One month ago, when discussing the most recent trends in the US subprime auto loan space, ZH revealed how despite a virtual halt in direct loans by depositor banks to subprime clients following the financial crisis, the US banking sector now has over a third of a trillion dollars in indirect subprime exposure, in the form of loans to non-banks financial firms which in the past decade have become the most aggressive lenders to America’s sub-620 FICO population.

As we further explained, the banks’ total indirect exposure to subprime loans – not just auto loans, but also subprime mortgages, and subprime consumer loans – could be pieced together through public filings, and according to FDIC reports, bank loans to non-banks subprime lenders soared this decade, with the following 5 names standing out:

- Wells Fargo: $81 billion, up from $13.4 billion in 2010

- Citigroup: $30 billion, up from $4.1 billion in 2010

- Bank of America: $30 billion, up from $2.8 billion in 2010

- JP Morgan: $28 billion, up from $10.4 billion in 2010

- Goldman Sachs: $22 billion

- Morgan Stanley: $16 billion

Visually:

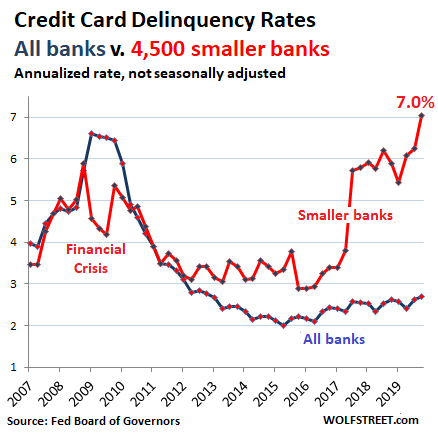

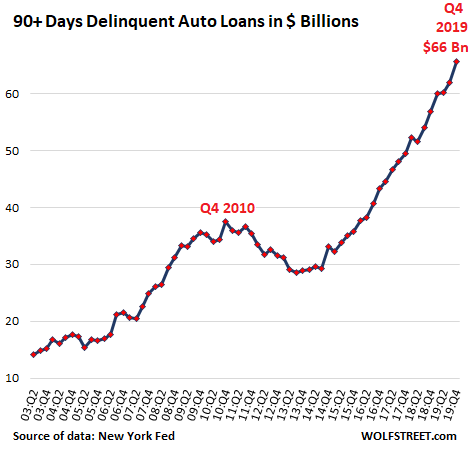

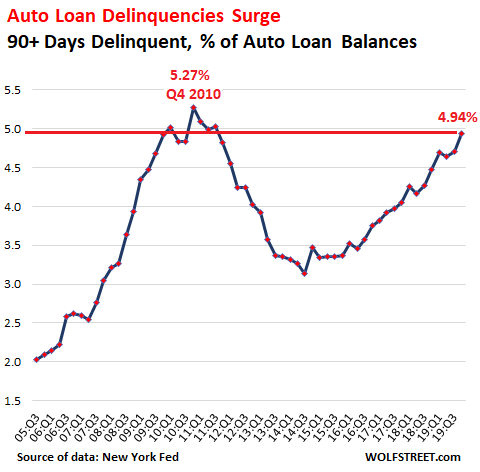

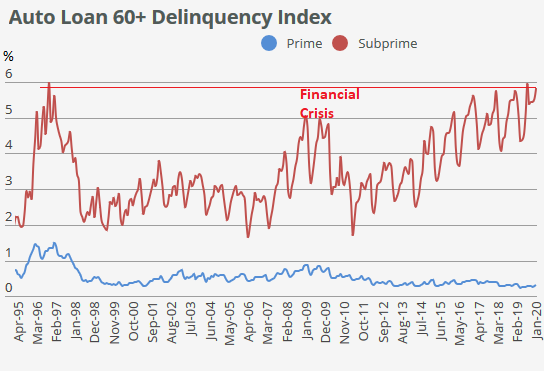

But while the supply side of the subprime equation is clearly firing on all cylinders – as only the next crash/crisis will stop desperate yield chasers – things on the demand side are going from bad to worse, and according to the latest Fitch Autoloan delinquency data, consumers are defaulting on subprime auto loans at a higher rate than during the 2008–2009 financial crisis.

The highly seasonal rate for subprime auto loans more than 60 days past due reached the highest in 22 years – since 1996 – at 5.8%, according to March data; this is well over 2% higher than the comparable March default rate in the low 3%s hit during the peak of the financial crisis a decade ago.

The more recent April data, showed a delinquency rate of 4.3%, higher than the 4.1% last year, and the second highest April on record. Keep in mind, April is the “best” month of the year from a seasonal perspective as that is when the bulk of tax refunds hit, which are then promptly used to repay outstanding bills – it’s all downhill from there… or rather uphill as the chart shows ever higher default rates.

And while delinquencies have been rising, the number of auto loans and leases to subprime borrowers has continued to shrink, falling 10% Y/Y according to Equifax. However, as we showed at the top, it’s not due to supply constraints at the non-bank subprime lenders, the slide in subprime loan volume is all on the demand side: auto-lease origination by subprime customers tumbled by 13.5%.

Meanwhile, as Bloomberg reports, the volume of bond sales backed by these loans are likely to remain the same because banks and credit unions don’t turn most of their loans into securities: “ABS is a fraction of the total auto credit market, which is mainly funded on balance sheets,” Wells Fargo analyst John McElravey told Bloomberg in an interview. “If the pullback from subprime is more from the balance-sheet lenders, banks, then maybe securitization keeps moving along.”

Not maybe: definitely. As the following chart show, the percentage of subprime securitization of all auto ABS as a share of total loans has not only surpassed the pre-crisis peak, it is at a new all time high.

Call it the latest “new (ab)normal” paradox: the underlying auto subprime loan market is shrinking fast, and yet the market for subprime auto ABS securitizations has never been stronger.

Subprime-auto asset-backed security sales are on pace with last year at about $9.5 billion compared to $9.6 billion a year ago, according to data compiled by Bloomberg. With new transactions from Santander, GM Financial, Flagship, and Credit Acceptance expected to hit the market this week, volume may exceed 2017’s total of about $25 billion.

And while it is safe to say it will all end in tears – again – as it did a decade ago, with the next recession the catalyst, the shape of the next crash will be very different. As we explained last month, this subprime bond market is vastly different from what it was even a few years ago, let alone during the last crisis as an influx of generally riskier, smaller lenders flooded into it in the post-crisis years, bankrolled by private-equity money and funded by big bank loans, pursued the riskiest borrowers in order to stay competitive.

“Neither banks nor credit unions have done ‘deep subprime’ lending,” Gunnar Blix, deputy chief economist at Equifax told Bloomberg. “That’s mainly done by smaller dealer-finance and independent finance companies” who rely almost solely on ABS for funding. According to Bloomberg, only about 10% of $437 billion of outstanding subprime auto loans have been securitized into ABS, according to Wells Fargo, which means that underwriters are generally massively exposed to the subprime auto loan crunch that is already playing out before our eyes, and which will be magnified exponentially in the next recession.

* * *

The latest subprime delinquency data seemed confusing, almost a misprint to Hylton Heard, Senior Director at Fitch Ratings who said that “it’s interesting that [smaller deep subprime] issuers continue to drive delinquencies on the index in an unemployment environment of around 4%, low oil prices, low interest rates — even though they are rising — and a positive economic story overall.” In other words, there is no logical explanation why in a economy as strong as this one, subprime delinquencies should be soaring.

Unless, of course the real, unvarnished, and non-seasonally adjusted economy is nowhere near as strong as the government’s “data” suggests.

Making matters worse, rising interest rates have made interest payment increasingly unserviceable for those subprime borrowers who are currently contractually locked up – hence the surge in delinquency rates – or those consumers with a FICO score below 620 who are contemplating taking out a new loan to buy a car, and suddenly find they could no longer afford it, an ominous development we first described one month ago in “Subprime Auto Bubble Bursts As “Buyers Are Suddenly Missing From Showrooms.“

And even if the subprime bubble hasn’t burst just yet, every incremental 0.25% increase in rates assures it is only a matter of time. For once, St. Louis Fed president James Bullard was not wrong when he warned this morning that he sees Fed policy as the reason behind the flattening of the yield curve, saying that “it’s been the Fed, I think, that has flattened the curve more than worries by investors on the state of the global economy.“

“My personal opinion is the Fed does not need to be so aggressive that we invert the yield curve” he noted, adding that “I do think we’re at some risk of an inverted yield curve later this year or early in 2019,” and “if that happens I think it would be a negative signal for the U.S. economy.”

If he’s correct, it begs the question: why is the Fed seeking to crash the economy and, by implication, the market?

We’ll close with a quote from the last Comptroller of the Currency, Thomas Curry, who during an October 2015 speech said that “what is happening in [the subprime auto lending] space today reminds me of what happened in mortgage-backed securities in the run up to the crisis.” It’s only gotten worse since then.

Source: ZeroHedge