by Morgan Myro

Summary

- Economic conditions are ripe for real estate trusts with short-term leases to improve, while longer lease duration REIT types will advance at a reduced rate.

- A presentation that suggests storage REITs are expensive and as such, other short-term lease property sectors are more desirable.

- A review of 5 U.S. REITs set to outperform, specifically in the apartment and hotel spaces.

“Strength does not come from winning. Your struggles develop your strengths. When you go through hardships and decide not to surrender, that is strength.” – Arnold Schwarzenegger

One of the most popular long-term holdings for income investors involves the real estate market. While single-property investments carry returns through a landlord-type management system, whether personally attained or through a management company, REITs (real estate investment trusts) offer professionally managed real estate portfolios that operate property, manage an ideal portfolio and use leverage to grow.

An investor with an after-debt market value of $1 MM in a personal real estate book could offer between one and several properties depending on market value, as well as income which investors call the “nut.” While is well known, these mom-and-pop type investors could fare much better in terms of growth and reduced risk to trade their entire real estate portfolio (save their own home) for a slice of several multi-million and billion-dollar, professionally managed REITs that pay dividends.

With the U.S. economy expanding and rates set to rise, major implications signal that the environment exists now to favor REITs with short-term leases, especially in terms of single-family and longer-term lease holdings in the real estate market.

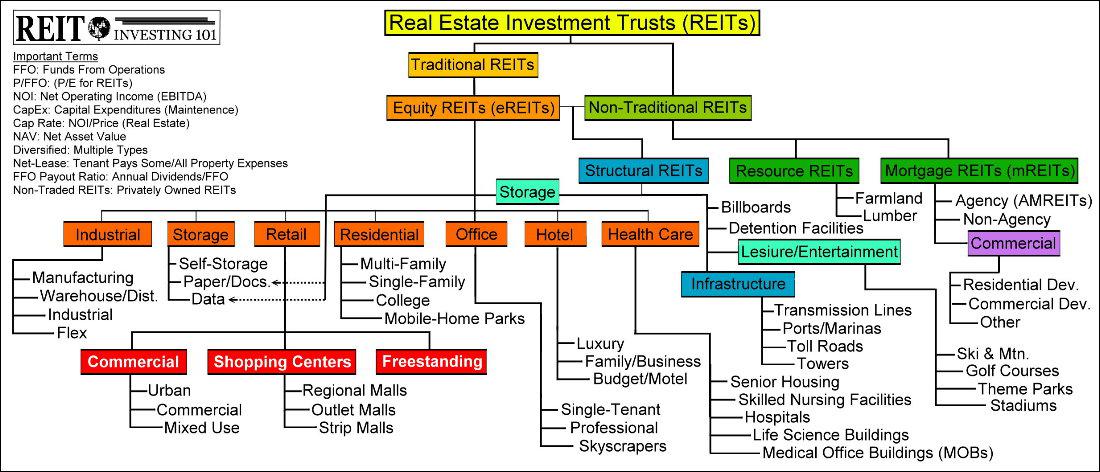

The U.S. REIT Market Sub-Sectors

The REIT market is heavily divided into several sub-sectors, such as hotels, apartments and healthcare. While there are non-traditional categories as well, such as resource, mortgage (mREITs) and structural REITs (such as cell phone towers, golf courses, etc…), this article focuses on what is known as traditional, equity REITs (eREITs).

The following map is a guide to discovering the wonderful world of REITs.

REIT Categories Set To Outperform Today

When it comes to REIT diversification, most investors classify their REIT portfolio in a traditional sense and avoid the non-traditional areas such as resource and mREITs. Income investors who do use mREITs to boost portfolio yield would be smart to categorize them as dividend stocks, as they do not generally own real estate.

Today the U.S. economy is fascinating investors as it continues to grow in the face of global turbulence, albeit at a slower post-recessionary recovery rate than normal. While this fact has caused concern, the economic trade-off is potentially very lucrative: slower long-term growth versus higher short-term growth followed by a recession.

In times of recession, short-term leases are not generally favorable as there is a general decline in demand for real estate. Those with long-term leases in stable sectors would be preferred, as companies such as Wal-Mart Stores, Inc. (NYSE:WMT) and other stable, long-term leaseholders would continue to operate.

In times of economic improvement, short-term leases are favored as there is a general uptick in demand for real estate. More people are working in upturns, which increases the supply of those looking to spend on all sorts of goods and services, of which real estate benefits.

Where Is The U.S. Economy Headed?

In looking at the U.S. unemployment rate, the clear trend is that more workers are entering the workforce (source: BLS) and that this trend will continue into 2015 with an estimated year-end unemployment rate of 5.2-5.3% (source: FOMC).

In addition to a trend of higher U.S. employment, U.S. GDP growth is also expected to continue to trend higher in 2015. The real GDP growth of 2.4% in 2014 is expected to increase to a range of 2.6% to 3.0% according to the Fed (central tendency), while Goldman Sachs (NYSE:GS) anticipates 3.1% growth on the heels of world GDP growth of 3.4%.

(click to enlarge)

In addition to favorable U.S. macroeconomic conditions, the U.S. dollar has trended higher in terms of both the U.S. dollar index versus leading currencies as well as in terms of emerging market and commodity nation currencies.

Termed currency risk, the flight to U.S. dollars increases the value of U.S. assets in terms of other global currencies while promoting the U.S. in terms of lowered-borrowing costs and an increase in investment demand.

All of these circumstances favor the U.S. real estate market and as such, the conditions for short-term lease operators in diversified publicly traded REITs are favorable for success.

5 Short-Term Lease REITs Set To Outperform

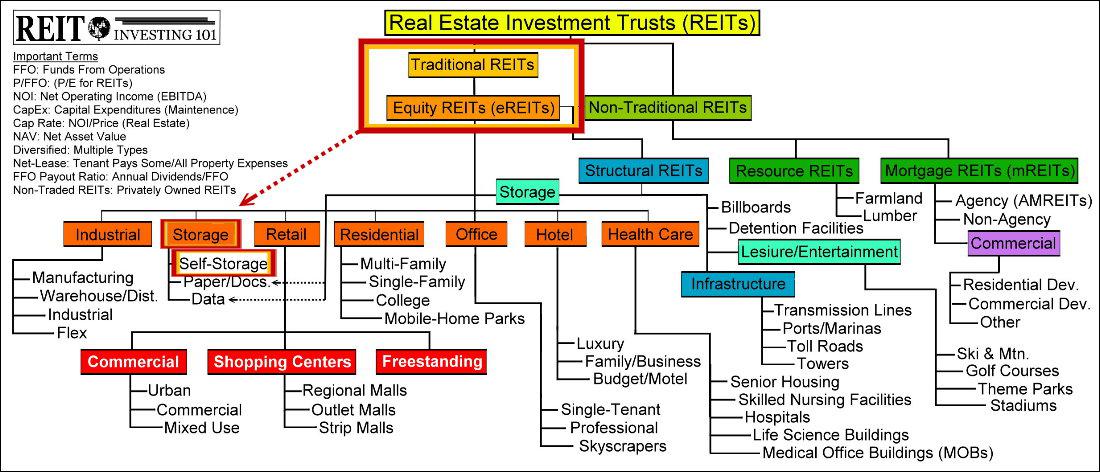

There are a few short-term lease operator types that may do well, which includes the residential, storage and hotel categories of the traditional REIT class.

While the self-storage outlook remains bright as this property sector has a short duration and a lower economic sensitivity to the business cycle, the aggregate sector valuation is high and the accompanying yields are relatively low with modest growth prospects.

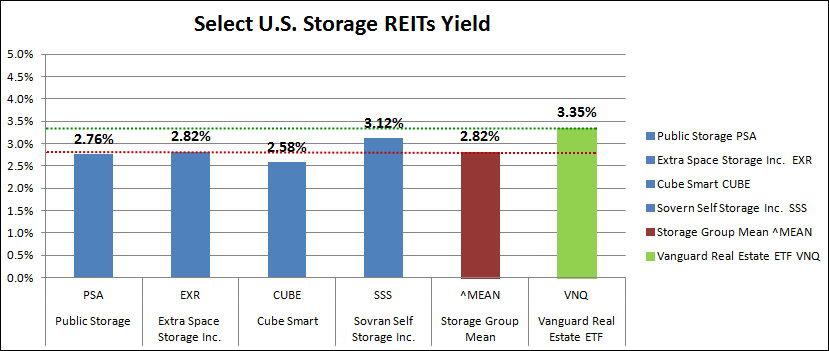

In addition to the high valuations and low yields, the top U.S. storage REITs have increased on average 26% in the past six months. The following charts include Public Storage (NYSE:PSA), Extra Space Storage Inc. (NYSE:EXR), Cube Smart (NYSE:CUBE), and Sovran Self Storage Inc. (NYSE:SSS).

These companies are all large players in the self-storage segment of the traditional, equity REIT class.

(click to enlarge)

There has been a huge run-up in the self-storage REITs over the past six months, with annualized returns of 52.89% on an equal-weighted average. When compared to the U.S. traditional equity REIT market as represented by the Vanguard REIT ETF (NYSEARCA:VNQ), self-storage has significantly outperformed.

(click to enlarge)

In looking at the average yield in the self-storage property sector versus the VNQ, self-storage is more expensive.

(click to enlarge)

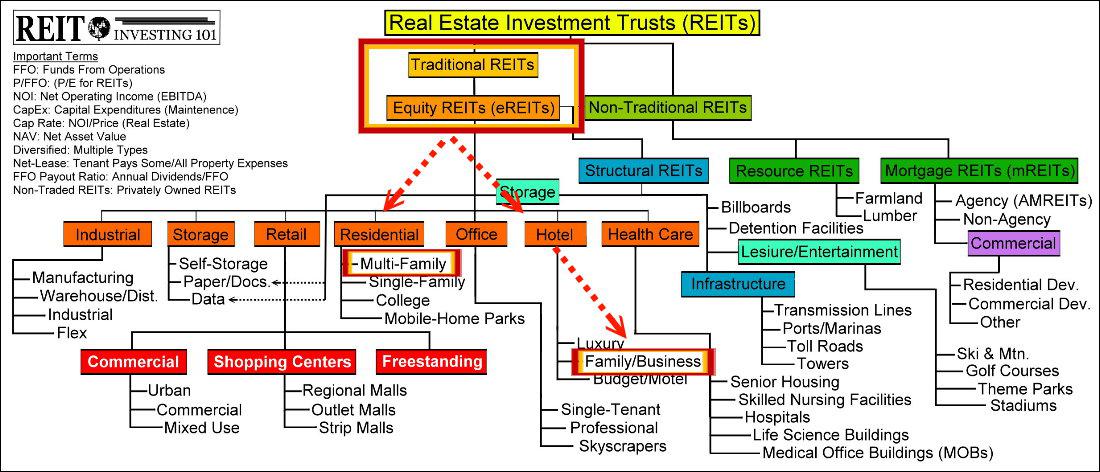

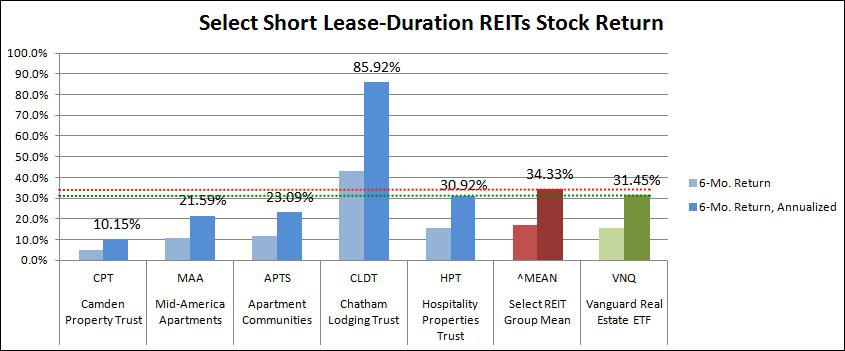

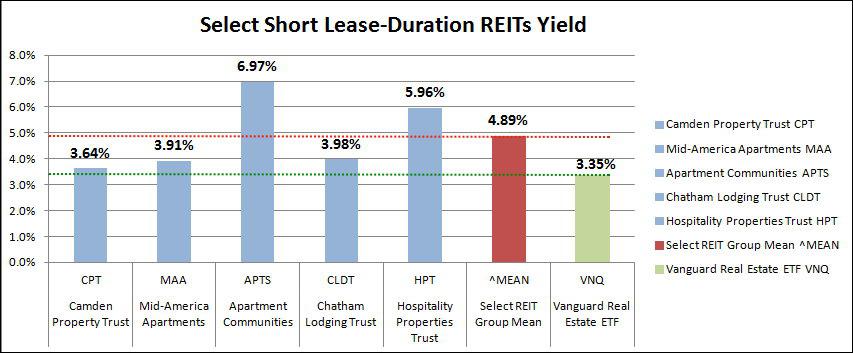

With the apartment and hotel sectors, there are companies that offer above-average yields while taking advantage of the short lease-durations that should outperform in conjunction with U.S. economic growth.

(click to enlarge)

To refocus on the lease durations, hotels are able to raise prices very quickly, while apartment landlords may increase rents after a year. Also, to note, the barriers to entry are constrained in a construction/approval cycle of two years for hotels and 1 to 1.5 years for the hotel and apartment landlords, respectively. Finally, the economic sensitivity is highest here, which equates to a faster uptick in demand during economic booms.

Hotel & Apartment Landlords To Outperform

The larger REITs in any property sector are generally more expensive versus smaller peers, which equates to a lower dividend and much larger acquisitions or developments needed (relative to smaller peers) to move the growth needle.

As seen by the average annualized six-month return of the five hotel and apartment REITs selected for this portfolio versus the VNQ, there hasn’t been such a dramatic over-performance versus the traditional equity REIT index.

In terms of yield, the group here easily outperforms the VNQ as well, with an average yield of 4.89%, versus 3.35% for VNQ. This represents 46% more income for investors of this select REIT portfolio versus the VNQ.

1. Camden Property Trust (NYSE:CPT)

Camden is the top under $10 billion apartment community landlord that focuses on high-growth markets in the sun-belt states.

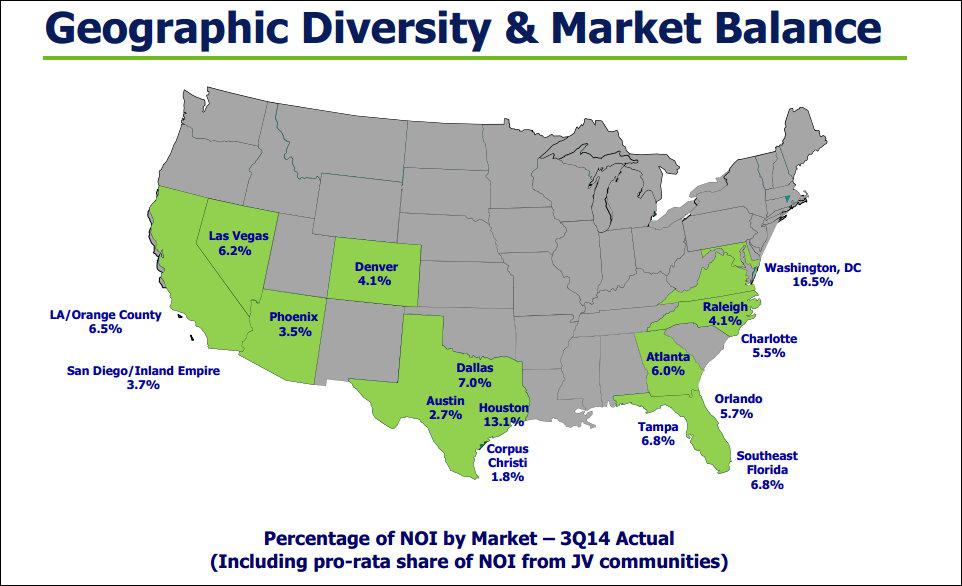

Camden’s Diversified Portfolio As Of 11/5/14

The company recently announced a raise to their quarterly dividend by 6.1% and as such, their 5-year CAGR (compound annual growth rate) of their dividend is an impressive 9.24%.

The company also has $1 billion in development projects that are currently in construction and has $684 million in the pipeline for future development. Using the midpoint of 2015 FFO guidance of $4.46 per share and a share price of $76.99, the company has a FWD P/FFO ratio of 17.26, or a FWD FFO yield of 5.8%.

2. Mid-America Apartment Communities (NYSE:MAA)

Mid-America Apartment Communities is slightly smaller than CPT with a market capitalization of $5.92 billion versus CPT’s $6.83 billion. MAA is also a takeover candidate, as the company is valued at much less than CPT (16.1x 2014 FFO versus CPT 18.3x 2014 FFO) but has a very similar and overlapping portfolio.

MAA raised their dividend 5.5% this year and over the past five years, the company has a dividend CAGR of 4.6%.

3. Preferred Apartment Communities (NYSEMKT:APTS)

APTS is a new player to the U.S. REIT market; however, it is only valued at 9.69x 2014 FFO and is run by John Williams, the founder of Post Properties Inc. (NYSE:PPS), a $3.3 billion apartment landlord and developer.

APTS Property Map

The company recently traded at $10.05 per share, just above the 2011 IPO price of $10. Regarding the dividend, the quarterly payout was raised 9.4% in December 2014.

From their first December payout of $0.125 in 2011 to the recent December 2014 payout of $0.175 (due to short operating history), the company has a three-year dividend CAGR of 11.87%, which is higher than both CPT and MAA’s 5-year CAGR.

4. Chatham Lodging Trust (NYSE:CLDT)

Chatham is a small-cap hotel operator that has shown significant growth over the past year. They have converted the dividend to monthly distributions, which is sure to appease income investors. Since going public in 2010, the dividend has increased by an average of 11.38% per year.

Chatham is an owner of the business/family segment of the hotel properties. Name brands include Residence at Marriott, Courtyard by Marriott, Homewood Suites by Hilton, Hyatt Place and Hampton Inn. While diversified, the company has a major interest in Silicon Valley, CA, home of several major U.S. technology companies.

The company just financed a secondary offering that raised ~$120 million in gross proceeds, which surely will help fuel future growth in same-store sales as well as property acquisitions.

5. Hospitality Properties Trust (NYSE:HPT)

Hospitality Properties Trust is the owner of hotels as well as travel centers throughout the U.S. They own mid-tier hotels in a similar fashion to Chatham, including similarly branded properties such as Courtyard by Marriott and Residence Inn by Marriott.

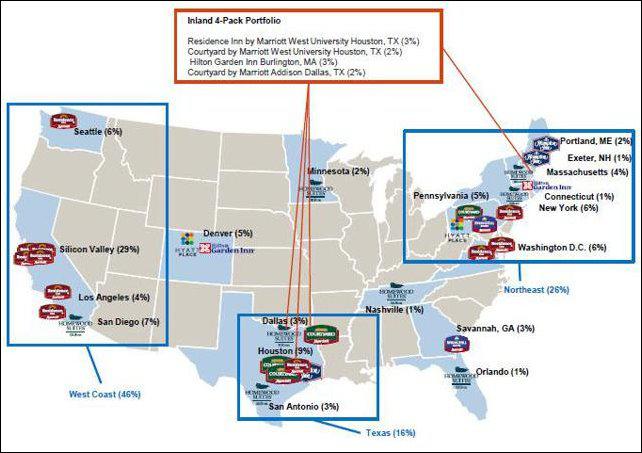

HPT Property Map

With gas prices down and the economy up, both car travel and commercial trucking should have strong demand this year. As such, the travel center aspect of the business should do well.

The company offers a high-yield of ~6% currently, however the five-year dividend CAGR is less impressive at 1.72%. Investors should look at this company to operate in more of a bond-like fashion, with limited dividend increases and a slow increase in the value of the stock.

Conclusion

While many investors have suffered losses from the energy sector as well as many foreign holdings over the past year, one can only look forward to succeed. With the economic conditions ripe for short lease-duration U.S. REITs to advance, the potential return within this area of investment is too alluring to ignore.

When considering hotels, apartments and storage, storage looks expensive with a huge recent run-up while hotels and apartments look appealing. Rather than surrender to index investing, smart investors may choose to strengthen their portfolio with hotel and apartment REITs that are positioned today for continued growth and above-average dividend distributions.

To learn more about CPT, MAA and APTS, please read “Currency Risk: The New Normal,” published February 3, 2015.

To learn more about CLDT and HPT, please read Chatham Lodging Trust: Still An Attractive Yield Play” and “Hospitality Properties Trust: High-Yield Play Continues To Deliver,” both published by Bret Jensen on December 11, 2014 and August 12, 2014, respectively.

To learn more about property sector lease durations and characteristics of these sectors, please read Cohen & Steers July 2014 Viewpoint report, “What History Tells Us About REITs And Rising Rates.”