Occupancy is an engine of local economies and there’s an unprecedented glut of space available.

Occupancy is an engine of local economies and there’s an unprecedented glut of space available.

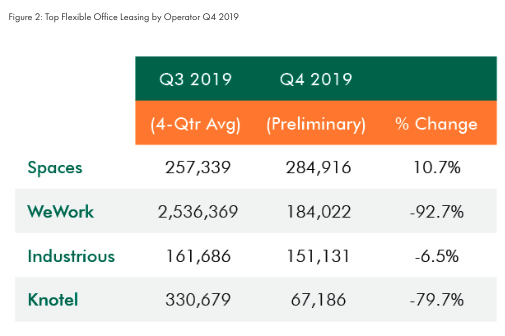

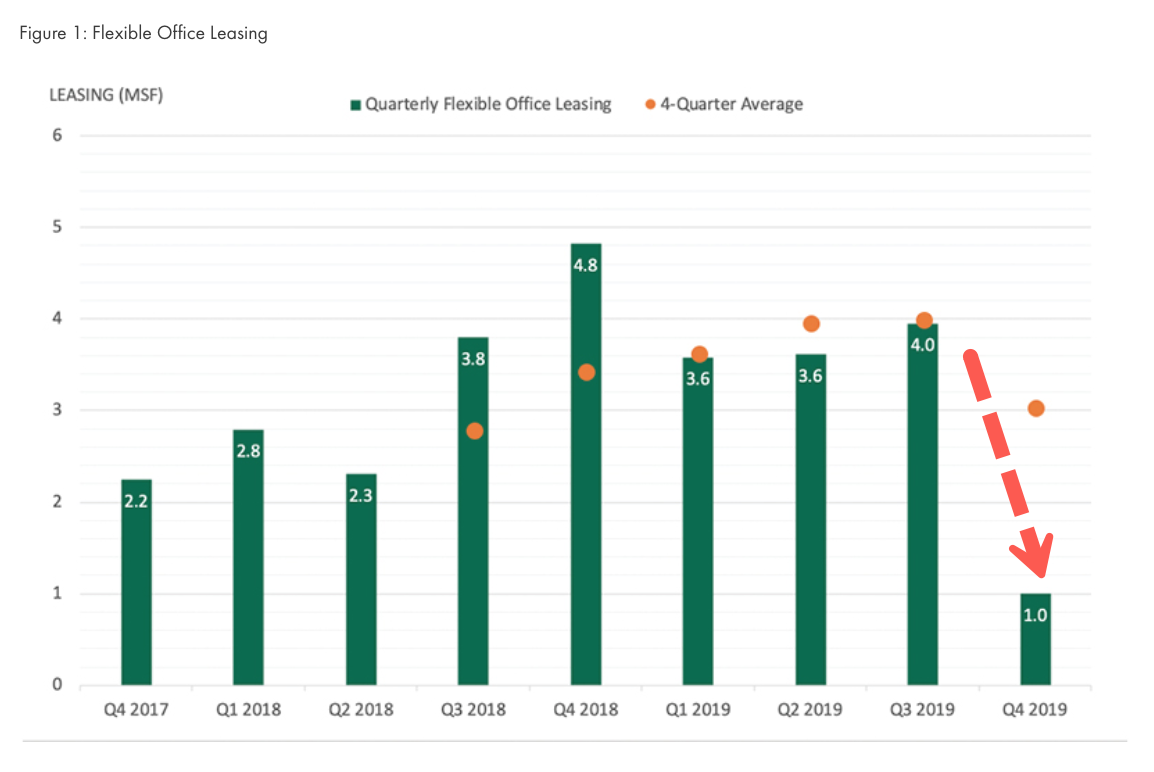

Several months after WeWork’s failed IPO — resulting in a bailout from SoftBank, the international money-losing office-sharing company leased just four new sites for a combined 184,00 sq. Ft. of space in 4Q19, marking a 93% plunge from its quarterly average rate of 2.54 million sq. Ft. over the last four quarters, according to data from real estate firm CBRE shared with CNBC.

The abrupt slowdown in leasing activity comes as the WeWork’s valuation imploded last August after it shelved its IPO and ran out of cash a month later, forcing its largest investor, SoftBank, to conduct an emergency bailout to rescue the company.

With a questionable business model and no plans on turning a profit, WeWork’s valuation plunged from $47 billion in late 2018 to $8 to $10 billion by 4Q19.

In 4Q19, WeWork had to cut costs, lay off workers, and scale back operations across the world to avoid going bankrupt. In return, the company lost the top spot in the flexible office leasing space to Regus, which in 4Q19, increased lease footprint by 11% to 284,916 sq. Ft.

CBRE showed that industrywide, there was a significant pullback in office space leasing, mainly due to WeWork’s implosion.

Data shows office sharing operators declined to 1 million sq. Ft. in 4Q19 from 4 million sq. ft. in 3Q19.

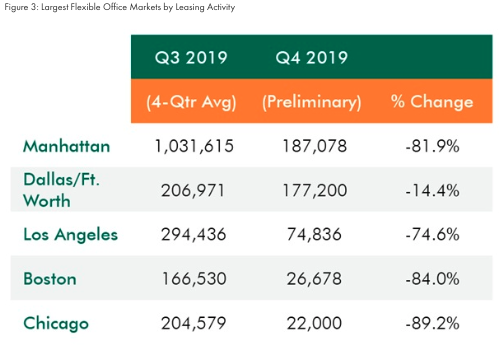

Manhattan was the top city for office sharing space, even though new space leased dropped 82% to 187,078 sq. Ft., on average, the prior four quarters. Activity in Chicago, Boston, and Los Angeles also saw notable declines over the period.

“We had seen this coming right after the IPO news,” said Julie Whelan, senior director of research at CBRE, who warned it could be a bumpy ride for WeWork and other office space sharing companies in 2020.

A darkening outlook for China’s economy continues to materialize week by week.

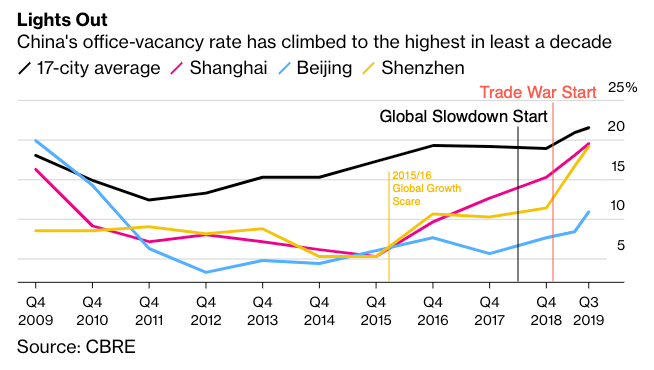

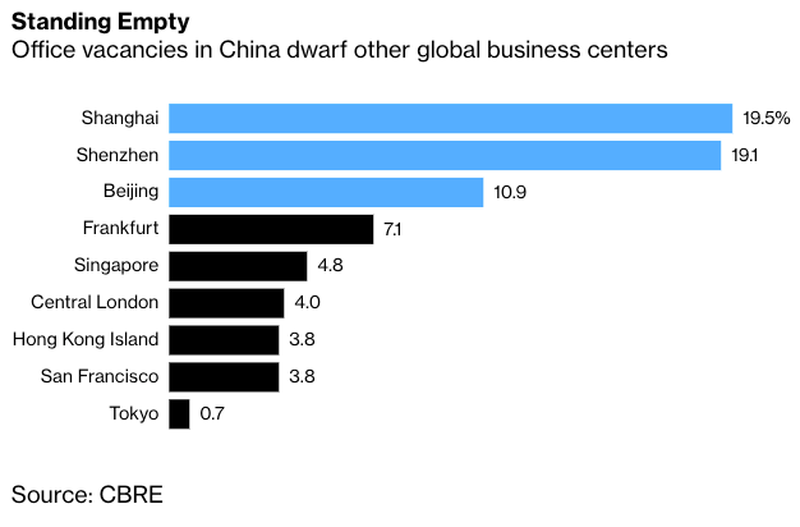

New data from commercial property group CBRE warns the country’s office vacancy rate has just surged to the highest since the financial crisis of 2007–2008, first reported by Bloomberg.

CBRE said the vacancy rate for commercial office space in 17 major cities rose to 21.5% in 3Q19, a level not seen since the global economy was melting down in 2008.

Sam Xie, CBRE’s head of research in China, said the recent “spike” in vacancies is one of the worst since the last financial crisis.

Catherine Chen, Cushman & Wakefield’s head of research for Greater China, told Financial Times that soaring commercial office vacancies in China was mainly due to dwindling demand, but not oversupplied conditions.

“Contributing factors included slower expansion of co-working operators and financial services companies, and a general cost-saving strategy adopted by most tenants given ongoing trade tensions and economic growth slowdown,” she added.

Henry Chin, head of research for Asia Pacific at CBRE, told Financial Times that macroeconomic headwinds relating to the trade war between the US and China were also a significant factor in rising office vacancies.

As shown in the Bloomberg chart below, using CBRE data, Shanghai and Shenzhen had the highest office vacancies than any other city, and both had around 20% of office spaces dormant.

And with the global economy in a synchronized slowdown, global growth estimates are now printing at 3%, the slowest pace since the financial crisis. The Chinese economy will likely continue to slow, and could see domestic growth under 6% this year. This suggests that China’s office space vacancies will continue to rise through year-end.Office Vacancies In China Hit Decade High Amid Economic Turmoil

Brookfield Asset Management has agreed to purchase the lease the office portion of 666 Fifth Ave. in midtown Manhattan from the Kushner family, the WSJ reported.

“Given Brookfield’s experience in successfully redeveloping and repositioning major office assets in New York and other cities around the world, we are well placed to capitalize on that opportunity,” Ric Clark, Brookfield Property Group’s chairman, said in a statement.

The infamous “devil” tower with the “666” sign on the entrance, has been under scrutiny because Jared Kushner is married to Ivanka Trump, and is a senior adviser to the president. When the Kushner Cos acquired the building in 2007 for $1.8 billion, it represented a New York commercial real estate record and was made when Kushner was taking a leadership role in the business. It remained precarious for years, and potential deals became complicated after Mr. Kushner took the senior White House job.

While terms of the deal weren’t disclosed in a statement Friday, the WSJ notes that the proceeds would give the family enough to pay off the more than $1.1 billion of debt on the building and buy out its partner, Vornado Realty Trust, for $120 million so it can transfer 666 Fifth to Brookfield unencumbered.

The sale means that the Kushner family likely won’t make any money on its investment in 666 Fifth Ave.

In recent years, the building hasn’t been generating enough money to pay its debt service. Jared Kushner had already sold his stake in 666 Fifth to a trust controlled by other family members to avoid potential conflicts. Still, the talks between Anbang and his father ignited criticism that Kushner might use his position to help his family salvage its investment.

Brookfield, which is buying the property through one of its private-equity funds, also plans to invest more than $600 million in overhauling the 39-story building, giving it a new lobby, façade and mechanical systems, according to a person familiar with the matter.

The building has seen its rental payments suffer in recent years due to a relatively high vacancy rate but is viewed in real-estate circles as having potential due to its prime location on Fifth Avenue between 52nd and 53rd Streets.

The structure of the deal is different from what Brookfield and Kushner Cos. discussed in the spring. Back then, Brookfield was considering a deal in which it would essentially acquire Vornado’s 49.5% stake in the property and become partners with the Kushner family.

One of the uncertainties about the Brookfield purchase of the 99-year lease is how much of the current debt on the building is going to be repaid. In the 2011 restructuring, the debt was carved into two pieces—a senior piece and a junior piece. The senior piece is worth $1.1 billion and the junior piece has increased since 2011 to over $300 million, because interest on it has been accruing.

Kushner executives have been arguing that only the senior debt on the building has to be repaid, partly because 666 Fifth isn’t worth the total $1.4 billion of debt on the building.

The recent history of the building is remarkable.

The property has taken numerous twists, both financial and political. Kushner Cos. sold a controlling stake in the retail space for more than $500 million a few years after it purchased the tower in 2007, using most of the proceeds to repay debt.

But that wasn’t enough to shore up the property in the post-crash years. In 2011, Kushner Cos. renegotiated what was then $1.2 billion in debt and brought in Vornado as a 49.5% partner.

In 2017, soon after Mr. Trump took office, Mr. Kushner’s father, Charles Kushner, was negotiating with Anbang Insurance Group, a Chinese insurer with connections to Beijing government. The elder Mr. Kushner’s plan at the time was to use Anbang’s capital in a $7.5 billion plan to convert 666 Fifth Ave. into a 1,400-foot-tall mixed use skyscraper with retail, hotel and condominiums.

Soon after, the Anbang talks soon collapsed. Since then, Kushner Cos. has steered clear of any deals with sovereign funds, a decision which has made the firm rein in its ambitious plans for the site. The family also faced a deadline: the debt on the building needs to be repaid next year.

And thanks to Brookfield, that will no longer be Jared’s problem any more.

Construction giant Skanska AB is developing two office buildings in Houston’s “Energy Corridor.” The one that is nearly complete is mostly leased; the other building doesn’t yet have any tenants. Photo: Michael Stravato for Wall Street Journal. Article by Eliot Brown

Construction giant Skanska AB is developing two office buildings in Houston’s “Energy Corridor.” The one that is nearly complete is mostly leased; the other building doesn’t yet have any tenants. Photo: Michael Stravato for Wall Street Journal. Article by Eliot BrownHOUSTON—The jagged skyline of this oil-rich city is poised to be the latest victim of falling crude prices.

As the energy sector boomed in recent years, developers flocked to Houston, so much so that one-sixth of all the office space under construction in the entire U.S. is in the metropolitan area of the Texas city.

But now, the need for more offices is drying up, thanks to a drop in oil prices that has spun energy companies from an outlook of optimism and growth to anxiety and cutbacks. Oil prices have fallen by more than 50% since June.

Demand for office space is “going to basically stop,” said Walter Page, director of office research at property data firm CoStar Group Inc. “It hurts a lot more when you have a lot of construction.”

By the end of 2014, construction had started on about 80 buildings with about 18 million square feet of office space in the greater Houston area, according to CoStar. Many of the buildings were planned or started when oil was above $100 a barrel. On Tuesday, oil futures traded around $50. The amount under construction is equal to Kansas City, Mo.’s entire downtown office market and is 16% of all U.S. office development under way.

The rush of building has created thousands of jobs—not only at building sites, but also at window manufacturers, concrete companies and restaurants that feed the workers.

But just as the wave of office-space supply approaches, energy companies, including Halliburton Co. , Baker Hughes Inc., Weatherford International and BP PLC, have collectively announced that more than 23,000 jobs would be cut, with many of them expected to be in Houston.

Fewer workers, of course, means less need for office space. Employers have rushed to sublease space in recent months, with 5.2 million square feet of space on the market as of last month, up about 1 million square feet from mid-2014, according to brokerage firm Savills Studley. BP, for example, is trying to sublet 240,000 square feet of space at its campus in the Westlake neighborhood, which represents about 11% of BP’s space at the campus, according to CoStar. A BP spokesman said the company is “consolidating” its footprint.

Conditions could improve if oil prices rise. The International Energy Agency on Tuesday said oil companies’ recent cutbacks in production will likely slow the growth of U.S. oil output, which in turn would lead to a rebound in prices.

But the current building boom is Houston’s biggest since the 1980s, when an oil bust, coupled with a rash of empty skyscrapers, made Houston a national symbol of overbuilding. Then, armed with debt from a banking sector eager to lend, developers brought a tidal wave of building to Houston, in some years increasing the office stock by well over 10%. Vacancy rates shot up past 30% from single digits, property values plummeted and landlords defaulted on mortgages.

That contributed to a wave of failures for banks stuffed with commercial-property loans. More than 425 Texas institutions between 1980 and 1989 failed, including nine of the state’s 10 largest banks.

Few are predicting a shock near that scale this time. Even if oil prices stay low, the local economy is more diversified than in the 1980s with sectors such as health care and higher education comprising a larger share of the workforce. In addition, new construction represents about 6.3% all the area’s total office stock, and there is far less speculative construction done before a tenant is signed up.

“Everybody here in Houston is waiting to exhale,” said Michael Scheurich, chief executive of general contractor Arch-Con Corp., which currently is building two midsize office projects in the area. Mr. Scheurich said his company has grown to about 80 employees from fewer than 25 in 2011 amid the construction boom. Now he is hoping the local economy will have “a soft landing.”

Still, cranes abound throughout Houston, thanks to publicly traded real-estate companies, pension funds and other interests like Swedish construction giant Skanska AB, which are funding construction without as much reliance on debt as in the 1980s.

‘Everybody here in Houston is waiting to exhale.’

Running west from the downtown along Interstate 10, numerous midsize construction projects aimed at the “upstream” companies focused on energy extraction are being built in the so-called Energy Corridor.

Analysts say this shows how the sector is highly susceptible to booms and busts because of the long lag time between when buildings are started and when they are delivered, compounded by the tendency of developers and financiers to start projects en masse, late in cycles.

Developers are often victims of “herding and group think,” said Rachel Weber, an urban planning professor at the University of Illinois at Chicago who is writing a book about office over development in Chicago. “There is a sense that if everybody is moving in the same direction and acting the same way, that you do better to mimic that kind of behavior.”

Many of those building are bracing for a sting in the short-term. It could be even more painful if oil prices stay low.

It “is going to be a soft year—it’s hard not to see that,” said Mike Mair, an executive vice president in charge of Houston-area development for Skanska. The company is putting the finishing touches on a new 12-story tower in the Energy Corridor that is 62% leased. Construction is under way on a nearly identical building next door for which it doesn’t have any tenants.

Still, Mr. Mair said he believes in the city’s economic strength in the mid- and long-term, giving him confidence to finish work on the second tower. “I’m not afraid of ’16 and ’17,” he said.

It “is going to be a soft year—it’s hard not to see that,” said Mike Mair, an executive vice president in charge of Houston-area development for Skanska. The company is putting the finishing touches on a new 12-story tower in the Energy Corridor that is 62% leased. Construction is under way on a nearly identical building next door for which it doesn’t have any tenants.

Still, Mr. Mair said he believes in the city’s economic strength in the mid- and long-term, giving him confidence to finish work on the second tower. “I’m not afraid of ’16 and ’17,” he said.

Of course, higher vacancy rates would mean lower rents, which is good for anyone signing a lease. Rents at top-quality buildings averaged $34.51 a square foot at the end of 2014, up about 15% from early 2012, according to CoStar. But brokers say landlord incentives have grown, and rents typically follow the direction of oil prices, with a lag of one or two quarters. Still, the rents are a bargain compared with other major cities such as New York, where top-quality offices rent for an average $59 a square foot.

The city of Houston, for one, could be a beneficiary of lower rents. The government had been planning to build a new police department headquarters at an estimated cost of between $750 million and $1 billion.

Late last month, the mayor’s office said it was examining the possibility of leasing the building that Exxon Mobil is leaving, which would cost far less than the city’s original plan.