‘US Dollar has lost 98.2% of its value since 1913 which renders the DXY meaningless’

‘US Dollar has lost 98.2% of its value since 1913 which renders the DXY meaningless’

(Alasdiar Macleod) We will look back at current events and realize that they marked the change from a dollar-based global economy underwritten by financial assets to commodity-backed currencies. We face a change from collateral being purely financial in nature to becoming commodity based. It is collateral that underwrites the whole financial system.

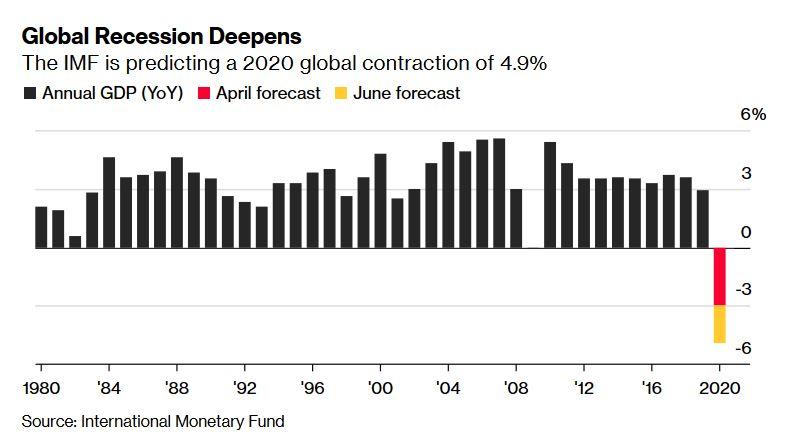

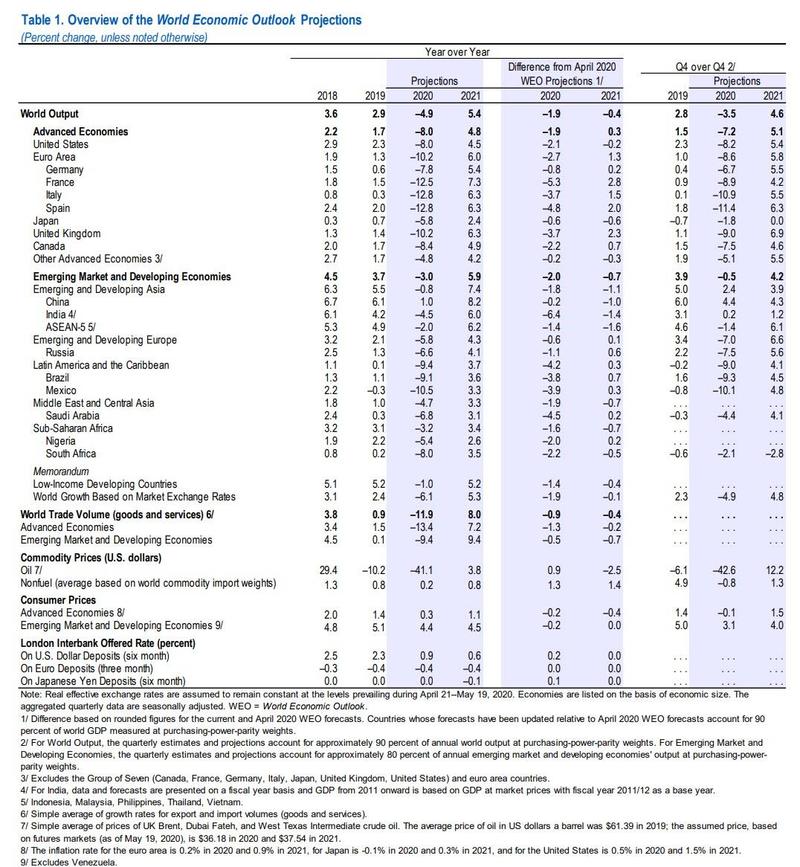

In the latest revision to the IMF’s economic outlook published this morning, the fund warns that the world is facing “a crisis like no other”, and now expects global growth to shrink -4.9% in 2020, 1.9% below the April 2020 forecast of -3.0%.

The COVID-19 pandemic has had a more negative impact on activity in the first half of 2020 than anticipated, the IMF said, adding that the recovery is projected to be more gradual than previously forecast. In 2021 global growth is projected at 5.4% down from 5.8%, a number which will also be revised lower, with China’s expected 1.0% growth (down from 1.2%) the big wildcard.

As shown in the table below, the IMF has made the following GDP revisions for 2020:

India suffered the biggest downward GDP revision from the April forecasts, with a 4.5% contraction now expected, compared with a prior projection of a 1.9% expansion. Latin America has been hit by the virus due in part due to less developed health systems; its two biggest economies Brazil and Mexico are now forecast to contract 9.1% and 10.5%, respectively.

“With the relentless spread of the pandemic, prospects of long-lasting negative consequences for livelihoods, job security and inequality have grown more daunting,” the global emergency lender said in its update to the World Economic Outlook.

The IMF conceded that as with the April 2020 WEO projections, there is a higher-than-usual degree of uncertainty around this forecast, with the baseline projection resting on key assumptions about the fallout from the pandemic.

In economies with declining infection rates, the slower recovery path in the updated forecast reflects:

The fund lowered its expectations for consumption in most economies based on a larger-than-expected disruption to domestic activity, demand shocks from social distancing and an increase in precautionary savings.

For economies struggling to control infection rates, a lengthier lockdown will inflict an additional toll on activity. Moreover, the forecast assumes that financial conditions—which have eased following the release of theApril 2020 WEO—will remain broadly at current levels. Alternative outcomes to those in the baseline are clearly possible, and not just because of how the pandemic is evolving. The extent of the recent rebound in financial market sentiment appears disconnected from shifts in underlying economic prospects—as the June 2020 Global Financial Stability Report (GFSR) Update discusses—raising the possibility that financial conditions may tighten more than assumed in the baseline.

Overall, this would leave 2021 GDP some 6.5% percentage points lower than in the pre-COVID-19 projections of January 2020. The adverse impact on low-income households is particularly acute, imperiling the significant progress made in reducing extreme poverty in the world since the 1990s.

More importantly, the IMF also warned that the rebound in “financial market sentiment appears disconnected from shifts in underlying economic prospects raising the possibility that financial conditions may tighten more than assumed in the baseline.”

Back to the surprisingly gloomy forecast, the IMF said that downside risks remain significant, as “outbreaks could recur in places that appear to have gone past peak infection, requiring the reimposition of at least some containment measures. A more prolonged decline in activity could lead to further scarring, including from wider firm closures, as surviving firms hesitate to hire jobseekers after extended unemployment spells, and as unemployed workers leave the labor force entirely.”

Furthermore, financial conditions may again tighten as in January–March, exposing vulnerabilities among borrowers. “This could tip some economies into debt crises and slow activity further.” Moreover, the sizable policy response following the initial sudden stop in activity may end up being prematurely withdrawn or improperly targeted due to design and implementation challenges, leading to misallocation and the dissolution of productive economic relationships.

The IMF warned of a collapse in global trade volume in goods and services, which is expected to tumble 11.9% in 2020.

Finally, the IMF warned that the pandemic’s impact may significantly increase inequality, with more than 90% of emerging-market and developing economies forecast to show declines in per capita income.

Oddly enough, it had nothing to say about the biggest source of global inequality for the past decade: central banks that have injected over $30 trillion in liquidity in the past ten years, and whose actions assure that the next crash may well be the last.

* * *

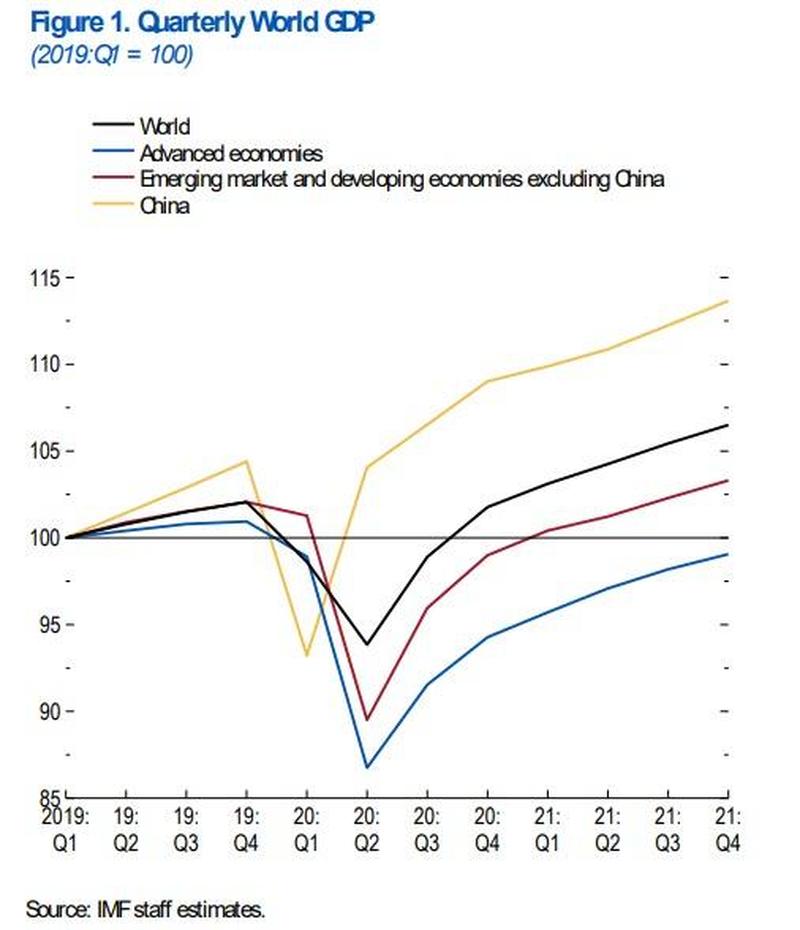

Looking ahead, The IMF presents two alternative scenarios: In one, there’s a second virus outbreak in early 2021, with disruptions to domestic economic activity about half the size of those assumed for this year. The scenario assumes emerging markets experience greater damage than advanced economies, given more limited space to support incomes. In that case, output would be 4.9% below the baseline for 2021 and would remain below the baseline in 2022. In the second scenario, with a faster-than-expected recovery, global output would be about a half percentage point better than the baseline this year and 3% above the baseline in 2021.

“We are ruined if we do not overrule the principles that the more we owe, the more prosperous we shall be” – Thomas Jefferson

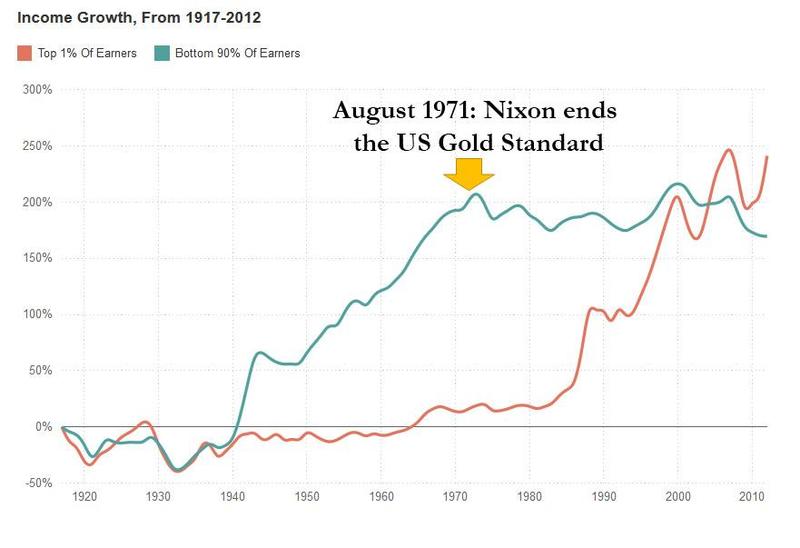

There is no more subversive entity in the US, more destructive, more inflammatory yet out of the spotlight of public outrage, than the Federal Reserve: it is the Fed’s actions over the past 108 years – and especially over the past decade – that have spawned much of the anger, resentment and hatred that has permeated US society to its very core as a result of the Fed’s monetary policies.

Yet because much of the public fails to grasp the insidious implications of endless money-printing which makes owners of assets exorbitantly rich at the expense of regular workers, popular anger at the Fed remains virtually non-existent, despite clear warnings from Thomas Jefferson, and countless others over the decades, about the dangers posed by central banking.

And so, taking advantage of the general public’s general gullibility, the Fed continues to lie and dissemble at every opportunity, of which the most recent example was last week when Powell said that “inequality has been with us for increasingly for four decades” and arguing that monetary policy is not a cause for that. What he forgot to mention is that four decades ago is when the Nixon closed the gold window….

… severing the last link of the US dollar to tangible value, and allowing the Fed to print with impunity, creating the current wealth divide which has now spilled over into the streets of America.

One other thing the Fed has been consistently lying about is that it does not monetize the debt. The chart below is evidence that this, too, is a lie, with US Treasury debt increasing by $2.86 trillion in 2020 (most of it in the past three months) which is less than the $3.0 trillion increase in the Fed’s balance sheet over the same period. In other words, the Fed has monetized 105% of all Treasury issuance this year.

So although Powell may never admit it, Helicopter Money, also known as “MMT”, is now here, and will never go away as Deutsche Bank hinted earlier.

And speaking of MMT, below we republish the latest article from Adventures in Capitalism discussing how MMT is Going Mainstream – yes, even rap musicians endorse MMT now – and how this wanton printing of money to address every social ill will have profound ramifications that will last generations.

So without further ado, here is…

“MMT Going Mainstream…” by Kuppy of ‘Adventures in Capitalism’

My good friend Kevin Muir from Macro Tourist (I highly recommend that you subscribe) has been banging on about Modern Monetary Theory (MMT) for ages. I’ll admit, some of his pieces have been difficult to read as I’m firmly planted in the Austrian school—I believe gold is money and everything else is fiat. I believe governments create inefficiency and corruption while politicizing common sense ideas. I am against MMT in all of its insidious forms as it only legitimatizes all that I disagree with. With that out of the way, I’ve matured enough to know that what I think doesn’t matter. My job isn’t to stake the moral high ground; it is to make money for my hedge fund clients by noticing trends before others do. While I disagree strongly with MMT, Kevin has been right to repeatedly educate himself and his readers on MMT because it’s coming (whether or not you want it).

With Kevin’s permission, I have re-posted his most recent MMT note in full. I think this will be one of the most important macro pieces I’ll post on this site. There’s been a fundamental change in how governments tax and spend, yet most do not yet realize it. MMT is going mainstream. Are you ready…???

Yesterday, MMT-advocate, Stephanie Kelton released her much-awaited book, The Deficit Myth.

You might think MMT to be a crock. It might make every bone in your body shudder. You might feel sick to your stomach as you read the theory. These are just a few of the responses I have heard from traditionally trained hard-money types who learn about MMT.

I suspect most of you know that I am open-minded to many aspects of MMT, but expect it will be taken too far – just like monetarism has been taken too far.

When I see the extreme monetary policy of Europe and other countries with negative rates, all I can ask is how can anyone claim with a straight face that monetarism is working for us? So yeah, I would rather try something new than continue down the current road of easier and easier monetary policy.

Yet, what you or I think about a particular economic policy doesn’t mean squat. I am not here to debate what should be done, but what will be done.

So let’s put aside the economic merits of the different schools of thought, and focus on discounting their probable implementation.

The Deficit Myth

I haven’t yet fully read Prof Kelton’s book, but glancing at the introduction, she does an admirable job sketching out her viewpoint in easy-to-understand layman’s terms. I have taken the liberty of pulling the important bits:

There is nothing new in Kelton’s introduction. MMT’ers have understood these concepts for more than a decade.

But we always must remind ourselves, as traders and investors, what’s important is to discount how the public perceives those ideas. Remember the whole Keynesian beauty contest concept (probably not the most politically correct analogy, but let’s remember that Keynes lived in a different era. In fact, I suspect if Keynes were alive today, he would be more politically correct than some of his most vocal opponents –Niall Ferguson apologizes for remarks).

Keynes rightfully understood that investors discount what the crowd will perceive as the most likely outcome as opposed to the best choice.

Which brings me to my main point. And I know some of you might think this is nuts. But I don’t care.

I have been watching for signs that the concept of “governments are not financially restrained” taking hold within the non-financial community.

I have even postulated that the corona virus crisis might prove to be the tipping point for this theory gaining traction. With all the extreme fiscal measures being put in place (without undue immediate negative effects), the public might realize that the government’s large fiscal response works miracles at staving off short-term economic pain. They might suddenly understand there is nothing holding society back from doing that again for other priorities.

Well, I think I got my signal. Earlier in the week, I noticed a popular rapper tweeting out the following:

Yup. The whole theory behind MMT is being endorsed by rap musicians now!

When disputing the need for a balanced fiscal budget, MMT’ers have often resorted to the argument, “if there is always money for war, then why isn’t there always money for other social programs?”

I don’t want to dispute the validity of their argument. However, the narrative that “we need to balance budgets” has been torn down by the corona crisis better than the war argument ever did.

Over the last month, a growing portion of society has concluded that there was never any financial constraint to spending money.

I know the hard-money and traditionally-trained-economic thinkers will scream bloody murder at that thought. I get it. It doesn’t seem to make any sense. How can there be a free lunch? There is no such thing.

I will repeat again – I don’t want to discuss the merits of MMT. We will save that for another post.

What’s important – and it’s probably the most important thing that has ever happened in my investing career – is that the narrative surrounding deficit spending has changed.

Deficits are no longer “bad”. The budget hawks have all been silenced.

This will have ramifications that will last generations.

If this MMT school of thought continues to gain traction, then many of the investment playbooks from the last few decades need to be thrown out the window. It will be as a dramatic shift as the 1981-Paul-Volcker-stamping-out-of-inflation. It will be an end of an era.

Over the course of the coming months I will discuss the long-term investment consequences. But I wanted to highlight that MMT is about to go mainstream. And as it becomes more popular, it will turn investing as we know it on its head.

Decades from now we will look back at the corona crisis and say it changed more than just our attitudes about viruses, it marked the beginning of a change in the way we think about money.

Americans have become numb to financial intelligence. This is no more evident than a recent Sallie Mae survey, which indicated that college graduates can’t even answer simple questions about financial concepts, such as interest.

The statistics are not looking good for the United States, a nation deeply indebted, addicted to consumerism, and woefully ignorant about it all. Not long ago, SHTFPlanreported that a mere 1 in 10 Americans is actually capable of getting an A on a basic financial security test.

And even college graduates, who are likely tens of thousands (if not more) dollars in debt because of school, learned little to nothing about handling their personal finances. The big red flag comes from consumer banking firm Sallie Mae. The firm released its new “Majoring in Money” study which asked hundreds of current and recently graduated college students up to age 29 about basic financial concepts. The results are worrisome.

Sallie Mae asked these individuals four questions related to credit and interest, and fewer than one in four got all four of these correct.

1. Interest accumulation:

Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow?

a. More than $102

b. Exactly $102

c. Less than $102

d. Not sure2. Effects of payment behavior on credit cost:

Assuming the following individuals have the same credit card with the same interest rate and balance, which will pay the most in interest on their credit card purchases over time?

a. Joe, who makes the minimum payment on his credit card bill every month

b. Jane, who pays the balance on her credit card in full every month

c. Joyce, who sometimes pays the minimum, sometimes pays less than the minimum and missed one payment on her credit card bill

d. All of them will pay the same amount in interest over time

e. Not sure3. Impact of repayment term on cost of credit:

Imagine that there are two options when it comes to paying back a loan and both come with the same interest rate. Provided you have the needed funds, which option would you select to minimize your total costs over the life of the loan (i.e., all of your payments combined until the loan is completely paid off)?

a. Option 1 allows you to take 10 years to pay back the loan

b. Option 2 allows you to take 20 years to pay back the loan

c. Both options have the same out-of-pocket cost over the life of the loan

d. Not sure4. Interest terminology:

Which of the following best defines the term “interest capitalization”?

a. The type of interest charged on high-balance loans

b. The addition of unpaid interest to the principal balance of a loan

c. Interest that is charged when you postpone payments on your loan

The fact that we have an entire generation, largely college educated, who cannot answer these questions does not bode well for our future as a society. Not knowing the answers to these could end up costing people a lot of money down the road. According to Market Watch, 83% of college grads carry a credit card as revealed by Sallie Mae, but only about six in 10 say they pay the balance(s) in full and on time each month. Coupled with the fact that nearly seven in 10 college students take out student loans, graduating with an average of nearly $30,000 in debt, the decline in financial intelligence is evident.

There are ways to learn the basics of personal finance. Dave Ramsey’s Total Money Makeover book was of the most help to many people, and Ramsey is perhaps the most well-known personal finance guru out there. He takes a strick “no debt” approach that has worked not only for himself, buy countless others. He also offers an easy to follow guide which he’s dubbed “the baby steps” that will get people on the path to financial freedom.

Other resources are those such as Robert Kiyosaki’s Rich Dad, Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle Class Do Not!

Both books are excellent resources that teach the very basics about money and personal finance that no one is learning about in their public school educations.

* * *

The answers are 1: A, 2: C, 3: A, and 4: B

Eariler this week, when the San Fran Fed published a paper that suggested that the recovery would have been stronger if only the Fed had cut rates to negative, we proposed that this is nothing more than a trial balloon for the next recession/depression, one in which the Federal Reserve will seek affirmative “empirical evidence” that greenlights this unprecedented NIRPy step (in addition to QE of course).

Today, in his latest note to clients after returning from a 2 week vacation in Jamaica, SocGen’s Albert Edwards picks up on this point and cranks it up to 11 writing that “as central banks thrash around for new tools, I have long thought the next recession would trigger the adoption of helicopter money and deeply negative Fed Funds. Clients have been sceptical of the latter because of the negative impact on bank margins, but now I am more convinced than ever that we will see negative Fed Funds.”

Predictably, Edwards takes aim at the SF Fed “analysis”, writing that “just because the San Fran Fed has published this paper doesn’t mean the Washington Fed will adopt the policy in the next recession, but with this economic cycle clearly now in its final act, one can sense that a number of trial balloons are being floated on what the Fed might do in the next recession. This is just one of them.“

More to the point, Edwards also focuses on the recent resurgence of interest in Modern-Money Theory, i.e., MMT, or government-mandated helicopter money, which is predictably a “theory” espoused by socialists everywhere most notably Bernie Sanders and his economic advisors…

… and writes that “many of the more radical Democrats in the US seem to be adopting the idea and since I expect the US budget deficit to soar to 15% of GDP in the next recession, the ideas of MMT will surely become even more popular.” Edwards is convinced that “the Fed and other central banks will be desperate enough to adopt outright monetisation (aka helicopter money, that is to say the direct central bank financing of public sector deficits) in the next recession. And as that will coincide with public sector deficits in the mid teens, we will be conducting a live MMT experiment. Welcome to a brave new world!”

As validation of his (not all that controversial) view, Edwards believes that in recent weeks we have seen the Fed “take a large step away from Quantitative Easing (QE) and towards outright monetisation.”

When QE was introduced the central bankers vehemently denied that QE was monetisation as the latter sounded too scary. Their argument was QE is different from outright monetisation because they (the central banks) were absolutely going to unwind QE as soon as practical (aka Quantitative Tightening or QT – remember how they told us it was going to be so easy with minimal consequences!). And as economic agents knew QE would be reversed and did not regard it permanent, QE could not be equated to monetisation. My own view has always been that until QE is actually fully reversed, it is to all intents and purposes the equivalent of outright monetisation, and so the central banks are merely splitting hairs.

Naturally, Powell’s recent commentary which switched off the balance sheet unwind “autopilot” caught Edwards’ attention, and the recent trial balloons by the WSJ – and the Fed – hinting at the like likely abandonment of QT, just as it was getting started- removes any doubt in Edwards’ mind “that what we have seen since 2008 is in fact outright monetization” and asks rhetorically, “does anyone really think these bloated central bank balance sheets will ever be reduced before the next recession brings yet another tidal wave of QE?”

The answer: of course not, especially if it only took a 20% drop in stocks for the Fed to immediately reverse its “autopilot” course.

Which brings us to the topic of the next inevitable recession, in which Edwards expects our “all-knowing” central bankers will pull any and every policy lever they have to hand and that in my view includes the Fed pursuing deeply negative interest rates.”

Here the SocGen strategist concedes that the reason most clients reject this outcome is “the destructive impact negative interest rates would have on bank margins, which might exacerbate any credit crunch. Hence policy makers would therefore shy away from negative rates.”

Needless to say, Edwards himself disagrees, reasoning that unlike in the 2008 Global Financial Crisis he does not expect banks to be at the apex of the next recession, perhaps as a result of an ocean of liquidity thanks to the $1.5 trillion in excess reserves currently in the system.

I have long said that in the next recession the main toxic asset to avoid will be US corporate bonds – most especially Investment Grade. In the next recession, banks will inevitably lose money if commercial and residential property prices decline and corporate and consumer loans default – although we have been reassured that banks are better capitalised than before and that they have been vigorously stress-tested.

But more importantly due to the Volker Rule and other macro-prudent regulations, banks do not sit on mountains of corporate and mortgage paper as they did in 2007. It is pension funds, insurance companies and via ETFs, mom and pop – who bought the avalanche of US corporate bonds issued since the last GFC.

So the good news, according to the grumpy SocGen permabear, is that banks are unlikely to be a systemic risk as the next crisis drives a rapid unravelling of the global economy, like they were in 2008 (sarcastically, he then notes that he is “not known for seeing a cup half full!”).

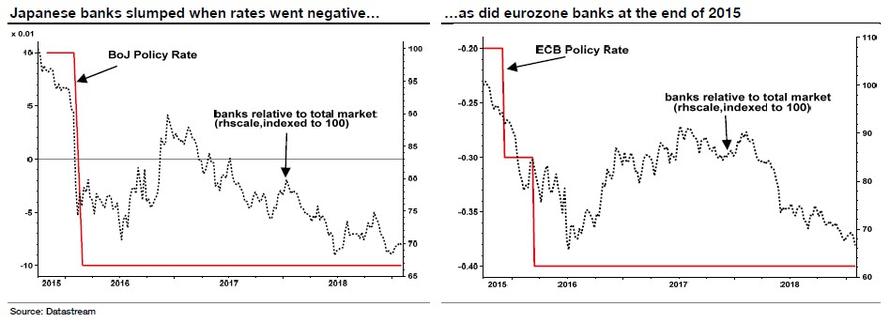

That is why he is confident that central bankers will not care if bank profits are squeezed as interest rates are pushed deep into negative territory – including the sort of adverse market reaction towards the banking sector we saw when Japan cut interest rates from +0.1% to -0.1% in early 2016 (Japanese banks fell around 25% relative to the market as did the eurozone banks as the ECB pushed interest rates to minus 0.4%, see charts below).

Addressing just this hot topic, moments ago Dallas Fed president Robert Kaplan said that he is “skeptic about whether that’s a viable option” although he quickly added that the central bank should “not take any option off the table” even as he admitted that deploying negative interest rates in the U.S. could cause problems for the financial system.

Perhaps that’s some advice the Fed could have given the ECB, SNB and BOJ before they launched NIRP, but we digress, especially since Edwards is ultimately right, and with fears about banks off the table, banks will be driven by just one prerogative (the same one that Nomura’s Charlie McElligott hinted at earlier) – doing everything to preserve inflation, and avoid deflation, to wit:

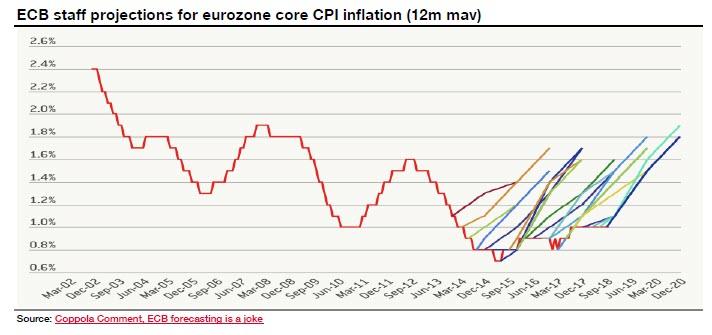

The primary central bank objective will be to avoid outright deflation. The inability of the ECB, in particular, to escape the gravitational pull of zero core inflation, despite its continual predictions of success, has been truly shocking

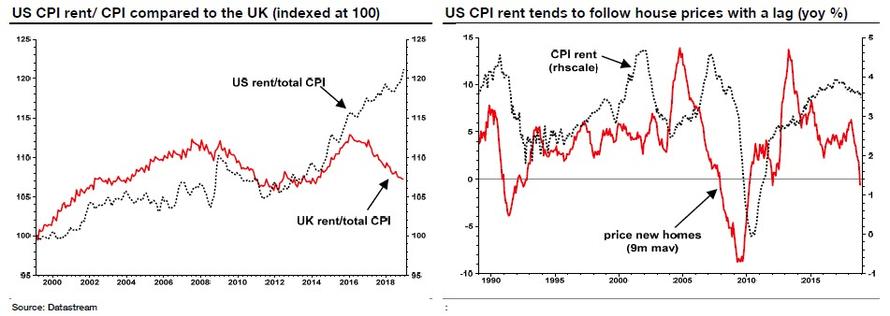

However, it is not just the eurozone that risks falling into outright deflation in the next recession: according to Edwards, the US is also vulnerable, and while core CPI and core PCE have remained relatively healthy in recent months, and roughly at the

Feds 2% target, this has been mostly a function of strong rents and Owner Equivalent Rent, i.e. housing prices, which dominate the core CPI calculation.

However, the risk is that US rent inflation “tends to broadly follow the fortunes of the housing market overall and there is no doubt that the US housing market has begun to unravel quickly over the past six months. New home prices are now actually falling yoy (even with a heavy 9-month moving average, see right-hand chart below). The last two occasions this happened were Nov 1990 and Dec 2007 when the US economy had entered recession! Rent inflation slumped shortly afterwards. In the next recession, the reality of outright deflation will dominate investors’ fears.

Meanwhile, in addition to inflation, central banks will be keeping a close eye on the dollar (recall we noted earlier that only two factors matter for the fate of the current rally: inflation and the dollar).

The reason for that, according to Edwards, is that one key policy lesson from Japan in the 1990s (and the GFC of 2008) when the economy slipped towards outright deflation is that a strong currency must be avoided at all costs as it exacerbated the deflation impulse still further.

Finance 101 dictates that a strong currency means import prices begin to decline and what we found in Japan, was that even where an industry was dominated by domestic Japanese producers, the marginal importer was able to undercut domestic producers and became the price setter for the whole sector. “Economists’ models could just not pick up this behavior and were unable to foresee the strong deflationary pull.”

So while Edwards predicts that the Fed does not want to rush to cut Fed Funds into negative territory, the cost of delaying will be very high if others are doing it (via a strong dollar).

The Fed will be forced to participate as avoiding deflation will be the number 1 priority – not the profitability of the banking sector. Investors should contemplate a brave new world of negative Fed Funds, negative US 10y and 30y bond yields, 15% budget deficits and helicopter money. Sounds ridiculous doesn’t it? What I said in 2006 sounded ridiculous too.

Concluding, as he often does, Edwards says that he hopes he is wrong, but fears that he will be proved right (again… eventually).

Wayne Jett, author of “Fruits of Graft”, interviewed by Sarah Westall in an eight part (video) series to discuss in depth the amazing history of events and actions leading up to the Great Depression. They also discuss the activities and actions taken during the Great Depression that caused increased misery for millions of Americans. This is an epic historical view of the Great Depression you have not heard before; that also serves to explain what is really driving most current events we are living through today.

Progress and Poverty by Henry George

While Wall Street looked upon today’s Durable Goods report with caution, noting the substantial beat in the headline print which was entirely as a result of a surge in non-defense aircraft orders (read Boeing) which soared by 65%, there was substantial weakness below the surface especially in the core CAPEX print, the capital goods orders non-defense ex-aircraft, which disappointed significantly, sliding 0.8% on expectations of a 0.3% rebound.

However, that was just part of the story. A far bigger part was missed by most because as always Wall Street was focused on the sequential change, and not on the absolute number.

As it turns out, the Department of Commerce decided to quietly revise all the core data going back all the way back to 2014. In doing so it stripped away about 4% from the nominal dollar amount in Durable Goods ex-transports, where the March print was slashed from $154.7 Billion to $148.3 Billion…

… and, worse, the government just confirmed what many had said for years, namely that CAPEX spending had been far lower than reported all along when it revised the capital goods orders non-defense ex-aircraft series lower by a whopping 6%, taking down the March print from $66.9 billion to only $62.4 billion, the lowest absolute number since early 2011.

So how did this downward revision to a critical historical series, and key driver of GDP, change the current GDP estimte? Well, according to the Atlanta Fed, “the GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2016 is 2.9 percent on May 26, up from 2.5 percent on May 17. The forecast for second-quarter real gross private domestic investment growth increased from -0.3 percent to 0.4 percent following this morning’s durable manufacturing release from the U.S. Census Bureau.“

Oddly not a word about the sharp revisions to the core data in main stream media.

The Inexplicable Divergence

After the closing bell last Thursday, four heavyweights in the S&P 500 index (NYSEARCA:SPY) reported results that disappointed investors. The following morning, Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL), Microsoft (NASDAQ:MSFT), Starbucks (NASDAQ:SBUX) and Visa (NYSE:V) were all down 4% or more in pre-market trading, yet the headlines read “futures flat even as some big names tumble post-earnings.” This was stunning, as I can remember in the not too distant past when a horrible day for just one of these goliaths would have sent the broad market reeling due to the implications they had for their respective sector and the market as a whole. Today, this is no longer the case, as the vast majority of stocks were higher at the opening of trade on Friday, while the S&P 500 managed to close unchanged and the Russell 2000 (NYSEARCA:IWM) rallied nearly 1%.

This is but one example of the inexplicable divergence between the performance of the stock market and the fundamentals that it is ultimately supposed to reflect – a phenomenon that has happened with such frequency that it is becoming the norm. It is as though an indiscriminate buyer with very deep pockets has been supporting the share price of every stock, other than the handful in which the selling is overwhelming due to company-specific criteria. Then again, there have been rare occasions when this buyer seems to disappear.

Why did the stock market cascade during the first six weeks of the year? I initially thought that the market was finally discounting fundamentals that had been deteriorating for months, but the swift recovery we have seen to date, absent any improvement in the fundamentals, invalidates that theory. I then surmised, along with the consensus, that the drop in the broad market was a reaction to the increase in short-term interest rates, but this event had been telegraphed repeatedly well in advance. Lastly, I concluded that the steep slide in stocks was the result of the temporary suspension of corporate stock buybacks that occur during every earnings season, but this loss of demand has had only a negligible effect during the month of April.

The bottom line is that the fundamentals don’t seem to matter, and they haven’t mattered for a very long time. Instead, I think that there is a more powerful force at work, which is dictating the short- to intermediate-term moves in the broad market, and bringing new meaning to the phrase, “don’t fight the Fed.” I was under the impression that the central bank’s influence over the stock market had waned significantly when it concluded its bond-buying programs, otherwise known as quantitative easing, or QE. Now I realize that I was wrong.

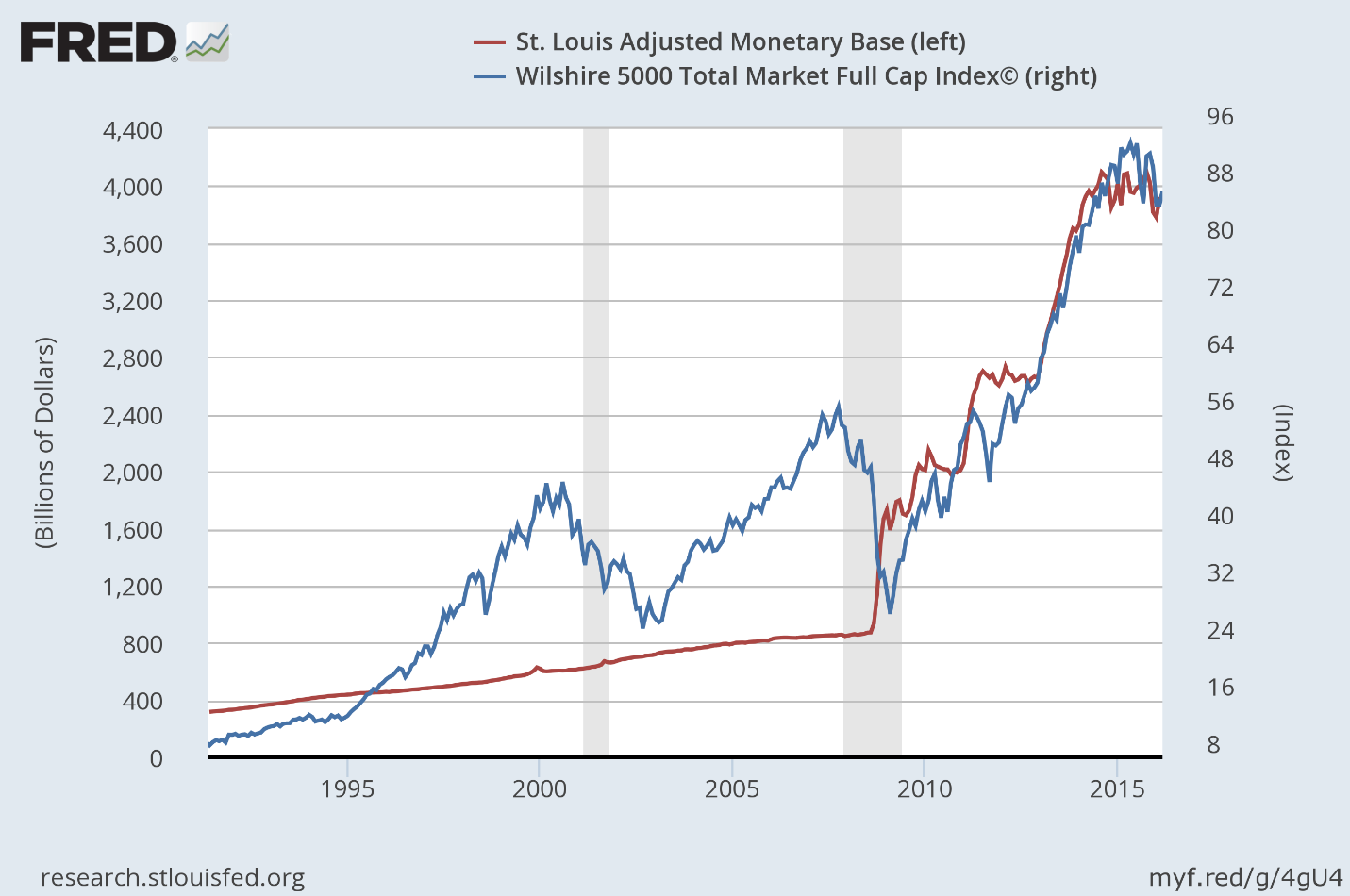

The Monetary Base

In my view, the most influential force in our financial markets continues to be the ebb and flow of the monetary base, which is controlled by the Federal Reserve. In layman’s terms, the monetary base includes the total amount of currency in public circulation in addition to the currency held by banks, like Goldman Sachs (NYSE:GS) and JPMorgan (NYSE:JPM), as reserves.

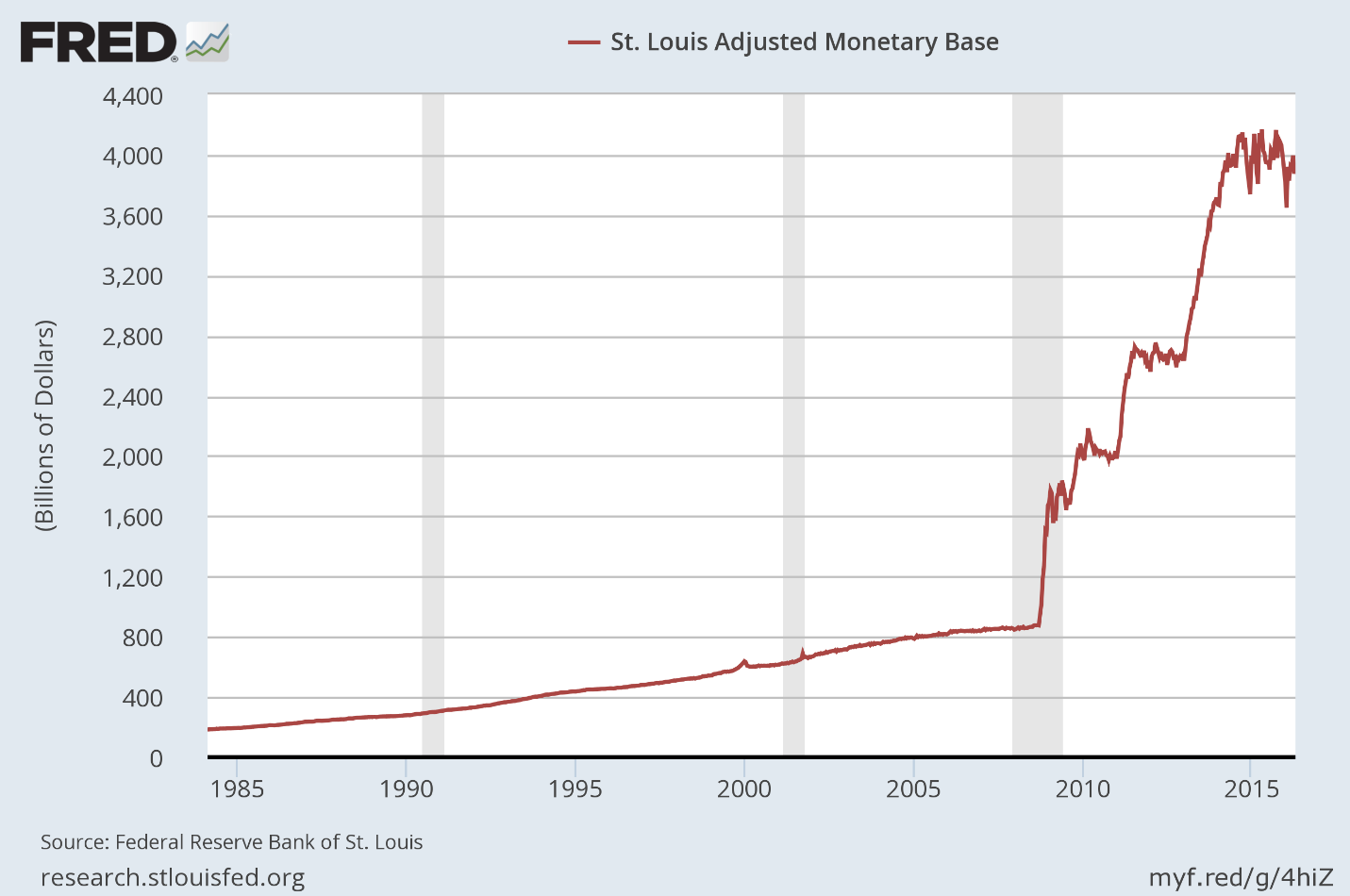

Bank reserves are deposits that are not being lent out to a bank’s customers. Instead, they are either held with the central bank to meet minimum reserve requirements or held as excess reserves over and above these requirements. Excess reserves in the banking system have increased from what was a mere $1.9 billion in August 2008 to approximately $2.4 trillion today. This accounts for the majority of the unprecedented increase in the monetary base, which now totals a staggering $3.9 trillion, over the past seven years.

The Federal Reserve can increase or decrease the size of the monetary base by buying or selling government bonds through a select list of the largest banks that serve as primary dealers. When the Fed was conducting its QE programs, which ended in October 2014, it was purchasing US Treasuries and mortgage-backed securities, and then crediting the accounts of the primary dealers with the equivalent value in currency, which would show up as excess reserves in the banking system.

A Correlation Emerges

Prior to the financial crisis, the monetary base grew at a very steady rate consistent with the rate of growth in the US economy, as one might expect. There was no change in the growth rate during the booms and busts in the stock market that occurred in 2000 and 2008, as can be seen below. It wasn’t until the Federal Reserve’s unprecedented monetary policy intervention that began during the financial crisis that the monetary base soared, but something else also happened. A very close correlation emerged between the rising value of the overall stock market and the growth in the monetary base.

It is well understood that the Fed’s QE programs fueled demand for higher risk assets, including common stocks. The consensus view has been that the Fed spurred investor demand for stocks by lowering the interest rate on the more conservative investments it was buying, making them less attractive, which encouraged investors to take more risk.

Still, this does not explain the very strong correlation between the rising value of the stock market and the increase in the monetary base. This is where conspiracy theories arise, and the relevance of this data is lost. It would be a lot easier to measure the significance of this correlation if I had proof that the investment banks that serve as primary dealers had been piling excess reserves into the stock market month after month over the past seven years. I cannot. What is important for investors to recognize is that an undeniable correlation exists, and it strengthens as we shorten the timeline to approach present day.

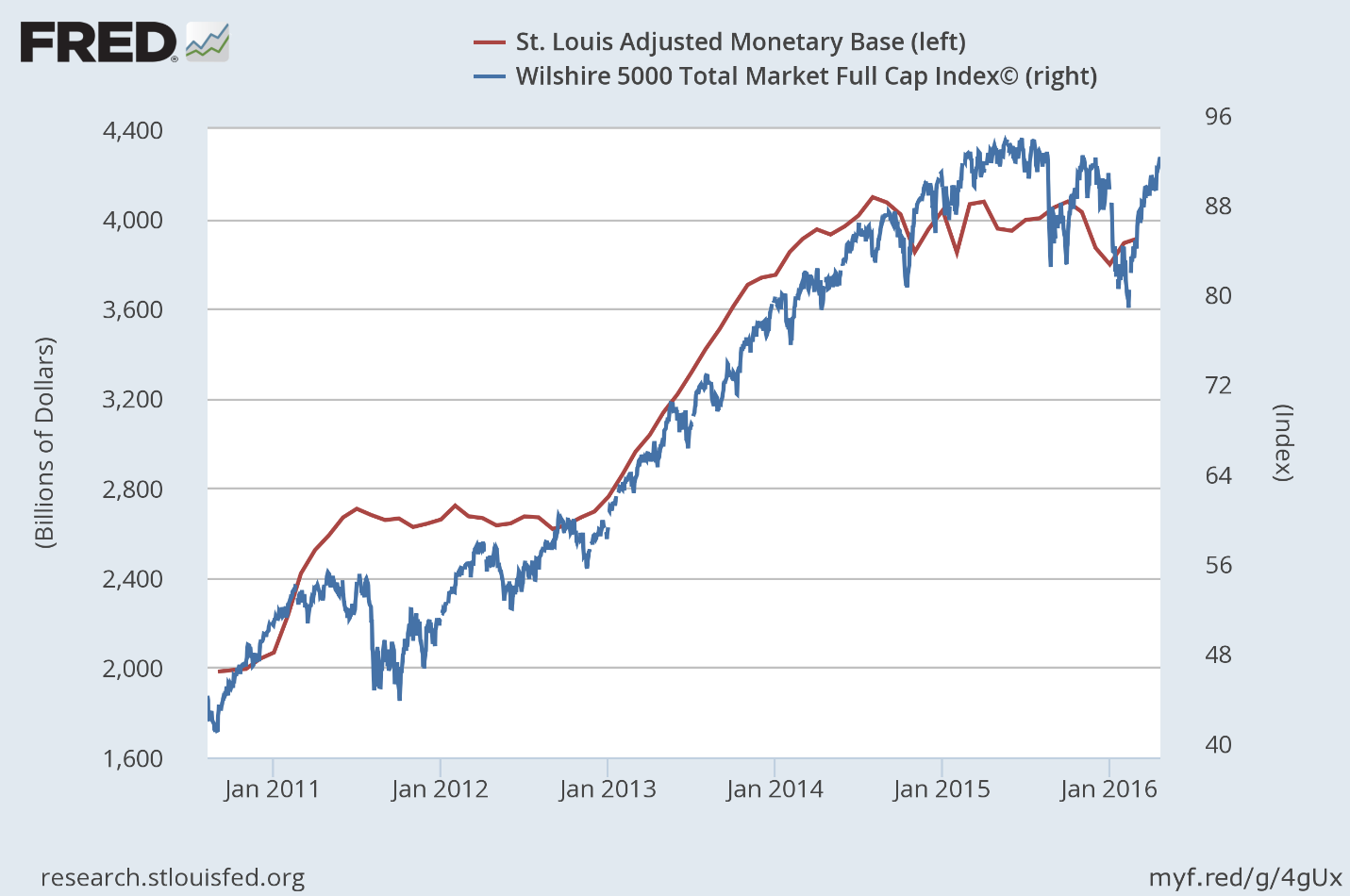

The Correlation Cuts Both Ways

Notice that the monetary base (red line) peaked in October 2014, when the Fed stopped buying bonds. From that point moving forward, the monetary base has oscillated up and down in what is a very modest downtrend, similar to that of the overall stock market, which peaked a few months later.

What I have come to realize is that these ebbs and flows continue to have a measurable impact on the value of the overall stock market, but in both directions! This is important for investors to understand if the Fed continues to tighten monetary policy later this year, which would require reducing the monetary base.

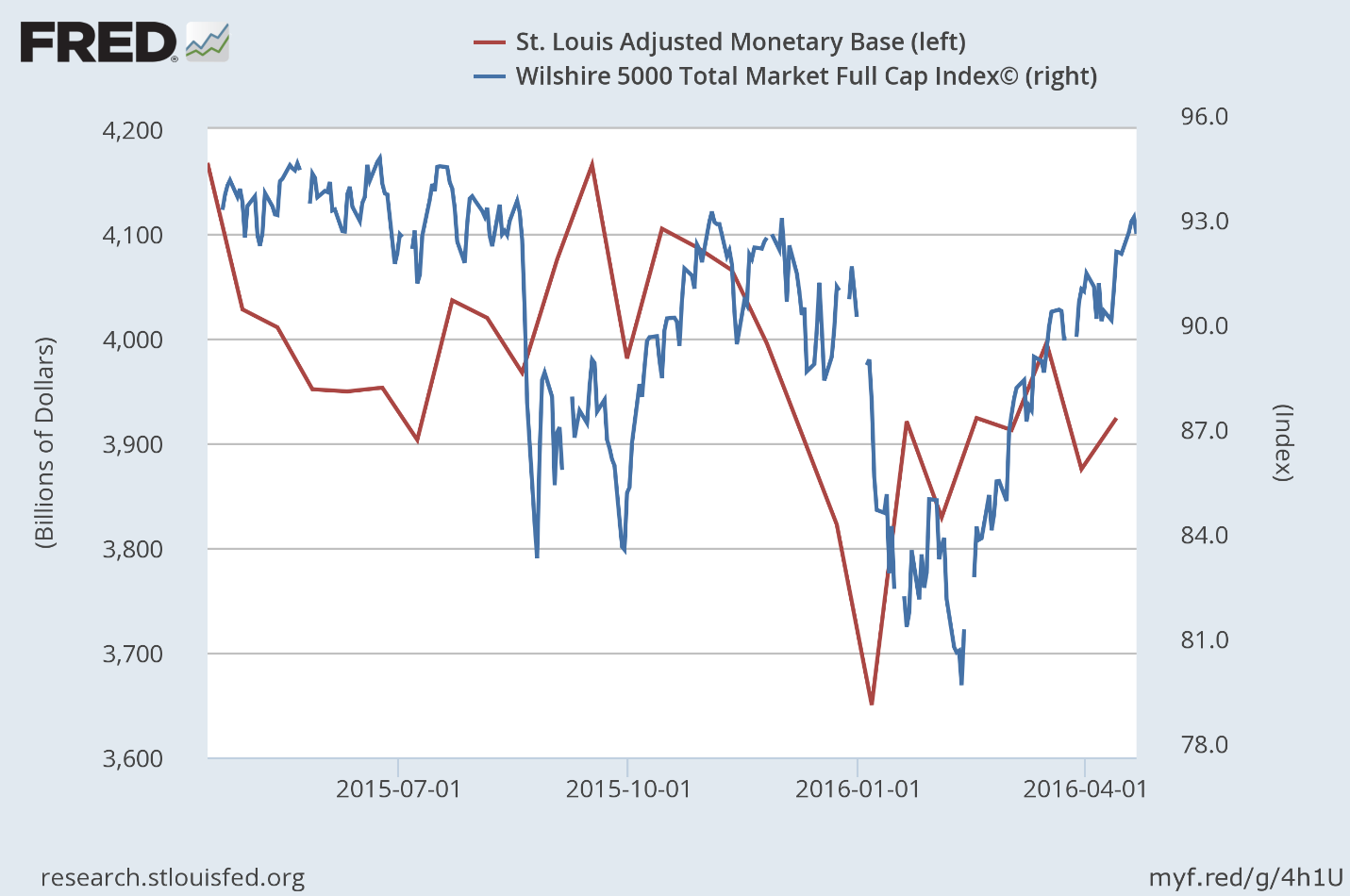

If we look at the fluctuations in the monetary base over just the past year, in relation to the performance of the stock market, a pattern emerges, as can be seen below. A decline in the monetary base leads a decline in the stock market, and an increase in the monetary base leads a rally in the stock market. The monetary base is serving as a leading indicator of sorts. The one exception, given the severity of the decline in the stock market, would be last August. At that time, investors were anticipating the first rate increase by the Federal Reserve, which didn’t happen, and the stock market recovered along with the rise in the monetary base.

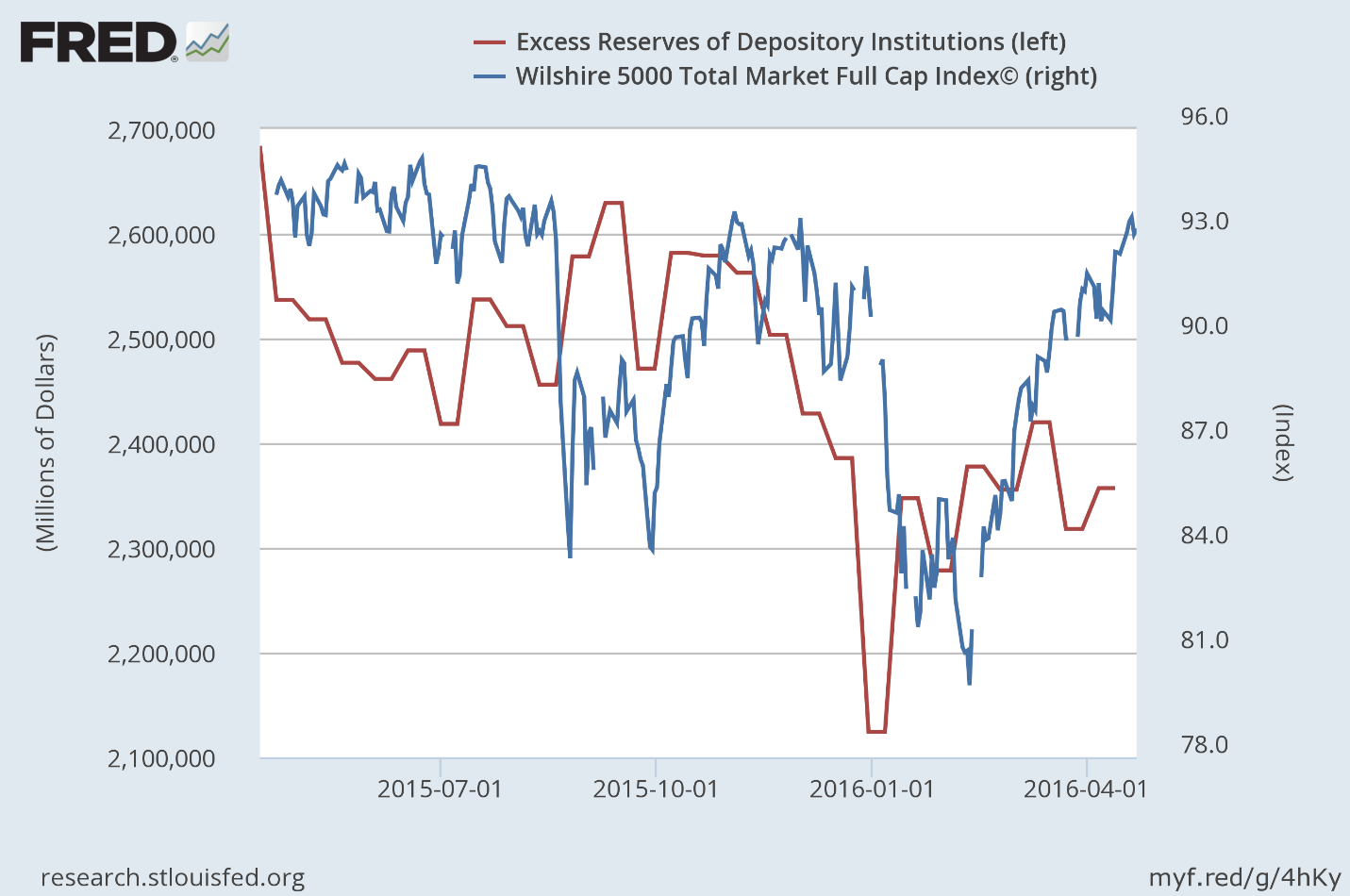

If we replace the fluctuations in the monetary base with the fluctuations in excess bank reserves, the same correlation exists with stock prices, as can be seen below. The image that comes to mind is that of a bathtub filled with water, or liquidity, in the form of excess bank reserves. This liquidity is supporting the stock market. When the Fed pulls the drain plug, withdrawing liquidity, the water level falls and so does the stock market. The Fed then plugs the drain, turns on the faucet and allows the tub to fill back up with water, injecting liquidity back into the banking system, and the stock market recovers. Could this be the indiscriminate buyer that I mentioned previously at work in the market? I don’t know.

What I can’t do is draw a road map that shows exactly how an increase or decrease in excess reserves leads to the buying or selling of stocks, especially over the last 12 months. The deadline for banks to comply with the Volcker Rule, which bans proprietary trading, was only nine months ago. Who knows what the largest domestic banks that hold the vast majority of the $2.4 trillion in excess reserves were doing on the investment front in the years prior. As recently as January 2015, traders at JPMorgan made a whopping $300 million in one day trading Swiss francs on what was speculated to be a $1 billion bet. Was that a risky trade?

Despite the ban on proprietary trading imposed by the Volcker Rule, there are countless loopholes that weaken the statute. For example, banks can continue to trade physical commodities, just not commodity derivatives. Excluded from the ban are repos, reverse repos and securities lending, through which a lot of speculation takes place. There is also an exclusion for what is called “liquidity management,” which allows a bank to put all of its relatively safe holdings in an account and manage them with no restrictions on trading, so long as there is a written plan. The bank can hold anything it wants in the account so long as it is a liquid security.

My favorite loophole is the one that allows a bank to facilitate client transactions. This means that if a bank has clients that its traders think might want to own certain stocks or stock-related securities, it can trade in those securities, regardless of whether or not the clients buy them. Banks can also engage in high-frequency trading through dark pools, which mask their trading activity altogether.

As a friend of mine who is a trader for one of the largest US banks told me last week, he can buy whatever he wants within his area of expertise, with the intent to make a market and a profit, so long as he sells the security within six months. If he doesn’t sell it within six months, he is hit with a Volcker Rule violation. I asked him what the consequences of that would be, to which he replied, “a slap on the wrist.”

Regardless of the investment activities of the largest banks, it is clear that a change in the total amount of excess reserves in the banking system has a significant impact on the value of the overall stock market. The only conclusion that I can definitively come to is that as excess reserves increase, liquidity is created, leading to an increase in demand for financial assets, including stocks, and prices rise. When that liquidity is withdrawn, prices fall. The demand for higher risk financial assets that this liquidity is creating is overriding any supply, or selling, that results from a deterioration in market fundamentals.

There is one aspect of excess reserves that is important to understand. If a bank uses excess reserves to buy a security, that transaction does not reduce the total amount of reserves in the banking system. It simply transfers the reserves from the buyer to the seller, or to the bank account in which the seller deposits the proceeds from the sale, if that seller is not another bank. It does change the composition of the reserves, as 10% of the new deposit becomes required reserves and the remaining 90% remains as excess reserves. The Fed is the only institution that can change the total amount of excess reserves in the banking system, and as it has begun to do so over the past year, I think it is finally realizing that it must reap what it has sown.

The Conundrum

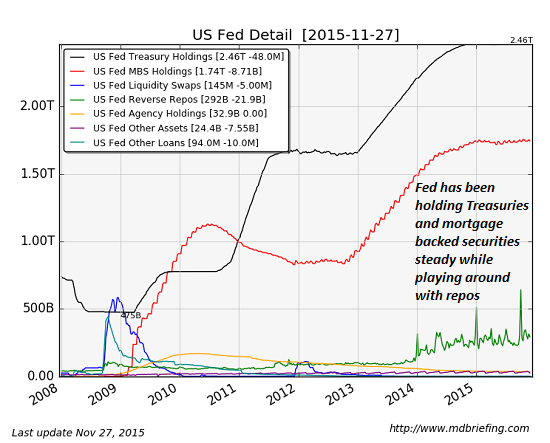

In order to tighten monetary policy, the Federal Reserve must drain the banking system of the excess reserves it has created, but it doesn’t want to sell any of the bonds that it has purchased. It continues to reinvest the proceeds of maturing securities. As can be seen below, it holds approximately $4.5 trillion in assets, a number which has remained constant over the past 18 months.

Therefore, in order to drain reserves, thereby reducing the size of the monetary base, the Fed has been lending out its bonds on a temporary basis in exchange for the reserves that the bond purchases created. These transactions are called reverse repurchase agreements. This is how the Fed has been reducing the monetary base, while still holding all of its assets, as can be seen below.

There has been a gradual increase in the volume of repurchase agreements outstanding over the past two years, which has resulted in a gradual decline in the monetary base and excess reserves, as can be seen below.

I am certain that the Fed recognizes the correlation between the rise and fall in excess reserves, and the rise and fall in the stock market. This is why it has been so reluctant to tighten monetary policy further. In lieu of being transparent, it continues to come up with excuses for why it must hold off on further tightening, which have very little to do with the domestic economy. The Fed rightfully fears that a significant market decline will thwart the progress it has made so far in meeting its mandate of full employment and a rate of inflation that approaches 2% (stable prices).

The conundrum the Fed faces is that if the rate of inflation rises above its target of 2%, forcing it to further drain excess bank reserves and increase short-term interest rates, it is likely to significantly deflate the value of financial assets, based on the correlation that I have shown. This will have dire consequences both for consumer spending and sentiment, and for what is already a stall-speed rate of economic growth. Slower rates of economic growth feed into a further deterioration in market fundamentals, which leads to even lower stock prices, and a negative-feedback loop develops. This reminds me of the deflationary spiral that took place during the financial crisis.

The Fed’s preferred measurement of inflation is the core Personal Consumption Expenditures, or PCE, price index, which excludes food and energy. The latest year-over-year increase of 1.7% is the highest since February 2013, and it is rapidly closing in on the Fed’s 2% target even though the rate of economic growth is moving in the opposite direction, as can be seen below.

The Bubble

If you have been wondering, as I have, why the stock market has been able to thumb its nose at an ongoing recession in corporate profits and revenues that started more than a year ago, I think you will find the answer in $2.4 trillion of excess reserves in the banking system. It is this abundance of liquidity, for which the real economy has no use, that is decoupling the stock market from economic fundamentals. The Fed has distorted the natural pricing mechanism of a free market, and at some point in the future, we will all learn that this distortion has a great cost.

Alan Greenspan once said, “how do we know when irrational exuberance has unduly escalated asset values?” Open your eyes.

What you see in the chart below is a bubble. It is much different than the asset bubbles we experienced in technology stocks and home prices, which is why it has gone largely unnoticed. It is similar from the standpoint that it has been built on exaggerated expectations of future growth. It is a bubble of the Fed’s own making, built on the expectation that an unprecedented increase in the monetary base and excess bank reserves would lead to faster rates of economic growth. It has clearly not. Instead, this mountain of money has either directly, or indirectly, flooded into financial assets, manipulating prices to levels well above what economic fundamentals would otherwise dictate.

The great irony of this bubble is that it is the achievement of the Fed’s objectives, for which the bubble was created, that will ultimately lead it to its bursting. It was an unprecedented amount of credit available at historically low interest rates that fueled the rise in home prices, and it has also been an unprecedented amount of credit at historically low interest rates that has fueled the rise in financial asset prices, including the stock market. How and when this bubble will be pricked remains a question mark, but what is certain is that the current level of excess reserves in the banking system that appear to be supporting financial markets cannot exist in perpetuity.

It seems the end really is nigh for the U.S. dollar.

It seems the end really is nigh for the U.S. dollar.

And the mudfight for global dominance and currency war couldn’t be more ugly or dramatic.

The Saudis are now openly threatening to take down the U.S. economy in the ongoing fallout over collapsing oil prices and tense geopolitical events involving the 9/11 cover-up. The New York Times reports:

Saudi Arabia has told the Obama administration and members of Congress that it will sell off hundreds of billions of dollars’ worth of American assets held by the kingdom if Congress passes a bill that would allow the Saudi government to be held responsible in American courts for any role in the Sept. 11, 2001, attacks.

China has been working for years to establish global currency status, and will strengthen the yuan by backing it with gold in moves clearly designed to cripple the role of the dollar. Zero Hedge reports:

China’s shift to an official local-currency-based gold fixing is “the culmination of a two-year plan to move away from a US-centric monetary system,” according to Bocom strategist Hao Hong. In an insightfully honest Bloomberg TV interview, Hong admits that “by trading physical gold in renminbi, China is slowly chipping away at the dominance of US dollars.”

Putin also waits in the shadows, making similar moves and creating alliances to out-balance the United States with a growing Asian economy on the global stage.

Luke Rudkowski of WeAreChange asks “Is This The End of the U.S. Dollar?” in the video below.

He writes:

In this video Luke Rudkowski reports on the breaking news of both China and Saudi Arabia making geopolitical moves that could cause a U.S economic collapse and obliteration of the U.S hegemony petrodollar. We go over China’s new gold backed yuan that cannot be traded in U.S dollars and rising tension with Saudi Arabia threatening economic blackmail if their role in 911 is exposed.

Visit WeAreChange.org where this video report was first published.

The Federal Reserve, Henry Kissinger, the Rockefellers and their allies created the petrodollar and insisted upon the world using the U.S. dollar to buy oil, placing debt in American currency and entire countries under the yoke of the West.

But that paradigm has been crumbling as world order shifts away from U.S. hegemony.

It is a matter of when – not if – these events will change the U.S. financial landscape forever.

As SHTF has warned, major events are taking place, and no one can say if stability will be here tomorrow.

Stay vigilant, and prepare yourself and your family as best as you can.

Read more:

Pay Attention To The Economy Right Now, Because A Disturbing Series Of Events Seems To Be In Motion

Here’s How We Got Here: A Short Primer On The History Of The Petrodollar

Shock Report: China Dumps Half a Trillion Dollars: “Something Is Very, Very Wrong”

Dollar Moves Shake the World: “Federal Reserve Could Start a Currency War”

• No empire has ever prospered or endured by weakening its currency.

• Those who argue the Fed can’t possibly raise rates in a weakening domestic economy have forgotten the one absolutely critical mission of the Fed in the Imperial Project is maintaining U.S. dollar hegemony.

• In essence, the Fed must raise rates to strengthen the U.S. dollar ((USD)) and keep commodities such as oil cheap for American consumers.

• Another critical element of U.S. hegemony is to be the dumping ground for exports of our trading partners.

• If stocks are the tail of the bond dog, the foreign exchange market is the dog’s owner.

• No empire has ever prospered or endured by weakening its currency.

Now that the Fed isn’t feeding the baby QE, it’s throwing a tantrum. A great many insightful commentators have made the case for why the Fed shouldn’t raise rates this month – or indeed, any other month. The basic idea is that the Fed blew it by waiting until the economy is weakening to raise rates. More specifically, former Fed Chair Ben Bernanke – self-hailed as a “hero that saved the global economy” – blew it by keeping rates at zero and overfeeding the stock market bubble baby with quantitative easing (QE).

On the other side of the ledger, is the argument that the Fed must raise rates to maintain its rapidly thinning credibility. I have made both of these arguments: that the Bernanke Fed blew it big time, and that the Fed has to raise rates lest its credibility as the caretaker not just of the stock market but of the real economy implodes.

But there is another even more persuasive reason why the Fed must raise rates. It may appear to fall into the devil’s advocate camp at first, but if we consider the Fed’s action through the lens of Triffin’s Paradox, which I have covered numerous times, then it makes sense.

The Federal Reserve, Interest Rates and Triffin’s Paradox

Understanding the “Exorbitant Privilege” of the U.S. Dollar (November 19, 2012)

The core of Triffin’s Paradox is that the issuer of a reserve currency must serve two quite different sets of users: the domestic economy, and the international economy.

Those who argue the Fed can’t possibly raise rates in a weakening domestic economy have forgotten the one absolutely critical mission of the Fed in the Imperial Project is maintaining U.S. dollar hegemony.

No nation ever achieved global hegemony by weakening its currency. Hegemony requires a strong currency, for the ultimate arbitrage is trading fiat currency that has been created out of thin air for real commodities and goods.

Generating currency out of thin air and trading it for tangible goods is the definition of hegemony. Is there any greater magic power than that?

In essence, the Fed must raise rates to strengthen the U.S. dollar (USD) and keep commodities such as oil cheap for American consumers. The most direct way to keep commodities cheap is to strengthen one’s currency, which makes commodities extracted in other nations cheaper by raising the purchasing power of the domestic economy on the global stage.

Another critical element of U.S. hegemony is to be the dumping ground for exports of our trading partners. By strengthening the dollar, the Fed increases the purchasing power of everyone who holds USD. This lowers the cost of goods imported from nations with weakening currencies, who are more than willing to trade their commodities and goods for fiat USD.

The Fed may not actually be able to raise rates in the domestic economy, as explained here: “But It’s Just A 0.25% Rate Hike, What’s The Big Deal?” – Here Is The Stunning Answer.

But in this case, perception and signaling are more important than the actual rates: By signaling a sea change in U.S. rates, the Fed will make the USD even more attractive as a reserve currency and U.S.-denominated assets more attractive to those holding weakening currencies.

If stocks are the tail of the bond dog, the foreign exchange market is the dog’s owner. Despite its recent thumping (due to being the most over loved, crowded trade out there), the USD is trading in a range defined by multi-year highs.

The Fed’s balance sheet reveals its basic strategy going forward: maintain its holdings of Treasury bonds and mortgage-backed securities (MBS) while playing around in the repo market in an attempt to manipulate rates higher.

Whether or not the Fed actually manages to raise rates in the real world is less important than maintaining USD hegemony. No empire has ever prospered or endured by weakening its currency.

Romania draws foreign buyers looking for historic mansions and modern villas in resort areas

Romania draws foreign buyers looking for historic mansions and modern villas in resort areasCount Dracula, the central character of Irish author Bram Stoker’s classic vampire novel, eagerly left for England in search of new blood, in a story that popularized the Romanian region of Transylvania. Today, house hunters are invited to make the reverse journey now that Romania is a member of the European Union and that restrictions were lifted this year on purchases of local real estate by the bloc’s nationals.

Britain’s Prince Charles, for one, unwinds every year in Zalanpatak. The mud road leading to the remote village stretches for miles, with the clanging of cow bells accompanying tourists making the trek.

Elsewhere in the world, the heir to the British throne occupies great castles and sprawling mansions. In rural Romania, he resides in a small old cottage. His involvement, since 2006, in the restoration of a few local farmhouses has given the hamlet global popularity and added a sense of excitement about Transylvania living.

A living room in Bran Castle, a Transylvania property marketed as Count Dracula’s castle. The home is for sale, initially listed for $78 million.

A living room in Bran Castle, a Transylvania property marketed as Count Dracula’s castle. The home is for sale, initially listed for $78 million. Transylvania, with a population of more than seven million in the central part of Romania, has a number of high-end homes on the market. And, yes, one is a castle. Bran Castle in Brasov county is marketed as the home of Count Dracula. In reality it was a residence of Romanian Queen Marie in the early 20th century. In 2007, the home was available for $78 million. The sellers are no longer listing a price, said Mark A. Meyer, of Herzfeld and Rubin, the New York attorneys representing the queen’s descendants, but will entertain offers.

Foreign buyers had been focused on Bucharest, where there was speculative buying of apartments after the country joined the EU in 2007. But Transylvania has been luring house hunters away from the capital city.

A guesthouse on the property in Zalanpatak, Transylvania, that is owned by Britain’s Prince Charles. His presence has boosted interest in Romanian real estate.

A guesthouse on the property in Zalanpatak, Transylvania, that is owned by Britain’s Prince Charles. His presence has boosted interest in Romanian real estate. Transylvania means “the land beyond the forest” and the region is famous for its scenic mountain routes. Brasov, an elegant mountain resort and the closest Transylvanian city to the capital, has many big villas built in the 19th century by wealthy merchants. A 10-room townhouse from that period in the historic city center is listed for $2.7 million. For $500,000, a 2,200-square-foot apartment offers rooftop views of the city and the surrounding mountains.

A seven-bedroom mansion in the nearby village of Halchiu, close to popular skiing resorts, is on the market for $2.4 million. The modern villa features two huge living rooms, a swimming pool, a tennis court and spectacular views of the Carpathian Mountains.

The village, founded by Saxons in the 12th century, has rows of historic houses across the street. Four such buildings were demolished to make way for the mansion, completed in 2010.

A $2.4 million mansion is for sale in Halchiu village.

A $2.4 million mansion is for sale in Halchiu village. “Rather than invest a million or more to buy an existing house, the wealthy prefer to build on their own because construction materials and work is cheaper,” said Raluca Plavita, senior consultant at real-estate firm DTZ Echinox in Bucharest.

Non-EU nationals can’t purchase land outright—although they may use locally registered companies to circumvent the restriction—but they can buy buildings freely, said Razvan Popa, real-estate partner at law firm Kinstellar. High-end properties are out of reach for many Romanians, who make an average of $500 in monthly take-home pay.

The country saw a rapid inflation of real-estate prices before 2008, on prospects of Romania’s entry to the EU and the North Atlantic Treaty Organization, as well as aggressive lending by banks. Values then fell by half during the global financial crisis.

The economy is stronger now, with the International Monetary Fund estimating 2.4% growth this year. But the country is still among Europe’s poorest. Its isolation during the dictatorship of Nicolae Ceausescu gave it a bad image.

The interior of the seven-bedroom Halchiu mansion, which was built on the site of four traditional Saxon homes.

The interior of the seven-bedroom Halchiu mansion, which was built on the site of four traditional Saxon homes.“Interest in Romania isn’t comparable with Prague or Budapest where some may be looking to buy a small apartment with a view of Charles Bridge or the Danube,” said Mr. Popa, the real-estate lawyer.

The international publicity around Prince Charles’s properties offers a counterbalance to some of the negative press Romania has received in Western Europe, which is worried about well-educated Romanians moving to other countries to provide inexpensive labor.

The Zalanpatak property is looked after by Tibor Kalnoky, a descendant of a Hungarian aristocratic family. The 47-year-old studied in Germany to be a veterinarian and, after reclaiming family assets in Romania, has managed the prince’s property and has hosted him during his visits.

These occasional visits are enough to attract scores of tourists throughout the year to the formerly obscure village in a Transylvanian valley. The fact that few street signs lead there, that the property offers no Internet or TV and that cellphone signals are absent for miles, seems only to add to the mystery of the place.