Here we go again. The 10-year – 3-month Treasury curve has turned negative again.

Here we go again. The 10-year – 3-month Treasury curve has turned negative again.

Three Worlds

“America’s yield curve inversion can mean one of three things,” said (Eric Peters, CIO of One River Asset Management). “We’re either living in a world of secular stagnation and investors worry that central banks no longer have sufficient policy tools to spur growth and inflation,” he continued. “Or the economy is simply sliding toward recession and the inversion will persist until the Fed panics and spurs a recovery,” he said. “Or we’re living in a world, where the market is moving in ways that defy historical norms because of global QE. And if that’s the case, the curve is sending a false signal.”

“If we’re sliding toward recession, then it seems odd that credit markets are holding up so well,” continued the same CIO. “So keep an eye on those,” he said. “And if the curve is sending a false signal due to German and Japanese government bonds yielding less than zero out to 10yrs, then the recent Fed pivot and these low bond rates in America may very well spur a blow-off rally in stocks like in 1999.” A dovish Fed in 1998 (post-LTCM) and 1999 (pre-Y2K) provided the liquidity without which that parabolic rally could have never happened.

“But if investors believe America is succumbing to the secular stagnation that has gripped Japan and Europe, and if they’re growing scared that global central banks are no longer capable of rescuing markets, then we have a real problem,” said the CIO. “Because a recession is bad for markets, but not catastrophic provided that central banks can step in to spur recovery. But with global rates already so low, if investors lose faith in the ability of central banks to do what they have always done, then we’re vulnerable to a stock market crash.”

Sovereignty:

Turkish overnight interest rates squeezed to 300% on Monday. Then 600% on Tuesday. By Wednesday, they hit 1,200%. Downward pressure on the Turkish lira, and the government’s efforts to punish speculators fueled the historic rise. Erdogan allegedly wants to limit lira loses ahead of today’s elections. The pressures that drove the currency lower were mainly of Turkish origin. Of course, the Turks have every right to their own economic policies, but they must bear the consequences. That’s what comes with being a sovereign state.

The Greeks and Turks are neighbors. The Turks began negotiations to join the EU in 2005, with plans to adopt the Euro after their acceptance. Those negotiations stalled in 2016. As they look across the border at their Greek neighbors now, and see their interest rates stuck at -0.40%, are they envious? Perhaps. But having witnessed the 2011 Greek humiliation, would the Turks be willing to forfeit sovereignty for the Euro’s stability and stagnation? And how do the Greeks (and Italians) feel about having forfeited their sovereignty?

Anecdote:

“Only optimists start companies,” I answered. The Australian superannuation CEO had asked if I’m an optimist or pessimist. “I see the potential for technological advances to produce abundance in ways difficult to fathom. But I also see the chance of something profoundly dark,” I continued. He observed that people seemed consumed by the latter but spend so little time on the former. “That’s good. Humans are wonderful at solving problems of our own creation. The more we worry, the less goes wrong,” I said. So he asked what worries me most?

“Not the displacement of human labor by machines, we can solve the resulting social challenges. I worry that the only thing Americans seem to agree on now is that China is our adversary.” And pressing, he asked me to list the things I admire about China. “Okay. I admire China’s work ethic, drive, ambition, economic accomplishments. They’ve overtaken us in many advanced scientific fields. I admire that very much.” He smiled and asked me to carry on. “I’m grateful for their competition. It makes us better. And I admire that they’ve evolved communism to make it work while all others failed. The world is better with diversity of thought, philosophy – diversity increases resiliency, robustness. And democratic free-market capitalism will grow stronger with a formidable competitor.” He smiled.

“But China’s system values the collective over the individual. We value the opposite. And I’m concerned the two systems cannot peacefully coexist now that we’re the world’s two largest economies. I don’t want to live under their system, I don’t want their vision of the future for my children. They probably feel the same way. Both views are valid but incompatible, and increasingly in conflict,” I explained. He nodded and said, “I don’t want that for our children either.”

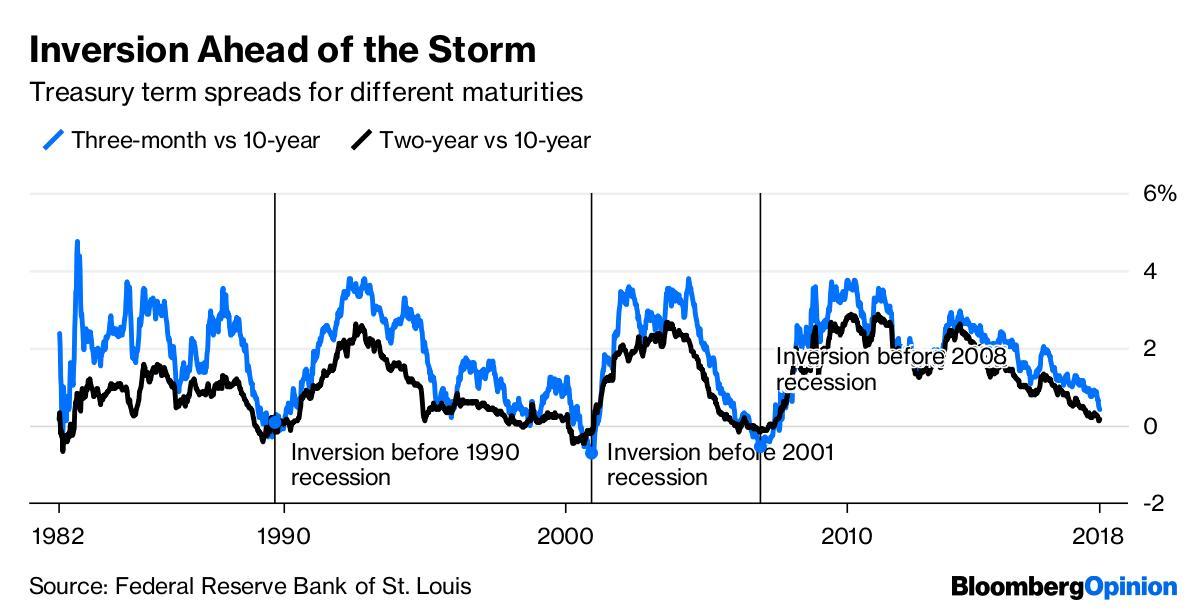

The most prescient recession indicator in the market just inverted for the first time since 2007.

Don’t believe us? Here is Larry Kudlow last summer explaining that everyone freaking out about the 2s10s spread is silly, they focus on the 3-month to 10-year spread that has preceded every recession in the last 50 years (with few if any false positives)… (fwd to 4:20)

“Actually we’re reading the spread wrong,” Larry Kudlow says of the flattening yield curve. “There’s no recession in sight right now.” #DeliveringAlpha https://t.co/gcJmBKvV1x pic.twitter.com/zj2SWqIXhd

— CNBC (@CNBC) July 19, 2018

As we noted below, on six occasions over the past 50 years when the three-month yield exceeded that of the 10-year, economic recession invariably followed, commencing an average of 311 days after the initial signal.

And here is Bloomberg showing how the yield curve inverted in 1989, in 2000 and in 2006, with recessions prompting starting in 1990, 2001 and 2008. This time won’t be different.

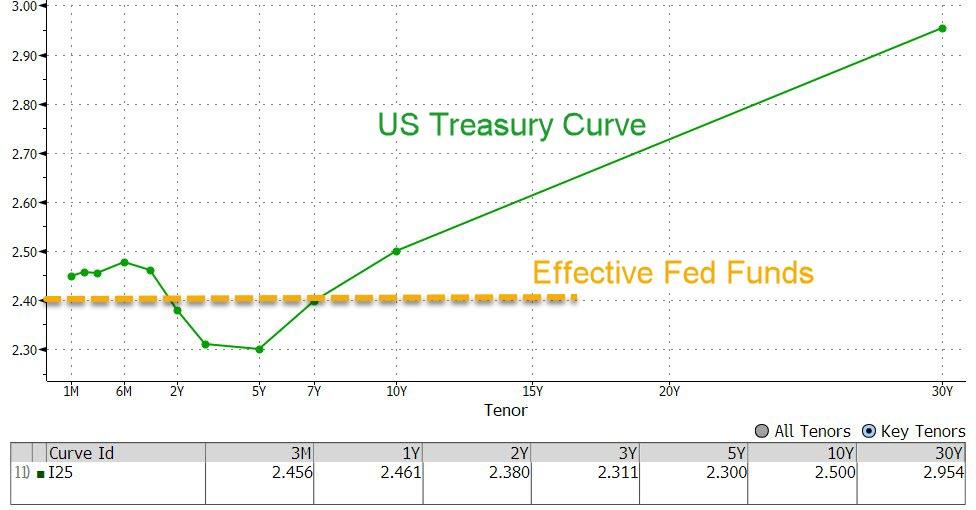

On the heels of a dismal German PMI print, world bond yields have tumbled, extending US Treasuries’ rate collapse since The Fed flip-flopped full dovetard.

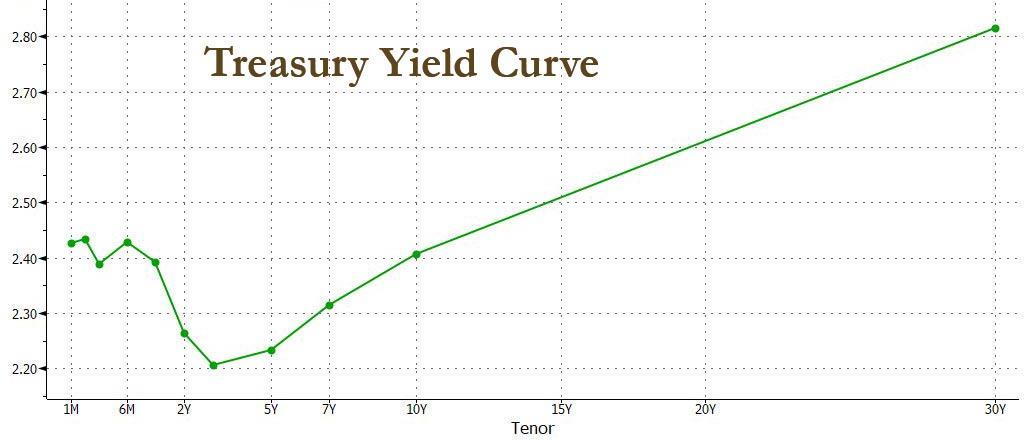

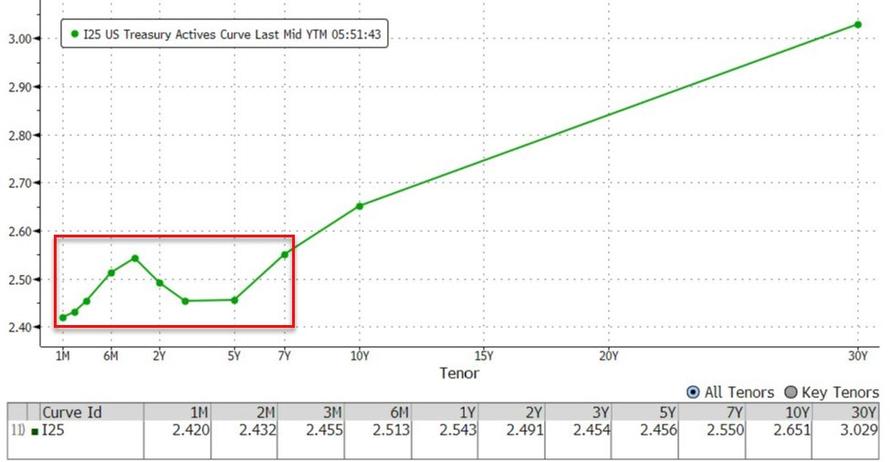

The yield curve is now inverted through 7Y…

With the 7Y-Fed-Funds spread negative…

Bonds and stocks bid after Powell threw in the towell last week…

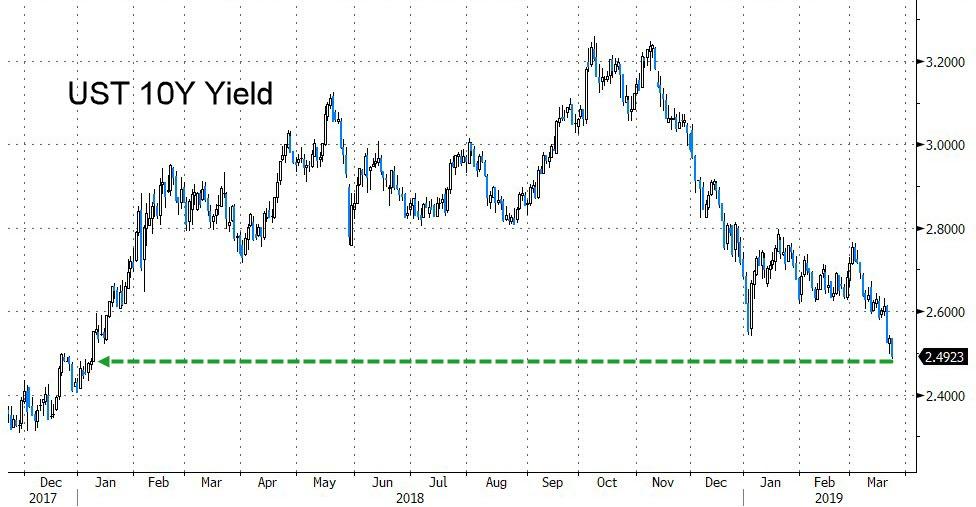

But the message from the collapse in bond yields is too loud to ignore. 10Y yields have crashed below 2.50% for the first time since Jan 2018…

Crushing the spread between 3-month and 10-year Treasury rates to just 2.4bps – a smidge away from flashing a big red recession warning…

Critically, as Jim Grant noted recently, the spread between the 10-year and three-month yields is an important indicator, James Bianco, president and eponym of Bianco Research LLC notes today. On six occasions over the past 50 years when the three-month yield exceeded that of the 10-year, economic recession invariably followed, commencing an average of 311 days after the initial signal.

Bianco concludes that the market, like Trump, believes that the current Funds rate isn’t low enough:

While Powell stressed over and over that the Fed is at “neutral,” . . . the market is saying the rate hike cycle ended last December and the economy will weaken enough for the Fed to see a reason to cut in less than a year.

Equity markets remain ignorant of this risk, seemingly banking it all on The Powell Put. We give the last word to DoubleLine’s Jeff Gundlach as a word of caution on the massive decoupling between bonds and stocks…

“Just because things seem invincible doesn’t mean they are invincible. There is kryptonite everywhere. Yesterday’s move created more uncertainty.”

The bond bull market is alive and well with yesterday’s bond-bear-battering by The Fed extending this morning.

10Y Yields are back below 2.50% for the first time since Jan 2018…

…completely decoupled from equity markets….

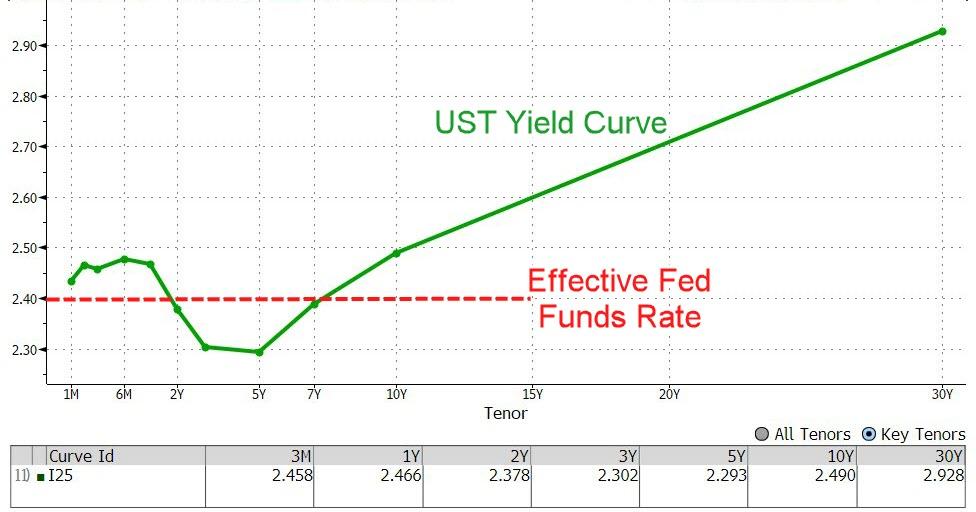

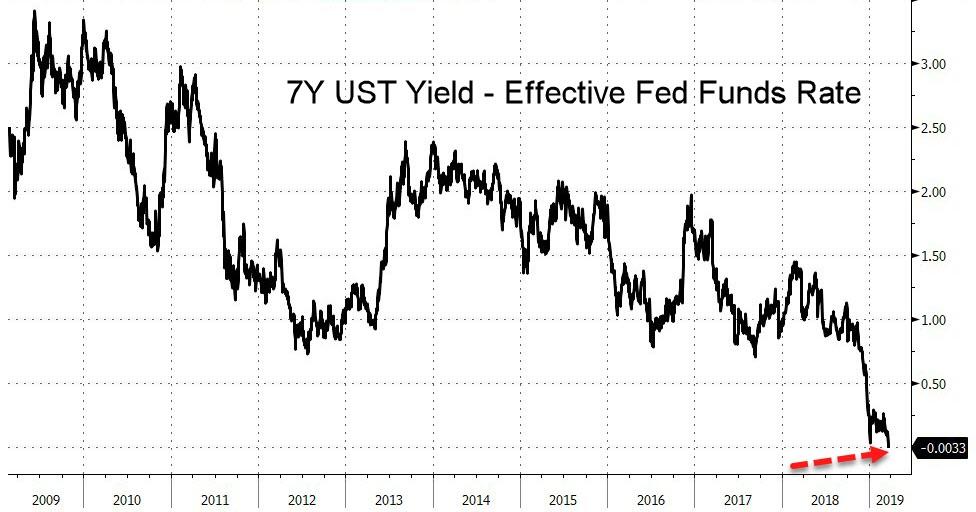

The yield is now massively inverted to Fed Funds…

With 7Y yields now below effective fed funds rate…

The yield curve is inverted in 11 different spots. The latest is 5-year to 3-month inversion.

The yield curve recession signal is louder and louder. Inversions are persistent and growing.

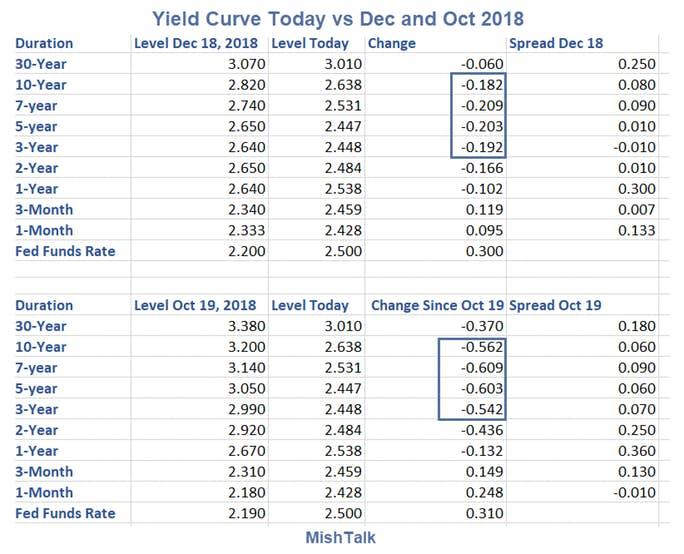

Let’s compare the spreads today to that of December 18, the start of the December 2018 FOMC meeting.

Yield Curve 2019-02-26 vs December and October 2018

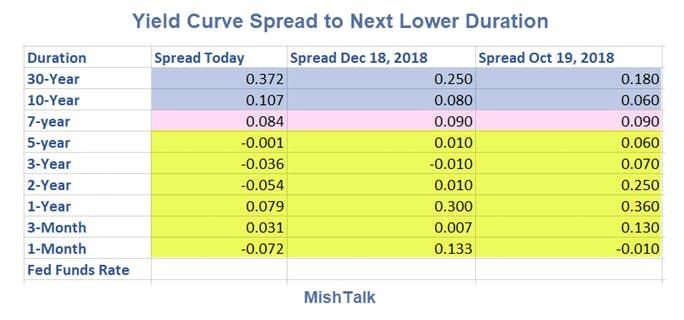

Yield Curve Spread Analysis

Spread Changes

Something Happening

Something is happening. What is it?

Possibilities

My take is number one and possibly all three.

An in regards to recession the economy is weakening fast.

Source: by Mike Shedlock via MishTalk| ZeroHedge

US core factory orders (ex transports) fell for the second month in a row in December. This is the worst sequential drop since Feb 2016.

New orders ex-trans fell 0.6% in Dec. after falling 1.3% the prior month.

The headline factory orders rose 0.1% MoM (well below the 0.6% MoM gain expected).

Capital goods non-defense ex aircraft new orders for Dec. fall 1% after falling 1.1% in Nov.

Non-durables shipments for Dec. fall 1% after falling 2% in Nov.

Not a pretty picture, but it was an 8.0% drop in Defense spending that triggered the weakness – so we’re gonna need moar war.

Money manager Michael Pento is sounding the alarm because we are getting very close to something called a “yield curve inversion.” Pento explains, “Why do I care if the yield curve inverts? Because 9 out of the last 10 times the yield curve inverted, we had a recession… The spread with the yield curve is the narrowest it has been since outside of the start of the Great Recession that commenced in December of 2007… The last two times the yield curve inverted, we had a stock market drop of 50%. The market dropped, and the S&P 500 lost 50% of its value.”

For those who don’t have enough money to require professional management, consider storing water and food because that will never go out of style.

The curious case of the inverted yield curve in China’s $1.7 trillion bond market is worsening as WSJ notes that an odd combination of seasonally tight funding conditions and economic pessimism pushed long-dated yields well below returns on one-year bonds, the shortest-dated government debt.

10-Year China bond yields fell to 3.55% overnight as the 1-Year yield rose to 3.61% – the most inverted in history, more so than in June 2013, when an unprecedented cash crunch jolted Chinese markets and nearly brought the nation’s financial system to its knees.

This inversion is being exacerbated by seasonally tight funding conditions.

This inversion is being exacerbated by seasonally tight funding conditions.

June is traditionally a tight time for banks because of regulatory checks, and, as Bloomberg reports, this year, lenders are grappling with an official campaign to reduce the level of borrowing as well.

Wholesale funding costs climbed to the most expensive in history, and the 30-day Shanghai Interbank Offered Rate has jumped 51 basis points this month to the highest level in more than two years.

And this demand for liquidity comes as Chinese banks’ excess reserve ratio, a gauge of liquidity in the financial system, fell to 1.65 percent at the end of March, according to data from the China Banking Regulatory Commission. The index measures the money that lenders park at the PBOC above and beyond the mandatory reserve requirement, usually to draw risk-free interest.

“Major banks don’t have much extra funds, as is shown by the excess reserve data,” analysts at China Minsheng Banking Corp.’s research institute wrote in a June 5 note. Lenders have become increasingly reliant on wholesale funding and central bank loans this year, they said.

As The Wall Street Journal reports, an inverted yield curve defies common understanding that bonds requiring a longer commitment should compensate investors with a higher return. It usually reflects investor pessimism about a country’s long-term growth and inflation prospects.

“But the curve inversion we are seeing right now is one with Chinese characteristics and it’s different from the previous one in the U.S.,” said Deng Haiqing, chief economist at JZ Securities.

The current anomaly in the Chinese bond market is partly the result of mild inflation and expectations of a slowing economy, Mr. Deng said. “At the same time, short-term interest rates will likely stay elevated because the authorities will keep borrowing costs high so as to facilitate the deleveraging campaign,” he said.

Notably, it appears officials are concerned at the potential for fallout from this crisis situation.

In an article published Saturday, the central bank’s flagship newspaper, Financial News, said that the severe credit crunch four years ago won’t repeat itself this month because the central bank will keep liquidity conditions “not too loose but also not too tight.”

Chinese financial markets tend to be particularly jittery come June due to a seasonal surge of cash demand arising from corporate-tax payments and banks’ need to meet regulatory requirements on capital.On Sunday, the official Xinhua News Agency ran a similar commentary that sought to stabilize markets expectations. “Don’t panic,” it urged investors.

Sounds like exactly the time to ‘panic’ if your money is in this.