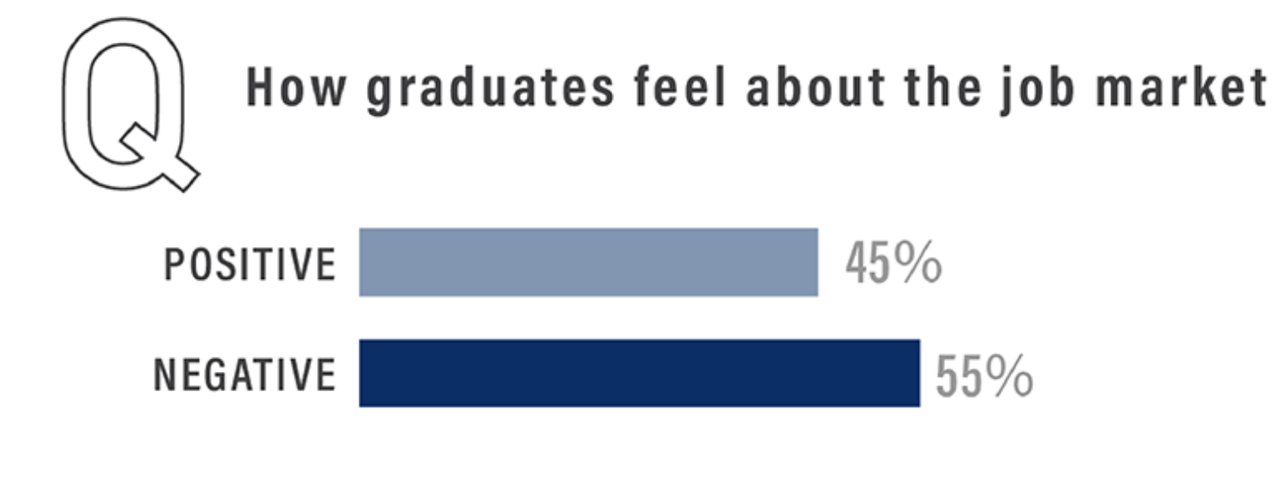

This doesn’t bode well for the labor market.

American students carry an aggregate pile of student loan debt equivalent to roughly $1.5 trillion, a generational burden that has helped contribute to plunging birth rates, lower home-ownership rates among young people, and even lower rates of stock ownership, as more young people dedicate more financial resources to paying down debt.

But to gauge exactly how much a students’ finances factor into their decisions about which school to attend and which majors to choose, MidAmerica Nazarene University surveyed 2,000 recent graduates from around the country to learn more about how they financed their degrees, and how much they will owe after graduation.

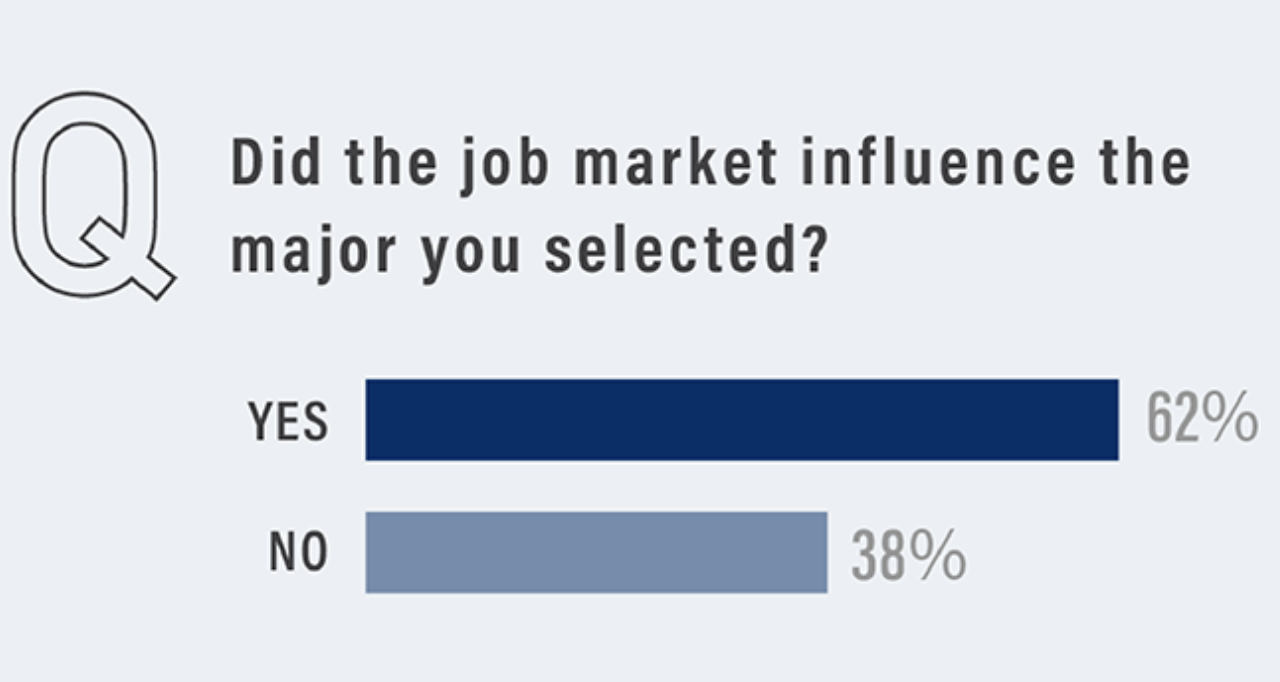

Given the cost of higher education in the US, the majority of students answered that post-grad job prospects influenced the major they selected (those who answered ‘no’ either really enjoy studying STEM, or majored in gender studies).

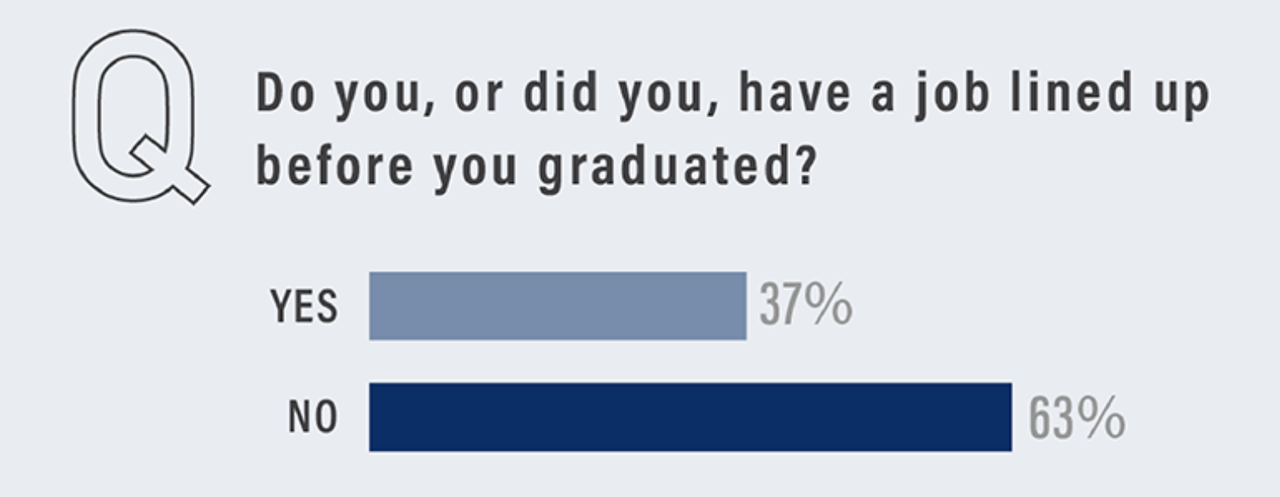

It might seem surprising given the financial stakes, but the survey also showed that more than 60% of recent grads didn’t have jobs lined up when they received their diplomas.

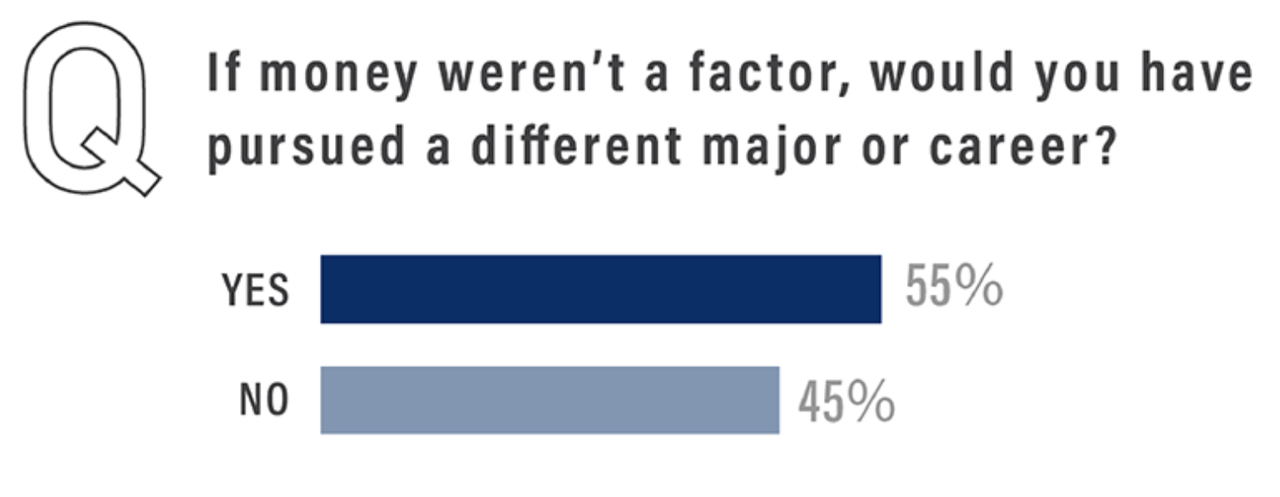

For those who did choose their careers based on financial considerations, a majority said they would have picked another line of work if finances weren’t a consideration (but hey, we can’t all be artists).

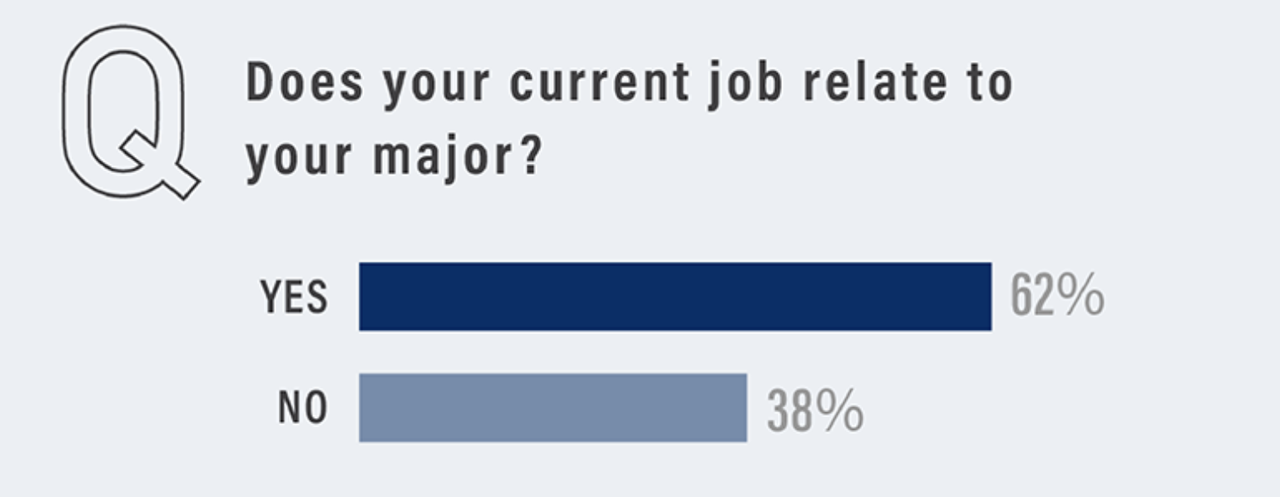

Once upon a time, there wasn’t as much of a correlation between a students’ field of study and their eventual chosen career (investment bankers who studied English at Middlebury College wound up on Wall Street thanks to ‘Uncle Jim’s’ connections). But as the world of higher education becomes increasingly costly and cut throat, situations like this are becoming increasingly rare.

One of the more telling data points in the study was the gauge of graduates’ feelings about the job market. Even with unemployment at multi-decade lows, a majority of graduates had a negative outlook on the job market.

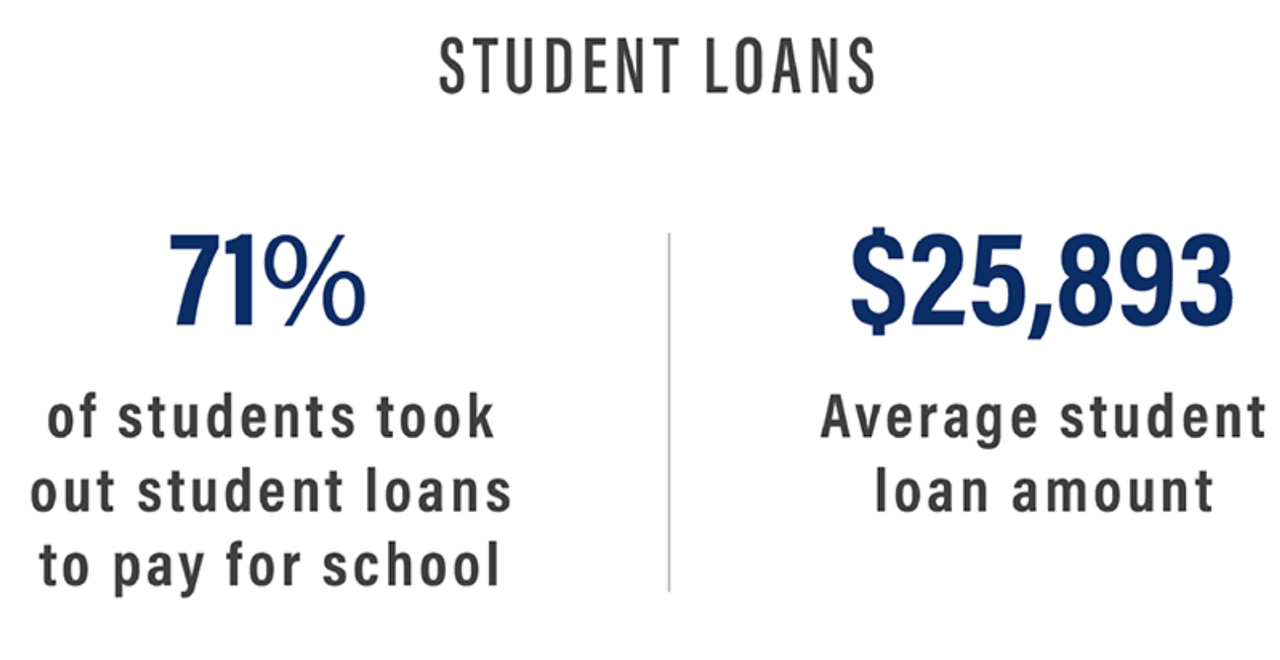

The overwhelming majority of students took out loans to pay for some or all of college, with 71% taking out loans and the average amount borrowed equivalent to just over $25,000.

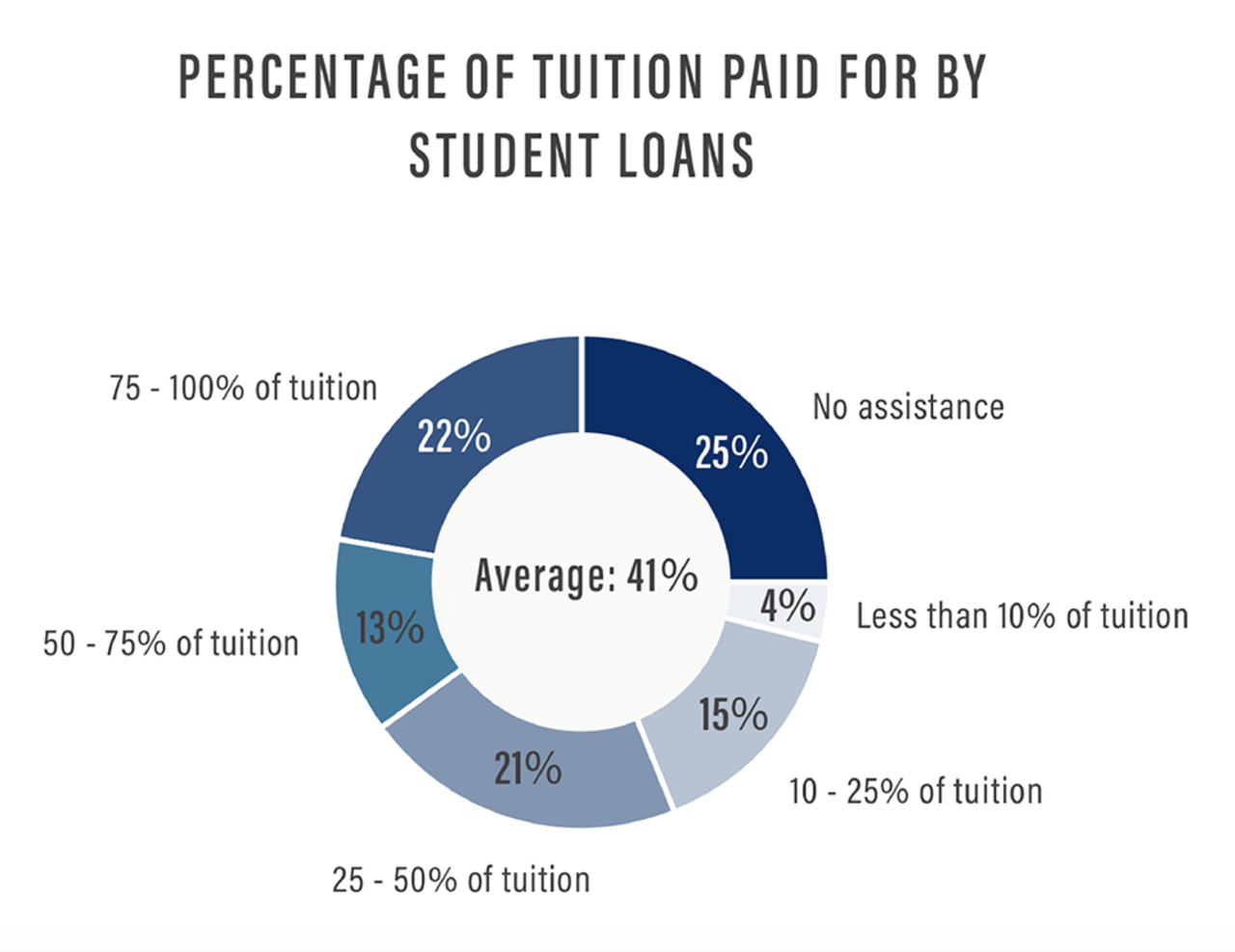

In addition to taking on loans, most college students receive at least some help from family members or other sources, as only one-quarter of respondents said they completely self-financed their degree.

On average, students expect to pay off their loans in 9.5 years, meaning that most of these students will be in their mid-30s when they finally reach a zero balance.

Imagine what that number would be if students had no help from their families?

But some trade jobs go unfilled

LikeLiked by 1 person