The Fed, reportedly, took action in 2019 – with its massive flip-flop, cutting rates drastically and expanding its balance sheet at the fastest pace since the financial crisis – in order to ‘fix’ the yield curve which had dropped into the media-terrifying inverted state… but what investors (and The Fed) appear to have forgotten (or choose to ignore) is that it is now much more concerning.

The last few months have seen the yield curve steepen dramatically, up 35bps from August’s -5bps spread in 2s10s to over 30bps today – the steepest since October 2018…

Source: Bloomberg

That is great news, right? No more recession risk, right?

Wrong!

While investors buy stocks with both hands and feet, we take a look at how risk assets perform after the curve flattens and/or inverts. According to back tests from Goldman, while risky assets in general can have positive performance with a flat yield curve, risky asset performances tend to be lower. This is consistent with Goldman’s base case forecast combining low (but positive) returns from here given the lack of profit growth and a less favorable macro backdrop.

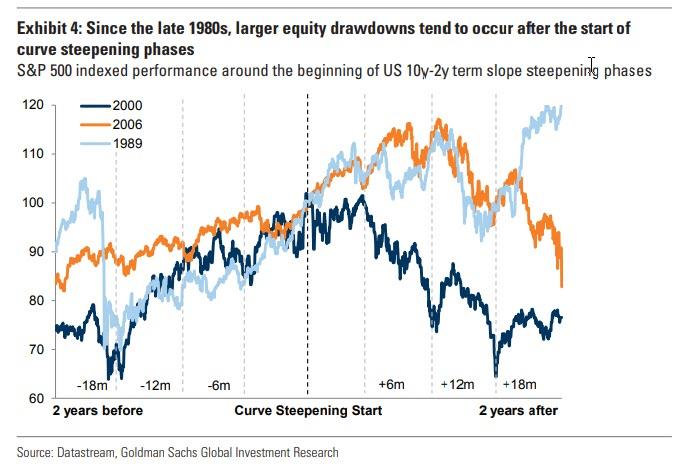

What is far more notable, as ZeroHedge showed most recently last July, is that since the mid-1980s, significant stock draw downs (i.e. market crashes) began only when term slope started steepening after being inverted.

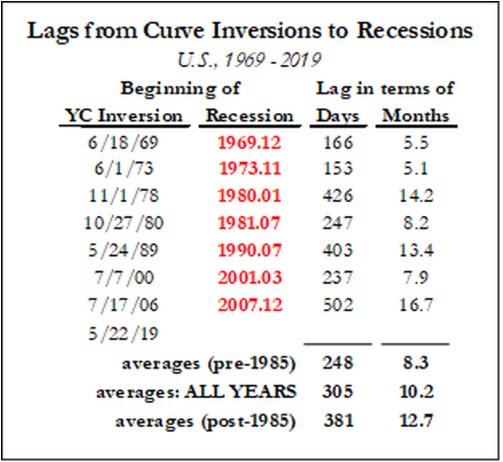

And remember, the yield curve’s forecasting record since 1968 has been perfect: not only has each inversion been followed by a recession, but no recession has occurred in the absence of a prior yield-curve inversion. There’s even a strong correlation between the initial duration and depth of the curve inversion and the subsequent length and depth of the recession.

So, be careful what you wish for… and celebrate; because as history has shown, the un-inverting of the yield curve is when the recessions start and when the markets begin to reflect reality.