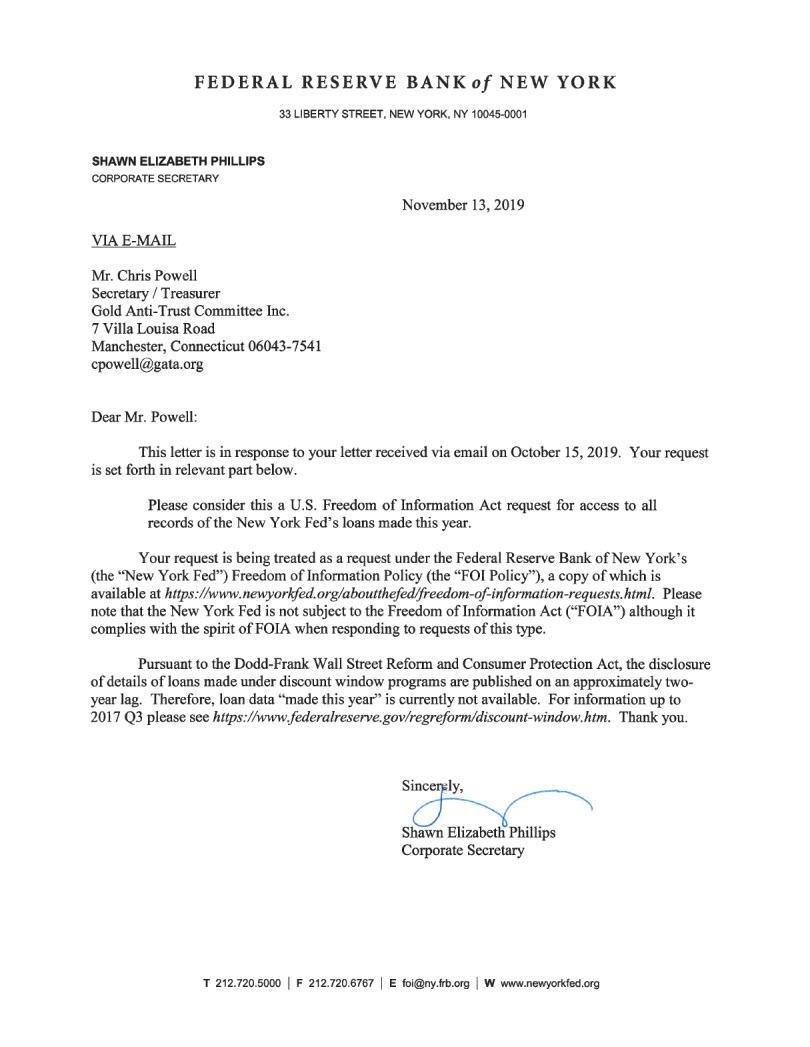

If you want to know which investment houses have been getting the infamous “repo” loans from the Federal Reserve Bank of New York in recent weeks, as GATA has wanted to know, you’ll have to wait two years, according to a letter received from the bank today in response GATA’s request for the information.

The delay, the New York Fed’s letter says, is authorized by the Dodd-Frank Wall Street Reform and Consumer Protection Act.

Perhaps more interestingly, the New York Fed’s letter, signed by Corporate Secretary Shawn Elizabeth Phillips, contends that the bank is exempt from the federal Freedom of Information Act but tries to comply with its spirit.

Such a claim of exemption was not made by the Federal Reserve’s Board of Governorsduring GATA’s FOIA lawsuitagainst it in 2011, in which GATA sought access to the board’s gold-related documents. GATA technically won the case when U.S. District Judge Ellen Segal Huvelleruled that one such document was illegally withheld and ordered the board to disclose it to GATA and pay the organization court costs of $2,670:

What kind of system of government is it when every week an entity created by ordinary legislation can create enormous amounts of a nation’s currency and disburse it to unidentified parties without any oversight by the people’s elected representatives, news organizations, and ordinary citizens? It sure doesn’t sound like “the land of the free and the home of the brave.”

The New York Fed’s response to GATA can be read below (pdf link):

‘The volume of billions being lent into existence from nothing by the Fed to bail banks out will go parabolic. It must, otherwise credit will freeze, asset prices will fall, forced bank depositor bail-ins will ensue’

With stocks threatening to close in the red, late on Wednesday the Fed sparked a furious last hour rally…

The Desk has released an update to the schedule of repurchase agreement (repo) operations for the current monthly period. Consistent with the most recent FOMC directive, to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation…

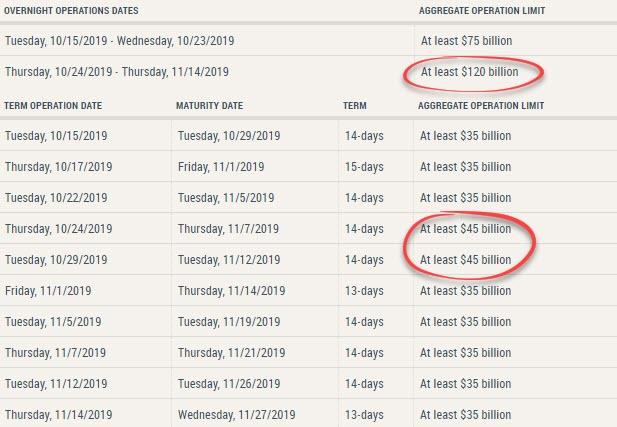

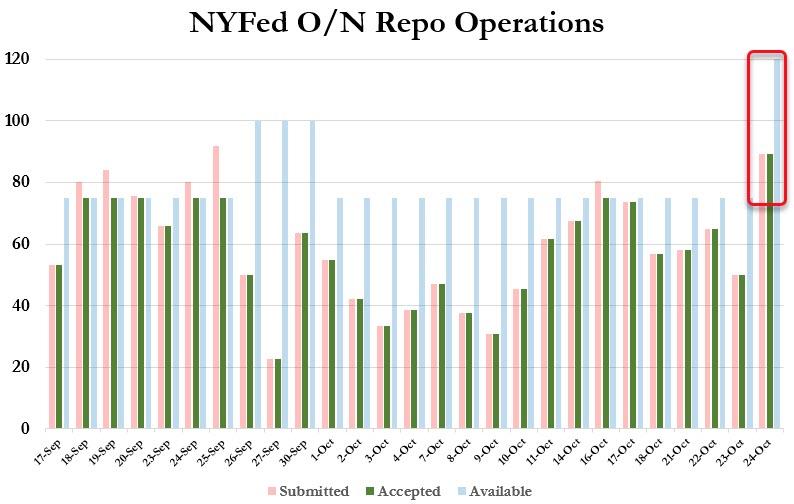

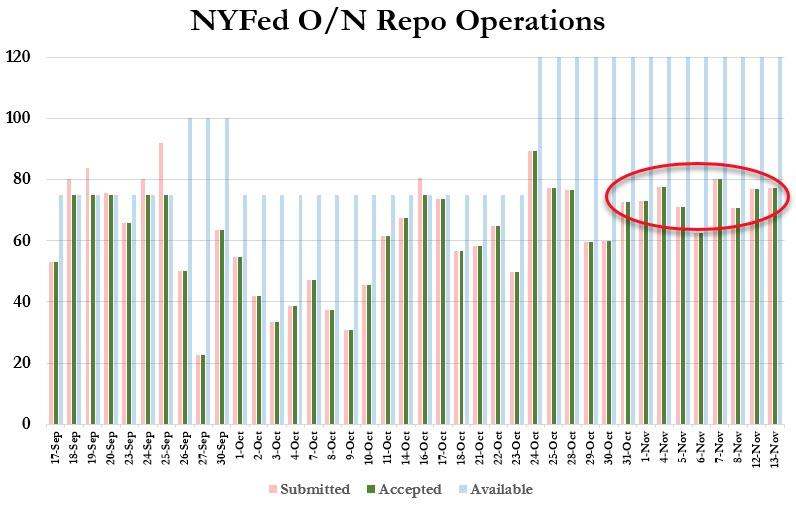

As we noted yesterday, that was a massive 60% increase in the overnight repo liquidity availability (from $75 billion to $120 billion) and a 28% jump in the term repo provision (from $35 billion to $45 billion).

“It’s just more evidence the Fed will not back off as year-end gets closer,” said Wells Fargo’s rates strategist, Mike Schumacher. “The Fed wants to take out more insurance. You had repo pick up last week. That might not have gone over too well.”

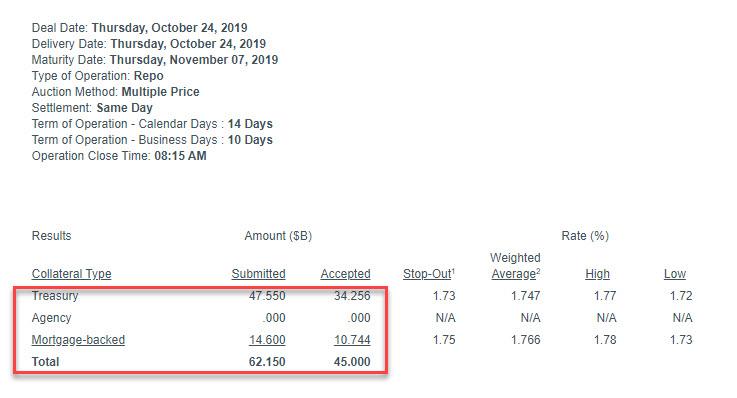

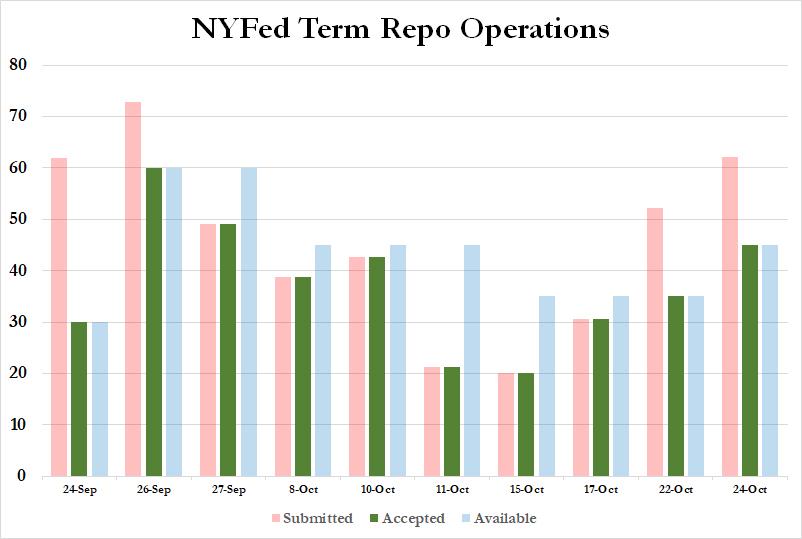

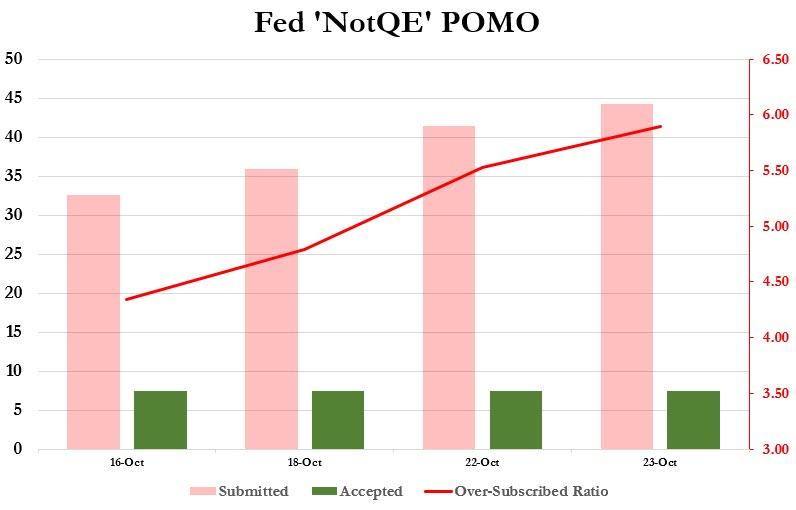

And now we know that there was good reason for that, because according to the latest, just concluded Term Repo operation, a whopping $62.15BN in securities were submitted to the Fed’s 14-day operation, ($47.55BN in TSYs, $14.6BN in MBS), resulting in a 1.38x oversubscribed term operation, the second consecutive oversubscription following Tuesday’s Term Repo, when $52.2BN in securities were submitted into the Fed’s then-$35BN operation.

This was the highest uptake of the Fed’s term repo operation since Sept 26.

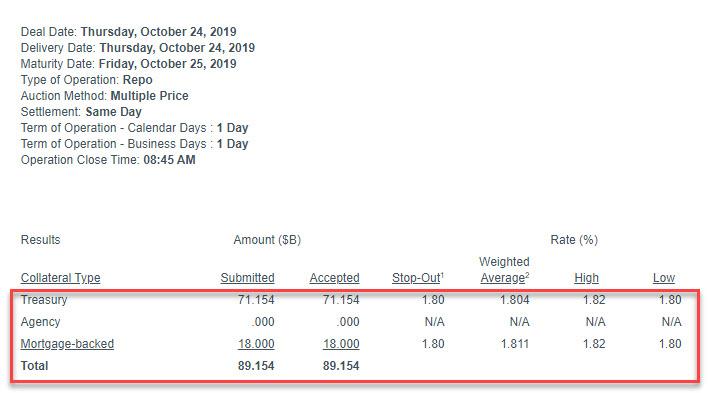

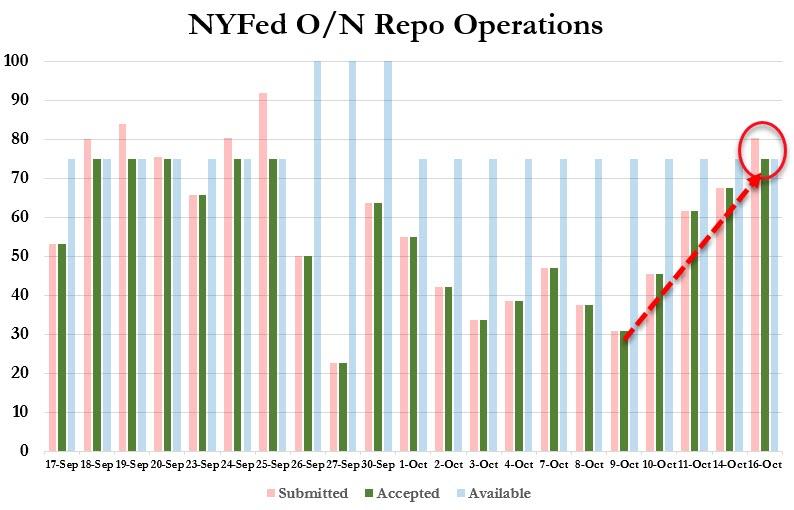

But wait there’s more, because while the upsized term-repo saw the biggest (oversubscribed) uptake in one month, demand for the Fed’s overnight repo also soared, with dealers submitting 89.2BN in securities for the newly upsized, $120BN operation.

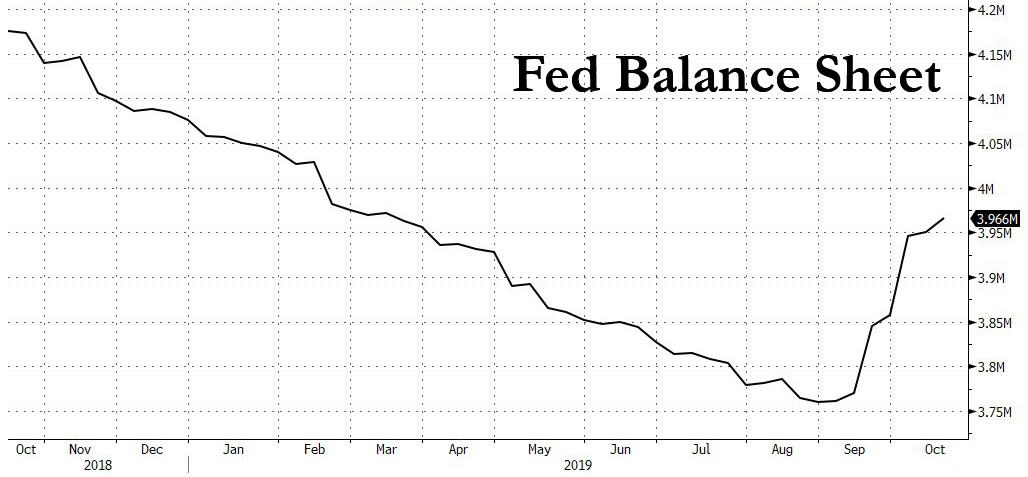

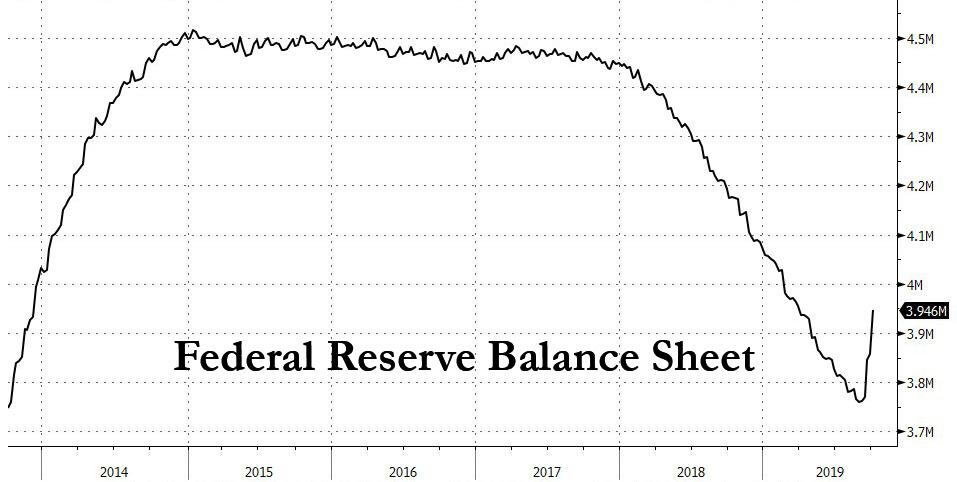

In total, between the $45BN term repo and the $89.2BN overnight repo, the Fed just injected a whopping $134.2BN in liquidity just to make sure the US banking system is stable. That, as the Fed’s balance sheet soared by $200BN in the past month rising to just shy of $4 trillion.

Meanwhile, funding tensions weren’t evident only in repo, but also in the Fed’s T-Bill POMO, where as we noted yesterday, demand for liquidity has also been increasing with every subsequent operation, peaking with yesterday’s operation.

Needless to say, if the funding shortage was getting better, none of this would be happening; instead it appears that with every passing day the liquidity shortage is getting worse, even as the Fed’s balance sheet is surging.

The only possible explanation, is someone really needed to lock in cash for month end (the maturity of the op is on Nov 7) which is when a “No Deal” Brexit may go live, and as a result one or more banks are bracing for the worst. The question, as before, remains why: just what is the source of this unprecedented spike in liquidity needs in a system which already has $1.5 trillion in excess reserves? And while we await the answer, expect stocks to close pleasantly in the green as dealers transform their newly granted liquidity into bets on risk assets.

‘The powers that shouldn’t be would rather us experience a mad max world while they hide in luxury bunkers, than allow us a treasury issued gold backed currency, absent a central bank once again’

‘The Fed is an outpost of a foreign power that controls our economy, most of our politics and our financial future. It’s an instrument of the Rothschild global cabal. It always has been since 1913’

First it was supposed to be just a mid-month tax payment issue coupled with an accelerated cash rebuild by the US Treasury. Then, it was supposed to be just quarter-end pressure. Then, once the Fed rolled out QE4 while keeping both its overnight and term repo operations, the mid-September repo rate fireworks which sent the overnight G/C repo rate as high as 10% was supposed to go away for good as Powell admitted the level of reserves was too low and the Fed launched a $60BN/month Bill POMO to boost the Fed’s balance sheet.

Bottom line: the ongoing repo market pressure – which indicated that one or more banks were severely liquidity constrained – was supposed to be a non-event.

Alas, as of this morning when the Fed’s latest repo operation was once again oversubscribed, it appears that the repo turmoil is not only not going away, but is in fact (to paraphrase Joe Biden) getting worse, because even with both term and overnight repos in play and with the market now expecting the Fed to start injecting copious liquidity tomorrow with the first Bill POMO, banks are still cash starved.

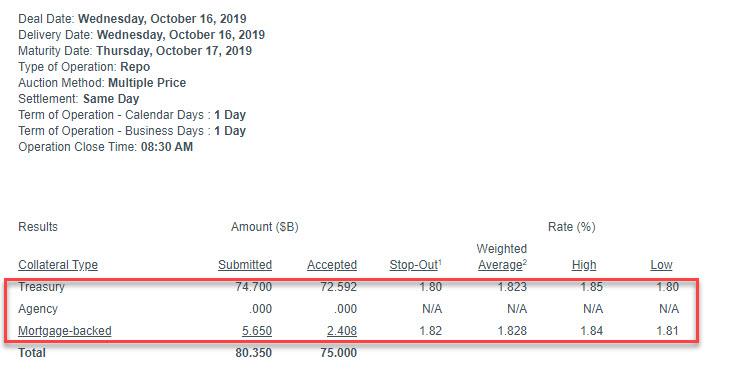

To wit: in its latest overnight operation, the Fed indicated that $80.35BN in collateral ($74.7BN in TSYs, $5.65BN in MBS) had been submitted into an operation that maxed out at $75BN, with a weighted average rate on both TSY and MBS rising to 1.823% and 1.828% respectively.

While it was clear that the repo market was tightening in the past week, with each incremental overnight repo operation rising, today was the first oversubscribed repo operation since September 25, and follows yesterday’s $67.6BN repo and $20.1BN term repo.

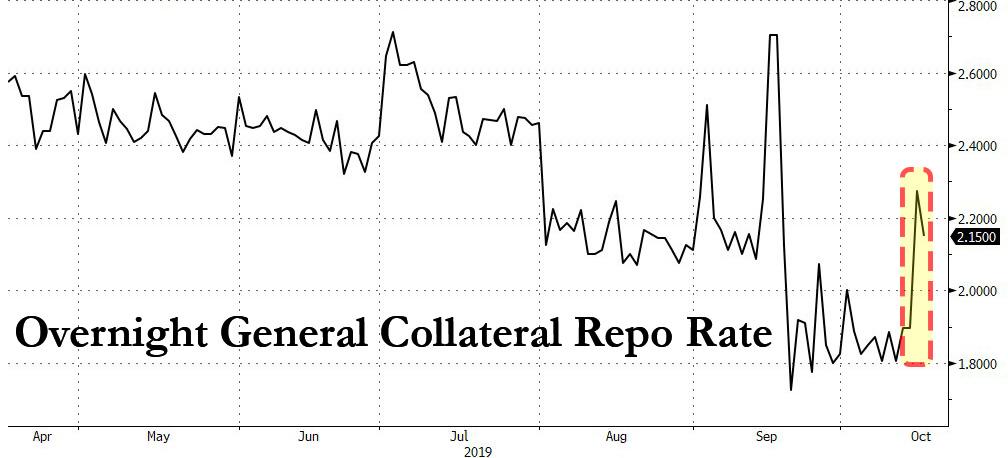

But the clearest sign that the repo market is freezing up again came from the overnight general collateral rate itself, which after posting in the 1.80%-1.90% range for much of the past two weeks, spiked as high as 2.275% overnight and was last seen at 2.15%, well above the fed funds upper range…

‘The powers that be would rather us experience a mad max world while they hide in luxury bunkers, than allow a treasury issued gold backed currency, absent a central bank once again’

(Daniel Lacalle) The Federal Reserve has injected $278 billion into the securities repurchase market for the first time. Numerous justifications have been provided to explain why this has happened and, more importantly, why it lasted for various days. The first explanation was quite simplistic: an unexpected tax payment. This made no sense. If there is ample liquidity and investors are happy to take financing positions at negative rates all over the world, the abrupt rise in repo rates would simply vanish in a few hours.

Let us start with definitions. The repo market is where borrowers seeking cash offer lenders collateral in the form of safe securities. Repo rates are the interest rate paid to borrow cash in exchange for Treasuries for 24 hours.

Sudden bursts in the repo lending market are not unusual. What is unusual is that it takes days to normalize and even more unusual to see that the Federal Reserve needs to inject hundreds of billions in a few days to offset the unstoppable rise in short-term rates.

Because liquidity is ample, thirst for yield is enormous and financial players are financially more solvent than years ago, right? Wrong.

What the Repo Market Crisis shows us is that liquidity is substantially lower than what the Federal Reserve believes, that fear of contagion and rising risk are evident in the weakest link of the financial repression machine (the overnight market) and, more importantly, that liquidity providers probably have significantly more leverage than many expected.

In summary, the ongoing -and likely to return- burst in the repo market is telling us that risk and debt accumulation are much higher than estimated. Central banks believed they could create a Tsunami of liquidity and manage the waves. However, like those children’s toys where you press one block and another one rises, the repo market is showing us a symptom of debt saturation and massive risk accumulation.

When did hedge funds and other liquidity providers stop accepting Treasuries for short-term operations? It is easy money! You get a safe asset, provide cash to borrowers, and take a few points above and beyond the market rate. Easy money. Are we not living in a world of thirst for yield and massive liquidity willing to lend at almost any rate?

Well, it would be easy money… Unless all the chain in the exchange process is manipulated and rates too low for those operators to accept even more risk.

In essence, what the repo issue is telling us is that the Fed cannot make magic. The central planners believed the Fed could create just the right inflation, manage the curve while remaining behind it, provide enough liquidity but not too much while nudging investors to longer-term securities. Basically, the repo crisis -because it is a crisis- is telling us that liquidity providers are aware that the price of money, the assets used as collateral and the borrowers’ ability to repay are all artificially manipulated. That the safe asset is not as safe into a recession or global slowdown, that the price of money set by the Fed is incoherent with the reality of the risk and inflation in the economy, and that the liquidity providers cannot accept any more expensive “safe” assets even at higher rates because the rates are not close to enough, the asset is not even close to be safe and the debt and risk accumulated in other positions in their portfolio is too high and rising.

The repo market turmoil could have been justified if it had lasted one day. However, it has taken a disguised quantitative easing purchase program to mildly contain it.

This is a symptom of a larger problem that is starting to manifest in apparently unconnected events, like the failed auctions of negative-yielding eurozone bonds or the bankruptcy of companies that barely needed the equivalent of one day of repo market injection to finance the working capital of another year.

This is a symptom of debt saturation and massive risk accumulation. The evidence of the possibility of a major global slowdown, even a synchronized recession, is showing that what financial institutions and investors have hoarded in recent years, high-risk, low-return assets, is more dangerous than many of us believed.

It is very likely that the Fed injections become a norm, not an anomaly, and the Fed’s balance sheet is already rising. Like we have mentioned in China so many times, these injections are a symptom of a much more dangerous problem in the economy. The destruction of the credit mechanism through constant manipulation of rates and liquidity has created a much larger bubble than any of us can imagine. Like we have seen in China, it is part of the zombification of the economy and the proof that unconventional monetary measures have created much larger imbalances than the central planners expected.

The repo crisis tells us one thing. The collateral damages of excess liquidity include the destruction of the credit transmission mechanism, disguising the real assessment of risk and, more importantly, leads to a synchronized excess in debt that will not be solved by lower rates and more liquidity injections.

Many want to tell us that this episode is temporary. It has happened in the most advanced, diversified and competitive financial market. Now imagine if it happens in the Eurozone, for example. This is, like the inverted yield curve and the massive rise in negative-yielding bonds, the tip of a truly scary iceberg.

The Fed’s “temporary” liquidity injections are starting to look rather permanent…

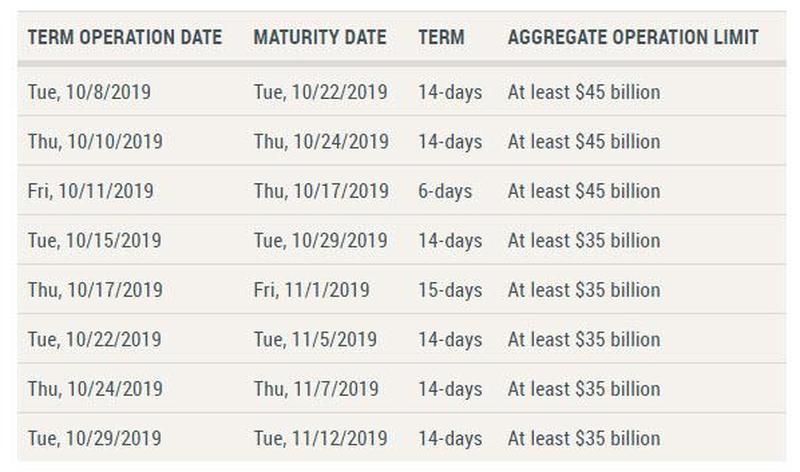

Anyone who expected that the easing of the quarter-end funding squeeze in the repo market would mean the Fed would gradually fade its interventions in the repo market, was disappointed on Friday afternoon when the NY Fed announced it would extend the duration of overnight repo operations (with a total size of $75BN) for at least another month, while also offering no less than eight 2-week term repo operations until November 4, 2019, which confirms that the funding unlocked via term repo is no longer merely a part of the quarter-end arsenal but an integral part of the Fed’s overall “temporary” open market operations… which are starting to look quite permanent.

In accordance with the most recent Federal Open Market Committee (FOMC) directive, the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York will conduct a series of overnight and term repurchase agreement (repo) operations to help maintain the federal funds rate within the target range.

Effective the week of October 7, the Desk will offer term repos through the end of October as indicated in the schedule below. The Desk will continue to offer daily overnight repos for an aggregate amount of at least $75 billion each through Monday, November 4, 2019.

Securities eligible as collateral include Treasury, agency debt, and agency mortgage-backed securities. Awarded amounts may be less than the amount offered, depending on the total quantity of eligible propositions submitted. Additional details about the operations will be released each afternoon for the following day’s operation(s) on the Repurchase Agreement Operational Details web page. The operation schedule and parameters are subject to change if market conditions warrant or should the FOMC alter its guidance to the Desk.

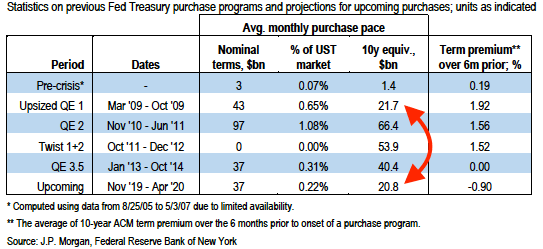

What this means is that until such time as the Fed launches Permanent Open Market Operations – either at the November or December FOMC meeting, which according to JPMorgan will be roughly $37BN per month, or approximately the same size as QE1…

… the NY Fed will continue to inject liquidity via the now standard TOMOs: overnight and term repos. At that point, watch as the Fed’s balance sheet, which rose by $185BN in the past month, continues rising indefinitely as QE4 is quietly launched to no fanfare.

The New York Fed’s response to GATA can be read below (pdf link):

The New York Fed’s response to GATA can be read below (pdf link):