But what will happen to banks and automakers when the cycle turns?

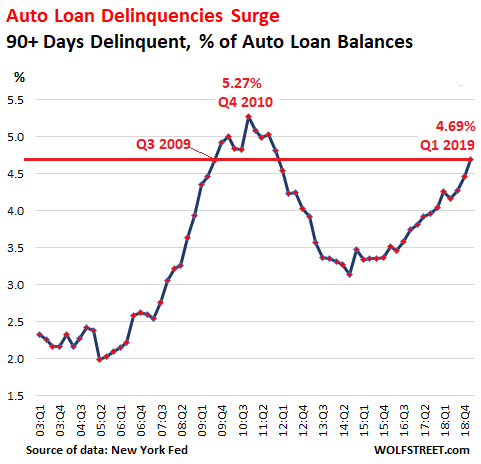

Serious auto-loan delinquencies – 90 days or more past due – jumped to 4.69% of outstanding auto loans and leases in the first quarter of 2019, according toNew York Fed data. This put the auto-loan delinquency rate at the highest level since Q4 2010 and merely 58 basis points below the peak during the Great Recession in Q4 2010 (5.27%):

Back in 2007/2008, Wall Street drastically pulled back on mortgage origination for their own balance sheets while ramping up their issuance of RMBS securities. Of course, the goal was very simple: package up all the mortgage-related nuclear waste on your balance sheet into a pretty package, tie a ribbon around it with that AAA-rating from Moody’s and sell it all to unsuspecting pension funds and insurance companies around the globe.

Both banks have grown more reluctant to make new subprime loans using money from their own balance sheets. Wells Fargo tightened its underwriting standards and slashed the volume of all loans it made to car buyers in the first quarter by 29 percent after greater numbers of borrowers fell behind on payments. JPMorgan’s consumer and community banking head Gordon Smith earlier this year said the bank had cut its new lending for subprime auto loans “dramatically.”

At the same time the firms are indirectly funding billions of dollars of the loans by helping companies like Santander Consumer USA Holdings Inc. borrow in the asset-backed securities market, essentially shunting money from bond investors to finance companies. Wall Street banks packaged more loans from finance companies into bonds in the first quarter than the same period last year, and Wells Fargo and JPMorgan remained two of the top underwriters of the securities.

Of course, with only ~$200 billion of auto ABS outstanding, compared to $9 trillion in RMBS, the auto loan market hardly represents the same “systemic risk” to the financial industry today as mortgage loans did back in 2007. That said, deterioration in lending standards could certainly wreak havoc on consumers, investors and the auto industry which will undoubtedly have ripple effects throughout the economy.

The risks to Wall Street firms from subprime auto bonds are smaller. Big banks provide lines of credit to finance companies that make subprime loans, but these tend to be a small part of major firms’ balance sheets. The auto loan bond market is much smaller, too: there were just $192.3 billion of securities backed by auto loans, including prime and subprime, outstanding at the end of March according to the Securities Industry and Financial Markets Association, compared with around $8.9 trillion of residential mortgage bonds at the end of last year.

Banks might not get hurt much by subprime auto securities, but for investors who buy them, the risks are growing. Subprime borrowers are falling behind on their car loan payments at the highest rate since the financial crisis. General Motors Co. expects car prices to drop 7 percent this year and auto lender Ally Financial Inc. reported last month that prices fell that much during its first quarter, so the value of the loans’ collateral is dropping. Even Wells Fargo’s analysts who look at bonds backed by car loans cautioned in March that it may be a good time for investors to cut their exposure.

And while JPM and Wells are pulling back on their own auto loan underwriting, we wonder whether they’re sharing these details regarding auto loan delinquencies with new buyers of their sparkling auto ABS securities?

Or the fact that loss severities are also starting to rise…

Oh well, losses are never possible on those highly-engineered, complex wall street structures…until they are.

In the history of data from The Fed, this has never happened before…

Aggregate Auto Loan volume actually fell last week… And less loans means one simple thing… less sales (because prices have never been higher and no one is paying cash)…

Which is a major problem since motor vehicle production continues to rise as management is blindly belieiving the Hillbama narrative that everything is (and will be) awesome.

The problem is… inventories are already at near record highs relative to sales (which are anything but plateauing)…

In fact, the last time inventories were this high relative to sales, GM went bankrupt and was bailed out by Obama.

The big picture here is simple… US Automakers face a plunge in auto loans for the first time in this ‘recovery’, and with sales plunging and inventories near record highs, production (i.e. labor) will have to take a hit… and that plays right into Trump’s wheelhouse and crushes Hillbama’s narrative just weeks before the election.

Rising interest rates are a negative for real estate.

Gold and oil are still dropping.

Company earnings are not beating expectations.

So, where do we begin?

The economy has been firing on all eight cylinders for several years now. So long, in fact, that many do not or cannot accept the fact that all good things must come to an end. Since the 2008 recession, the only negative that has remained constant is the continuing dilemma of the “underemployed”.

Let me digress for a while and delve into the real issues I see as storm clouds on the horizon. Below are the top five storms I see brewing:

Real estate

Subprime auto loans

Falling commodity prices

Stalling equity markets and corporate earnings

Unpaid student loan debt

1. Real Estate

Just this past week there was an article detailing data from the National Association of Realtors (NAR), disclosing that existing home sales dropped 10.5% on an annual basis to 3.76 million units. This was the sharpest decline in over five years. The blame for the drop was tied to new required regulations for home buyers. What is perplexing about this excuse is NAR economist Lawrence Yun’s comments. The article cited Yun as saying that:

“most of November’s decline was likely due to regulations that came into effect in October aimed at simplifying paperwork for home purchasing. Yun said it appeared lenders and closing companies were being cautious about using the new mandated paperwork.”

Here is what I do not understand. How can simplifying paperwork make lenders “more cautious about using… the new mandated paperwork”?

Also noted was the fact that median home prices increased 6.3% in November to $220,300. This comes as interest rates are on the cusp of finally rising, thus putting pressure (albeit minor) on monthly mortgage rate payments. This has the very real possibility of pricing out investors whose eligibility for financing was borderline to begin with.

2. Subprime auto loans

Casey Research has a terrific article that sums up the problems in the subprime auto market. I strongly suggest that you read the article. Just a few of the highlights of the article are the following points:

The value of U.S. car loans now tops $1 trillion for the first time ever. This means the car loan market is 47% larger than all U.S. credit card debt combined.

According to the Federal Reserve Bank of New York, lenders have approved 96.7% of car loan applicants this year. In 2013, they only approved 89.7% of loan applicants.

It’s also never been cheaper to borrow. In 2007, the average rate for an auto loan was 7.8%. Today, it’s only 4.1%.

For combined Q2 2015 and Q3 2015, 64% of all new auto loans were classified as subprime.

The average loan term for a new car loan is 67 months. For a used car, the average loan term is 62 months. Both are records.

The only logical conclusion that can be derived is that the finances of the average American are still so weak that they will do anything/everything to get a car. Regardless of the rate, or risks associated with it.

3. Falling commodity prices

Remember $100 crude oil prices? Or $1,700 gold prices? Or $100 ton iron ore prices? They are all distant faded memories. Currently, oil is $36 a barrel, gold is $1,070 an ounce, and iron ore is $42 a ton. Commodity stocks from Cliffs Natural Resources (NYSE:CLF) to Peabody Energy (NYSE:BTU) (both of which I have written articles about) are struggling to pay off debt and keep their operations running due to the declines in commodity prices. Just this past week, Cliffs announced that it sold its coal operations to streamline its business and strengthen its balance sheet while waiting for the iron ore business to stabilize and or strengthen. Similarly, oil producers and metals mining/exploration companies are either going out of business or curtailing their operations at an ever increasing pace.

For 2016, Citi’s predictions commodity by commodity can be found here. Its outlook calls for 30% plus returns from natural gas and oil. Where are these predictions coming from? The backdrop of huge 2015 losses obviously produced a low base from which to begin 2016, but the overwhelming consensus is for oil and natural gas to be stable during 2016. This is clearly a case of Citi sticking its neck out with a prediction that will garnish plenty of attention. Give it credit for not sticking with the herd mentality on this one.

4. Stalling equity markets and corporate earnings

Historically, the equities markets have produced stellar returns. According to an article from geeksonfinace.com, the average return in equities markets from 1926 to 2010 was 9.8%. For 2015, the markets are struggling to erase negative returns. Interestingly, the Barron’s round table consensus group predicted a nearly 10% rise in equity prices in 2015 (which obviously did not materialize) and also repeated that bullish prediction for 2016 by anticipating an 8% return in the S&P. So what happened in 2015? Corporate earnings were not as robust as expected. Commodity prices put pressure on margins of commodity producing companies. Furthermore, there are headwinds from external market forces that are also weighing on the equities markets. As referenced by this article which appeared on Business Insider, equities markets are on the precipice of doing something they have not done since 1939: see negative returns during a pre-election year. Per the article, on average, the DJIA gains 10.4% during pre-election years. With less than one week to go in 2015, the DJIA is currently negative by 1.5%

5. Unpaid student loan debt

Once again, we have stumbled upon an excellent Bloomberg article discussing unpaid student loan debt. The main takeaway from the article is the fact that “about 3 million parents have $71 billion in loans, contributing to more than $1.2 trillion in federal education debt. As of May 2014, half of the balance was in deferment, racking up interest at annual rates as high as 7.9 percent.” The rate was as low as 1.8 percent just four years ago. It is key to note that this is debt that parents have taken out for the education of their children and does not include loans for their own college education.

The Institute for College Access & Success released a detailed 36 page analysis of what the class of 2014 faces regarding student debt. Some highlights:

69% of college seniors who graduated from public and private non-profit colleges in 2014 had student loan debt.

Average debt at graduation rose 56 percent, from $18,550 to $28,950, more than double the rate of inflation (25%) over this 10-year period.

Conclusion

So, what does this all mean?

To look at any one or two of the above categories and see their potential to stymie the economy, one would be smart to be cautious. To look at all five, one needs to contemplate the very real possibility of these creating the beginnings of another downturn in the economy. I strongly suggest a cautious and conservative investment outlook for 2016. While the risk one takes should always be based on your own risk tolerance levels, they should also be balanced by the very real possibility of a slowing economy which may also include deflation. Best of health and trading to all in 2016!

Rodney Durham stopped working in 1991, declared bankruptcy and lives on Social Security. Nonetheless, Wells Fargo lent him $15,197 to buy a used Mitsubishi sedan.

“I am not sure how I got the loan,” Mr. Durham, age 60, said.

Mr. Durham’s application said that he made $35,000 as a technician at Lourdes Hospital in Binghamton, N.Y., according to a copy of the loan document. But he says he told the dealer he hadn’t worked at the hospital for more than three decades. Now, after months of Wells Fargo pressing him over missed payments, the bank has repossessed his car.

This is the face of the new subprime boom. Mr. Durham is one of millions of Americans with shoddy credit who are easily obtaining auto loans from used-car dealers, including some who fabricate or ignore borrowers’ abilities to repay. The loans often come with terms that take advantage of the most desperate, least financially sophisticated customers. The surge in lending and the lack of caution resemble the frenzied subprime mortgage market before its implosion set off the 2008 financial crisis.

Auto loans to people with tarnished credit have risen more than 130 percent in the five years since the immediate aftermath of the financial crisis, with roughly one in four new auto loans last year going to borrowers considered subprime — people with credit scores at or below 640.

The explosive growth is being driven by some of the same dynamics that were at work in subprime mortgages. A wave of money is pouring into subprime autos, as the high rates and steady profits of the loans attract investors. Just as Wall Street stoked the boom in mortgages, some of the nation’s biggest banks and private equity firms are feeding the growth in subprime auto loans by investing in lenders and making money available for loans.

And, like subprime mortgages before the financial crisis, many subprime auto loans are bundled into complex bonds and sold as securities by banks to insurance companies, mutual funds and public pension funds — a process that creates ever-greater demand for loans.

The New York Times examined more than 100 bankruptcy court cases, dozens of civil lawsuits against lenders and hundreds of loan documents and found that subprime auto loans can come with interest rates that can exceed 23 percent. The loans were typically at least twice the size of the value of the used cars purchased, including dozens of battered vehicles with mechanical defects hidden from borrowers. Such loans can thrust already vulnerable borrowers further into debt, even propelling some into bankruptcy, according to the court records, as well as interviews with borrowers and lawyers in 19 states.

In another echo of the mortgage boom, The Times investigation also found dozens of loans that included incorrect information about borrowers’ income and employment, leading people who had lost their jobs, were in bankruptcy or were living on Social Security to qualify for loans that they could never afford.

Photo

Credit

Many subprime auto lenders are loosening credit standards and focusing on the riskiest borrowers, according to the examination of documents and interviews with current and former executives from five large subprime auto lenders. The lending practices in the subprime auto market, recounted in interviews with the executives and in court records, demonstrate that Wall Street is again taking on very risky investments just six years after the financial crisis.

The size of the subprime auto loan market is a tiny fraction of what the subprime mortgage market was at its peak, and its implosion would not have the same far-reaching consequences. Yet some banking analysts and even credit ratings agencies that have blessed subprime auto securities have sounded warnings about potential risks to investors and to the financial system if borrowers fall behind on their bills.

Pointing to higher auto loan balances and longer repayment periods, the ratings agency Standard & Poor’s recently issued a report cautioning investors to expect “higher losses.” And a high-ranking official at the Office of the Comptroller of the Currency, which regulates some of the nation’s largest banks, has also privately expressed concerns that the banks are amassing too many risky auto loans, according to two people briefed on the matter. In a June report, the agency noted that “these early signs of easing terms and increasing risk are noteworthy.”

Despite such warnings, the volume of total subprime auto loans increased roughly 15 percent, to $145.6 billion, in the first three months of this year from a year earlier, according to Experian, a credit rating firm.

“It appears that investors have not learned the lessons of Lehman Brothers and continue to chase risky subprime-backed bonds,” said Mark T. Williams, a former bank examiner with the Federal Reserve.

In their defense, financial firms say subprime lending meets an important need: allowing borrowers with tarnished credits to buy cars vital to their livelihood.

Lenders contend that the risks are not great, saying that they have indeed heeded the lessons from the mortgage crisis. Losses on securities made up of auto loans, they add, have historically been low, even during the crisis.

Autos, of course, are very different than houses. While a foreclosure of a home can wend its way through the courts for years, a car can be quickly repossessed. And a growing number of lenders are using new technologies that can remotely disable the ignition of a car within minutes of the borrower missing a payment. Such technologies allow lenders to seize collateral and minimize losses without the cost of chasing down delinquent borrowers.

That ability to contain risk while charging fees and high interest rates has generated rich profits for the lenders and those who buy the debt. But it often comes at the expense of low-income Americans who are still trying to dig out from the depths of the recession, according to the interviews with legal aid lawyers and officials from the Federal Trade Commission and the Consumer Financial Protection Bureau, as well as state prosecutors.

While the pain from an imploding subprime auto loan market would be much less than what ensued from the housing crisis, the economy is still on relatively fragile footing, and losses could ultimately stall the broader recovery for millions of Americans.

Photo

Rodney Durham, 60, of Binghamton, N.Y., had his car repossessed.Credit Heather Ainsworth for The New York Times

The pain is far more immediate for borrowers like Mr. Durham, the unemployed car buyer from Binghamton, N.Y., who stopped making his loan payments in March, only five months after buying the 2010 Mitsubishi Galant. A spokeswoman for Wells Fargo, which declined to comment on Mr. Durham citing a confidentiality policy, emphasized that the bank’s underwriting is rigorous, adding that “we have controls in place to help identify potential fraud and take appropriate action.”

The Mitsubishi was repossessed last month, leaving Mr. Durham without a car. But his debt ordeal may not be over.

Some lenders go after borrowers like Mr. Durham for the debt that still remains after a repossessed car is sold, according to court filings. Few repossessed cars fetch enough when they are resold to cover the total loan, the court documents show. To get the remainder, some lenders pursue the borrowers, which can leave them shouldering debts for years after their cars are gone.

But for now, Mr. Durham, who is disabled, has a more immediate problem.

“I just can’t get around without my car,” he said.

The Brokers

Outside, the banner proclaimed: “No Credit. Bad Credit. All Credit. 100 percent approval.” Inside the used-car dealership in Queens, N.Y., Julio Estrada perfected his sales pitches for the borrowers, including some immigrants who spoke little English.

Sure, the double-digit interest rates might seem steep, Mr. Estrada told potential customers, but with regular payments, they would quickly fall. Mr. Estrada, who sometimes went by John, and sometimes by Jay, promised others cash rebates.

If the soft sell did not work, he played hardball, threatening to keep the down payments of buyers who backed out, according to court documents and interviews with customers.

The salesman was ultimately indicted by the Queens district attorney on grand larceny charges that he defrauded more than 23 car buyers with refinancing schemes.

Relatively few used-car dealers are charged with fraud. Yet the extreme example of Mr. Estrada comes as some used-car dealers — a business that has long had a reputation for aggressive pitches — are pushing sales tactics too far, according to state prosecutors and federal regulators.

And these are among the thousands of used-car dealers who are working hand-in-hand with Wall Street to sell cars. Court records show that Capital One and Santander Consumer USA all bought loans arranged by Mr. Estrada, who pleaded guilty last year. Since then, Mr. Estrada was indicted on separate fraud charges in March by Richard A. Brown, the Queens district attorney. That case is still pending.

To guard against fraud, the banks say, they vet their dealer partners and routinely investigate complaints. Capital One has “rigorous controls in place to identify any potential issues,” said Tatiana Stead, a bank spokeswoman, adding that last year “we terminated our relationship with the dealership” where Mr. Estrada worked. Dawn Martin Harp, head of Wells Fargo Dealer Services, said that “it’s important to note that not all claims of dealer fraud turn out to be fraud.”

James Kousouros, Mr. Estrada’s lawyer, said that “for those individuals for whom Mr. Estrada bore responsibility, he accepted this and is committed to the restitution agreed to.” Some civil lawsuits filed by borrowers were found to be without merit, he said.

For their part, car dealers note that like any industry they sometimes have rogue employees, but add that customers are overwhelmingly treated fairly.

“There is no place for fraud or any other nefarious activities in the industry, especially tactics that seek to take advantage of vulnerable consumers,” said Steve Jordan, executive vice president of the National Independent Automobile Dealers Association.

In their role as matchmaker between borrowers and lenders, used-car dealers wield tremendous power. They make the pitch to customers, including many troubled borrowers who often believe that their options are limited. And the dealers outline the terms and rates of the loans.

In interviews, more than 40 low-income borrowers described how they were worn down by used car dealers who kept them in suspense for hours before disclosing whether they even qualified for a loan. The seemingly interminable wait, the borrowers said, left them with the impression that the loan — no matter how onerous the terms — was their only chance.

The loans also came with other costs, according to interviews and an examination of the loan documents, including add-on products like unusual insurance policies. In many cases, the examination by The Times found, borrowers ended up shouldering loans that far exceeded the resale value of the car. A reason for that disparity is that some borrowers still owe money on cars that they are trading in when they purchase a new one. That debt is then rolled over into the new loan.

“By the end, they are paying $600 a month for a piece of junk,” said Charles Juntikka, a bankruptcy lawyer in Manhattan.

The dealers have an incentive to increase both the size and the interest rate of the loans.

The arithmetic is simple. The bigger size and rate of the loan, the bigger the dealers’ profit, or so-called markup — the difference between the rate charged by the lenders and the one ultimately offered to the borrowers. Under federal law, dealers do not have to disclose the size of the markup.

Photo

Dolores Blaylock, 51, of Austin, Tex., and her father, Fidencio Muñiz, 84. Like many buyers, she found she had unwittingly purchased an add-on — in her case, a life insurance policy.Credit Erich Schlegel for The New York Times

To buy her 2004 Mazda van, Dolores Blaylock, 51, a home health care aide in Austin, Tex., said she unwittingly paid for a life insurance policy that would cover her loan payments if she died.

Her loan totaled $13,778 — nearly three times the value of the van that she uses to shuttle her father, who uses a wheelchair, to his doctor’s appointments.

Now, Ms. Blaylock says she regrets ever buying the van, which frequently breaks down. “I am afraid to drive it out of town,” she said.

In some cases, though, the tactics veer toward outright fraud. The Times’s scrutiny of loan documents, including some produced in litigation, found that some used-car dealers submitted loan applications to lenders that contained incorrect income and employment information. As was the case in the subprime mortgage boom, it is unclear whether borrowers provided incorrect information to qualify for loans or whether the dealers falsified loan applications. Whatever the cause, the result is the same: Borrowers with scant income qualified for loans.

Mary Bridges, a retired grocery store employee in Syracuse, N.Y., said she repeatedly explained to a car salesman that her only monthly income was about $1,200 in Social Security. Still, Ms. Bridges said that the salesman falsely listed her monthly income as $2,500 on the application for a car loan submitted by a local dealer to Wells Fargo and reviewed by The Times.

As a result, she got a loan of $12,473 to buy a 2004 used Buick LeSabre, currently valued by Kelley Blue Book at around half that much. She tried to keep up with the payments — even going on food stamps for the first time in her life — but ultimately the car was repossessed in 2012, just two years after she bought it.

“I have always been told to do the responsible thing, but I said, ‘This is too much,’ ” the 76-year-old widow said.

The dealer agreed to pay Ms. Bridges $1,000 after Syracuse University law students threatened to file a lawsuit accusing the company of violating state and federal consumer protection laws.

But Wells Fargo, which resold the car for $4,500 last July, is still pursuing Ms. Bridges for $2,900 — a total that includes her remaining loan balance and an $835 fee for “cost of repossession and sale,” according to a copy of a letter that Wells Fargo sent to Ms. Bridges last August. (Wells Fargo declined to comment on Ms. Bridges.)

Photo

Shahadat Tuhin, 42, with his daughter Sadia Oishika, 10. He says his auto dealer used deceptive practices.Credit Hiroko Masuike/The New York Times

Even when authorities have cracked down on dealers, borrowers are still vulnerable to fraud. Last June, Shahadat Tuhin, a New York City taxi driver, bought a car from Mr. Estrada, the salesman in Queens who less than a year earlier had been indicted.

The charge by the Queens district attorney didn’t keep him out of the business. While his criminal case was pending, the salesman persuaded Mr. Tuhin to buy a used car for 90 percent more than the price he agreed upon. Needing the car to take his daughter, who has a heart condition, to the doctor, Mr. Tuhin said he unwittingly signed for a $26,209 loan with completely different terms than the ones he had reviewed.

Immediately after discovering the discrepancies, Mr. Tuhin, 42, said he tried to return the car to the dealership and called the lender, M&T Bank, to notify them of the fraud.

The bank told him to take up the issue with the dealer, Mr. Tuhin said.

M&T declined to comment on Mr. Tuhin, but said it no longer does business with that dealership.

The Money

Investors, seeking a higher return when interest rates are low, recently flocked to buy a bond issue from Prestige Financial Services of Utah. Orders to invest in the $390 million debt deal were four times greater than the amount of available securities.

What is backing many of these securities? Auto loans made to people who have been in bankruptcy.

An affiliate of the Larry H. Miller Group of Companies, Prestige specializes in making the loans to people in bankruptcy, packaging them into securities and then selling them to investors.

“It’s been a hot space,” Richard L. Hyde, the firm’s chief operating officer, said during an interview in March. Investors are betting on risky borrowers. The average interest rate on loans bundled into Prestige’s latest offering, for example, is 18.6 percent, up slightly from a similar offering rolled out a year earlier. Since 2009, total auto loan securitizations have surged 150 percent, to $17.6 billion last year, though some estimates have put the total volume even higher. To meet that rising demand, Wall Street snatches up more and more loans to package into the complex investments.

Much like mortgages, subprime auto loans go through Wall Street’s securitization machine: Once lenders make the loans, they pool thousands of them into bonds that are sold in slices to investors like mutual funds, pensions and hedge funds. The slices that include loans to the riskiest borrowers offer the highest returns.

Rating agencies, which assess the quality of the bonds, are helping fuel the boom. They are giving many of these securities top ratings, which clears the way for major investors, from pension funds to employee retirement accounts, to buy the bonds. In March, for example, Standard & Poor’s blessed most of Prestige’s bond with a triple-A rating. Slices of a similar bond that Prestige sold last year also fetched the highest rating from S.&P. A large slice of that bond is held in mutual funds managed by BlackRock, one of the world’s largest money managers.

Private equity firms have also seen the opportunity in auto subprime lending. A $1 billion investment by Kohlberg Kravis Roberts & Co., Centerbridge Partners and Warburg Pincus in a large subprime lender roughly doubled in about two years. Typically, it takes private equity firms three to five years to reap significant profit on their investments.

It is not just the private equity firms and large banks that are fanning the lending boom. Major insurance companies and mutual funds, which manage money on behalf of mom-and-pop investors, are also snapping up securities backed by subprime auto loans.

While there are no exact measures of how many of these loans end up on banks’ balance sheets, interviews with consumer lawyers and analysts suggest the problem is spreading, propelled by the very structure of the subprime auto market.

The vast majority of banks largely rely on dealers to screen potential borrowers. The arrangement, which means the banks rarely meet customers face to face, mirrors how banks relied on brokers to make mortgages.

In some cases, consumer lawyers say, the banks actually ignore complaints by borrowers who accuse dealers of fabricating their income or even forging their signatures.

“Even when they are presented with clear evidence of fraud, the banks ignore it,” said Peter T. Lane, a consumer lawyer in New York. “The typical refrain is, ‘It’s not our problem, take it up with the dealer.’ ”

It could quickly become the banks’ problem, analysts say, if questionable loans sour, causing losses to multiply.

For now, the banks are not pulling back. Many are barreling further into the auto loan market to help recoup the billions in revenue wiped out by regulations passed after the 2008 financial crisis.

Wells Fargo, for example, made $7.8 billion in auto loans in the second quarter, up 9 percent from a year earlier. At a presentation to investors in May, Wells Fargo said it had $52.6 billion in outstanding car loans. The majority of those loans are made through dealerships. The bank also said that as of the end of last year, 17 percent of the total auto loans went to borrowers with credit scores of 600 or less. The bank currently ranks as the nation’s second-largest subprime auto lender, behind Capital One, according to J. D. Power & Associates.

Wells Fargo executives say that despite the surge, the credit quality of its loans has not slipped. At the May presentation, Thomas A. Wolfe, the head of Wells Fargo Consumer Credit Solutions, emphasized that the overall quality of its auto loans was improving. And Tatiana Stead, the Capital One spokeswoman, said that Capital One worked “to ensure we do not follow the market to pursue growth for growth’s sake.”

Prestige says its loans experience relatively low losses because borrowers have discharged many of their other debts in bankruptcy, freeing up more cash for their car payments. Another advantage for the lender: No matter how tough things get for troubled borrowers, federal law prevents them from escaping their bills through bankruptcy for at least another seven years.

“The vast majority of our customers have been successful with their loans and leave us with a much higher credit score,” said Mr. Hyde, Prestige’s chief operating officer.

The Risks

All it took was three months.

Dolores Jackson, a teacher’s aide in Jersey City, says she thought she could handle the $540 a month on the 2012 Chevy Malibu she bought in January 2013.

But the payments on the $27,140 loan from Exeter Finance, which is owned by Blackstone, quickly overwhelmed her, and she prepared to declare bankruptcy in April.

“I was drowning,” she said.

Other borrowers have also found themselves quickly overwhelmed by car loan payments.

Even after getting a second job at Staples, Alicia Saffold, 24, a supply technician at the Fort Benning military base in Georgia, could not afford the monthly payments on her $14,288.75 loan from Exeter. The loan, according to a copy of her loan document reviewed by The Times, came with an interest rate of nearly 24 percent. Less than a year after she bought the gray Pontiac G6, it was repossessed.

Photo

Marcelina and Jonathan Mojica, and their dog, Lilly. “The car gets more money than what we put in our fridge,” Mr. Mojica said.Credit Damon Winter/The New York Times

In the case of Marcelina Mojica and her husband, Jonathan, they are keeping up with their payments on their $19,313.45 Wells Fargo auto loan — but just barely. They are currently living in a homeless shelter in the Bronx.

“The car gets more money than what we put in our fridge,” said Mr. Mojica, 28. Such examples of distress underscore the broader strains within the subprime auto loan market.

Exeter Finance declined to comment on Ms. Saffold or Ms. Jackson, but Blackstone, its parent company, emphasized that the credit quality of its lender’s loans was improving and that it worked hard to ensure its customers received the best rates. To ensure the accuracy of loan documents, Blackstone said, employees vet both dealers and borrowers.

“Exeter Finance believes it’s important to provide people with the option to finance transportation essential to their livelihood,” said Mark Floyd, the company’s chief executive.

Still, financial firms are beginning to see signs of strain. In the first three months of this year, banks had to write off as entirely uncollectable an average of $8,541 of each delinquent auto loan, up about 15 percent from a year earlier, according to Experian.

Some investors think the time is right to start selling their holdings. Earlier this year, for example, private equity firms, including K.K.R., sold most of their stake in the subprime auto lender, Santander Consumer USA, when the lender went public. Since the company’s initial public offering, the stock has fallen more than 16 percent.

While losses from soured car loans would be far less than those on subprime mortgages, the red ink could still deal a blow to the banks not long after they recovered from the housing bust. Losses from auto loans might also cause the banks to further retrench from making other loans vital to the economic recovery, like those to small business and would-be homeowners.

In another sign of trouble ahead, repossessions, while still relatively low, increased nearly 78 percent to an estimated 388,000 cars in the first three months of the year from the same period a year earlier, according to the latest data provided by Experian. The number of borrowers who are more than 60 days late on their car payments also jumped in 22 states during that period.

As a result, some rating agencies, even those that had blessed auto loan securitizations with high ratings, are starting to question the quality of the loans backing those securities, and warn of losses that investors could suffer if the bonds start to sour. Describing the potential trouble ahead, Kevin Cole, an analyst with Standard & Poor’s, said, “We believe these trends could lead to higher losses and weakened profitability in a few years.”

If those losses materialize, they could pummel a wide range of investors, from pension funds to insurance companies to mutual funds held by Americans preparing for retirement. For the huge baby-boomer generation, including many whose savings were sapped by the 2008 crisis and the ensuing recession, any losses from the auto loan securities could deal them another setback.

“Borrowers are haunted by this debt, and it can crater their credit scores, prevent them from getting other loans and thrust them even further onto the financial margins,” said Ahmad Keshavarz, a consumer lawyer in New York.

Some borrowers are stuck making payments on loans that were fraudulently made by dealers, according to an examination of dozens of lawsuits against dealers. There are no exact measures of just how many people whose cars have been repossessed end up in this predicament, but lawyers for borrowers say that it is a growing problem, and one that points to another element of subprime auto lending.

Thanks to an amendment to the Dodd-Frank financial overhaul, the vast majority of dealers are not overseen by the Consumer Financial Protection Bureau. Since its start in 2010, the agency has earned a reputation for aggressively penalizing lenders, but it has limited authority over dealers.

The Federal Trade Commission, the agency that does oversee the dealers, has cracked down on certain questionable practices. And although the agency has won a number of cases against dealers for failing to accurately disclose car costs and other abuses, it has not taken aim at them for falsifying borrowers’ incomes, for example.

Photo

Alicia Saffold, 24, received a loan with an interest rate of nearly 24 percent. Her car was soon repossessed.Credit Tami Chappell for The New York Times

And the help is not coming fast enough for borrowers like Mr. Durham, the retiree in Binghamton; Mr. Tuhin, the taxi driver in Queens; or Ms. Saffold, the technician in Georgia.

“Buying the car was the worst decision I have ever made,” Ms. Saffold said.