Sky news reportsthat Twitter is preparing to prohibit a range of cryptocurrency advertisements amid looming regulatory intervention in the sector.

The microblogging platform is following similar moves by Facebook and Google which have restricted financial advertisements due to concerns about illicit activities.

Sky News understands that the new advertising policy will be implemented in two weeks and currently stands to prohibit advertisements for initial coin offerings (ICOs), token sales, and cryptocurrency wallets globally.

The reaction was swift, just as we have seen to the other crypto ad bans… smashing Bitcoin back below $7500 (into mystery-dip-buyer territory)…

But Ethereum and Ripple have been the worst performers since the crypto ad bans began…

Reportedly, Twitter has experienced an influx of fake accounts pretending to advertise cryptocurrency giveaways, often by users posing asfamous crypto sphere personaslikeLitecoin’sCharlie Lee.

Just about a month or so ago, many agents where laughing about Bitcoin, blockchain, and other cryptocurrencies, talking about how people won’t use it to buy real estate. Hmmm…

Where did this transaction happen?

In Burlington, Vermont.

The first property to be sold this way in the United States.

It was sold entirely through the blockchain. Completely.

Ethereum was the token used. This puts Vermont on the map.

Propy is a company in San Francisco. Propy handled the entire transaction including recording of the documents and contracts instead of using the city system.

Vermont is the first state to allow this kind of transaction and soon coming up are Colorado and Arizona.

The encryption technology in blockchain is the best available at this time.

This transaction used cryptocurrency for the purchase and it was then turned into the fiat money on the other end.

The first Bitcoin to Bitcoin transaction in the United States was when Michael Komaransky sold his Miami mansion for 455 Bitcoin which was the most expensive Bitcoin real estate transaction to date.

While most people will still not do a cryptocurrency real estate transaction, it is here, and it will be here to stay.

The different tokens will fail and others will rise. Ethereum is very stable. Blockchain is here to stay and evolve.

Speculative booms are often poor guides to future valuations and the maturation trajectory of a new sector.

Charles Hugh Smith recently came across a December 1996 San Jose Mercury News article on tech pioneers’ attempts to carry the pre-browser Internet’s bulletin board community vibe over to the new-fangled World Wide Web.

In effect, the article is talking about social media a decade before MySpace and Facebook and 15 years before the maturation of social media.

(Apple was $25 per share in December 1996. Adjusted for splits, that’s about the cost of a cup of coffee.)

So what’s the point of digging up this ancient tech history?

— Technology changes in ways that are difficult to predict, even to visionaries who understand present-day technologies.

— The sources of great future fortunes are only visible in a rear view mirror.

Many of the tech and biotech companies listed in the financial pages of December 1996 no longer exist. Their industries changed, and they vanished or were bought up, often for pennies on the dollar of their heyday valuations.

Which brings us to cryptocurrencies, which entered the world with bitcoin in early 2009.

Now there are hundreds of cryptocurrencies, and a speculative boom has pushed bitcoin from around $600 a year ago to $2600 and Ethereum, another leading cryptocurrency, from around $10 last year to $370.

Where are cryptocurrencies in the evolution from new technology to speculative boom to

maturation? Judging by valuation leaps from $10 to $370, the technology is clearly in the speculative boom phase.

If recent tech history is any guide, speculative boom phases are often poor guides to future valuations and the maturation trajectory of a new sector.

Anyone remember “push” technologies circa 1997? This was the hottest thing going, and valuations of early companies went ballistic. Then the fad passed and some new innovation became The Next Big Thing.

All of which is to say: nobody can predict the future course of cryptocurrencies, other than to say that speculative booms eventually end and technologies mature into forms that solve real business problems in uniquely cheap and robust ways no other technology can match.

So while we can’t predict the future forms of cryptocurrencies that will dominate the mature marketplace, we can predict that markets will sort the wheat from the chaff by a winnowing the entries down to those that solve real business problems (i.e. address scarcities) in ways that are cheap and robust and that cannot be solved by other technologies.

The ‘Anything Goes’ Speculative Boom

Technologies with potentially mass applications often spark speculative booms. The advent of radio generated a speculative boom just as heady as any recent tech frenzy.

Many people decry the current speculative frenzy in cryptocurrencies, and others warn the whole thing is a Ponzi scheme, a fad, and a bubble in which the gullible sheep are being led to slaughter.

Tribalism is running hot in the cryptocurrencies space, with promoters and detractors of the various cryptocurrencies doing battle in online forums: bitcoin is doomed by FUD (fear, uncertainty and doubt) about its warring camps, or it’s the gold standard; Ethereum is either fundamentally flawed or the platform destined to dominate, and so on.

The technological issues are thorny and obtuse to non-programmers, and the eventual utility of the many cryptocurrencies is still an open question/in development.

It’s difficult for non-experts to sort out all these claims. What’s steak and what’s sizzle? We can’t be sure a new entrant is actually a blockchain or if its promoters are using blockchain as the selling buzzword.

Even more confusing are the debates over decentralization. One of the key advances of the bitcoin blockchain technology is its decentralized mode of operation: the blockchain is distributed on servers all over the planet, and those paying for the electricity to run those servers are paid for this service with bitcoin that is “mined” by the process of maintaining the blockchain. No central committee organizes this process.

Critics have noted that the mining of bitcoin is now dominated by large companies in China, who act as an informal “central committee” in that they can block any changes to the protocols governing the blockchain.

Others claim that competing cryptocurrencies such as Ethereum are centrally managed, despite defenders’ claims to the contrary.

Meanwhile, fortunes are being made as speculators jump from one cryptocurrency to the next as ICOs (initial coin offerings) proliferate. Since the new coins must typically be purchased with existing cryptocurrencies, this demand has been one driver of soaring prices for Ethereum.

As if all this wasn’t confusing enough, the many differences between various cryptocurrencies are difficult to understand and assess.

While bitcoin was designed to be a currency, and nothing but a currency, other cryptocurrencies such as Ethereum are not just currencies, they are platforms for other uses of blockchain technologies, for example, the much-touted smart contracts. This potential for applications beyond currencies is the reason why the big corporations have formed the Enterprise Ethereum Alliance (https://entethalliance.org/).

Despite the impressive credentials of the Alliance, real-world applications that are available to ordinary consumers and small enterprises using these blockchain technologies are still in development: there’s lots of sizzle but no steak yet.

Who Will The Winner(s) Be?

How can non-experts sort out what sizzle will fizzle and what sizzle will become dominant? The short answer is: we can’t. An experienced programmer who has actually worked on the bitcoin blockchain, Ethereum and Dash (to name three leading cryptocurrencies) would be well-placed to explain the trade-offs in each (and yes, there are always trade-offs), but precious few such qualified folks are available for unbiased commentary as tribalism has snared many developers into biases that are not always advertised upfront.

So what’s a non-expert to make of this swirl of speculation, skepticism, tribalism, confusing

technological claims and counterclaims and the unavoidable uncertainties of the exhilarating but dangerously speculative boom phase?

There is no way to predict the course of specific cryptocurrencies, or the potential emergence of a new cryptocurrency that leaves all the existing versions in the dust, or governments’ future actions to endorse or criminalize cryptocurrencies. But what we can do — now, in the present — is analyze present-day cryptocurrencies through the filters of scarcity and utility.

InPart 2: The Value Drivers Of Cryptocurrency, we analyze the necessary success requirements a cryptocurrency will need to excel on in order to become adopted at a mass, mainstream level. Once this happens (which increasingly looks like a matter of “when” not “if”), the resultant price increase of the winning coin(s) will highly likely be geometric and meteoric.

Sadly, the most probable catalyst for this will be a collapse of the current global fiat currency regime — something that increasingly looks more and more inevitable. This will destroy a staggering amount of the (paper) wealth currently held by today’s households. Which makes developing a fully-informed understanding of the cryptocurrency landscape now — today — an extremely important requirement for any prudent investor.

I was wrong about Ethereum because it’s such a good store of value…

no wait, let me try again.

I was wrong about Ethereum because it’s such a decentra…

nope.

I was wrong about Ethereum because everyone is using it as a supercomputer…

No.

I do admit I didn’t see this Ethereum bubble coming, but then again I wrongly assumed that no startup would need or even dare to ask $50 million in funding and I also wrongly assumed that people would use common sense and that leading developers would speak out against this sort of practice. Quite the opposite it seems.

Ethereum’s sole use case at the moment is ICOs and token creation.

What’s driving the Ethereum price?

Greed.

Greed from speculators, investors and developers.

Can you blame them?

Speculators and investors: No.

Developers: Absolutely.

So let’s think for a minute and think what determines the price? Supply + demand. Pretty straightforward.

Supply: the tokens that are available on the market, right? But with every ICO there are more tokens that are being “locked up”. Obviously the projects will liquidate some, to get fiat to pay for development of their project, but they also see the rising price of Ethereum. So at that point greed takes over and they think, totally understandable, “We should probably just cash out what we really need and keep the rest in ETH, that’s only going up anyway it seems.” And obviously there are new coins being mined, but if you look at the amount of ETH these ICOs raise, at this point, it’s just a drop in a bucket.

Demand: You have the normal investors (who are already very late to the game at this point… as usual), but the buy pressure that these ICOs are creating is crazy and scary. Take TenX for example, it’s an upcoming ICO at the end of the month. The cap is 200,000 ETH (at current ETH price of $370) that’s $74,000,000 for a startup. Here’s the best part: it’s only 51% of the tokens. Effectively giving it an instant $150 million valuation (if it sells out, which it probably will). Another example is Bancor, a friend of mine runs a trading group, he collected 1,100+ BTC to put into Bancor. This needs to be converted into ETH before the sale starts. These are decent size players, but not even the big whales who participate in these ICOs.

What will the price do next?

It can go quite a bit higher, there are so many coins being taken off the market by these ICOs, that it can still continue for a while and everyone is seeing this and thinking: “Why aren’t I doing an ICO”. There are lots more coming.

At one point it will crash, hard. What the trigger will be? Bug(s) in smart contracts, major hack, big ICO startup that fails/fucks up, network split, even something as silly as not having a decent ICO for a couple of weeks which creates sell pressure from miners and ICO projects can cause a big crash. It’s not a question of “if”, it’s a question of “when”. That being said: Markets can remain irrational for quite a long time.

Usually when a bubble like this pops we could easily see 70–80% loss of value (for reference: Bitcoin went from $1,200 to $170 after 2013–2014 bubble). This is however quite the unusual situation and I’m not sure to what kind of bubble I can really compare it.

I’m sure most of you have seen “Wolf of Wall Street”. Just re-watch this clip and see if you find any similarities with the current situation. (bonus clip)

What I really find interesting is what the ICO startups will do, Bitcoin had hodlers and investors mainly, individuals who most of the time had a fulltime job and didn’t need to sell. With Ethereum there is this huge amount being held by companies who need to pay bills. Will they panic dump to secure a “healthy” amount of fiat funding, will they try to hold through a bear cycle?

Taking Responsibility:

Everyone loves making money, you can’t blame traders or investors from taking advantage of this hype. That would be silly. People will buy literally anything if they can make a quick buck out of it.

The responsibility here is with the developers, Consensys and the Ethereum Foundation but they don’t take responsibility since they’re getting more money. This will end with the regulators stepping in.

The reason why I say that it’s with developers, Consensys and the Ethereum Foundation is simple:

The developers of a project assign these crazy token sale caps, more money than any startup would ever need.

The Ethereum foundation members+ core developers use their own celeb status to actively promote these projects as advisors, for which they’re compensated well, luring in people who have no clue what they’re buying.

Consensys promotes all of this since it’s the marketing branch of Ethereum. The more fools that buy in, the better.

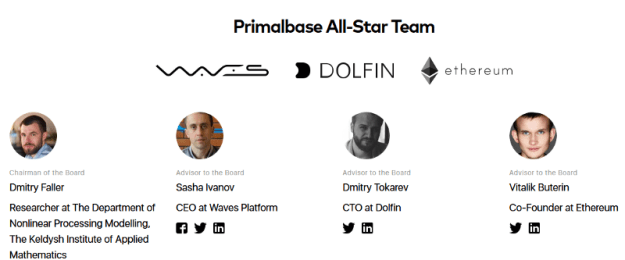

Let me illustrate this with an example. Have you heard of primalbase? It’s an ICO with a token for shared work spaces. Why would a shared work space need its own token? It doesn’t, it really really really doesn’t. Let’s take a look at the advisors:

First thing that an advisor should’ve said in this case was: “Don’t do it, it’s stupid, it makes no sense.” But well there we have Mr Ethereum himself.

We all know that Vitalik has a cult-like following with the Ethereum investors so it will be very easy for primal base to launch their ICO and use Vitalik’s face and name to get itself funded.

This is just one example, if you go through all of these ICOs you find a lot of familiar names and faces. Nothing wrong with being an advisor, but when you’re just sending people to the slaughterhouse…

The sad part is that a lot of people will lose a lot of money on this, some of them obviously more than they can afford to lose, that’s how it always goes. The regulators will step in after this bubble pops and what scares me is the fact that it will damage all of crypto, including Bitcoin, not just Ethereum and its ICO’s.

But you’re just an Ethereum hater

I’ve heard all the accusations:

I hate Ethereum because I’m a Bitcoin Maximalist. I’m not, I like other projects too, like Siacoin for example.

I hate Ethereum because I missed out. I did miss out on the crowdsale, but I traded plenty of Ethereum and it’s ICOs and made some nice profit.

I hate Ethereum because I don’t understand it. Really? Do you? The only smart contracts running on it are ICO token sales. Or contracts to buy ICO tokens the second they become available.

I hate Ethereum because I’m jealous of Vitalik. No, it’s impressive what he did at his young age. At the same time I think he’s largely responsible for this bubble and he has made a lot of mistakes. We all make mistakes, but bailing out your friends from the DAO while other hacks and losses aren’t compensated or fixed just shows total lack of integrity. Or it’s everything or it’s nothing. And when it comes to immutability in crypto, it should be nothing.

For the people that are scared that Ethereum will replace Bitcoin

Ethereum is not a store of value. It isn’t capped. Yes, I know they’re planning to switch to PoS (which it already kind of is). Do you think they managed to create the first software implementation ever without any bugs? Doing such a major change on a (currently) $30 billion market is completely irresponsible, borderline insanity. Even if we assume that there are no bugs, what about the miners? The miners who bought their equipment to mine Ethereum, the miners that supported the network for years. “But they knew we were switching to PoS.” Of course they knew, and do you think they’ll just give up on such a profitable coin? Some might switch immediately to Zcash and Ethereum Classic but there will be another fork and we’ll have ETHPoS and ETHPoW, with of course all the Ethereum tokens being on both chains. Even Ethereum developers think that his is a very likely scenario.

Ethereum’s fees are lower. They are, sometimes, by a bit. If you’re trying to send something when no token sale is active obviously, else you have people spending $100’s to get in on the token sale and clog up the network. Also doesn’t apply when you send something from exchanges since for example with Poloniex it’s about $1.9 vs $0.28 for Bitcoin. Oh and another exception is when you actually use it for smart contracts, which require more gas to process than a normal transactions from account A to account B. You know.. the actual reason why Ethereum was created.

Ethereum is not decentralized. Bitcoin isn’t as decentralized as it should be, we all know that, but compared to most other coins, Bitcoin is very decentralized. Vitalik has called himself a benevolent dictator in the past. He is the single point of failure in this project and if he gets compromised in any way that’s the end. There is no way of knowing if this happens and since people blindly follow everything he says, he has the power to do anything. Satoshi was smart enough to remove himself from the Bitcoin project.

Ethereum is not immutable. Don’t have to spend much time on this: see DAO and split that lead to Ethereum and Ethereum Classic.

Ethereum has the Enterprise Ethereum Alliance. But but but.. all those big banks use Ethereum. No, they don’t. They use “an” Ethereum, which is a (private) fork of Ethereum. By that definition 99% of all altcoins are using Bitcoin. Still a separate chain. The fact that we’re talking about a private blockchain here actually makes altcoins more like Bitcoin than “an Ethereum” that EEA uses like Ethereum. You can compare it to 2013–2014 when some companies started to get interested in blockchain vs Bitcoin, only difference here is that for Ethereum it’s part of their marketing campaign to lure in potential investors.

If you think I’m just full of crap, which is fair, I am just some random popular guy on Twitter who has been around from before Ethereum. Have a look at what Vlad has to say about the current state of Ethereum here and here. Vlad Zamfir is probably the smartest guy on the Ethereum team, and I say this while I don’t agree with him on many of his opinions, I do respect him.

Conclusion:

If you’re an actual developer, be realistic and honest with your investors. Do you really ever need more than $5 mill? Finish a MVP first and then do a tokensale, if you really really need to do an ICO. Plenty of rich crypto investors and traders now that would love to be part of your project and who would be happy to just invest for equity. Yes, it will probably be less than what you can get in an ICO, but at least you didn’t sell out and it shows you actually really care about your product/service/…

If you’re a trader or investor, be realistic about the bubble. I know you hear this a 100 times when you’re trading but: don’t invest what you can’t afford to lose. I have some Ethereum, not as a long term investment, but because the price is going up and I need it to invest in tokens which I can quickly flip as soon as they come on the market. That’s just the type of market we’re in. Everyone is making a lot of money, awesome right? What could potentially go wrong.

(The International Reporter, Editor’s Note): Let me remind Bundesbank and all the other banks, that after the 2008 crisis and the ‘too big to fail”criminality that since then has stolen tax payers money globally, that nobody is interested in the banking industry anymore. Along with their compounding interest rates they are seen as liars, cheats, thieves and outright criminals cashing in on the misfortune of others. Digital currencies are far safer…so far… and are the only outlet since these same criminals have been rigging the precious metals prices, currencies exchange rates and the markets in general to their own benefit and to the detriment of everyone else.

* * *

(ZeroHedge) When global financial markets crash, it won’t be just “Trump’s fault” (and perhaps the quants and HFTs who switch from BTFD to STFR ) to keep the heat away from the Fed and central banks for blowing the biggest asset bubble in history: according to the head of the German central bank, Jens Weidmann, another “pre-crash” culprit emerged after he warned that digital currencies such as bitcoin would worsen the next financial crisis.

As theFT reports, speaking in Frankfurt on Wednesday the Bundesbank’s president acknowledged the creation of an official digital currency by a central bank would assure the public that their money was safe. However, he warned that this could come at the expense of private banks’ ability to survive bank runs and financial panics.

As Citigroup’sHans Lorenzen showed yesterday, as a result of the global liquidity glut, which has pushed conventional assets to all time highs, a tangent has been a scramble for “alternatives” and resulted in the creation and dramatic rise of countless digital currencies such as Bitcoin and Ethereum. Citi effectively blamed the central banks for the cryptocoinphenomenon.

Weidmann had a different take, and instead he focused on the consequences of this shift towards digitalisation which the Bundesbank president predicted, would be the main challenge faced by central banks. In an ironic twist, in order to challenge the “unofficial” digital currencies that have propagated in recent years, central banks have also been called on to create distinct official digital currencies, and allow citizens to bypass private sector lenders. As Weidmann explained, this will only make the next crisis worse:

Allowing the public to hold claims on the central bank might make their liquid assets safer, because a central bank cannot become insolvent. This is an feature which will become relevant especially in times of crisis – when there will be a strong incentive for money holders to switch bank deposits into the official digital currency simply at the push of a button. But what might be a boon for savers in search of safety might be a bane for banks, as this makes a bank run potentially even easier.

Essentially, Weidmann warned that digital currencies – whose flow can not be blocked by conventional means – make an instant bank run far more likely, and in creating the conditions for a run on bank deposits lenders would be short of liquidity and struggle to make loans.

“My personal take on this is that central banks should strive to make existing payment systems more efficient and still faster than they already are – instant payment is the buzzword here,” the Bundesbank president said. “I am pretty confident that this will reduce most citizens’ interest in digital currencies.”

Which, considering the all time highs in both Bitcoin and Ethereum, would suggest that citizens faith and confidence in the existing “payment systems”, and thus central banks, are at all time lows.

The wild card in cryptocurrencies is the role of Big Institutional Money.

Charles Huge Smith has taken the liberty of preparing a projection of bitcoin’s price action going forward:

You see the primary dynamic is continued skepticism from the mainstream, which owns essentially no cryptocurrency and conventionally views bitcoin and its peers as fads, scams and bubbles that will soon pop as price crashes back to near-zero.

Skepticism is always a wise default position to start one’s inquiry, but if no knowledge is being acquired, skepticism quickly morphs into stubborn ignorance.

Bitcoin et al. are not the equivalent of Beanie Babies. Cryptocurrencies have utility value. They facilitate international payments for goods and services.

The primary cryptocurrencies are not a scam. Advertising a flawless Beanie Baby and shipping a defective Beanie Baby is a scam. Advertising a mortgage-backed security as low-risk and delivering a guaranteed-to-default stew of toxic mortgages is a scam.

The primary cryptocurrencies (bitcoin, Ethereum and Dash) have transparent rules for emitting currency. The core characteristic of a scam is the asymmetry between what the seller knows (the product is garbage) and what the buyer knows (garsh, this mortgage-backed security is low-risk–look at the rating).

Both buyers and sellers of primary cryptocurrencies are in a WYSIWYG market: what you see is what you get. While a Beanie Baby scam might use cryptocurrencies as a means of exchange, this doesn’t make primary cryptocurrencies a scam, any more than using dollars to transact a scam makes the dollar itself a scam.

Bubbles occur when everyone and their sister is trading/buying into a “hot” market. Bubbles pop when the pool of greater fools willing and able to pay nose-bleed valuations runs dry. In other words, when everyone with the desire and means to buy in and has already bought in, there’s nobody left to buy in at a higher price (except for central banks, of course).

At that point, normal selling quickly pushes prices off the cliff as there is no longer a bid from buyers, only frantic sellers trying to cash in their winnings at the gambling hall.

While a few of my global correspondents own/use the primary cryptocurrencies, and a few speculate in the pool of hundreds of lesser cryptocurrencies, I know of only one friend/ relative /colleague / neighbor who owns cryptocurrency.

When only one of your circle of acquaintances, colleagues, friends, neighbors and extended family own an asset, there is no way that asset can be in a bubble, as the pool of potential buyers is thousands of times larger than the pool of present owners.

The Network Effect is expressed mathematically inMetcalfe’s Law:the value of a communications network is proportional to the square of the number of connected devices/users of the system.

The Network Effect cannot be fully captured by Metcalfe’s Law, as the value of the network rises with the number of users in communication with others and with the synergies created by networks of users within the larger network, for example, ecosystems of suppliers and customers.

In other words, the Network Effect is not simply the value created by connected users; more importantly, it is the value created by the information and knowledge shared by users in sub-networks and in the entire network.

This is The Smith Corollary to Metcalfe’s Law: the value of the network is created not just by the number of connected devices/users but by the value of the information and knowledge shared by users in sub-networks and in the entire network.

In the context of the primary cryptocurrencies, the network effect (and The Smith Corollary to Metcalfe’s Law) is one core driver of valuation: the more individuals and organizations that start using cryptocurrencies, the higher the utility value and financial value of those networks (cryptocurrencies).

In other words, cryptocurrencies are not just stores of value and means of exchange–they are networks.

The true potential value of cryptocurrencies will not become visible until the global economy experiences a catastrophic collapse of debt and/or a major fiat currency. These events are already baked into the future, in my view; nothing can possibly alter the eventual collapse of the current debt/credit bubble and the fiat currencies that are being issued to inflate those bubbles.

The skeptics will continue declaring bitcoin a bubble that’s bound to pop at $3,000, $5,000, $10,000 and beyond. When the skeptics fall silent, the potential for a bubble will be in place.

When all the former skeptics start buying in at any price, just to preserve what’s left of their fast-melting purchasing power in other currencies, then we might see the beginning stages of a real bubble.

The wild card in cryptocurrencies is the role of Big Institutional Money. When hedge funds, insurance companies, corporations, investment banks, sovereign wealth funds etc. start adding bitcoin et al. as core institutional holdings, the price may well surprise all but the most giddy prognosticators.

The Network Effect can become geometric/exponential very quickly. It’s something to ponder while researching the subject with a healthy skepticism.

Back on February 27, when bitcoin was trading in the mid-teens, we wrote “Step aside bitcoin, there is a new blockchain kid in town.”

In recent days, the world’s second most popular digital currency, Ethereum, has been surging (despite its embarrassing hack last June when some $59 million worth of “ethers” were stolen forcing the blockchain to implement a hard fork to undo the damage), prompting many to wonder if some big announcement was imminent. It appears that yet again someone “leaked” because on Monday, an alliance of some of the world’s most advanced financial and tech companies including JPMorgan Chase, Microsoft, Intel and more than two dozen other companies teamed up to develop standards and technology to make it easier for enterprises to use blockchain code Ethereum – not bitcoin – in the latest push by large firms to move toward the holy grail of a post-central bank world in which every transaction is duly tracked: a distributed ledger systems.

Commenting on the sharp – for the time – rise in ETH price (which hadmoved from $13 to $15), we said “the move may be just the beginning if most corporations adopt Ethereum as the distributed ledger standard: Accenture released a report last month arguing that blockchain technology could save the 10 largest banks $8 billion to $12 billion a year in infrastructure costs — or 30 percent of their total costs in that area.” Since then most corporations have indeed adopted Ethereum as the distributed ledger standard.

* * *

Three months later, and with Ethereum 15x higher at $230,Bloomberg today writes: “Step aside, bitcoin. There’s another digital token in town that’s winning over the hearts and wallets of cryptocurrency enthusiasts across the globe.”

It’s not just the lede that is familiar, it’s everything else too, especially the forecast.

The value of ether – the digital currency linked to the ethereum blockchain – could surpass that of bitcoin by the end of 2018, according to Olaf Carlson-Wee, chief executive officer of cryptocurrency hedge fund Polychain Capital who was interviewed by Bloomberg.

“What we’ve seen in ethereum is a much richer, organic developer ecosystem develop very, very quickly, which is what has driven ethereum’s price growth, which has actually been much more aggressive than bitcoin,” said Carlson-Wee, in an interview on Bloomberg Television Tuesday.

As wepreviously reported, while Ethereum suffered an embarrassing hack last summer resulting in the theft in millions of ether, the cryptocurrency has drawn the interest of industries from finance to health care because its blockchain does far more than let bitcoin users send value from one person to another. “Its advocates think it could be a universally accessible machine for running businesses, as the technology allows people to do more complex actions in a shared and decentralized manner.“

Which is why ethereum is gaining increasingly more converts. Carlson-Wee wasn’t the first to forecast a bright future for ethereum. Fred Wilson, co-founder and managing partner at Union Square Ventures, laid out an even more ambitious timeline for the cryptocurrency in an interview earlier this month.

“The market cap of ethereum will bypass the market cap of bitcoin by the end of the year,” said Wilson, who is also chairman of the board at Etsy.

In fact, if one looks at the relative market share of various cryptocurrencues, and extrapolates current trends, ethereum could surpass bitcoin in just a few months.

Bitcoin currently dominates a little less than half of the digital currency market, down from almost 90 percent three months ago, according to Coinmarketcap.com data. Meanwhile, ethereum has quadrupled its share, which now represents more than a quarter of the pie.

Indicatively, as of this moment, the market cap of Bitcoin is $37 billion, 75% higher than Ethereum. If the optimsitic forecasts are accurate, Ethereum, which is currently offered at $230, will cost roughly $400 next time we look at it, if not more. What is more interesting is that while bitcoin hit an all time high of approximately $2900 one week ago, it has failed to recapture the highs, even as ethereum has continued surging ever higher, perhaps a sign of a broad momentum shift from the legacy “cryptocoin” to the “up and comer.”

“We’re absolutely still in the infrastructure building phase,” Carlson-Wee said. “But I do think within one to two years, we’ll start to see the first viral applications that are user facing.”

In any case, for readers interested in putting money into either extremely volatile crypto, be prepared, in fact assume, a complete loss of your investment as chasing such speculative manias rarely has a happy ending. Then again, trying to time the peak of any bubble is a fool’s endeavor. Just look at the S&P.

Bitcoin’s growth has started to catch up to its fundamentals, which is likely what has been driving its astronomical gain as of late, he said. Others have attributed the surge to speculation, as well as increased interest in Asia and adoption by established companies.

Impressive performance aside, more than $150 has been knocked off bitcoin’s price since late last week amid concerns about transaction speed, safety and a possible price bubble.

You might have been hearing about Bitcoin more frequently in the past few years. Recently it made a lot of news because of the ransomware attacks that affected countries around the world by demanding Bitcoin ransom to release embargoed documents on computers. So what the heck is Bitcoin, and how does it work?

First, let’s get this out of the way: bitcoin is money. It’s money as much as the dollar or euro or yen is money. And it’s fully interconvertible with these or any other currencies. Bitcoin is different than these national currencies in many key ways, however, because Bitcoin is a type of digital money that basically runs itself without any government intervention and minimal regulation.

Bitcoin is both the network for using the currency as well as the currency itself. It’s usually denoted Bitcoin (big B) when talking about the network and bitcoin (small b) when talking about the actual currency. For example, I have about four bitcoin in my online wallet, and I use the Bitcoin network to send payments.

How do you get bitcoin? There are two ways: Either you buy bitcoin, or you mine bitcoin. Buying bitcoin is quite easy. There are many online exchanges that will sell you bitcoin in exchange for whatever currency you normally use (dollars, etc.). I useCoinbaseto buy my bitcoin, and it’s the most mainstream and scrutinized of the current exchanges. It was founded by Wall Street types in order to help Bitcoin become more mainstream. There aremany others you can use, such as KrakenorCoinMama.

You can also buy bitcoin in person at various bitcoin ATMs around the world. There are now about 1,200 such ATMs in 60 countries around the world, and they’re growing rapidly. Here’s asitethat allows you to find the nearest ATM.

Last, you can buy bitcoin through real people by usinglocalbitcoins.comto find people in your area who will sell you bitcoin without going through an online exchange at all.

The second way to get bitcoin is by ”mining” them. You mine bitcoin using fast computers specially built for doing this. These specialized machines crunch numbers to discover the right codes. Every 10 minutes, the Bitcoin network releases a new block of bitcoin and the party or parties who discovered the right codes gets that block of coins (currently 12.5 coins per block). Bitmain is one of the bigger mining machine manufacturers and their newest model, the T9, sells for about one bitcoin.

This number crunching for “mining” is why bitcoin is referred to as a “crypto currency”: it’s all about using very large numbers that take massive computing power to preserve the integrity of the system and avoid hacking. The Bitcoin system basically turns electricity into money.

Security concerns?

So far, Bitcoin has never been hacked. There’s a common misconception that it has. Many companies that buy and sell bitcoin — bitcoin exchanges — have been hacked. Most famously, MtGox, one of the earliest exchanges, was hacked in 2013 and people lost a lot of money. But even then the Bitcoin network wasn’t hacked. Only the exchange was hacked.

That said, security is very important for those buying and selling bitcoin because the code itself is the currency. It’s a string of numbers and letters called a “hash key.” If someone has your hash keys, they have your bitcoin. There’s nothing extra beyond the hash key.

Your bitcoin are kept generally in an online wallet at an exchange like Coinbase or Xapo. Here’s a site that compares the security of the various means for storing bitcoin. Coinbase wins that comparison currently for online wallets and the Ledger Nano wins for hardware wallets.

You can also keep your bitcoin in an online “vault,” which adds extra layers of security for bitcoin that you don’t plan to use for a while. For example, it takes a couple of days to withdraw bitcoin from the Coinbase vault, and various types of authentication are required before the transaction is complete.

For those who want to take matters more into their own hands and avoid having to trust an online wallet or vault, you can keep your bitcoin in a physical hard drive, or you can even just write your codes by hand on paper and keep them in your physical wallet in your pocket.

Personally, I use a variety of online wallets and vaults in order to prevent any single mishap or hack from hitting me too hard. I can’t be bothered with keeping the codes offline but maybe I will one day as an extra layer of security.

How much is Bitcoin worth?

The price of one bitcoin has grown from nothing in 2009 when the Bitcoin network was created to more than $1,800 in May. If you had invested $1,000 in bitcoin in 2010, you would be sitting on more than $12 million now. How has it gone up so much? Well, because increasing numbers of investors have decided to place their confidence in the system.

We can look at the stats to get a good feel for how fast Bitcoin has grown.Blockchain.infokeeps detailed stats.

» The number of bitcoin in circulation has grown from zero in the beginning of 2009 to almost 16.5 million now, with only about 4.5 million more to mine (but this will take about a century to complete because mining becomes intentionally more and more difficult).

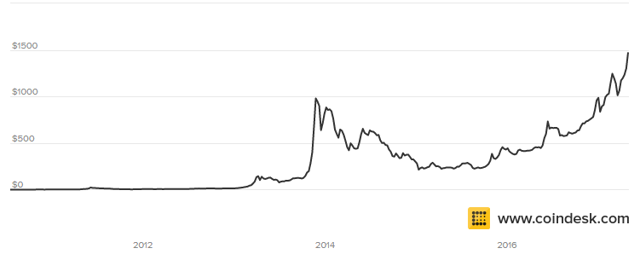

» The Bitcoin price grew from nothing to almost $1,200 at the end of 2013, plummeted to around $200 in 2014, and rose again to more than $1,800 in May.

» Bitcoin’s market capitalization has gyrated similarly, but is now about $30 billion, up from zero in 2009 and $12 billion at the end of 2016, and is enjoying a strong upward trend in 2017.

» All crypto currencies combined now have amarket cap over $60 billion, including Ripple, Ethereum, Litcoin and many others, many of which are also on very strong upward trajectories.

» The number of Bitcoin wallet users (required to buy and conduct business using bitcoin) has grown from zero in 2009 to more than 7 million by mid-2016 and 14 million now.

» Bitcoin daily transactions have grown from nothing in 2009 to 210,000 in mid-2016 and more than 350,000 by May.

So we’re seeing the Bitcoin system roughly doubling in size each year, and there’s little reason to believe that this rate of growth will slow down at this point. If anything, it’s likely to increase.

What does “deflationary” currency mean?

Bitcoin is different than regular money in that there’s a limit to how many can be created: just 21 million. Ever. The idea behind this limit is that the value of this currency can’t be inflated away by policymakers. The dollar loses about 2 percent in value each year because of planned inflation, and this provides a strong incentive to invest rather than save — and that’s literally why the Federal Reserve has a target inflation rate of 2 to 3 percent.

Bitcoin is the opposite: It’s designed to always increase in value, so simply buying and holding may be a very good investment strategy. This is why Bitcoin is described as a “deflationary” currency rather than an inflationary currency.

There’s also a limit on how small each Bitcoin can be divided: into 100 million parts. This tiny part of a bitcoin is called a satoshi, in honor of its mysterious and anonymous creatorSatoshi Nakamoto.

What is the blockchain?

The magic ingredient in Bitcoin is the distribution of trust in a vast electronic network. This distribution moots the need for the “centralization of trust” that is the function of central banks like the Federal Reserve. Central banks issue money, control interest rates and act as a lender of last resort in “fiat currency” systems like in the United States. The distribution of trust to the network performs these roles in the Bitcoin ecosystem. This trust network is called the “blockchain,” and it is the heart of Bitcoin.

The blockchain is an electronic record (ledger) of all bitcoin transactions that is stored on every node of the ever-increasing network of the Bitcoin ecosystem. Because it is completely distributed and constantly updated in real time, using very difficult cryptographic keys that require massive amounts of computing power, the blockchain can’t be shut down by any outside force. This fully decentralized system renders Bitcoin as a system practically immune from hackers. As mentioned above, individual bitcoin exchanges can and have been hacked, but Bitcoin itself has never been hacked.

The beauty of the blockchain and Bitcoin ecosystem is that it allows any person or people using it to avoid the centralized (and often abusive) power of central banks and of national governments entirely. ABN Amro bank chiefsaidit well in 2015: “What the Internet has done for information and the way we communicate, the blockchain will do for value and the way we look at trust. The financial world is going to flip upside-down.”

We are witnessing that upside-down flip right now in real time. This is why we’ve seen literally $30 billion in new money come into the Bitcoin and other crypto currency space in the past six months alone.

Obviously, the decentralized nature and independence from government influence has appealed to libertarians and techno-optimists since Bitcoin’s creation. Bitcoin long has had a bad rep because it’s been used by various versions of the Silk Road website to buy and sell drugs and other illegal items. But there’s far more to Bitcoin than illegal drugs.

Bitcoin is now accepted by thousands of companies and vendors around the world. Japan recently recognized Bitcoin as a legitimate currency, and this means that more than 260,000 stores in Japansoon will startaccepting Bitcoin.

We are very likely seeing the beginning of a very large wave of growth for Bitcoin and other crypto currencies like Ethereum.

Investing in Bitcoin

How should you invest in Bitcoin? I’ve always advised people that you shouldn’t invest anything in Bitcoin that you don’t mind losing. That’s generally still good advice because this currency and the technology behind it are still very new. They could just disappear for a variety of reasons.

But the highly positive trends in terms of wallet growth, acceptance by businesses and governments, as well as market cap and price, discussed above have led me recently to change my mind a little and suggest that Bitcoin should in fact be a part of any smart investor’s portfolio.

It shouldn’t be a large part, but it should definitely be a part of it. With returns like we’ve seen on Bitcoin in the past eight years, it’s reasonable to accept some risk.

Will Bitcoin change the world?

The last thing I’ll look at is the revolutionary potential for Bitcoin and other cryptocurrencies in terms of how they may change the world. Iwrote a piecein 2015 looking at how Bitcoin may stop China from replacing the United States on the world stage. This would be a good thing and could happen if enough Chinese simply start to prefer using bitcoin instead of yuan to conduct business. If China can’t control its currency it can’t control the world.

I also looked in a piece last year at whether Bitcoin is likely to be thefuture of moneymore generally. I concluded then and still believe that Bitcoin (or maybe some other coin built on the blockchain) will probably either grow in the next couple of decades to become a global currency or shrink down such that it becomes just an interesting historical footnote.

What happens if Bitcoin or something like it does replace national fiat currencies around the world? First, it makes it much harder for nations to raise massive amounts of money through printing or borrowing. This means that deficit spending will shrink or even go away. And, according to at least some Bitcoin libertarian optimists, this would also stop nations from waging war as much because they’d have to finance such wars as they go, with real money, rather than using deficit spending. A more peaceful world would indeed be a nice consequence of the Bitcoin revolution.

In closing, Bitcoin is a potentially transformative new type of currency that promises to create a more borderless and peaceful world, and an increasing flow of information and goods. It also may well lead to many unpredictable effects that we’ll simply have to sit back and watch as they unfold.

For months we have been getting messages and e-mails about Bitcoin.

We have long been advocate for buying the BTC dips and riding it out for the longer term.

We explain why we think everyone’s BTC strategy should simply be: “Buy one Bitcoin and forget about it”.

By Parke Shall

That is our simple bitcoin advice. “Buy one and forget about it for a while.” Your loss today is going to be capped at about $1400 but, as was said in Back to the Future, “if this thing hits 88 miles per hour, you’re going to see some serious s***.”

We wanted to take the time to write a small note today about our continued thinking on bitcoin and why we think a small investment in perhaps just one bitcoin could be a prudent strategy for asset diversification for any investor.

Hopefully, our track record on the digital currency also helps our credibility today. In the past, we have advocated for buying any and all dips in the digital currency making the argument time and time again that we believed bitcoin would continue to appreciate regardless of small aberrations that have occurred along the way. For instance in December of last year, we predicted bitcoin would soar through $1200 this year.

The conclusion has generally been the same in each of our bitcoin articles: we expect demand for bitcoin to continue to rise and, with a limited supply, and we expected this demand will push the price significantly higher. This is the dynamic we have seen during the course of bitcoin’s life cycle thus far,

Many people have been deterred from investing or purchasing bitcoin at these levels because of how much the prices has appreciated so far. This is akin to not wanting to buy a stock while it is on its way up, despite its best years possibly being ahead of it. If you didn’t buy at $700 like we advocated, then yes, you missed out on a double. But who is to say that if you don’t buy here at around $1400 you won’t miss another double? In fact, we think the reality is that an investment in bitcoin today could pay off many multiples in the future as long as, as an investor, you have patience.

We also don’t think owning gold is a bad idea either. We are not sure why this argument of gold versus bitcoin started, but we own both. We like to think of them as our “old-school” and our “new school” hedges. Gold is an “old-school” hedge because it is actually a physical asset that you can reach out and touch that has been intertwined with economics for thousands of years. It has a great track record of demand and comes in finite amounts, therefore making it a great hedge against anything and everything that is “new school” in the market, from Keynesian theory to bitcoin.

Bitcoin obviously has the biggest track for potential appreciation, we believe. While gold may not go up 10 times in the event of a catastrophe or a risk off event, it still may appreciate significantly. We believe bitcoin, on the other hand, actually has the potential to appreciate over 100 times in the future, if it holds up. By that, we mean that there is definitely a theoretical case for the asset to appreciate this much, although there is probably a cautious likelihood of it happening. In other words, and not to sound hyperbolic, Bitcoin going to $1 million may not prove to be a total impossibility.

This appreciation may occur without a catastrophe or without a risk off event. In other words, we like bitcoin not only as an investment in the financial technology and not only as an investment in a digital currency but also as an investment in a hedge against central banks and the markets.

To explain:

1. We know that blockchain is at the core of what makes Bitcoin tick. Companies and governments have continued to invest in blockchain, and we believe that owning Bitcoin is another way to invest in one of the earliest and possibly the most well known blockchain project out there. Therefore, an investment in Bitcoin is an investment in Blockchain.

2. Not unlike gold, people use Bitcoin because they want less government and less regulation in their lives. Buying Bitcoin is a way to, at least for now, shore up a method of transacting value outside of the “system”. Gold offers the same benefits and is tangible, which is why we like owning both gold and Bitcoin as hedges against the “system”.

We have gotten numerous questions over the last year or so about what our strategy would be if we were new to investing in bitcoin. Put simply, the strategy would be to “buy one bit coin and just leave it”. One of a couple scenarios are going to happen.

The first situation is the worst. Let’s assume bitcoin winds up going to zero eventually and is somehow either rejected as a digital currency or disproven as a financial technology. In that case, you take a 100% loss. Sorry. At least your risk was defined.

The second situation is one where bitcoin is adopted in somewhat of the same fashion as it has been adopted of recent. Its use starts to drift from outside the mainstream to inside the mainstream and the price continues to appreciate. This is a case where you’d likely see appreciation in a bitcoin that you purchased today.

Finally, the third situation. We call this the grand slam. Bitcoin is unanimously excepted as the first and only prominent digital currency. It becomes a full-scale hedge, adopted by a significant portion of the population, against central banking systems and finance as we know it today. Given the fact that only about 20 million bitcoin will be issued in total, there will be a severe dry up in supply as billions of people worldwide look to get their share of the digital currency. This is a situation where the currency could appreciate 100 times what its worth now or more. Obviously, this is the most speculative of the three situations but could be a reality if an investor has enough patience to wait it out. This type of situation could take 15 to 30 years and this is why the title of this article is “buy one bitcoin and forget about it“.

Again, bitcoin does not come without risk.

Relative to other assets you may hold, like stocks, options and other currencies, Bitcoin is going to be extraordinarily volatile. Due to the fact that it is easily in the digital currency’s life cycle and that it has yet to be proven on a wide scale, investors can expect significant volatility, sometimes 20%+ in one day’s time, for the capital they have invested in Bitcoin.

Also, it is an all digital currency meaning that it needs digital infrastructure to survive. In a catastrophic scenario where our infrastructure is compromised, we have no idea what would happen to bitcoin. It isn’t tangible and you can’t physically hold it, which are two of its major detracting points versus gold. However, we see buying bitcoin at $1400 as a speculative investment that could yield immense results in the future if you have the wherewithal and you have the strength to hold it over time.

{kind=link}