Summary

- U.S. equity markets surged this week, buoyed by positive vaccine data and on renewed hopes of a V-shaped economic recovery as countries around the world begin the reopening process.

- The S&P 500 ended the week higher by 3.1%, closing nearly 35% above its lows in late March despite another slate of ugly unemployment data that looms over the recovery.

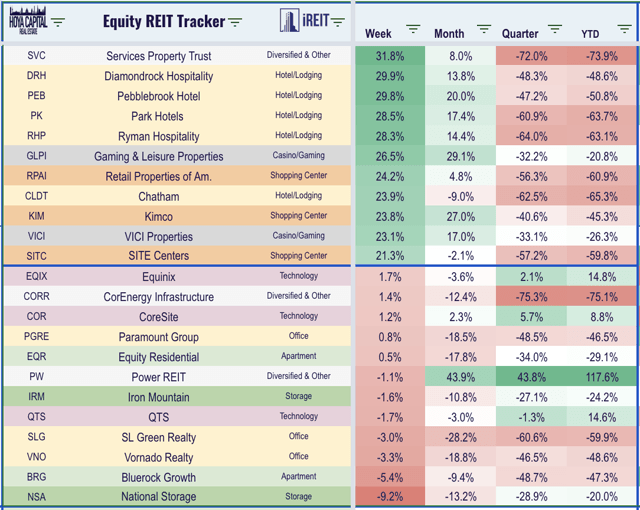

- Real estate equities led the gains this week, propelled by a bounce-back in many of the most beaten-down property sectors including retail and hotels that were ravaged by the lock downs.

- Home builders continued their recent resurgence as high-frequency housing data has indicated that the housing industry may indeed be leaders of the post-coronavirus economic rebound.

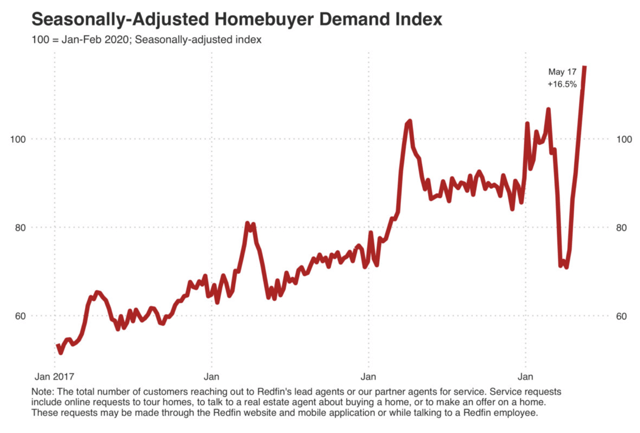

- Fresh data from Redfin showed a “stunning” rebound in housing market activity over the last month as home buying demand is now 16.5% above pre-coronavirus levels while home values have seen accelerating growth.

Real Estate Weekly Outlook

(via Hoya Capital) U.S. equity markets surged this week, buoyed by news of positive clinical trial results from Moderna (MRNA) and Inovio Pharmaceuticals (INO) and on renewed hopes of a V-shaped economic recovery as most states and countries around the world have begun the post-coronavirus reopening process. Contrary to the predictions of some experts, the virus has remained on the retreat even in states that were among the first to reopen, while emerging evidence – detailed in a report by JPMorgan – suggests that lock downs may have actually aggravated rather than mitigated the impacts of the disease. Uncertainty remains, however, over how quickly the economic damage can be reversed and the “shape” of the economic recovery in the back half of 2020.

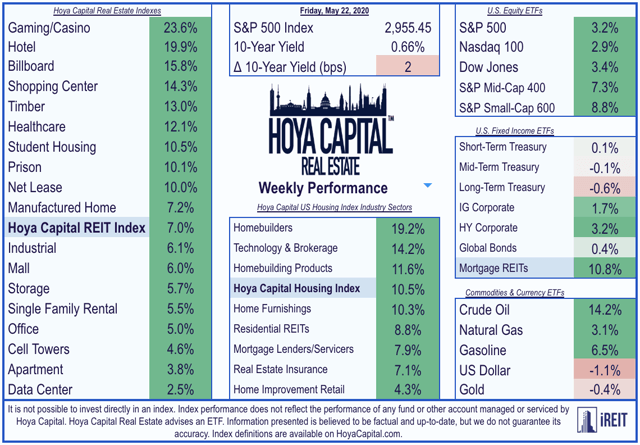

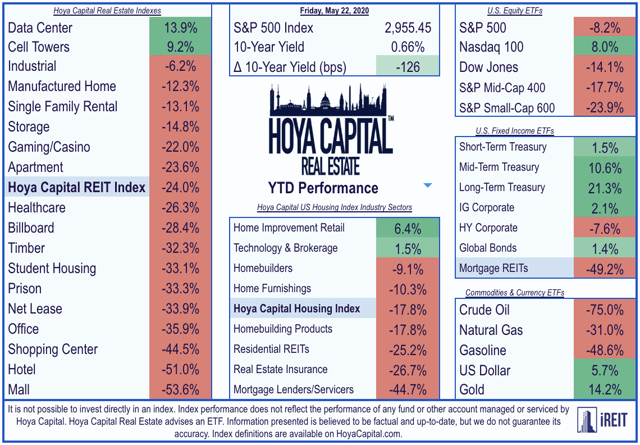

Following a decline of 2.1% last week, the S&P 500 ETF (SPY) ended the week higher by 3.1%, closing nearly 35% above its lows in late March. Real estate equities led the gains this week, reversing almost all of last week’s steep declines, propelled by a bounce-back in many of the most beaten-down property sectors that were ravaged by the economic lock downs. Closing roughly 30% off its lows in March, the broad-based Equity REIT ETFs (VNQ) (SCHH) surged 7.0% with all 18 property sectors in positive territory while Mortgage REITs (REM) jumped 10.8% on the week, closing 55% above its March lows amid clear signs of stabilizing in the mortgage markets.

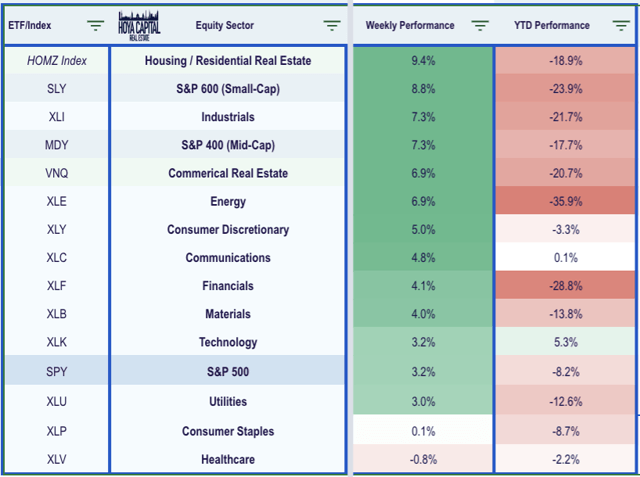

The more pronounced strength this week was seen in the recently lagging Mid-Cap (MDY) and Small-Cap (SLY) indexes which delivered strong out performance, surging by 7.3% and 8.8% respectively. The gains this week came despite another round of ugly economic data including Initial Jobless Claims data that showed that another 2.43 million Americans filed for unemployment benefits last week, bringing the eight-week total to over 38 million. However, flashes of strength have become increasingly more evident in recent weeks – particularly in the all-important U.S. housing market – and commentary from corporate earnings reports over the last two weeks indicated that the economic rebound is already beginning to take hold in many segments of the economy. The Industrials (XLI), Energy (XLE), and Consumer Discretionary (XLY) sectors joined the real estate sectors as top-performers on the week while Healthcare (XLV) was the lone sector in the red.

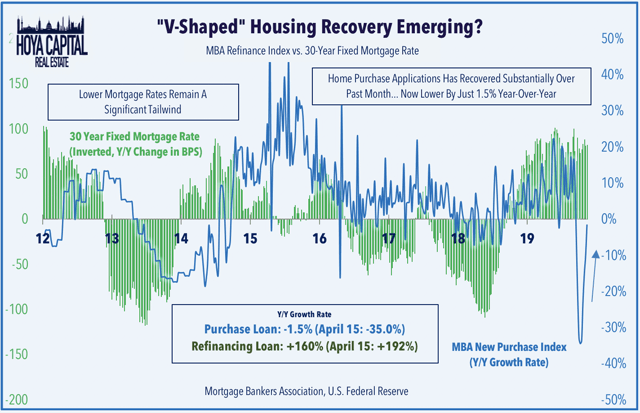

Home builders and the broader Hoya Capital Housing Index were among the standouts this week as recent high-frequency housing data has indicated that the housing market may indeed be the leader of the post-coronavirus economic rebound. The gains came following fresh data from Redfin (RDFN) that showed a “stunning” rebound in housing market activity over the last month as home buying demand is now 16.5% above pre-coronavirus levels on a seasonally-adjusted basis, gains which have been “driven by record-low mortgage rates as pent-up demand is unleashed.” This data was broadly consistent with recent commentary from home builders and data released earlier this week from the Mortgage Bankers Association which showed that home purchase mortgage applications rose for the 5th straight week and are now lower by just 1.5% from last year compared to the 35% decline in April.

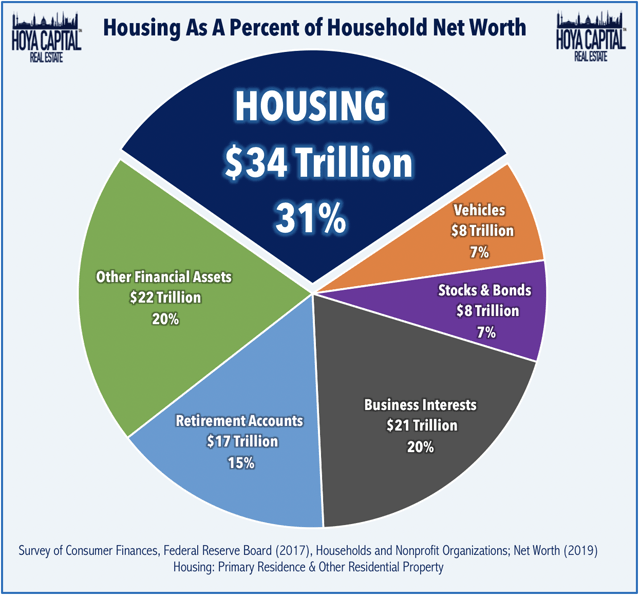

As goes the U.S. housing market, so goes the U.S. economy. Residential real estate is by far the most significant asset on the aggregate U.S. household balance sheet and the value of the U.S. housing market is larger than the combined market capitalization of every U.S. listed company. As we’ve discussed for many years, it’s impossible to overstate the importance of the U.S. housing market in forecasting macroeconomic trends for the broader economy and just as it was impossible to avoid a deep and lasting economic recession from the sub-prime housing crisis, it is difficult to envision the “depression-like” economic environment forecasted by some analysts without first seeing substantial instability in the housing market. While very early in the economic recovery, we’re so far observing quite the opposite as the combination of favorable millennial-led demographics, record-low mortgage rates, and a substantial under supply of housing units after a decade of historically low levels of new construction continue to be relentless tailwinds.

Real Estate Earnings Season Wrap-Up

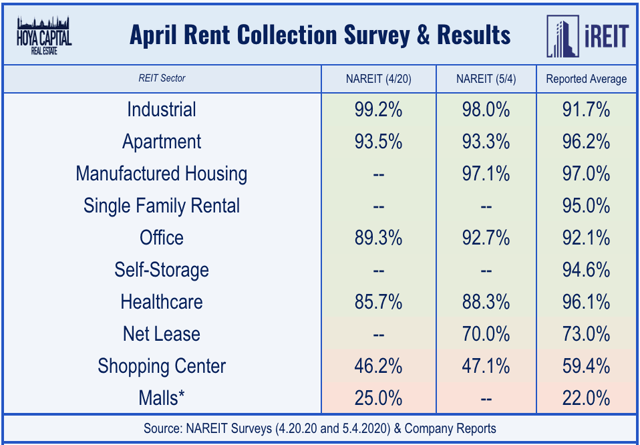

While the residential real estate sector may be an area of relative out performance during the post-coronavirus economic recovery, other areas of the commercial real estate sector face a more uncertain future. Real estate earnings season wrapped up this week with a handful of late-reporting stragglers, so the final numbers for rent collection are now in. Rent collection has been largely a non-issue for residential, industrial, and office REITs, as each sector has collected over 90% of April rents. For retailers, if you’re not essential, you’re not probably paying the rent. Collection among mall REITs averaged around 22% while shopping center REITs collected roughly 60% of April rents and net lease REITs collected 73% of rents.

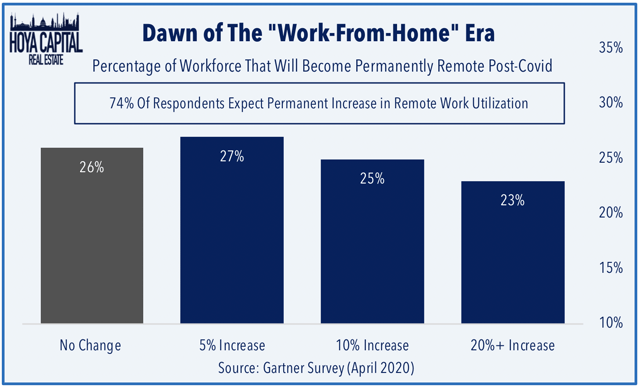

Even among the commercial REIT sectors that reported solid rent collection in April, there are some areas of concern regarding their respective long-term outlook in the post-coronavirus world. Earlier this week, we published Office REITs: Coronavirus Killed Corporate Culture. Office REITs have been pummeled during the coronavirus pandemic amid mounting questions over the long-term demand outlook as businesses become increasingly more comfortable with “remote work” environments as reports surfaced this week that Facebook (FB) and others plan to permanently shift workers to work-from-home arrangements. Zoom (ZM) and “work-from-home” technology suites have emerged as the bigger competitive threat to the office REIT sector as more than half of the companies expect to shrink their physical footprint.

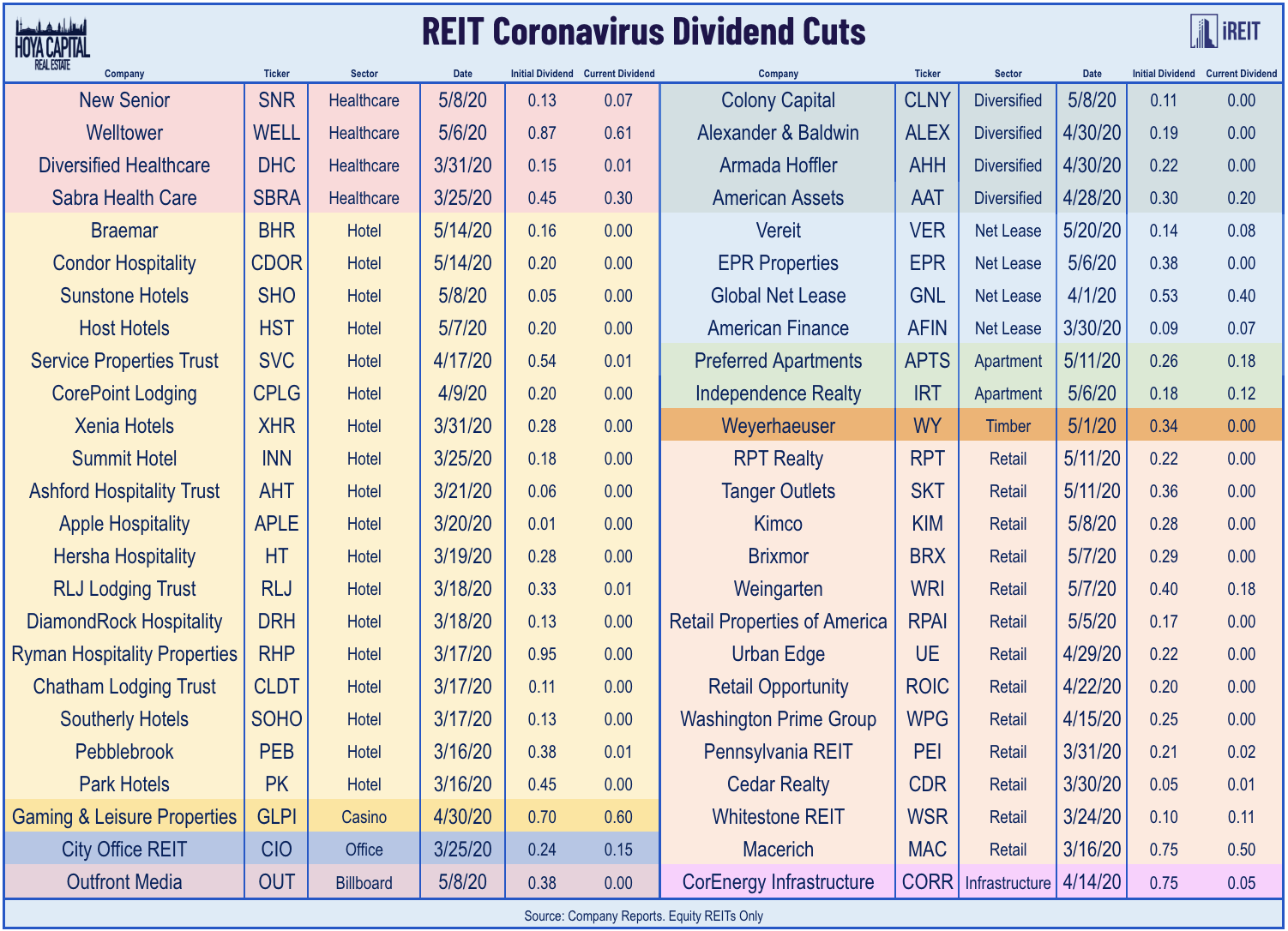

Two more equity REITs were added to the Coronavirus Dividend Cut list this week: net lease REIT VEREIT (VER) and Braemar Hotels (BHR). We’ve now tracked 50 equity REITs in our universe of 165 names to announce a cut or suspension of their dividends, the vast majority of which have come from the retail and hotel REIT sectors. Apart from their sector affiliations, the equity REITs that have cut or suspended their dividends have been almost exclusively companies in the smallest third of market capitalization within the REIT sector and in the highest third in terms of leverage metrics as the “outperforming factors” that we discussed earlier this year in The REIT Paradox: Cheap REITs Stay Cheap have been on full display in 2020.

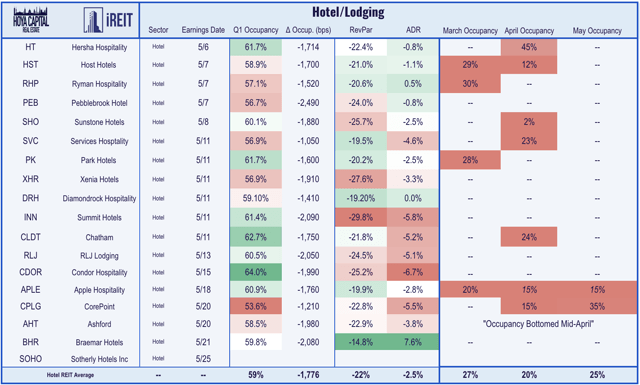

Among the handful of stragglers to report results this week were four hotel REITs including the aforementioned Braemar Hotels along with Apple Hospitality (APLE), CorePoint (CPLG), and Ashford (AHT). While Q1 occupancy and Revenue Per Available Room (RevPAR) metrics were understandably ugly across the hotel REIT sector, commentary on earnings calls this week suggested that we’ve likely seen the worst of the occupancy declines as Ashford’s management noted that “occupancy continues to increase on a weekly basis. We are seeing pick-up of room nights on a short-term basis and the pace of that pickup is increasing almost daily.”

All 18 REIT sectors finished in positive territory this week as hotel and casino REITs including Gaming & Leisure Properties (GLPI) and VICI Properties (VICI) were among the top performers this week as a growing number of hotels and casino properties across the country have announced plans to re-open over the next several weeks. Shopping center REITs, particularly those focused on the big-box segments like Retail Properties of America (RPAI), Kimco Realty (KIM), and SITE Centers (SITC), were also leaders this week after generally positive commentary on reopening plans from several big-box retailers including Best Buy (BBY). The technology REIT sectors – data centers and cell towers – were among the laggards this week, but remain the only two REIT sectors in positive territory on the year.

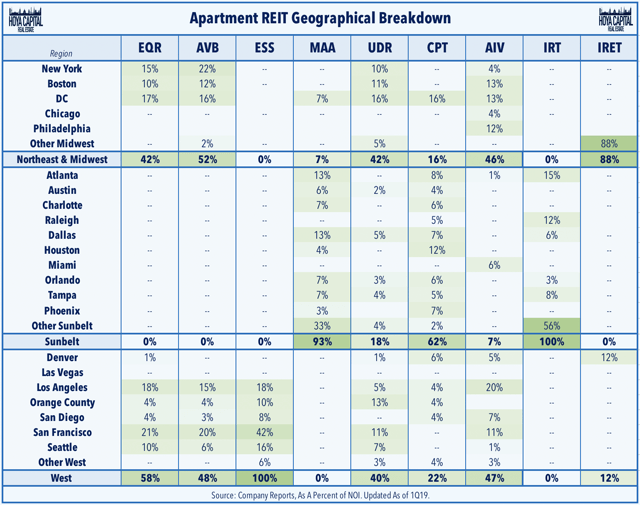

This week, published Apartment REITs: No Rent Strike, But Fears Of Urban Exodus. We discussed how apartment REITs reported limit issues with rent collection in April and early-May amid the depths of the pandemic-related shutdowns as more than 95% of rents were collected. Ultra-dense metros like NYC, Chicago, and San Francisco, however, may see lasting pain as residents flee to lower-cost and “safer” semi-urban and suburban markets, including faster-growing Sunbelt metros. Several REITs are more exposed than others from this trend and we detailed the geographical exposure of the nine largest multifamily REITs. As one of the more defensively-oriented and counter cyclical REIT sectors, we remain bullish on long-term rental fundamentals.

Mortgage REITs

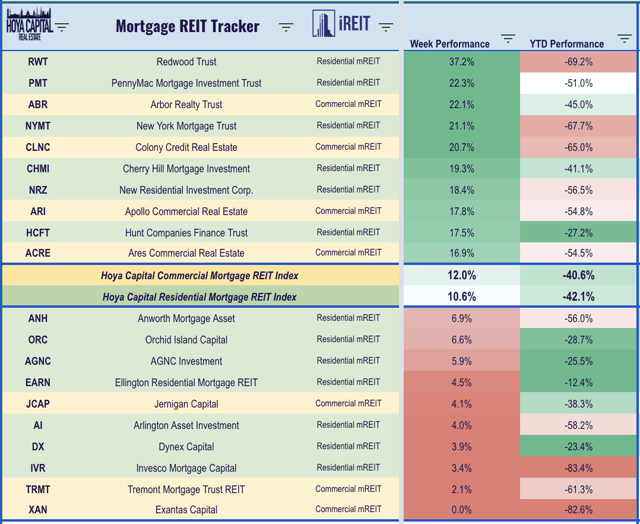

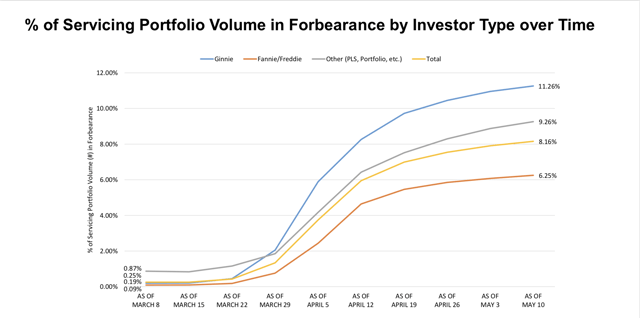

Strong housing market data over the last several weeks has been good news for mortgage REITs as well as residential mREITs jumped another 10.6% this week while commercial mREITs gained 12.0%, each rebounding more than 50% from their lows in early April. New York Mortgage REIT (NYMT) was among the leaders this week after reporting solid Q1 results. New Residential (NRZ) was also among the leaders after providing an interim update in which it noted that had bolstered its liquidity position through an additional capital raise and noting that forbearance requests have continued to be lower than previously forecasted.

Helping the residential mREITs this week was news the FHFA has issued temporary guidance that should make it easier for homeowners who have taken advantage of COVID forbearance programs to refinance or buy a new home. Borrowers will be allowed to get a new mortgage three months after their forbearance period ends and they have made three consecutive payments under their repayment plan. Roughly 9% of mortgage loans representing roughly 4.75 million homeowners are now in forbearance, according to data released this week from Black Knight (BK), but a recent survey from LendingTree found that the majority of these borrowers chose to enter forbearance not out of necessity but simply because it was offered and available without any apparent penalty under the CARES Act.

Real Estate Economic Data

Below, we analyze the most important macroeconomic data points over the last week affecting the residential and commercial real estate marketplace.

Housing Recovery Has Already Begun

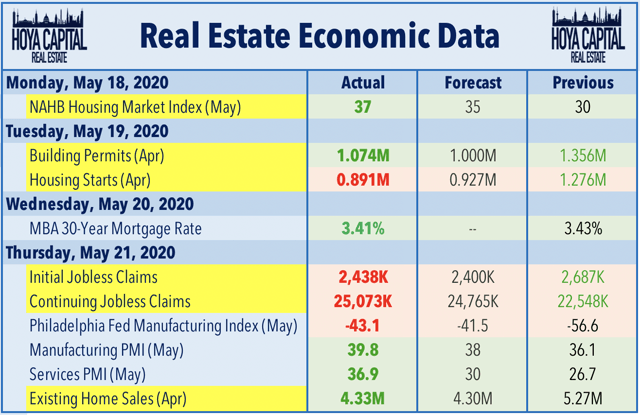

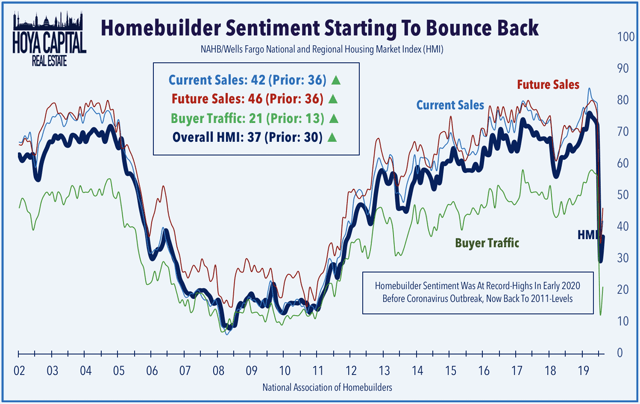

Home builder Sentiment data released on Monday showed that confidence among home builders – particularly in the Southern region where the majority of publicly-traded home builders are based – has begun to bounce back from the lows in April. The NAHB Housing Market Index climbed to 37 from last month’s reading of 30, driven by a 12-point rebound in Future Sales expectations and an 8 point bounce in Buyer Traffic. Consistent with recent reports from other home builders, Meritage Home (MTH) announced this week that it believes that May orders could be “in line” with last May’s as the strong sales momentum seen during the last two weeks of April has carried over into early May.

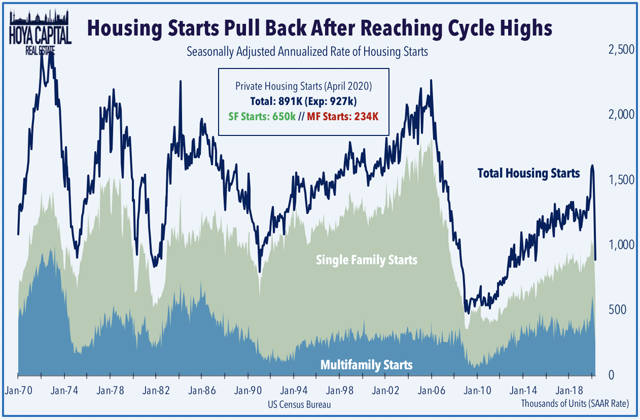

The U.S. housing industry was red-hot before the onset of the coronavirus crisis with Housing Starts, Building Permits, and New Home Sales all eclipsing post-cycle highs in early 2020. Backward-looking data released this week by the U.S. Census Bureau showed the magnitude of the decline in construction activity in April amid the worst of the pandemic. On a seasonally-adjusted annualized basis, housing starts and building permits fell to the lowest level since 2015 in April at 891k and 1,074k units, respectively, following a relatively solid March. Single-family starts and permits were actually quite a bit stronger than expected while the always volatile multifamily construction activity showed sharper declines in April.

Existing Home Sales also beat expectations in April, coming in at 4.33 million versus expectations of 4.30 million. Home purchase mortgage applications – a leading indicator of Existing Home Sales – rose for the 5th straight week and are now remarkably lower by just 1.5% from last year compared to the 35% decline in April according to data released this week by the Mortgage Bankers Association. The 30-Year Mortgage rate remains lower by roughly 90 basis points from the same week last year, a level of decline in mortgage rates that has historically been strongly correlated with robust growth in housing market activity under normal conditions.

2020 Performance Check-Up

REITs are now lower by roughly 24.0% this year compared with the 8.2% decline on the S&P 500 and 14.1% decline on the Dow Jones Industrial Average. Consistent with the trends displayed within the REIT sector, mid-cap and small-cap stocks continue to under perform their larger-cap peers as the S&P Mid-Cap 400 and S&P Small-Cap 600 are lower by 17.7% and 23.9%, respectively. The top-performing REIT sectors of 2019 have continued their strong relative performance through the early stages of 2020 as data centers and cell tower REITs remain the real estate sectors in positive territory for the year, while industrial and residential REITs have also delivered notable out performance. At 0.66%, the 10-Year Treasury Yield has retreated by 126 basis points since the start of the year and is roughly 260 basis points below recent peak levels of 3.25% in late 2018.

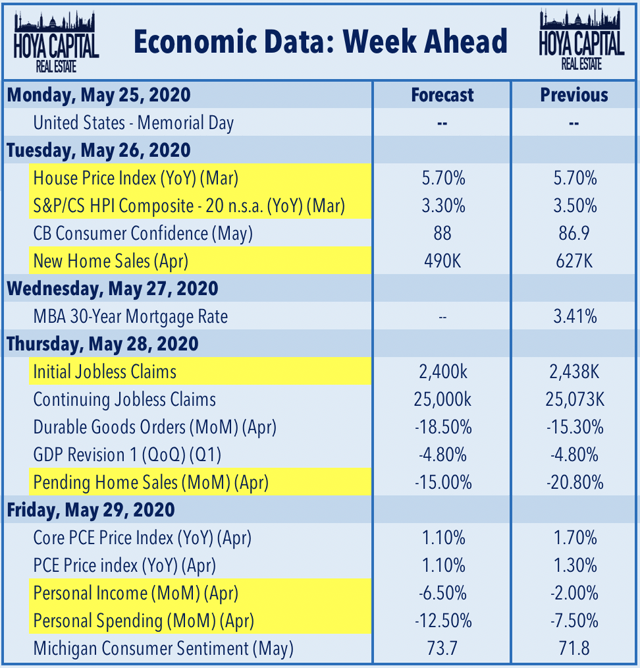

Next Week’s Economic Calendar

A busy two-week stretch of housing data continues next week with Home Price data from the FHFA and S&P Case-Shiller on Tuesday which is expected to show a steady rise in home prices in March during the early stages of the pandemic. New Home Sales data for April is also released on Tuesday while Pending Home Sales data for April is released on Thursday. Initial Jobless Claims data on Thursday will again be another “blockbuster” report with expectations that we will see another 2.5 million job losses, but we’ll be watching closely to the continuing claims for indications that temporarily-unemployed Americans are returning to work.