Summary

- US production remains high due to high-grading, well design, cost efficiencies, and lower oil service contracts.

- High-grading from marginal to core areas can increase per well production from 200% to 500% depending on area, which means one core well can equate to several marginal producers.

- Shorter stages, increased proppant and frac fluids increase production and flatten the depletion curve.

- EOG’s work in Antelope field provides a framework for other operators to increase production while completing fewer wells.

- Few operators are currently developing Mega-fracs, this provides significant upside to US shale production as others start producing more resource per foot.

by Michael Filloon, Split Rock Private Trading and Wealth Management

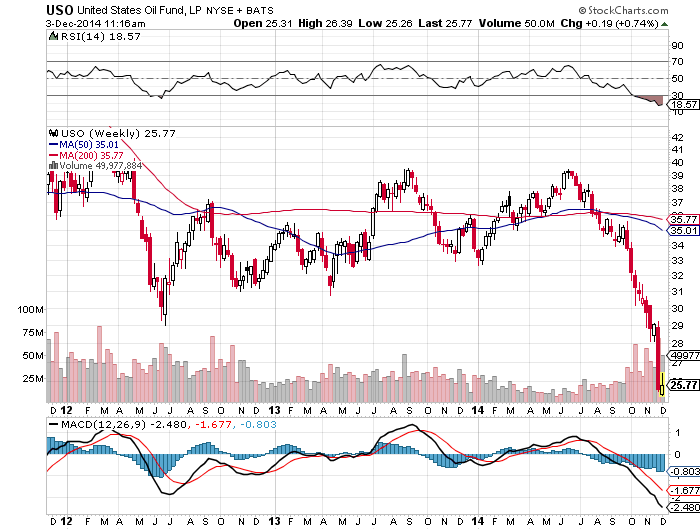

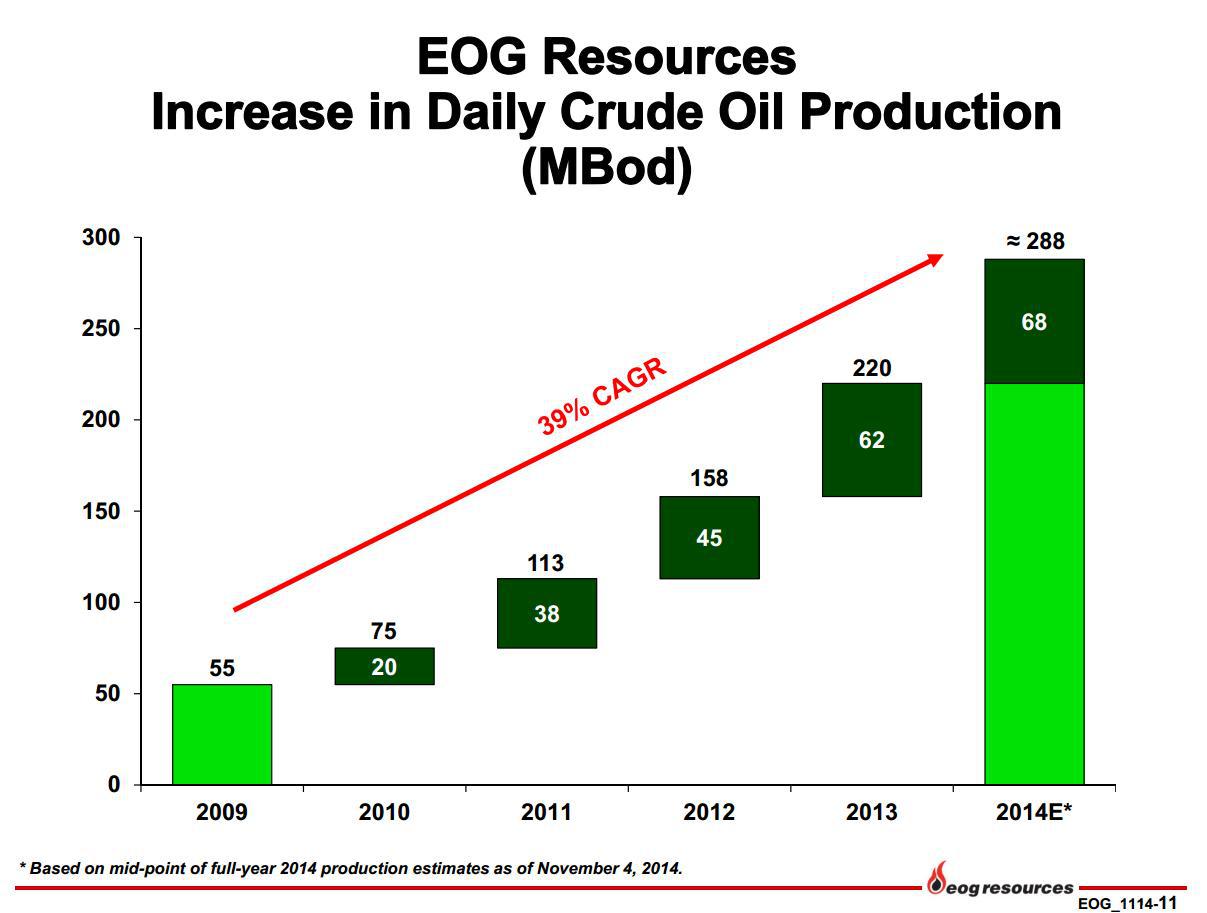

US Oil production remains at volumes seen when WTI was at $100/bbl. Many analysts believed operators couldn’t survive, but $60/bbl may be good enough for operators to drill economic wells. Oil prices have decreased significantly, and the US Oil ETF (NYSEARCA:USO) with it. Many were wrong about US production, and the belief $60/bbl oil would decrease US production. Although completions have been deferred, high-grading and mega-fracs have made up for fewer producing wells. When calculating US production going forward, it is important to account for the number of new completions. If more wells are completed, the higher the influx of production should be. We are finding the quality of geology and well design have a greater effect on total production than originally thought.

(click to enlarge)

(Source: Shaletrader.com)

There are several factors influencing US production. Operators have moved existing rigs to core areas. This decreases its ability getting acreage held by production. In the Bakken, rigs have moved near the Nesson Anticline.

In the Eagle Ford, Karnes seems to be the area of interest. Midland County in the Permian has also been attractive. Operators have decided to complete wells with better geology. When an operator completes wells in core acreage versus marginal leasehold, we see increased production per location. This is just part of the reason US production remains high.

The average investor does not understand the significance. Most think wells have like production, but areas are much different. When oil was at a $100/bbl, it allowed operators to get acreage held by production, although payback times were not as good. Marginal acreage was more attractive, even at lower IRRs. Operators have a significant investment in acreage, and do not want to lose it. Because of this, many would operate in the red expecting future rewards. Just because E&Ps lose money, does not mean the business isn’t economic. It is the way business is done in the short term as oil is an income stream. Wells produce for 35 to 40 years, and once well costs are paid back there are steady revenues. Changes in oil prices have changed this, as now operators will have to focus on better acreage.

Re-fracs are starting to influence production. Although most operators have not begun programs, interest is high. Re-fracs may not be a game changer, but could be an excellent way to increase production at a lower cost. This is not as significant with well designs of today, but older designs left a significant amount of resource. More importantly, when operators began, it was drilling the best acreage. Archaic well designs could leave some stages completely untouched. Current seismic can now identify this, and provide for a better re-frac. We expect to see some very good results in 2016. In conjunction with high-grading, well design continues to be the main reason production has maintained. Changes to well design have been significant, and the resulting production increases much better than anticipated.

No operator is better than EOG Resources (NYSE:EOG) at well design. From the Bakken, to the Eagle Ford and Permian it continues to outperform the competition.

The following map courtesy of ShaleMapsPro.com does a good job of illustrating EOG’s exposure in the Eagle Ford.

(Source: Shalemapspro.com)

EOG’s focusing of frac jobs closer to the well bore has provided for much better source rock stimulation (fraccing). Since more fractures are created, there is a greater void in the shale. This means more producing rock has contact with the well. EOG continues to push more sand and fluids in the attempt to recover more resource per foot. To evaluate production, it must be broken into days over 6 to 12 months. To evaluate well design, locations must be close to one another and by the same operator. This consistency allows us to see advantages to well design changes. Lastly, we compare marginal acreage it is no longer working to the high-grading program. This is how operators are spending less and producing more.

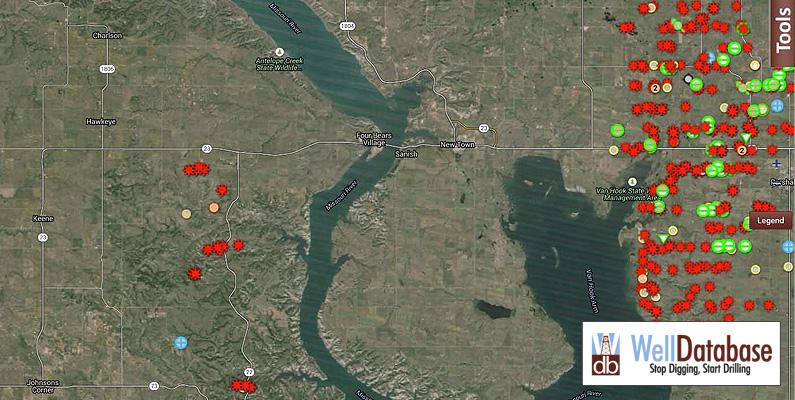

EOG is working in the Antelope field of northeast McKenzie County. This is Bakken core acreage and considered excellent in both the middle Bakken and upper Three Forks.

(click to enlarge)

(Source: Welldatabase.com)

The center of the above map is the location of both its Riverview and Hawkeye wells. These six wells are located in two adjacent sections. The pad is just west of New Town in North Dakota. Riverview 100-3031H was completed in 6/12. It is an upper Three Forks well. 39 stages were used on an approximate 9000 foot lateral. 5.7 million pounds of sand were used with 85000 barrels of fluids.

(click to enlarge)

(Source: Welldatabase.com)

| Date | Oil (BBL) | Gas ((NYSEMKT:MCF)) | BOE |

| 6/1/2012 | 4,384.00 | 3,972.00 | 3972 |

| 7/1/2012 | 27,133.00 | 15,337.00 | 15337 |

| 8/1/2012 | 24,465.00 | 17,223.00 | 17223 |

| 9/1/2012 | 21,457.00 | 9,190.00 | 9190 |

| 10/1/2012 | 18,040.00 | 12,601.00 | 12601 |

| 11/1/2012 | 19,924.00 | 13,366.00 | 13366 |

| 12/1/2012 | 28,134.00 | 22,259.00 | 22259 |

| 1/1/2013 | 15,382.00 | 12,661.00 | 12661 |

| 2/1/2013 | 3,429.00 | 2,451.00 | 2451 |

| 3/1/2013 | 15,242.00 | 22,774.00 | 22774 |

| 4/1/2013 | 15,761.00 | 8,479.00 | 8479 |

| 5/1/2013 | 13,786.00 | 18,372.00 | 18372 |

| 6/1/2013 | 14,485.00 | 18,555.00 | 18555 |

| 7/1/2013 | 15,668.00 | 27,250.00 | 27250 |

| 8/1/2013 | 12,084.00 | 23,876.00 | 23876 |

| 9/1/2013 | 13,841.00 | 46,815.00 | 46815 |

| 10/1/2013 | 11,388.00 | 45,800.00 | 45800 |

| 11/1/2013 | 2,711.00 | 10,533.00 | 10533 |

| 12/1/2013 | 0 | 0 | 0 |

| 1/1/2014 | 5,953.00 | 35 | 35 |

| 2/1/2014 | 11,368.00 | 20,851.00 | 20851 |

| 3/1/2014 | 8,784.00 | 11,179.00 | 11179 |

| 4/1/2014 | 5,607.00 | 8,479.00 | 8479 |

| 5/1/2014 | 4,727.00 | 5,663.00 | 5663 |

| 6/1/2014 | 8,359.00 | 12,726.00 | 12726 |

| 7/1/2014 | 8,799.00 | 22,957.00 | 22957 |

| 8/1/2014 | 7,958.00 | 31,621.00 | 31621 |

| 9/1/2014 | 7,218.00 | 44,318.00 | 44318 |

| 10/1/2014 | 3,778.00 | 14,058.00 | 14058 |

| 11/1/2014 | 3,701.00 | 9,951.00 | 9951 |

| 12/1/2014 | 6,612.00 | 18,435.00 | 18435 |

| 1/1/2015 | 6,181.00 | 24,142.00 | 24142 |

| 2/1/2015 | 3,517.00 | 10,722.00 | 10722 |

| 3/1/2015 | 5,218.00 | 24,175.00 | 24175 |

| 4/1/2015 | 4,275.00 | 24,233.00 | 24233 |

(Source: Welldatabase.com)

Riverview 100-3031H was a progressive well design for 2012. It produced well. To date it has produced 379 thousand bbls of crude and 615 thousand Mcf of natural gas. This equates to $24 million in revenues. Over the first 360 days (using the true number of production days) it produced 240,036 bbls of crude. The month of December 2013, this well was shut in for the completion of an adjacent well. There was a return to production but no significant jump in production from pressure generated by the new locations. This well declined 42% over 12 months. This is much lower than estimates shown through other well models. The next year we see a 35% decline. 10 months later we see an additional decline of approximately 55%. The decline curve of a well is very specific to geology and well design. Keep in mind averages are just that, and do not provide specific data. These averages should not be used to evaluation acreage and operator as there are wide average swings. Also, averages are generally over a long time frame. Production in the Bakken began in 2004 (first horizontal well completed). Wells in 2004 produce nothing like wells today. Updated averages based on year (IP 360) are more useful. Riverview 100-3031H was part of a two well pad. A middle Bakken well was also completed.

Riverview 4-3031H began producing a month after Riverview 100-3031H. It was a 38 stage 9000 foot lateral. 4.3 million lbs of sand were used and 69000 bbls of fluids.

(click to enlarge)

(Source: Welldatabase.com)

The Riverview and Hawkeye wells analyzed in this article were drilled in a southern fashion.

| Date | Oil | Gas | BOE |

| 7/1/2012 | 20,529.00 | 12,537.00 | 12537 |

| 8/1/2012 | 16,553.00 | 16,903.00 | 16903 |

| 9/1/2012 | 17,096.00 | 10,148.00 | 10148 |

| 10/1/2012 | 23,197.00 | 17,914.00 | 17914 |

| 11/1/2012 | 20,122.00 | 14,402.00 | 14402 |

| 12/1/2012 | 27,340.00 | 33,217.00 | 33217 |

| 1/1/2013 | 16,044.00 | 24,394.00 | 24394 |

| 2/1/2013 | 4,267.00 | 4,946.00 | 4946 |

| 3/1/2013 | 27,516.00 | 26,219.00 | 26219 |

| 4/1/2013 | 20,792.00 | 7,940.00 | 7940 |

| 5/1/2013 | 17,516.00 | 35,948.00 | 35948 |

| 6/1/2013 | 15,457.00 | 50,500.00 | 50500 |

| 7/1/2013 | 13,480.00 | 50,807.00 | 50807 |

| 8/1/2013 | 11,254.00 | 42,300.00 | 42300 |

| 9/1/2013 | 9,319.00 | 40,341.00 | 40341 |

| 10/1/2013 | 8,559.00 | 33,116.00 | 33116 |

| 11/1/2013 | 2,190.00 | 40 | 40 |

| 12/1/2013 | 0 | 0 | 0 |

| 1/1/2014 | 1,124.00 | 11 | 11 |

| 2/1/2014 | 5,271.00 | 81 | 81 |

| 3/1/2014 | 8,931.00 | 9,827.00 | 9827 |

| 4/1/2014 | 5,469.00 | 7,940.00 | 7940 |

| 5/1/2014 | 4,807.00 | 5,748.00 | 5748 |

| 6/1/2014 | 8,522.00 | 13,819.00 | 13819 |

| 7/1/2014 | 7,982.00 | 17,983.00 | 17983 |

| 8/1/2014 | 7,169.00 | 26,755.00 | 26755 |

| 9/1/2014 | 5,750.00 | 22,586.00 | 22586 |

| 10/1/2014 | 1,349.00 | 3,194.00 | 3194 |

| 11/1/2014 | 6,495.00 | 15,947.00 | 15947 |

| 12/1/2014 | 6,442.00 | 18,806.00 | 18806 |

| 1/1/2015 | 5,840.00 | 22,126.00 | 22126 |

| 2/1/2015 | 4,171.00 | 18,682.00 | 18682 |

| 3/1/2015 | 4,221.00 | 18,539.00 | 18539 |

| 4/1/2015 | 3,878.00 | 19,725.00 | 19725 |

(Source: Welldatabase.com)

Riverview 4-3031H has produced 361 thousand bbls of crude and 657 thousand Mcf of natural gas. It under produced Riverview 100-3031H, but this is consistent with well design. 360 day production totaled 237,735 bbls of oil. We do not know if the Three Forks is a better pay zone than the middle Bakken as the well design was not consistent. Most operators have reported better results from the middle Bakken. The Three Forks well used one more stage (less feet per stage should mean better fracturing). It also used significantly more sand and fluids. Either way both wells were good results. Riverview 4-3031H only declined approximately 36% in a comparison of the first month to month 12. This was 7% better than 100-3031H. It declined another 41% in year two on a month to month comparison. This was 6% greater. 56% was seen when compared to adjusted production for 5/15. The Three Forks well declines slower in later production than 4-3031H. This may be due to well design. The well with more stages, proppant and fluids continues to out produce the Bakken well. It is possible the source rock is better. There are many other variables to look at, but this data provides why EOG continues to push ahead with more complex locations.

In September of 2012, EOG drilled its next well in this area. Hawkeye 100-2501H is a 13700 foot lateral targeting the upper Three Forks. It is a 47 stage frac. 14 million pounds of sand were used with 158000 bbls of fluids.

(click to enlarge)

(Source: Welldatabase.com)

Of the three pads, this well is located in the center. It was an interesting design, given the length of the lateral.

| Date | Oil | Gas | BOE |

| 9/1/2012 | 21,959.00 | 444 | 444 |

| 10/1/2012 | 54,927.00 | 155 | 155 |

| 11/1/2012 | 47,557.00 | 57,300.00 | 57300 |

| 12/1/2012 | 55,367.00 | 92,144.00 | 92144 |

| 1/1/2013 | 33,396.00 | 55,877.00 | 55877 |

| 2/1/2013 | 22,100.00 | 32,810.00 | 32810 |

| 3/1/2013 | 36,631.00 | 57,544.00 | 57544 |

| 4/1/2013 | 29,075.00 | 32,696.00 | 32696 |

| 5/1/2013 | 22,210.00 | 33,351.00 | 33351 |

| 6/1/2013 | 17,544.00 | 25,794.00 | 25794 |

| 7/1/2013 | 15,872.00 | 23,600.00 | 23600 |

| 8/1/2013 | 19,647.00 | 28,746.00 | 28746 |

| 9/1/2013 | 15,486.00 | 22,352.00 | 22352 |

| 10/1/2013 | 21,325.00 | 31,678.00 | 31678 |

| 11/1/2013 | 6,418.00 | 9,214.00 | 9214 |

| 12/1/2013 | 0 | 0 | 0 |

| 1/1/2014 | 0 | 0 | 0 |

| 2/1/2014 | 0 | 0 | 0 |

| 3/1/2014 | 29,699.00 | 23,822.00 | 23822 |

| 4/1/2014 | 39,782.00 | 32,696.00 | 32696 |

| 5/1/2014 | 35,267.00 | 61,543.00 | 61543 |

| 6/1/2014 | 27,554.00 | 49,551.00 | 49551 |

| 7/1/2014 | 7,229.00 | 12,565.00 | 12565 |

| 8/1/2014 | 31,155.00 | 98,086.00 | 98086 |

| 9/1/2014 | 12,617.00 | 32,742.00 | 32742 |

| 10/1/2014 | 2 | 4 | 4 |

| 11/1/2014 | 7,769.00 | 15,996.00 | 15996 |

| 12/1/2014 | 15,487.00 | 49,147.00 | 49147 |

| 1/1/2015 | 4,427.00 | 9,918.00 | 9918 |

| 2/1/2015 | 9,344.00 | 20,654.00 | 20654 |

| 3/1/2015 | 8,459.00 | 25,171.00 | 25171 |

| 4/1/2015 | 7,235.00 | 24,752.00 | 24752 |

(Source: Welldatabase.com)

Hawkeye 100-2501H had some excellent early production numbers. From that perspective, it is one of the best wells to date in the Bakken. It has already produced 655,000 bbls of crude and 960,000 Mcf of natural gas. It has revenues in excess of $42 million to date. This includes roughly four non-producing or unproductive months. Crude production over the first 360 days was 389,835 bbls. Over the first 12 months, this well produced crude revenues in excess of $23 million. Decline rates were higher, as the first full month of production declined 65% over the first year. This isn’t important as early production rates were some of the highest seen in North Dakota. It is important to note, decline rates are emphasized but higher pressured wells may deplete faster depending on choke and how quickly production is propelled up and out of the wellbore. Any well that produces very well initially will have higher decline rates, but this does not lessen the value of the well. This specific well is depleting faster, but no one is complaining about payback times well under a year. Decline rates decrease significantly in year two at 11%. This well saw a marked increase in production when adjacent wells were turned to sales. The additional pressure associated with well communication increased production from 20,000 bbls/month to 35,000 bbls/month on average. This occurred over a 6 month period.

(click to enlarge)

(Source: Welldatabase.com)

Hawkeye 102-2501H was the fourth completion. This 14,000 foot 62 stage lateral targeted the upper Three Forks. It used 14.5 million pounds of sand and 164,000 bbls of fluids.

| Date | Oil | Gas | BOE |

| 1/1/2013 | 18,486.00 | 41 | 41 |

| 2/1/2013 | 27,120.00 | 8,705.00 | 8705 |

| 3/1/2013 | 39,702.00 | 15,748.00 | 15748 |

| 4/1/2013 | 17,714.00 | 30,501.00 | 30501 |

| 5/1/2013 | 41,368.00 | 57,489.00 | 57489 |

| 6/1/2013 | 26,602.00 | 34,399.00 | 34399 |

| 7/1/2013 | 0 | 0 | 0 |

| 8/1/2013 | 133 | 0 | 0 |

| 9/1/2013 | 0 | 0 | 0 |

| 10/1/2013 | 0 | 0 | 0 |

| 11/1/2013 | 0 | 0 | 0 |

| 12/1/2013 | 0 | 0 | 0 |

| 1/1/2014 | 5,163.00 | 6,403.00 | 6403 |

| 2/1/2014 | 41,917.00 | 74,353.00 | 74353 |

| 3/1/2014 | 36,439.00 | 18,111.00 | 18111 |

| 4/1/2014 | 19,477.00 | 30,501.00 | 30501 |

| 5/1/2014 | 26,388.00 | 43,071.00 | 43071 |

| 6/1/2014 | 27,480.00 | 49,456.00 | 49456 |

| 7/1/2014 | 14,529.00 | 33,072.00 | 33072 |

| 8/1/2014 | 24,542.00 | 62,753.00 | 62753 |

| 9/1/2014 | 17,613.00 | 53,460.00 | 53460 |

| 10/1/2014 | 17,451.00 | 66,544.00 | 66544 |

| 11/1/2014 | 9,634.00 | 33,366.00 | 33366 |

| 12/1/2014 | 16,338.00 | 76,547.00 | 76547 |

| 1/1/2015 | 11,450.00 | 65,277.00 | 65277 |

| 2/1/2015 | 8,971.00 | 50,919.00 | 50919 |

| 3/1/2015 | 3,177.00 | 14,820.00 | 14820 |

| 4/1/2015 | 6,495.00 | 13,616.00 | 13616 |

(Source: Welldatabase.com)

It has produced 458,000 bbls of crude and 839,000 Mcf to date. This equates to roughly $30 million over well life. 360 day production was 394,673 bbls of crude. Production was interesting as initial production was outstanding. The big production numbers were hindered as many of the early months had missed production days. We don’t know if there were production problems, but do know the well was shut when adjacent wells were turned to sales. Production was over 1000 bbls/d over the first six months. It was shut in for another six months. After this production jumped, but this is misleading. Given the fewer days of production per month, there wasn’t much of an increase when the new wells were turned to sales. The decline over the first year on a monthly basis is 20%. The second year is much greater at 80%. We have seen recent production decrease significantly, and is something to watch. Lower decline rates initially are more important. This is because production rates are higher. It equates to greater total production.

Hawkeye 01-2501H was completed in January of 2013.

(click to enlarge)

(Source: Welldatabase.com)

It is a 64 stage, 15000 foot lateral targeting the middle Bakken. This well used 172,000 bbls of fluids and 15 million pounds of sand.

| Date | Oil | Gas | BOE |

| 1/1/2013 | 18,792.00 | 43 | 43 |

| 2/1/2013 | 30,211.00 | 13,879.00 | 13879 |

| 3/1/2013 | 42,037.00 | 17,648.00 | 17648 |

| 4/1/2013 | 17,433.00 | 36,881.00 | 36881 |

| 5/1/2013 | 38,754.00 | 63,501.00 | 63501 |

| 6/1/2013 | 28,602.00 | 48,817.00 | 48817 |

| 7/1/2013 | 0 | 0 | 0 |

| 8/1/2013 | 134 | 1 | 1 |

| 9/1/2013 | 0 | 0 | 0 |

| 10/1/2013 | 0 | 0 | 0 |

| 11/1/2013 | 0 | 0 | 0 |

| 12/1/2013 | 0 | 0 | 0 |

| 1/1/2014 | 6,311.00 | 7,186.00 | 7186 |

| 2/1/2014 | 43,713.00 | 74,099.00 | 74099 |

| 3/1/2014 | 39,156.00 | 18,492.00 | 18492 |

| 4/1/2014 | 23,408.00 | 36,881.00 | 36881 |

| 5/1/2014 | 21,681.00 | 33,498.00 | 33498 |

| 6/1/2014 | 28,502.00 | 51,543.00 | 51543 |

| 7/1/2014 | 18,795.00 | 45,017.00 | 45017 |

| 8/1/2014 | 25,512.00 | 58,837.00 | 58837 |

| 9/1/2014 | 20,522.00 | 60,662.00 | 60662 |

| 10/1/2014 | 19,137.00 | 68,576.00 | 68576 |

| 11/1/2014 | 12,093.00 | 37,043.00 | 37043 |

| 12/1/2014 | 16,587.00 | 45,980.00 | 45980 |

| 1/1/2015 | 14,246.00 | 62,819.00 | 62819 |

| 2/1/2015 | 9,220.00 | 35,931.00 | 35931 |

| 3/1/2015 | 3,617.00 | 6,634.00 | 6634 |

| 4/1/2015 | 13,702.00 | 42,551.00 | 42551 |

(Source: Welldatabase.com)

It has produced 492,170 bbls of crude and 866,520 Mcf of natural gas. 360 day production was 412,072 bbls of oil.

(click to enlarge)

(Source: Welldatabase.com)

This is an excellent well, but the location of focus is Hawkeye 02-2501H. It was completed last in this group. This well provides the link between changes in well design to production improvements.

| Date | Oil | Gas | BOE |

| 12/1/2013 | 3,022.00 | 6,533.00 | 6533 |

| 1/1/2014 | 37,385.00 | 75,940.00 | 75940 |

| 2/1/2014 | 30,066.00 | 58,949.00 | 58949 |

| 3/1/2014 | 22,876.00 | 50,690.00 | 50690 |

| 4/1/2014 | 26,703.00 | 43,926.00 | 43926 |

| 5/1/2014 | 31,987.00 | 55,124.00 | 55124 |

| 6/1/2014 | 27,777.00 | 47,166.00 | 47166 |

| 7/1/2014 | 31,500.00 | 50,279.00 | 50279 |

| 8/1/2014 | 51,709.00 | 99,583.00 | 99583 |

| 9/1/2014 | 43,292.00 | 98,069.00 | 98069 |

| 10/1/2014 | 40,143.00 | 98,927.00 | 98927 |

| 11/1/2014 | 24,064.00 | 50,495.00 | 50495 |

| 12/1/2014 | 31,488.00 | 99,684.00 | 99684 |

| 1/1/2015 | 27,087.00 | 94,621.00 | 94621 |

| 2/1/2015 | 22,207.00 | 94,490.00 | 94490 |

| 3/1/2015 | 22,590.00 | 125,634.00 | 125634 |

| 4/1/2015 | 17,707.00 | 94,910.00 | 94910 |

(Source: Welldatabase.com)

The production numbers are significant. In less than a year and a half, it has produced 490,000 bbls of crude and 1.25 Bcf of natural gas. Revenues to date are $33.2 million. Its 360 day crude production was 427,663 bbls. The production is impressive but the decline curve is more important. This Hawkeye well has a steady production rate with only a slight decline. This is where the analysts may be getting it wrong, as decline curves change significantly by area and well design. What EOG has done is not only increased production significantly, but also flattened the curve. Initial production is interesting as we don’t see peak production until nine months. This means our best month is August of 2014, and not the first full month. When we analyze the production after one full year of production, there is no drop off.

This 12800 foot 69 stage lateral is a very good middle Bakken design. EOG decided to pull back some of the lateral length. There are several possible reasons for this. We think it is possible EOG has discovered it was having difficulty in getting proppant to the toe of the well. But this is why operators test the length. More importantly, the increase in stages in conjunction with a shorter lateral provides for shorter stages. This means the operator will probably do a better job of stimulating the source rock. This well also used massive volumes of fluids and sand. 460,000 bbls of fluids were used with over 27 million lbs of proppant. I don’t normally break down the types of sand, as it can be trivial to some but in this case I have as the design seems somewhat unique. This well used approximately 16 million lbs of 100 mesh sand, 7 million lbs of 30/70 and 4 million 40/70. The large volumes of mesh sand are interesting. It would seem EOG is trying to push the finest sand deep into the fractures to maintain deeper shale production.

| Well | Date | Lateral Ft. | Stages | Proppant Lbs. | Fluids Bbls. | 12 mo. Oil Production Bbls. | Production/Ft. |

| Riverview 100-3031H | 6/12 | 9,000 | 39 | 5.7M | 85,000 | 240,036 | 26.67 |

| Riverview 4-3031H | 7/12 | 9,000 | 38 | 4.3M | 69,000 | 237,735 | 26.42 |

| Hawkeye 100-2501H | 9/12 | 13,700 | 47 | 14M | 158,000 | 389,835 | 28.46 |

| Hawkeye 102-2501H | 1/13 | 14,000 | 62 | 14.5M | 164,000 | 394,673 | 28.19 |

| Hawkeye 01-2501H | 1/13 | 15,000 | 64 | 15M | 172,000 | 412,072 | 27.47 |

| Hawkeye 02-2501H | 12/13 | 12,800 | 69 | 27M | 460,000 | 427,663 | 33.41 |

I completed the above table for several reasons. The first was to show well design’s effect on one year total production. We used 360 days as a base. We didn’t use 12 months as that will skew data, as some wells don’t produce every day of every month. Wells are shut in for service or more importantly when new production from adjacent locations are turned to sales. So these are a specific number of days and not estimates. We also broke down production per foot of lateral. This may be more important than any other factor. Production per well is important, but lateral length is a key as it shows how well the source rock was stimulated. In reality, production per foot matters more at longer lateral lengths. Many operators don’t like to do laterals longer than 10,000 feet, as production per foot decreases sharply. When looking at well production data, it is obvious that production per foot suffers as the toe of the lateral gets farther from the vertical.

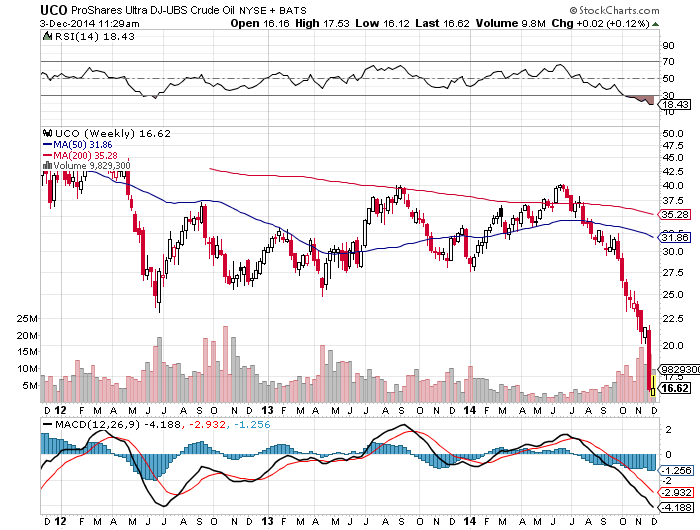

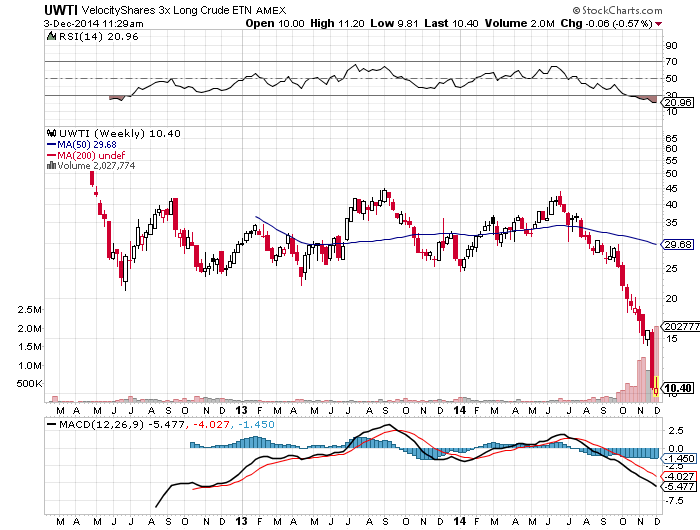

There are several other ETFs that focus on U.S. and world crude prices:

- iPath S&P Crude Oil Total Return Index ETN (NYSEARCA:OIL)

- ProShares Ultra Bloomberg Crude Oil ETF (NYSEARCA:UCO)

- VelocityShares 3x Long Crude Oil ETN (NYSEARCA:UWTI)

- ProShares Ultrashort Bloomberg Crude Oil ETF (NYSEARCA:SCO)

- U.S. Brent Oil ETF (NYSEARCA:BNO)

- PowerShares DB Oil ETF (NYSEARCA:DBO)

- VelocityShares 3x Inverse Crude Oil ETN (NYSEARCA:DWTI)

- PowerShares DB Crude Oil Double Short ETN (NYSEARCA:DTO)

- U.S. 12 Month Oil ETF (NYSEARCA:USL)

- U.S. Short Oil ETF (NYSEARCA:DNO)

- PowerShares DB Crude Oil Long ETN (NYSEARCA:OLO)

- PowerShares DB Crude Oil Short ETN (NYSEARCA:SZO)

- iPath Pure Beta Crude Oil ETN (NYSEARCA:OLEM)

All six wells had fantastic results. The first two Riverview wells are still considered sand heavy fracs and produced almost a quarter of a million barrels of oil. This does not include natural gas in the estimates, but EURs for these wells are approximately 1200 MBo. We don’t put much emphasis on EURs other than an indicator of how good production is in comparison. Since locations will produce from 35 to 40 years, we are more inclined to emphasize one year production. Although the Hawkeye wells drilled on 9/12 and 1/13 didn’t show a large uptick in production per foot, it is still quite impressive considering the lateral length. Overall production uplift was exceptional, and these wells produce decent payback times at current oil price realizations.

There is no doubt this area has superior geology. It is definitely a core area, but may not be as good as Parshall field. Because of this, we know other areas would not produce as well, but still it provides a decent comparison for the upside to well design. Geology is still key and this is probably why EOG recently drilled a 15 well pad in the same general area. These wells are still in confidential status, so we do not know the outcome. Given the results in this area, these wells could be very interesting. The most important reason to focus on these Mega-Fracs is repeatability. If EOG can do this, so can other operators. Our expectations are many operators will be able to complete wells this good within the next 12 to 24 months. If this occurs we could see production maintained at much lower prices and fewer completions.

The reason oil stayed as high as it did was the fact that India and China subsidized it. The fact that China passed the US in imports misses the point. China uses 36mm boe in coal every year. They manufacture 700 million tons of steel versus 40 in the US. This is due largely to $5 trillion in QE. In the process of this absurd borrowing, they have wiped out most of their neighbors.

Earnest and Young estimates that there is 300 million tons of excess steel capacity in the world and China is STILL building new capacity. That 300 million tons is assuming China continues to use 640 million tons internally. Once countries start to protect their steel producers, China is going to collapse. Steel requires 11 BOE of energy per ton. 300 million tons is the equivalent of 10 million BOE of energy per day. If there’s a recession, you could see total energy use drop by 15-20 million BOE per day.

Demand isn’t what people want, demand is what they can pay for. Once the wold starts defaulting on this junk corporate debt, petroleum demand is going to collapse. The last time we went through a shock like this was 1982 and 6 million BPD of demand came of the market. This one is going to be far far worse. You could easily see oil go to $50 and stay there for a decade. According to Evans-Ambrose Prichard, Jim Chanos and Kyle Bass, China is going to collapse.

” The recovery of the oil price will be much quicker than the recovery of the real estate sector, given that this slump of the oil price has been driven by lame thinking, arbitrary speculation and sentiment, while having nothing to do with evaporating geopolitical risks around the world or a material deterioration of the global supply-demand fundamentals”.

and this one:

” In fact, the rapid decline has already started. First, the Energy Information Administration said yesterday U.S. crude-oil supplies declined 3.7 million barrels on the week ended Nov. 28. Analysts surveyed by Platts had expected crude inventories to increase by 380,000 barrels on the week.

According also to today’s news from Seeking Alpha, new permits, which outline what drilling rigs will be doing 60-90 days in the future, showed heavy declines for the first time this year across the top three U.S. onshore fields: the Permian Basin, Eagle Ford and Bakken shale. Specifically, there is an almost 40% decline in new well permits issued across the U.S. in November 2014, with only 4,520 new well permits approved last month, down from 7,227 in October 2014. “

I did not actually expect such big declines so soon. Both declines really surprised me. How long can an investor remain in denial?

“China is going to collapse.”

People have been saying that for around, well, forever.

How many people world-wide have been sitting on the proverbial sidelines at $100+ oil? Waiting to start or expand a biz. Waiting to buy a car?

All of a sudden, poof, 40% off on the COGS!

Possibly a big demand shock coming.

Answer: None.

Most people (Americans) can’t even tell you who Ben Franklin was, much less tell you the price of oil.

They can’t even remember how much their last tattoo cost them, or their boyfriend.

Nonetheless, I don’t buy some of the talk I’m reading on the internet that “the US shale drillers will keep right on going with oil at $65”. That idea is just totally ridiculous. The operating cash flow generated by US shale producers will decline dramatically if oil stays below $80 and they won’t be able to raise nearly as much capital because of lower stock prices and substantially higher yields required to sell bonds. So US shale drillers will be forced to cut back on drilling activity because of a simple lack of capital and cash flow to pay for horizontal drilling, which is expensive. This big drop in drilling activity, which will happen for sure if oil stays below $80, should cause US oil production growth to drop sharply in the first half of next year and that drop will probably cause the oil market to correct back up into the 80s by the second half of next year.

I’ve been surprised that the Saudis have been willing to let oil prices fall all the way below $70. I’m starting to wonder if anyone really knows what oil price they need to balance their national budget. Same thing with the Russians–it’s difficult to get good credible information from the Middle East, South America, and Russia about national budgets and other subjects like what kind of oil production technology they’re using today and what their marginal cost of production is today. Do Wall Street analysts and those sleepy international agencies in Europe really know what’s going on in the Middle East and Russia? I’m starting to wonder.

Thank you for your compliments. The huge divergence between the reality and the market perception is more than apparent in the oil markets now.

The geopolitical risks have worsened compared to 2013 and H1 2014, the GDP growth rates in 2014 are at or above expectations in the world’s largest oil consumers compared to 2013, while the crude inventories and the new permits have already started to drop rapidly. We talk for a 40% decline here.

To me, this is the definition of: THEATER OF THE ABSURD.

Let’s see how long this THEATER OF THE ABSURD will go on.

Regards,

VD

Thank you for your compliments. As mentioned above, what is going on now in the oil markets is the definition of the: THEATER OF THE ABSURD.

Let’s see how long the oil bears will keep behaving in this irrational manner trying to make money at the bottom although the facts are not there.

Regards,

VD

Re: “I don’t buy some of the talk I’m reading on the internet that “the US shale drillers will keep right on going with oil at $65″. That idea is just totally ridiculous. The operating cash flow generated by US shale producers will decline dramatically if oil stays below $80 and they won’t be able to raise nearly as much capital because of lower stock prices and substantially higher yields required to sell bonds”

If oil price keeps going down, and I’m a shale driller with sunk cost already, wouldn’t I want to try to keep pumping MUCH, MUCH more first to try to keep my fixed costs even lower, to try my best to survive, before the inevitable happens? In other words, I think we might just be seeing the beginning of the price fall … sure, 6-12 months down the road, we’ll see some real bust happening (not all producers have enough liquidity to last 6-12 months), but the time from today to the next 3-6 months could be really painful for longs … before they cut production, I think, they’ll try to produce a heck of a lot more to try to survive, before the financial constraints starts to work – remember, financials have many avenues, some will still pump more, borrow from banks to suvive, etc. i.e. we could be looking at 6-12 months pain before recovery, before the banks finally say enough is enough, before capital markets starts to rate the bonds as junk, etc. These process could last a long time, and until then, we might be seeing continued increased weekly production which will keep depressing crude oil prices …

Originally, I plan to go long on crude oil stocks, but I’m now thinking of holding back my longs until I see a real bottom in prices. I like to see US production slows down for 2 to 3 weeks in a row, and right now, we are just not seeing this happening at all – US producers keep producing more oil every week, and with Saudis not cutting down, the supply of oil on a weekly basis keeps going up, and prices inevitably must come down … I have a feeling, $65 will not be the immediate bottom yet … but let’s see …

I do think there is a temporary glut of supply that triggered the decline, coupled with the obligatory unwinding of long positions…crude prices may capitulate further, but they won’t stay down for long. The tricky part is staying patient and waiting for a tradeable bottom, and separating the long term winners from the ones with excess leverage and poor fundamentals. We know the hedge funds are herd animals so expect more piling on of short positions to drive crude lower.

I am getting sick when I see how quickly all these highly paid “gurus” change their mind depending on which way the wind blows, while ignoring the facts. And they behave like parrots repeating the words and imitating the actions of another.

This is why, I felt the need to write this factual article that clearly demonstrates what these “gurus” were telling us in 2013 and H1 2014, and what could drive prices at $150/bbl.

Also, separating the wheat from the chaff is something that ALL the investors must do now. They must NOT make the mistake to load the heavily indebted energy companies because it will be a “dead cat bounce”, if these companies ever bounce back.

Regards,

VD

I greatly value your research, time and effort put into you articles.

However, timing is everything. This piece feels desperate. I have read a lot of details on the subject of late and there were many signs of this slump in prices coming that were not accounted for by those who only see oil prices as going up.

Prices go up and they go down. I don’t see the compelling evidence that it will suddenly go up soon.

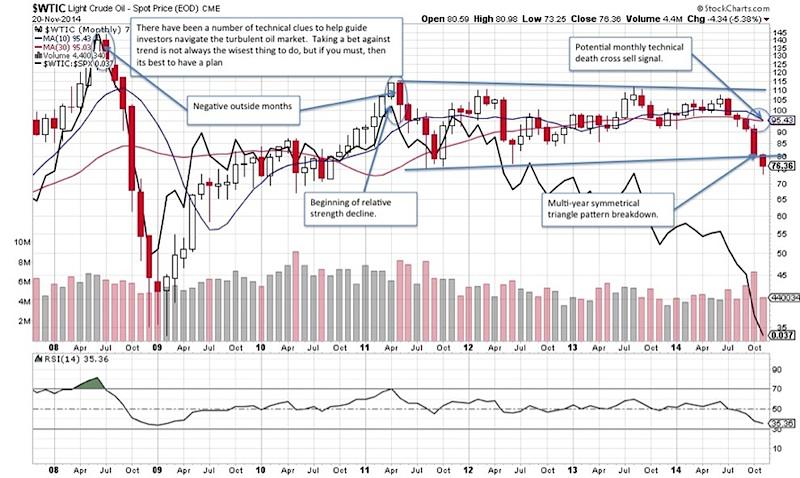

Just pull up the price charts of crude oil over the past 20 years.

You’ll see this current price drop is the 2nd longest drop over that period.

The only time when crude had a bigger drop was back in 2008, from a peak of $147, down to a low of $33, near the 200 month MA. Today, we are near the 200 month MA as well which is currently around $60-$65 … we can’t time it precisely, but over the next few months, I feel we are close to the current bottom, and it makes sense to pick good quality issues relating to crude oil, and slowly work your way inside. Never go on margin, this is really Value Investing at its finest, and if you are not scared, you are not doing Value Investing properly – I won’t bat an eyelid if the purchases made this week drops by 50% more at the bottom, because history has shown that they will rise much, much more. I’m looking at +100% gains over the next 1-3 years at the least …

Demand for oil in the six segments that simply cannot stop are impervious to economic slowdown (plastics, oceangoing freight, train freight, fertilizer, aviation, modern armies). Regardless of consumer slowdowns, these six segments represent 80% of oil and net gas consumed around the world. When economies slow down, the food, freight, aviation and military segments do not, they continue on. A recession in Europe or China would only slow the rise in demand, not reverse it. Look at the demand trend of the past year and understand that even if demand only rises at one half the slope is has followed from 2004 until now, it will still outstrip current expected global production for Q1 2015. Oil price strip is highly elastic to tiny percentage changes in the supply-demand balance. Current situation is creating the coiled spring and that coiled spring WILL unwind before the end of 2015.

We just hope it is a measured controlled unwind throughout the year, otherwise we will have the $140 spike we saw in 2008 for a month or two before settling down to something in the $90 – $100 brent range.

Set your DCF and NAV models for $90 brent / $85 WTI. This is going to get ugly before the weather gets cold again in 2015. I’m willing to go out on a limb and say you can quote me on this one.

Here is the reality when Brent is $70/bbl for more than one or two months…

1. Venezuela is cash flow negative and cannot make coupon payments on its foreign debt. Venezuela WILL default on its debt before end of 2015 in this price regime.

2. Iran cannot feed its army at this price. The mullahs depend on the support of their army to maintain power. Kicking this leg out from under the government stool makes their continued existence precarious. Martial law kind of precarious.

3. The government in Tripoli cannot feed their guard at these prices. If the government in Tripoli cannot do this, they cannot protect the pipes that carry crude to their northern port. When that happens the other government in the west breaks through and shuts the pipe down to prevent revenue from reaching the Tripoli government and thereby trying to strangle it. 800,000 bbl/day go off stream.

4. Saudi Arabia is burning $2b/month from their sovereign wealth fund. At that burn rate, the ENTIRE sovereign wealth fund runs dry in 60 months. They need to turn the boat around long before that happens because if they burn through more than about 25% of it, angry men with beards and automatic rifles start to hang around the palace gates. Not a stable internal situation. Riyadh has made major financial promises to its citizens in return for peace and their support. And in Saudi Arabia, the citizens do not have peaceful protest marches when they are aggrieved.

5. Russia is burning $2.5b/month form their sovereign wealth fund. At that burn rate, the ENTIRE sovereign wealth fund runs dry in 48 months. They will tighten their belts, suffer, freeze, grit their teeth and tough it out. BUT! (and this is a big one) understand that at the back of the mind of every strategist in the Kremlin is the nagging thought that all they have to do to cause a global geopolitical crisis and force the price of energy to whipsaw back up to $100/bbl in the course of a week is to kick the hornets nest: Roll the tanks into Donetsk and Lukhansk. Overnight crisis and EU buckles because it is now winter and Germany will freeze without the Ukrainian transit gas (Nordstream can only supply about one third of what Europe needs to stay warm).

6. I can’t even begin to fathom what the dynamics going on in Syria / Iraq are right now, but it can’t be good. I’m sure Baghdad had to guarantee Kurdistan a minimum cut in the negotiation to let them export. Well, either Baghdad or Kurdistan is not going to get that minimum cut agreed in that negotiation. How do you think things are panning out in their relations now?

This situation has the makings of a new Arab Spring / Cold War settling in… and it cannot remain in equilibrium for a whole 12 months.

Thank you for your comment. But, my article is full of facts as always. If you disagree with the facts, it is your choice.

Regards,

VD

Thank you for your compliments. Good luck with your investments.

Regards,

VD

Oil Bears and Analysts are driving the oil price down with their unrealistic attitude towards:

a) Negative growth;

b) India’s energy appetite; and

c) The fallacy of Nirvana in the Middle East.

Not to mention that Pick-Ups and large SUVs are back in vogue in North America…

I also believe that Putin will rattle his sabre and agitate conflict somewhere, to raise uncertainty and thus prices – if the drought in Oil prices remains lower much longer. After all, the fall in the price of crude in the mid 80’s (and Reagan) brought the USSR to its knees. He will not repeat that. Guaranteed.

Waiting for a firm bottom – then backing up the truck for more PTA.

No one will know the absolute bottom, at the “Hard Right Edge” of the charts. Bottoms are only know once some time are passed, and by then, you won’t be able to buy at the bottom price. That’s the reality of prices. The key is Money Management – always make sure to have enough cash to buy at lower prices when bargains avails themselves. For highly cyclical stocks, a rough yardstick is 75% fall in prices from the peak for decent names. E.g. SDRL is one that I think could be interesting – peak price was $48 in 2013, and is now trading near $12, or 75% fall. I would allocate around 4% of my portfolio to this, to be split into 4 bullets, and have actually deployed first bullet at $13.50. I’ll be looking for a final buy price of around $7 (approximately 50% fall from my first entry), and these types of buys are just put into the drawer and forget. When the drawer is opened in 1-3 year’s time, you will most likely earn anywhere from 50% to 100% gains or more.

Meanwhile, have the stomach to see the value of what you bought dropped by 50% from what you purchased. Don’t ever think about selling then, because the Reward to Risk of holding is much, much better.

And diversify into 3 issues at the very least, so that total exposure to crude oil is no more than say 12% trading capital. I am just very cautious, but of course, at the very bottom, for the 4th buy, you could double or triple the buy size and raise the 12% up to say 15%-20% capital … but these type of substantial increase must show capitulation, i.e. big price drops with big volumes …. (SDRL has shown the first capitulation last week and this week, and usually, there’s more than 1 capitulation). And if you are a nimble trader, you would also consider adding on the way up, e.g. when Weekly RSI(14) crossed above 20 and Daily RSI(14) dropped back down to around 30-40 or so ie. dipping on the way up, if you are worried that you only have 3% capital in this during the bottom.

PS. SDRL falls into my screen, because at $13.50, it is trading at NAV, and well below Replacement Cost. So, if it falls to $7, that would be trading at 50% NAV approximately, and is good enough for me.

Thank you for your compliments. Also, good luck with PTA (Petroamerica Oil) which is debt free with a pristine balance sheet, as shown in my previous articles.

Regards,

VD

Warren Buffett has said more than once that he has NEVER managed to buy at the bottom and sell at the top. Nevertheless, he is a billionaire.

Regards,

VD

– more and more suppliers will go out of business or reduce supply

– consumption and hence demand will rise if oil is that cheap.

There are a lot of factors at play as you well demonstrated – geopolitical, GDP growth, but also competing energy sources (and I’m not talking nuclear fission, but renewables). But the overriding factors appear to be speculation and herd behaviour. And we all know they can only go for so long into one direction.

Thank you for your compliments.

Regards,

VD

Also, not all shale formations are so thin as to horizontally support only single laterals. Some, like the Wolfcamp, are very thick, and the first wells drilled are really only the first of many stacked laterals.

Back to innovation and knowledge, that is not limited to shale plays, either. Not all of the new oil production is shale production. At least some if not much of it is from new horizontal development of non-shale assets. For example, look at the Spraberry in W TX.

Also, the shale wells that are drilled and produced typically hold under the leases of unsophisticated lessors other zones that have not yet been tapped.

There is more to be squeezed out of these formations than most people realize, and with advances in cost savings along the way, there still remains quite a bit of money to be made.

If it is “not fully understood” then you cannot say anything about future shale production. Currently, the author is correct. Until production is realized, such as current retrievable shale oil, for investment purposes, it doesn’t exist.

What it is going to take to send men to Mars is not fully understood, either. But that does not mean that we cannot say anything about sending men to Mars at some point in the future.

Thank you for your kind words.

In terms of the shale oil and the technology, I believe that the technology cannot make wonders overnight. And more importantly, the current technology cannot get a lot better overnight, given that it took us (George Mitchell) many years to improve this shale process and bring it to the point where we are now.

If the oil price remains at the current levels for long, the peak oil event will occur in 2015, in my view.

Regards,

VD

———————-…

Please let me know when the majority of oil newsletter writers turn bearish, that is when I’ll be a buyer.

best,

-samberpax

You are NOT a subscriber of my newsletter that was out just 3 months ago, in September 2014, when the oil price was already falling.

If you were a subscriber, you could check my picks and the recommended entry prices.

And please let me know and I will gladly send you the returns from my picks in H1 2015, based on the recommended entry prices.

Regards,

VD

I buy the long case for Oil, long term. But the question is that of how long it will take to come back.

The political unrest in the middle east ist not necessarily a cause for less supplies: the ISIS for instance uses Oil to finance their war. The anarchy actually can dislocate the production discipline and lead to lower prices. But agreed with you, anarchy is not sustainable and Oil prices will eventually move up again.

Rgeards,

VD

The author seeks to discount the additional 3.5 million barrels the US produces that were not available 5 years ago by saying the wells dry up fast and the production cost are too high. That is the true “lame thinking” here. I heard estimates that some production cost in the Bakken are as low as $29 dollars and that $70 is actually on the high end. His cost estimates are from years ago. Good ole American ingenuity drives down the cost of recovering this oil daily.

The author doesn’t deal with the death spiral that OPEC currently finds itself in. The more profligate members need a high oil price in order to maintain their spending. If I can’t make my revenue with a high oil price what is my alternative? That’s right pump more. Their state goal at this last meeting was to keep the production quotas in place. What was unsaid and the real reason oil took another dive is cheating on production quotas will reach an all time high over the coming months as these governments seek to shore up their finances.

Finally, the author displays several charts but proceeds to ignore what the charts say. We have firmly broken all uptrends and any recovery will be very difficult. I would further break his argument down but that would just give more credence to yesterday’s theory about the state of energy supplies in the world.

So whats the max production capacity for the rest of OPEC for them to keep ‘pumping more’ to make budgets meet?

Secondly, just like in October when everybody “woke up!!” and sent the market down 10%, because NOW the world is going into recession, good call btw. I highly doubt you bears are any more correct on your reactionary projections after crude fell from $90, you must be rich predicting this stuff.

As an aside Gartman has been one of the best contrarian indicators of the past 2 years.

And just to put my money where it counts, not that seeking alpha isn’t awesome.I recently sold multiple strike puts on EOG, NOV, PXD, XOM, CLR. Implied volatility is ridiculously high, and if history is any indicator its a very high probability trade.

Edmund

Yes, that would be Dennis “Marty McFly” Gartman. To be honest, I would rather have the sports almanac than my oil stocks right now.

Thank you for the compliments. And when it comes to the nuclear fusion reactor, I do not disagree with you. We can definitely see it both ways.

Regards,

VD

Both oil and oil stocks have a lot further to fall in upcoming months. There will be a far better entry point for both later in 2015. Investors would be wise to exercise some patience here and let things play out for a while. Buying the first sharp break is rarely a good idea, particularly not when there are so many signals indicating that the global economy is losing momentum.

Oil prices will ultimately come back, until then focus on the myriad of economic sectors that benefit from cheaper energy. It should also present a great buying opportunity for a whole host of energy stocks.

This piece has too much emotion embedded in it for my liking.

I am not a professional analyst who is living from this analysis.

I am an investor instead.

Regards,

VD

Thank you for your compliments.

Please see my previous articles and comments to find my bearish calls on several energy stocks over the last months i.e. Halcon Resources (HK), Goodrich Petroleum (GDP), Cobalt International (CIE), GMX Resources (GMXRQ), ATP Oil and Gas (ATPGQ), CAMAC Energy (CAK), Pinecrest Energy (PRY.V), Midstates Petroleum (MPO) etc.

Regards,

VD

The title really sums up how stupid investors are being now. The current daily correlation between a 50 cent or $1 move in oil taking down oil stocks by a few percent is ridiculous. Dennis Gartman has no credibility, I don’t understand why CNBC has him on regularly.

Thanks again for the article!

They have Jim Cramer on, so why not Dennis Gartman? They both change their minds on a daily basis and do it with conviction.

Right now, small cap oil stocks should be bought for a year end rally, stocks like MDR, WG, etc could see huge gains from current levels.

Thank you for your compliments.

Regards,

VD

I think investors need to pull the trigger on stocks they wanted lower instead of watching tv for a buying signal.

What you describe is the definition of “HERD MENTALITY” that has brought the oil price at the current ridiculously low levels.

But Einstein has said: “Two things are infinite: the Universe and human stupidity. And I am not sure about the Universe.”

Regards,

VD

However, the claim that $80-$100 is the breakeven for shale seems unfounded – I think it was the IEA that said that only 4% of production uneconomic under $70?

I also read a very interesting article today, I think on CNBC (apologies for the lack of sources), that discussed how transportation costs have plummeted in the past years.

It mentioned that in 2011, companies were paying up to $28 a barrel in transport costs. It is now $1-$3 because of pipeline construction.

If that is indeed the case, it is clear that a lot of shale is economic way below $70.

Gartman and his nuclear fusion. What a tool. I made the exact same point elsewhere that unless engines are replaced with fusion reactors and someone discovers how to make plastic from ‘fusion’ we will be using oil for some time to come…

I think the plummeting oil prices are the result of speculation more than any other factor but, as always, the market can remain irrational for longer than most of us can remain solvent.

GL

Saudi only produces 10M bbl out of 30M bbl. I predict NOCs can only withstand the pain for 6 months. after that, they can elect to exit OPEC, and form a non-Saudi cartel to sell at $80-$90 band. Saudi can sell their 10M bbl cheap if they elect to, but that’s not enough to meet global demand, so buyers will have to pay non-Saudi price.

Regards, VD

He is betting that the price of oil will increase. He is correct in this assertion. Everyone knows the price of oil is going to go up, eventually.

““When you believe something, facts become inconvenient obstacles,” Hall wrote in April, taking issue with an analyst who predicted a shale renaissance could result in $75-a-barrel oil over the next five years.”

He should listen to his own advice, it seems.

Here is one article where the “5 year” buzz line comes from:

http://bit.ly/1viOe43

“The team acknowledges that the project is in its earliest stages, and many key challenges remain before a viable prototype can be built. However, McGuire expects swift progress. The Skunk Works mind-set and “the pace that people work at here is ridiculously fast,” he says. “We would like to get to a prototype in five generations. If we can meet our plan of doing a design-build-test generation every year, that will put us at about five years, and we’ve already shown we can do that in the lab” . . . . An initial production version could follow five years after that.”

And then ramping up commercialization of fusion power, another decade? we’re looking at 15-20 years best case scenario before fusion has any affect on fossil fuel prices. This just goes to support the author’s conclusion that oil prices are low due to “lame thinking.”

No chart of the relationship between the strength of the dollar and the price of oil. Is it relevant?

Good luck with your picks.

To all those investors who believe operators in the unconventional reservoirs can keep producing while oil prices are dropping, check out their H1 budget forecasts for negative changes in CAPEX. That will remove much of the guess work and hand waving on how profitable they expect their operations to be. They know better than the analysts and economists on when to turn the taps off.

gartman is the worst of the worst in my opinion. he really is clueless. I dont know why they keep having him on every other day on fast money and the like.

Its funny how media affect sentiment changes on a dime that makes everyone forget the bigger picture as you referenced above.

remember ebola and the airline stocks in october? ignore the noise.

Regards,

VD

I think at some point sooner than the media and herd thinks that oil will bounce hard upward. OPEC made a good move to instigate a needed correction and put the industry in check. Now I think (in the short term) we will see a scary drop lower fueled by more moves by OPEC such as todays move to cut prices from SA to Asia/India and USA. SA sees India as growing and needs to subdue the fact that demand is growing. I would not be surprised if massive amounts of capital is also used to force the commodity down further to keep the herd moving ion that direction. OPEC knows that they can turn it around very quickly (just tell the world they are cutting production and the herd reverses quickly) when they need to so they are in the drivers seat for sure.

Thank you for the compliments.

A LOT of people and greedy oil speculators will be burned by shorting at the current levels. They have to pay for their mistakes and their greed, as always.

Regards,

VD

There is nothing about ego here. You misunderstood it. I have a clear opinion that I support it with facts and links. If you have a different opinion, you are welcome to present it coupled with facts in another article. If you present speculation only, it will not help, I think.

Regards,

VD

when you started quoting your” gods ” and casting scorn on any who disagree i lost interest.

ps mr market is always right no matter how much fundamentalist cry.

Another paradigm changing event already mentioned is China. The enormous real estate debt bubble and steel production bubble also fueled by debt has to come to a head soon. Yes, the collapse of China has been forecasted “forever” but so was the 2007 US recession which also was belittled for years right up to the edge. So was the collapse of the Soviet Union. The Chinese Govmnt has been able to keep the ball in the air because they control most of the economy but the Piper stands at the door. A Chinese economic collapse which WILL come will also collapse the oil price. Maybe it will recover some first but no energy investor can afford to ignore this.

Caveat Emptor!

position, firmly. [until I change it]

What I am sure of, is that this situation will change, and that change

is inevitable.

NO, I am not an analyst.

What I want to know is a chart from the EIA on Zero Hedge showing retail gasoline sales in the USA have declined almost 75%!!!! since 2004. Then Bloomberg showed a photo of the first gas station in America selling gas for below $ 2.00. Weird that below the gas price it showed Diesel selling for $3.39 plus! The EIA does not explain that stuff well why diesel is much more expensive than gasoline.(a six cents higher tax from the Feds. low suphur costs and “demand” globally????) Then the EIA shows gasoline production in the USA has risen!!! OK that tells me big oil is exporting refined petroleum products to other countries to make tons of money off us. Killing diesel over environmental EPA type stuff for political reasons because gasoline costs more to make than Diesel even with the other factors and six cent tax, and Exxon is back in Green River developing their shale oil in situ electro-fracking method for the largest oil play on earth-TRILLIONS of BARRELS in AMERICA. All comes down to costs, the big boys games, and ignorance of the average US citizen willing to be played and fleeced.

Yes overall your article was good but there’s a lot more going on the secret weird world of big oil than any of us will understand like how in the 70’s the US “government” supposedly allowed Saudi Arabia to shut down our nation in the WINTER and I froze waiting in gas lines? The USA??? Biggest army on earth plus Standard Oil of California developed the Saudi oil???? Or that their lawyer, John J. McCloy told at least seven US “presidents” what to do and say through Reagan and HW Bush? Heck he even ran the Warren Commission with Dulles and World War 11. Harold Hamm says he can drill existing wells in the “Scoop” at 99 cents a barrel and tried to sue OPEC. He is not going to shut down next year and plans on ramping up oil production big no matter what the price is. He wants to ream OPEC and make them blink unlike the 1986 oil bust when we went broke.

All highly interesting and I am watching and going to buy back when I think oil has hit the low-could be next year though?

why are you looking at GDP growth rates when talking about oil demand when oil demand figures for those same countries are available?

I dislike articles that spend their time making fun of other oracles and then turn around and make their own guesses of what the future holds. It’s an emotional argument.

Actually, I like that part – in my nearly 2 decade experience, I’ve seen far too many investors put too much faith on analysts and it’s important to show actual real life examples where analysts are fallible also.

For example, take a look at SDRL. When SDRL was above $40, there were not many analysts telling investors to sell, the prevailing tone was “crude oil is going up, up, up, and buy, buy, buy”.. But when SDRL cuts dividends to zero at $15-$20, they are now downgrading SDRL. Buy at $40, sell at $20? I think you can go to the poorhouse very fast following these “anal-ysts”.

SDRL is not an isolated example. Today, after massive price falls, I see Zacks now telling investors to sell their energy mutual funds after these funds have massive falls …

As for the future, no one knows what is going to happen, you have to follow your own investing/trading thesis. For me, I think SDRL has fallen 75% from peak, cut dividends to zero, so, I am slowly starting to accumulate SDRL, looking to spend up to 4% capital when it finally gets down to say $7. Yes, no guarantee it will fall down that far when today is only $12, but I like the fact that it has fallen from a peak of $48 down to $12 … that’s my unsubstantiated opinion also, and probably emotional as well 🙂 And yes, I’m starting to think of accumulating when analysts consensus is to sell … it worked very well for me over the past decade ….

———————-…

Exactly so! I am elevating my standard by lowering theirs. Sad, very sad indeed.

Best,

-samberpax

http://bloom.bg/12CBfjp

Here is the link to Lockheed-Martin’s compact fusion announcement. These researchers/engineers are the best of the best, I would think, so if they’re making an announcement, they must have something legitimate up their sleeve, I would think:

http://lmt.co/1yJEu5x

Interesting article on Fusion, nice read.

However, the recent crude oil price fall down to $66 is most likely unrelated to Lockheed-Martin’s fusion piece, as that piece seems more about promoting Lockheed-Martin in research and what they think they could achieve in 5 years time, and still not yet confirmed …. but good to cast a quick glance from time to time on these sort of things ….

If Lockheed-Martin managed to bring this to commercial production at small enough sizes at reasonable prices (that’s a BIG IF), then, I think we first see Lockheed-Martin’s stock price zooms up first a lot more than what we’ve seen so far, before we see global crude oil prices comes down significantly … that’s just my gut feel …

There is no guarantee we’ve seen bottom in crude yet, but I feel we are now entering a period where Value Investors should start to feel excited on some of the high quality issues that are beaten up hugely, to trade below NAV and trade well below Replacement Costs …

Cheers,

TF

I haven’t sold any of my oil stocks, but I haven’t added yet, either. Would love to buy some LNCO to bring down my cost basis, but I’m concerned they’ll have to cut, or pull a Seadrill and eliminate, their dividend.

I have been waiting for a follow-up and this seems to be the one.

Again I am impressed by your knowledge and your reasoning but I’m a bit disappointed too. Especially by not addressing points 3 and 4 of these 8 major reasons.

———————-

Just to refresh, points 3 and 4 of these 8 major reasons:

3) The weakening of the U.S. dollar.

4) OPEC’s decision to cut supply in November 2014.

Best,

-samberpax

Please bear in mind that the HERD MENTALITY is like the TITANIC cruise ship. The big ships need a couple of miles to turn….

Regards,

VD

Agree this is very much a TITANIC cruise ship that will take a few miles to turn … apparently, the weekly US Oil production figure need to show 2 to 3 consecutive week of decline at the very least first. Until then, odds are crude oil will keep falling (short term momentum). I now feel we may be close to bottom, but we are not confirmed there yet, and I won’t be surprised if crude makes $30 very briefly, before a strong and fast recovery once a few of these marginal producers are out of the picture …

Just as Saudis and US are stubborn right now to curtail production, in a year’s time when a few of the US producers goes bust, the Saudis will have achieved their objective and cut production, and just as quick, I see crude oil could rise back to $100 very fast … the US production numbers are always a surprise to markets, I expect the Saudi’s response to also be a surprise to the market when they cut back production in 6-12 months time – those looking for signs will not find it, I believe it will be a surprise to the market when it happen anytime within the next 12 months …

Whilst I agree with your base thesis and believe that the price of oil is going back up to what are more “normal” levels, some of the biggest consumers of oil on the planet are likely going to use less-and-less of it as time goes on. For example, there are pretty strict rules in place for future vehicle mileage requirements in the US, the EU has been clamping down hard on emissions for a pretty long time and lots of companies are now involved in the business of making energy efficient equipment and machinery. The list is long – GE, Siemens, Caterpillar, Deere, Hitachi, Volvo, Komatsu…..and so on.

The historical environment for oil consumption is becoming more-and-more dated when compared to what the oil consumption environment will look like going forward. It’s hard if not impossible to use the past as an accurate guide to the future.

The future oil consumption environment in two words – different and lower.

If you are short on crude oil, I don’t see a reason why you need to close your shorts now as crude keeps falling. You should only close it when you see a confirmed uptrend, at least, that’s my view.

Value Investors though are a different breed – they ease their way in specific value stocks, and now, many oil related stocks are trading at below NAV and well below Replacement Costs with strong cashflows during the last oil crisis … these stocks could still fall by another 25%-50% or close to bottom, no one really knows and so, they start to accumulate a little bit at a time … history has shown that crude oil will eventually recover, and they could be looking at +100% returns in 1-3 years time … the Value approach does not require market timing, and crude oil being highly cyclical in nature means we will definitely see $80-$100 crude oil again eventually over the next 1-3 years, we just don’t know exactly when. If it goes back to $100, you can be sure many of these crude related counters will go back up to their former levels, potentially 100%-300% gains …

Mr Market has presented a compelling opportunity, the key is Money Management, accumulate a few high quality counters, and once bought, lock them up in a drawer and don’t worry about the daily price volatilities. In 1-3 years time, the gains of +100%-300% can be had … know the strategies in advance, never allocate more than 15%-20% portfolio to oil related counters at the bottom, and certainly, never go on margins. I have been staying cash majority of my portfolio, I just recently allocate 2% capital on oil counters, and plan to slowly work my way to 15%-20% assuming these stocks could fall up to 50% from current levels … This is a no-brainer approach, I just don’t care about the daily price volatilities.

Cheers,

TF.

i am heavily long on oil and hurting badly but i keep buying as price drops. i am in your camp

Oil futures, stocks or options? I hope it is not leveraged instruments? The trend is still down …

I’m eyeing SDRL – originally, I plan to go in with 4 bullets, at $13.50 (already done), $11, $9 and $7 very roughly speaking, but now, I will most likely try to take advantage of the short term down momentum (I am a trader) to cut loss some and take wait to pick it up at lower prices, and wait for a better technical signal. Allocating just 4% capital for SDRL.

The other 2 counters are HP (this is a Dividend Aristocrat that keeps paying higher dividends every year for over 25 years) and NE (this is a nice Value play), but I haven’t triggered any buys in either yet as Crude keeps falling and the counters keep falling … Again, 4 bullets each, total 12% capital when I’m done all the 3 buys at the bottom.

Originally, I plan to make a “simple” buy approach of just buying at set levels, but the more I study the crude markets fundamentally, the more I realize that I can fine-tune my entry better, so, let’s see if this is successful or not …

How about you? What counters are you looking at?

Glad you didn’t go for futures / options with time expiries – I just don’t know how long these crude oil price can fall – it can keep falling and falling, and the bottom and recovery I believe will be a huge surprise to me.

Personally, I prefer safer, large caps, very liquid stocks that institutional buys with average daily volume greater than 500k to 1000k shares, and try to buy using a combination of writing puts and directly, and sell covered calls also.

Whilst my current list is SDRL, HP and NE, if I find something else better, I’ll most likely drop one for that …

Good luck.

Cheers,

TF

Oil company stock valuation is based on EV/B/D; EV/EBITDA and EV/Reserve; It does not matter whether large cap or debt; In case of low rev they can always curtail drilling and be very liquid to pay down debt. Worse come worse they will sell their reserves for better price than current valuation. We just bid on various leases offered by Chevron and we did not get it as there are numerous buyers willing to pay higher price.

raj

One could make educated guesses based on the geopolitical actions/goals of the major oil producing countries, changes in demand, etc.

I’d rather see oil stay around these levels for a while as I accumulate.

Looking at Venezuela and Iran for example – the oil price before the crash, at it’s peak…was nowhere near the quoted figures given for these countries to approach break even; so who goes broke first…small shale producers in the USA or the countries that need $150 oil to just break even, or do they just continue to go broke forever?

I don’t think the OPEC decision is targeted solely at US shale plays…there’s others that are in far more pain over this, the rest of the global economy benefits while oil producers suffer a small but probably needed shakeout: I’ve got investments in oil but it’s ok to lose paper money on one part of the portfolio if another part benefits… I think sovereign default would be a lot worse for everyone involved. Oil will go back up in price eventually, and the median price will rise over time as the asset depletes. When is actually not that important unless you need your money tomorrow.

Please see the excerpt below:

” On top of that, there are some additional geopolitical clouds on the horizon that can make oil jump by H1 2015. For instance, the current low oil price has brought many OPEC members to their knees, while the holders of those countries’ sovereign debt are toast as long as oil stays at the current levels. Iran, Iraq, Libya, Algeria and Venezuela are not prepared to withstand low oil prices for long and they are now in serious danger of political upheaval at current prices.

According to yesterday’s news from CNBC, the first signs of an escalating social unrest in Venezuela are already there, and things will definitely get worse over the next weeks.

Furthermore, Russia and Saudi Arabia will be anxiously watching the rapid depletion of their sovereign wealth funds, which will make the political situation in these two countries dicey over the next months. “

Regards,

VD

The sharp increase in production in the US over the past 5 years is simply amazing, however, it would be interesting to see what the overall average decline rate is for the US over the same time period.

I’m inclined to believe that the decline rate is substantially higher in part due to the tremendous number of unconventional wells that have been drilled in the past few years and the fact that they are in the steep part of the decline curve. So, while production has been climbing, it seems that the Saudi’s are hoping to curb drilling and therefore let the decline curve catch up with the industry. With a sustained drop in prices, eventually borrowing base redeterminations will result in at least a moderate decrease in drilling, perhaps even drilling within cash flow!

Also, while my opinions mean very little, I think it is important to point out somewhat misleading comments about certain plays being profitable at $40 or whatever they want to insert. Yes, if lease operating expenses and field level costs, transportation, ad valorem etc are $25-$40 per barrel, then those wells will be cash flow positive as long as pricing remains above that price.

However $25-$40 oil will not provide a decent IRR for new wells. Remember most of these shale wells exhibit very high initial production and have sharp hyperbolic type declines. Producers need to get full payout in the first 12-24 months. Wells might decline 60-70% within the first 24 months. Look at the NPV of many of the Bakken wells at $60/bbl. Not nearly as attractive as when they were $100.

I don’t know what oil pricing will do in the next few months, nor do I know what OPEC and the Saudi’s will do in 6 months. I do however believe that US oil producers will eventually have to reign in drilling budgets as cash flow wanes. I don’t know if that will mean production growth will taper, if production will hold steady with new production offsetting natural decline or if total US production will slowly decrease. I do know that it will be interesting to see it unfold.

And while my opinion isn’t worth much, I believe that we will eventually find some happy medium where US producers can achieve decent IRRs and production can grow modestly. My guess is $75-$80 bbl.

While VD is great at pointing out value, guessing what will happen to the price of oil will always be speculation. I like the argument given here, but the truth is that no one really knows.

Investors in oil-producing companies should do so because they believe that their fundamentals will allow them to be successful and profitable in any environment of oil pricing.

– The recommended entry price for my picks, given that timing matters when it comes to investing. Buying a good company is not enough.

– The investment horizon, given that I am not a day trader.

Regards,

VD

Thanks for your reply. One of the things I appreciate about your articles is always standing by your track record. Given that, here are some of your picks from this year:

CAZFF Recommended 5/15/14 – market price $0.30, currently at $0.14.

PTAXF Recommended 8/26/14 – Market price $0.38, currently at $0.14

LNREF Recommended 6/7/14 – Market price $0.35, currently at $0.19

They have all experienced significant losses (on average 52%). However, I agree that I am not a day trader so if I liked these companies enough to buy them, I would still hold on as long as the fundamentals have not changed. As Buffet said, if you aren’t willing to lose half of your investment in the market, you shouldn’t be there.

I remain long, but the simple fact is that there have been some significant losses in the short term.

I was wondering why you did not mention:

AEI.T recommended at C$4.95, now at C$6.85, up 40% despite the slump of the energy stocks.

CKE.T recommended at C$0.82, now at C$1.25, up 50% despite the slump of the energy stocks.

CAZ.T was recommended at C$0.24 in May 2014.

LNR was recommended at $0.32 in June 2014.

PTA.V was recommended at C$0.39 AND C$0.25 in October 2014:

http://seekingalpha.co…

and for reference, Oasis (OAS) has dropped from $55 to $14,

Sandridge (SD) from $7 to $2.4

Magnum (MHR) from $8.6 to $3.9

Penn Virginia (PVA) from $17 to $4.8

Quicksilver (KWK) from $3 to $0.40

and many many other producers have returned back to their 2010 levels. I can continue if you want. This might help you see the big picture.

Regards,

VD

My view is some new tight oil wells would still be drilled if oil stayed below $70, but likely not enough to overcome the rapid depletion from existing wells. I believe we will start to see US production drop sometime in H2 2015, but until then US production keeps going up. Think it will take maybe 6 months for wells already committed to be drilled and completed. After that market should at some point get back to $80-$85, maybe 12 months. But likely to be a volatile ride along the way. I personally think we have not seen bottom yet. Too much downward momentum, global oil production likely to keep increasing for the near term.

Best to prepare for the volatility and try to recognize the opportunities as they play out, IMO. So many things could intervene ( geopolitics, global economic activity, China credit, etc)!

Take care

http://bit.ly/12EquNo

Regards,

Nawar

Thank you for your compliments and your insightful comment. Yes, the news you mention is another very strong bullish indicator.

Regards,

VD

If this 5 million BOEPD were not on the world market today, where would we be?

We would be short on oil.

Instead, we are long on barrels because every dumba** American oilman that drills a good well immediately turns around and puts all of the cash flow from his good well into ANOTHER well. Plus he borrows a few million bucks to drill a few more wells.

How else can you explain the unprecedented exponential oil production growth in this country?

I wish these geniuses would spend their profits on wine, women, song, jet airplanes, country houses or something, besides plowing every single dollar of profit back into the ground.

You make a statement in your piece that sums up your whole thesis: “new oil is not cheap.”

Any way we look at the supply situation, most new production will continue to come from expensive unconventional means such as shale or tar sands. Surely there are new conventional pockets of crude to be found, but they won’t be Elephants and will probably be expensive “deep water” reservoirs.

Petroleum remains a key product for Global Energy & Industrial production and current low prices will NOT allow future demand to be satisfied.

Us reserves….

http://bit.ly/1vYF4uf

china oil reserves