Tag Archives: US Dollar

Saudis Sign Historic Military Cooperation Agreement With Russia

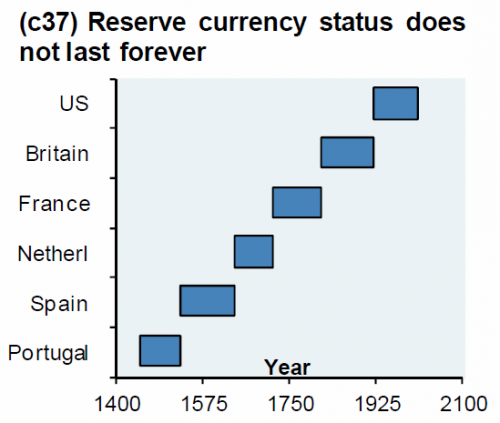

JPMorgan: We Believe The Dollar Could Lose Its Status As World’s Reserve Currency

(ZeroHedge) Almost eight year ago, we first presented a chart first created by JPMorgan’s Michael Cembalest, which showed very simply and vividly that reserve currencies don’t last forever, and that in the not too distant future, the US Dollar would also lose its status as the world’s most important currency, since it is never different this time.

As Cembalest put it back in January 2012, “I am reminded of the following remark from late MIT economist Rudiger Dornbusch: ‘Crisis takes a much longer time coming than you think, and then it happens much faster than you would have thought.'”

Perhaps it is not a coincidence then that in light of the growing number of mentions of MMT and various other terminal, destructive monetary policies that have been proposed to kick on the current financial system the can just a little bit longer, that the topic of longevity of reserve currency status is once again becoming all the rage, and none other than JPMorgan’s Private Bank ask in this month’s investment strategy note whether “the dollar’s “exorbitant privilege” is coming to an end?”

So why is JPM, after first creating the iconic chart above which has since spread virally across all financial corners of the internet, not only worried that the dollar’s reserve status may be coming to an end, but in fact goes so far as to state that “we believe the dollar could lose its status as the world’s dominant currency (which could see it depreciate over the medium term) due to structural reasons as well as cyclical impediments.”

Read on to learn why even the largest US bank has started to lose faith in the world’s most powerful currency.

Is the dollar’s “exorbitant privilege” coming to an end?

In Brief

The U.S. dollar (USD) has been the world’s dominant reserve currency for almost a century. As such, many investors today, even outside the United States, have built and become comfortable with sizable USD over weights in their portfolios. However, we believe the dollar could lose its status as the world’s dominant currency (which could see it depreciate over the medium term) due to structural reasons as well as cyclical impediments.

As such, diversifying dollar exposure by placing a higher weighting on other currencies in developed markets and in Asia, as well as precious metals makes sense today. This diversification can be achieved with a strategy that maintains the underlying assets in an investment portfolio, but changes the mix of currencies within that portfolio. This is a completely bespoke approach that can be customized to meet the unique needs of individual clients.

The Rise Of The U.S. Dollar

It is commonly perceived that the U.S. dollar overtook the Great British Pound (GBP) as the world’s international reserve currency with the signing of the Bretton Woods Agreements after World War II. The reality is that sterling’s value was eroded for many decades prior to Bretton Woods. The dollar’s rise to international prominence was fueled by the establishment of the Federal Reserve System a little over a century ago and U.S. economic emergence after World War I. The Federal Reserve System aided in the establishment of more mature capital markets and a nationally coordinated monetary policy, two important pillars of reserve-currency countries. Being the world’s unit of account has given the United States what former French Finance Minister Valery d’Estaing called an “exorbitant privilege” by being able to purchase imports and issue debt in its own currency and run persistent deficits seemingly without consequence.

The Shifting Center

There is nothing to suggest that the dollar dominance should remain in perpetuity. In fact, the dominant international currency has changed many times throughout history going back thousands of years as the world’s economic center has shifted.

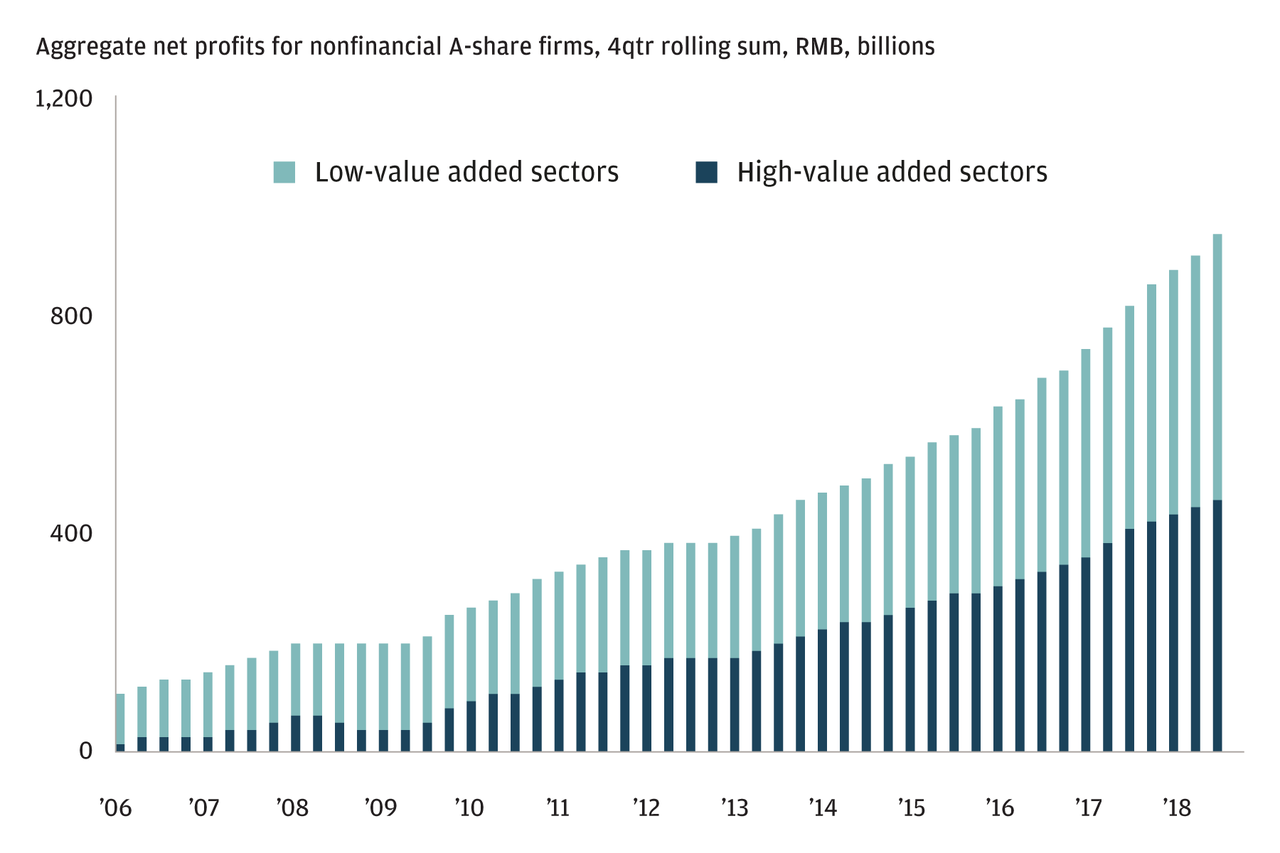

After the end of World War II, the U.S. accounted for biggest share of world GDP at more than 25%. This number is brought to more than 40% when we include Western European powers. Since then, the main driver of economic growth has shifted eastwards towards Asia at the expense of the U.S. and the West. China is at the epicenter of this recent economic shift driven by the country’s strong growth and commitment to domestic reforms. Over the last 70 years, China has quadrupled its share of global GDP to around 20%—roughly the same share as the U.S.—and this share is expected to continue to grow in the years ahead. China is no longer just a manufacturer of low cost goods as a growing share of corporate earnings is coming from “high value add” sectors like technology.

China Regaining Its Status As A Global Superpower

Earnings In China Are Becoming More Balanced

In addition to China, the economies of Southeast Asia, including India, have strong secular tailwinds driven by younger demographics and proliferating technological know-how. Specifically, the Asian economic zone—from the Arabian Peninsula and Turkey in the West to Japan and New Zealand in the East and from Russia in the North and Australia in the South—now represents 50% of global GDP and two-thirds of global economic growth. Of the estimated $30 trillion in middle-class consumption growth between 2015 and 2030, only $1 trillion is expected to come from today’s Western economies. As this region grows, the share of non-USD transactions will inevitably increase which will likely erode the dollar’s “reserveness”, even if the dollar isn’t replaced as the dominant international currency.

In other words, in the coming decades we think the world economy will transition from U.S. and USD dominance toward a system where Asia wields greater power. In currency space, this means the USD will likely lose value compared to a basket of other currencies, including precious commodities like gold.

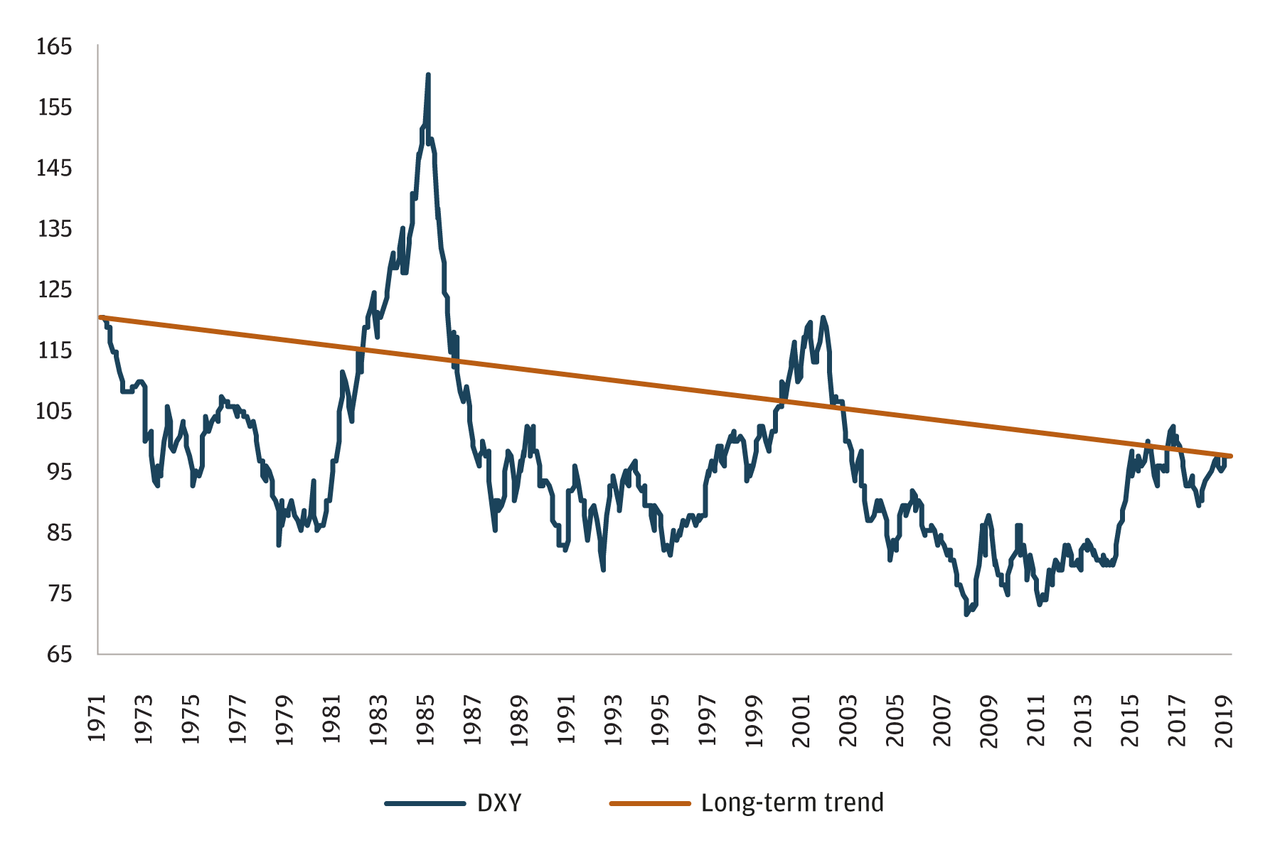

Dollar’s Declining Role Already Under Way?

Recent data on currency reserve holdings among global central banks suggests this shift may already be under way. As a share of overall central bank reserves, the USD’s role has been declining ever since the Great Recession (see chart). The most recent central bank reserve flow data also suggests that for the first time since the euro’s introduction in 1999, central banks simultaneously sold dollars and bought euros.

Central banks across the globe are also adding to gold reserves at their strongest pace on record. 2018 saw the strongest demand for gold from central banks since 1971 and a rolling four-quarter sum of gold purchases is the strongest on record. To us, this makes sense: gold is a stable source of value with thousands of years of trust among humans supporting it.

USD Share Of Central Bank Reserves, %

Trade Wars Have Long-Term Consequences

The current U.S. administration has called into question agreements with nearly all of its largest partners—tariffs on China, Mexico and the European Union, renegotiating NAFTA, as well as abandoning the Trans Pacific Partnership. A more adversarial U.S. administration could also encourage countries to reduce their reliance on USD in trade. Currently 85% of all currency transactions involve the USD despite the U.S. accounting for only roughly 25% of global GDP.

Countries around the world are already developing payment mechanisms that would avoid using the dollar. These systems are small and still developing but this is likely to be a structural story that will extend beyond one particular administration. In a recent speech on the international role of the euro, Bank for International Settlements Chief Economist Claudio Borio brought up the benefits of pricing oil in the euro saying, “Trading and settling oil in the euro would move payments from dollars to euros and thereby shift ultimate settlement to the euro’s TARGET2 system. This could limit the reach of U.S. foreign policy insofar as it leverages dollar payments.” The European Central Bank also alluded to this theme in a recent report saying that “growing concerns about the impact of international trade tensions and challenges to multilateralism, including the imposition of unilateral sanctions seem to have lent support to the euro’s global standing.”

We believe we are at an important juncture. On a real basis, the dollar stands currently more than 10% above its long-term average and on a nominal basis has actually been trending lower for 50 years (see chart below).

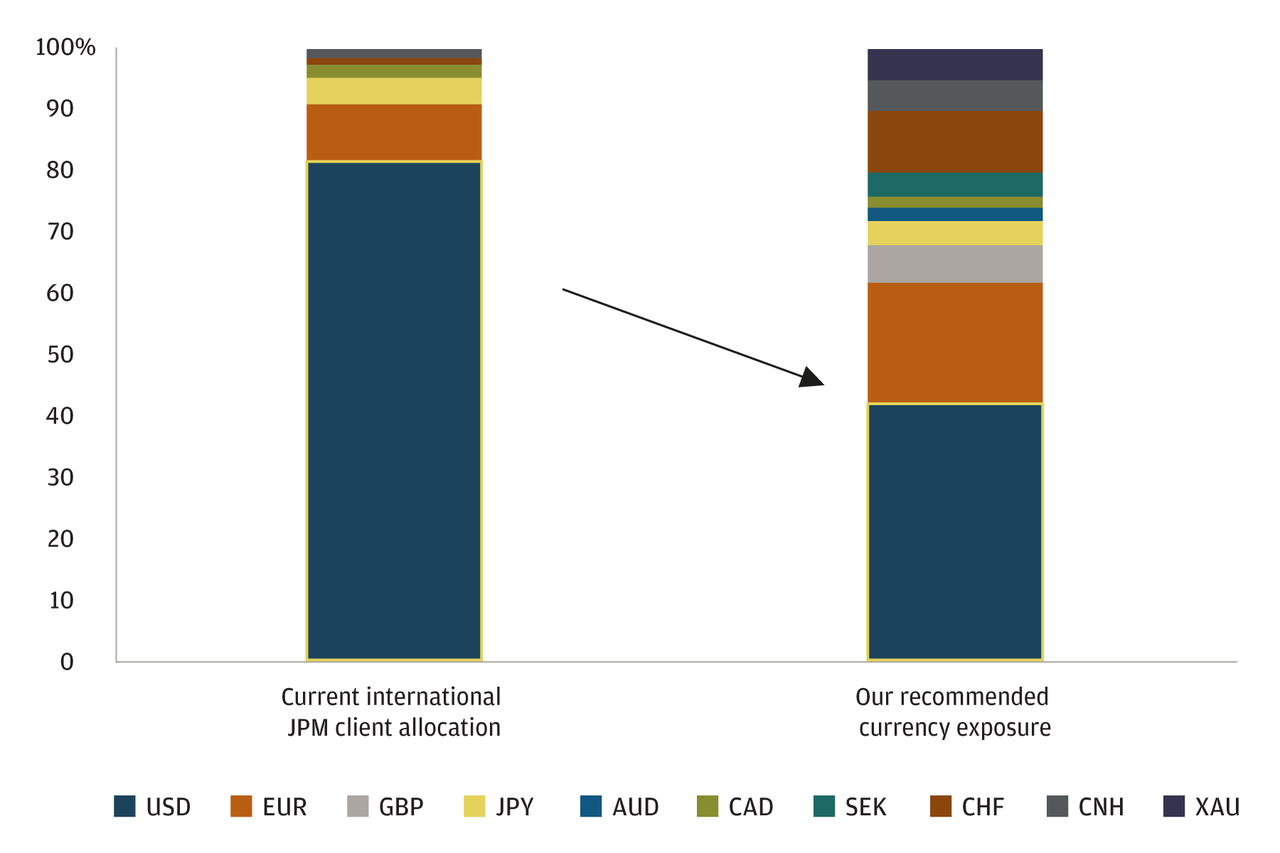

Given the persistent—and rising—deficits in the United States (in both fiscal and trade), we believe the U.S. dollar could become vulnerable to a loss of value relative to a more diversified basket of currencies, including gold. As we scan client portfolios, we see that many of them have far more U.S. dollar exposure than we feel is prudent. At this stage of the economic cycle, we believe this exposure should be more diversified. In many cases, our recommendation would likely be to place a higher weighting on other G10 currencies, currencies in Asia and gold (see chart).

FX Exposure

Source: JPMorgan Private Bank June 13, 2019

Did Russia Just Trigger A Global Reserve Currency Reset Process?

Russia De-Dollarizes Deeper: Shifts $100 Billion To Yuan, Yen, And Euro

Russia is continuing to ramp up its efforts to move away from the American dollar (Federal Reserve Notes). The country just shifted $100 billion of its reserves to the yuan, the yen, and the euro in their ongoing effort to ditch the US Dollar.

The Central Bank of Russia has moved further away from its reliance on the United States dollar and has axed its share in the country’s foreign reserves to a historic low, transferring about $100 billion into euro, Japanese yen, and Chinese yuan according to a report by RT. The share of the U.S. dollar in Russia’s international reserves portfolio has dramatically decreased in just three months between March and June 2018. The holding decreased from 43.7 percent to a new low of 21.9 percent, according to the Central Bank’s latest quarterly report, which is issued with a six-month lag.

The money pulled from the dollar reserves was redistributed to increase the share of the euro to 32 percent and the share of Chinese yuan to 14.7 percent. Another 14.7 percent of the portfolio was invested in other currencies, including the British pound (6.3 percent), Japanese yen (4.5 percent), as well as Canadian (2.3 percent) and Australian (1 percent) dollars.

The Central Bank’s total assets in foreign currencies and gold increased by $40.4 billion from July 2017 to June 2018, reaching $458.1 billion. –RT

Russian and others have been consistently moving away from the dollar and toward other currencies. Economic sanctions, which are losing their power as more countries move from the dollar, and trade wars seem to be fueling the dollar’s uncertainty.

Peter Schiff warns that as the supply of dollars is going to grow and grow, the demand for the American currency can fall, while the US Fed will be unable to stop the dollar’s demise. Schiff says that what is coming for Americans, is massive inflation.

“Eventually, what’s going to happen is it’s going to be the demand for those dollars is going to collapse, not the supply. And when the demand for dollars collapses, then the price of the dollar collapses. You get massive inflation. That is what is coming.”

Russia began its unprecedented dumping of U.S. Treasury bonds in April and May of last year. Russia appears to be moving on from the rise in tensions with the United States. The massive $81 billion spring sell-off coincided with the U.S.’s sanctioning of Russian businessmen, companies, and government officials. But Russia has long had plans to “beat” the U.S. when it comes to sanctions by stockpiling gold.

The Russian central bank’s First Deputy Governor Dmitry Tulin said that Moscow sees the acquisition of gold as a “100-percent guarantee from legal and political risks.”

As reported by RT, the Kremlin has openly stated that American sanctions and pressure are forcing Russia to find alternative settlement currencies to the U.S. dollar to ensure the security of the country’s economy. Other countries, such as China, India, and Iran, are also pursuing steps to challenge the greenback’s dominance in global trade.

***

India Begins Paying For Iranian Oil In Rupees Instead Of US Dollars

Three months ago, in Mid-October, Subhash Chandra Garg, economic affairs secretary at India’s finance ministry, said that India still hasn’t worked out yet a payment system for continued purchases of crude oil from Iran, just before receiving a waiver to continue importing oil from Iran in its capacity as Iran’s second largest oil client after China.

That took place amid reports that India had discussed ditching the U.S. dollar in its trading of oil with Russia, Venezuela, and Iran, instead settling the trade either in Indian rupees or under a barter agreement. One thing was certain: India wanted to keep importing oil from Iran, because Tehran offers generous discounts and incentives for Indian buyers at a time when the Indian government is struggling with higher oil prices and a weakening local currency that additionally weighs on its oil import bill.

Fast forward to the new year when we learn that India has found a solution to the problem, and has begun paying Iran for oil in rupees, a senior bank official said on Tuesday, the first such payments since the United States imposed new sanctions against Tehran in November. An industry source told Reuters that India’s top refiner Indian Oil Corp and Mangalore Refinery & Petrochemicals have made payments for Iranian oil imports.

To be sure, India, the world’s third biggest oil importer, has wanted to continue buying oil from Iran as it offers free shipping and an extended credit period, while Iran will use the rupee funds to mostly pay for imports from India.

“Today we received a good amount from some oil companies,” Charan Singh, executive director at state-owned UCO Bank told Reuters. He did not disclose the names of refiners or how much had been deposited.

Hinting that it wants to extend oil trade with Tehran, New Delhi recently issued a notification exempting payments to the National Iranian Oil Company (NIOC) for crude oil imports from steep withholding taxes, enabling refiners to clear an estimated $1.5 billion in dues.

Meanwhile, in lieu of transacting in US Dollars, Iran is devising payment mechanisms including barter with trading partners like India, China and Russia following a delay in the setting up of a European Union-led special purpose vehicle to facilitate trade with Tehran, its foreign minister Javad Zarif said earlier on Tuesday.

As Reuters notes, in the previous round of U.S. sanctions, India settled 45% of oil payments in rupees and the remainder in euros but this time it has signed deal with Iran to make all payments in rupees as New Delhi wanted to fix its trade balance with Tehran. Case in point: Indian imports from Iran totaled about $11 billion between April and November, with oil accounting for about 90 percent.

Singh said Indian refiners had previously made payments to 15 banks, but they will now be making deposits into the accounts of only 9 Iranian lenders as one had since closed and the U.S has imposed secondary sanctions on five others.

It’s all about control… Robert Fripp

Who Does America Really Belong To?

Not to Americans…

(Paul Craig Roberts) The housing market is now apparently turning down. Consumer incomes are limited by jobs offshoring and the ability of employers to hold down wages and salaries. The Federal Reserve seems committed to higher interest rates – in my view to protect the exchange value of the US dollar on which Washington’s power is based. The arrogant fools in Washington, with whom I spent a quarter century, have, with their bellicosity and sanctions, encouraged nations with independent foreign and economic policies to drop the use of the dollar. This takes some time to accomplish, but Russia, China, Iran, and India are apparently committed to dropping or reducing the use of the US dollar.

A drop in the world demand for dollars can be destabilizing of the dollar’s value unless the central banks of Japan, UK, and EU continue to support the dollar’s exchange value, either by purchasing dollars with their currencies or by printing offsetting amounts of their currencies to keep the dollar’s value stable. So far they have been willing to do both. However, Trump’s criticisms of Europe has soured Europe against Trump, with a corresponding weakening of the willingness to cover for the US. Japan’s colonial status vis-a-vis the US since the Second World War is being stressed by the hostility that Washington is introducing into Japan’s part of the world. The orchestrated Washington tensions with North Korea and China do not serve Japan, and those Japanese politicians who are not heavily on the US payroll are aware that Japan is being put on the line for American, not Japanese interests.

If all this leads, as is likely, to the rise of more independence among Washington’s vassals, the vassals are likely to protect themselves from the cost of their independence by removing themselves from the dollar and payments mechanisms associated with the dollar as world currency. This means a drop in the value of the dollar that the Federal Reserve would have to prevent by raising interest rates on dollar investments in order to keep the demand for dollars up sufficiently to protect its value.

As every realtor knows, housing prices boom when interest rates are low, because the lower the rate the higher the price of the house that the person with the mortgage can afford. But when interest rates rise, the lower the price of the house that a buyer can afford.

If we are going into an era of higher interest rates, home prices and sales are going to decline.

The “on the other hand” to this analysis is that if the Federal Reserve loses control of the situation and the debts associated with the current value of the US dollar become a problem that can collapse the system, the Federal Reserve is likely to pump out enough new money to preserve the debt by driving interest rates back to zero or negative.

Would this save or revive the housing market? Not if the debt-burdened American people have no substantial increases in their real income. Where are these increases likely to come from? Robotics are about to take away the jobs not already lost to jobs offshoring. Indeed, despite President Trump’s emphasis on “bringing the jobs back,” Ford Motor Corp. has just announced that it is moving the production of the Ford Focus from Michigan to China.

Apparently it never occurs to the executives running America’s off shored corporations that potential customers in America working in part time jobs stocking shelves in Walmart, Home Depot, Lowe’s, etc., will not have enough money to purchase a Ford. Unlike Henry Ford, who had the intelligence to pay workers good wages so they could buy Fords, the executives of American companies today sacrifice their domestic market and the American economy to their short-term “performance bonuses” based on low foreign labor costs.

What is about to happen in America today is that the middle class, or rather those who were part of it as children and expected to join it, are going to be driven into manufactured “double-wide homes” or single trailers. The MacMansions will be cut up into tenements. Even the high-priced rentals along the Florida coast will find a drop in demand as real incomes continue to fall. The $5,000-$20,000 weekly summer rental rate along Florida’s panhandle 30A will not be sustainable. The speculators who are in over their heads in this arena are due for a future shock.

For years I have reported on the monthly payroll jobs statistics. The vast majority of new jobs are in lowly paid nontradable domestic services, such as waitresses and bartenders, retail clerks, and ambulatory health care services. In the payroll jobs report for June, for example, the new jobs, if they actually exist, are concentrated in these sectors: administrative and waste services, health care and social assistance, accommodation and food services, and local government.

High productivity, high value-added manufactured jobs shrink in the US as they are offshored to Asia. High productivity, high value-added professional service jobs, such as research, design, software engineering, accounting, legal research, are being filled by offshoring or by foreigners brought into the US on work visas with the fabricated and false excuse that there are no Americans qualified for the jobs.

America is a country hollowed out by the short-term greed of the ruling class and its shills in the economics profession and in Congress. Capitalism only works for the few. It no longer works for the many.

On national security grounds Trump should respond to Ford’s announcement of offshoring the production of Ford Focus to China by nationalizing Ford. Michigan’s payrolls and tax base will decline and employment in China will rise. We are witnessing a major US corporation enabling China’s rise over the United States. Among the external costs of Ford’s contribution to China’s GDP is Trump’s increased US military budget to counter the rise in China’s power.

Trump should also nationalize Apple, Nike, Levi, and all the rest of the offshored US global corporations who have put the interest of a few people above the interests of the American work force and the US economy. There is no other way to get the jobs back. Of course, if Trump did this, he would be assassinated.

America is ruled by a tiny percentage of people who constitute a treasonous class. These people have the money to purchase the government, the media, and the economics profession that shills for them. This greedy traitorous interest group must be dealt with or the United States of America and the entirety of its peoples are lost.

In her latest blockbuster book, Collusion, Nomi Prins documents how central banks and international monetary institutions have used the 2008 financial crisis to manipulate markets and the fiscal policies of governments to benefit the super-rich.

These manipulations are used to enable the looting of countries such as Greece and Portugal by the large German and Dutch banks and the enrichment via inflated financial asset prices of shareholders at the expense of the general population.

One would think that repeated financial crises would undermine the power of financial interests, but the facts are otherwise. As long ago as November 21, 1933, President Franklin D. Roosevelt wrote to Col. House that “the real truth of the matter is, as you and I know, that a financial element in the larger centers has owned the Government ever since the days of Andrew Jackson.”

Thomas Jefferson said that “banking institutions are more dangerous to our liberties than standing armies” and that “if the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks . . . will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered.”

The shrinkage of the US middle class is evidence that Jefferson’s prediction is coming true.

Bloomberg’s Cudmore Stands By His Call: “The Dollar Is In A Multi-Year Down Trend”

This week on Erik Townsend’s MacroVoices podcast, Bloomberg macro strategist Mark Cudmore (a frequent contributor to ZeroHedge) and Townsend discussed last week’s “lower low” in the US dollar index and what this means for the near-term future of the greenback – a trade that will have profound ramifications for financial markets.

Back in October, Cudmore projected that the rise in the US dollar still had room to run as a shift in Chinese monetary policy (keep in mind this was months before the rumors about China cutting back on purchases of US debt emerged) would cause Treasury yields to climb, dragging the US dollar higher. The dollar finished the year on an upswing, but has slumped in recent weeks, ignoring the bounce in Treasury yields.

Treasury yields finished last week at their highest levels in years, but the dollar index slipped to its weakest level since late the final days of 2014.

Cudmore started by contrasting the consensus view heading into 2017 with the view heading into this year: Early last year, markets were dominated by the expectation that the US would lead a global reflation trade – but, as things turned out, the US wound up in the middle of the pack in terms of growth and inflation in terms of the G-10 economies.

This year, there’s been a shift: The US is still expected to be one of the fastest-growing G-10 economies this year. Yet positioning is much more bearish. Case in point: Two-year yields have gained about 70 basis points during the past four months.

And so, suddenly, that massive negative real yield you had in the US has kind of disappeared. So both the rates argument and the growth argument are much more supportive of the dollar this year than 12 months ago. And yet the kind of positioning and sentiment have switched massively.

Now I should say that this is kind of making me feel that the dollar is vulnerable to probably a sustainable bounce that could last several weeks, several months. But I think overall, structurally, in the much more longer term, I do kind of stick by my call from January of last year that the dollar is in a multi-year down trend.

And the background picture here is that the dollar still makes up roughly 63.5% of global reserves. And yet the US economy is a slowly shrinking part of the global economy. It’s currently about 24.5%.

Now, the US is the world’s reserve currency. It’s always going to retain a premium in terms of large financial markets. But that premium is going to shrink more and more. So the fact that it’s still 63.5% of reserves seems too high.

While Chinese authorities denied reports that they would scale back Treasury purchases, several European central banks, including – most notably – the German Bundesbank, said they would begin including yuan reserves for the first time. To make room on their balance sheets, they said, they would replace dollar-denominated assets with yuan-denominated assets.

Chart courtesy of Quartz

Chart courtesy of Quartz

…This would support Cudmore’s long-term view that the level of dollar-denominated reserves held by the largest central banks is “too large” – one reason Cudmore sees the long-term dollar downtrend continuing.

And the background picture here is that the dollar still makes up roughly 63.5% of global reserves. And yet the US economy is a slowly shrinking part of the global economy. It’s currently about 24.5%.

Now, the US is the world’s reserve currency. It’s always going to retain a premium in terms of large financial markets. But that premium is going to shrink more and more. So the fact that it’s still 63.5% of reserves seems too high.

So I think, structurally, the world is still long dollars and will slowly start trimming that position.

And that’s going to be a headwind for the dollar. But for the next couple of months I think people are maybe over their skis and being bearish, and I think there’s a chance of a bounce.

That’s the dynamic I’m looking at, at the moment.

Asked about the possibility that the impact of rising interest rates on the dollar might be delayed, resulting in a mid-year rally for the greenback as Powell continues his predecessors’ plan to raise the Fed funds rate at least three times this year, Cudmore argued that the reality is closer to the inverse of that view.

Instead of rising interest rates having a delayed effect on the greenback, Cudmore believes currency traders were far too eager to price in rising interest rates back in 2014, when the Bloomberg Dollar Index rallied more than 25% between mid-2014 and early 2017.

So, basically, when there were only two rate hikes we saw a 25% increase in the dollar on the trade weighted index. That’s because FX markets tend to front run the expectation of the rate hiking cycle. And this rate hike cycle was very much forecast, it was expected, it was predicted.

And, in fact, it kind of came through slower than expected. So what we saw was actually the FX already made that massive appreciation. And this is why we kind of saw the dynamic last year that, even though the Euro – Europe has done very little to withdraw stimulus. They’ve done a small bit of tapering and some signaling, but still they’ve got negative yields. We’ve seen the Euro benefit. And that’s because FX markets drive it ahead.

And I think people who get very excited about the fact that there were rate hikes in 2017 and wonder why isn’t the dollar rallying – they’re not really looking at history. We generally see this in US rate hiking cycles; we quite often see that the dollar trades poorly.

The notion that the dollar would weaken during interest-rate hiking cycles actually isn’t all that counter-intuitive: When the global economy is expanding rapidly, investors in developed markets pour money into the emerging world, which generally involves selling the world’s reserve currency – the dollar.

Another factor driving the dollar’s weakness is the new yuan-denominated oil futures contract which was slated to start trading on the Shanghai Futures Exchange this week, but was recently delayed. Asked if he believes the contract will have a lasting impact on the greenback, Cudmore said its impact will likely be more nuanced, starting with the notion that the impact will be gradual: Though ultimately it will help change the narrative surrounding the dollar at the margins.

I think this is another step in the process of the dollar’s dominance of world trade, world commodity pricing, being slightly eroded at the margin.

But it’s not going to be a sudden thing. The dollar will remain the world’s reserve currency for a number of years to come. There’s just no viable alternative. It’s just that its complete share of global trading will continue to be eroded. And that’s another step in this process.

I think it is also important about how successful China manages to make this whole oil contract. And I think this may tie in with the – some people speculate this may tie in with the Saudi Aramco IPO, that maybe they can exchange some kind of support there, from Saudi Arabia for their pricing in terms of maybe investing in the IPO.

In recent months, Bill Gross has doubled down on his call that the 30-year bull market in bonds is over. DoubleLine’s Jeffrey Gundlach has made a similar argument, though the two disagree on details like timing (“Bill Gross is early”) and the location of the crucial barrier in the 10-year yield that, once breached, will trigger a correction in US equity prices.

Cudmore says he agrees that great bond bull market has ended. But having said this, Cudmore cautioned that he’s “absolutely not a bond bear.”

I think the 30-year bond bull market ended a year or so ago. I don’t think that suddenly means we need to go into a bear market. I think that – I’m absolutely not a bond bear and I think we kind of stay in this slightly volatile range for a long time to come.

And I’ll even go further and say that I don’t think the long end yields in developed, functioning societies, and developed, functioning markets are rising substantially for many years to come.

So I don’t think we’re going to see much higher yields at the back end of the curve. We can see tickups and they’ll kind of move back and forth. But, to me, there are structural disinflationary pressures which are still underestimated in the market. Particularly from technology. But also from demographics.

Townsend then moved the conversation to a painful topic for both himself and Cudmore: The rally in oil that has brought WTI futures north of $70 for the first time since 2014.

Both Townsend and Cudmore had gone on record to predict that the bounce in energy prices would be temporary – the result of worsening instability in Venezuela and certain Middle Eastern energy producers. However, the sustained rally has forced Cudmore to reevaluate his views on the energy market.

While speculative long positions have become dangerously stretched (net longs on NYMEX recently touched an all-time high), Cudmore says he only recently came around to the notion that speculators can dominate the directionality of commodity markets for long periods of time.

I thought we’d see spikes when we saw Middle East tension. I thought there would be various reasons for supply spikes. And I thought they could be very large spikes. But I thought they’d be a thing that would last for a month or so and then we’d see prices come down. Instead we’ve just seen oil continue to trend higher. And definitely this has taken me by surprise.

I think, though, that it’s not a permanent change of situation. One of the things that’s driving the markets at the moment – and I didn’t really pick up on this into December so much – is that, importantly for oil markets, speculators can actually dominate the price action for such a long period of time.

And, at the moment, we still have this backwardation in the oil curve, which means it rewards speculators for being long oil. And so a lot of people look at the market and go, oh my God, speculative positioning in oil is just completely stretched, it’s crazy, it’s due a massive correction. And people were saying this from a couple of months ago.

Yet it continues to motor higher. And that’s because, you know what, these speculators are getting paid to hold this position. So, even if it falls back a little bit, they’re not too worried. And that means it’s a very comfortable position. That will change at some point.

Over the long term, of course, oil prices will likely decline as alternatives like solar – and to a larger degree natural gas – eat into demand.

Listen to the rest of the interview below:

https://publisher.podtrac.com/player/NzE4NDQ1/MTM20

Suddenly, “De-Dollarization” Is A Thing

For what seems like decades, other countries have been tiptoeing away from their dependence on the US dollar.

China, Russia, and India have cut deals in which they agree to accept each others’ currencies for bi-lateral trade while Europe, obviously, designed the euro to be a reserve asset and international medium of exchange.

These were challenges to the dollar’s dominance, but they weren’t mortal threats.

What’s happening lately, however, is a lot more serious.

It even has an ominous-sounding name: de-dollarization. Here’s an excerpt from a much longer article by “strategic risk consultant” F. William Engdahl:

Gold, Oil and De-Dollarization? Russia and China’s Extensive Gold Reserves, China Yuan Oil Market

(Global Research) – China, increasingly backed by Russia—the two great Eurasian nations—are taking decisive steps to create a very viable alternative to the tyranny of the US dollar over world trade and finance. Wall Street and Washington are not amused, but they are powerless to stop it.

So long as Washington dirty tricks and Wall Street machinations were able to create a crisis such as they did in the Eurozone in 2010 through Greece, world trading surplus countries like China, Japan and then Russia, had no practical alternative but to buy more US Government debt—Treasury securities—with the bulk of their surplus trade dollars. Washington and Wall Street could print endless volumes of dollars backed by nothing more valuable than F-16s and Abrams tanks. China, Russia and other dollar bond holders in truth financed the US wars that were aimed at them, by buying US debt. Then they had few viable alternative options.

Viable Alternative Emerges

Now, ironically, two of the foreign economies that allowed the dollar an artificial life extension beyond 1989—Russia and China—are carefully unveiling that most feared alternative, a viable, gold-backed international currency and potentially, several similar currencies that can displace the unjust hegemonic role of the dollar today.

For several years both the Russian Federation and the Peoples’ Republic of China have been buying huge volumes of gold, largely to add to their central bank currency reserves which otherwise are typically in dollars or euro currencies. Until recently it was not clear quite why.

For several years it’s been known in gold markets that the largest buyers of physical gold were the central banks of China and of Russia. What was not so clear was how deep a strategy they had beyond simply creating trust in the currencies amid increasing economic sanctions and bellicose words of trade war out of Washington.

Now it’s clear why.

China and Russia, joined most likely by their major trading partner countries in the BRICS (Brazil, Russia, India, China, South Africa), as well as by their Eurasian partner countries of the Shanghai Cooperation Organization (SCO) are about to complete the working architecture of a new monetary alternative to a dollar world.

Currently, in addition to founding members China and Russia, the SCO full members include Kazakhstan, Kyrgyzstan, Tajikistan, Uzbekistan, and most recently India and Pakistan. This is a population of well over 3 billion people, some 42% of the entire world population, coming together in a coherent, planned, peaceful economic and political cooperation.

Gold-Backed Silk Road

It’s clear that the economic diplomacy of China, as of Russia and her Eurasian Economic Union group of countries, is very much about realization of advanced high-speed rail, ports, energy infrastructure weaving together a vast new market that, within less than a decade at present pace, will overshadow any economic potentials in the debt-bloated economically stagnant OECD countries of the EU and North America.

What until now was vitally needed, but not clear, was a strategy to get the nations of Eurasia free from the dollar and from their vulnerability to further US Treasury sanctions and financial warfare based on their dollar dependence. This is now about to happen.

At the September 5 annual BRICS Summit in Xiamen, China, Russian President Putin made a simple and very clear statement of the Russian view of the present economic world. He stated, “Russia shares the BRICS countries’ concerns over the unfairness of the global financial and economic architecture, which does not give due regard to the growing weight of the emerging economies. We are ready to work together with our partners to promote international financial regulation reforms and to overcome the excessive domination of the limited number of reserve currencies.”

To my knowledge he has never been so explicit about currencies. Put this in context of the latest financial architecture unveiled by Beijing, and it becomes clear the world is about to enjoy new degrees of economic freedom.

China Yuan Oil Futures

According to a report in the Japan Nikkei Asian Review, China is about to launch a crude oil futures contract denominated in Chinese yuan that will be convertible into gold. This, when coupled with other moves over the past two years by China to become a viable alternative to London and New York to Shanghai, becomes really interesting.

China is the world’s largest importer of oil, the vast majority of it still paid in US dollars. If the new Yuan oil futures contract gains wide acceptance, it could become the most important Asia-based crude oil benchmark, given that China is the world’s biggest oil importer. That would challenge the two Wall Street-dominated oil benchmark contracts in North Sea Brent and West Texas Intermediate oil futures that until now has given Wall Street huge hidden advantages.

That would be one more huge manipulation lever eliminated by China and its oil partners, including very specially Russia. Introduction of an oil futures contract traded in Shanghai in Yuan, which recently gained membership in the select IMF SDR group of currencies, oil futures especially when convertible into gold, could change the geopolitical balance of power dramatically away from the Atlantic world to Eurasia.

In April 2016 China made a major move to become the new center for gold exchange and the world center of gold trade, physical gold. China today is the world’s largest gold producer, far ahead of fellow BRICS member South Africa, with Russia number two.

Now to add the new oil futures contract traded in China in Yuan with the gold backing will lead to a dramatic shift by key OPEC members, even in the Middle East, to prefer gold-backed Yuan for their oil over inflated US dollars that carry a geopolitical risk as Qatar experienced following the Trump visit to Riyadh some months ago. Notably, Russian state oil giant, Rosneft just announced that Chinese state oil company, CEFC China Energy Company Ltd. Just bought a 14% share of Rosneft from Qatar. It’s all beginning to fit together into a very coherent strategy.

Meanwhile, in Latin America:

De-Dollarization Spikes – Venezuela Stops Accepting Dollars For Oil Payments

(Zero Hedge) – Did the doomsday clock on the petrodollar (and implicitly US hegemony) just tick one more minute closer to midnight?

Apparently confirming what President Maduro had warned following the recent US sanctions, The Wall Street Journal reports that Venezuela has officially stopped accepting US Dollars as payment for its crude oil exports.

As we previously noted, Venezuelan President Nicolas Maduro said last Thursday that Venezuela will be looking to “free” itself from the U.S. dollar next week. According to Reuters, “Venezuela is going to implement a new system of international payments and will create a basket of currencies to free us from the dollar,” Maduro said in a multi-hour address to a new legislative “superbody.” He reportedly did not provide details of this new proposal.

Maduro hinted further that the South American country would look to using the yuan instead, among other currencies.

“If they pursue us with the dollar, we’ll use the Russian ruble, the yuan, yen, the Indian rupee, the euro,” Maduro also said.

The state oil company Petróleos de Venezuela SA, known as PdVSA, has told its private joint venture partners to open accounts in euros and to convert existing cash holdings into Europe’s main currency, said one project partner.

This first step towards one or more gold-backed Eurasian currencies certainly looks like a viable and — for a lot of big players out there — welcome addition to the global money stock.

Venezuela, meanwhile illustrates the growing perception of US weakness. It used to be that a small country refusing to take dollars could expect regime change in short order. Now, maybe not so much.

Combine the above with the emergence of bitcoin and its kin as the preferred monetary asset of techies and libertarians, and the monetary world suddenly looks downright multi-polar.

ALERT: The US Dollar Getting Dumped By Investors

What the heck is going on?

China Quietly Prepares Golden Alternative to Dollar System

China, as current chair of the G-20 group of nations, called on France to organize a very special conference in Paris. The fact such a conference would even take place in an OECD country is a sign of how weakened the hegemony of the US-dominated Dollar System has become.

On March 31 in Paris a special meeting, named “Nanjing II,” was held. People’s Bank of China Governor, Zhou Xiaochuan, was there and made a major presentation on, among other points, broader use of the IMF special basket of five major world currencies, the Special Drawing Rights or SDR’s. The invited were a very select few. The list included German Finance Minister Wolfgang Schaeuble, UK Chancellor of the Exchequer George Osborne, IMF Managing Director Christine Lagarde discussed the world’s financial architecture together with China. Apparently and significantly, there was no senior US official present.

On the Paris talks, Bloomberg reported: “China wants a much more closely managed system, where private-sector decisions can be managed by governments,” said Edwin Truman, a former Federal Reserve and US Treasury official. “The French have always favored international monetary reform, so they’re natural allies to the Chinese on this issue.”

A China Youth Daily journalist present in Paris noted, “Zhou Xiaochuan pointed out that the international monetary and financial system is currently undergoing structural adjustment, the world economy is facing many challenges…” According to the journalist Zhou went on to declare that China’s aim as current President of the G20 talks is to “promote the wider use of the SDR.”

For most of us, that sounds about as exciting as watching Johnson grass grow in the Texas plains. However, behind that seemingly minor technical move, as is becoming clearer by the day, is a grand Chinese strategy, if it succeeds or not, a grand strategy to displace the dominating role of the US dollar as world central bank reserve currency. China and others want an end to the tyranny of a broken dollar system that finances endless wars on other peoples’ borrowed money with no need to ever pay it back. The strategy is to end the domination of the dollar as the currency for most world trade in goods and services. That’s no small beer.

Despite the wreck of the US economy and the astronomical $19 trillion public debt of Washington, the dollar still makes up 64% of all central bank reserves. The largest holder of US debt is the Peoples Republic of China, with Japan a close second. As long as the dollar is “king currency,” Washington can run endless budget deficits knowing well that countries like China have no serious alternative to invest its foreign currency trade profits but in US Government or government-guaranteed debt. In effect, as I have pointed out, that has meant that China has de facto financed the military actions of Washington that act to go against Chinese or Russian sovereign interests, to finance countless US State Department Color Revolutions from Tibet to Hong Kong, from Libya to Ukraine, to finance ISIS in the Middle East and on and on and on…

Multi-currency world

If we look more closely at all the steps of the Beijing government since the global financial crisis of 2008 and especially since their creation of the Asian Infrastructure Investment Bank, the BRICS New Development Bank, the bilateral national currency energy agreements with Russia bypassing the dollar, it becomes clear that Zhou and the Beijing leadership have a long-term strategy.

As British economist David Marsh pointed out in reference to the recent Paris Nanjing II remarks of Zhou, “China is embarking, pragmatically but steadily, towards enshrining a multi-currency reserve system at the heart of the world’s financial order.”

Since China’s admission into the IMF select group of SDR currencies last November, the multi-currency system, which China calls “4+1,” would consist of the euro, sterling, yen and renminbi (the 4), co-existing with the dollar. These are the five constituents of the SDR.

To strengthen the recognition of the SDR, Zhou’s Peoples’ Bank of China has begun to publish its foreign reserves total–the world’s biggest–in SDRs as well as dollars.

A golden future

Yet the Chinese alternative to the domination of the US dollar is about far more than paper SDR currency basket promotion. China is clearly aiming at the re-establishment of an international gold standard, presumably one not based on the bankrupt Bretton Woods Dollar-Gold exchange that President Richard Nixon unilaterally ended in August, 1971 when he told the world they would have to swallow paper dollars in the future and could no longer redeem them for gold. At that point global inflation, measured in dollar terms, began to soar in what future economic historians will no doubt dub The Greatest Inflation.

By one estimate, the dollars in worldwide circulation rose by some 2,500% between 1970 and 2000. Since then the rise has clearly brought it well over 3,000%. Without a legal requirement to back its dollar printing by a pre-determined fixed amount of gold, all restraints were off in a global dollar inflation. So long as the world is forced to get dollars to settle accounts for oil, grain, other commodities, Washington can write endless checks with little fear of them bouncing, stamped “insufficient funds.”

Combined with the fact that over that same time span since 1971 there has been a silent coup of the Wall Street banks to hijack any and all semblance of representative democracy and Constitution-based rules, we have the mad money machine, much like the German poet Goethe’s 18th Century fable, Sorcerers’ Apprentice, or in German, Der Zauberlehrling. Dollar creation is out of control.

Since 2015 China is moving very clearly to replace London and New York and the western gold futures price-setting exchanges. As I noted in a longer analysis in this space in August, 2015, China, together with Russia, is making major strides to back their currencies with gold, to make them “as good as gold,” while currencies like the debt-bloated Euro or the debt-bloated bankrupt dollar zone, struggle.

In May 2015, China announced it had set up a state-run Gold Investment Fund. The aim was to create a pool, initially of $16 billion making it the world’s largest physical gold fund, to support gold mining projects along the new high-speed railway lines of President Xi’s New Economic Silk Road or One Road, One Belt as it is called. As China expressed it, the aim is to enable the Eurasian countries along the Silk Road to increase the gold backing of their currencies. The countries along the Silk Road and within the BRICS happen to contain most of the world’s people and natural and human resources utterly independent of any the West has to offer.

In May 2015, China’s Shanghai Gold Exchange formally established the “Silk Road Gold Fund.” The two main investors in the new fund were China’s two largest gold mining companies–Shandong Gold Group who bought 35% of the shares and Shaanxi Gold Group with 25%. The fund will invest in gold mining projects along the route of the Eurasian Silk Road railways, including in the vast under-explored parts of the Russian Federation.

A little-known fact is that no longer is South Africa the world’s gold king. It is a mere number 7 in annual gold production. China is Number One and Russia Number Two.

On May 11, just before creation of China’s new gold fund, China National Gold Group Corporation signed an agreement with the Russian gold mining group, Polyus Gold, Russia’s largest gold mining group, and one of the top ten in the world. The two companies will explore the gold resources of what is to date Russia’as largest gold deposit at Natalka in the far eastern part of Magadan’s Kolyma District.

Recently, the Chinese government and its state enterprises have also shifted strategy. Today, as of March 2016 official data, China holds more than $3.2 trillion in foreign currency reserves at the Peoples’ bank of China, of which it is believed approximately 60% or almost $2 trillion are dollar assets such as US Treasury bonds or quasi-government bonds such as Fannie Mae or Freddie Mac mortgage bonds. Instead of investing all its dollar earnings from trade surpluses into increasingly inflated and worthless US government debt, China has launched a global asset buying strategy.

Now it happens that prime on the Beijing foreign asset “to buy” shopping list are gold mines around the world. Despite a recent slight rise in the gold price since January, gold is still at 5 year-lows and many quality proven mining companies are cash-starved and forced into bankruptcy. Gold is truly at the beginning of a renaissance.

The beauty of gold is not only what countless gold bugs maintain, a hedge against inflation. It is the most beautiful of all precious metals. The Greek philosopher Plato, in his work The Republic, identified five types of regimes possible–Aristocracy, Timocracy, Oligarchy, Democracy, and Tyranny, with Tyranny the lowest most vile. He then lists Aristocracy, or rule by Philosopher Kings with “golden souls” as the highest form of rule, benevolent and with the highest integrity. Gold has worth in its own right throughout mankind’s history. China and Russia and other nations of Eurasia today are reviving gold to its rightful place. That’s very cool.