Source: Seeking Alpha About: Federal Agricultural Mortgage Corporation (AGM), Includes: FNMA

Summary

- Farmer Mac, the Fannie Mae of agriculture, trades at 1 times book and 7 times earnings despite delivering sustainable 15-20% ROEs.

- Organizational improvements are finally enabling Farmer Mac to rapidly gain share; penetration remains low, so the growth runway is long.

- Investors drew the wrong lesson from Fannie Mae’s failure. GSE privileges enable super profits from mundane activities. Fannie failed because it strayed from its core business.

Farmer Mac’s Birth

During the late 1980s, plunging agricultural prices threatened the solvency of the Farm Credit System (FCS), a problem congress tried to address in the usual manner. They bailed it out. Non-FCS banks weren’t happy about that since they thought the FCS’ (“unfair”) advantages were the primary cause of the boom-bust cycle that required the bailout in the first place. So congress chartered Farmer Mac (NYSE:AGM) to help level the playing field for banks by providing a secondary market for their loans.

The FCS is old and big; it was chartered by the Feds in 1916 and it supplies ~40% of US farm credit. (All you really need to know about the FCS is that its institutions have lower long-term funding costs than deposit fueled banks; and they’re supposed to restrict their lending to agricultural and certain rural development situations.) It’s hierarchically structured and cooperatively owned. Agricultural operators borrow from and own stock in its retail lenders (Farm Credit Associations, FCAs, of which there are presently ~80); FCAs borrow from and own stock in wholesale lenders (Farm Credit Banks, FCBs, 4); who borrow from and own stock in the FCS Funding Corp. which taps capital markets; these proceeds then flow down through wholesalers to retailers to farmers. The FCS Insurance Corp. which has a $10b line of credit with Treasury guarantees FCS bond issuances. The system can borrow longer and cheaper than any purely private sector entities of lesser quality than, say, ExxonMobil, which enables the usual GSE competitive edge (like Fannie Mae, (OTCQB:FNMA) at funding long-term fixed rate assets. The system is exempt from taxes on certain types of lending. For these privileges the FCS is constrained to lend to underserved rural America, which it likes to define as widely as possible (a wholesaler recently lent to Verizon Wireless!). Though wholesale FCS institutions are in some ways similar to AGM they’re not allowed the leverage necessary to be an effective maker of secondary markets; and they can’t deal with non-FCS lenders (commercial banks). (See Bert Ely’s articles on the FCS for an insightful banker side point of view.) Anyway, back to the chronology.

Ag Banks, by which I mean non-FCS commercial banks with agriculturally concentrated portfolios, always hated the FCS for their privileges. So you can imagine their displeasure with the 1987 FCS bailout.

Farmer Mac was the bone congress threw to banks to apologize for the bailout of their rival. If a bank couldn’t offer a borrower as low a long-term fixed rate as a “predatory” FCS lender, they could still originate the loan and keep the customer by selling it to AGM. The rate ought to be FCS competitive since AGM, with their $1.5b emergency Treasury line of credit, can borrow cheap and long like the other GSEs. And banks could still make maybe 0.7% risk-free for servicing the sold loan. That was the idea at least, but it’s taken some time for things to work that way.

1996 Reform Launches Farmer Mac..Sort of

AGM, which was chartered in 1987 and operationalized in 1989, had nothing to do with the ag recovery that was gaining steam in 1995. They’d executed less than $1b in securitizations (transactions where purchased loans are pooled, made into a bond, guaranteed by AGM and sold) to that point, a trivial fraction of their potential addressable market. When AGM’s charter was initially being considered experts had expected $2-3b in securitizations per year.

In 1995 having never turned a profit and with just 43%, or $12m, of their original capital remaining, AGM appealed to congress to liberalize their straitjacket of a charter. They got what they asked for in the form of the 1996 Ag Reform Act.

The first key change was the elimination of the skin in the game rule that required originators to hold loan residuals, the first 10% loss position on loans sold. That provision in practice meant sellers retained all the credit risk. So selling banks had been getting neither relief of credit risk nor required capital.

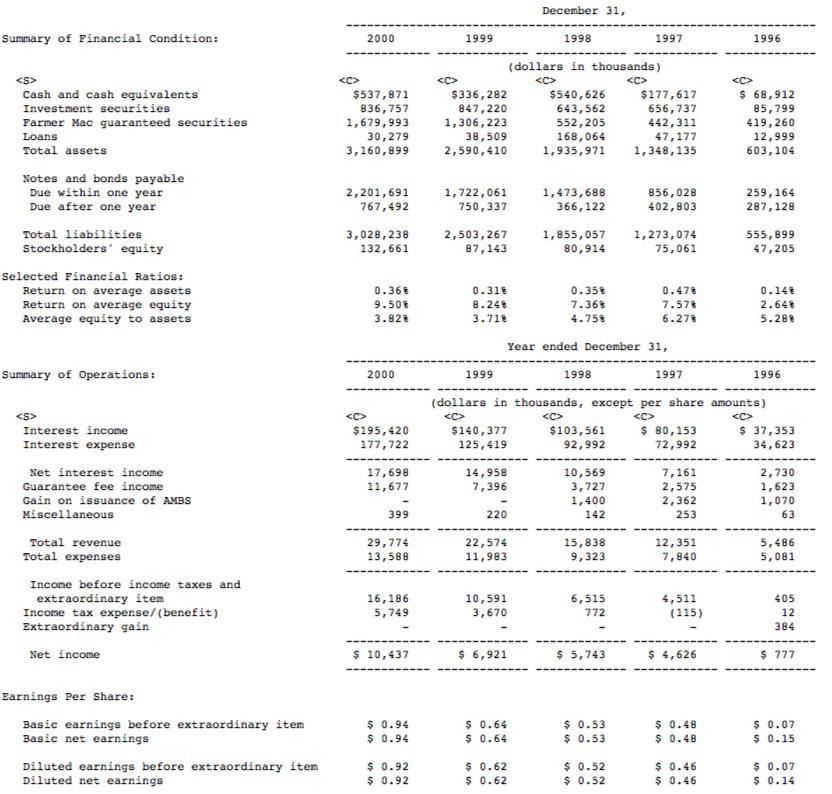

Secondly, the Act let AGM bypass loan poolers (insurers and big banks) to buy loans directly from originators. It’s unclear to me why direct purchase was ever forbidden since an extra pooling intermediary adds cost and complexity, and makes both AGM and ag banks dependent on the efforts and interests of third parties. But anyway, the 1996 Act transformed AGM. The removal of these two key restrictions let them generate the business volume necessary to immediately turn and remain profitable. Business volume and profits grew rapidly from 1996 through 2003. Though the majority of the growth, especially between 2000 and 2003, was generated by transactions between FCS lenders and Farmer Mac!

(click to enlarge)

Internal Problems Limit Farmer Mac’s Growth With non-FCS Lenders

Much of their growth in this era was produced by a product called long-term standby purchase commitments (LTSPCs) which are sold primarily to FCS associations (they generate the Guarantee fee income you see above). These “credit enhancements,” or default insurance, are promises to buy defaulted loans from a predefined eligible pool in exchange for a guarantee fee of 20-50 bps assessed based on the size and quality of the pool. They reduce a lender’s required capital and credit concentrations, but leave it with the interest rate risk. The FCS prefers them to outright loan sales because they’re simple and cheap and because the FCS is less worried about rate risk than banks are. FCS lenders like LTSPCs; banks like outright loan sales. (AGM’s LTSPCs are held off-balance sheet, but they are required to allocate capital to them.)

By 2003 the popularity of LTSPCs meant that the FCS was doing three times more business with AGM than banks; an irony and an outrage for AGM’s initial supporters!

In 2003 the Independent Community Bankers Association (ICBA) told congress that AGM wasn’t doing a good job for its constituents. You see, there are 1,500 ag banks in the US and yet in any given year between the late 1990s and 2010 only 40-80 of them transacted with AGM. Of those, the top 10 would often comprise 90% of their volume. So most years AGM truly mattered to less than 1% of US ag banks! In contrast, ~30 of the 80 FCS associations bought LTSPCs each year. This is not how Farmer Mac was supposed to operate.

The asymmetry between FCS and bank participation was caused by two things. First, ag banks tend to be smaller than FCS lenders, and AGM’s programs were too clunky and time consuming for small lenders to participate in. Second, AGM was less rigid in the loan structures they were willing to guarantee with LTSPCs than the ones they’d purchase.

All Systems Go

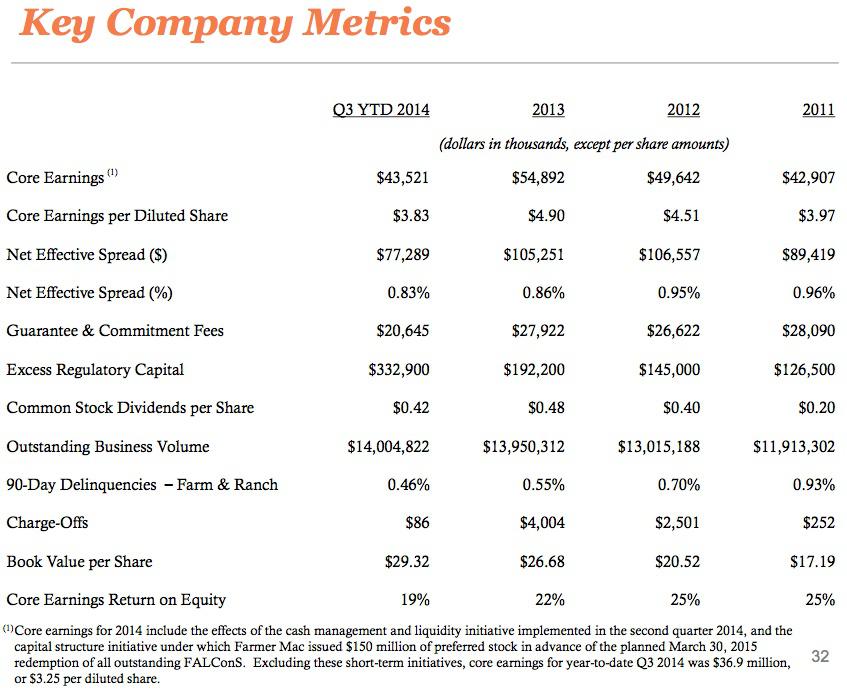

Flash forward. After a decade of little quantifiable progress in expanding breadth, the number of banks who sold loans to AGM in 2013 nearly tripled to 220 from 80 in 2010; eligible and approved sellers tripled too, to more than 600. Here is the path of the dollar volume of loan purchases between 2008 and 2013: $196m, $195, $382, $495, $570, $825. Most tellingly, the top ten 2013 loan sellers comprised just 53% of AGM’s record $825m in 2013 volume. Breadth of participation is exploding. Right now.

What changed?

First, whereas the ICBA said underwriting took weeks or months back in 2003, AGM now targets two days. The 2005 launch of their web-based underwriting system (AgPower LOS), and its subsequent iterative improvement, deserves much of the credit.

Second, AGM was a young company back in 2003; officially 14 years old, but really just seven. It didn’t help that the data required to model prepayment speeds and credit losses was tough to come by. The result was rigid underwriting. For example, in 2003 the vast majority of their fixed rate portfolio loans carried prepayment protection, which borrowers hate; now it’s just 2%. (AGM never cared about prepayment protection in their LTSPC book because the lender kept the loans and interest rate risk on their own book.)

Third, was their outreach. AGM formed alliances with the American Banking Association (ABA) in 2005, and ICBA in 2009 featuring, among other things, pricing discounts for members and a commitment to get in the field to educate and learn from ag banks. This doesn’t sound important, but I gather that sleepy $25m rural banks aren’t the most proactive institutions, which in some ways is a good thing when I think about Countrywide and Indymac. Anyway.

In 2010, a ripe AGM collided with an amenable macro environment, with borrowers scrambling to refinance into long-term fixed rate loans, and their volume exploded. Today 75% of new loan and LTSPC transaction volume comes from non-FCS bank lenders, which is the way it always should have and would have been if AGM’s organization weren’t so immature until recently.

The fraction of US ag banks working with AGM has tripled from 5% to 15% since 2010; and AGM’s share of existing farm debt is still well under 5%. Low and rapidly growing penetration is the sort of thing you want to get exposure to. CEO Tim Buzby told the ABA in 2013, “…if you had told me five years ago that we were going to purchase $1 billion in loans [including $400m USDA guaranteed loans] in 2012, I would have said, ‘You need to explain to me how we’re going to do that.’ Now, if you told me that we’re not going to do $2 billion annually five years from now, I’d ask you to explain to me why not.'”

(click to enlarge)

[The source for the graphics and tables are AGM’s most recent investor presentation.]

Let me summarize before I move on. AGM’s charter restricted their growth before 1996; its liberalization enabled rapid (but narrowly fueled) growth and increasing profitability through 2003. With their addressable FCS market addressed, growth then stalled due to organizational problems that hindered their ability to serve non-FCS banks, which is ironic because it’s these entities who their funding capabilities complement best. More efficient underwriting, smarter and more flexible pricing, and successful outreach programs prepared the ground that spurred re-ignition of gradual growth in 2008-2010 and explosive growth post-2010 when the macro environment turned favorable. AGM has been posting 15-20% ROEs since 2010 and looks poised to do similarly in the future, as they continue to penetrate a huge non-FCS addressable market.

GSE Business Model Fundamentals

An institution’s structure determines what it ought to do. Farmer Mac can borrow cheap and long; and it’s allowed ~3 times the leverage of an ordinary bank. Therefore they are uniquely capable of transforming low credit risk, low fixed rate assets into substantial ROEs. And since it’s easy to underwrite prime assets originated by third parties they can run the business with 1/10th the overhead of an ordinary bank, amplifying their competitiveness in their niches.

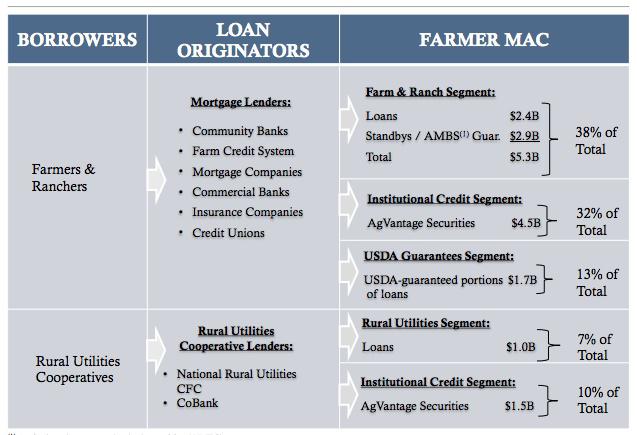

Basic ag loans and LTSPCs, the stuff I’ve talked about so far, are actually the riskiest and most profitable bucket of assets AGM is exposed to. The other half of their program volume (assets + off-balance sheet guarantees) contains virtually no credit risk. For example, 13% of assets are USDA guaranteed rural loans backed by the full faith and credit of the US government. Another 32% are general obligation bonds issued by high quality credits like Metlife, all of which are 100-111% collateralized by eligible ag loans. Last, 17% of volume is a combination of direct and AgVantage (collateralized bond) exposure to Rural Utilities loans, which are highly regulated entities that enjoy the safety of cost-plus pricing. Their charter was expanded to include this business in 2008.

Spreads are low in these other business lines, but a 0.6% match-funded spread (locked-in by matched duration debt issuance) with no credit risk, requiring little labor to underwrite, levered 25-30 times (including preferred equity; 40 times on common equity), is a highly profitable risk adjusted deal. GSE charter privileges let you earn big profits in mundane ways.

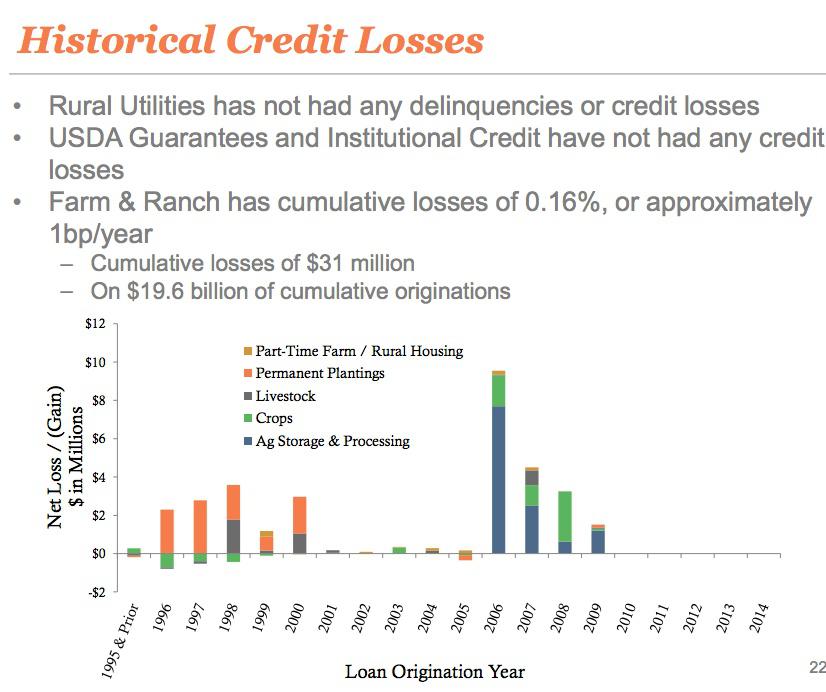

Getting back to the “Farm & Ranch Segment,” which is how AGM collectively refers to their portfolioed ag loans and off-balance sheet guarantees: I’d mentioned that these are their riskiest assets. How risky?

(click to enlarge)

Not very. Cumulative losses are 1 bp per year; that is $1 on each $10,000 of loans. Total historical losses of $31m equate to about $2.00 per share fully-taxed. AGM’s actual book value is ~$30; it’d be $32 if they’d never lost a penny since 1989. Excluding a 2006 foray into ethanol facilities, which has been aborted, historical losses are half as large, 1/2 bp per year.

Credit losses are historically immaterial. And by every metric credit is more pristine than ever. The weighted average loan-to-value ratio is presently 44% based on originally appraised real estate values; factoring in land price appreciation, the market LTV is surely below 40%. That sort of collateral with sub 0.5% delinquency rates means minimal credit risk.

The Bull Thesis

Fannie Mae beat the market by a factor of 7.5 between 1984 and 1999. Digest that.

GSE privileges are valuable if you don’t venture from the core business model, which is pretty simple: don’t take substantial credit risk. Ever. Fannie imploded because, in an effort to gain back lost market share and to prove their social worth, they ventured into subprime and alt-a exposures between 2004-2006. Their prime book of business did just fine during this period.

AGM is priced at 1 times their ~$30 book value; and ~7 times their ~$4-4.40 EPS run-rate. With the organization and processes (finally) in place to play an ever increasing role in non-FCS agricultural/rural lending, I think they can grow program volume and earnings by 10-15% per year; and that they can maintain ROE in a 13-20% range indefinitely, at manageable risk. Obviously the market disagrees. What is AGM worth? Play around with how book value grows over long horizons at a 15%+ ROE; and with expansion in P/Book from a starting value of 1.0 to an ending value of 2.0, or 3.0. A 15% ROE for five years and an ending P/Book of 2.0 gives us a target of $120, 300% upside.

The Bear Thesis

Its corporate governance is awkward to say the least. Us “C” class shareholders can’t vote. The A and B shares are respectively restricted to non-FCS financial institutions, and FCS ones, who each elect 5 board reps. The remaining 5 reps of the 15 member board are presidential appointees who, I’d assume, are there to make sure everyone plays nice. As AGM’s role in banking grows at the expense of the FCS board, which seems to be functioning fine presently, may become more interesting. Further, AGM and the FCS share a common regulator, the Farm Credit Agency (FCA). If you ask bankers they’ll tell you the FCA is captured by the FCS. That’s not clear to me but do your own diligence.

Secondly, though AGM’s assets appear superbly safe, their leverage means the error margin is small. For example, AGM may not have survived 2008 if not for a capital injection from a group of concerned counterparties. The problems stemmed not at all from the core business; their liquidity portfolio contained Fannie and Lehman preferred stock! They’ve since tightened their investment standards considerably, but the Fannie/Lehman writedowns were life threatening only because AGM is so levered. Relatedly, though AGM’s interest rate risk management has dealt well with the stress of the last 7 years, and their duration gap never is more than a few months, it’s hard to tell what would happen if rates spiked 3-5% quickly.

Lastly, with the sector so healthy and liquid, there’s the risk that AGM won’t be needed. Back in 2003-2004, AGM blamed its shrinking program volume on just that. But in retrospect, I think we see that the problems were internal, not macroeconomic, because today, in a similarly healthy environment, we see their program volume and breadth marking new records quarterly.

Wrapping It Up

Michael Burry allocates his attention to investments that inspire in investors a reaction of superficial disgust; “ick!”. AGM does that. People see AGM and think Fannie, Leverage, whoa what happened in 2008 and what heck is an LTSPC? (Like this Seeking Alpha contributor does here.) Sure, they’ve been delivering ~18% ROEs in recent years, but that probably just reflects the blow-up risk they’re taking.

All these impressions are wrong in a nuanced way. AGM’s leverage has proven appropriate, maybe even inadequate, relative to the volatility of their core assets. Fannie was one of the best performing stocks on earth for 15 years; and their implosion was the product of stupidly straying into credit markets they never belonged in during the biggest housing bubble ever. And AGM’s problems in 2008 reflected specific, fixable mistakes in their liquidity portfolio, not a fundamental problem with the core business.

With a broader view we see a company that is constantly, concretely, and quantifiably improving its ability to translate its unique privileges into an abnormally high and steady return on equity. And those of us prone to long term, optimistic thinking can’t help but analogize to Fannie’s millionaire making run between 1984 and 1999.

I could be wrong. But I don’t think many folks have put the time in to find out.