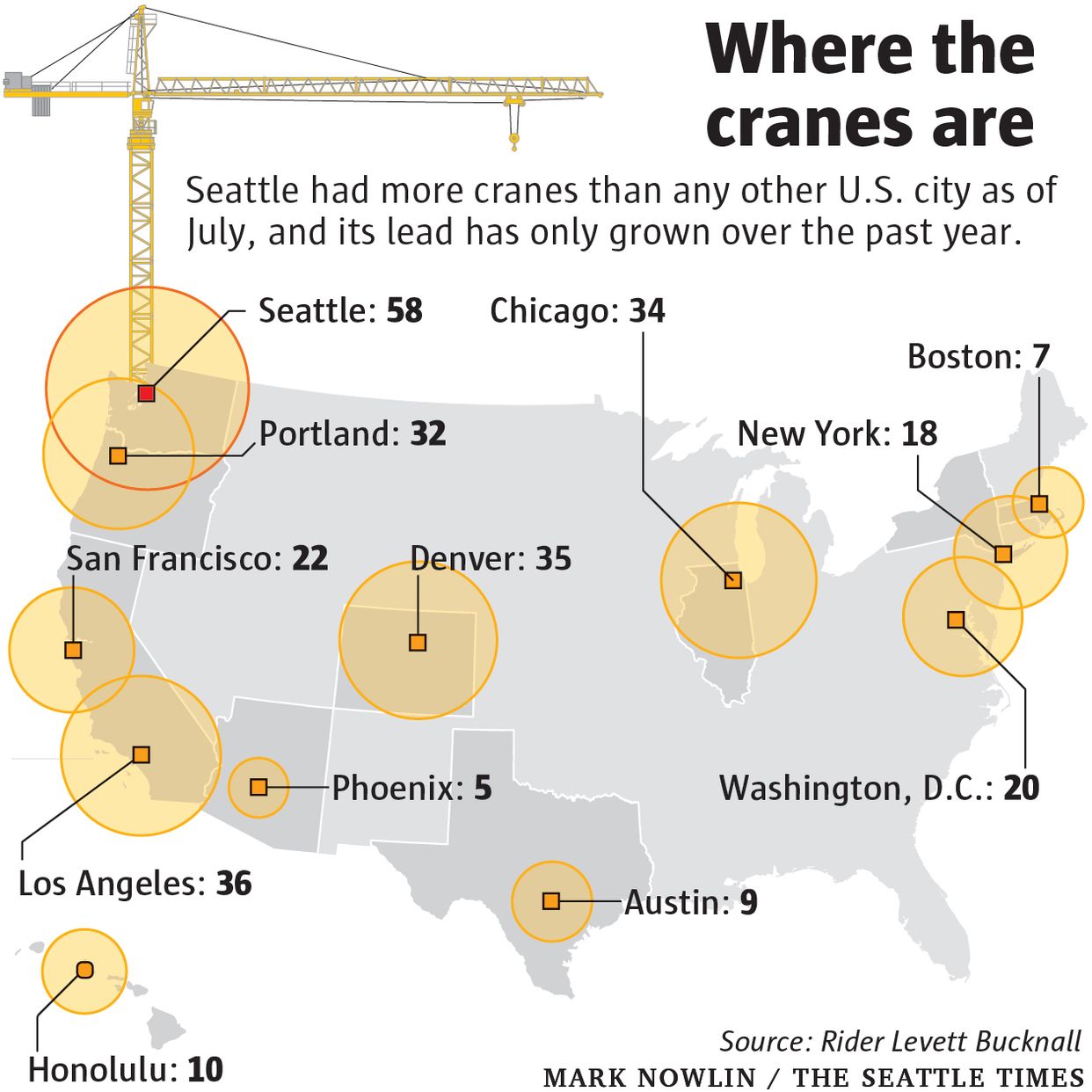

This is how housing markets turn. Slowly, then all at once.

Seven years of Seattle home prices outpacing wage growth because of low rates; bidding wars replaced by sales at the asking price; days or weeks on the market turning into months; sellers reduce home prices; surging mortgage rates; buyers disappear, and wallah – a classic turning point in an auction, otherwise known as an unfair high that is now rippling through the real estate food chain in the Seattle area.

As a reminder, before we dive into the faltering real estate market in Seattle. Back in September, we outlined a significant clue about the overall health of America’s housing industry: Bank of Ameria called it: “The Peak In-Home Sales Has Been Reached; Housing No Longer A Tailwind.”

With that in mind, it comes as no surprise that inventory countywide soared 86% among single-family homes and 188% among condos in October compared to a year prior, according to newly published data by the Northwest Multiple Listing Service. It was the most massive year-over-year increase on record, dating back to the Dotcom bust, a rhythm that has some asking: Is the housing industry about to go bust?

Mike Rosenberg, a Seattle Times real estate reporter, has been documenting the rise and fall of the real estate market on the West Coast.

Rosenberg said the median home price plummeted to $750,000, down $25,000 in one month and down $80,000 from all-time highs in spring.

He warned, “that is not a normal seasonal drop — prices in the city actually went up during those time frames last year.”

Compared to 2017, prices inched up about 2%. He said interest rates had moved higher in that span have increased monthly mortgage costs.

On the Eastside, the median home sold for $890,000, unchanged from the previous month, but down $87,000 from the all-time high in late summer. On a year-over-year basis, prices were still up 5.3%.

Rosenberg notes that prices dipped on a month-over-month basis in South King County but surged at the northern end of the county. He said inventory is flooding the market at the same time as buyer demand evaporates.

As we highlighted in the BofA report, sellers across the country are unloading properties into a weakening market will trigger downward momentum in prices.

Back to Seattle, that is precisely what is happening, as sellers have reacted by cutting asks faster than any other metro area in the country. To make matters worse, buyers are now negotiating prices down even further, as the average home is selling for below list price for the first time in four years, said Rosenberg.

Rising interest rates, declining demand, and flat-lining rents have been the main drivers of failing home buyer demand in the second half of 2018.

Into the fall months, brokers told Rosenberg that buyers are now pausing as they wait for the storm to blow over.

Ken Graff, a broker with Coldwell Banker Bain in Seattle, listed a townhouse in Magnolia on the market in April, “right before the apparent peak of the market,” and had 11 bidders who ferociously fought for the home, with a winning bid for $800,000. In September, he listed an identical town home in the same neighborhood, it stood on the market for three weeks before selling for $725,000.

“Buyers are still having to pay a premium for Seattle-area properties, but it lacks the frenzy we’ve seen in the last few years,” Graff said.

“People can be a little more measured now, which is a good thing.”

Among other regions where home prices have dropped in October on a year-over-year basis: West Bellevue, Southeast Seattle, Burien-Normandy Park, and the Skyway area. On the other end, prices rose more than 10% from a year ago in Jovita-West Hill Auburn, Auburn, Kent, Renton-Benson Hill, Mercer Island, Kirkland-Bridle Trails and Juanita-Woodinville.

Elsewhere, the rest of the Puget Sound region also saw expanding inventory, including a 65% increase in Snohomish County.

The slowdown in Seattle housing shows little signs of abating as the Federal Reserve is expected to hold rates on Thursday before a hike in December. At their most recent meeting in late September, Fed officials communicated a plan for three more hikes in 2019. With one more rate hike forecasted in 2018 and three more in 2019, it seems that Seattle and much of the country’s real estate market could be at a significant turning point into the 2020 presidential elections. Let us hope real estate prices do not fall even further, as many home buyers could vote with their home prices.