(ZeroHedge) Back in March 2017, a bearish trade emerged which quickly gained popularity on Wall Street, and promptly received the moniker “The Next Big Short.”

As we reported at the time, similar to the run-up to the housing debacle, a small number of bearish funds were positioning to profit from a “retail apocalypse” that could spur a wave of defaults. Their target: securities backed not by subprime mortgages, but by loans taken out by beleaguered mall and shopping center operators which had fallen victim to the Amazon juggernaut. And as bad news piled up for anchor chains like Macy’s and J.C. Penney, bearish bets against commercial mortgage-backed securities kept rising.

The trade was simple: shorting malls by going long default risk via CMBX 6 (BBB- or BB) or otherwise shorting the CMBS complex. For those who have not read our previous reports (here, here, here, here, here, here and here) on the second Big Short, here is a brief rundown via the Journal:

each side of the trade is speculating on the direction of an index, called CMBX 6, which tracks the value of 25 commercial-mortgage-backed securities, or CMBS. The index has grabbed investor attention because it has significant exposure to loans made in 2012 to malls that lately have been running into difficulties. Bulls profit when the index rises and shorts make money when it falls.

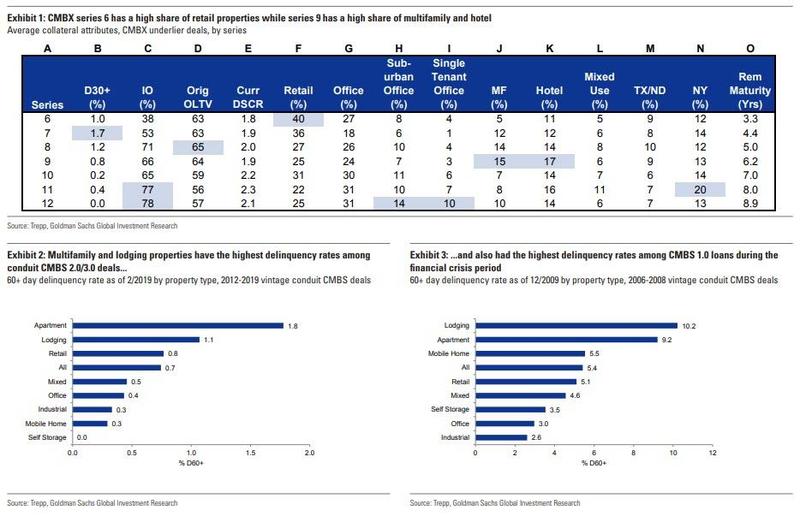

The various CMBX series are shown in the chart below, with the notorious CMBX 6 most notable for its substantial, 40% exposure to retail properties.

One of the firms that had put on the “Big Short 2” trade back in late 2016 was hedge fund Alder Hill Management – an outfit started by protégés of hedge-fund billionaire David Tepper – which ramped up wagers against the mall bonds. Alder Hill joined other traders which in early 2017 bought a net $985 million contracts that targeted the two riskiest types of CMBS.

“These malls are dying, and we see very limited prospect of a turnaround in performance,” said a January 2017 report from Alder Hill, which began shorting the securities. “We expect 2017 to be a tipping point.”

Alas, Alder Hill was wrong, because while the deluge of retail bankruptcies…

… and mall vacancies accelerated since then, hitting an all time high in 2019…

… not only was 2017 not a tipping point, but the trade failed to generate the kinds of desired mass defaults that the shorters were betting on, while the negative carry associated with the short hurt many of those who were hoping for quick riches.

One of them was investing legend Carl Icahn who as we reported last November, emerged as one of the big fans of the “Big Short 2“, although as even he found out, CMBX was a very painful short as it was not reflecting fundamentals, but merely the overall euphoria sweeping the market and record Fed bubble (very much like most other shorts in the past decade). The resulting loss, as we reported last November, was “tens if not hundreds of millions in losses so far” for the storied corporate raider.

That said, while Carl Icahn was far from shutting down his family office because one particular trade has gone against him, this trade put him on a collision course with two of the largest money managers, including Putnam Investments and AllianceBernstein, which for the past few years had a bullish view on malls and had taken the other side of the Big Short/CMBX trade, the WSJ reports. This face-off, in the words of Dan McNamara a principal at the NY-based MP Securitized Credit Partners, was “the biggest battle in the mortgage bond market today” adding that the showdown is the talk of this corner of the bond market, where more than $10 billion of potential profits are at stake on an obscure index.

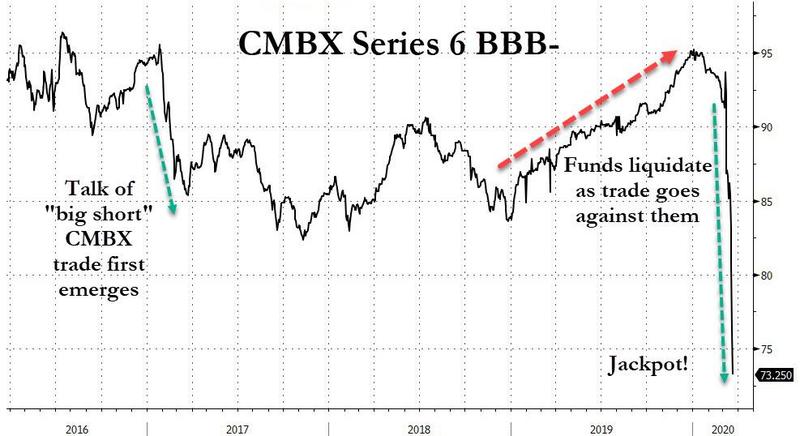

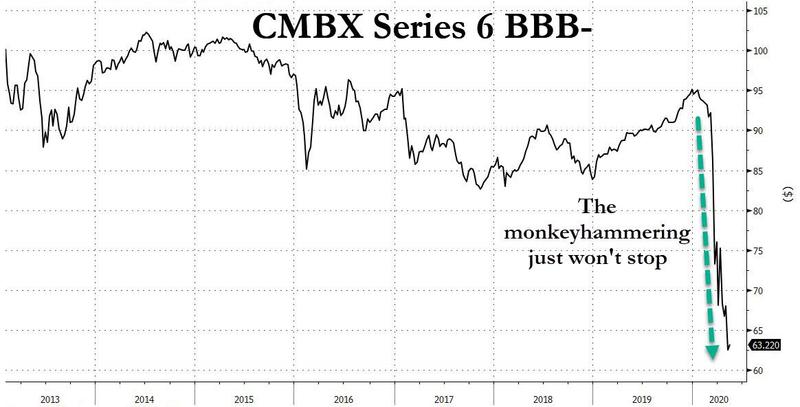

However, as they say, good things come to those who wait, and are willing to shoulder big losses as they wait for a massive payoffs, and for the likes of Carl Icahn, McNamara and others who were short the CMBX, payday arrived in mid-March, just as the market collapsed, hammering the CMBX Series BBB-.

And while the broader market has rebounded since then by a whopping 30%, the trade also known as the “Big Short 2” has continued to collapse and today CMBX 6 hit a new lifetime low of just $62.83, down $10 since our last update on this storied trade several weeks ago.

That, in the parlance of our times, is what traders call a “jackpot.”

Why the continued selling? Because it is no longer just retail outlets and malls: as a result of the Covid lock down, and America’s transition to “Work From Home” and “stay away from all crowded places”, the entire commercial real estate sector is on the verge of collapse, as we reported last week in “A Quarter Of All Outstanding CMBS Debt Is On Verge Of Default“

Sure enough, according to a Bloomberg update, a record 167 CMBS 2.0 loans turned newly delinquent in May even though only 25% of loans have reported remits so far, Morgan Stanley analysts said in a research note Wednesday, triple the April total when 68 loans became delinquent. This suggests delinquencies may rise to 5% in May, and those that are late but still within grace period track at 10% for the second month.

Looking at the carnage in the latest remittance data, and explaining the sharp leg lower in the “Big Short 2” index, Morgan Stanley said that several troubled malls that are a part of CMBX 6 are among the loans that were newly delinquent or transferred to special servicers. Among these:

- Crystal Mall in Waterford, Connecticut, is currently due for the April and May 2020 payments. There has been a marked decline in both occupancy and revenue. This loan accounts for nearly 10% of a CMBS deal called UBSBB 2012-C2

- Louis Joliet Mall in Joliet, Illinois, is also referenced in CMBX 6. The mall was originally anchored by Sears, JC Penney, Carson’s, and Macy’s. The loan is also a part of the CMBS deal UBSBB 2012-C2

- A loan for the Poughkeepsie Galleria in upstate New York was recently transferred to special servicing for imminent monetary default at the borrower’s request. The loan has exposure in two 2012 CMBS deals that are referenced by CMBX 6

- Other troubled mall-chain tenants include GNC, Claire’s, Body Works and Footlocker, according to Datex Property Solutions. These all have significant exposure in CMBX 6.

Of course, the record crash in the CMBX 6 BBB has meant that all those shorts who for years suffered the slings and stones of outrageous margin calls but held on to this “big short”, have not only gotten very rich, but are now getting even richer – this is one case where everyone will admit that Carl Icahn adding another zero to his net worth was fully deserved as he did it using his brain and not some crony central bank pumping the rich with newly printed money – it has also means the pain is just starting for all those “superstar” funds on the other side of the trade who were long CMBX over the past few years, collecting pennies and clipping coupons in front of a P&L mauling steamroller.

One of them is mutual fund giant AllianceBernstein, which has suffered massive paper losses on the trade, amid soaring fears that the coronavirus pandemic is the straw on the camel’s back that will finally cripple US shopping malls whose debt is now expected to default en masse, something which the latest remittance data is confirming with every passing week!

According to the FT, more than two dozen funds managed by AllianceBernstein have sold over $4 billion worth of CMBX protection to the likes of Icahn. One among them is AllianceBernstein’s $29 billion American Income Portfolio, which crashed after written $1.9bn of protection on CMBX 6, while some of the group’s smaller funds have even higher concentrations.

The trade reflected AB’s conviction that American malls are “evolving, not dying,” as the firm put it last October, in a paper entitled “The Real Story Behind the CMBX. 6: Debunking the Next ‘Big Short’” (reader can get some cheap laughs courtesy of Brian Philips, AB’s CRE Credit Research Director, at this link).

Hillariously, that paper quietly “disappeared” from AllianceBernstein’s website, but magically reappeared in late March, shortly after the Financial Times asked about it.

“We definitely still like this,” said Gershon Distenfeld, AllianceBernstein’s co-head of fixed income. “You can expect this will be on the potential list of things we might buy [more of].”

Sure, quadruple down, why not: it appears that there are still greater fools who haven’t redeemed their money.

In addition to AllianceBernstein, another listed property fund, run by Canadian asset management group Brookfield, that is exposed to the wrong side of the CMBX trade recently moved to reassure investors about its financial health. “We continue to enjoy the sponsorship of Brookfield Asset Management,” the group said in a statement, adding that its parent company was “in excellent financial condition should we ever require assistance.”

Alas, if the plunge in CMBX continues, that won’t be the case for long.

Meanwhile, as stunned funds try to make sense of epic portfolio losses, the denials got even louder: execs at AllianceBernstein told FT the paper losses on their CMBX 6 positions reflected outflows of capital from high-yielding assets that investors see as risky. They added that the trade outperformed last year. Well yes, it outperformed last year… but maybe check where it is trading now.

Even if some borrowers ultimately default, CDS owners are not likely to be owed any cash for several years, said Brian Phillips, a senior vice-president at AllianceBernstein.

He believes any liabilities under the insurance will ultimately be smaller than the annual coupon payment the funds receive. “We’re going to continue to get a coupon from Carl Icahn or whoever — I don’t know who’s on the other side,” Phillips added. “And they’re going to keep [paying] that coupon in for many years.”

What can one say here but lol: Brian, buddy, no idea what alternative universe you are living in, but in the world called reality, it’s a second great depression for commercial real estate which due to the coronavirus is facing an outright apocalypse, and not only are malls going to be swept in mass defaults soon, but your fund will likely implode even sooner between unprecedented capital losses and massive redemptions… but you keep “clipping those coupons” we’ll see how far that takes you. As for Uncle Carl who absolutely crushed you – and judging by the ongoing collapse in commercial real estate is crushing you with every passing day – since you will be begging him for a job soon, it’s probably a good idea to go easy on the mocking.

Afterthought: with CMBX 6 now done, keep a close eye on CMBX 9. With its outlier exposure to hotels which have quickly emerged as the most impacted sector from the pandemic, this may well be the next big short.