government. Shortly after, Congress passed the Gold Reserve Act of 1934, artificially raising the price of gold and guaranteeing the government a profit of $14.33 for each ounce of gold it had seized from the people.

Finally, in 1971, President Richard Nixon—like any self-respecting twentieth-century Keynesian—committed himself to finishing the work of Wilson and Roosevelt by closing the gold window, forever divorcing the gold standard from the dollar. Rather than usher in a new era of economic stability, this unnatural union between the Fed and the federal government produced a vicious loop of boom-bust cycles and depressions. The consequences have not only been inflation and devaluation (both of which have stripped the people of their purchasing power and savings); now, every time a depression hits, the government is allowed to do two things: grow its power and tax and spend at will without fear of accountability.

In other words, with every inflation of currency comes an inflation of government power.

With government shutdowns of local economies, the second economic quarter of this year was among the worst in history, with the total debt-to-GDP reaching a staggering 136 percent. As the national debt approaches $27 trillion (with even bigger spending bills in the works), we can expect the days of such flagrant government spending to come to a screeching halt. If we continue on this path, that correction will result in an unprecedented collapse of the dollar and the monetary system. The ultimate danger in this scenario: the government eventually confiscates the vast majority or even all private property in order to pay off the national debt. As German American economist Hans Sennholz once said, “Government debt is a government claim against personal income and private property—an unpaid tax bill.”

This is why a dramatic downsizing of government is key to bringing the US out of this manic, outmoded cycle of depressions and upswings. For the government to fulfill its core function as a safeguard of liberty, we must prevent it from meddling in affairs beyond the boundaries prescribed by the Founding Fathers. This includes a swift withdrawal from the use of paper fiat currency and spending cuts across the board.

Such a sweeping transformation could begin with the state governments, the legislatures of which could override the federal government by passing legislation allowing individuals to use gold and silver currency.

Regardless, if meaningful legislative action is not taken somewhere, we have little choice other than to acquiesce to the gloom and terror of socialism—a system that would devour all in its path and make slaves of once free people for generations to come. Freedom is the natural ability of people to control their own destiny. Sound money has the ability to help keep people free.

George Washington’s crossing of the Delaware River

The U.S. Constitution states:

Article 1, Section 8

1. The Congress shall have Power …

5. To coin Money, regulate the value thereof, and of foreign coin….

6. To provide for the punishment of counterfeiting … current coin of the United States.

Article 1, Section 10

- No state shall … emit Bills of Credit and make any Thing but gold and silver Coin a Tender in Payment of Debts.

The intent of the Framers could not have been clearer. The Constitution clearly and unequivocally brought into existence a monetary system based on gold coins and silver coins being the official money of the United States.

Sound Money

Notice that the states are prohibited from issuing “bills of credit.” What are “bills of credit.” That was the term used during that time for paper money. The Constitution expressly prohibited the states from publishing paper money and making anything but gold and silver coins official legal money.

What about the federal government? The Constitution didn’t expressly prohibit it from emitting “bills of credit” like it did with the states. Does that mean that the federal government was empowered to make paper money the official money of the United States?

No, it does not mean that. In the case of the federal government, its powers are limited to those enumerated in the Constitution. If a power isn’t enumerated, then the federal government is automatically prohibited from exercising it.

Therefore, it was unnecessary for the Framers to provide for an express prohibition on the federal government to make paper money the official legal tender of the nation. All that was necessary was to ensure that the Constitution did not empower the federal government to issue paper money.

The powers relating to money that are delegated to the federal government, which are stated above, expressly make it clear that gold coins and silver coins, not paper, were to be the official money of the country. That is reflected by the power given the federal government to “coin money.” At the risk of belaboring the obvious, one does not “coin” paper. Paper is published or “emitted.” It is not coined. Coins are coined.

The provision on counterfeiting also expressly confirms that the official money of the United States was to be gold coins and silver coins. The Framers didn’t provide for punishment for counterfeiting paper money because there was no paper money. They provided for punishment for counterfeiting “current coin of the United States.”

Add up all of these provision and there is but one conclusion that anyone can logically and reasonably draw: The Constitution established a monetary system in which gold and silver coins were to be the official money of the United States.

That’s not to say, of course, that federal officials could not borrow money. The Constitution did give them that power:

Article1, Section 8

1. The Congress shall have Power …

2. To borrow money on the credit of the United States.

When the federal government borrows money, it issues debt instruments to lenders, consisting of bills, notes, or bonds. But everyone understood that federal debt instruments were not money but instead simply promises to pay money. The money that they promised to pay was the gold and silver coins, which were the official money of the country.

And in fact, that was the monetary system of the United States for more than a century, one in which gold coins and silver coins were the official money of the American people.

It is often said that the “gold standard” was a system in which paper money was “backed by gold.” Nothing could be further from the truth. There was no paper money. The “gold standard” was a system where gold coins, along with silver coins, were the official money of the country.

It all came to an end in the 1930s, when the (D) Franklin Roosevelt regime ordered all Americans to deliver their gold coins to the federal government. Anyone who failed to do so would be prosecuted for a federal felony offense and severely punished through incarceration and fine if convicted.

In exchange, people were handed federal debt instruments, ones that promised to pay money. But since the money was now illegal, the debt instruments were promises to pay nothing. That’s reflected by the Federal Reserve Notes that people now use to pay for things.

Roosevelt’s actions were among the most abhorrent in the history of the United States. In one fell swoop, he and his regime destroyed what had been the finest and soundest monetary system in the history of the world, one that contributed mightily to the tremendous increase in prosperity and standards of living in the 19th century.

What is also amazing is that Roosevelt did it without even the semblance of a constitutional amendment. To change a system that the Constitution established requires a constitutional amendment. That is an arduous and difficult process, which is what the Framers wanted. Roosevelt circumvented that process by simply getting Congress to nationalize people’s gold.

The result of Roosevelt’s illegal and immoral actions regarding money and the Constitution? Moral, economic, and monetary debauchery, which has entailed almost 90 years of plundering and looting people through monetary debasement and devaluation to finance the ever-burgeoning expenses of America’s welfare-warfare state way of life.

The solution to all this monetary mayhem is doing what the Framers did: Separate private banking from the state entirely, in the same way that they separated church and state. This means terminate all government involvement in banking, including by ending the private Federal Reserve Bank. And while we’re at it, nationalize the sovereign city, District Of Columbia which would end London and Vatican maritime law control over America. No doubt they won’t go down without a fight however, this is the jump start necessary towards restoring any chance for freedom, peace, and prosperity to our land.

Source: Adapted from an article by Jacob Hornberger, reposted in ZeroHedge

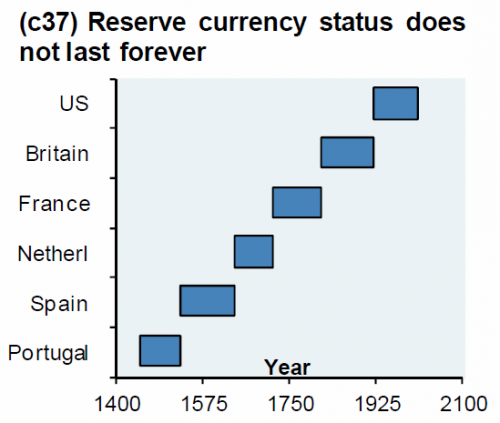

(ZeroHedge) Almost eight year ago, we first presented a chart first created by JPMorgan’s Michael Cembalest, which showed very simply and vividly that reserve currencies don’t last forever, and that in the not too distant future, the US Dollar would also lose its status as the world’s most important currency, since it is never different this time.

As Cembalest put it back in January 2012, “I am reminded of the following remark from late MIT economist Rudiger Dornbusch: ‘Crisis takes a much longer time coming than you think, and then it happens much faster than you would have thought.'”

Perhaps it is not a coincidence then that in light of the growing number of mentions of MMT and various other terminal, destructive monetary policies that have been proposed to kick on the current financial system the can just a little bit longer, that the topic of longevity of reserve currency status is once again becoming all the rage, and none other than JPMorgan’s Private Bank ask in this month’s investment strategy note whether “the dollar’s “exorbitant privilege” is coming to an end?”

So why is JPM, after first creating the iconic chart above which has since spread virally across all financial corners of the internet, not only worried that the dollar’s reserve status may be coming to an end, but in fact goes so far as to state that “we believe the dollar could lose its status as the world’s dominant currency (which could see it depreciate over the medium term) due to structural reasons as well as cyclical impediments.”

Read on to learn why even the largest US bank has started to lose faith in the world’s most powerful currency.

Is the dollar’s “exorbitant privilege” coming to an end?

In Brief

The U.S. dollar (USD) has been the world’s dominant reserve currency for almost a century. As such, many investors today, even outside the United States, have built and become comfortable with sizable USD over weights in their portfolios. However, we believe the dollar could lose its status as the world’s dominant currency (which could see it depreciate over the medium term) due to structural reasons as well as cyclical impediments.

As such, diversifying dollar exposure by placing a higher weighting on other currencies in developed markets and in Asia, as well as precious metals makes sense today. This diversification can be achieved with a strategy that maintains the underlying assets in an investment portfolio, but changes the mix of currencies within that portfolio. This is a completely bespoke approach that can be customized to meet the unique needs of individual clients.

The Rise Of The U.S. Dollar

It is commonly perceived that the U.S. dollar overtook the Great British Pound (GBP) as the world’s international reserve currency with the signing of the Bretton Woods Agreements after World War II. The reality is that sterling’s value was eroded for many decades prior to Bretton Woods. The dollar’s rise to international prominence was fueled by the establishment of the Federal Reserve System a little over a century ago and U.S. economic emergence after World War I. The Federal Reserve System aided in the establishment of more mature capital markets and a nationally coordinated monetary policy, two important pillars of reserve-currency countries. Being the world’s unit of account has given the United States what former French Finance Minister Valery d’Estaing called an “exorbitant privilege” by being able to purchase imports and issue debt in its own currency and run persistent deficits seemingly without consequence.

The Shifting Center

There is nothing to suggest that the dollar dominance should remain in perpetuity. In fact, the dominant international currency has changed many times throughout history going back thousands of years as the world’s economic center has shifted.

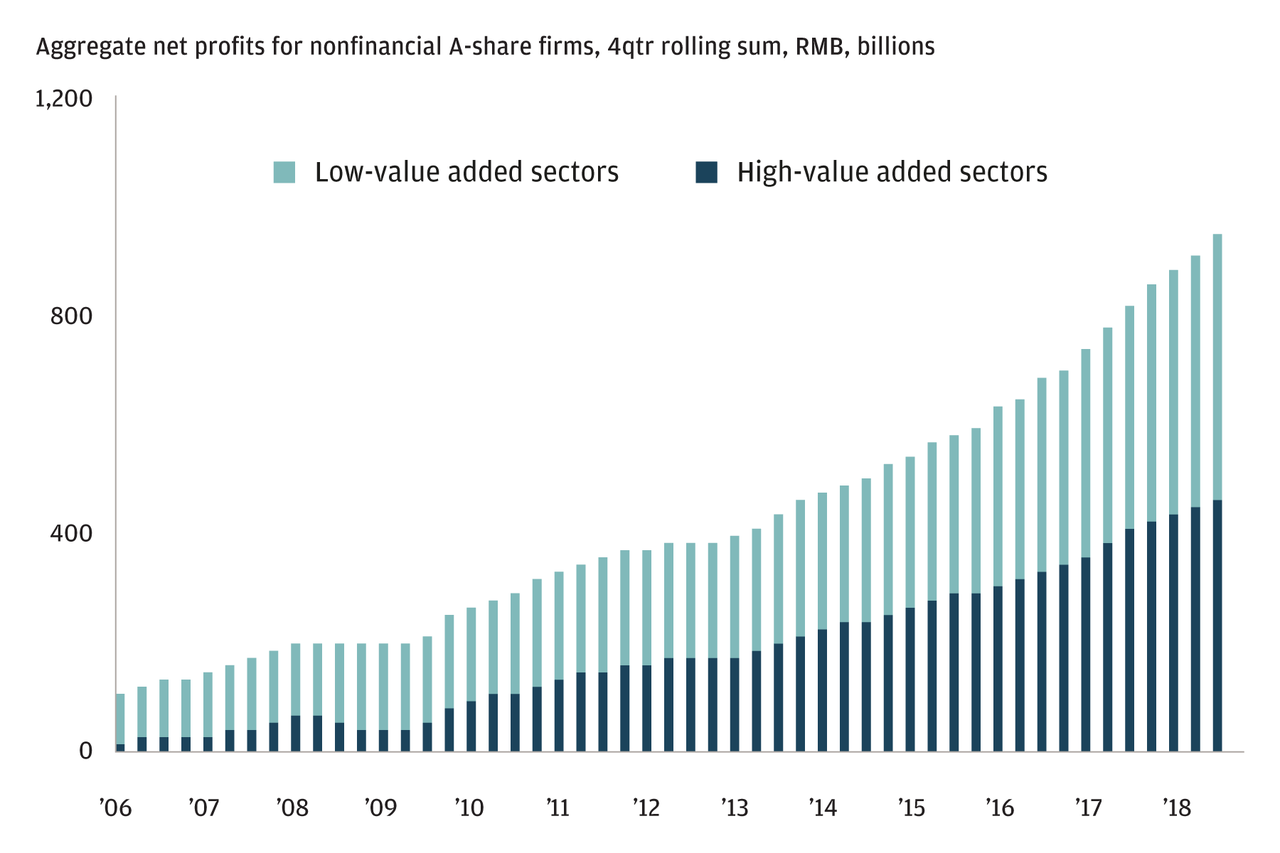

After the end of World War II, the U.S. accounted for biggest share of world GDP at more than 25%. This number is brought to more than 40% when we include Western European powers. Since then, the main driver of economic growth has shifted eastwards towards Asia at the expense of the U.S. and the West. China is at the epicenter of this recent economic shift driven by the country’s strong growth and commitment to domestic reforms. Over the last 70 years, China has quadrupled its share of global GDP to around 20%—roughly the same share as the U.S.—and this share is expected to continue to grow in the years ahead. China is no longer just a manufacturer of low cost goods as a growing share of corporate earnings is coming from “high value add” sectors like technology.

China Regaining Its Status As A Global Superpower

Earnings In China Are Becoming More Balanced

In addition to China, the economies of Southeast Asia, including India, have strong secular tailwinds driven by younger demographics and proliferating technological know-how. Specifically, the Asian economic zone—from the Arabian Peninsula and Turkey in the West to Japan and New Zealand in the East and from Russia in the North and Australia in the South—now represents 50% of global GDP and two-thirds of global economic growth. Of the estimated $30 trillion in middle-class consumption growth between 2015 and 2030, only $1 trillion is expected to come from today’s Western economies. As this region grows, the share of non-USD transactions will inevitably increase which will likely erode the dollar’s “reserveness”, even if the dollar isn’t replaced as the dominant international currency.

In other words, in the coming decades we think the world economy will transition from U.S. and USD dominance toward a system where Asia wields greater power. In currency space, this means the USD will likely lose value compared to a basket of other currencies, including precious commodities like gold.

Dollar’s Declining Role Already Under Way?

Recent data on currency reserve holdings among global central banks suggests this shift may already be under way. As a share of overall central bank reserves, the USD’s role has been declining ever since the Great Recession (see chart). The most recent central bank reserve flow data also suggests that for the first time since the euro’s introduction in 1999, central banks simultaneously sold dollars and bought euros.

Central banks across the globe are also adding to gold reserves at their strongest pace on record. 2018 saw the strongest demand for gold from central banks since 1971 and a rolling four-quarter sum of gold purchases is the strongest on record. To us, this makes sense: gold is a stable source of value with thousands of years of trust among humans supporting it.

USD Share Of Central Bank Reserves, %

Trade Wars Have Long-Term Consequences

The current U.S. administration has called into question agreements with nearly all of its largest partners—tariffs on China, Mexico and the European Union, renegotiating NAFTA, as well as abandoning the Trans Pacific Partnership. A more adversarial U.S. administration could also encourage countries to reduce their reliance on USD in trade. Currently 85% of all currency transactions involve the USD despite the U.S. accounting for only roughly 25% of global GDP.

Countries around the world are already developing payment mechanisms that would avoid using the dollar. These systems are small and still developing but this is likely to be a structural story that will extend beyond one particular administration. In a recent speech on the international role of the euro, Bank for International Settlements Chief Economist Claudio Borio brought up the benefits of pricing oil in the euro saying, “Trading and settling oil in the euro would move payments from dollars to euros and thereby shift ultimate settlement to the euro’s TARGET2 system. This could limit the reach of U.S. foreign policy insofar as it leverages dollar payments.” The European Central Bank also alluded to this theme in a recent report saying that “growing concerns about the impact of international trade tensions and challenges to multilateralism, including the imposition of unilateral sanctions seem to have lent support to the euro’s global standing.”

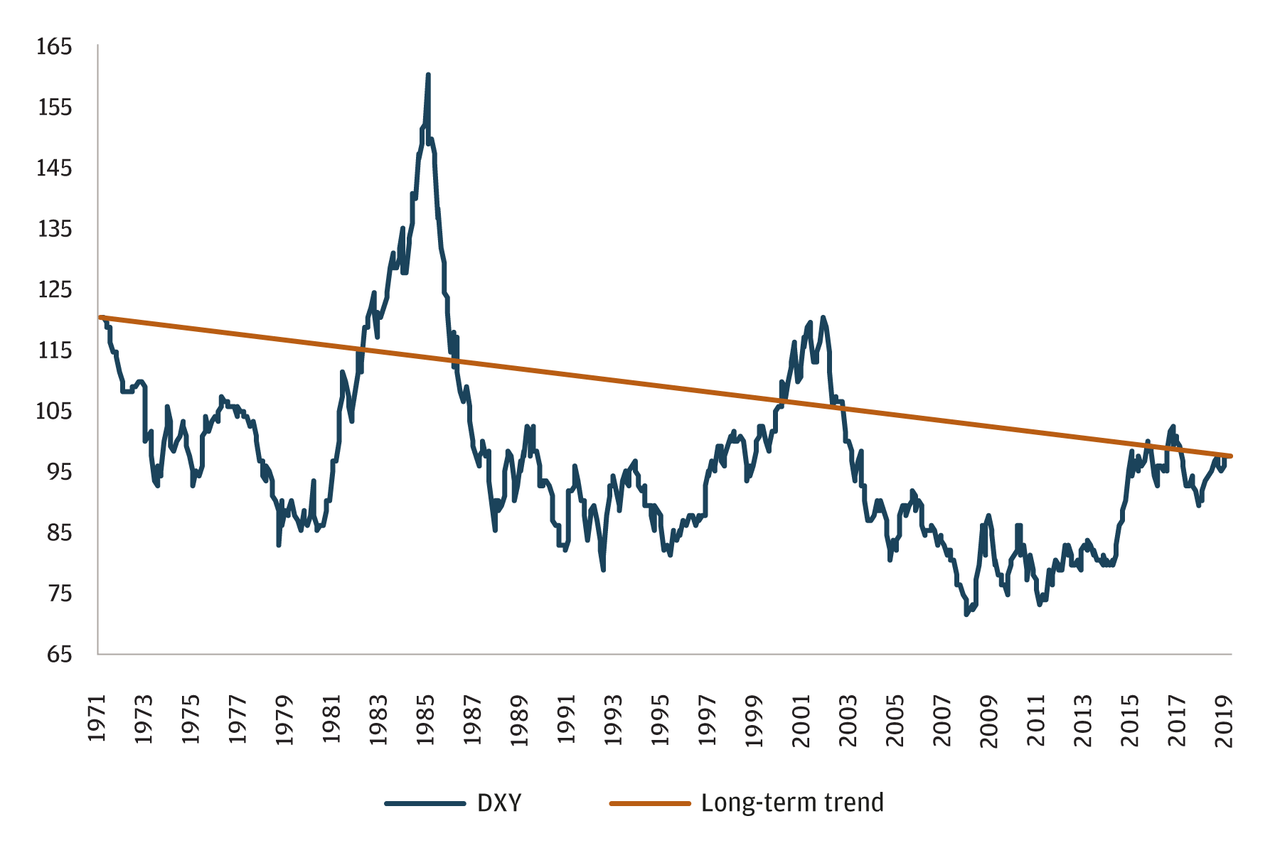

We believe we are at an important juncture. On a real basis, the dollar stands currently more than 10% above its long-term average and on a nominal basis has actually been trending lower for 50 years (see chart below).

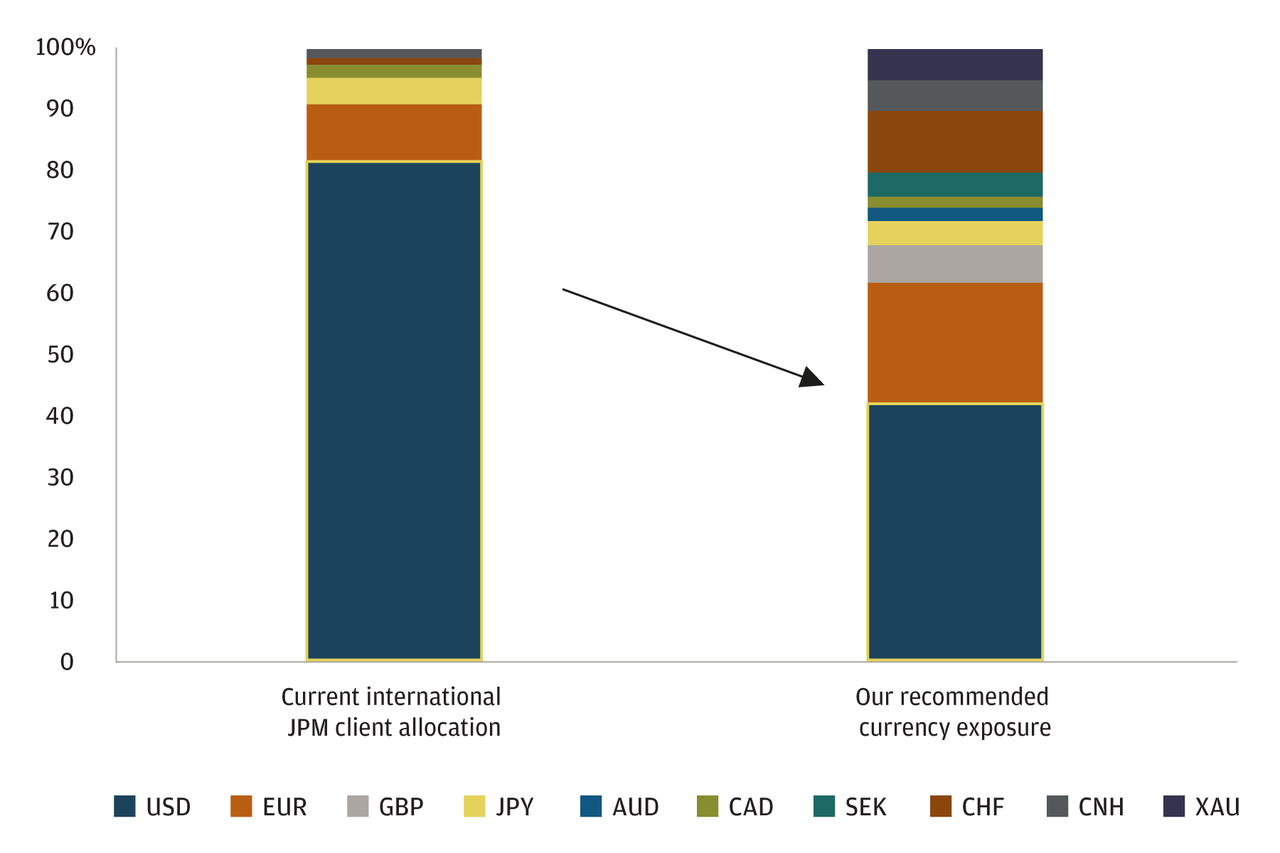

Given the persistent—and rising—deficits in the United States (in both fiscal and trade), we believe the U.S. dollar could become vulnerable to a loss of value relative to a more diversified basket of currencies, including gold. As we scan client portfolios, we see that many of them have far more U.S. dollar exposure than we feel is prudent. At this stage of the economic cycle, we believe this exposure should be more diversified. In many cases, our recommendation would likely be to place a higher weighting on other G10 currencies, currencies in Asia and gold (see chart).

FX Exposure

Source: JPMorgan Private Bank June 13, 2019

The reaction to the “Weaponization” of the US dollar via US sanctions has accelerated the ongoing global de-dollarization efforts. We outlined the rapidly unfolding developments earlier this year in our 151 page Annual Thesis paper entitled, De-Dollarization. Documented de-dollarization efforts are now underway in China, Russia, Venezuela, Iran, India, Turkey, Syria, Qatar, Pakistan, Lebanon, Libya, Egypt, Philippines and more.

The real power of the dollar is its relationship with sanctions programs. Legislation such as the International Emergency Economic Powers Act, The Trading With the Enemy Act and The Patriot Act have allowed Washington to weaponize payment flows. The proposed Defending Elections From Threats by Establishing Redlines Act and Defending American Security From Kremlin Aggression Act would extend that armory.

When combined with access it gained to data from Swift, the Society for Worldwide Interbank Financial Telecommunication’s global messaging system, the U.S. exerts unprecedented control over global economic activity. Sanctions target persons, entities, organizations, a regime or an entire country. Secondary curbs restrict foreign corporations, financial institutions and individuals from doing business with sanctioned entities. Any dollar payment flowing through a U.S. bank or the American payments system provides the necessary nexus for the U.S. to prosecute the offender or act against its American assets. This gives the nation extraterritorial reach over non-Americans trading with or financing a sanctioned party. The mere threat of prosecution can destabilize finances, trade and currency markets, effectively disrupting the activities of non-Americans.

The countries cited above are aggressively reacting to this. Gold is non-digital and does not move through electronic payments systems, so it is impossible for the U.S. to freeze on interdict.

Central banks are stocking up on gold. According to the World Gold Council, net buying by central banks reached 145.5 tons in the first quarter of 2019. That’s a 68% increase over last year. And it’s the most gold central banks have bought in the first quarter since 2013.

Soon both the buying of gold by major players such as Russia, China, India, Iran and Turkey, along with an emerging gold backed cryptocurrency for international settlements, will take gold towards testing prior 2011 highs.

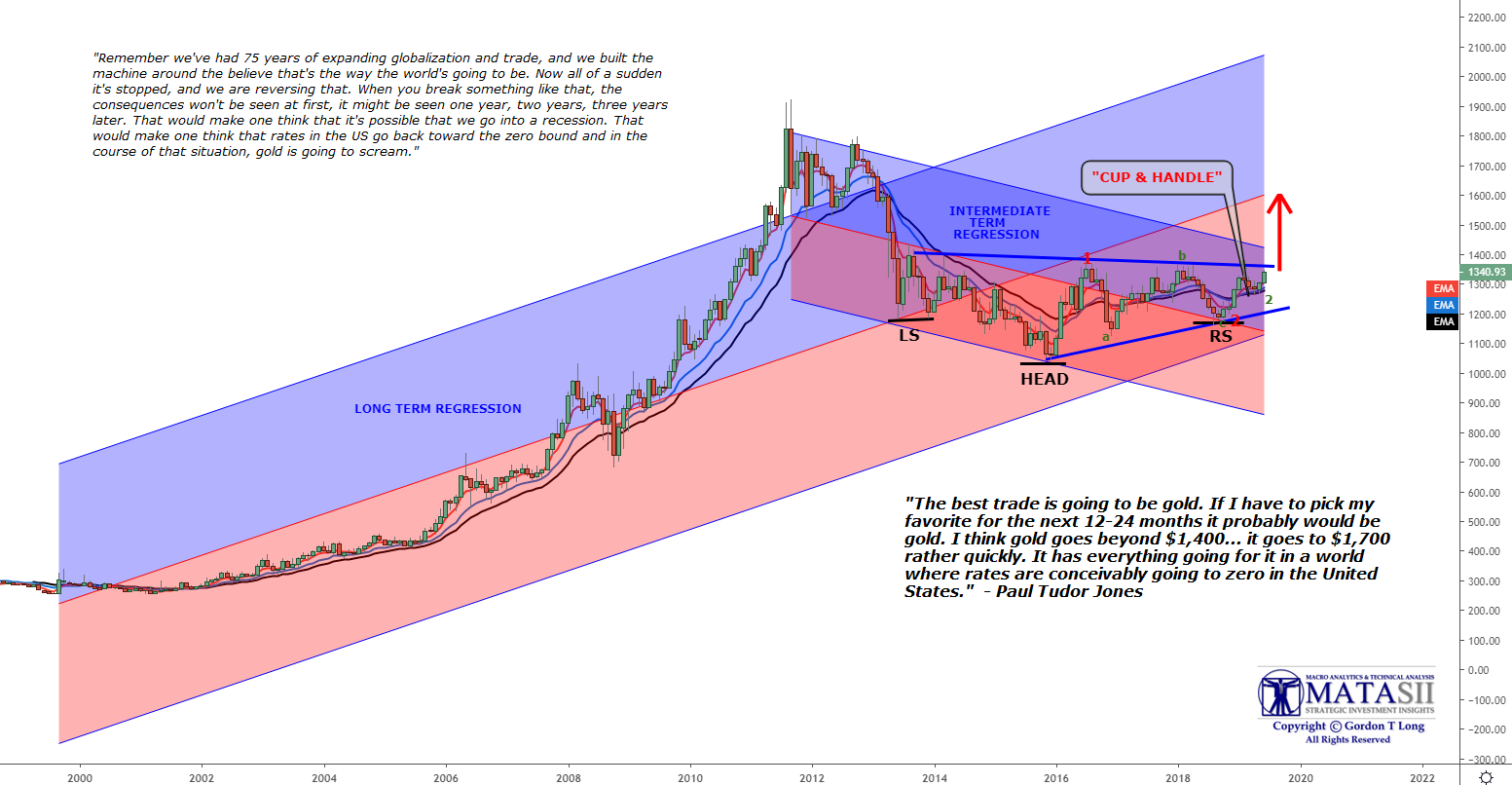

Major investors such as Paul Tudor Jones recently went on record as saying:

“The best trade is going to be gold. If I have to pick my favorite for the next 12-24 months it probably would be gold. I think gold goes beyond $1,400… it goes to $1,700 rather quickly. It has everything going for it in a world where rates are conceivably going to zero in the United States.”

“Remember we’ve had 75 years of expanding globalization and trade, and we built the machine around the believe that’s the way the world’s going to be. Now all of a sudden it’s stopped, and we are reversing that. When you break something like that, the consequences won’t be seen at first, it might be seen one year, two years, three years later. That would make one think that it’s possible that we go into a recession. That would make one think that rates in the US go back toward the zero bound and in the course of that situation, gold is going to scream. “

Of course, we have heard this sort of talk ever since gold hit its prior high in 2011.

However, this time the technical charts are starting to sing the same tune with lyrics such as “Reverse Head & Shoulders”, “Cup & Handle” and “Bullish Ascending Triangle”.

All of this leaves us currently at critical overhead resistance levels, which if broken will likely take gold denominated in US dollar towards previous highs.

What the gold buying strategies of Russia, China, India, Iran, Turkey et al. have in common is a desire to escape from dollar hegemony and the imposition of dollar-based sanctions by the U.S. The practical implication for gold investors is a firm floor under gold prices since these players can be relied upon to buy any dips.

According to James Rickards:

“The primary factor that has been keeping a lid on gold prices is the strong dollar. The dollar itself has been propped up by the Fed’s policy of raising interest rates and reducing money supply, so-called “quantitative tightening” or QT. These tight money policies have amplified disinflationary trends and pushed the Fed further away from its 2% inflation goal.

However, the Fed reversed course on rate hikes last December and has announced it will end QT next September. These actions will make gold more attractive to dollar investors and lead to a dollar devaluation when measured in gold.

The price of gold in euros, yen and yuan could go even higher since the ECB, Bank of Japan and People’s Bank of China will still be trying to devalue against the dollar as part of the ongoing currency wars. The only way all major currencies can devalue at the same time is against gold, since they cannot simultaneously devalue against each other.

A situation in which there is a solid floor on the dollar price of gold and a need to devalue the dollar means only one thing – higher dollar prices for gold. A breakout to the upside is the next move for gold.“

Former Assistant Secretary of HUD, Catherine Austin Fitts, explains what covert wars for resources resulting from the US Dollar System Domination means for the rest of us.

Not to Americans…

(Paul Craig Roberts) The housing market is now apparently turning down. Consumer incomes are limited by jobs offshoring and the ability of employers to hold down wages and salaries. The Federal Reserve seems committed to higher interest rates – in my view to protect the exchange value of the US dollar on which Washington’s power is based. The arrogant fools in Washington, with whom I spent a quarter century, have, with their bellicosity and sanctions, encouraged nations with independent foreign and economic policies to drop the use of the dollar. This takes some time to accomplish, but Russia, China, Iran, and India are apparently committed to dropping or reducing the use of the US dollar.

A drop in the world demand for dollars can be destabilizing of the dollar’s value unless the central banks of Japan, UK, and EU continue to support the dollar’s exchange value, either by purchasing dollars with their currencies or by printing offsetting amounts of their currencies to keep the dollar’s value stable. So far they have been willing to do both. However, Trump’s criticisms of Europe has soured Europe against Trump, with a corresponding weakening of the willingness to cover for the US. Japan’s colonial status vis-a-vis the US since the Second World War is being stressed by the hostility that Washington is introducing into Japan’s part of the world. The orchestrated Washington tensions with North Korea and China do not serve Japan, and those Japanese politicians who are not heavily on the US payroll are aware that Japan is being put on the line for American, not Japanese interests.

If all this leads, as is likely, to the rise of more independence among Washington’s vassals, the vassals are likely to protect themselves from the cost of their independence by removing themselves from the dollar and payments mechanisms associated with the dollar as world currency. This means a drop in the value of the dollar that the Federal Reserve would have to prevent by raising interest rates on dollar investments in order to keep the demand for dollars up sufficiently to protect its value.

As every realtor knows, housing prices boom when interest rates are low, because the lower the rate the higher the price of the house that the person with the mortgage can afford. But when interest rates rise, the lower the price of the house that a buyer can afford.

If we are going into an era of higher interest rates, home prices and sales are going to decline.

The “on the other hand” to this analysis is that if the Federal Reserve loses control of the situation and the debts associated with the current value of the US dollar become a problem that can collapse the system, the Federal Reserve is likely to pump out enough new money to preserve the debt by driving interest rates back to zero or negative.

Would this save or revive the housing market? Not if the debt-burdened American people have no substantial increases in their real income. Where are these increases likely to come from? Robotics are about to take away the jobs not already lost to jobs offshoring. Indeed, despite President Trump’s emphasis on “bringing the jobs back,” Ford Motor Corp. has just announced that it is moving the production of the Ford Focus from Michigan to China.

Apparently it never occurs to the executives running America’s off shored corporations that potential customers in America working in part time jobs stocking shelves in Walmart, Home Depot, Lowe’s, etc., will not have enough money to purchase a Ford. Unlike Henry Ford, who had the intelligence to pay workers good wages so they could buy Fords, the executives of American companies today sacrifice their domestic market and the American economy to their short-term “performance bonuses” based on low foreign labor costs.

What is about to happen in America today is that the middle class, or rather those who were part of it as children and expected to join it, are going to be driven into manufactured “double-wide homes” or single trailers. The MacMansions will be cut up into tenements. Even the high-priced rentals along the Florida coast will find a drop in demand as real incomes continue to fall. The $5,000-$20,000 weekly summer rental rate along Florida’s panhandle 30A will not be sustainable. The speculators who are in over their heads in this arena are due for a future shock.

For years I have reported on the monthly payroll jobs statistics. The vast majority of new jobs are in lowly paid nontradable domestic services, such as waitresses and bartenders, retail clerks, and ambulatory health care services. In the payroll jobs report for June, for example, the new jobs, if they actually exist, are concentrated in these sectors: administrative and waste services, health care and social assistance, accommodation and food services, and local government.

High productivity, high value-added manufactured jobs shrink in the US as they are offshored to Asia. High productivity, high value-added professional service jobs, such as research, design, software engineering, accounting, legal research, are being filled by offshoring or by foreigners brought into the US on work visas with the fabricated and false excuse that there are no Americans qualified for the jobs.

America is a country hollowed out by the short-term greed of the ruling class and its shills in the economics profession and in Congress. Capitalism only works for the few. It no longer works for the many.

On national security grounds Trump should respond to Ford’s announcement of offshoring the production of Ford Focus to China by nationalizing Ford. Michigan’s payrolls and tax base will decline and employment in China will rise. We are witnessing a major US corporation enabling China’s rise over the United States. Among the external costs of Ford’s contribution to China’s GDP is Trump’s increased US military budget to counter the rise in China’s power.

Trump should also nationalize Apple, Nike, Levi, and all the rest of the offshored US global corporations who have put the interest of a few people above the interests of the American work force and the US economy. There is no other way to get the jobs back. Of course, if Trump did this, he would be assassinated.

America is ruled by a tiny percentage of people who constitute a treasonous class. These people have the money to purchase the government, the media, and the economics profession that shills for them. This greedy traitorous interest group must be dealt with or the United States of America and the entirety of its peoples are lost.

In her latest blockbuster book, Collusion, Nomi Prins documents how central banks and international monetary institutions have used the 2008 financial crisis to manipulate markets and the fiscal policies of governments to benefit the super-rich.

These manipulations are used to enable the looting of countries such as Greece and Portugal by the large German and Dutch banks and the enrichment via inflated financial asset prices of shareholders at the expense of the general population.

One would think that repeated financial crises would undermine the power of financial interests, but the facts are otherwise. As long ago as November 21, 1933, President Franklin D. Roosevelt wrote to Col. House that “the real truth of the matter is, as you and I know, that a financial element in the larger centers has owned the Government ever since the days of Andrew Jackson.”

Thomas Jefferson said that “banking institutions are more dangerous to our liberties than standing armies” and that “if the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks . . . will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered.”

The shrinkage of the US middle class is evidence that Jefferson’s prediction is coming true.

By quick way of review, here’s the key chart. As you can see, the $USD staged a large bull market run in 2014 as the [Foreign] Federal Reserve wound down its QE program. The greenback was then range bound for three years until this month when it broke down in a big way.

US Dollar ($USD) dropping below critical support.

Here’s the $USD’s chart running back 40 years. I call this the “single most important chart in the world,” because how the $USD moves has a massive impact on all other asset classes.

As you can see the $USD broke out of a massive 40 year falling wedge pattern [between 2014-2016]. This initial breakout has failed to reach its ultimate target (120) and is now rolling over for a retest of the upper trendline in the mid-to low-80s.

The Long Term [40 year] Chart Of The $USD

What happens when new currency is created with few limits by central and commercial banks?

Answer:

Far too much debt and currency are created.

Central Bank Balance Sheets have increased by $10 trillion in the last decade and $1 trillion YTD in 2017.

Question:

What happens when an extra $10 trillion in central bank debt plus another $80 trillion or so in other global debt is created in a decade?

Answer:

Prices rise because each unit of fiat currency purchases less.

NASDAQ Composite 2,400 6,000

S&P 500 Index 1,400 2,370

T-Bond 110 150

Gold 700 1,250

Silver 13 18

Crude Oil 60 50

Now might be a good time to grab some physical gold, silver and cold stored Crypto.

It seems the end really is nigh for the U.S. dollar.

It seems the end really is nigh for the U.S. dollar.

And the mudfight for global dominance and currency war couldn’t be more ugly or dramatic.

The Saudis are now openly threatening to take down the U.S. economy in the ongoing fallout over collapsing oil prices and tense geopolitical events involving the 9/11 cover-up. The New York Times reports:

Saudi Arabia has told the Obama administration and members of Congress that it will sell off hundreds of billions of dollars’ worth of American assets held by the kingdom if Congress passes a bill that would allow the Saudi government to be held responsible in American courts for any role in the Sept. 11, 2001, attacks.

China has been working for years to establish global currency status, and will strengthen the yuan by backing it with gold in moves clearly designed to cripple the role of the dollar. Zero Hedge reports:

China’s shift to an official local-currency-based gold fixing is “the culmination of a two-year plan to move away from a US-centric monetary system,” according to Bocom strategist Hao Hong. In an insightfully honest Bloomberg TV interview, Hong admits that “by trading physical gold in renminbi, China is slowly chipping away at the dominance of US dollars.”

Putin also waits in the shadows, making similar moves and creating alliances to out-balance the United States with a growing Asian economy on the global stage.

Luke Rudkowski of WeAreChange asks “Is This The End of the U.S. Dollar?” in the video below.

He writes:

In this video Luke Rudkowski reports on the breaking news of both China and Saudi Arabia making geopolitical moves that could cause a U.S economic collapse and obliteration of the U.S hegemony petrodollar. We go over China’s new gold backed yuan that cannot be traded in U.S dollars and rising tension with Saudi Arabia threatening economic blackmail if their role in 911 is exposed.

Visit WeAreChange.org where this video report was first published.

The Federal Reserve, Henry Kissinger, the Rockefellers and their allies created the petrodollar and insisted upon the world using the U.S. dollar to buy oil, placing debt in American currency and entire countries under the yoke of the West.

But that paradigm has been crumbling as world order shifts away from U.S. hegemony.

It is a matter of when – not if – these events will change the U.S. financial landscape forever.

As SHTF has warned, major events are taking place, and no one can say if stability will be here tomorrow.

Stay vigilant, and prepare yourself and your family as best as you can.

Read more:

Pay Attention To The Economy Right Now, Because A Disturbing Series Of Events Seems To Be In Motion

Here’s How We Got Here: A Short Primer On The History Of The Petrodollar

Shock Report: China Dumps Half a Trillion Dollars: “Something Is Very, Very Wrong”

Dollar Moves Shake the World: “Federal Reserve Could Start a Currency War”