This is as close to a failed auction as we have ever come…

Ahead of today’s closely watched 7Y treasury auction, where the bulk of the recent Treasury rout has been concentrated as traders hammered the belly of the curve, we said that “If the 7Y tails a lot, watch out below” as that would only add insult to today’s furious selloff injury. Well, that’s precisely what happened, because with the 7Y pricing at 1.195%, this was a whopping 4.1bps tail to the 1.151% When Issued.

If the 7Y tails a lot, watch out below

— zerohedge (@zerohedge) February 25, 2021

The auction was, in a word, catastrophic.

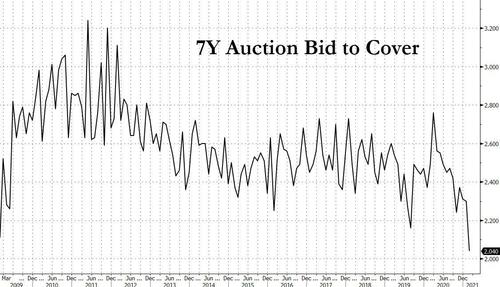

Starting at the top, the bid to cover tumbled from 2.305 to 2.045, the lowest on record, and far, far below the 2.35 recent average.

But if that was ugly, the internals were even worse, with the Indirects plunging from 64.10% to just 38.06%, the lowest since 2014, as no foreigner suddenly wants to even smell US debt!

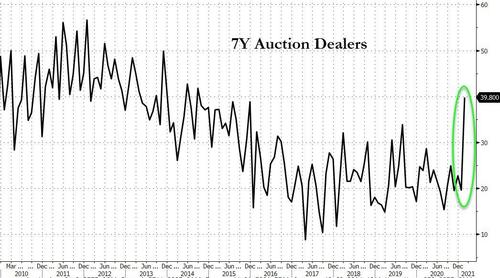

And with the collapse in Indirects, and Directs taking down 22.13%, the highest since Jun – perhaps simply because there was no Indirect demand at all – Dealers we left with a whopping 39.81%, the highest since 2014 as nobody else wants the paper.

In short- this was an absolutely catastrophic 7Y auction, the ugliest in years, and it came at the worst possible time – just as the curve was selling off on inflation fears.

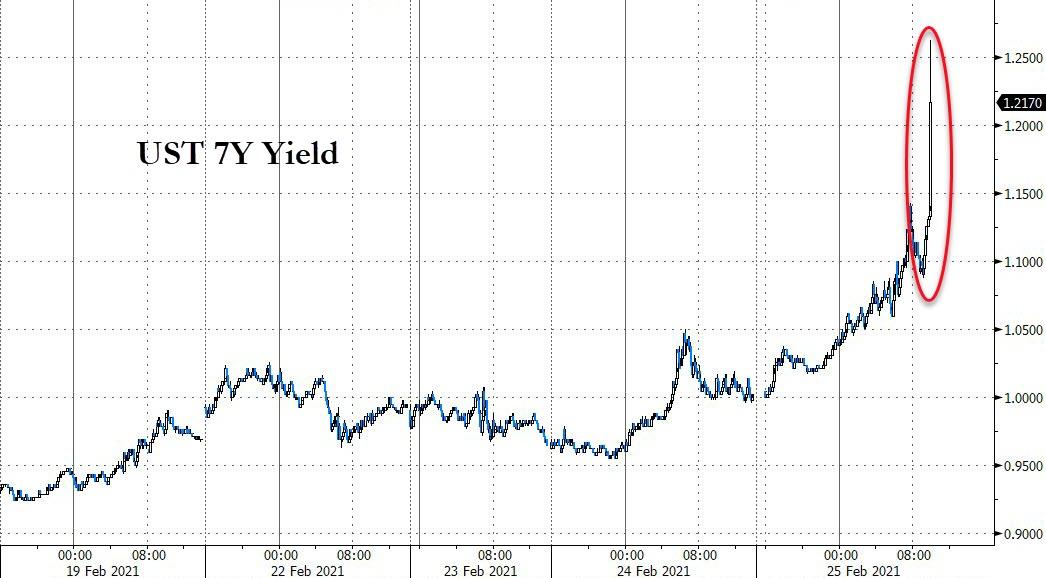

The result has been an instant spike in 10Y yields, which blew out more than 10bps, surging as high as 1.60% before reversing some losses.

The Fed better do YCC NOW, or else we are about to find out just how much absolute bullshit MMT really is.