Those curious who is more impacted by the sudden re-escalation in trade hostilities between the US and China can get a quick answer by looking at the market reaction to Sunday’s unexpected news: while the S&P is down barely 1%, overnight Chinese stocks plunged nearly 6%, their biggest drop in over three years, indicating just how much more sensitive to every twist and turn in trade relations Chinese stocks are.

Of course, one can counter just how smaller – and far less relevant – the Chinese stock market is in comparison to the S&P500, which is also the basis for the vast majority of household net worth for Americans, and global investors (whereas in China, it is the local housing that is far more critical and accounts for roughly 70% of household net worth).

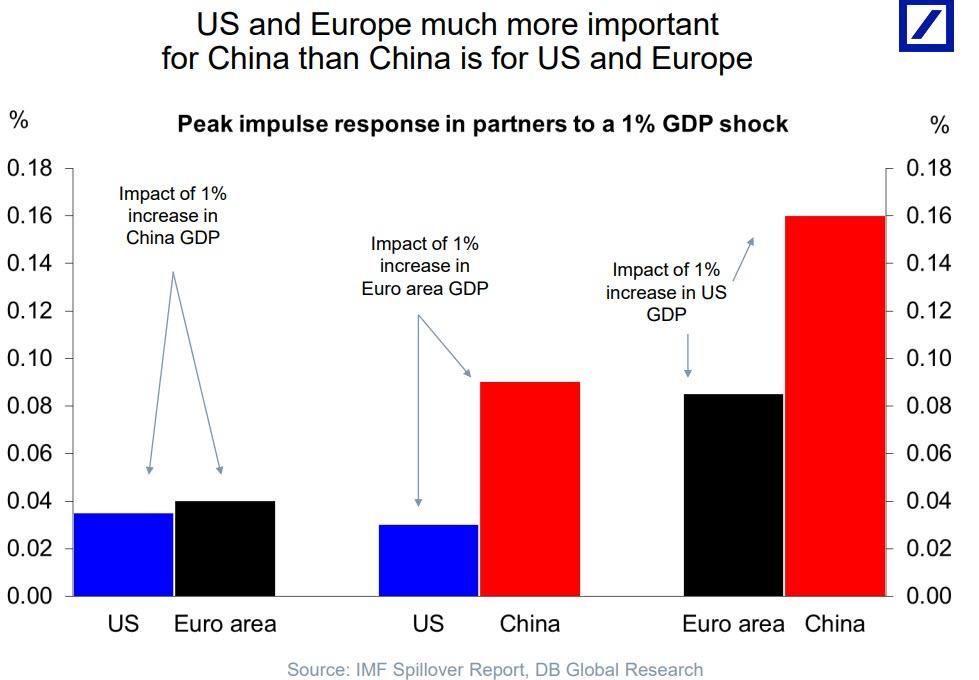

But it’s not just the stock market that shows why China should tread very lightly in its ongoing negotiations with Trump, or why the US president has decided suddenly to re-escalate. Below we lay out [ ] charts showing just why the US indeed continues to have the upper hand in negotiations with China, starting with the relative importance of the US and European economies to China rather than vice versa.

As the first chart below from Deutsche Bank shows, the US and Europe are “much more important for China than China is for US and Europe” as China remains the nation with the highest beta, or the highest relative impact, from a 1% move in either direction for either the US or the Euro area.

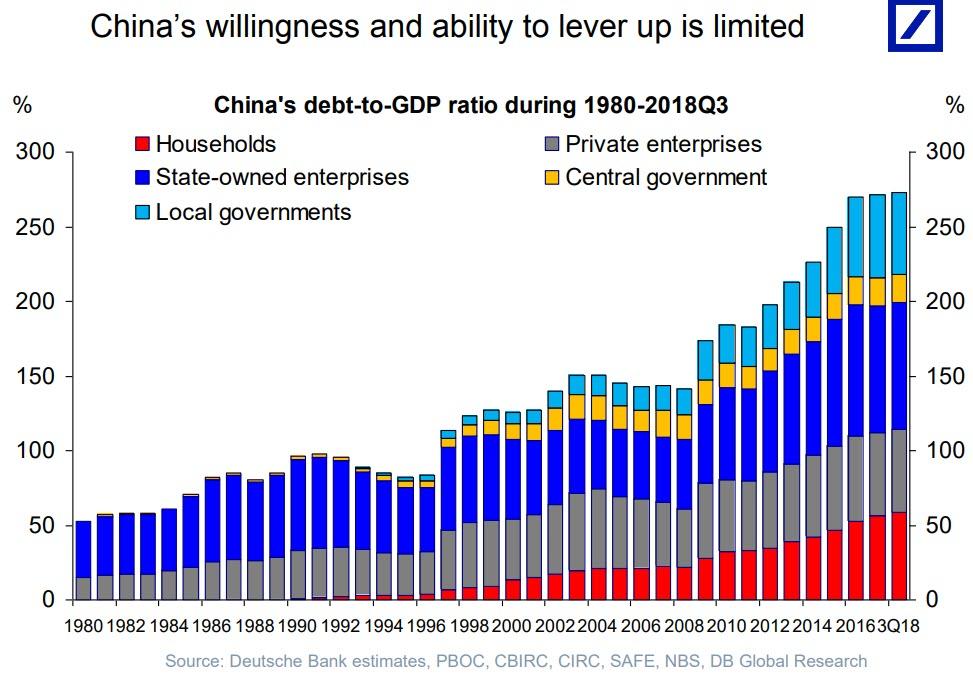

Second, whereas the US is now actively contemplating the launch of MMT, and exploding the US twin deficit by issuing virtually unlimited amounts of debt – which it ostensibly can do as long as the US Dollar is the world’s reserve currency – China is already near its leverage peak. In fact, as shown in the chart below, both China’s willingness and ability to lever up is now quite limited according to Deutsche Bank’s Torsten Slok.

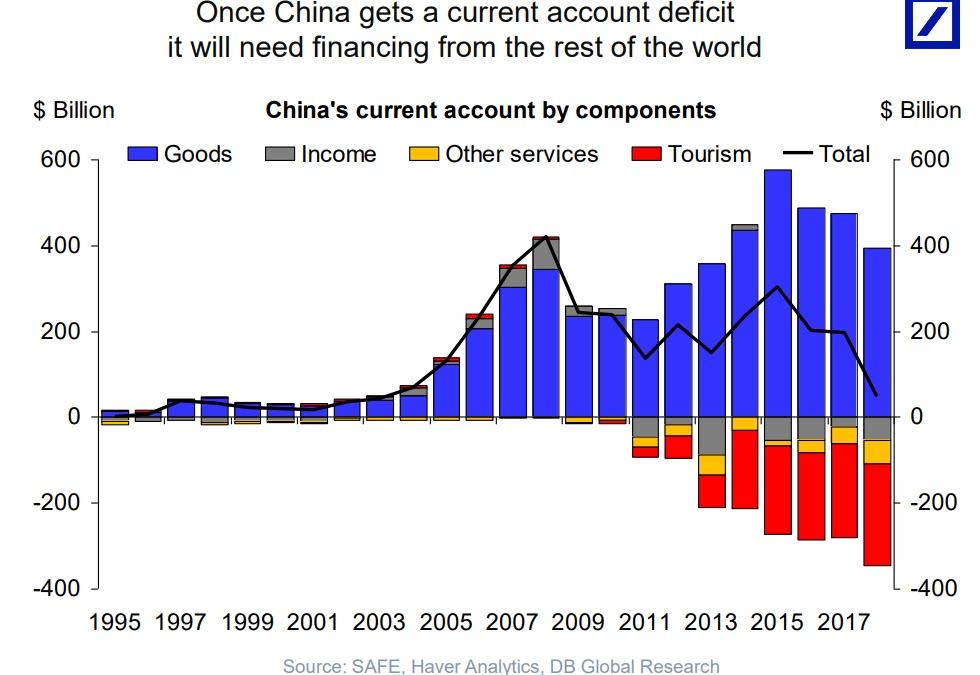

Last, and certainly not least, is what we said back in January represented a “tectonic shift” in China’s economy, when we observed that this year, for the first time in history, China’s current account deficit will turn negative meaning that China will henceforth need financing from the rest of the world, and specifically the US. Which is why, as we said five months ago, it is not Beijing that has leverage over the US, but rather the US whose ability – and desire – to allocate capital to China could mean all the difference for China’s economic growth, or lack thereof.

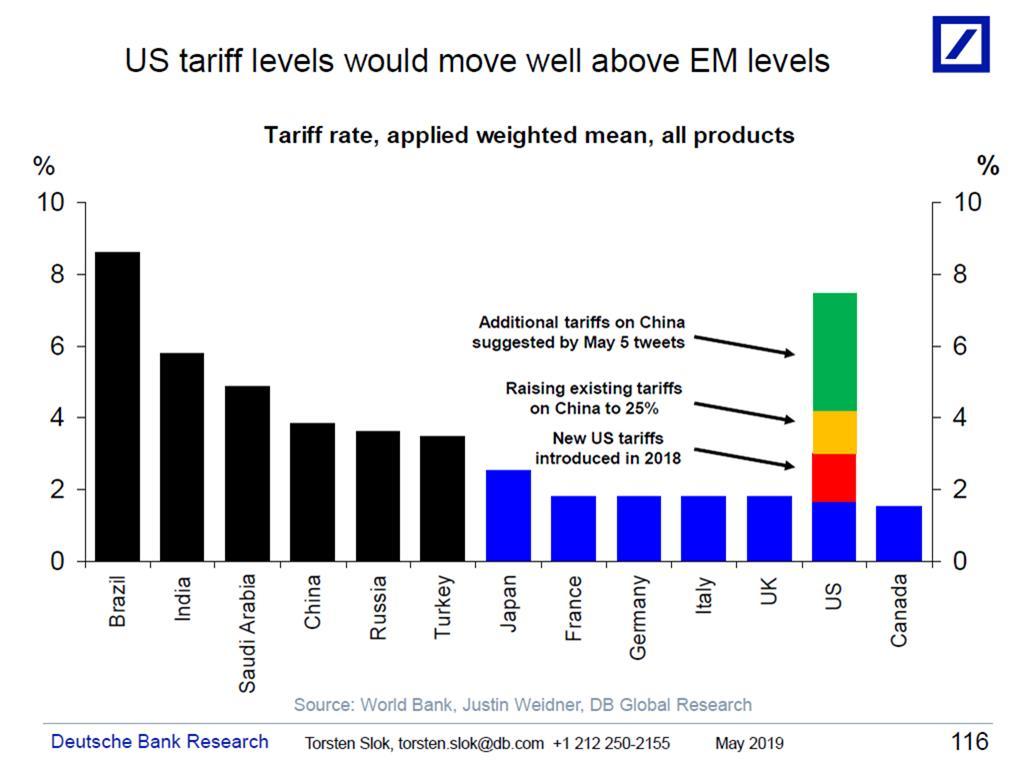

Finally, and tangentially, assuming trade talks collapse and Trump follows through on his threat of hiking taxes on Chinese imports, it would, as Torsten Slok shows in his latest chart, push US tariffs – which are already higher than most advanced economies – higher than many emerging market countries making the US one of the leading protectionist countries in the work.

That alone would cripple China’s economy, and is perhaps the main reason why Trump decided to once again flex his muscles, if so far only on twitter.