Illinois has passed a law requiring landlords to open their doors to illegal immigrants.

Illinois has passed a law requiring landlords to open their doors to illegal immigrants.

A lethal combination of rising property taxes and stagnant incomes has forced many Illinoisans to rethink their relationship with their state. More than 1.5 million net residents have already fled the state since 2000 – and you can’t blame others for thinking about joining them.

Property taxes have become punitive in Illinois. We’ve written about how these taxes have destroyed the equity in people’s homes across the state. Many families have done the math, and whether they’re in the struggling south suburbs of Chicago or the affluent North Shore, they’ve decided to leave Illinois behind.

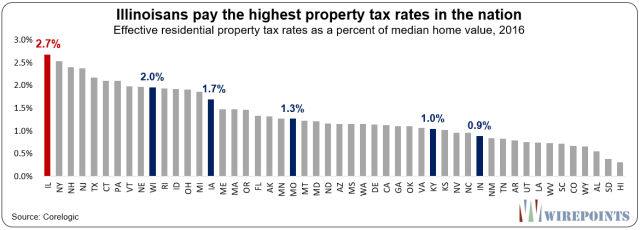

The traditional method for measuring the burden of property taxes is to look at a household’s property tax bill and compare it to a home’s value. Under this method, Illinoisans pay the highest property taxes in the nation. At 2.7 percent, Illinoisans pay far more than residents in neighboring states – twice more than those in Missouri and three times more than residents in Indiana.

That fact is outrageous on its own.

But to really understand the pain that these taxes inflict on Illinoisans, it’s important to compare property tax bills to household incomes. After all, those bills are paid straight from people’s earnings.

The unfortunate reality is that Illinois incomes have been stagnant for years – and falling when you consider the impact of inflation.

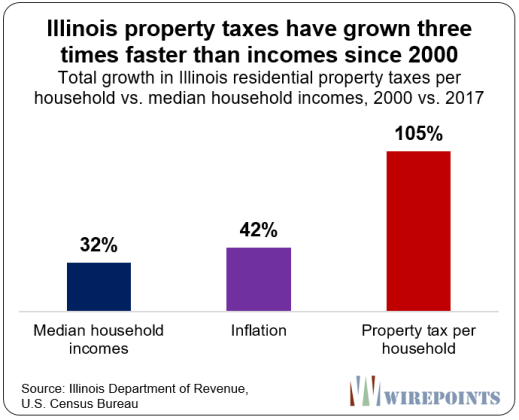

Between 2000 and 2017, Illinois median household incomes increased just 34 percent, far short of inflation. In contrast, household property tax bills are up 105 percent, according to Illinois Department of Revenue data.

The net result: Property tax bills per household have grown three times faster than household incomes since 2000.

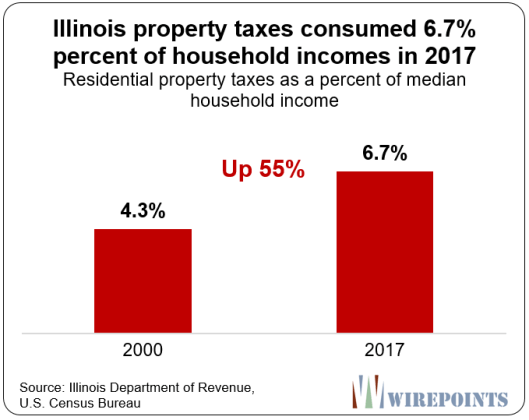

That means more of Illinoisans’ hard-earned incomes are going toward property taxes and less towards groceries, college tuition, and retirement savings. In 2017, 6.73 percent of household incomes went toward property taxes, up from 4.3 percent in 2000.

That’s a 55 percent increase in the effective tax rate.

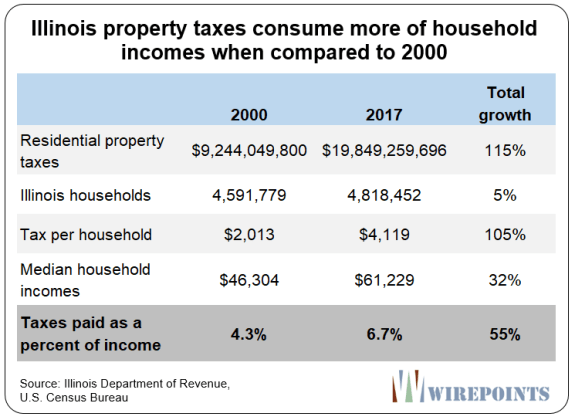

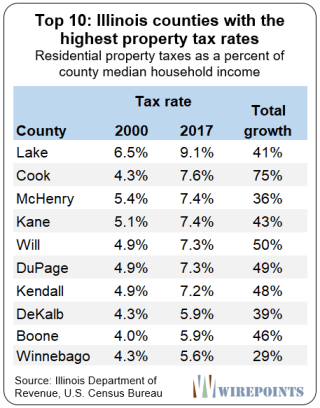

The detailed data is below:

Residents of Lake County pay the highest property taxes in Illinois when measured as a percentage of household incomes. In 2000, Lake County residents paid 6.5 percent of their household incomes toward property taxes. Today, residents pay 9.1 percent. That’s a 40 percent increase. The average Lake County property tax bill is now over $7,500 per household.

Meanwhile the residents of the other collar counties and Cook pay more than 7 percent of their incomes to property taxes, with average bills ranging from $4,500 to $6,200 a year.

Overall, the collar counties pay the highest taxes as a percent of income in the state. But it’s not just the Chicago suburbs that are taking a hit. Taxpayers statewide have seen their taxes rise.

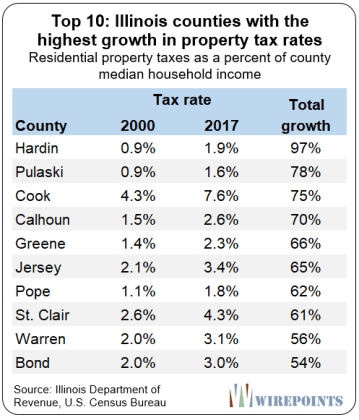

In fact, most of the counties that have had the biggest tax growth, in percentage terms, are found downstate. Hardin County residents, though they pay low rates, have seen them jump 97 percent since 2000. Residents in Pulaski County, have seen their rates go up by 78 percent.

Cook County comes next at 75 percent, but after that it’s all deep downstate again: Calhoun (70 percent), Greene (66 percent), Jersey (65 percent), and Pope County (62 percent).

Any way you cut it, Illinoisans are being punished by property taxes.

That’s prompted some, including new Gov. J.B. Pritzker, to propose a reduction in property taxes by increasing income taxes.

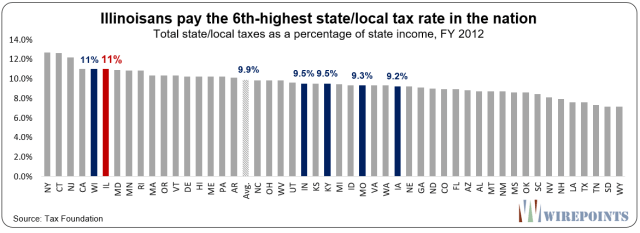

But that would do Illinoisans no good. Illinoisans already pay the nation’s 6th-highest rates when you lump all state and local taxes together.

Shifting them around won’t help when the total tax bill is too high to begin with. What Illinoisans need is tax cut, not a tax shift.

Source: ZeroHedge

By Ted Dabrowski and John Klingner via WirePoints.com

If there was one guy you’d think wouldn’t succumb to the pressures of living in Illinois, it’s Lakewood Mayor Paul Serwatka.

He’s a reformer and a fighter. In the past year he’s succeeded where most politicians refuse to go. He lowered the Village of Lakewood’s property taxes by 10 percent and eliminated a TIF district, going against the trend of higher spending and bigger tax bills in communities across the state. And he did all that without cutting services. He was showing Illinoisans what reform-oriented leadership could look like.

But every family that’s chosen to flee Illinois in recent years hit a breaking point and Serwatka finally hit his. For him, it was the risk he wouldn’t be able to care financially for his growing family.

You can’t blame him and those families that have already left. For many, it’s become too expensive to live in Illinois. For others, good-paying working class and manufacturing jobs have disappeared. And for yet others, they’re tired of being taken for granted and mistreated by their politicians.

At the core of the decision for many families to leave is the burden of higher property taxes. They’ve become punitive in too many parts of the state, as Wirepoints has covered in detail.

That’s true even in Lakewood, a city of nearly 5,000 people located in McHenry County. Residents in that county pay some of the state’s – and the nation’s – highest effective tax rates, measured as a percentage of household incomes.

Serwatka has four young children to think about – ages 3 to 8 – and he did the basic math that many Illinois families are doing in their kitchens or family rooms. They’re comparing what their property taxes are in Illinois to what they could be in other states – and what they could do with all the money they save.

For Serwatka, his comparison city was Decatur, Alabama.

There his family found 10 acres and a house that’s 25 percent bigger than their current Illinois home, all at roughly the same cost. The Alabama house also has access to a private lake shared by some 60 homeowners. And his home in Decatur is only 20 miles from Huntsville, which is booming in all kinds of ways.

What are his Alabama property taxes going to cost him? Just $2,200 a year. That’s a lot lower than the $15,400 he’s paying on the home in Lakewood.

If Serwatka saves that $13,000 difference every year and invests it at 6 percent annually for the next 20 years, he’ll have accumulated savings of more than $600,000 dollars.

It’s a difference Serwatka and his wife, Robin, just couldn’t ignore.

Sadly, Illinois politicians continue to push property tax rates to record levels. They are the highest in the nation, double the rate in Missouri and three times higher than those in Indiana.

* * *

Serwatka is confident he’s delivered on the promises he made when he took office. Residents who were looking for reforms, lower taxes and more respect from their politicians got exactly that from him .

But in the end, the savings he produced as the mayor of a small town weren’t enough to offset the tax increases coming from the school district and the other myriad of local governments, not to mention the state itself.

Those taxes are now so high they’re chasing out even the reformers – those bold enough to buck the system in Illinois.

The reality is, Illinois’ failed policies discriminate against no one. People are being forced to do what’s best for their families. And if that means leaving, they’re doing it.

An audible gasp went out in the breakout room I was in at last month’s pension event cosponsored by The Civic Federation and the Federal Reserve Bank of Chicago. That was when a speaker from the Chicago Fed proposed levying, across the state and in addition to current property taxes, a special property assessment they estimate would be about 1% of actual property value each year for 30 years.

Evidently, that wasn’t reality-shock enough. This week the Chicago Fed published that proposal formally. It’s linked here.

It surely ranks among the most blatantly inhumane and foolish ideas we’ve seen yet.

Homeowners with houses worth $250,000 would pay an additional $2,500 per year in property taxes, those with homes worth $500,000 would pay an additional $5,000, and those with homes worth $1 million would pay an additional $10,000.

Is the Chicago Fed blind to human consequences? Confiscatory property tax rates have already robbed hundreds of thousands, maybe millions, of Illinois families of their home equity — probably the lion’s share of whatever wealth they had.

Property taxes in many Illinois communities already exceed 3%, 4% and even 5% of home values. Across Illinois, the average is a sky-high 2.67 percent, the highest in the nation.

In south Cook County they already average over 5%. Most of those communities are working class, often African-American. The Fed says maybe you could make the tax progressive by exempting lower values, but that’s very difficult to do and, if you did somehow exempt the poor and working class, the bill pushed to the others would be astronomical.

Those rates have already plunged many communities into death spirals, demanding an immediate solution, but the Chicago Fed apparently wants to pour on more of the accelerant.

Don’t they understand that people won’t build on or improve property when property taxes are that high? When taxes are 3 percent to 6 percent, any value you add to your home is going to be taxed at that high rate forever. Have they never been to our communities with countless dis-repaired, abandoned homes and commercial properties, which are the result?

Get this, which is part of the Fed’s reasoning: “New taxes wouldn’t affect people thinking of moving to Illinois. While they would have to pay higher property taxes, that would be offset by not having to pay as much for their new homes. In addition, current homeowners would not be able to avoid the new tax by selling their homes and moving because home prices should reflect the new tax burden quickly.”

In other words, just confiscate wealth from current owners because they will pay, whether they stay or not, through an immediate reduction in home value.

This proposed tax would only address the five state pensions. What about the other 650-plus pensions in Illinois, particularly those for overlapping jurisdictions in Chicago which are grossly underfunded? The Fed was asked that at last month’s seminar and they, without explanation, said they didn’t bother to cover that.

I’ve earlier met Rick Mattoon, one of the Chicago Fed authors of the proposal. He’s a smart, likeable guy who I thought had lots of interesting information. For the life of me, however, I can’t understand how he would put his name on this proposal.

Real Property can’t leave, so seize more of it. That’s the basic idea.

First Maine, then Connecticut, and finally late on Friday, confirming the worst case outcome many had expected, Illinois entered its third straight fiscal year without a budget as Republican Governor Bruce Rauner and Democratic lawmakers failed to agree on how to compromise over the government’s chronic deficits, pushing it closer toward becoming the first junk-rated U.S. state.

By the end of Friday – the last day of the fiscal year – Illinois legislators failed to enact a budget, and while negotiations continued amid some glimmers of hope and lawmakers planned to meet over the weekend, the failure marked a continuation of the historic impasse that’s left Illinois without a full-year budget since mid-2015, and which, recall, S&P warned one month ago will likely result in a humiliating and unprecedented downgrade of the 5th most populous US state to junk status.

Then came the begging.

According to Bloomberg, on Friday Illinois House Speaker Michael Madigan, a Democrat who controls much of the legislative agenda, pleaded with rating companies to “temporarily withhold judgment” as lawmakers negotiate. “Much work remains to be done,” the Democrat said on the floor of the House Friday, before the chamber adjourned for the day. “We’ll get the job done.”

Meanwhile, the state remains without a spending plan, its tax receipts and outlays mostly on “autopilot”, leaving it with a record $15 billion of unpaid bills as it spent over $6 billion more than it brought in over the past year, and with $800 million in interest on the unpaid bills alone. The impasse has devastated social-service providers, shuttering services for the homeless, disabled and poor. The lack of state aid has wrecked havoc on universities, putting their accreditation at risk.

However, in a “shocking” development, just hours remaining before the midnight deadline to pass the Illinois budget, and Illinois’ imminent loss of its investment grade rating, federal judge Joan Lefkow in Chicago ordered Illinois to come up with hundreds of millions of dollars it owes in Medicaid payments that state officials say the government doesn’t have, the Chicago Tribune reported. Judge Lefkow ordered the state to make $586 million in monthly payments (from the current $160 million) as well as another $2 billion toward a $3 billion backlog of payments – a $167 million increase in monthly outlays – the state owes to managed care organizations that process payments to providers.

While it is no secret that as part of its collapse into the financial abyss, Illinois has accumulated $15 billion in unpaid bills, the state’s Medicaid recipients had had enough, and went to court asking a judge to order the state to speed up its payments. On Friday, the court ruled in their favor. The problem, of course, is that Illinois can no more afford to pay the outstanding Medicaid bills, than it can to pay any of its $14,711,351,943.90 in overdue bills as of June 30.

The backlog of unpaid claims the state owes to managed-care companies directly, as well as to the doctors, hospitals, clinics and other organizations “is crippling these providers and thereby dramatically reducing the Medicaid recipients’ access to health care,” Lefkow said in her ruling (attached below).

* * *

Friday’s court ruling, which meant that the near-insolvent state must pay an additional $593 million per month, may have been the straw that finally broke the Illinois camel’s back.

“Friday’s ruling by the U.S. District Court takes the state’s finances from horrific to catastrophic,” Comptroller Susana Mendoza, a Democrat, said in an emailed statement after the ruling.

As a result of the court decision, “payments to the state’s pension funds; state payroll including legislator pay; General State Aid to schools and payments to local governments — in some combination — will likely have to be cut.”

“As if the governor and legislators needed any more reason to compromise and settle on a comprehensive budget plan immediately, Friday’s ruling by the U.S. District Court takes the state’s finances from horrific to catastrophic,” Mendoza said in a statement. “A comprehensive budget plan must be passed immediately.” Realizing where all this is headed, she said that payments to bond holders won’t be interrupted (more below).

Illinois Comptroller Susana Mendoza

Friday night’s legal decision followed a previously discussed ruling, when on June 7, Judge Lefkow ordered lawyers for the state to negotiate with Medicaid recipients to come up with more money, but she stopped short of dictating how much more the state should pay each month, or when. That decision sent Illinois General Obligation bond soaring.

Earlier this week, the parties again went before the judge to say they were at an impasse, with lawyers for Medicaid recipients asking for more than $1 billion a month to cover past and ongoing costs.

Lawyers for Illinois countered that they could only come up with approximately $75 million more a month, which would translate to $150 million with federal matching dollars. Although the state is way behind, state officials said in court filings that they have been making more than $1 billion in Medicaid related payments each month in 2017, “including payments to safety net hospitals, MCOs, and other providers.”

While the state was livid over the decision, plaintiffs were delighted. Tom Yates, one of the lawyers who represented the Medicaid recipients. said the judge’s ruling is a “fair result” that will help them have access to care. “Medicaid is an incredibly important program for 25 percent of the state’s population,” Yates said. It remains unclear, however, where Illinois would find the required funds.

In her ruling, Lefkow said the state must pay the $2 billion toward its past obligations beginning July 1 and ending June 30, 2018. She ordered the state to file monthly reports showing that it’s making the payments consistent with the ruling. The Judge said she considered submissions by managed care organizations, including The Meridian MCO and Aetna Better Health Inc., in reaching her decision. Meridian is owed $540 million and Aetna is owed $700 million, the judge said. In addition, she considered submissions from doctors and clinics.

Adding insult to crippling financial injury, the judge also ordered the state to file monthly reports showing that they are making the payments consistent with the ruling.

* * *

Meanwhile, despite the recent fireworks, things in Illinois remain on autopilot as the state needs a new budget to change financial direction.

Without a budget, Bloomberg writes, the state has continued to spend more than it brings in. That’s forced it to cover “core priority” payments first, including payroll, debt service and pensions that total about $1.85 billion a month. While those bills include some Medicaid-covered payments like health services for children and adults, the state has said there aren’t enough funds to include general payments to managed-care organizations as a top priority.

Also, without a budget that includes borrowing to pay down the bill backlog, Illinois by August will run out of money for key expenses for the first time since the stalemate began, according to Comptroller Mendoza. That means school funding, state payroll, and pension payments could be affected, she said. There won’t be enough money for these mandated or court-ordered payments.

As noted above, Mendoza said that this won’t jeopardize debt-service payments, however she probably should have added “for now.” For now, Illinois hasn’t missed any bond payments and state law requires it to make monthly deposits to its debt-service funds.

For now, despite the Illinois deadline coming and going, the political standoff shows no signs of ending.

And now the market is set to react: investors have already punished Illinois for its fiscal woes. Yields on the state’s 10-year bonds have soared to 4.8%, 2.8% points higher than benchmark debt. That’s the highest yield of all 22 states that Bloomberg tracks.

Summarizing best the chaos in Illinois was John Humphrey, the head of credit research for Gurtin Municipal Bond Management, which oversees about $10.1 billion of state and local debt who said that “recognizing that they’re continuing to work through the weekend, it doesn’t look good to adjourn halfway through your last day.”

Chicago area sees greatest population loss of any major U.S. city, region in 2015

Ten years ago, Bonita Hatchett built her dream home in Flossmoor. A lawyer by trade, she moved to the south Chicago suburb to join a diverse community that included black professionals like herself.

But Hatchett is now planning to leave it all behind. The culprit? Property taxes.

“You’re told all your life: Be educated, be successful, work hard and buy a house. But, we’re being abused for doing so,” Hatchett said. “Living in a town like Flossmoor, it’s just not worth it.”

She’s not alone.

Illinoisans pay among the highest property taxes in the nation, according to the nonpartisan Tax Foundation. Some Illinoisans’ property-tax bills are more than their mortgage payments. And the squeeze is getting worse.

Since 1990, the average property-tax bill in Illinois has grown more than three times faster than the state’s median household income, according to Illinois Policy Institute research.

While Hatchett estimates the value of her home has been slashed in half over the past decade, her property tax bill has only gone up. She paid more than $18,000 in property taxes last year — well over 5 percent of what she thinks her house is worth.

Hatchett plans to move to Indiana, where taxes on residential property are capped at 1 percent of the value.

Seventy miles from Hatchett’s home, in the northwest Chicago suburb of Crystal Lake, Cassandra Bajak thinks this coming Christmas will be her two children’s last in their home. Since she and her husband, an Army veteran, built the house in 2002, their property-tax bills have doubled — eclipsing their mortgage payments.

Her family now is choosing between a move to a southern state or downsizing in their community.

“We’re being taxed out of our home,” Mrs. Bajak said. “The only reason we would ever leave our home or this state is property taxes, and that’s what’s going to happen.”

In McHenry County, where the Bajaks reside, property taxes eat up nearly 8 percent of the median household income. What’s worse, Illinoisans aren’t getting much bang for their tax bucks.

Property taxes at the municipal level have not been going to fund spotless roads or other public works. Instead, they’re mostly funding out-of-control pension costs.

Just take a look at Springfield, where 98 percent of the city’s 2014 property tax levy went to pensions. And where, from 2000 to 2014, members of the typical household have seen their property-tax bill grow more than twice as fast as their income.

Despite that, city-worker retirements are still in jeopardy.

While taxpayers have more than doubled their contributions to the local police and firefighter pension systems over the past decade, Springfield’s police pension fund has a mere 53 cents in the bank for every dollar it needs to pay out future benefits; for firefighter pensions, only 45 cents.

Forcing homeowners to keep shoveling more property tax dollars into broken pension systems has become a morally bankrupt solution to the problem.

In Springfield, for example, residents already contribute four times more money into police, fire and municipal employee pensions than do the employees.

The problem is that, in Illinois, state politicians mandate pension benefits for local government workers, with little regard to fairness for local taxpayers.

Many communities would prefer not to pay the high cost of workers enjoying early retirement ages, health insurance benefits normal residents could never afford, and annual 3 percent cost-of-living adjustments that private-sector workers could only dream of.

So how can the state protect homeowners?

Forcing local governments to begin to live within their means through a property-tax freeze, as has been proposed by Gov. Bruce Rauner, is necessary. But solving the root cause of the property-tax problem will require further reform, such as moving all new government workers from defined-benefit to self-managed retirement plans, transferring the power to negotiate pension benefits down to local leaders, and encouraging aggressive consolidation and resource-sharing across units of local government. For some communities, the only option to undo decades of mismanagement will be bankruptcy.

Until sincere efforts are made at reform, Illinoisans will continue to live in fear: taxpayers of being squeezed out of their homes, and government workers of pension payments that may never come.

by Austin Berg | Chicago Tribune

After years of financial woes, Lindsey Yates and her husband had to at last address the nagging question: Should they stay or should they go?

The young couple’s continued residency in Chicago was threatened by new obstacles every few months. First came the rising property taxes, then the stress of finding a decent school for their 2-year-old son in a neighborhood they could afford.

Three weeks ago, Yates and her family hit the road, leaving the South Loop and successful careers in the rearview mirror as they headed toward their new house in a Denver suburb.

“The thing that boggles my mind: How is it that a dentist and a business professional and their one young son” can’t make it work financially? Yates asked from the road, at a pit stop in Nebraska, where her in-laws are living. “If we can’t make it work, who can?” she asked.

By almost every metric, Illinois’ population is sharply declining, largely because residents are fleeing the state. The Tribune surveyed dozens of former residents who’ve left within the last five years, and each offered their own list of reasons for doing so. Common reasons include high taxes, the state budget stalemate, crime, the unemployment rate and the weather. Census data released Thursday suggest the root of the problem is in the Chicago metropolitan area, which in 2015 saw its first population decline since at least 1990.

Chicago’s metropolitan statistical area, defined by the U.S. Census Bureau, includes the city and suburbs and extends into Wisconsin and Indiana.

The Chicago area lost an estimated 6,263 residents in 2015 — the greatest loss of any metropolitan area in the country. That puts the region’s population at 9.5 million.

While the numbers fell overall, there were some bright spots in the Chicago area: Will, Kane, McHenry and Kendall counties saw growth spurts, according to census data.

A crumbling, dangerous South Side creates exodus of black Chicagoans

The Chicago region’s decline extended to the state. In fact, Illinois was one of just seven states to see a population dip in 2015, and had the second-greatest decline rate last year after West Virginia, census data show. While the state’s population dropped by 7,391 people in 2014, the number more than tripled in 2015, to 22,194.

The plunge is mainly a result of the large number of residents leaving the state last year — about 105,200 in all — which couldn’t be offset by new residents and births, according to census data. The last year Illinois saw its population plunge was 1988.

The potential fallout is both political and financial. Federal and state government dollars are often distributed to local government agencies based on population; so the population loss creates long-term budget concerns. Communities pouring millions into new roads and schools, for example, based on rosy projections of future growth are left with fewer taxpayers to cover the cost.

Sights set on sun

Illinois has a long-standing pattern of losing residents to other states, but the loss has generally been offset by births and migration from other countries. Residents are mostly flocking to Sun Belt states — those with the country’s warmest climates, such as Nevada, Arizona and Florida.

During the years after the economic recession of the mid-2000s, migration to those states slowed, but it’s heated up again as states in the South and West have sunnier job opportunities and affordable housing.

“The old Snow Belt-to-Sun Belt movement is picking back up again, and movement south and west is fueling up,” said William Frey, a demographer with the Brookings Institution who analyzes census data.

Richard Morton, an Illinois resident of 62 years, is building a house in Panama City Beach, Fla., and plans to move into it in March 2017.

“We’ll say ‘hasta la vista, Illinois.’ I say that rather humorously, but I’m really rather sad about it,” he said. “My mother was born in Illinois. My grandparents lived their entire lives in Downers Grove.”

The clear draw for Morton is Florida’s weather but also what he calls an “attractive economy.”

“I used to enjoy Illinois and the area,” he said. “But everyday there’s a reason to not want to stay here. Between (Gov. Bruce) Rauner and (House Speaker Michael) Madigan, how will the state ever fix its pension problem? To me it seems unfixable, and I don’t want to have to pay for it.”

Texas attracts the greatest number of Illinois residents, followed by Florida, Indiana, California and Arizona, according to 2013 IRS migration data. Weather isn’t the only reason people are leaving the state.

More Illinois residents move to other Midwestern states than the number of Midwesterners moving to Illinois, said Michael Lucci, vice president of policy at the right-leaning Illinois Policy Institute. Job and business creation are simply stronger in neighboring states, he said.

“We talk opportunity all the time. If you’re moving to California, you might be a tech worker, or you might be someone who likes sunshine,” he said. “But when you see Illinois losing people to every Midwestern state, you know it’s not weather. People are moving for economic reasons.”

Through the 1990s and 2000s, Illinois saw what demographers consider normal rates of exodus for the state, about 50,000 to 70,000 more residents moving away from the state than moving in. But in 2015, the number spiked to about 95,000, and in 2015 it reached more than 100,000 people, according to census data.

Several moving companies that examine industry trends found high numbers of Illinoisans moving out of state. Allied Van Lines this year ranked Illinois No. 2 on its list of states with greatest outbound moves with 1,240, said spokeswoman Violette Sieczka. The numbers are limited to the movement of entire households.

The loss of residents over the last 20 years translates to about $50 billion in lost taxable income, and about $8 billion each year in lost state and local tax revenues, Lucci said.

“Frankly, we have this state budget problem, and it would be a lot less of a problem if we had all these people,” he said. “Growth makes problems better, out-migration makes problems worse.”

Losing faith in city

The main factors in Chicago’s population dip are diminished immigration, the aging of the Mexican immigrant population that bolstered the city throughout the 1990s as well as an exodus of African-Americans, experts say.

More than any other city, Chicago has depended on Mexican immigrants to balance the sluggish growth of its native-born population, said Rob Paral, a Chicago-based demographer who advises nonprofits and community groups. During the 1990s, immigration accounted for most of Chicago’s population growth. The number of Mexican immigrants rose by 117,000 in Chicago that decade, according to data gathered by Paral’s firm, Rob Paral and Associates.

After 2007, falling Mexican-born populations became a trend across the country’s major metropolitan areas. But most of those cities were able to make up for the loss with the growth of their native populations, Paral said. Chicago couldn’t.

Some experts also attribute the decline to the city’s African-American population, in part because of historically black communities hit hard by the foreclosure crisis, making houses cheap and easy to buy for Hispanics and whites who were willing to move for a bargain.

The 2010 census reported a 17 percent drop in the city’s black population over the previous decade. That number declined another an additional 4 percent through 2014, to 852,756.

“White people have left the state for years,” Paral said. “But African-Americans? That’s the one-two punch.”

Chicago residents leaving the state have cited the Chicago Public Schools’ financial crisis and the city’s red light camera controversy as motivating factors. The greatest concern, however, seems to be safety. Despite being the nation’s third most populous city, Chicago outpaces New York City and Los Angeles in the number of homicides and shootings, though it fares better than some smaller cities on a per capita comparison.

Melissa Koski, who moved to Arizona in 2008, said she left after being the victim of two crimes. One involved a break-in at her University Village neighborhood apartment while she slept, and the second involved being robbed at gunpoint near Grand and Milwaukee avenues with her mother.

“He got a whopping $40, but I still remember his smell and can feel his sweaty body wrapped around mine, with what felt like a gun pressed to my back,” she said.

Pat and Anna van Slee, longtime residents of the Uptown neighborhood, spent Thursday morning packing their house, preparing for their move to Thousand Oaks, Calif.

Their last apartment was in a six-flat that saw a series of crimes in and around the building in recent years. In one instance, a neighbor was mugged outside the complex; in another, a homeless man seeking shelter in the complex’s basement crawled through the window of the van Slees’ downstairs neighbor, Anna van Slee said.

“We’ve always lived in developing neighborhoods, but when you have a baby it makes you look at things differently,” Anna van Slee said, referring to her son, 4-month-old Orion. While the couple is moving primarily because of job opportunities, they’re glad to not have to enroll Orion in a CPS school, either, they said.

“Oddly, this was a safer neighborhood when it was rougher. It didn’t have some of the tension there is now, when million-dollar condos are going up next to subsidized housing,” she said.

Stemming the tide

There are things that can be done in coming years to mitigate the further exodus of residents from the state, said Lucci, of the Illinois Policy Institute. He recommends refocusing on manufacturing jobs in the state and curbing property taxes.

“We’re never gonna have Colorado’s mountains or California’s beaches,” he said. “But we have historically had an attractive business and job market. The problem is that we don’t have that anymore.”

Indeed, the employment rate is an issue: Illinois this year is tied with West Virginia for the 46th worst employment rate of all states, at 6.3 percent, according to Bureau of Labor Statistics.

“People are leaving Illinois because we rank near the bottom in job growth in the Midwest and have among the highest property taxes in America,” Catherine Kelly, a spokeswoman for Rauner, wrote in an emailed statement. “We have to make structural changes in Illinois to ensure talented people — many of whom run businesses — stay in Illinois to help grow the economy and improve our state’s future.”

In response to the decline in the region’s census numbers, Mayor Rahm Emanuel’s office issued a statement, saying the mayor was “working hard to build the Chicago economy of tomorrow by investing in a diverse economy and highly educated workforce that will continue to bring jobs and people to Chicago.”

It’s important that communities engage in careful discussion about cutbacks, and begin planning for smaller populations and smaller economic growth, said Eric Zeemering, a professor at Northern Illinois University’s School of Public and Global Affairs. But those discussions tend to be difficult and unpopular, he said.

“When politicians are focused on their next elections, it’s hard to have conversations about cutbacks and the realistic budgetary future,” Zeemering said.

In the meantime, he expects local leaders will make efforts to promote and advertise their towns as great places to live. The goal is that these communities will keep their residents despite the state’s problems.

“At the end of the day, some people are happy to live in snowy weather,” Zeemering said. “We don’t want to be a state people view in a negative light.”

Houses in Chicago’s Beverly neighborhood (Warren Skalski / Chicago Tribune)

Illinois still has the second-highest property taxes in the nation, according to a survey by personal finance website WalletHub.

Only New Jersey has a higher effective property tax rate, the survey found.

Though property taxes vary from county to county across the state, the average effective rate in Illinois — the proportion of the value of a home that a homeowner must pay each year in taxes — was 2.25 percent, just a hair below the New Jersey rate of 2.29 percent.

Hawaii has the lowest effective property tax rate in the nation at 0.28 percent, WalletHub found. But before you rush to move to Honolulu, bear in mind that the median Hawaiian home costs $504,500, nearly three times as much as the median Illinois home.

“Over their lifetimes, some Illinois residents end up paying more in property taxes than the value of their home.” – Governor Bruce Rauner

Missouri had a median effective property tax rate of 1 percent, WalletHub calculated. Most of the lowest property tax states are in the South and West.

Gov. Bruce Rauner has complained that Illinois’ high property tax rates mean that, over their lifetimes, some Illinois residents end up paying more in property taxes than the value of their home.

Previous surveys by the conservative-leaning Tax Foundation and the nonpartisan Tax Policy Center have also found that Illinois has some of the nation’s highest property taxes.